What is the Global Printed Electronics Market Size?

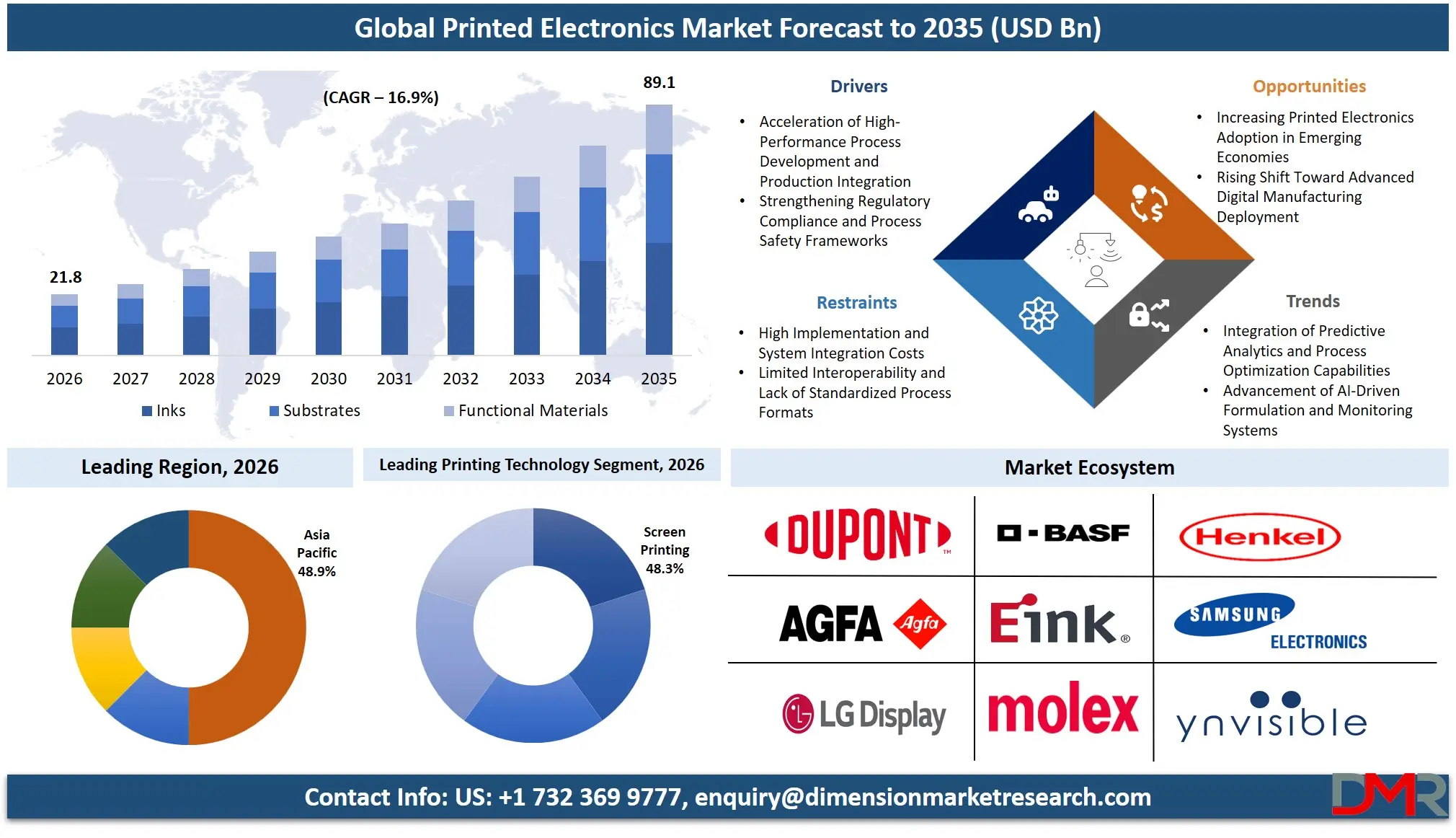

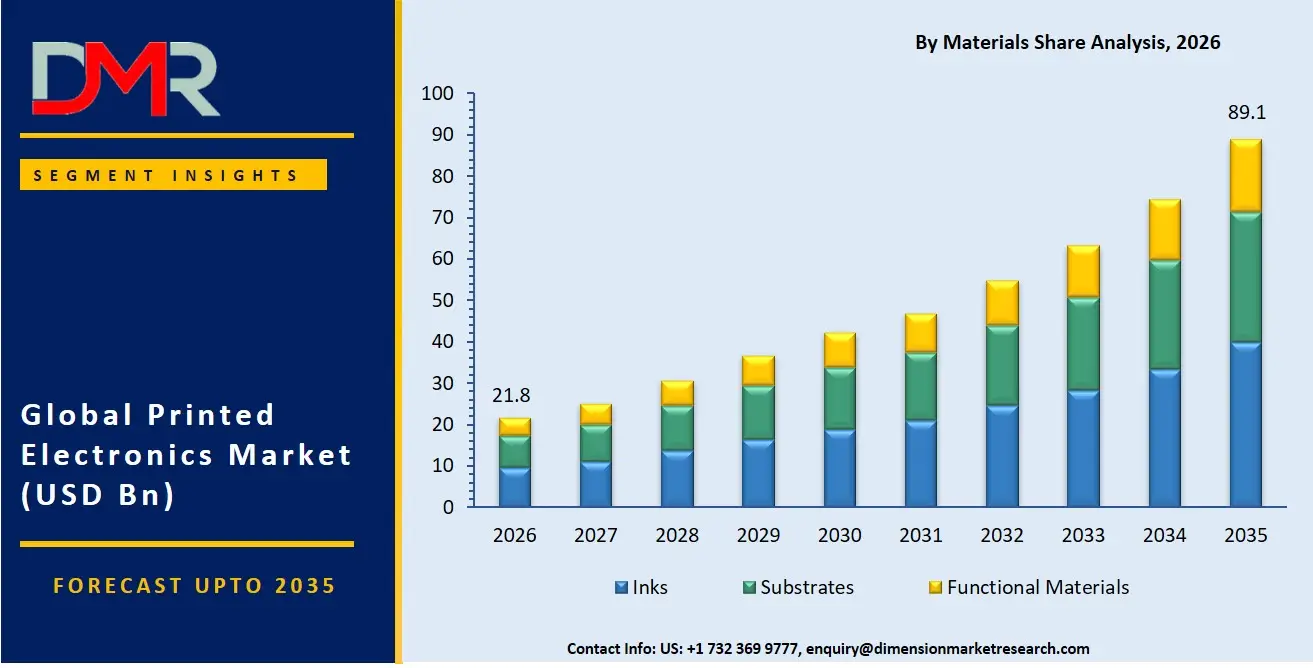

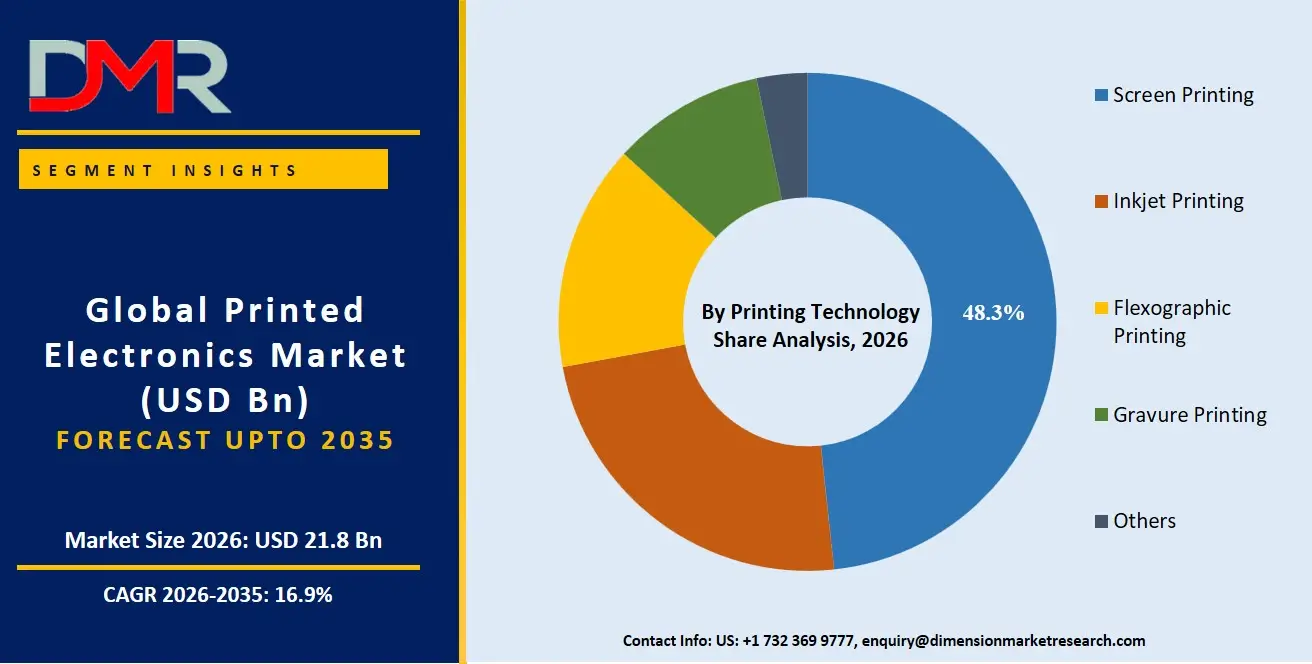

The Global Printed Electronics Market size is estimated at USD 21.8 billion in 2026 and is projected to reach USD 89.1 billion by 2035, exhibiting a CAGR of 16.9% during the forecast period, driven by the rising use of low-cost, flexible electronic component production, decentralized manufacturing patterns in modular and roll-to-roll architectures, and connected digital governance and compliance management systems for smart devices.