What Is Precipitated Calcium Carbonate?

Precipitated calcium carbonate (PCC) is a synthetically manufactured form of calcium carbonate (CaCO3, CAS 471-34-1) produced by reacting calcium hydroxide (Ca(OH)2) with carbon dioxide (CO2) under controlled conditions. Unlike ground calcium carbonate (GCC), which is mechanically milled from natural limestone, PCC is chemically precipitated, allowing manufacturers to control particle size, crystal morphology, and purity with precision. This makes PCC a preferred functional additive across paper manufacturing, plastics, pharmaceuticals, paints and coatings, and personal care products.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

PCC is primarily produced through the carbonation, lime soda, and Solvay processes, with carbonation accounting for about 70% of global production. In this widely used method, calcium hydroxide reacts with CO₂ under controlled conditions, enabling precise control over particle size, crystal structure, and product performance.

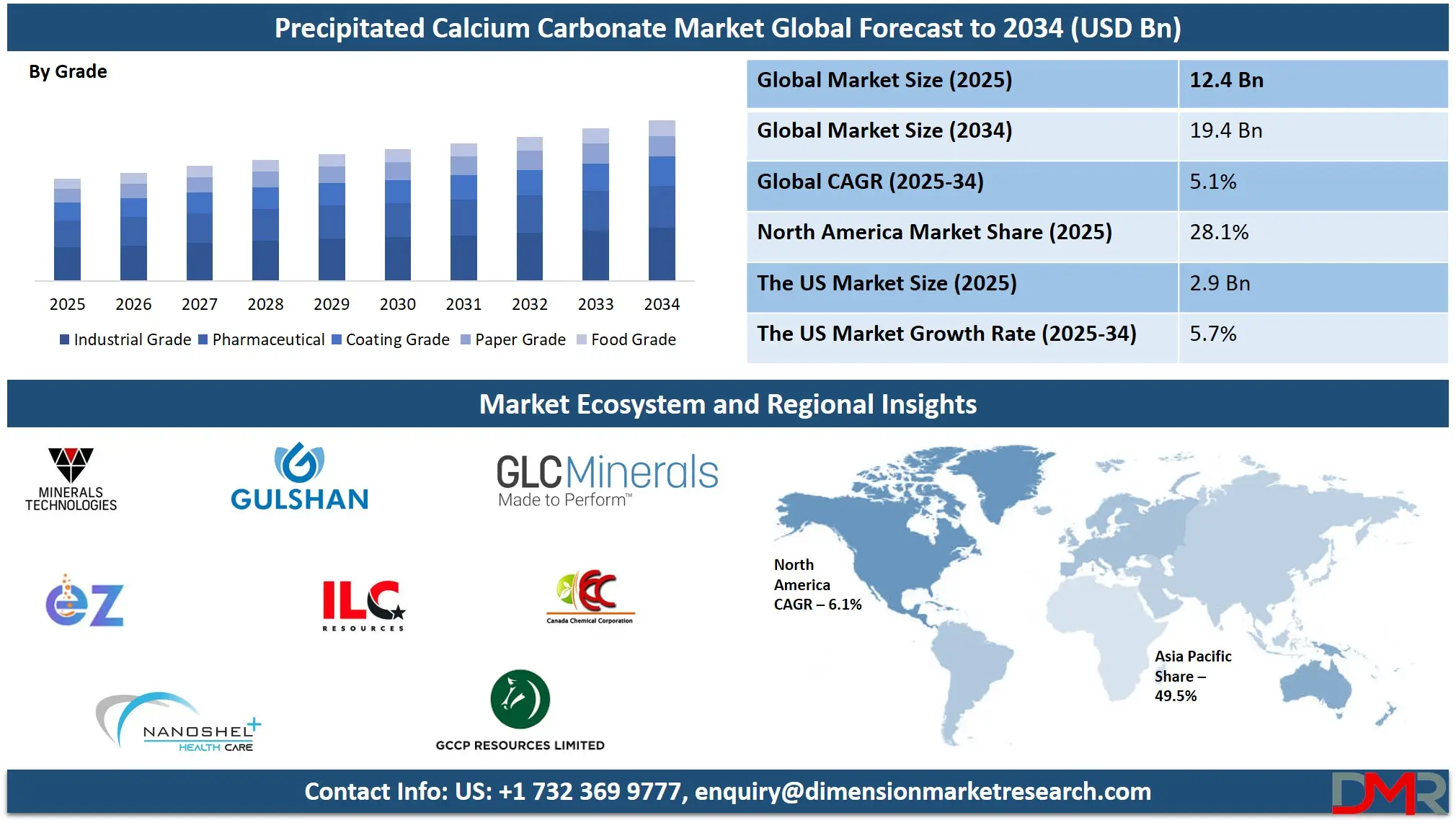

Precipitated Calcium Carbonate Market Size & Forecast (2025–2034)

