What is the Playout Automation and Channel-in-a-Box Market Size?

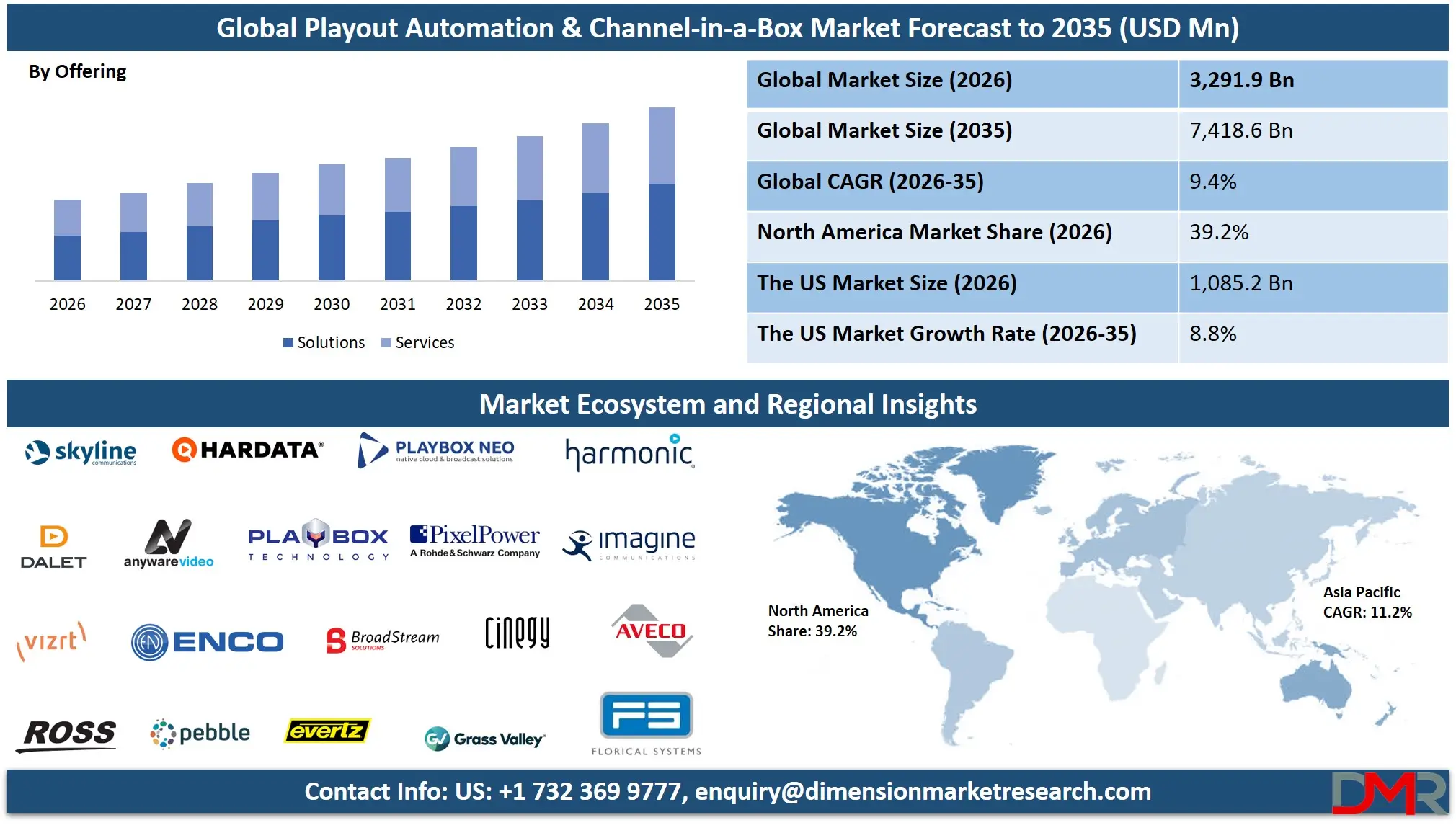

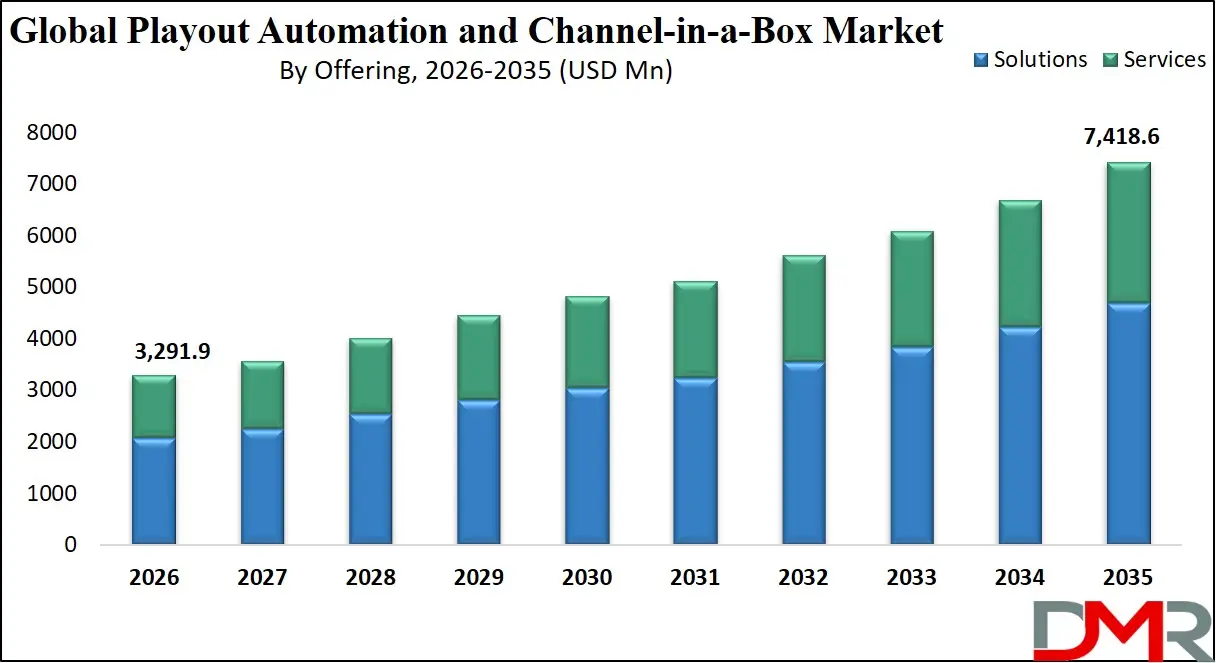

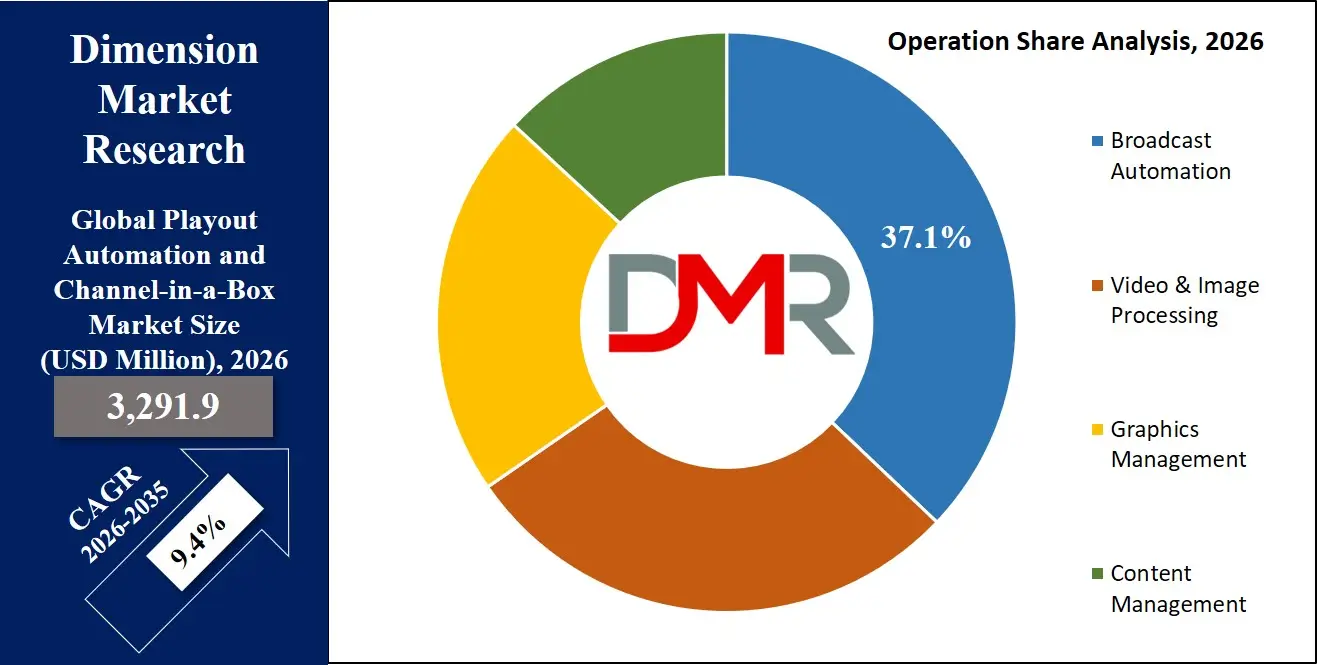

The Global Playout Automation and Channel-in-a-Box Market is expected to reach a value of USD 3,291.9 million in 2026, and it is further anticipated to reach USD 7,418.6 million by 2035, growing at a CAGR of 9.4% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The playout automation and channel-in-a-box market has been growing exponentially, with broadcasters and media organizations rapidly moving their legacy hardware broadcasting infrastructure towards software-defined, IP-based playout automation. Market includes integrated solutions, incorporating playout scheduling and management, master control automation software, media asset and content management, graphics and branding solutions, and related professional services, allowing broadcasters to launch, run, and distribute linear and on-demand channels effectively in both the traditional broadcast, as well as cable, satellite, and OTT environments.

