Market Snapshot

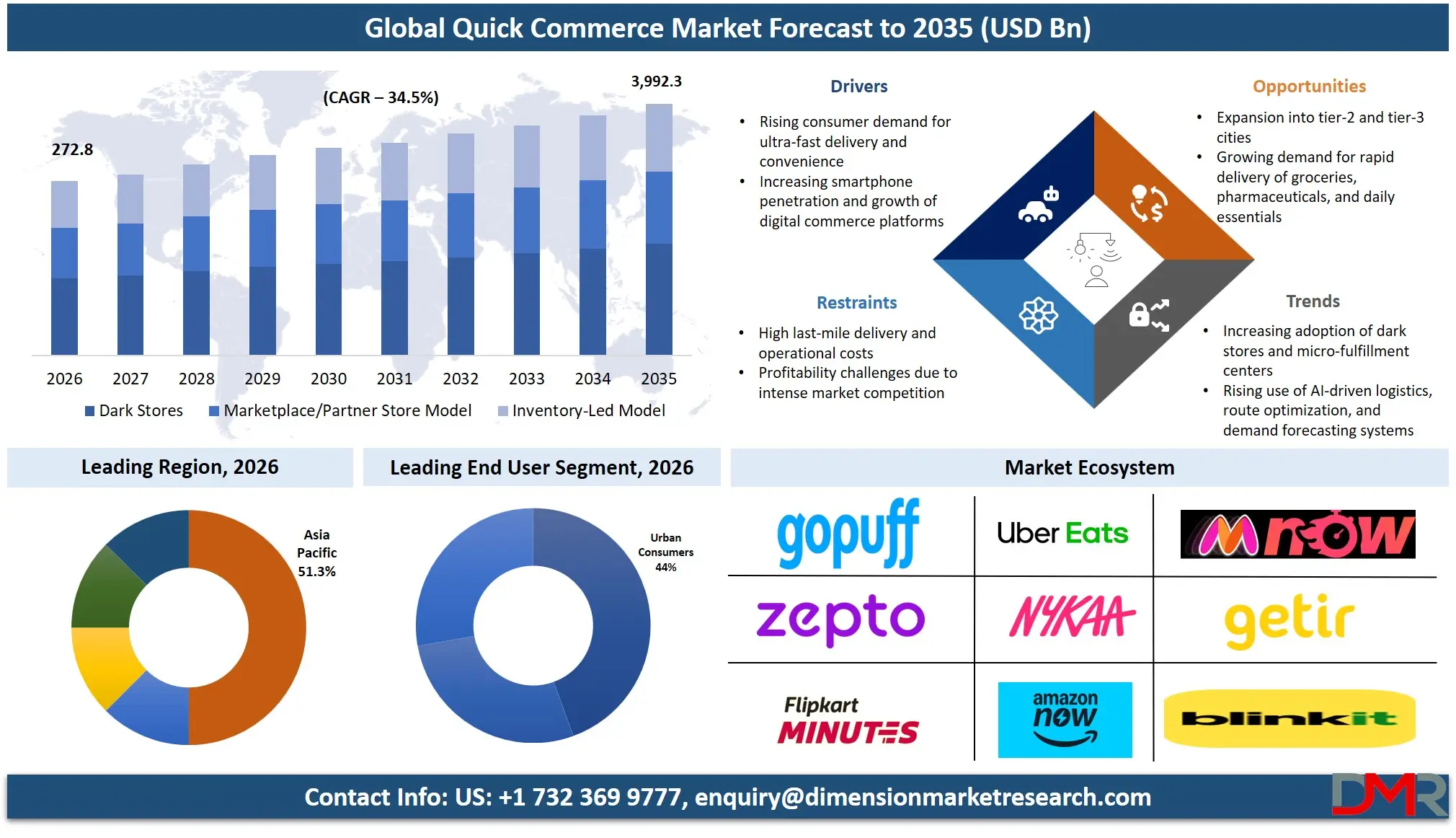

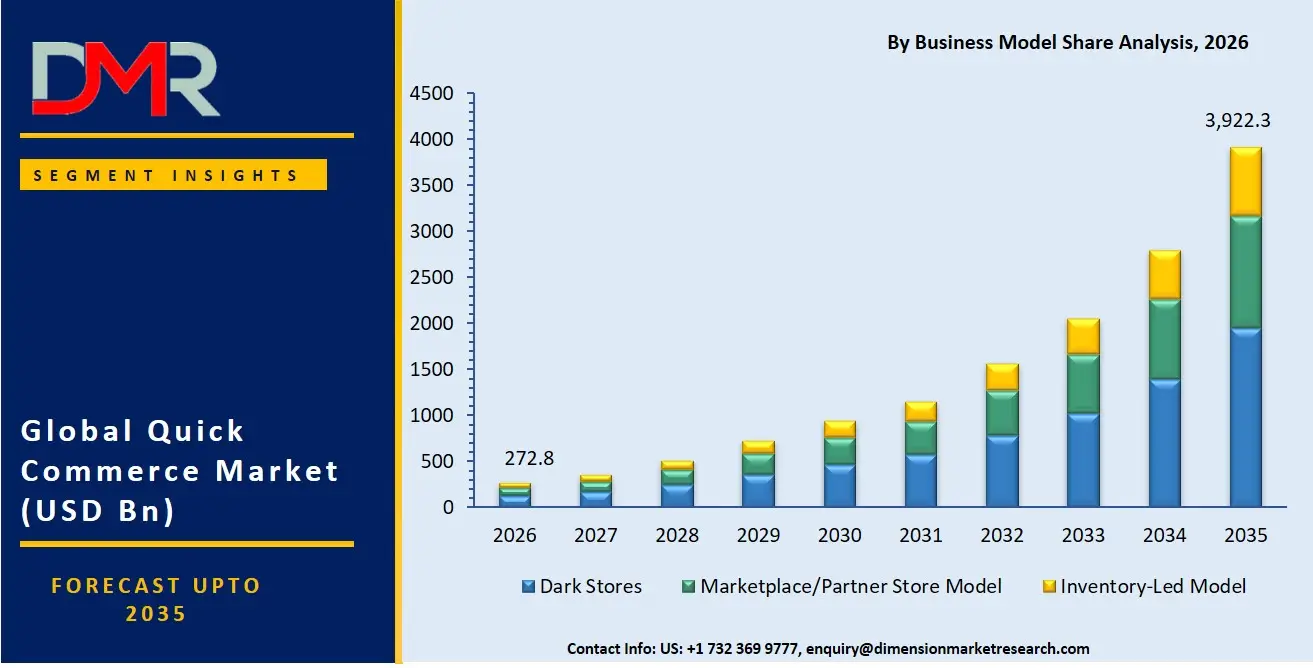

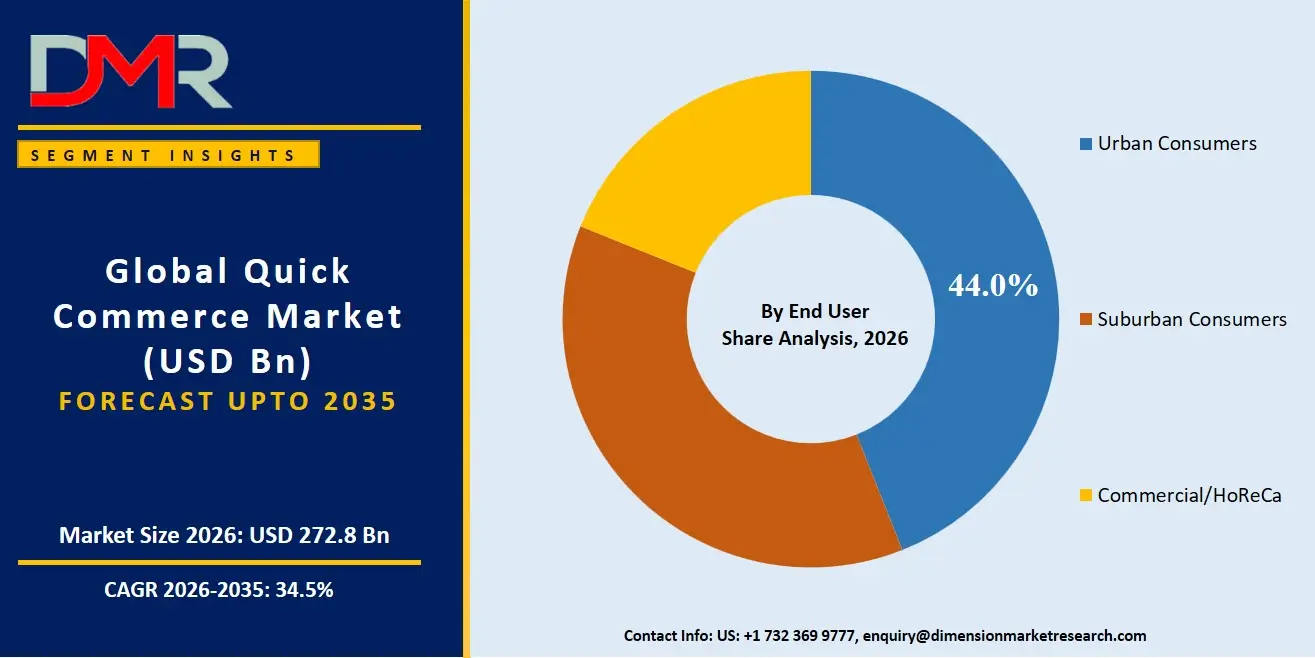

- The global Quick Commerce Market is valued at USD 201.2 Billion in 