Market Snapshot

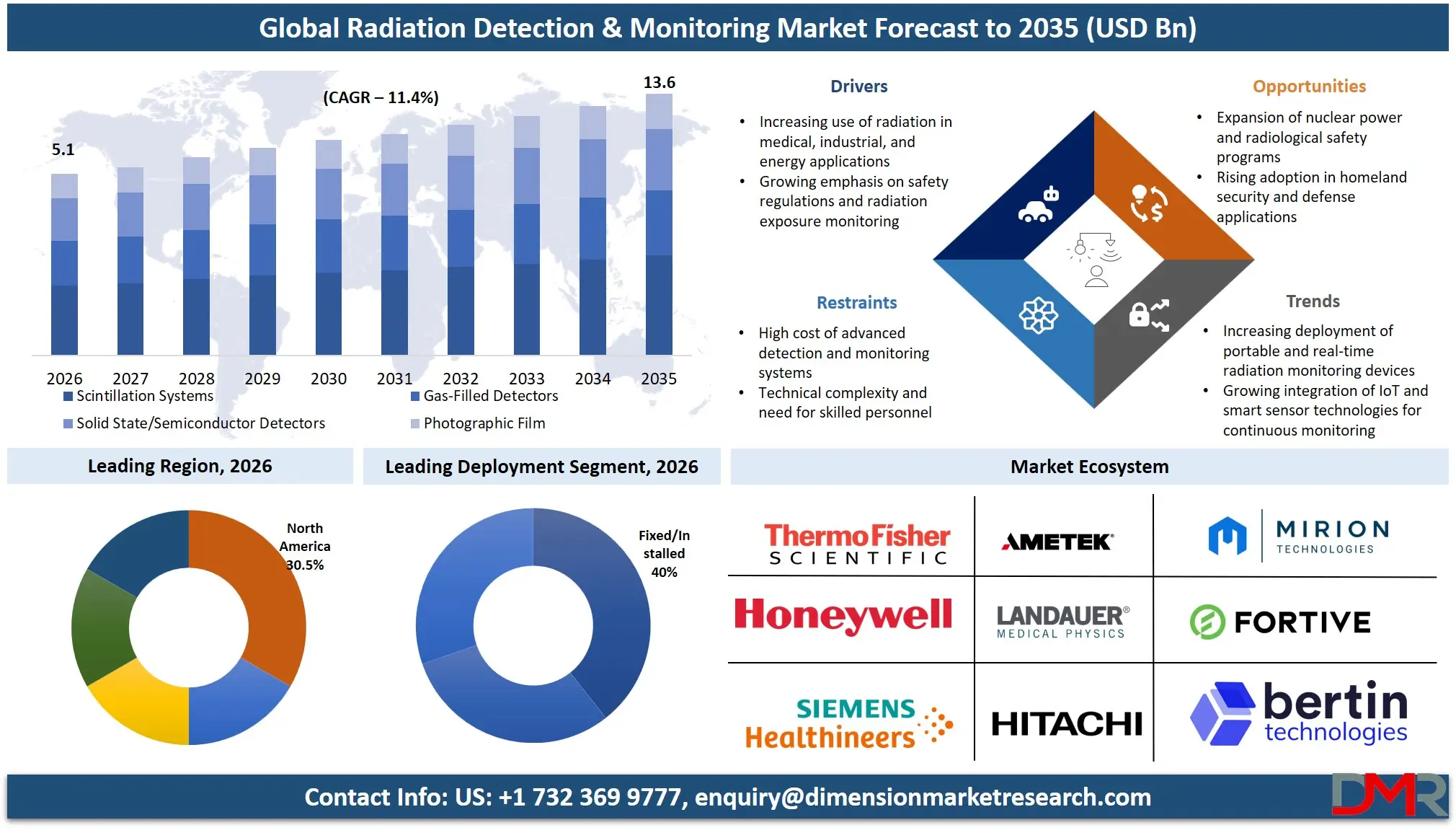

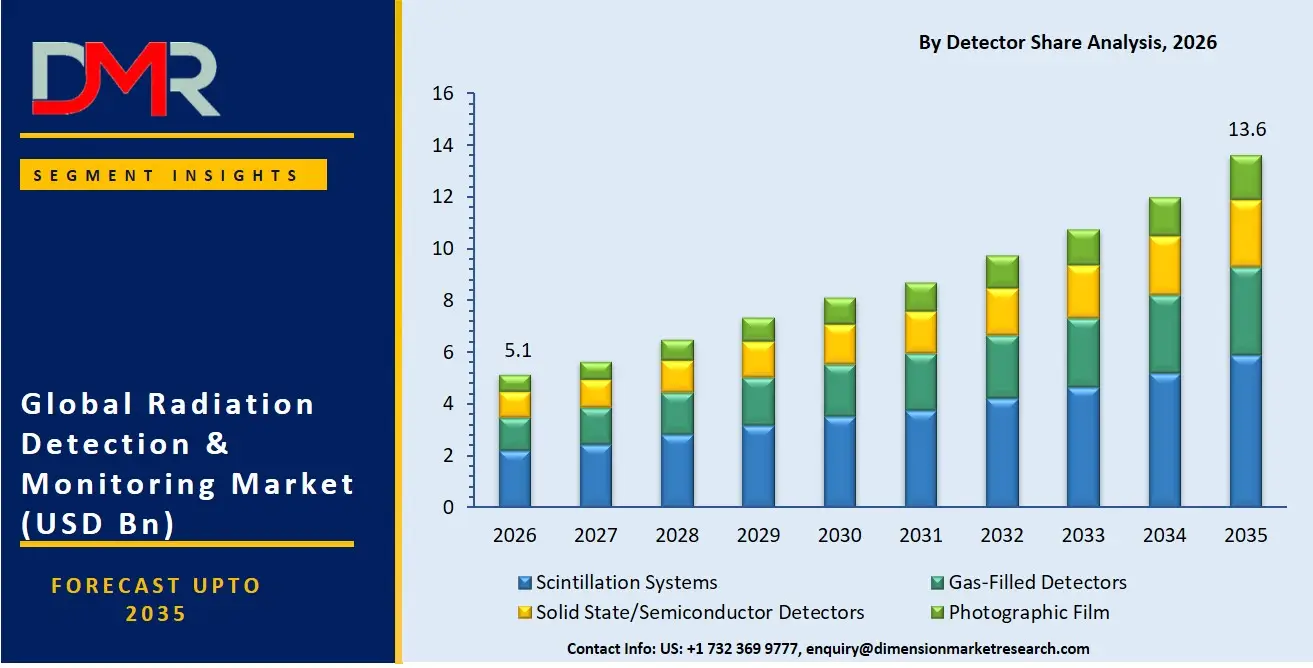

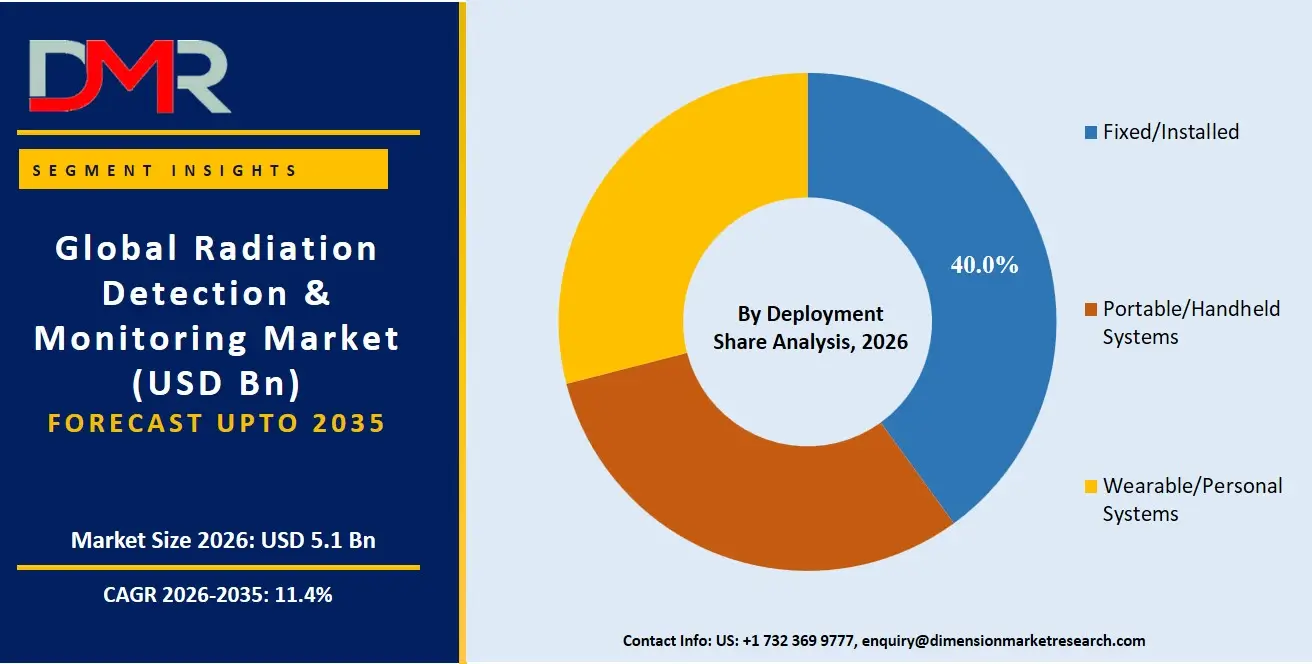

- The global Radiation Detection and Monitoring Market is valued at USD 4.6 Billion in 2025, reached USD 5.1 Billion