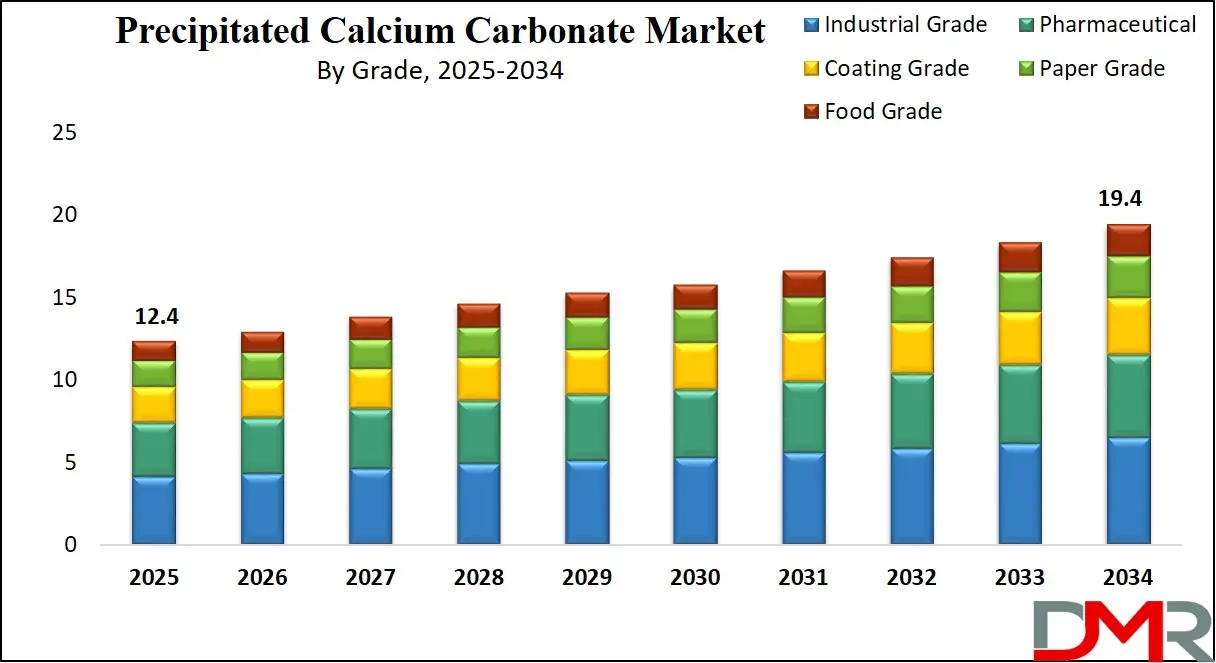

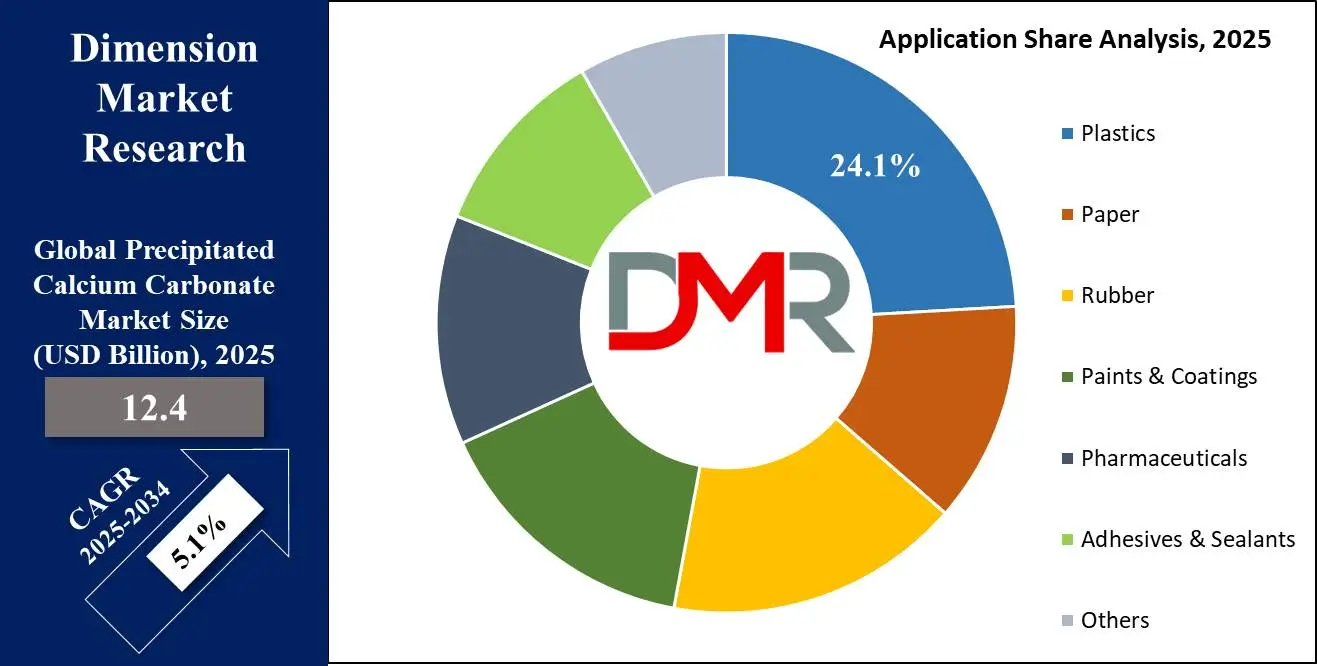

The global precipitated calcium carbonate market is valued at USD 12.4 billion in 2025 and is projected to reach USD 19.4 billion by 2034, registering a compound annual growth rate (CAGR) of 5.1% over the forecast period. Rising demand from the paper, plastics, pharmaceutical, and construction sectors continues to underpin market expansion, while advances in nano-PCC technology and sustainable production methods are opening new application areas.

Global Precipitated Calcium Carbonate Market — Key Figures (2025)