2025, reached USD 272.8 Billion in 2026, and is projected to hit USD 3,922.3 Billion by 2035 at a CAGR of 34.5%.

- Food and Groceries leads the By Product Type segment with a 33.6% revenue share in 2026.

- Dark Stores lead the By Business Model segment with a 49.8% revenue share in 2026.

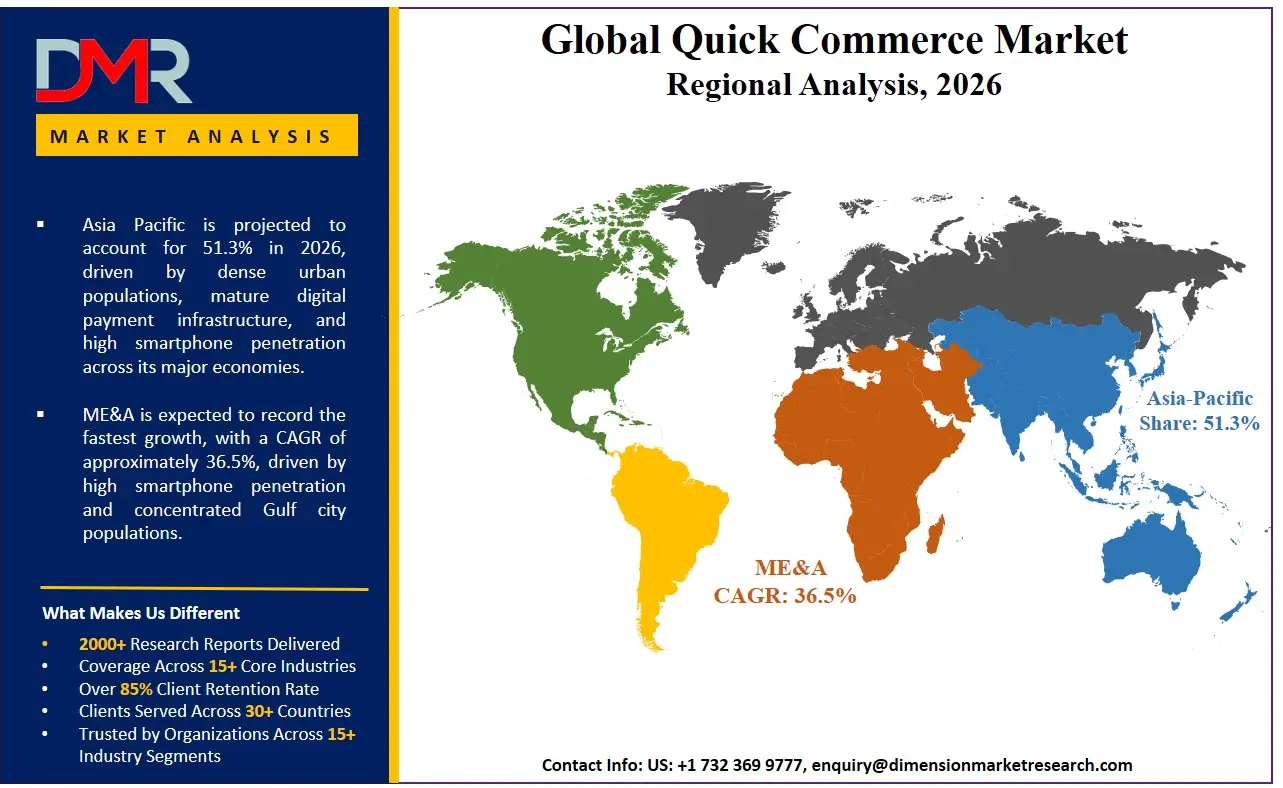

- Asia Pacific leads all regions with a 51.3% revenue share, equivalent to USD 139.9 Billion in 2026.