in 2026, and is projected to hit USD 13.6 Billion by 2035 at a CAGR of 11.4%.

- By Product Type, Detection and Monitoring Solutions leads with a 51.1% revenue share in 2026.

- By Detector/Technology Type, Scintillation Systems holds a 43.3% revenue share in 2026.

- By End-User, Medical and Healthcare accounts for 37.8% of total market revenue in 2026.

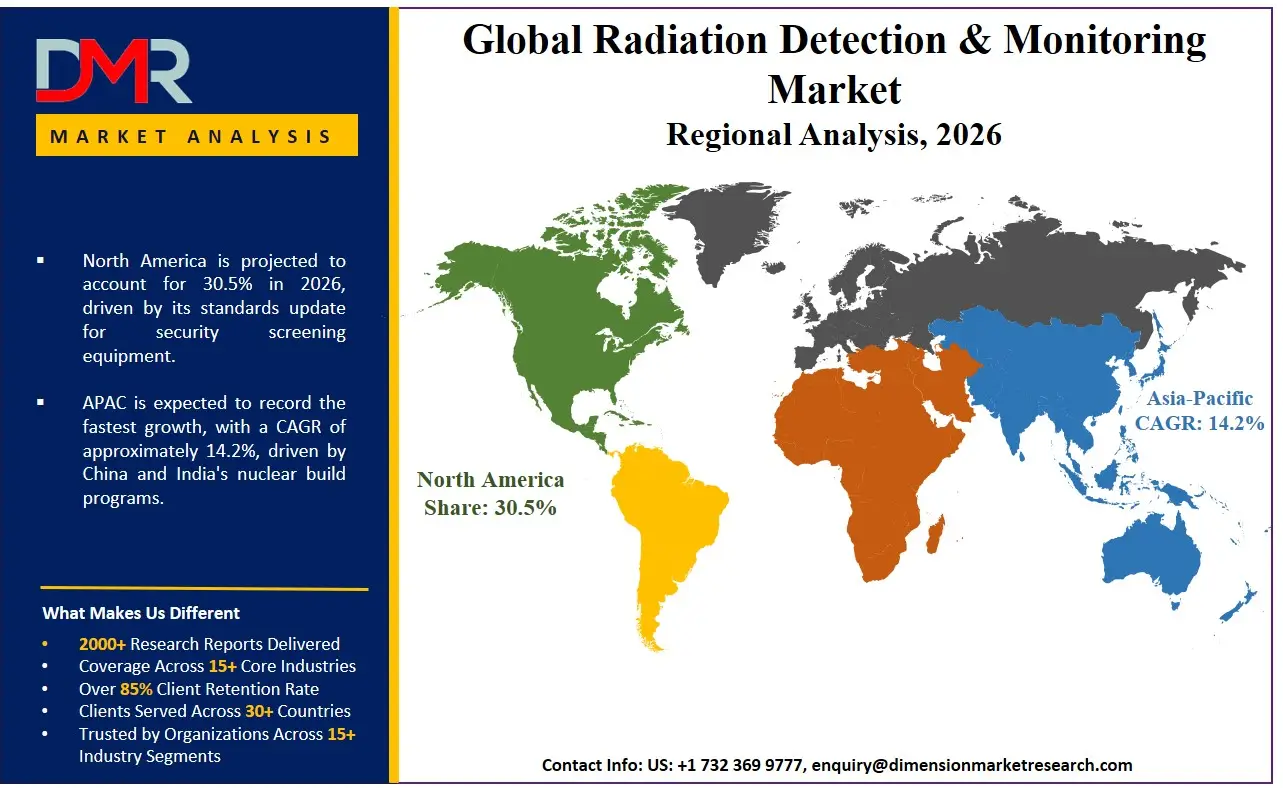

- North America leads all regions with a 30.5% revenue share, valued at approximately USD 1.6 Billion in 2026.