The increasing demand to launch pop-up channels for live events, FAST (Free Ad-Supported Streaming TV) channels for digital audiences, and multi-language regional feeds is driving the necessity for agile, cost-effective playout automation solutions. TV stations are moving to cloud-based deployment models, which provide flexibility in operations, remote productions, and reduced capital investment by a large margin than the conventional on-premises master control rooms. The top adopters are the media and entertainment, telecommunications and corporate sectors, which need scalable, reliable and compliant broadcasting ecosystems that can support high-quality content distribution through a variety of distribution channels.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The US Playout Automation and Channel-in-a-Box Market

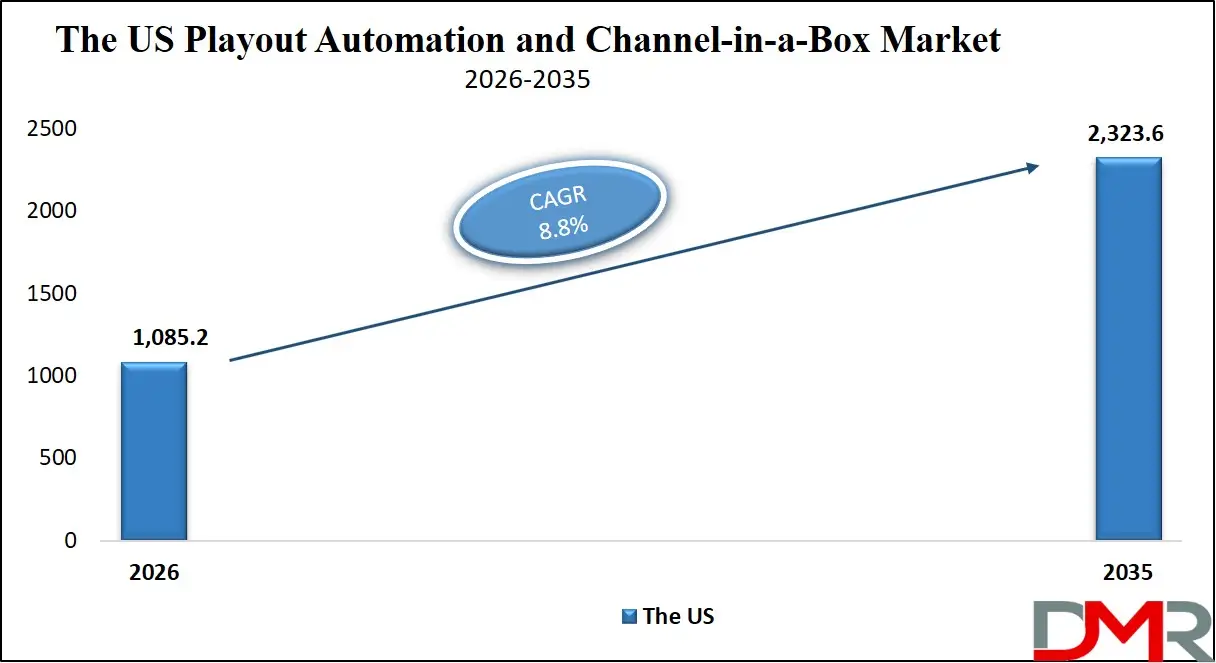

The US Playout Automation and Channel-in-a-Box Market is projected to reach USD 1,085.2 million in 2026 at a compound annual growth rate of 8.8% over its forecast period, culminating in a value of USD 2,323.6 million by 2035.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The US remains the biggest and most industrialized playout automation systems marketplace because of the intense modernization endeavors of large-scale broadcast systems, the skyrocketing of FAST channels, and the provision of a continuous migration of SDI-based infrastructure to SMPTE ST 2110 IP-based workflows. It has been characterized by a high demand of cloud-based master control automation software and remote playout software, where broadcasters operate many channels by using centralized and virtualized environments. The growth of OTT-based channels and ad-supported streaming platforms has driven previously unseen demands on integrated graphics and branding solutions capable of dynamically placing localized content, targeted advertisement, and real-time graphics generation into hundreds of variants of channels. Moreover, the automation of content scheduling and automatic compliance record keeping is creating a need to use consulting and advisory services to navigate the complicated regulatory environment of broadcast operations.

The Europe Playout Automation and Channel-in-a-Box Market

The Europe Playout Automation and Channel-in-a-Box Market is estimated to be valued at USD 987.6 million in 2026 and is further anticipated to reach USD 2,188.5 million by 2035 at a CAGR of 9.2%. The European market is greatly affected by regulatory requirements such as the Audiovisual Media services Directive (AVMSD) and country-specific content quota provisions that result in the necessity of advanced traffic and timetable software that can efficiently handle the intricate compliance requirements at the multijurisdictional level. Increased pace of deployment of cloud-based playout solutions is also being seen in the region as the public broadcasters in Germany, France and the United Kingdom look to upgrade aging broadcasting infrastructure and retain high availability to meet the critical public service broadcasting requirements.

Multi-language channel automation is also occurring on a large scale in the region, especially in Switzerland, Belgium, and the Nordic countries where the broadcasters have to effectively address the content delivery in multiple linguistic areas. Efforts by the European Broadcasting Union on sustainable broadcasting are also pushing the service providers to come up with energy-efficient playout systems that decrease the carbon footprint of the 24/7 broadcasting activity.