- Blinkit holds over 50% Q-Commerce market share in India as of September 2025.

Market Overview

Quick Commerce, commonly called Q-Commerce, delivers consumer orders within 10 to 30 minutes of placement. The model runs through dark stores, which are purpose-built fulfilment centres positioned within short distances of residential zones. Standard scheduled e-commerce, last-mile logistics services, and traditional brick-and-mortar retail fall outside the market boundary, even where those formats are testing faster delivery pilots. Product coverage spans Food and Groceries, Consumer Electronics, Fashion and Apparel, Household Essentials, Personal Care and Beauty, Snacks and Beverages, and Fresh Produce.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Q-Commerce sits inside the broader digital retail ecosystem but competes directly with physical convenience stores. Sub-30-minute delivery positions Q-Commerce as a channel replacement threat, not a convenience upgrade. The sector already accounts for approximately two-thirds of Indian e-grocery orders and approximately 10% of total Indian e-retail spend in 2024. India's Q-Commerce GMV stood above USD 5 Billion in 2025, confirming the market has crossed from early adoption into structural scale.

Platform consolidation is reshaping the global competitive structure. Meituan agreed to acquire Dingdong's China Quick Commerce and fresh grocery business for USD 717 Million in February 2026. This deal confirms that standalone Q-Commerce operators without super-app integration or deep capital backing cannot sustain viable businesses at scale in China's market.

Market Size and Forecast

The Global Quick Commerce Market size is estimated at USD 272.8 Billion in 2026 from USD 201.2 Billion in 2025, and is projected to reach USD 3,922.3 Billion by 2035, exhibiting a CAGR of 34.5% during the forecast period.

China's market reached USD 72.6 Billion in 2025 and is projected to hit USD 958.9 Billion by 2035 at a CAGR of 29.4%. These two markets together confirm that Asia is the engine pulling the global blended growth rate upward.

The forecast assumes continued dark store expansion, category diversification beyond groceries, and sustained consumer adoption in Tier-2 and Tier-3 urban centres. The upside scenario centres on Q-Commerce capturing a larger share of FMCG distribution faster than expected, particularly as platforms push electronics, beauty, and apparel into 10-minute delivery windows. The downside scenario centres on regulatory pressure compressing margins. India's trade body CAIT demanded a 28% GST on e-commerce purchases in May 2025. If enacted, platform profitability timelines could extend by two to three years, reducing early-stage investor appetite in the near term.

Product Type Analysis

Food and Groceries led the By Product Type segment with a 33.6% share in 2026.

Groceries and daily essentials carry the highest repurchase frequency of any retail category. Perishable and time-sensitive needs align directly with sub-30-minute delivery infrastructure, making Food and Groceries the natural anchor for every Q-Commerce platform. No other product category generates the daily purchase volumes required to sustain dark store economics at the unit level.

Consumer Electronics represents Q-Commerce's highest-value category extension, with platforms including Blinkit and Flipkart Minutes pushing phones and small appliances into 10-minute delivery windows in 2026. Fashion and Apparel is emerging through Myntra M-Now and Swiggy Instamart, targeting impulse and event-driven purchase occasions. Household Essentials complement grocery baskets by expanding order value without requiring separate fulfilment infrastructure. Personal Care and Beauty, led by Nykaa Now, offers higher margins than commoditised grocery items. Snacks and Beverages capture occasion-driven impulse demand where delivery speed tolerance is near zero. Fresh Produce is the most operationally demanding category, requiring precise temperature management and tight stock rotation, but platforms that master it earn the strongest repeat purchase rates.

Business Model Analysis

With a 49.8% share in 2026, Dark Stores outpaced all other Business Model categories.

Dark stores are dedicated micro-fulfilment centres closed to public shopping. They enable the precise inventory positioning and picking speed required for sub-30-minute delivery. Blinkit's network of 1,816 dark stores as of Q2 FY26 confirms this model as the structural standard for high-volume Q-Commerce operations. Platforms that control their own dark store locations control their delivery time commitments, their inventory availability, and ultimately their unit economics.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The Marketplace and Partner Store Model connects platforms with existing retail partners without owning inventory, reducing capital expenditure but sacrificing delivery speed consistency. As platforms mature, this model's structural dependence on partner store readiness becomes a competitive liability. The Inventory-Led Model is the direction the market is moving. Blinkit transitioned 80% of its Net Order Value to inventory-led fulfilment, gaining direct control over product margins, stock availability, and supplier terms. Platforms operating marketplace models face increasing pressure to migrate toward inventory ownership as competition intensifies on delivery reliability.