Market Overview

The radiation detection and monitoring market covers instruments, systems, and services designed to detect, measure, and continuously track ionizing radiation across nuclear, medical, industrial, and security environments. Personal dosimeters, area process monitors, environmental radiation sensors, surface contamination monitors, radioactive material detection systems, and dosimetry data management services all fall within scope. Radiation therapy equipment, nuclear fuel cycle hardware, and reactor control systems beyond their instrumentation interfaces sit outside this market's boundary.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

This market connects directly to global nuclear energy expansion, healthcare regulation, and national security policy. Every new nuclear reactor requires area monitors, effluent sensors, and worker dosimetry systems. Every hospital operating a nuclear medicine unit needs dose verification equipment. Based on data from UNSCEAR, approximately 24 million workers worldwide are monitored for ionizing radiation exposure, of whom approximately 11.4 million, or 48%, work in sectors involving artificial ionizing radiation sources. The average annual effective dose for workers in human-made radiation environments is estimated at 0.5 mSv, well below the 20 mSv occupational annual limit, confirming that monitoring infrastructure rather than dose reduction alone sustains this market's volume of equipment and service contracts.

Technology evolution is reshaping detection hardware at the component level. A novel 1D photonic crystal gamma radiation detector achieved a record-high quality factor of 447,747 and a sensitivity of 0.2267 nm/RIU in 2025, according to research published in Nature Scientific Reports. CsPbBr3 perovskite detectors separately demonstrated long-term stability over 225 days and outperformed CdZnTe at gamma-ray energies above 500 keV in 2025 research. These two advances signal a hardware transition that will affect procurement decisions and upgrade cycles across clinical, security, and nuclear applications over the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Market Size and Forecast

The Global Radiation Detection and Monitoring Market size is estimated at USD 5.1 Billion in 2026 from USD 4.6 Billion in 2025, and is projected to reach USD 13.6 Billion by 2035, exhibiting a CAGR of 11.4% during the forecast period.

The U.S. market stood at USD 1.1 billion in 2026 and is projected to reach USD 2.4 billion by 2035 at a CAGR of 8.9%. China's market reached USD 1.0 billion in 2026, forecast to reach USD 3.0 billion by 2035 at a faster CAGR of 12.5%, reflecting accelerated domestic reactor commissioning and regulatory compliance build-out. China's State Council approved 10 new reactors across five coastal projects in April 2025, representing a combined investment exceeding CNY 200 billion (approximately USD 212.54 billion), per Reuters, with more than 30 additional reactors under construction, adding approximately 34,000 megawatts. China alone creates a multi-decade instrumentation procurement pipeline that underpins the global forecast trajectory through 2035.

The upside scenario centers on accelerated SMR deployment. India's Union Budget 2025-26 allocated INR 20,000 crore (approximately USD 1.0 billion) under the Nuclear Energy Mission, targeting at least five indigenous SMRs operational by 2033, according to the Nuclear Business Platform. If SMR deployment accelerates beyond current timelines, the installed base requiring monitoring instrumentation will scale faster than baseline forecasts assume. The downside scenario is shaped by multi-jurisdictional regulatory approval cycles that lengthen commercialization timelines for new detection products and high capital costs for nuclear-grade detection hardware that constrain adoption outside tier-1 utilities, as identified in Mirion Technologies' FY2024 10-K filing.

Market Dynamics

Nuclear Capacity Expansion and Medical Compliance Requirements Drive Non-Discretionary Procurement

Nuclear capacity expansion is the single largest structural force generating new demand for radiation detection equipment. As reported by the World Nuclear Association, approximately 80 power reactors were under construction in 15 countries, and 120 further reactors were planned as of early 2026. Each new installation requires area monitors, environmental sensors, and worker dosimetry systems as a contractual compliance requirement embedded in every reactor build program. Mirion Technologies Q1 2026 Nuclear and Safety segment revenue reached USD 186 million, up 39% year-over-year, confirming that reactor build activity is already converting into commercial order flow at a measurable scale.

Medical sector adoption adds a parallel and structurally resilient demand channel. Mirion Technologies Medical segment revenue reached USD 310.8 million in FY2025, growing from USD 299.6 million in FY2024, according to the company's SEC filing, driven by radiopharmaceutical therapy expansion and dosimetry compliance requirements. Thermo Fisher Scientific received a five-year, USD 94.5 million U.S. Department of Defense contract in June 2025 to supply the Navy with its occupational dosimetry system, confirming that government procurement at scale continues to anchor the medical and defense instrumentation base independently of commercial healthcare budget cycles.