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The global printed electronics market is expanding because of increasing use of high-fidelity conductive ink compatibility testing and impurity profiling in detecting and analyzing anomalous printing pattern activity, increasing regulatory mandates, which reduce the chance of electrical short circuits during flexible electronics operations and speed up compliance audits for new production lines, and more funding in automating privacy-preserving formulation logging for functional inks.

Some other reasons for expansion in this market include new technologies in runtime process stability management, stencil fouling prediction through behavior analytics, automated solvent lifecycle handling for inks, high-volume print process data platforms, and improved cross-supplier formulation-sharing rules. The digital shift in specialty printed electronics production and batch processing has helped speed up product development and make sensitive process transaction management easier. This includes nano silver ink analytics research. In addition, government plans focusing on preventing industrial waste and the secure electronic materials economy have ensured steady research in printed electronics systems.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

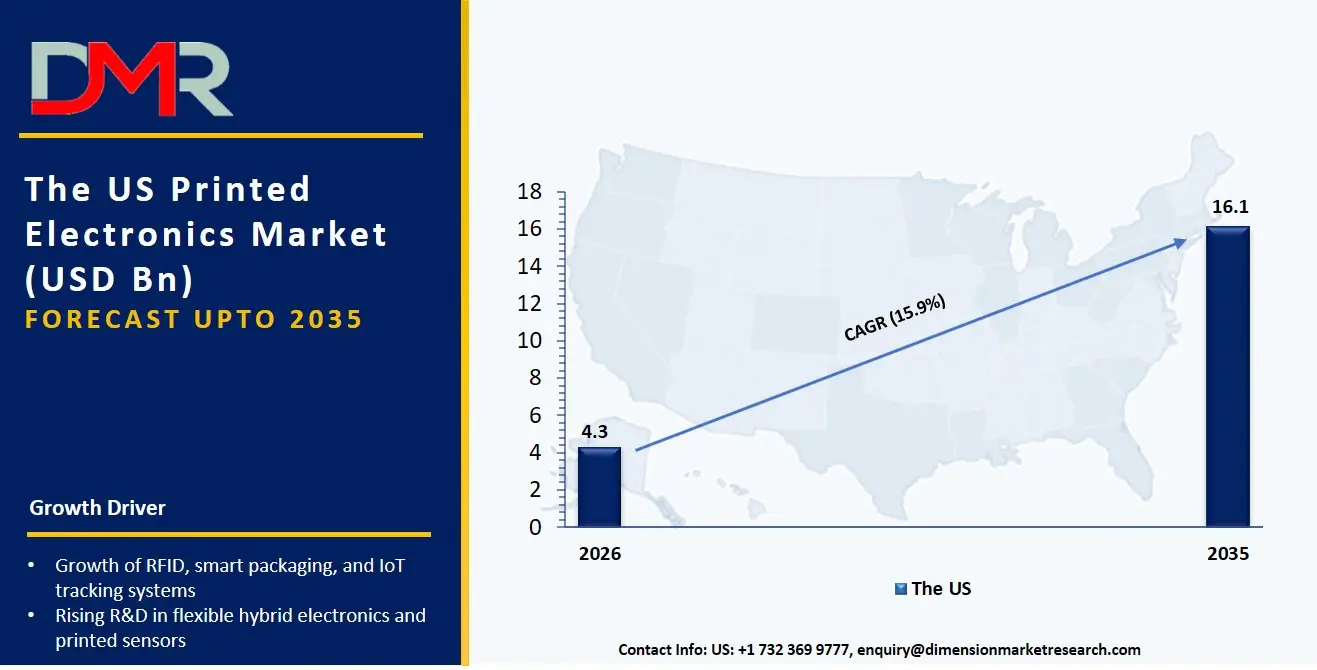

The US Printed Electronics Market

The US Printed Electronics Market is estimated to grow to USD 4.3 billion in 2026 with a compound annual growth rate of 15.9% during the forecast period.