The Japan Playout Automation and Channel-in-a-Box Market

The Japan Playout Automation and Channel-in-a-Box Market is projected to be valued at USD 246.9 million in 2026. It is further expected to witness robust growth, holding USD 527.1 million in 2035 at a CAGR of 8.8%. The Japanese market has its distinct features due to the well-developed terrestrial digital broadcasting system in the country and the strategic need to ensure the stability of broadcasting in the seismically active area. Large commercial stations are investing in hybrid playout architectures which combine local master control automation software on the main channels with cloud-based disaster recovery and playout back-up possibilities. The Japanese market has also shown high demand of integrated media asset and content management solution capable of effectively managing the large historical archives of broadcast material in the country most of which is currently being digitized and ready to be distributed through the new OTT-based distribution channels and FAST platforms. Also, the incorporation of sophisticated graphics control to support real-time graphics output is essential to Japanese broadcasters who heavily depend on real-time on-screen information presentation in the broadcasting of news, weather, and emergency warnings.

Key Takeaways

- Market Size & Forecast: The Global Playout Automation and Channel-in-a-Box market is expected to grow to USD 3,291.9 million in 2026, which is further anticipated to reach to USD 7,418.6 million in 2035, driven by the dual drivers of FAST channel proliferation and the imperative to move the broadcast industry to IP-based workflows.

- Growth Rate & Outlook: Global market growth is expected at a CAGR of 9.4%, driven by the urgent need to cut down on operational expenses in linear broadcasting, lack of trained master control operators, and the ever-increasing complexity of distributing multi-platform content within the traditional broadcast and OTT streaming source.

- Primary Growth Drivers: The overall drivers are the prevalence of migration of capital expenditure-intensive hardware playout systems to operational expenditure-based cloud playout models, the requirement of graphics and branding solutions to preserve channel identity amidst the fragmented distribution channels, and the integration of automated ad-insertion software to optimize revenue on addressable advertising opportunities.

- Key Market Trends: The growth of FAST channel automation systems that allow for quick development and monetization of channels, the implementation of AI-based content scheduling and media asset management to maximize programming lineups, and distributed playout software to allow remote production teams to run channels remotely are among the key market trends.

- By Offering Analysis: Solutions are poised to dominate this segment because they directly participate in the playout, monetization, and workflow control. Master control, MAM, and ad insertion lead. Services expand through cloud migration and consulting, yet are minor, and they are usually included with core solution deployments.

- By Deployment Mode Analysis: Cloud-based deployments are projected to dominate because they have scalability and flexibility and is cheaper, which allows channel launches to be introduced quickly. On-premises is applicable in controlled settings where control and security is required. Hybrid models are emerging, yet the cloud is leading the way to the future.

- By Vertical Analysis: The leading vertical in this segment is expected to be media and entertainment, where TV broadcasting and OTT streaming are the primary sources of playout automation investments.

- Regional Leadership: North America is poised to dominate this market with 39.2% of the market share in 2026 because of its developed broadcast technology ecosystem, the agglomeration of large media conglomerates, and the innovation and adoption of FAST channels and deployment leadership in the region.

What is the Automation and Channel-in-a-Box?

Playout Automation and Channel-in-a-Box systems are integrated broadcast technology systems that package the basic operation of a conventional master control room - video server playback, graphics insertion, audio processing, and transmission switching - into single software packages or small hardware boxes. Channel-in-a-Box systems combine these functionalities into single, manageable units, as opposed to traditional broadcast infrastructure which uses dedicated, separate hardware to implement each service, leading to a huge footprint reduction in equipment, power use and operational complexity.

Use Cases

- FAST Channel Launch and Monetization: Media companies deploy dozens of Free Ad-Supported Streaming TV channels, each with ad-insertion software, using cloud-based playout automation platforms to quickly launch their channels and reach narrow audience segments.

- Live Sports Pop-Up Channels: Sports broadcasters use remote playout software and automation of cloud-based master controls to create temporary channels during major tournaments and events.

- Disaster Recovery and Business Continuity: National broadcasters implement hybrid playout systems which provide on-premises master control automation to primary operations and use cloud-based backup playout systems to provide disaster recovery.

- Multi-Language Regional Broadcasting: Multi-channel playout automation with built-in media asset management is used by international broadcasters to effectively deliver content in multiple language versions.

How AI is Transforming the Playout Automation and Channel-in-a-Box Market?

The playout automation is being radically changed with AI introducing intelligent automation, which is able to maximize content scheduling, graphics rendering, and operational efficiency. Within the context of playout scheduling and management, AI-based algorithms will process historical viewer data, content performance indicators, and real-time viewership data to dynamically optimize program schedules, automatically reallocating content to achieve an optimal audience retention and advertising revenue potential.

In media asset and content management, the indexing and metadata generation of content using AI can accelerate the process of preparing library content to be distributed on FAST channels by several factors. Machine learning algorithms automatically analyze video content to produce descriptive metadata, detect important scenes, highlight content suitability concerns, and produce chapter markers, greatly simplifying the manual effort needed to prepare content to be played out automatically. Playout systems are also being integrated with AI-driven content recommendation engines in order to provide a personalized channel experience, dynamically manipulating programming based on individual viewer preferences.

Market Dynamics

Key Drivers in the Global Playout Automation and Channel-in-a-Box Market

Proliferation of FAST Channels and OTT Distribution

The viral expansion of Free Ad-Supported Streaming Television channels is the paradigm shift in the economics of content distribution. International media corporations are introducing hundreds of thematic, niche channels to help attract divided audience attention on connected television systems. Conventional hardware-based playout infrastructure is incapable of supporting the deployment of dozens or hundreds of low cost channels economically. The scalability and cost efficiency of cloud-based playout automation and Channel-in-a-Box solutions are needed to run large portfolio of FAST channels, allowing media companies to generate revenue on library content by automatically playing out 24/7 with ad-insertion software.