| Metric |

Value |

| Global Market Size (2025) |

USD 12.4 billion |

| Forecast Value (2034) |

USD 19.4 billion |

| CAGR (2025–2034) |

5.1% |

| Base Year |

2024 |

| Historical Data |

2019–2024 |

| US Market Size (2025) |

USD 2.9 billion |

| US Forecast (2034) |

USD 4.8 billion |

| US CAGR (2025–2034) |

5.7% |

| Dominant Region |

Asia-Pacific (49.5% share) |

| Leading Application (2025) |

Paper |

| Leading Grade (2025) |

Industrial Grade |

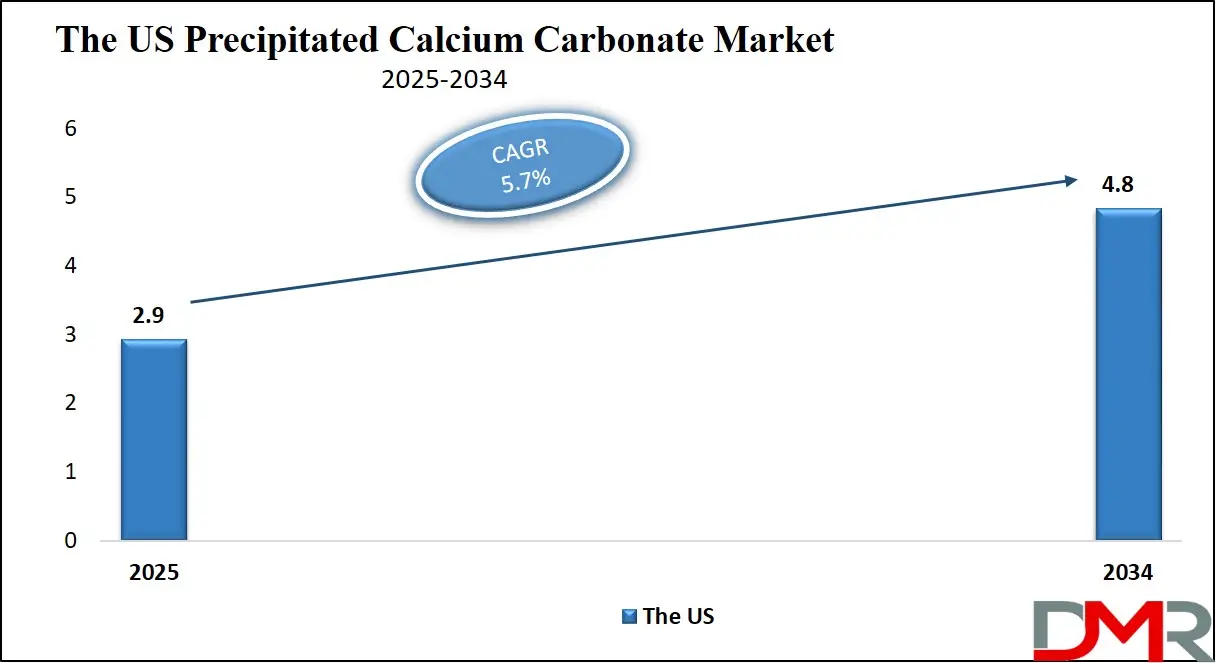

US Precipitated Calcium Carbonate Market

The US precipitated calcium carbonate market is projected at USD 2.9 billion in 2025, growing to USD 4.8 billion by 2034 at a CAGR of 5.7%. North America registers the highest regional CAGR within the global forecast, driven primarily by pharmaceutical sector expansion, an aging population requiring advanced drug delivery formats, and the packaging industry's continued shift toward high-performance paper-based substrates. The US also benefits from regulatory alignment with USP and FDA 21 CFR Part 184 standards, which create a consistent demand floor for pharmaceutical-grade PCC from domestic formulators.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Additional growth drivers in the US market include the expansion of the e-commerce packaging sector, the adoption of lightweight PCC-filled plastics in automotive components, and increasing investment in nanotechnology-enhanced PCC grades for specialty coatings and adhesives. The 2025 US tariff landscape has also introduced shifts in PCC supply chain dynamics, with domestic producers gaining a cost-competitiveness advantage over import-dependent buyers.

Market Dynamics: Key Market Drivers, Restraints, and Opportunities

Driver: Growing Demand in the Paper and Packaging Industry