End-User Analysis

Urban Consumers accounted for the highest share of Quick Commerce demand in 2026, ahead of all other end-user categories.

Dark store economics depend on residential density. The closer consumers are to fulfilment locations, the lower the cost per delivery. Urban concentration is not a preference, it is an operational prerequisite. Blinkit directed more than 75% of its Q2 FY26 new store additions into India's top 10 cities precisely because those markets already meet the density threshold for viable dark store economics.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Suburban Consumers represent the next addressable demand wave as platforms extend geographic reach. Lower population density in suburban zones means platforms must accept higher cost-per-delivery until order volumes per dark store reach viable thresholds. Commercial and HoReCa buyers represent a structurally distinct but high-value segment. Hotels, restaurants, and catering operators place larger, more predictable orders that improve dark store utilisation rates and reduce fulfilment cost per unit. Platforms building dedicated B2B fulfilment capabilities within existing dark store footprints unlock revenue streams with materially better per-order economics than single-household consumer orders.

Delivery Time Analysis

10-Minute Delivery captured the leading position across Delivery Time categories in 2026.

Ten-minute delivery is the primary basis on which leading platforms compete for consumer mindshare. Achieving this window consistently requires dark store placement within approximately one kilometre of the delivery address. Flipkart Minutes launched with an explicit 10-to-15-minute delivery commitment in Bengaluru in August 2024. This geographic precision requirement explains why top-10-city dark store concentration is operationally mandated rather than strategically optional.

Fifteen-minute delivery serves as a viable middle tier for platforms expanding into areas where sub-10-minute fulfilment is not yet achievable. This window still positions Q-Commerce as categorically faster than any traditional retail alternative while allowing broader geographic coverage with existing infrastructure. Thirty-minute delivery is the entry-level threshold adopted by newer entrants and incumbent retailers. Reliance Retail's JioMart network delivers most orders under 30 minutes across 5,000-plus pin codes, making 30-minute fulfilment the natural starting point before network optimisation enables faster windows.

Payment Mode Analysis

Digital Wallets and UPI held the dominant position across Payment Mode categories in 2026.

Digital wallet transactions reduce cash handling costs, accelerate order confirmation, and enable seamless refund processing. In India, UPI has achieved near-universal adoption among smartphone users, making it the default payment layer for Q-Commerce platforms operating in the country. Platforms that remove payment friction at checkout reduce order abandonment and improve fulfilment throughput at scale.

Credit and Debit Card payments remain the primary non-cash payment mode in markets where UPI equivalents do not exist, and enable higher average order values through credit facilities. Cash on Delivery remains operationally necessary in markets where digital payment adoption is incomplete. However, COD increases per-order costs through failed delivery risk, particularly as platforms expand into Tier-2 and Tier-3 cities where digital payment penetration is lower. Managing COD economics without undermining overall platform unit economics is a material operational challenge for any platform pursuing geographic expansion.

Key Market Segments

By Product Type

- Food and Groceries

- Consumer Electronics

- Fashion and Apparel

- Household Essentials

- Personal Care and Beauty

- Snacks and Beverages

- Fresh Produce

By Business Model

- Dark Stores

- Marketplace/Partner Store Model

- Inventory-Led Model

By End-User

- Urban Consumers

- Suburban Consumers

- Commercial/HoReCa

By Delivery Time

- 10-Minute Delivery

- 15-Minute Delivery

- 30-Minute Delivery

By Payment Mode

- Digital Wallets/UPI

- Credit/Debit Card

- Cash on Delivery

Regional Analysis

Asia Pacific held a 51.3% share in 2026, valued at USD 139.9 Billion.

Asia Pacific's lead reflects the convergence of dense urban populations, mature digital payment infrastructure, and high smartphone penetration across its major economies. China and India anchor the region. China's market is forecast to reach USD 958.9 Billion by 2035 at a CAGR of 29.4%, while India's GMV exceeded USD 5 Billion in 2025. Asia Pacific is where Q-Commerce business models are being stress-tested at the largest scale globally, and where the outcomes of that stress test will define the next decade of platform strategy.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