The US market is shaped by major federal and state-level programs promoting flexible and stretchable electronic architectures, secure digital adoption supported by DOE and NIST, and DOD-led electronic modernization initiatives. These programs encourage the use of high-purity conductive inks, real-time impurity-in-solution protection for printed layers, and predictive compliance software for ink blending. Automated print process safety platforms are being rapidly adopted, and the US continues to invest in better data sharing between R&D labs, encrypted formulation audit systems, and reliable electrical short-circuit detection tools for printed electronics platforms. Service providers are also influenced by laws like IPC standards, FCC regulations, and national digital electronics strategies to offer services that ensure process safety, rule-following, and smooth integration across hybrid and modular production environments.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Europe Printed Electronics Market

The European Printed Electronics Market is estimated to be valued at USD 4.8 billion in 2026, witnessing growth at a CAGR of 15.2%, during the forecast period.

Europe's printed electronics market is well-established, shaped by EU-wide policies such as the RoHS Directive, REACH, and national policies to support sustainable digital markets (e.g., Germany's organic photovoltaic production digital plans and France's national printed battery recycling strategies). Countries are also making process safety management more flexible to align plant operator and customer demands and enable the sharing of anonymized conductive ink data across borders. The market grows due to new tools like software for real-time ionic conductivity validation and risk scoring systems for process thermal stability of printed layers. Use is made easier by teamwork between public and private groups and shared digital safety rules. Manufacturers have access to technologies such as sulfide-based solid-state battery printing fine-tuning, ink-substrate interaction modeling, and secure process audit logging, and Europe is at the forefront of the digitisation of safe and efficient printed electronics operations.

Japan Printed Electronics Market

The Japan Printed Electronics Market is projected to be valued at USD 2.1 billion in 2026, progressing at a CAGR of 16.8%, during the period spanning from 2026 to 2035.

Japan's printed electronics market is well developed, with high-purity nano silver ink data platforms, connected secure printed layer blending management systems, and a wide array of printed layer aging simulation software tools. National focus on automation, efficiency, and process integrity is delivered via conductivity models and smart print process protection. Growth opportunities are helped by government measures under the Green Growth Strategy by Japan's Ministry of Economy, Trade and Industry (METI), and continued investment in electronics cloud modernization. AI-driven print process research, multi-party analytics for application-specific process data sharing, and virtualized print safe environments all need effective printed electronics software to keep pace with high-voltage flexible electronic processing. Higher costs for validating new printed electronics systems and connecting them with older infrastructure are significant, but there are opportunities for the export of Japanese printed electronics technologies to the Asian and Pacific markets.

Key Takeaways

- Market Size & Forecast: The Global Printed Electronics Market is estimated to be valued at USD 21.8 billion in 2026 and is expected to grow to USD 89.1 billion by 2035.

- Growth Rate & Outlook: The market is expected to witness growth at a compound annual growth rate of 16.9% in the forecast period.

- Primary Growth Drivers: The availability of new printed processing technologies that use real-time degradation detection, the need to speed up compliance results and improve success rates of process data sharing, and more government investment in a national secure electronic material infrastructure are key growth drivers.

- Key Market Trends: The real-time profiling of print thermal stability risks, solvent handling for conductive inks, and the shift to AI-driven formulation platforms and automated digital asset inventory management are key market trends.

- By Materials: The Inks segment is expected to take the largest revenue share in the global printed electronics market in 2026.

- By Printing Technology: Screen Printing is expected to take the largest revenue share in 2026 in the printed electronics market.

- By Application: The Sensors segment is estimated to take the lead in 2026 with the largest share in the printed electronics market.

- Regional Leadership: Asia Pacific is estimated to take the lead in 2026 with 48.9% share in the printed electronics market.

What are Printed Electronics?

Printed Electronics refers to a combination of additive manufacturing and real-time monitoring technologies that provide electronics manufacturers, plant operators, and compliance entities with enhanced capabilities beyond traditional PCB fabrication, including helping to protect conductive formulations during production, preventing electrical shorts via substrate engineering, and enabling secure multi-party process analytics. They include printing simulation & modeling software, asset performance management platforms, print process optimization tools, and visualization systems. These platforms use modern systems such as real-time viscosity validation, digital asset inventory management software, and remote process advisory to manage, verify, and track sensitive print process events and results. To improve electronic safety outcomes, manage process variability and application-specific programs, and expand protection into customized digital coverage to support individual production line designs and promote the development of safe electronic products.

Use Cases

- Process Stability and Manufacturing Control Applications: Printed electronics platforms can provide process-stability benefits through software and control systems to reduce print defects and support faster, reliable production cycles compared to manual process handling. These systems improve monitoring of ink conductivity variations, print alignment, and electrical failure risks during manufacturing.

- Long-Term Printed Electronic Material Performance Monitoring: Long-term data on ongoing performance issues, including conductive ink intermittency, raw material price fluctuations for silver or copper, and printed layer degradation, are studied to better understand production performance and to help plan long-term reliability and lifecycle management of printed electronic components.