PCC serves as a filler and coating pigment in paper production, improving brightness, opacity, and print quality while reducing wood fiber consumption. The e-commerce sector's rapid growth has accelerated demand for high-quality packaging paper, and sustainability mandates from major consumer goods companies are reinforcing the shift toward PCC-filled paper over heavier, less recyclable alternatives. Paper remains the largest single application segment by revenue, holding the highest market share in 2025.

Driver: Expanding Pharmaceutical and Personal Care Applications

Pharmaceutical-grade PCC meets USP, BP, and FDA 21 CFR Part 184.1191 (GRAS) standards, making it an approved excipient in tablet formulations, calcium supplement products, and antacid medications. Its biocompatibility, controlled particle distribution, and chemical inertness support uniform drug release profiles. In personal care, PCC functions as a mild abrasive in toothpaste, an opacifying agent in cosmetics, and a bulking agent in skincare formulations. Healthcare expenditure growth in emerging markets, particularly in China, India, and Brazil, continues to drive demand volume in this high-margin segment.

Restraint: Environmental Regulations and Carbon Emission Costs

PCC production involves limestone calcination and CO2 generation, placing manufacturers under increasing regulatory pressure as carbon taxation and emission control standards tighten in North America, Europe, and parts of Asia. Compliance investment requirements and the potential for bio-based substitute materials represent medium-term demand risks, particularly for commodity-grade industrial PCC.

Restraint: Raw Material Price Volatility

Limestone and CO2 are the primary raw material inputs for PCC manufacturing. Price fluctuations tied to energy costs, geopolitical supply disruptions, and transportation constraints create margin pressure across the supply chain. Producers are mitigating this through satellite plant models, where PCC is manufactured on-site at large paper mills, eliminating transportation costs and using the mill's own CO2 emissions as a feedstock.