Transition to IP-Based Broadcast Infrastructure

The broadcast sector is experiencing a generation shift in technology of Serial Digital Interface infrastructure to SMPTE ST 2110 IP-based workflow. Such migration necessitates broadcasters to upgrade or eliminate old master control automation software and playout systems to enable IP-native operation. The transition drives a great demand in terms of installation and deployment services, migration and upgrade services, and training and education to prepare broadcast engineering teams with the skills necessary to work in IP-based playout environments. The ability to support existing SDI workflows and new IP workflows smoothly is especially appreciated in software-defined playout solutions at this transitional stage.

Restraints in the Global Playout Automation and Channel-in-a-Box Market

Legacy Infrastructure Integration Complexity

Most of the established broadcasters have systems of legacy broadcast equipment that are difficult to replace or retire. It takes major custom engineering and integration to integrate the modern playout automation solutions with aging video servers, routing switchers and transmission systems. Migration and upgrade services are complex and expensive, and may slow down automation projects, especially to those with tight capital constraints or those with mission-critical channels where any form of interference is unacceptable. Operational complexity and cost is added by the challenge of having parallel legacy and modern playout workflows in transitional periods.

Broadcast Engineering Skills Shortage

The shift to software-defined, IP-based playout automation demands broadcast engineering staff to acquire new skills in IT networking, cloud computing, and software-defined processes. The lack of specialists with the traditional background of broadcast engineering and contemporary IT infrastructure is a severe issue. This skills deficit makes them reliant on external consulting and advisory services and impedes the implementation of more advanced playout automation capabilities. Organizations that are not able to attract or develop the required talent might postpone automation programs or under-use the available capacity of the implemented solutions.

Growth Opportunities in the Global Playout Automation and Channel-in-a-Box Market

Cloud-Native Playout for Tier-1 Broadcasters

Whilst cloud-based playout has been extensively used in FAST channels and secondary services, there is much potential to support the high demands of tier-1 broadcasters in primary channel playout. Solutions capable of providing the reliability, low latency and deterministic performance demanded by major network broadcasting and tapping into cloud economics is a significant growth prospect. High-value deployments with major broadcast networks will go to providers who can provide carrier-grade reliability through extensive monitoring and control mechanisms and failover.

Integrated Advertising Technology Platforms

The overlap of linear broadcasting and digital advertising opens up the prospects of integrated solutions that will combine the conventional ad-insertion software with the programmatic advertising potential. Broadcasters are interested in a single platform that would be capable of handling advertisements in both the traditional linear channels, OTT-based channels, and FAST channels and provide a consistent reporting and optimization. A combination of playout automation and sophisticated advertising decisioning, dynamic advertising replacement, and real-time campaign analytics will win a lot of value as broadcasters aim to maximize the value of addressable advertising.

Trends in the Global Playout Automation and Channel-in-a-Box Market

Convergence of Playout and OTT Origination

The conventional line between linear broadcasting playout and OTT stream origination is becoming blurred. The capabilities available in modern playout automation platforms are gradually being enhanced with the ability to present both traditional SDI/IP stream content to broadcast distribution and content to OTT platforms in adaptive bitrate streams. This convergence allows broadcasters to serve all distribution platforms in one playout infrastructure, simplifying operations and providing consistent viewing experiences to all viewing environments.

Adoption of Microservices Architecture

Playout automation vendors are moving towards microservices architectures that split up traditional monolithic playout applications into discrete and independently deployable services. This architectural design permits broadcasters to scale individual functions autonomously, deploy updates without system-interfering with, and to incorporate best-of-breed modules to certain functions: graphics playout software or ad-insertion software. Microservices architecture also supports hybrid deployment models whereby some functions are on-premises and others are on the cloud.

Research Scope and Analysis

The market is driven by cloud-based playout, unified automation solutions, and multi-channel broadcasting, with strong dominance of media and entertainment, while OTT, FAST channels, and hybrid deployments fuel rapid digital transformation.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Offering Analysis

The playout automation and channel-in-a-box market is poised to dominate by the solutions segment based on offering, where broadcasters value software platforms that have an immediate impact on controlling the content delivery, monetization and efficiency of their operations. At solutions, master control automation, media asset management (MAM) and ad-insertion systems are the leading ones because they are at the core of a continuous playout and revenue production. The vendors of end-to-end solutions have an advantage as they are more likely to win over fragmented tools as broadcasters wish to have unified ecosystems. In the meantime, the services part is also increasing, especially in consulting, migration, and cloud deployment support, due to the shift of the legacy infrastructure to IP-based and cloud workflows. Services are, however usually enablers, and not core investments, and are usually bundled with solution contracts. Consequently, solutions are still enjoying the biggest market share with services growing as part of the digital transformation efforts.