- Production Optimization and Capacity Management: Print process efficiency is managed through digital simulation platforms and smart software in modular manufacturing settings to support production balance for high-volume printed electronics workloads. These systems help improve throughput, reduce errors, and optimize roll-to-roll printing operations.

- Government & Regulated Industry Applications: Faster printed electronics development supports data-driven innovation and development of targeted electronic programs. Government initiatives, through monitoring of electronic material standards and compliance frameworks, help advance safety regulations and support adoption of standardized printed electronics manufacturing practices.

How AI Is Transforming the Global Printed Electronics Market?

Artificial intelligence (AI) is being used progressively more often in printed electronics platforms to improve print process demand forecasting, find safety quality trends in conductive ink printing patterns, and automatically spot unusual degradation patterns in electronic cycling data. It also allows faster print thermal verification because it can handle digital formulation submissions on a large scale. Encrypted process audit logs are easier to study and help registries find integration issues, reduce mistakes, and improve the overall accuracy of print certification. This has resulted in operations being cost-effective, quicker, and more efficient than the old manual review method.

AI is also strengthening research and development by improving print process risk assessment and enabling more accurate capacity planning for ink blending. It helps electronics manufacturers predict how many safe print batches will be needed, find possible conductivity delays, and monitor the performance of print process safety networks more effectively. In addition, automation of routine print compliance checks and performance tracking is reducing operational workload, lowering administrative costs, and improving overall efficiency. This is leading to better financial results and more stable operations across the printed electronics production chain.

Market Dynamics

Key Drivers of the Global Printed Electronics Market

Acceleration of High-Performance Process Development and Production Integration

The market is growing with the rise of advanced digital formulations for printed electronics lines, better management of sensitive conductive processes, and a closer connection between print process performance monitoring and production integration. Printed electronics platforms provide real-time data that allows monitoring of ink conductivity, helping to spot degradation early, and checking print process performance much faster. This has improved operational efficiency and reduced human errors and production costs. At the same time, demand for more automated research and development is being supported by increased activity in predictive analytics for process risk assessment, as materials science further digitizes formulation and material processing tasks.

Strengthening Regulatory Compliance and Process Safety Frameworks

There is increasing emphasis on electronic safety, material purity, and regulatory compliance within the printed electronics system. Rules and frameworks such as EU RoHS, REACH, IPC standards, and electronic material regulations in key markets are encouraging better process handling practices and more structured safety systems. These advances are supporting the need for systems that can offer steady monitoring of sensitive conductive materials and standardized reporting. At the same time, active work to improve the sharing of process performance data and reduce verification issues is strengthening the need for more effective compliance management across both government and private market participants.

Restraints in the Global Printed Electronics Market

High Implementation and System Integration Costs

The rollout of printed electronics systems remains costly, requiring significant investment in printing simulation tools, conductivity validation technologies, system integration, testing, and alignment with existing electronic production workflows. In addition, compliance with environmental regulations such as RoHS and other regional laws adds to setup complexity. These factors increase upfront costs and can limit adoption, especially among smaller electronics manufacturers and new entrants.

Limited Interoperability and Lack of Standardized Process Formats

There is still fragmentation in the market in terms of digital ink formulation formats and process handling procedures. Although some areas have put in place organized production management systems, many production lines continue to work with both legacy process control and modern automated printing systems. Lack of standardized process and thermal stability protocols limits the ability to share performance data between manufacturers and suppliers and results in inefficiencies in production, deployment, and system integration.

Growth Opportunities in the Global Printed Electronics Market

Increasing Printed Electronics Adoption in Emerging Economies

Newly developing economies such as Brazil, Indonesia, Nigeria, the UAE, and Vietnam are slowly building their electronics manufacturing and printed electronics ecosystems. These regions have long-term growth possibilities, with increasing adoption of flexible electronics and growing awareness of material safety standards, along with gradual modernization of production infrastructure. These markets have limited legacy systems and can adopt new, technology-driven printed electronics platforms for scalable future growth.

Rising Shift Toward Advanced Digital Manufacturing Deployment

The move toward safer electronic systems, decentralized production models, and real-time process performance monitoring is creating demand for advanced printed electronics systems. These systems allow centralized process data access, better coordination between manufacturers and suppliers, and faster production tracking and optimization. Advanced digital manufacturing setups are increasingly becoming a trend among printed electronics providers as operational efficiency becomes a key competitive factor.

Global Printed Electronics Market Trends

Integration of Predictive Analytics and Process Optimization Capabilities

Printed electronics platforms are gradually adding data-driven tools to identify print degradation trends and improve accuracy in production optimization. These systems allow manufacturers and plant operators to better analyze conductive ink behavior, simplify process management, and improve overall production performance. This shift is making the industry more proactive and data-driven in process optimization rather than reactive.

