What is the Point-of-Care Testing (POCT) Women Health Market Size?

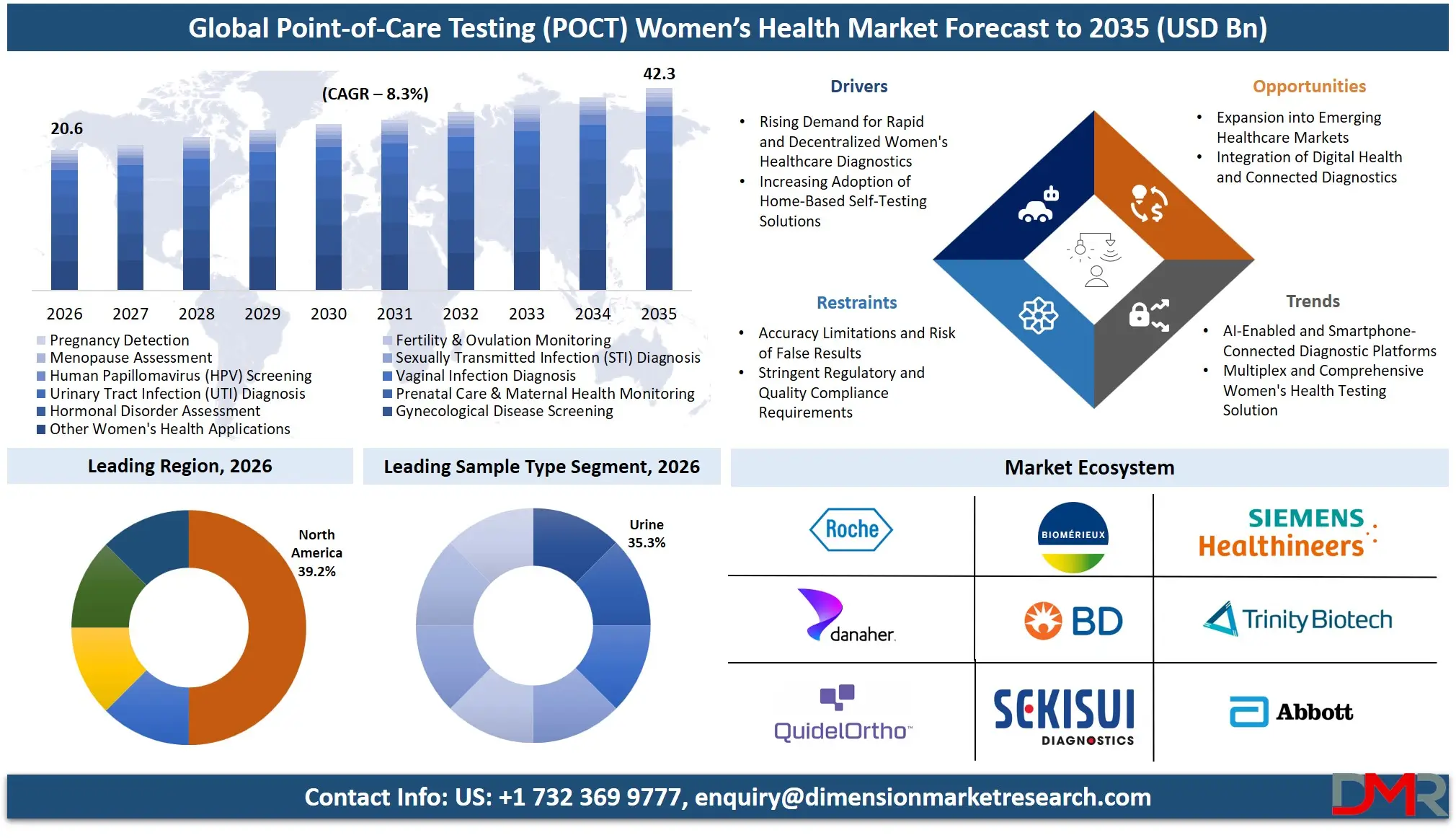

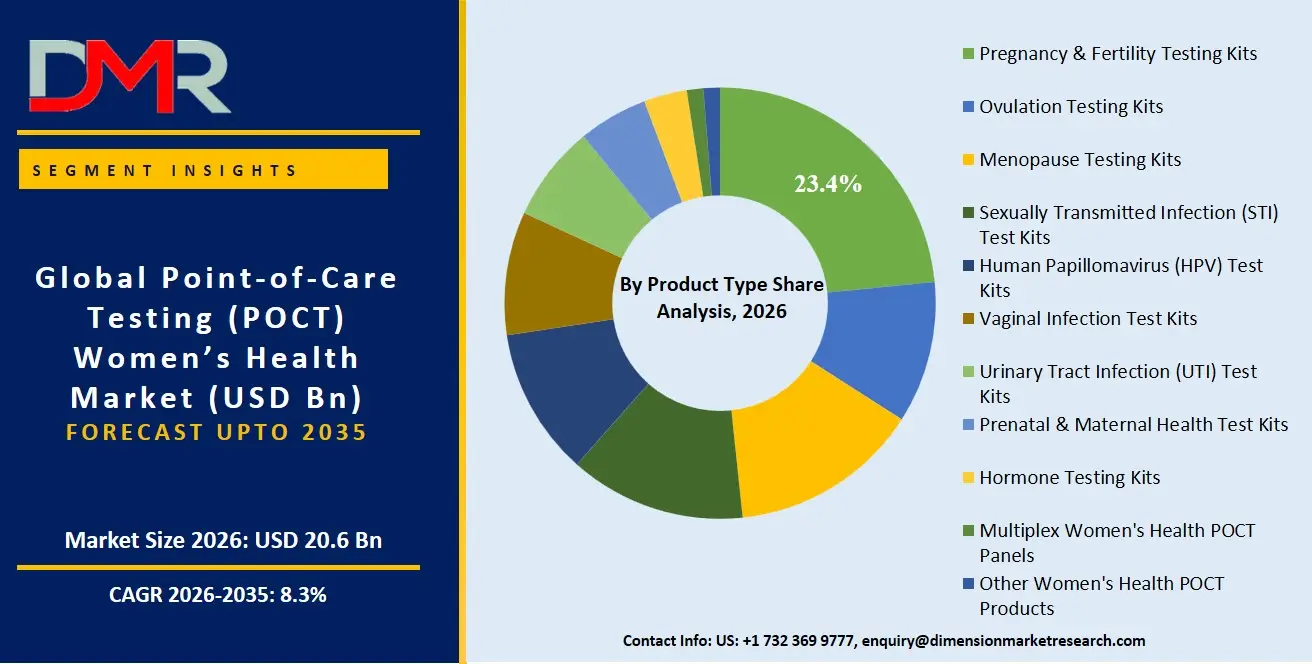

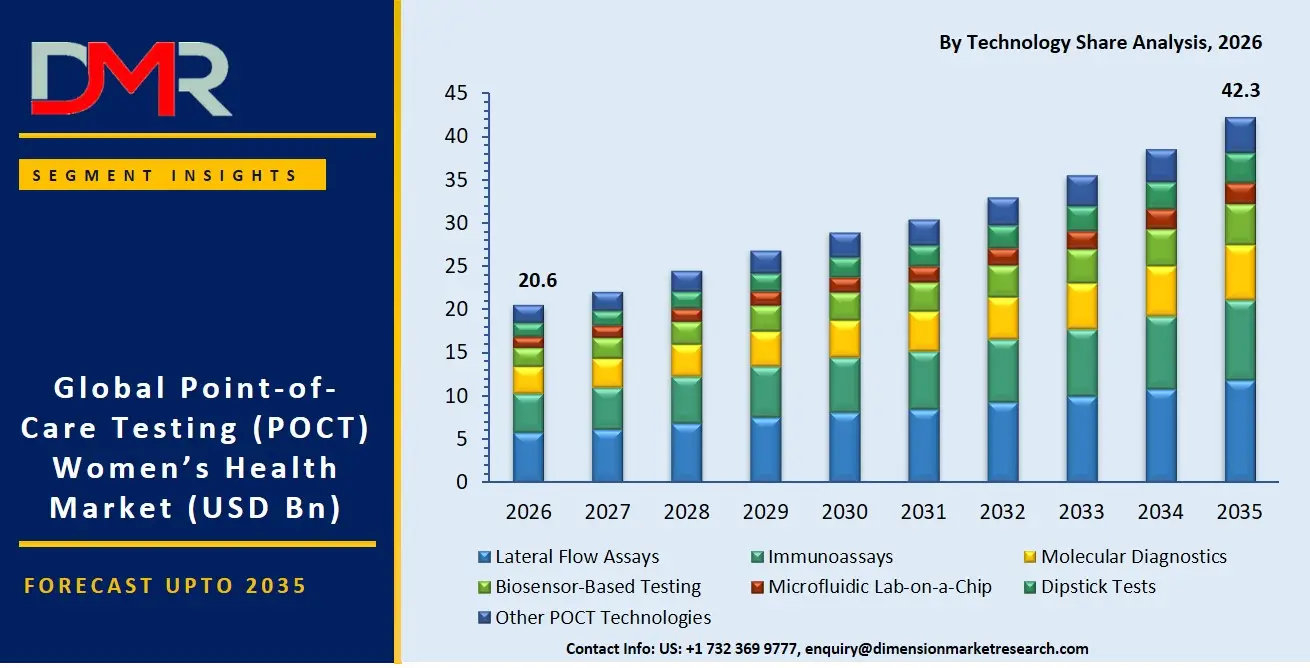

The Global Point-of-Care Testing (POCT) Women Health Market is expected to reach a value of USD 20.6 billion in 2026, and it is further anticipated to reach USD 42.3 billion by 2035, growing at a CAGR of 8.3% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The POCT Women health market is experiencing significant growth, fueled by a paradigm shift from centralized laboratory diagnostics to decentralized, patient-centric care models. This market encompasses a diverse array of rapid diagnostic tools, including pregnancy and fertility testing kits, ovulation and menopause assessment kits, and infectious disease screening solutions for STIs, HPV, and UTIs. The increasing consumer preference for privacy, convenience, and immediate results is a primary driver, particularly for over-the-counter (OTC) self-testing products. Technological advancements in lateral flow assays, molecular diagnostics, and biosensor-based platforms are enhancing test accuracy and expanding the scope of conditions that can be managed at home or in a primary care setting, making proactive Women health management more accessible than ever.