Opportunity: Nano-PCC and Specialty Grade Development

Nano-Precipitated Calcium Carbonate (NPCC) represents a high-growth subsegment within the broader PCC market. With particle sizes below 100 nanometers, NPCC delivers enhanced surface area, superior dispersibility, and improved mechanical reinforcement in composite applications. Current commercial uses include high-performance adhesives, specialty rubber compounds, advanced pharmaceutical formulations, and nano-coatings. Manufacturers that invest in NPCC production capability are positioned to capture premium pricing across multiple end-use industries where standard PCC cannot meet performance benchmarks.

Opportunity: Sustainable PCC via CO2 Sequestration

Several manufacturers are investing in production processes that use captured industrial CO2 emissions, primarily from power generation and steel production, as the carbonation feedstock. This approach converts a regulatory liability into a low-carbon production advantage, aligning PCC supply with the ESG procurement criteria increasingly applied by buyers in North America and Europe. Carbon-neutral or low-carbon PCC certifications are expected to command pricing premiums in regulated markets from 2026 onward.

2025 US Tariff Impact on PCC Supply Chains

The 2025 US tariff adjustments have recalibrated competitive dynamics for PCC importers and domestic producers. Companies that have historically sourced commodity-grade PCC from China and other Asian markets face increased landed costs, shifting procurement decisions toward domestic suppliers and near-shoring strategies. This creates a structural tailwind for US-based PCC producers, particularly those with established pharmaceutical-grade and specialty-grade manufacturing infrastructure. Investment in domestic capacity expansion is anticipated to accelerate through 2026 and 2027 as supply chain resilience becomes a procurement priority for large-volume buyers.

Precipitated Calcium Carbonate Market Segmentation Analysis

By Grade: Industrial Grade Leads by Revenue Share

Industrial-grade PCC holds the largest revenue share in 2025, reflecting its broad applicability across paper, paints, plastics, rubber, and construction materials. The grade balances acceptable purity with cost-effective production, making it the default choice for high-volume manufacturing applications that do not require pharmaceutical or food-grade certifications. Pharmaceutical-grade PCC ranks second, supported by its role in tablet excipients, calcium supplements, and antacid formulations in regulated markets. Coating-grade and food-grade PCC are the fastest-growing specialty subsegments within the grade classification.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Application: Paper Sector Holds Highest Revenue Share

The paper industry generates the highest application-level revenue share for PCC in 2025. PCC improves brightness, smoothness, and ink receptivity in both printing and packaging papers. It displaces more expensive wood fiber in alkaline papermaking, reducing total production cost per ton. The plastics segment is the fastest-growing application, with PCC adopted as a reinforcing filler in automotive interior components, food packaging films, and consumer goods, where it improves impact resistance and reduces reliance on petrochemical-based fillers.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Production Process: Carbonation Process Dominates

The carbonation process accounts for approximately 70% of global PCC production volume. It offers the highest degree of crystal morphology control, enabling manufacturers to produce scalenohedral, rhombohedral, and aragonitic PCC grades to specification. The lime soda process and Solvay process serve smaller specialty segments, primarily in Europe, where process integration with chemical manufacturing facilities provides cost advantages.