Advancement of AI-Driven Formulation and Monitoring Systems

The use of AI-based formulation systems is increasingly becoming part of modern electronics development processes. These systems enable real-time print stability monitoring, improved process control, and better coordination among production stakeholders. Advanced printed electronics platforms are improving efficiency and scalability by reducing dependence on manual formulation processes and enabling faster industrial deployment.

Research Scope and Analysis

The global printed electronics market is witnessing strong growth driven by rising adoption of flexible electronics, batch process optimization, and increasing demand for high-safety and high-efficiency electronic production. The market is segmented based on materials, printing technology, applications, and end-use industry.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Materials Analysis

The Inks segment is likely to continue dominating the market in 2026, accounting for approximately 55.2% of the global printed electronics market share. This is due to its key role in enabling high-conductivity printing, a wide operating parameter range, and long-term print stability, and its usefulness in various electronic settings where operational efficiency is needed. Within Inks, the Conductive Inks sub-segment holds the largest share, driven by high deployment volumes for silver, copper, and carbon-based inks, automated demand for stable conductivity, and compliance requirements. The Substrates segment is driven by its key role in enabling successful printing, with Flexible Substrates leading, followed by Rigid and Biodegradable Substrates. Functional Materials are the fastest-growing, including dielectrics, semiconductors, and encapsulation materials.

By Printing Technology Analysis

The Screen Printing segment is likely to continue holding the lead in 2026, accounting for approximately 48.3% of the global printed electronics market share, driven by strong demand for high-throughput, cost-effective, and thick-film patterning, as well as proven reliability for high-volume production of displays, RFID antennas, and sensors. This segment reflects the continued shift toward scalable and robust printed electronic manufacturing. The Inkjet Printing segment is the second-largest, supported by its material efficiency, digital flexibility, and suitability for R&D and low-to-medium volume production. Gravure and Flexographic Printing remain mature segments for high-speed roll-to-roll manufacturing, while Others (including aerosol jet and transfer printing) represent emerging technologies.

By Application Analysis

The Sensors segment is expected to dominate with around 28.4% market share in 2026, driven by its irreplaceable role in enabling flexible, wearable, and IoT-connected sensing solutions, including temperature, pressure, humidity, and biometric sensors. Printed sensors support customized electronic plans because they can offer multiple levels of sensitivity, form factors, and yearly stability plans, delivering fast results while keeping sensitive data within secure registry systems. The Displays segment is the second-largest, driven by demand for OLEDs, e-paper, and flexible backplanes. RFID is the fastest-growing within Applications, witnessing strong growth with increasing needs for smart packaging, inventory tracking, and contactless authentication. Photovoltaics, Lighting, and Batteries represent specialized segments with dedicated printed electronics requirements for energy efficiency and lightweight form factors.

By End-Use Industry Analysis

The Consumer Electronics segment is the largest end-use industry in 2026, accounting for approximately 32.6% share, driven by the need for wearable devices, foldable displays, smart home products, and flexible batteries. This segment reflects the continued shift toward lightweight, durable, and form-factor-free electronic devices. The Automotive segment is the second-largest and fastest-growing, supported by demand for in-mold electronics, printed heaters, interior lighting, and battery monitoring sensors. Healthcare represents a strong, specialized segment with applications in biosensors, drug delivery patches, and wearable monitors. Packaging/Retail is driven by smart labels and interactive packaging, while Aerospace & Defense and Industrial represent high-reliability segments with dedicated requirements for harsh-environment printed electronics.

The Global Printed Electronics Market Report is segmented based on the following:

By Materials

- Inks

- Substrates

- Functional Materials

By Printing Technology

- Inkjet Printing

- Screen Printing

- Gravure Printing

- Flexographic Printing

- Others

By Applications

- Displays

- RFID

- Sensors

- Photovoltaics

- Lighting

- Batteries

By End-Use Industry

- Automotive

- Consumer Electronics

- Healthcare

- Packaging/Retail

- Aerospace & Defense

- Industrial

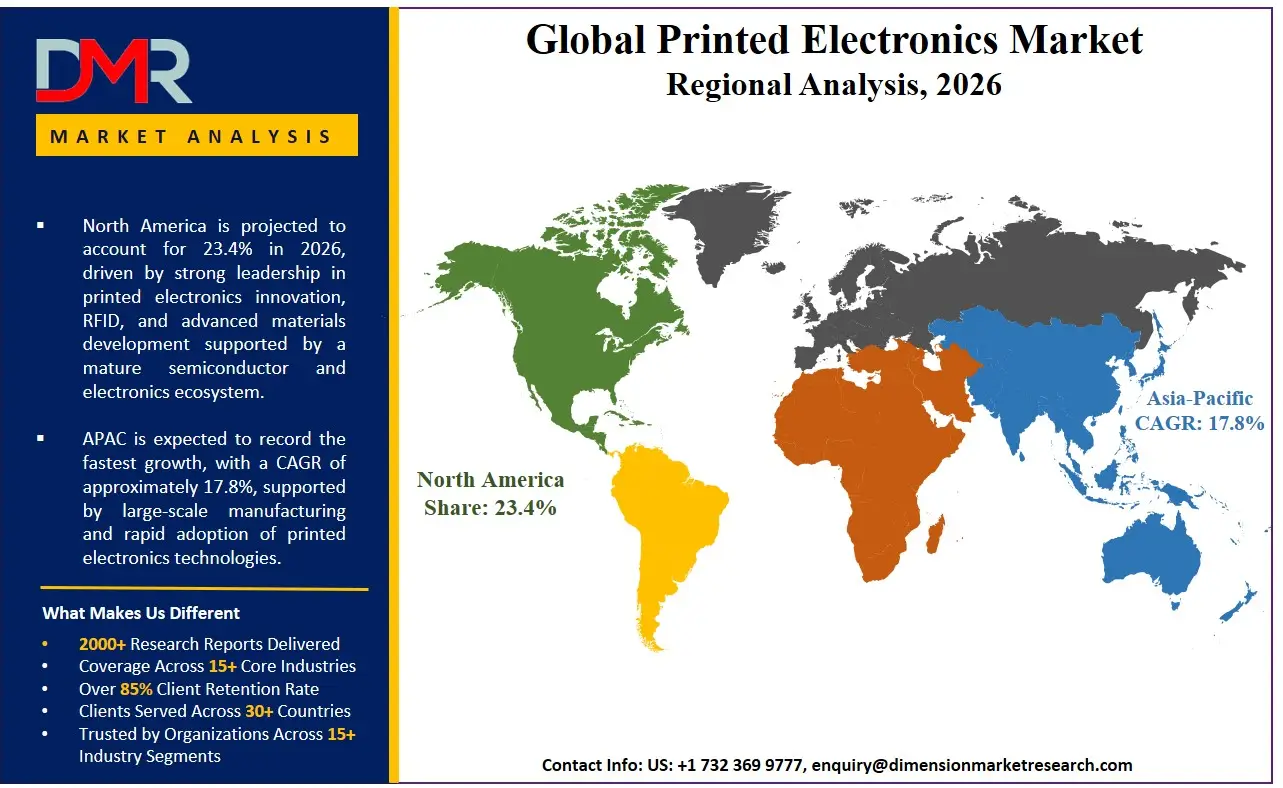

Regional Analysis

Largest Region in the Printed Electronics Market

It is projected that the Asia Pacific will take the lead in the global printed electronics market, covering a market share of about 48.9% in the year 2026. The region's dominance is driven by the presence of major electronics manufacturers and printed electronics material suppliers in China, Japan, South Korea, and Taiwan, strong government support for domestic flexible electronics production, and early adoption of high-volume screen printing and roll-to-roll manufacturing technologies across consumer electronics and automotive sectors. Asia Pacific benefits from significant investment in new printed electronics fabrication facilities, the highest concentration of greenfield production lines in China and Southeast Asia, and strong government backing through initiatives like China's Made in China 2025, South Korea's Digital New Deal, and Japan's Green Growth Strategy. The region is also home to leading display and battery manufacturers, enabling rapid deployment of printed electronics for OLEDs, e-paper, and solid-state batteries. Additionally, ongoing investments in workforce training for high-speed screen printing and automated production lines further strengthen Asia Pacific's leading position.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Fastest-Growing Region in the Printed Electronics Market

Asia Pacific is also the fastest-growing region, supported by aggressive domestic electronics manufacturing expansion in China, India, and Vietnam, substantial government funding for smart factory and Industry 4.0 initiatives, and increasing investments in greenfield flexible electronics complexes that integrate printed electronics from the initial design phase. The region is witnessing rapid growth in modular production line construction, driving demand for screen printing and process optimization software. Asia Pacific is also at the forefront of AI-driven printed electronics deployment in high-growth sectors like foldable displays and IoT sensors. The region benefits from lower labor costs, driving faster ROI on automation, along with rising corporate commitments to operational excellence and safety compliance. Moreover, increasing environmental regulations and the need to reduce electronic waste in rapidly industrializing economies are expected to keep Asia Pacific's growth momentum as the highest CAGR region during the forecast period.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The printed electronics market is highly competitive, with continuous innovation and strategic partnerships shaping the competitive environment. To gain an advantage, companies and providers are focused on developing advanced printed electronics solutions (such as process optimization systems, automated conductivity monitoring systems, and process management tools), smart conductive ink performance analysis, and digital monitoring of print quality and degradation. There are high barriers to entry due to the significant investment required for materials science capabilities, manufacturing infrastructure, regulatory compliance, and the need for mature process control systems.