North America follows a measured growth path. The US market stands at USD 63.8 Billion in 2026, forecast to reach USD 145.5 Billion by 2035 at a CAGR of 8.6%. High last-mile labour costs and lower residential density outside major metro areas constrain the economics of sub-30-minute delivery at national scale. Europe's Q-Commerce market is defined by consolidation rather than greenfield expansion. As reported by Reuters, Getir acquired Gorillas in a USD 1.2 Billion deal, creating a combined entity valued at approximately USD 10 Billion. European labour protections and higher operating costs make dark store operations more capital-intensive than in Asia, sustaining fewer but larger platforms. Latin America presents a structural opportunity based on high urban density in cities such as São Paulo and Mexico City, but infrastructure investment and digital payment adoption remain the primary rate-limiting factors. The Middle East, served by Noon Minutes alongside global operators, benefits from high smartphone penetration and concentrated Gulf city populations, though specific revenue figures for the MEA region are not available in the provided data.

Key Regions and Countries

North America

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Market Dynamics

Dark Store Scale and Capital Inflows Accelerate Infrastructure Build-Out

Dark store proliferation is the physical backbone of Q-Commerce economics. As reported by YourStory, Blinkit added 272 dark stores in Q2 FY26 alone, reaching 1,816 locations, with more than 75% of new additions concentrated in India's top 10 cities. Merchantspring data confirms Blinkit, Zepto, and Swiggy Instamart collectively processed up to 4.45 Million daily orders in March 2025. Order volume at this scale validates the dark store model and creates the threshold conditions for viable unit economics.

Capital inflows reinforce the infrastructure build-out. Amazon Now expanded to 100 cities in India in September 2025, backed by a INR 2,800 Crore (USD 304 Billion) investment targeting 1,000-plus micro-fulfilment centres by 2028. Swiggy shareholders approved a QIP in December 2025 to raise up to INR 10,000 Crore (USD 1 Trillion), with proceeds designated for Instamart's expansion. Institutional capital at this scale signals that investors view dark store infrastructure as a durable competitive asset rather than a subsidy-driven model.

Unit Economics Strain and Regulatory Pressure Constrain Profitability Timelines

Profitability remains structurally distant for all major Q-Commerce platforms. As reported by BW Retail World, Zepto's FY25 net loss reached INR 3,367 Crore (USD 355.4 Billion), widening 177% YoY despite strong revenue growth. This gap between revenue scale and margin reality defines the core tension in Q-Commerce. Capital availability, not consumer demand, is the binding constraint on market development for every platform operating below contribution margin breakeven.

Regulatory opposition adds a structural cost risk on top of existing unit economics pressure. CAIT launched a nationwide campaign in May 2025 demanding 28% GST on e-commerce purchases and a dedicated Q-Commerce regulator. If enacted, a tax increase of this magnitude would compress already-thin platform margins. Platforms already managing delivery worker costs across a workforce of 400,000-plus face compounding pressure from any additional regulatory burden imposed on the operating model.

Tier-2 City Expansion and Category Broadening Open New Revenue Pools

Geographic expansion beyond metro areas is the next structural growth phase for Q-Commerce. Reliance Retail's JioMart expanded its Quick Commerce network to more than 600 dark stores across 5,000-plus pin codes in October 2025, processing close to 1.6 Million daily orders by Q3 FY26 with a 42% sequential surge in Q2 FY26. Sector projections indicate approximately 40% annual GMV growth through 2030 for Tier-2 and Tier-3 city penetration. Smaller cities offer lower real estate costs and lower competitive intensity than top-10 metro markets, improving the economics of dark store entry for platforms with existing fulfilment infrastructure.

Category expansion beyond groceries unlocks a materially larger total addressable market. Flipkart Minutes and Swiggy Instamart pushed phones, small appliances, beauty, and pet care products into 10-minute delivery windows in 2025. Blinkit extended assortment into electronics, toys, and event-day gifting. Higher-margin categories spread fixed dark store costs across more valuable product mix and improve per-delivery economics without requiring additional location investment. For platforms already operating at scale, category broadening is the fastest available path to improving contribution margins without adding infrastructure capital.

Market Trends

Consolidation, Inventory Ownership, and Profitability Discipline Redefine Platform Strategy

Market consolidation is the defining structural shift across global Q-Commerce. Platforms without capital backing or ecosystem integration are exiting or being absorbed. Blinkit's Q2 FY26 revenue reached INR 9,891 Crore (USD 1,044 Billion), jumping 8.5X YoY following its transition to an inventory-led model covering 80% of Net Order Value. Inventory ownership gives platforms direct control over margins and supplier terms, advantages that compound as order volumes scale. Early movers who establish dense, profitable store networks before the next wave of incumbent capital arrives hold location advantages that are expensive and time-consuming to replicate.