Precipitated Calcium Carbonate Market Regional Analysis

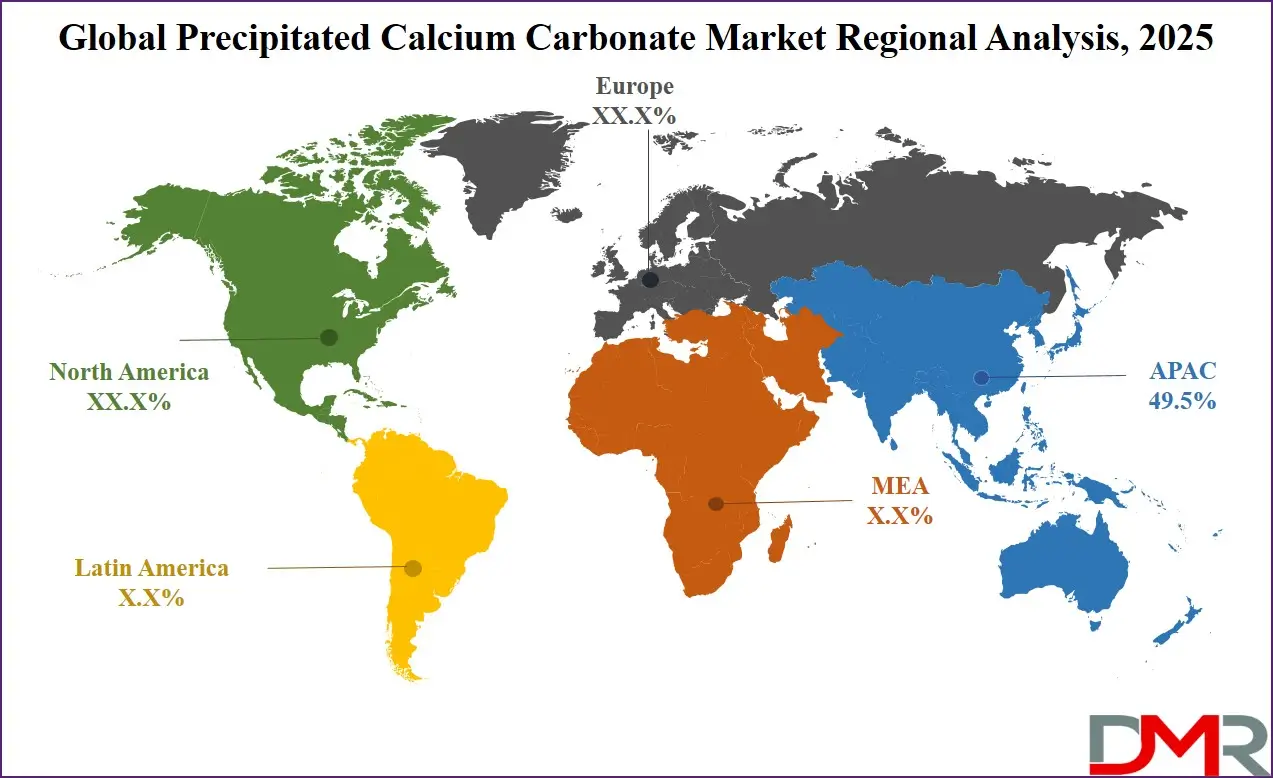

Asia-Pacific: Dominant Region with 49.5% Revenue Share

Asia-Pacific leads the global PCC market, holding approximately 49.5% of total revenue in 2025. China is the central driver, with large-scale paper, plastics, automotive, and construction manufacturing sectors creating consistent high-volume demand. India contributes significant growth from its expanding pharmaceutical production base, personal care sector, and paper industry capacity additions. Japan and South Korea maintain steady demand from specialty-grade PCC applications in electronics and high-performance coatings. The region's scale and diversity of industrial activity are expected to sustain its dominance through 2034.

North America: Fastest-Growing Region at 6.1% CAGR

North America registers the highest CAGR in the global forecast at 6.1%, driven by the US pharmaceutical sector's expansion and the automotive industry's adoption of lightweight, PCC-filled composite materials. The US market alone is valued at USD 2.9 billion in 2025. Regulatory advantages from FDA and USP certification alignment, combined with domestic capacity investments responding to 2025 tariff pressures, position the region for above-average growth through the forecast period. Canada contributes supplementary demand from its paper and pulp manufacturing base.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Europe: Regulatory-Driven Shift to Sustainable PCC

European demand is shaped by the REACH regulation, the EU Green Deal, and the European Paper Recycling Council's targets, which collectively favor sustainable PCC production methods and low-VOC coatings applications. Germany, France, and Italy represent the largest European markets, supported by pharmaceutical production, specialty chemicals, and premium coatings industries. Investment in carbon-neutral PCC production using captured CO2 is most advanced in the European market.

Competitive Landscape — Top Precipitated Calcium Carbonate Manufacturers

The global PCC market is characterized by a mix of large-scale integrated mineral producers, specialty chemical companies, and regional manufacturers serving domestic industries. Competition centers on particle size control capability, grade breadth, proximity to end-use manufacturing facilities, and investment in satellite and on-site production models that reduce customer transportation costs.

Minerals Technologies Inc. (MTI)

Minerals Technologies Inc. is a leading PCC producer known for its satellite plant strategy, in which dedicated PCC production units are installed directly within paper mill facilities. MTI's NewYield LO PCC technology, deployed in a partnership with a major global paper manufacturer in Brazil in July 2023, exemplifies this model. In a further expansion move, MTI partnered with India-based Satia Industries to establish a 42,000 metric ton per year satellite PCC plant within Satia's paper mill, strengthening MTI's Asia-Pacific footprint.