Strategic approaches to increase market presence include partnerships with electronics research institutes and technology providers, collaborations between materials suppliers and device manufacturers, and long-term supply and support agreements with industrial and enterprise customers. Additionally, research and development in formulation optimization techniques and advanced simulation-based process design are important for staying competitive and meeting the evolving requirements of the printed electronics industry.

Some of the prominent players in the Global Printed Electronics Market are:

- DuPont de Nemours, Inc.

- BASF SE

- Henkel AG & Co. KGaA

- Agfa-Gevaert N.V.

- E Ink Holdings Inc.

- Samsung Electronics Co., Ltd.

- LG Display Co., Ltd.

- Molex LLC

- Jabil Inc.

- Nissha Co., Ltd.

- NovaCentrix LLC

- Optomec, Inc.

- Canatu Oy

- Elephantech Inc.

- Ynvisible Interactive Inc.

- PragmatIC Semiconductor Ltd.

- Avery Dennison Corporation

- KURZ (LEONHARD KURZ Stiftung & Co. KG)

- Brewer Science, Inc.

- Palo Alto Research Center Incorporated (PARC)

- Other Key Players

Recent Developments

- March 2026: Avery Dennison Corporation announced the launch of its sterilization-compatible RFID inlays portfolio designed for healthcare applications, enabling full tracking of medical devices and surgical instruments through sterilization cycles without loss of RFID performance, strengthening its position in smart labeling and healthcare-grade printed electronics solutions.

- March 2026: Samsung Electronics Co., Ltd. introduced its 13-inch color e-paper display for digital signage applications, offering ultra-low power consumption and static image retention, advancing display-based printed electronics solutions for retail, enterprise communication, and sustainable digital information systems.

- June 2025: DuPont de Nemours, Inc. highlighted its advanced electronics materials portfolio at JPCA Show 2025, showcasing conductive inks, electroless copper systems, and flex-circuit material solutions designed for printed and flexible electronics applications in AI, 5G, and high-performance computing ecosystems, reinforcing its role in next-generation electronic interconnect and printed circuit technologies.

- March 2025: Pragmatic Semiconductor Limited launched its FlexIC Platform Gen 3, a next-generation flexible integrated circuit design platform delivering improved power efficiency and reduced chip area, advancing ultra-thin flexible printed semiconductor applications for wearable electronics and edge devices.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 21.8 Bn |

| Forecast Value (2035) |

USD 89.1 Bn |

| CAGR (2026–2035) |

16.9% |

| The US Market Size (2026) |

USD 4.3 Bn |

| Historical Period |

2021 – 2025 |

| Forecast Period |

2027 – 2035 |

| Base Year |

2025 |

| Estimated Year |

2026 |

| Segments Covered |

By Materials, By Printing Technology, By Applications, By End-Use Industry |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Global Printed Electronics Market?

▾ The Global Printed Electronics Market is estimated to be valued at USD 21.8 billion in 2026 and is expected to reach USD 89.1 billion by the end of 2035.

What is the CAGR of the Global Printed Electronics Market from 2026 to 2035?

▾ The market is growing at a CAGR of 16.9% over the forecasted period.

What factors are driving the growth of the Global Printed Electronics Market?

▾ The market is driven by advances in real-time print degradation detection and automated safety enforcement, regulatory pressure to speed up electronic compliance results and reduce short-circuit mistakes, and increased government investment in a national safe electronic material infrastructure.

What are the major trends in the Global Printed Electronics Market?

▾ The key market trends include the adoption of real-time print thermal stability tracking and conductive ink solvent analysis, along with a growing shift toward AI-driven formulation platforms and data-enabled digital asset inventory management systems.

Which region held the largest share of the Global Printed Electronics Market in 2026?

▾ Asia Pacific is expected to account for the largest market share in 2026, with a share of about 48.9%.

Which region is expected to grow the fastest in the Global Printed Electronics Market?

▾ Asia Pacific is the fastest-growing region in the market during the forecast period.

Who are the key players in the Global Printed Electronics Market?

▾ Some of the major key players in the Global Printed Electronics Market are BASF SE, Henkel AG & Co. KGaA, Molex LLC, Ynvisible Interactive Inc., Avery Dennison Corporation, E Ink Holdings Inc., and many others.

How is the Global Printed Electronics Market segmented?

▾ The market is segmented by materials, printing technology, applications, and end-use industry.