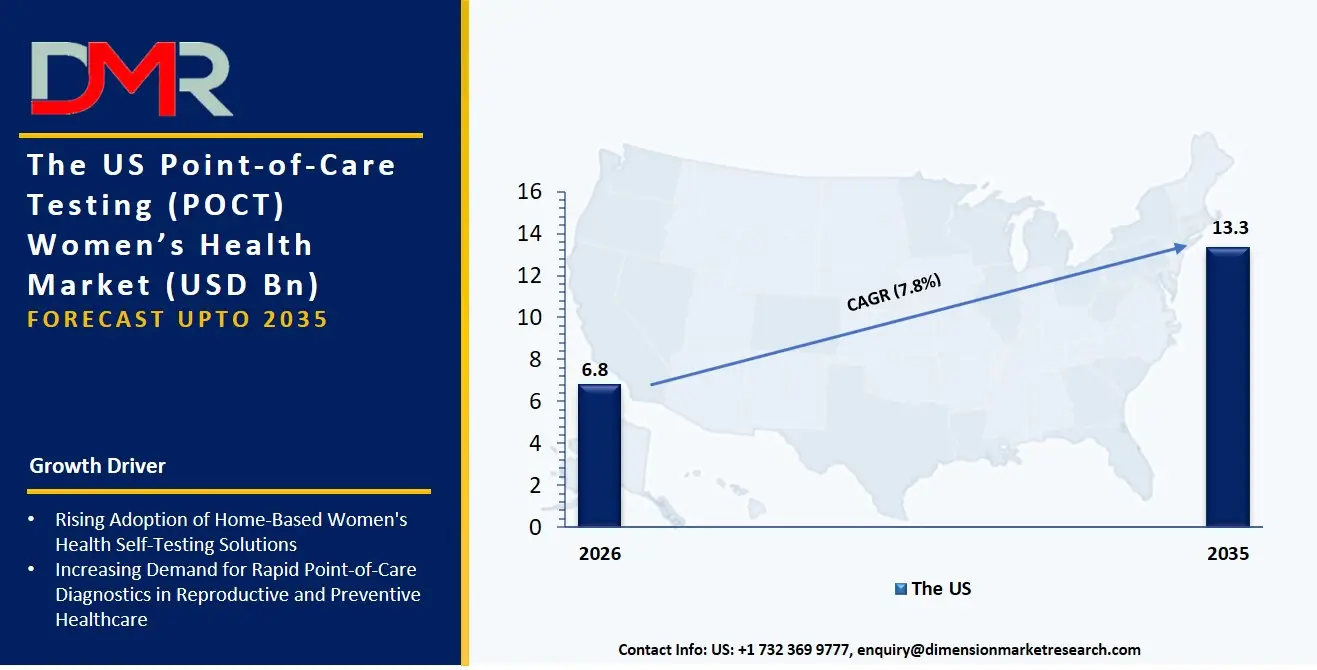

The US Point-of-Care Testing (POCT) Women Health Market

The US POCT Women Health Market is projected to reach USD 6.8 billion in 2026 at a compound annual growth rate of 7.8% over its forecast period, culminating in a value of USD 13.3 billion by 2035.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The United States maintains a commanding lead in this market, propelled by high health awareness, robust direct-to-consumer marketing, and a favorable regulatory pathway for OTC tests cleared by the FDA. The market is characterized by a high volume of self-testing, particularly with digital ovulation and pregnancy tests that offer app connectivity. A significant growth catalyst is the destigmatization of STI self-testing, with chlamydia and gonorrhea home kits gaining traction. Furthermore, the integration of multiplex panels into pharmacy and retail clinic settings is transforming the diagnosis of vaginitis and vaginosis, providing a comprehensive molecular profile from a single vaginal swab during a brief clinic visit.

The Europe Point-of-Care Testing (POCT) Women Health Market

The Europe POCT Women Health Market is estimated to be valued at USD 5.8 billion in 2026 and is further anticipated to reach USD 11.7 billion by 2035 at a CAGR of 8.1%. The European market is heavily influenced by progressive health policies and structured national screening programs, particularly for prenatal care and HPV screening. The shift toward self-sampling for cervical cancer screening, using HPV test kits that can be used at home, is creating a new non-invasive avenue for patient participation, circumventing the barriers of traditional Pap smears. In countries like the UK, France, and Germany, public health initiatives are increasingly incorporating POCT for rapid STI diagnosis to combat rising infection rates. The demand for hormone testing kits, especially FSH and estradiol tests for menopause assessment, is also surging as telemedicine platforms integrate these home-based diagnostics for remote consultations on hormone replacement therapy (HRT).

The Japan Point-of-Care Testing (POCT) Women Health Market

The Japan POCT Women Health Market is projected to be valued at USD 998.2 Million in 2026 at a CAGR of 7.4%. The Japanese market is uniquely shaped by its aging demographic and the strategic prioritization of Women health in a traditionally underserved sector. There is a pronounced demand for high-sensitivity menopause testing kits and related hormone monitoring tools (FSH and LH tests) as the "Femtech" movement gains corporate and governmental support. This market also shows a strong cultural preference for high-quality, user-friendly self-testing devices with minimal invasiveness, driving innovation in saliva and urine-based sample formats. Moreover, community health centers and pharmacies are evolving into key diagnostic points, using rapid vaginal infection and UTI test kits to provide immediate counseling and treatment, thereby reducing the strain on overburdened physician offices.

Key Takeaways

- Market Size & Forecast: The Global POCT Women Health market is projected to reach USD 20.6 billion in 2026, expanding significantly to USD 42.3 billion by 2035, fueled by the convergence of at-home diagnostic convenience and AI-driven health insights on smartphones.

- Growth Rate & Outlook: Global market growth is expected at a CAGR of 8.3%, driven by a paradigm shift toward decentralized healthcare models that prioritize privacy and immediate results for sensitive Women health conditions.

- Primary Growth Drivers: Key forces include the destigmatization of STI self-testing, the urgent need for accessible prenatal care in maternity deserts, and the consumerization of fertility tracking, which is moving hormone testing kits from the lab to the home bathroom.

- Key Market Trends: Major trends include the rise of multiplex POCT panels that differentiate between multiple vaginal infections simultaneously, the use of Bluetooth-enabled lateral flow assays, and the development of non-invasive microfluidic platforms requiring only saliva or a few drops of blood.