By Deployment Mode Analysis

Cloud-based deployment is projected to be the dominant and fastest-growing segment, due to the necessity of flexibility, scalability, and lower capital spending. Cloud playout is becoming popular among broadcasters and OTT providers to roll out new channels in seconds, notably FAST and niche digital channels, without significant investments in infrastructure. Cloud solutions facilitate remote operation and disaster recovery, as well as global distribution, and thus are very desirable in the broadcasting world today. Nevertheless, on-premise deployment continues to have a large market share, especially with large national broadcasters and organizations with regulated markets where latency, control, and data security are paramount. Such institutions tend to lean towards direct control of infrastructure. It is becoming a common trend to use a hybrid approach, which incorporates on-premises reliability as well as cloud platforms agility.

By Operation Analysis

Broadcast automation and linear channel automation are anticipated to dominate this segment, as it is the cornerstone of traditional television operations, providing reliable and constant playout. These are necessary systems that are used to plan, switch and assure a seamless flow of transmission between channels. Media asset management (MAM) is essential to them, coordinating content, storing, and retrieving it in an efficient way, and therefore cannot be ignored in any of the workflows. Nevertheless, the processing of videos, transcoding, compression, and real-time graphics rendering are emerging operations that are developing at a very high pace as a result of the emergence of OTTs and the consumption of content across multiple devices. Graphics management and branding solutions are also taking a centre stage with broadcasters looking to increase viewer interest and channel identity.

By Channel Type Analysis

The multi-channel segment are projected to dominate the market, as major broadcasters and media networks operate numerous channels across regions, languages, and genres. This needs to be supported by powerful automation solutions that are able to handle complex workflows and high content distribution volumes. But the most significant growth is seen in the OTT-based and FAST channels, which are fast becoming popular following the changing preferences of viewers and transitioning to digital streaming services. FAST channels, especially, are appealing since they provide free, advertisement-based content, which opens up new monetization possibilities. The regional and niche channels remain relevant, particularly in new markets where localized content leads to engagement. In the meantime, single-channel operations are slightly losing their comparative significance.

By Coverage Area Analysis

National broadcasters are expected to dominate this segment due to there vast infrastructure, large audience and operate various channels. They need advanced playout automation solutions that can process high amounts of content and provide a regular and high-quality broadcasting to all regions. These organizations tend to have already established workflows and a lot of investment in on-premises and hybrid systems. Conversely, international broadcasters are significant forces of innovation and expansion, since they extend into new markets worldwide and use new technologies like cloud play out, multi-language feeds and distributed content delivery. Their necessity to access a wide range of specialists drives them to use scalable and flexible solutions. National broadcasters are playing the biggest role in terms of revenue and deployment, however, international broadcasters are defining the direction of the future through adoption of digital transformation and cross-border content distribution approach.

By Application Analysis

The entertainment segment is expected to dominate the market, driven by the unending demand of movies, television shows and music channels which need effective playout systems to handle the large volumes of content. This group enjoys a steady audience and a wide range of programming requirements. Another significant factor is news broadcasting, specifically 24/7 news stations, which require real time automation, fast content delivery and high-level reliability. Sports broadcasting is a valuable consideration particularly with live events and highlights where low latency and accuracy is very important, but is less event-driven than entertainment. At the same time, children, lifestyle, and niche channels are growing steadily, frequently with the expansion into OTT platforms to address specific audiences.

By Vertical Analysis

The media and entertainment vertical is poised to dominate this segment, as it represents the primary user base for playout automation and channel-in-a-box solutions. Under this vertical, the biggest portion can be attributed to traditional TV broadcasting or OTT streaming platforms, which are necessitated by the need to have efficient content delivery and monetization. The second-largest segment is telecommunications, such as IPTV and cable operators, which incorporate playout systems as part of their content distribution infrastructure. In the meantime, the education, corporate, and government segments are becoming niche yet expanding markets. Educational institutions are leveraging playout systems for e-learning and distance broadcasting, while corporations use them for internal communication and branded content delivery. Governments are also using it in broadcasting public information and emergency communications. The scale, investment capacity and the sustained demand in the media and entertainment not withstanding this diversification, makes it apparent that it will dominate the market.

The Global Playout Automation and Channel-in-a-Box Market Report is segmented on the basis of the following:

By Offering

- Solutions

- Playout Scheduling & Management

- Master Control Automation Software

- Media Asset & Content Management (MAM)

- Graphics & Branding Solutions

- Graphics Playout Software

- Traffic & Scheduling Software

- Remote Playout Software

- Ad-Insertion Software

- Monitoring & Control Systems

- Network Management Software

- Other Solutions

- Services

- Consulting & Advisory

- Installation & Deployment

- Maintenance & Support

- Training & Education

- Migration & Upgrade

By Deployment Mode

By Operation

- Broadcast Automation

- Linear Channel Automation

- Live Event Playout

- Video & Image Processing

- Transcoding

- Compression & Encoding

- Graphics Management

- Branding & Channel Identity

- Real-Time Graphics Rendering

- Content Management

- Media Asset Management (MAM)