Market Competition Overview

The global Quick Commerce Market is moderately fragmented at the global level but consolidating rapidly at the national level. Blinkit crossed 50% Q-Commerce market share in India in September 2025, up from approximately 46% in late 2024, while Dunzo exited the sector entirely. Dark store economics reward density, and density rewards the platform with the most locations and the highest order volumes. Winner concentration in national markets is a structural outcome of this cost model, not a coincidental pattern.

Swiggy Instamart's Adjusted EBITDA loss stood at INR 849 Crore in Q2 FY26, but contribution margin improved approximately 200 basis points QoQ to -2.6%. This directional improvement separates platforms building toward sustainable economics from those that will eventually exit or consolidate. Platforms gaining competitive ground are those with access to deep capital or parent ecosystem advantages. Those without either face a structurally narrowing window to reach viable scale before incumbents with balance sheet strength lock up prime dark store locations.

Company Profiles

Zomato repositioned as a Q-Commerce-first platform after Blinkit's Net Order Value of INR 9,203 Crore (USD 971.4 Billion) in Q1 FY26 overtook Zomato's core food delivery NOV of INR 8,967 Crore for the first time. Blinkit's strategy of transitioning 80% of NOV to an inventory-led model gives it higher revenue recognition and direct supplier leverage. Swiggy Instamart operates 1,102 dark stores across 128 cities with 4.6 Million sq ft of dark store area. GOV reached INR 7,022 Crore in Q2 FY26, up 108% YoY. Cross-platform leverage with Swiggy's food delivery network provides consumer relationship advantages, though an Adjusted EBITDA loss of INR 849 Crore in Q2 FY26 confirms synergies have not yet translated to segment-level profitability.

Zepto raised USD 450 Million in a pre-IPO funding round at a USD 7 Billion valuation in October 2025, with CalPERS reported as the lead investor, bringing total capital raised to approximately USD 900 Million. As reported by BW Retail World, FY25 revenue reached approximately INR 11,110 Crore, representing approximately 150% YoY growth. Zepto's strategy prioritises market share capture over near-term profitability, a posture that requires sustained investor confidence to maintain. Reliance Retail entered Q-Commerce by repurposing existing store infrastructure rather than building from scratch, giving it a structurally lower cost base than pure-play competitors and positioning it to compete on price and coverage without requiring continued external capital raises.

Key Players

- Gopuff

- Getir

- Instacart

- Zomato (Blinkit)

- Zepto

- Swiggy Instamart

- BigBasket (BB Now)

- Flipkart Minutes

- Amazon Now

- Deliveroo (Hop)

- Noon Minutes

- JOKR

- DoorDash

- Uber Eats

- Walmart

- Nykaa Now

- Myntra M-Now

Supply Chain and Value Chain Analysis

The Q-Commerce value chain begins with suppliers, including FMCG brands, fresh produce vendors, electronics manufacturers, and apparel producers, who supply inventory directly to dark store operators. Unlike traditional retail, Q-Commerce compresses the distribution chain by removing regional warehousing and retail store intermediaries. Platforms operating inventory-led models negotiate directly with suppliers, shortening lead times and improving stock availability at the point of fulfilment. Maximum value creation sits at the dark store operations layer, where pick-and-pack efficiency, shrinkage rates, and inventory turnover determine whether a platform achieves competitive cost per order.

The last-mile delivery layer is the highest-cost segment of the value chain. Blinkit, Zepto, and Swiggy Instamart planned collective employment of over 400,000 workers by March 2025, confirming that workforce scale is a direct input to delivery capacity and a significant labour cost exposure. The biggest supply chain risk is inventory positioning accuracy. Dark stores carry limited SKUs relative to full-format supermarkets. Fresh produce carries near-zero tolerance for overstocking errors. Platforms investing in AI-driven demand forecasting and real-time inventory management reduce this risk and improve gross margin outcomes at scale.

Recent Developments

- December 2025 Eternal (Zomato parent). Strategy update. Blinkit's dark store target raised to approximately 2,100 stores by end of FY26, up from prior guidance of 2,000, reinforcing the platform's strategy of prioritising long-term footprint over near-term margin improvement.

- September 2025 Blinkit. Market share milestone. Blinkit crossed 50% Q-Commerce market share in India as Dunzo exited the sector entirely, with Q2 FY26 revenue growing 171% YoY across 1,816 operational dark stores.