- By Product Type Analysis: Pregnancy & Fertility Testing Kits are expected to command a dominant volume share due to their OTC availability and lifecycle demand. However, STI Test Kits and Multiplex Women Health POCT Panels are the fastest-growing categories, driven by the need for discreet, rapid diagnosis of chlamydia, gonorrhea, and trichomoniasis outside of traditional clinics.

- By Technology Analysis: Molecular Diagnostics, particularly isothermal amplification, is the most disruptive technological segment, bringing PCR-grade accuracy for HPV and STI detection directly to physician offices and home settings without the need for complex thermal cycling equipment.

- By End User Analysis: Home Care Settings constitute the most dynamic and fastest-expanding end-user segment due to the empowerment of self-care. Hospitals and Diagnostic Laboratories remain crucial for high-complexity confirmatory tests, while Pharmacies & Retail Clinics are emerging as pivotal hubs for professional-grade POCT.

- Regional Leadership: North America is poised to dominate this market with 39.2% of the market share in 2026, attributed to a strong FDA regulatory framework for OTC devices, a culture of proactive wellness, and high reimbursement levels for professional POCT in primary care settings.

What is the Point-of-Care Testing (POCT) Women Health?

Point-of-Care Testing (POCT) for Women Health refers to rapid diagnostic procedures and kits performed at or near the site of patient care, bypassing the logistical complexities of a central laboratory. These services and products, unlike external lab referrals, provide actionable clinical information within minutes. This includes everything from Lateral Flow Assays for pregnancy detection to advanced Molecular Diagnostics for the rapid identification of HPV genotypes. In a landscape where 70% of clinical decisions depend on diagnostic results, POCT empowers both clinicians in gynecology clinics and women in home care settings to make immediate, informed decisions about fertility, infection management, and hormonal health, translating complex biology into clear, timely outcomes.

Use Cases

- Proactive Fertility Management at Home: Women use connected ovulation testing kits that measure LH surges and integrate with mobile apps to predict fertile windows with clinical precision, facilitating timely conception without multiple clinic visits.

- Rapid Vaginitis Differential Diagnosis in Clinics: Nurse practitioners in retail clinics use single-use, multiplex molecular panels from vaginal swabs to distinguish between bacterial vaginosis, candida vaginitis, and trichomoniasis in under 30 minutes, enabling a single-visit diagnosis and prescription.

- Self-Sampling for Cervical Cancer Screening: Public health programs mail HPV self-collection kits directly to Women homes, allowing them to return a cervical swab sample via mail for lab-grade molecular analysis, dramatically increasing screening uptake for underserved populations.

- Hormonal Transition Monitoring in Menopause: Perimenopausal women purchase over-the-counter FSH testing kits from online pharmacies to track their hormonal transition over several days, using the data to prepare for informed discussions with telehealth providers about symptom management.

How AI is Transforming the Point-of-Care Testing (POCT) Women Health Market?

AI is fundamentally reshaping the POCT Women health market by digitizing and personalizing diagnostic interpretation. In the Lateral Flow Assays segment, AI-powered smartphone applications are moving beyond simple line detection; deep learning algorithms analyze the subtle spectral reflectance of test strips for pregnancy and ovulation kits, providing a quantitative hormone concentration instead of a binary result, which significantly improves accuracy for both early pregnancy detection and precise peak fertility identification. This "quantified self" approach turns a simple dipstick into a sophisticated health monitor.

Furthermore, AI is driving value into multiplex diagnostic panels by acting as an interpretation layer. For Vaginal Infection and STI Test Kits, machine learning models are trained to correlate a patient's rapid molecular results with reported symptoms, age, and cycle phase to recommend evidence-based treatment pathways directly to the patient or consulting physician, reducing diagnostic uncertainty. In the context of prenatal care, non-invasive, biosensor-based tests analyzing urine biomarkers are using predictive algorithms to establish personalized baseline health parameters during the first trimester, enabling earlier risk stratification for conditions like preeclampsia by detecting subtle deviations that would be missed by a human reading.

Market Dynamics

Key Drivers in the Global Point-of-Care Testing (POCT) Women Health Market

Rising Demand for Rapid and Decentralized Women Healthcare Diagnostics

The growing emphasis on early disease detection and timely reproductive health management is a major driver of the global Point-of-Care Testing (POCT) Women Health Market. Women increasingly seek rapid diagnostic solutions for pregnancy, fertility, sexually transmitted infections (STIs), urinary tract infections (UTIs), menopause, and hormonal disorders without lengthy laboratory procedures. Healthcare providers are also adopting POCT to improve clinical decision-making, reduce diagnostic turnaround times, and enhance patient outcomes. Expanding awareness of preventive healthcare, rising maternal health initiatives, and increased accessibility of self-testing kits through pharmacies and digital channels further accelerate market demand. Continuous innovation in portable diagnostic devices and user-friendly testing formats continues to strengthen market growth globally.

Increasing Adoption of Home-Based Self-Testing Solutions

The rapid expansion of home healthcare has significantly increased the demand for Women health POCT products. Consumers increasingly prefer self-testing due to greater convenience, privacy, affordability, and immediate results. Home pregnancy, ovulation, fertility, menopause, and infection detection kits have become widely accepted because they eliminate unnecessary clinic visits while supporting proactive health management. Improvements in digital health applications, smartphone-enabled result interpretation, and telemedicine integration have further enhanced user confidence. Manufacturers are introducing highly accurate, easy-to-use diagnostic kits with simplified instructions, expanding accessibility across developed and emerging economies. This growing consumer shift toward personalized healthcare continues to drive sustained demand for Women health POCT solutions.