- Content Scheduling & Archiving

By Channel Type

- Single Channel

- Regional Channels

- Niche/Thematic Channels

- Multi-Channel

- Network Broadcasting

- Multi-Language Channels

- Advanced / Multi-purpose Channels

- OTT-based Channels

- FAST (Free Ad-Supported Streaming TV) Channels

By Coverage Area

- National Broadcasters

- International Broadcasters

By Application

- Entertainment

- Movies

- TV Shows

- Music Channels

- News

- 24/7 News Broadcasting

- Regional News Channels

- Sports

- Live Sports Broadcasting

- Sports Highlights Channels

- Kids / Cartoons

- Animated Content Channels

- Educational Kids Programming

- Lifestyle

- Travel

- Food & Cooking

- Fashion

- Others

By Vertical

- Media & Entertainment

- TV Broadcasting

- OTT Streaming

- Telecommunications

- Education

- E-Learning Channels

- Distance Learning Broadcasting

- Corporate

- Internal Communication Channels

- Corporate TV

- Government

- Public Information Broadcasting

- Defense Media Systems

- Other Vertical

Regional Analysis

Leading Region by Market Share

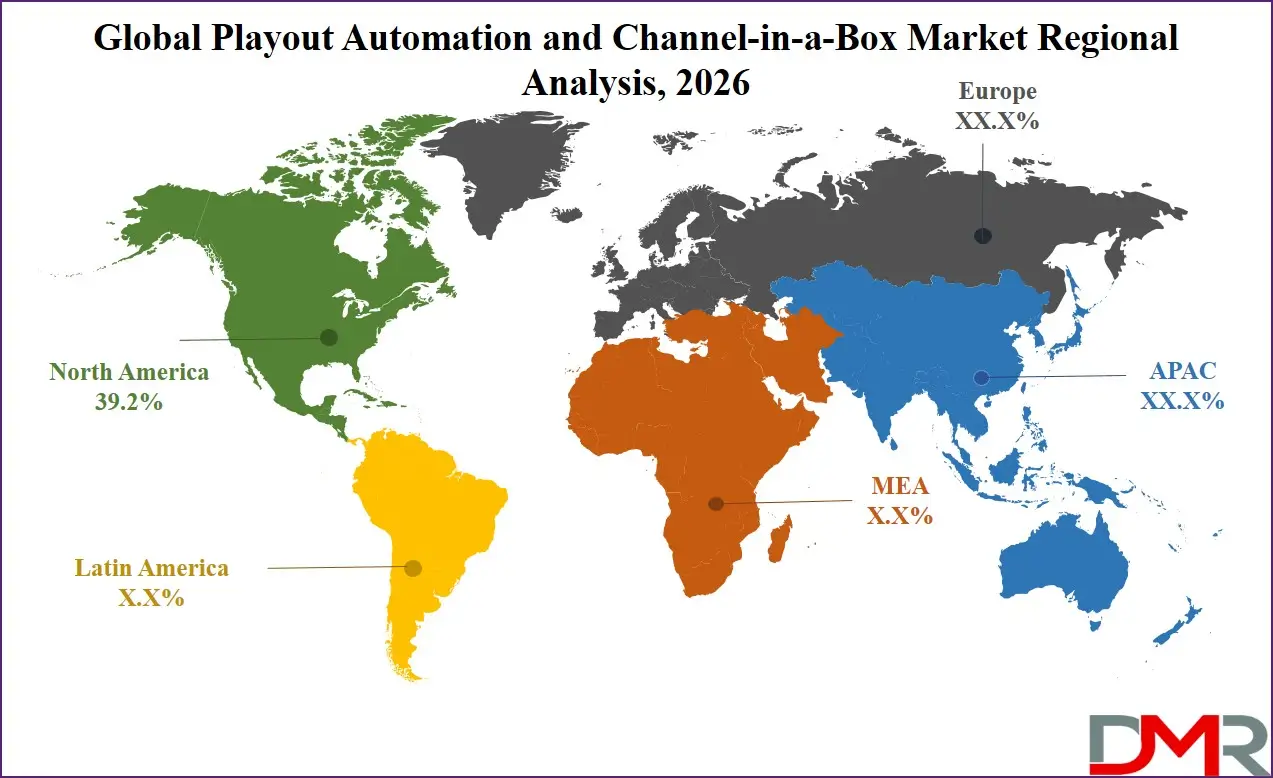

North America is poised to dominate the global playout automation and Channel-in-a-Box market as it is projected to hold 39.2% of the market share by the end of 2026. The United States, leading North America, has the largest market share in the playout automation sector, with the concentration of large media conglomerates, the technological innovation of FAST channels, and the vigorous modernization of broadcast infrastructure by large networks and station groups.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The region enjoys an established ecosystem of playout automation companies and systems integrators and technology partners who together enable innovations and the implementation of sophisticated broadcast solutions. Broadcaster investment in cloud playout platforms, IP-based infrastructure, and AI-based automation remains to gain pace as broadcasters pursue operational efficiencies and new sources of revenue.

Fastest-Growing Regional Market

The Asia-Pacific market is anticipated to experience the fastest growing playout automation and Channel in a Box market, owing to the swift digital transformation of the media industry in India, China, Southeast Asia, and Australia. The large and expanding television audience in the region, along with a rapidly increasing adoption of OTT, and government efforts to digitalize broadcast infrastructure, present significant demand on modern playout automation solutions.

The television market in India is a huge prospect to the playout automation vendors as more than 900 channels are registered and more broadcasters are modernizing their operations and are opening up regional as well as niche channels. Media modernization efforts by the state are fueling investment in modern broadcast facilities such as IP-based playout and cloud-based operations in China. Pay-TV and OTT services are growing rapidly in southeast Asian markets, which puts pressure on the need to find efficient multi-channel playout systems.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The market landscape of the global playout automation and Channel-in-a-Box is both competitive and marked by a wide range of established broadcast technology vendors, new cloud-native technologies, and solution providers. Traditional broadcast equipment manufacturers have diversified their product offerings with software-defined and cloud-enabled playout products, and pure-play software vendors have disrupted the market with new methods of channel automation.