- March 2025 Swiggy Instamart. Expansion. Swiggy Instamart expanded its Quick Commerce service to 100 cities across India, adding 32 new cities including Raipur, Siliguri, Jodhpur, and Thanjavur, offering 30,000-plus products through megapod dark stores of 10,000 to 12,000 sq ft housing up to 50,000 SKUs.

- April 2026 Flipkart Minutes. Product development. Flipkart was reported to be developing a standalone app for Flipkart Minutes, with a planned pilot in July 2026 ahead of the Big Billion Days sale, operating 750 to 800 dark stores as of March 2026.

Report Details

| Report Characteristics |

| Market Value (2025) |

USD 201.2 Billion |

| Market Value (2026) |

USD 272.8 Billion |

| Forecast Revenue (2035) |

USD 3,922.3 Billion |

| CAGR (2026–2035) |

34.5% |

| Base Year for Estimation |

2025 |

| Historic Period |

2020 to 2024 |

| Forecast Period |

2026 to 2035 |

| Report Coverage |

Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered |

By Product Type (Food and Groceries, Consumer Electronics, Fashion and Apparel, Household Essentials, Personal Care and Beauty, Snacks and Beverages, Fresh Produce), By Business Model (Dark Stores, Marketplace/Partner Store Model, Inventory-Led Model), By End-User (Urban Consumers, Suburban Consumers, Commercial/HoReCa), By Delivery Time (10-Minute Delivery, 15-Minute Delivery, 30-Minute Delivery), By Payment Mode (Digital Wallets/UPI, Credit/Debit Card, Cash on Delivery) |

| Regional Analysis |

North America – US and Canada; Europe – Germany, France, The UK, Spain, Italy, and Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, and Rest of APAC; Latin America – Brazil, Mexico, and Rest of Latin America; Middle East & Africa – GCC, South Africa, and Rest of MEA |

| Competitive Landscape |

Gopuff, Getir, Instacart, Zomato (Blinkit), Zepto, Swiggy Instamart, BigBasket (BB Now), Flipkart Minutes, Amazon Now, Deliveroo (Hop), Noon Minutes, JOKR, DoorDash, Uber Eats, Walmart, Nykaa Now, Myntra M-Now |

| Customization Scope |

Customization for segments and region or country level will be provided. Additional customization can be done based on requirements. |

| Purchase Options |

Three license options: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF). |

Frequently Asked Questions

What is the biggest investment opportunity in Quick Commerce Market?

▾ The highest-conviction opportunities lie in Tier-2 and Tier-3 city dark store infrastructure, category expansion into electronics and personal care, and the HoReCa commercial buyer segment. The global market grows from USD 201.2 Billion in 2025 to approximately USD 3,922.3 Billion by 2035 at a 34.5% CAGR. Early-mover location advantages in prime dark store sites are already closing in major metro markets.

Who are the top companies in Quick Commerce Market?

▾ Leading players include Zomato (Blinkit), Zepto, Swiggy Instamart, Reliance Retail (JioMart), Gopuff, Getir, Instacart, BigBasket (BB Now), Flipkart Minutes, Amazon Now, Deliveroo (Hop), Noon Minutes, JOKR, DoorDash, Uber Eats, Walmart, Nykaa Now, and Myntra M-Now. Blinkit holds the largest share in India at over 50% as of September 2025.

Which segment is growing fastest in Quick Commerce Market and why?

▾ Consumer Electronics, Fashion and Apparel, and Personal Care and Beauty are the fastest-expanding categories as platforms extend beyond the grocery anchor. Flipkart Minutes and Swiggy Instamart both pushed phones, small appliances, and beauty products into 10-minute delivery windows in 2025. These categories carry higher margins than grocery staples and serve impulse and event-driven purchase occasions that no other retail format can match on speed.

Which region is growing fastest in Quick Commerce Market and why?

▾ Asia Pacific drives the fastest structural expansion globally. China is forecast to reach USD 958.9 Billion by 2035 at a CAGR of 29.4%. India's Tier-2 and Tier-3 city penetration projects approximately 40% annual GMV growth through 2030, representing the single fastest sub-market by projected growth rate within the region.

What is the biggest challenge holding Quick Commerce Market back?

▾ Unit economics strain is the primary structural challenge. Zepto's FY25 net loss widened 177% YoY despite strong revenue growth, illustrating how difficult it is to scale Q-Commerce operations toward profitability under current cost structures. Regulatory pressure from trade bodies demanding higher GST on e-commerce purchases adds compounding risk to platforms already operating below contribution margin breakeven.