Restraints in the Global Point-of-Care Testing (POCT) Women Health Market

Accuracy Limitations and Risk of False Results

Despite technological advancements, certain point-of-care diagnostic tests continue to face challenges related to analytical sensitivity and specificity compared with centralized laboratory testing. False-positive or false-negative results may delay appropriate treatment or require confirmatory laboratory testing, particularly for infectious diseases and hormonal assessments. Variations in sample collection, improper test usage, environmental conditions, and user interpretation can affect diagnostic reliability. These concerns reduce physician confidence in certain POCT applications and may limit adoption in critical clinical settings. Manufacturers must continually improve assay performance, quality assurance, and user education to strengthen diagnostic accuracy and maintain regulatory compliance across global healthcare markets.

Stringent Regulatory and Quality Compliance Requirements

Women health diagnostic products must comply with rigorous regulatory standards governing safety, performance, manufacturing quality, labeling, and clinical validation. Approval processes often require extensive analytical studies, clinical trials, and post-market surveillance before commercialization. Regulatory requirements differ across countries, creating additional complexity for global manufacturers seeking market expansion. Frequent updates to diagnostic regulations, quality management standards, and reimbursement policies may increase product development costs and delay product launches. Smaller companies often face financial and technical barriers in meeting these evolving requirements, potentially limiting innovation and slowing commercialization of next-generation Women health POCT technologies.

Growth Opportunities in the Global Point-of-Care Testing (POCT) Women Health Market

Expansion into Emerging Healthcare Markets

Emerging economies present significant growth opportunities due to expanding healthcare infrastructure, increasing Women health awareness, rising healthcare expenditure, and improving access to primary care services. Governments are investing in maternal health programs, reproductive healthcare initiatives, and infectious disease screening, creating favorable conditions for wider POCT adoption. Rural healthcare facilities particularly benefit from portable diagnostic technologies that operate without sophisticated laboratory infrastructure. Growing pharmacy networks, online healthcare platforms, and community health programs further support product accessibility. As healthcare modernization continues across Asia-Pacific, Latin America, the Middle East, and Africa, manufacturers are expected to experience substantial long-term growth opportunities.

Integration of Digital Health and Connected Diagnostics

Digital transformation offers major opportunities for next-generation Women health diagnostics. Manufacturers are increasingly integrating POCT devices with smartphone applications, cloud platforms, artificial intelligence, and remote patient monitoring systems. Connected diagnostics enable automated result interpretation, longitudinal health tracking, physician consultation, and personalized reproductive health management. Fertility monitoring, pregnancy tracking, and hormonal assessment applications particularly benefit from digital integration, improving patient engagement and treatment adherence. As telehealth services continue expanding globally, connected POCT platforms will support decentralized healthcare delivery while creating recurring revenue opportunities through software services, subscription models, and integrated digital health ecosystems.

Trends in the Global Point-of-Care Testing (POCT) Women Health Market

AI-Enabled and Smartphone-Connected Diagnostic Platforms

Artificial intelligence and smartphone connectivity are becoming defining trends within Women health POCT. Modern diagnostic kits increasingly incorporate mobile applications capable of guiding sample collection, automatically interpreting results, tracking reproductive health trends, and securely sharing data with healthcare providers. AI-driven analytics enhance diagnostic precision while supporting personalized recommendations for fertility planning, pregnancy monitoring, and hormonal health management. These connected ecosystems improve user experience, encourage continuous health monitoring, and strengthen physician-patient communication. As digital healthcare adoption accelerates worldwide, AI-enabled POCT solutions are expected to become an integral component of personalized Women healthcare.

Multiplex and Comprehensive Women Health Testing Solutions

Manufacturers are increasingly developing multiplex POCT platforms capable of detecting multiple biomarkers or diseases from a single patient sample. Rather than performing separate tests for pregnancy, STIs, vaginal infections, hormonal disorders, or HPV, healthcare providers can obtain comprehensive diagnostic information simultaneously. Multiplex testing improves workflow efficiency, reduces diagnostic delays, minimizes sample collection requirements, and enhances clinical decision-making. Continued advances in microfluidics, molecular diagnostics, and biosensor technologies are enabling compact, highly accurate multiplex devices suitable for clinics, pharmacies, and home settings. This trend is expected to significantly expand the clinical utility and commercial value of Women health point-of-care diagnostics.

Research Scope and Analysis

The Global Point-of-Care Testing (POCT) Women Health Market is segmented by product type, technology, sample type, mode of prescription, test setting, distribution channel, application, and end user. These segments comprehensively evaluate demand across pregnancy, fertility, menopause, infectious disease, and hormonal diagnostics, while highlighting technology adoption, healthcare delivery models, consumer accessibility, and evolving Women health testing preferences globally.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Product Type Analysis

Pregnancy & Fertility Testing Kits is projected to dominate the global Point-of-Care Testing (POCT) Women Health Market due to their widespread consumer adoption, affordability, rapid results, and strong retail availability. Home pregnancy tests remain among the highest-volume diagnostic products worldwide, while fertility monitoring kits continue to gain popularity because of delayed pregnancies, rising infertility rates, and growing family planning awareness. These tests require minimal training, provide results within minutes, and are increasingly integrated with digital health applications for cycle tracking. Continuous technological improvements in sensitivity, ease of use, and smartphone compatibility have further strengthened demand. Their availability through pharmacies, supermarkets, e-commerce platforms, and healthcare providers ensures consistent global market leadership.