Competitive advantage is becoming more dependent on the scope and scale of cloud deployment offerings, and cloud-native architectures between vendors are becoming a major investment in the ability to support the scale and flexibility demanded by FAST channel operations. Alliances with major cloud service providers, such as AWS, Microsoft Azure, and Google Cloud are becoming a necessity among vendors who want to provide strong cloud-based playout solutions.

Some of the prominent players in the Global Playout Automation and Channel-in-a-Box Market are:

- Harmonic Inc.

- Imagine Communications Corp.

- Grass Valley USA LLC

- Evertz Microsystems Ltd.

- Pebble Beach Systems Ltd.

- Cinegy LLC

- Pixel Power Ltd.

- PlayBox Technology Ltd.

- PlayBox Neo

- BroadStream Solutions Inc.

- Axel Technology Srl

- Aveco s.r.o.

- Anyware Video Corp.

- Florical Systems

- Hardata Corp.

- ENCO Systems Inc.

- Ross Video Ltd.

- Vizrt Group

- Dalet Digital Media Systems

- Skyline Communications

- Other Key Players

Recent Developments

- March 2026: Harmonic Inc. added cloud-native playout investments, with a focus on SaaS-based channel origination and AI-based automation, making it possible to operationalize FAST and OTT channels quickly and reduce infrastructure costs, increasing flexibility and overall operational scalability across global media operations.

- October 2025: Imagine Communications has purchased Pixel Power, Rohde and Schwarz, reinforcing its cloud playout, automation and graphics offerings to provide fully integrated, scalable channel-in-a-box system solutions to meet the changing needs of the global broadcasters.

- September 2025: The major innovations exhibited at IBC Show 2025 included cloud playout, remote production, and AI-driven scheduling, with the key vendors demonstrating advanced channel-in-a-box platforms to address OTT and FAST channels and efficient multi-region content delivery strategies across the globe.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 3,291.9 Mn |

| Forecast Value (2035) |

USD 7,418.6 Mn |

| CAGR (2026–2035) |

9.4% |

| The US Market Size (2026) |

USD 1,085.2 Mn |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Offering (Solutions, and Services), By Deployment Mode (On-Premises, and Cloud-Based), By Operation (Broadcast Automation, Video & Image Processing, Graphics Management, and Content Management), By Channel Type (Single Channel, Multi-Channel, and Advanced/Multi-purpose Channels), By Coverage Area (National Broadcasters, and International Broadcasters), By Application (Entertainment, News, Sports, Kids/Cartoons, Lifestyle, and Others), By Vertical (Media & Entertainment, Telecommunications, Education, Corporate, Government, and Other Vertical) |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Global Playout Automation and Channel-in-a-Box Market?

▾ The Global Playout Automation and Channel-in-a-Box market is poised to be valued at USD 3,291.9 million in 2026 and is projected to reach USD 7,418.6 million by 2035, driven by the universal need for efficient multi-platform content delivery and the explosive growth of FAST channels.

What is the CAGR of the Global Playout Automation and Channel-in-a-Box Market from 2026 to 2035?

▾ The market is expected to grow at a CAGR of 9.4% from 2026 to 2035, reflecting the accelerating transition to IP-based broadcast infrastructure and the proliferation of OTT-based and FAST channel distribution models.

What factors are driving the growth of the Global Playout Automation and Channel-in-a-Box Market?

▾ Key drivers include the rapid expansion of FAST channel platforms, the broadcast industry's migration from SDI to IP-based workflows, the imperative to reduce operational costs in linear channel operations, and the integration of AI capabilities for intelligent content scheduling and graphics automation.

Which region held the largest share of the Playout Automation and Channel-in-a-Box Market in 2026?

▾ North America, specifically the United States, held 39.2% of market share in 2026, driven by the concentration of major media conglomerates, leadership in FAST channel innovation, and aggressive investment in next-generation broadcast infrastructure including cloud-based playout and ATSC 3.0 deployment.

Which region is expected to grow the fastest in the Playout Automation and Channel-in-a-Box Market?

▾ The Asia-Pacific region is expected to grow the fastest, fueled by rapid digital transformation in the media sector across India, China, and Southeast Asia, where broadcasters are modernizing infrastructure and launching new channels to serve diverse linguistic and regional audiences.

What are the major trends in the Global Playout Automation and Channel-in-a-Box Market?

▾ Major trends include the convergence of playout and OTT origination capabilities, the adoption of microservices architectures enabling hybrid deployment flexibility, the integration of AI for intelligent scheduling and content optimization, and the increasing focus on sustainability and energy efficiency in broadcast operations.

Who are the key players in the Global Playout Automation and Channel-in-a-Box Market?

▾ Key players include established broadcast technology vendors offering integrated playout solutions, cloud-native platform providers specializing in FAST channel automation, graphics and branding solution specialists, and systems integrators providing comprehensive deployment and migration services.

How is the Global Playout Automation and Channel-in-a-Box Market segmented?

▾ The market is segmented by Offering, Deployment Mode, Operation, Channel Type, Coverage Area, Application, and Vertical.