Imerys

Imerys is a global specialty minerals group with significant PCC production capacity across Europe, North America, and Asia. The company produces a broad range of functional PCC grades for paper, paints and coatings, polymers, and pharmaceutical applications. Imerys's scale and technical breadth make it one of the most frequently cited PCC suppliers in procurement benchmarking across multiple end-use industries.

Omya AG

Omya AG is a Swiss-based global producer of calcium carbonate and other industrial minerals, with operations in over 50 countries. Omya India's USD 25 million calcium carbonate plant investment in Gujarat, announced in April 2023, reflects the company's strategic commitment to serving the growing South Asian market. Omya competes across both the PCC and GCC markets, offering customers integrated sourcing flexibility.

Other Notable Players

Additional participants in the global PCC competitive landscape include Gulshan Polyols Ltd. and GCCP Resources Ltd. in South and Southeast Asia, Fujian Sanmu Nano Calcium Carbonate Co. Ltd. and Guangdong Qiangda New Materials Technology Co. in China, and GLC Minerals and ILC Resources serving North American industrial buyers. Cimbar Resources Inc. expanded its North American calcium carbonate presence through its August 2022 acquisition of Imerys Carbonate Inc.'s Arizona production assets.

Recent Developments

- Lime Chemicals CFO resigns (March 2026): Lime Chemicals Limited, an Indian manufacturer of precipitated and coated calcium carbonate, announced the resignation of CFO Amol Vijay Patil, effective March 2026.

- Saudi Carbonate wins Industrial Excellence Award (2025): Saudi Carbonate Company received the 2025 Industrial Excellence Award under the patronage of the Royal Commission for Jubail and Yanbu (RCY), recognizing its quality and industry leadership.

- Saudi Carbonate’s MEA expansion (2025): Saudi Carbonate Company announced the largest PCC production expansion in the Middle East and Africa to serve plastics, paints, pharmaceuticals, and paper industries, aligning with Saudi Arabia’s manufacturing hub vision.

- NSF-funded bio‑based PCC project (2025): A $304,901 NSF STTR Phase I project explores bacteria‑based production of high‑quality PCC, offering a cost‑effective, energy‑efficient alternative to traditional methods for US domestic supply.

- Domtar & Omya open on‑site PCC plant (2024): Domtar’s Nekoosa mill and Omya launched a 27,500‑dry‑ton‑per‑year PCC facility. It cuts transportation by 1.18 million miles annually and reduces carbon footprint by 15,000 short tons by reusing mill CO₂ emissions.

Frequently Asked Questions

What is the size of the global precipitated calcium carbonate market in 2025?

▾ The global precipitated calcium carbonate market is valued at USD 12.4 billion in 2025 and is projected to reach USD 19.4 billion by 2034, expanding at a CAGR of 5.1% over the forecast period.

What is the US precipitated calcium carbonate market size?

▾ The US precipitated calcium carbonate market is projected at USD 2.9 billion in 2025. It is expected to grow to USD 4.8 billion by 2034, registering a CAGR of 5.7%, driven by expanding pharmaceutical, paper, plastics, and automotive applications.

Which region dominates the precipitated calcium carbonate market?

▾ Asia-Pacific dominates the global PCC market with approximately 49.5% revenue share in 2025, led by China, India, and Japan. Strong demand from paper manufacturing, plastics, rubber, and the automotive sector, particularly within China's large industrial base, drives the region's leadership.

Who are the major precipitated calcium carbonate manufacturers?

▾ Key global PCC manufacturers include Minerals Technologies Inc. (MTI), Imerys, Omya AG, J.M. Huber Corporation, Gulshan Polyols Ltd., GCCP Resources Ltd., Fujian Sanmu Nano Calcium Carbonate Co. Ltd., and GLC Minerals. Minerals Technologies is recognized for its NewYield LO PCC satellite plant technology deployed at paper mills globally.

What drives growth in the pharmaceutical-grade PCC segment?

▾ Pharmaceutical-grade PCC is used as an excipient in tablet and capsule formulations, as an active ingredient in antacid medications, and as a calcium supplement. Growth is driven by aging global populations, rising healthcare expenditure in emerging markets, and strict USP and FDA 21 CFR Part 184 compliance requirements that favor high-purity, consistently-sized PCC over lower-grade alternatives.