By Technology Analysis

Lateral Flow Assays is expected to represent the dominant technology in the market because they provide rapid, cost-effective, portable, and easy-to-use diagnostic solutions suitable for both clinical and home settings.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Pregnancy, ovulation, menopause, and several infectious disease tests predominantly utilize lateral flow technology due to its high convenience and minimal infrastructure requirements. Manufacturers continue improving analytical sensitivity while maintaining low production costs, enabling mass commercialization across developed and emerging economies. Their long shelf life, room-temperature storage capability, and simple visual interpretation make them ideal for decentralized healthcare. Strong regulatory approvals and extensive global manufacturing capacity continue to reinforce the leadership of lateral flow assays across Women health POCT applications.

By Sample Type Analysis

Urine is poised to remain the dominant sample type because it is non-invasive, painless, easy to collect, and well suited for home-based diagnostics. Pregnancy, ovulation, fertility, menopause, and several urinary tract infection tests primarily rely on urine specimens, supporting exceptionally high testing volumes globally. Urine-based testing eliminates the need for trained healthcare professionals and specialized collection equipment, significantly improving patient convenience and compliance. Manufacturers have optimized urine-based assays for excellent analytical performance while maintaining affordability. Growing demand for self-testing, increasing retail availability, and expanding digital fertility monitoring platforms continue strengthening urine's position as the preferred specimen across numerous Women health point-of-care diagnostic applications.

By Mode of Prescription Analysis

Over-the-Counter (OTC) Tests is expected to dominate the market due to growing consumer preference for convenient, private, and self-directed healthcare. Pregnancy and ovulation tests have become household healthcare products that can be purchased without physician consultation. Increasing health awareness, expanding pharmacy networks, online retail growth, and supportive regulatory pathways have accelerated OTC adoption worldwide. Consumers increasingly prefer immediate access to diagnostic information while avoiding unnecessary clinical visits. Technological improvements have enhanced test accuracy and user confidence, encouraging repeat purchases. Rising digital health integration, smartphone connectivity, and discreet home testing continue to drive OTC dominance across multiple Women health diagnostic categories globally.

By Test Setting Analysis

Self-Testing/Home-Based Testing is poised to represent the leading test setting because it offers unmatched convenience, privacy, affordability, and accessibility. Women increasingly prefer conducting pregnancy, ovulation, fertility, and menopause assessments at home rather than visiting healthcare facilities. The expansion of digital health platforms, smartphone-enabled result interpretation, and e-commerce distribution has accelerated home testing adoption worldwide. The COVID-19 pandemic further normalized self-testing behavior, creating lasting consumer acceptance of decentralized diagnostics. Continuous improvements in test accuracy, user-friendly designs, instructional support, and connected healthcare applications have strengthened confidence in home-based diagnostics, making this segment the largest contributor to overall market revenue.

By Distribution Channel Analysis

Retail Pharmacies is projected to dominate distribution because they offer broad product availability, immediate purchase convenience, trusted pharmacist guidance, and strong consumer accessibility. Pregnancy tests, ovulation kits, menopause tests, and urinary tract infection diagnostics are routinely stocked across pharmacy chains worldwide. Consumers often prefer pharmacies for confidential purchasing while receiving professional advice when necessary. Pharmacy expansion across urban and semi-urban regions has significantly increased product penetration. Strong partnerships between diagnostic manufacturers and retail pharmacy networks ensure widespread product visibility and consistent replenishment. Growing integration of pharmacy-based healthcare services further supports retail pharmacies as the primary distribution channel within the market.

By Application Analysis

Pregnancy Detection is poised to be the dominant application owing to its exceptionally high testing frequency, global demand, and universal clinical importance. Early pregnancy confirmation is essential for prenatal care planning, medical decision-making, and reproductive health management. Home pregnancy tests have become widely accepted because they provide accurate results within minutes while maintaining affordability and ease of use. Increasing reproductive health awareness, expanding access to OTC diagnostics, and rising healthcare literacy continue driving demand across developed and emerging economies. Continuous improvements in assay sensitivity, digital pregnancy tests, and smartphone-connected monitoring solutions further reinforce pregnancy detection as the largest application segment.

By End User Analysis

Home Care Settings is anticipated to dominate the end-user segment because Women health POCT products are increasingly designed for independent use without professional supervision. Pregnancy, fertility, ovulation, and menopause tests are routinely performed at home, supported by clear instructions, reliable accuracy, and growing digital healthcare integration. Consumers value privacy, convenience, rapid results, and reduced healthcare costs, making home testing highly attractive. Expanding online purchasing options, telemedicine services, and smartphone health applications have further strengthened home-based diagnostics. Continuous innovation in user-friendly testing formats and increasing consumer confidence in self-monitoring continue to position home care settings as the largest end-user segment.

The Global Point-of-Care Testing (POCT) Women Health Market Report is segmented on the basis of the following:

By Product Type

- Pregnancy & Fertility Testing Kits

- Ovulation Testing Kits

- Menopause Testing Kits

- Sexually Transmitted Infection (STI) Test Kits

- Human Papillomavirus (HPV) Test Kits

- Vaginal Infection Test Kits

- Urinary Tract Infection (UTI) Test Kits

- Prenatal & Maternal Health Test Kits

- Hormone Testing Kits

- Follicle-Stimulating Hormone (FSH) Tests

- Luteinizing Hormone (LH) Tests

- Estradiol Tests

- Progesterone Tests

- Multiplex Women Health POCT Panels

- Other Women Health POCT Products

By Technology

- Lateral Flow Assays

- Immunoassays

- Molecular Diagnostics

- PCR-Based POCT

- Isothermal Amplification

- Biosensor-Based Testing

- Microfluidic Lab-on-a-Chip

- Dipstick Tests

- Other POCT Technologies

By Sample Type

- Urine

- Blood

- Vaginal Swab

- Cervical Swab

- Saliva

- Serum/Plasma

- Other Sample Types

By Mode of Prescription

- Prescription-Based Tests

- Over-the-Counter (OTC) Tests

By Test Setting

- Professional Point-of-Care Testing

- Self-Testing/Home-Based Testing

By Distribution Channel

- Retail Pharmacies

- Hospital Pharmacies

- Online Pharmacies

- Direct Sales

- Distributors & Wholesalers

By Application

- Pregnancy Detection

- Fertility & Ovulation Monitoring

- Menopause Assessment

- Sexually Transmitted Infection (STI) Diagnosis

- Human Papillomavirus (HPV) Screening

- Vaginal Infection Diagnosis

- Urinary Tract Infection (UTI) Diagnosis

- Prenatal Care & Maternal Health Monitoring

- Hormonal Disorder Assessment

- Gynecological Disease Screening

- Other Women Health Applications

By End User

- Home Care Settings

- Hospitals

- Diagnostic Laboratories

- Physician Offices & Gynecology Clinics

- Primary Care Centers

- Community Health Centers

- Pharmacies & Retail Clinics

- Ambulatory Surgical Centers (ASCs)

- Other End Users

Regional Analysis

Leading Region by Market Share

ℹ

To learn more about this report –

Download Your Free Sample Report Here

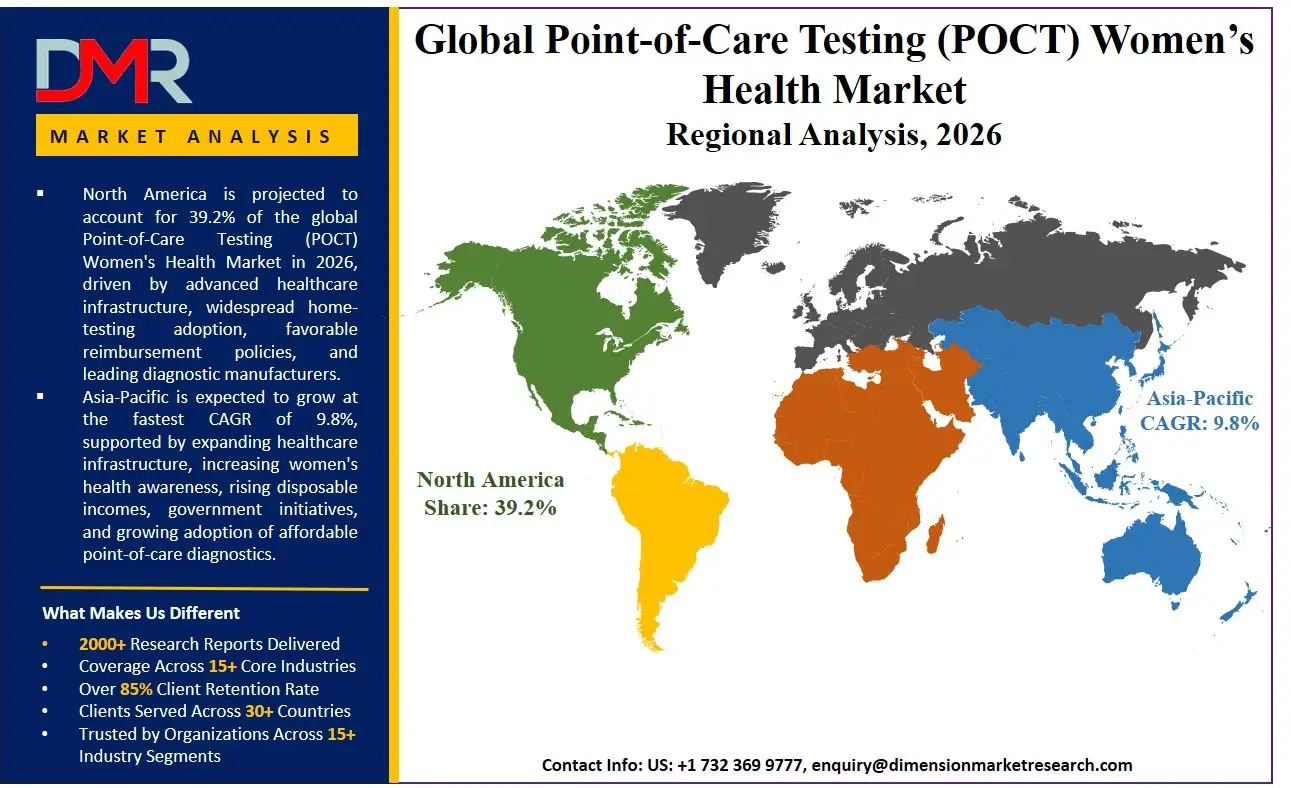

North America is poised to dominate the global POCT Women health market, holding a projected 39.2% of the market share by the end of 2026. The United States, which anchors the North American region, commands this leadership position due to a unique confluence of high disposable income, a powerful direct-to-consumer advertising culture, and an agile FDA regulatory framework that has been proactive in clearing OTC test kits for sensitive applications like STIs. The region features a mature ecosystem of retail chains like CVS and Walgreens that act as pseudo-clinical hubs, alongside a sophisticated telehealth infrastructure ready to manage the results of home-based tests. Furthermore, heavy venture capital investment into "Femtech" startups is accelerating innovation in multiplex panels and digital hormone tracking solutions, cementing a culture where proactive, self-managed diagnostics are a mainstream consumer expectation.

Fastest-Growing Regional Market

Asia-Pacific is expected to be the most rapidly expanding POCT Women health market, fueled by an explosive intersection of digital health adoption, huge underserved populations, and governmental efforts to modernize primary care. In this region, countries are leapfrogging legacy lab-based diagnostics directly to mobile-connected POCT solutions. The vast scale of China and India's internal markets, combined with rising health literacy among younger female populations, is creating a surge in demand for OTC pregnancy and ovulation kits available through dominant e-commerce ecosystems. Meanwhile, in more mature Asia-Pacific economies, the demand is pivoting to sophisticated hormone testing kits and self-sampling HPV solutions as they face aging populations and an increased policy focus on managing menopause and cervical cancer elimination through community health channels rather than expensive hospital infrastructure.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The competitive landscape of the global POCT Women health market is a dynamic battleground featuring large multinational diagnostics corporations, innovative Femtech startups, and consumer health giants. The key to sustained competitive advantage is shifting from simply selling hardware (test kits) to building integrated digital health ecosystems that offer connected readers, personalized AI-driven insights, and pathways to telehealth consultations. Large corporations are aggressively acquiring niche molecular POCT developers to add multiplex STI and vaginitis panels to their primary care portfolios. Simultaneously, traditional consumer product companies are applying their branding and retail distribution mastery to hormone and menopause testing, blurring the lines between a medical device and a lifestyle product. The competitive moat is increasingly defined by a seamless user experience, from saliva or swab collection to an actionable health dashboard on a smartphone.

Some of the prominent players in the Global Point-of-Care Testing (POCT) Women Health Market are:

- Abbott Laboratories

- F. Hoffmann-La Roche Ltd.

- Siemens Healthineers AG

- Danaher Corporation

- Becton, Dickinson and Company (BD)

- bioMérieux SA

- QuidelOrtho Corporation

- SEKISUI Diagnostics

- OraSure Technologies, Inc.

- Trinity Biotech plc

- EKF Diagnostics Holdings plc

- ACON Laboratories, Inc.

- Access Bio, Inc.

- Boditech Med Inc.

- LumiraDx Limited

- Hologic, Inc.

- Biosynex SA

- SD Biosensor, Inc.

- Nova Biomedical Corporation

- Cardinal Health, Inc.

- Other Key Players

Recent Developments

- June 2026: Roche Diagnostics continued expanding its point-of-care diagnostics portfolio by advancing decentralized molecular testing solutions following the integration of LumiraDx technologies. The company also strengthened its molecular diagnostics business through new platform innovations and strategic investments aimed at improving access to rapid infectious disease and Women health testing in outpatient and primary care settings.

- March 2026: Clearblue continued to expand its connected Women health ecosystem by enhancing its portfolio of digital fertility and reproductive health solutions. Across the FemTech sector, manufacturers increasingly integrated smartphone applications, hormone monitoring technologies, and AI-enabled analytics to provide more personalized reproductive and menopause health insights for consumers.

- October 2025: Investment and acquisition activity across the FemTech sector accelerated as pharmaceutical and diagnostics companies increased interest in home-based Women health diagnostics, microbiome research, and companion diagnostic platforms. The trend reflected growing demand for integrated diagnostic and therapeutic solutions delivered through digital health and home-care channels.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 20.6 Bn |

| Forecast Value (2035) |

USD 42.3 Bn |

| CAGR (2026–2035) |

8.3% |

| The US Market Size (2026) |

USD 6.8 Bn |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Product Type, By Technology, By Sample Type, By Mode of Prescription, By Test Setting, By Distribution Channel, By Application, and By End User |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Global POCT Women Health Market?

▾ The Global POCT Women Health market is poised to be valued at USD 20.6 billion in 2026 and is projected to reach USD 42.3 billion by 2035, driven by the universal shift toward decentralized, private, and immediate diagnostic solutions for sensitive health issues.

What is the CAGR of the Global POCT Women Health Market from 2026 to 2035?

▾ The market is expected to grow at a CAGR of 8.3% from 2026 to 2035, reflecting the rapid consumerization of diagnostics and the expansion of accessible testing menus beyond simple pregnancy detection to complex molecular panels.

What factors are driving the growth of the Global POCT Women Health Market?

▾ Key drivers include the regulatory deregulation of OTC self-testing for STIs, the destigmatization of sexual health screening, the crisis in maternity care accessibility, and the technological miniaturization enabling lab-grade molecular diagnostics at home.

Which region held the largest share of the POCT Women Health Market in 2026?

▾ North America, specifically the United States, held a 39.2% market share in 2026, driven by strong consumer health awareness, a mature OTC retail infrastructure, and a supportive regulatory climate for advanced home-use diagnostic devices.

Which region is expected to grow the fastest in the POCT Women Health Market?

▾ The Asia-Pacific region is expected to grow the fastest, fueled by mobile-first digital health economies, massive underserved female populations, and government-led primary care modernization that is leapfrogging directly to distributed POCT models.

What are the major trends in the Global POCT Women Health Market?

▾ Major trends include the rise of menopause-tech for longevity management, venipuncture-free microsampling technologies, the shift to multiplex panels for syndromic vaginal infection diagnosis, and the bundling of test kits with AI-driven telehealth consultations.

Who are the key players in the Global POCT Women Health Market?

▾ Key players include global diagnostic leaders like Abbott, Roche, and BD, as well as consumer health giants like Procter & Gamble, and specialized molecular POCT innovators like Cepheid and Hologic, competing at the intersection of medical diagnostics and consumer wellness.

How is the Global POCT Women Health Market segmented?

▾ The market is segmented by Product Type, Technology, Sample Type, Mode of Prescription, Test Setting, Distribution Channel, Application, and End User.