Regulatory Complexity and Capital Concentration Limit Mid-Market Penetration

IAEA safety standards require country-level adoption before radiation monitoring devices can be legally deployed for public, worker, and patient monitoring. This process varies in duration and administrative complexity across national regulatory bodies, creating uneven market access for vendors operating across multiple geographies. The resulting pre-commercialization runway is asymmetric. Large vendors with dedicated regulatory teams absorb it more efficiently than smaller innovators, concentrating market access among established platform providers.

Revenue within the Nuclear and Safety segment is heavily concentrated among large reactor operators, as identified in Mirion Technologies' FY2024 10-K filing. Smaller utilities, research institutions, and emerging-market operators often cannot absorb the full capital cost of compliant monitoring infrastructure without government grant support or phased procurement programs. Vendors that develop modular lower-cost product lines without compromising compliance standards can access the underserved mid-market, but the regulatory approval cycle for any new product configuration still applies, extending time-to-revenue for such strategies beyond what capital markets typically underwrite at early stage.

SMR Instrumentation, EU Sensor Networks, and Port Screening Standards Create Distinct Revenue Channels

Small Modular Reactor deployment is creating a distinct instrumentation sub-market with different technical and commercial requirements from conventional large reactors. India's allocation of INR 20,000 crore under the Nuclear Energy Mission for SMR development, targeting five indigenous SMRs by 2033, creates a confirmed national procurement pipeline for SMR-specific monitoring systems. The IAEA has published dedicated guidance on instrumentation and control systems for advanced SMRs, signaling regulatory readiness that converts vendor investment in SMR-compatible products into a commercially deployable asset rather than a speculative development program.

Environmental monitoring networks represent a separate opportunity driven by European digital infrastructure policy. The EU's Digital Decade Report committed member states to EUR 288.6 Billion in national roadmap investments in 2025, funding cross-border digital sensor networks, including environmental radiation monitoring grids.

Market Trends

Automated SMR Platforms, Vendor Consolidation, and AI-Enabled Analytics Are Redefining Market Structure

SPC Doza launched a dedicated SMR monitoring suite featuring continuous air and environmental sensors in October 2025, marking the first commercially available monitoring platform purpose-built for the SMR reactor format. Buyers now evaluate system-level data architecture and connectivity rather than sensor-level detection performance alone, shifting procurement criteria in a direction that favors integrated platform vendors over discrete instrument suppliers. Mirion Technologies completed the acquisition of Paragon Energy Solutions for approximately USD 585 million in December 2025, integrating over 100 nuclear engineers and achieving a presence in 100% of North American reactors.

Bertin Technologies grew detection and monitoring sales from EUR 132 million in 2023 to EUR 180 million in 2024, a 36% increase, through the acquisition of VF Nuclear. Vendors unable to match this consolidation scale through organic growth or M&A risk losing access to large utility and government contracts where comprehensive product portfolios are a qualification requirement.

India's IndiaAI Mission onboarded 38,000 GPUs at subsidized rates of INR 65 per hour as of November 2025, per a PIB release, enabling AI-based data processing across government-managed infrastructure including radiation monitoring networks. Research published in 2025 demonstrated that ML-guided sensor placement achieved an R2 score of 0.95 versus 0.85 for conventional networks and RMSE 30% lower, confirming that algorithm-driven network design measurably improves emergency response accuracy.

Product Type Analysis

Detection and Monitoring Solutions

Detection and Monitoring Solutions leads the By Product Type segment with a 51.1% share, reflecting mandatory continuous monitoring requirements across nuclear, medical, and environmental networks. As reported by the IAEA, 416 reactors across 31 countries require permanent area monitoring systems, making this product category the structural backbone of market revenue that cannot be deferred without regulatory consequence.

Solid State and Semiconductor Detectors represent the fastest-growing technology sub-segment within detection solutions. A CdZnTe semiconductor detector achieved 4.3% energy resolution with Cs-137 at room temperature in 2025, per research published in ScienceDirect, with high-purity configurations achieving energy resolution as low as 0.15% at 662 keV. Superior energy resolution in compact form factors is pulling semiconductor detectors into premium clinical and spectrometry applications at the expense of legacy gas-filled and scintillation alternatives.

Technology Type Analysis

Scintillation Systems

Scintillation Systems accounts for 43.3% of the By Detector/Technology Type segment, driven by broad deployment across nuclear portal monitors, environmental networks, and medical imaging systems. Scintillation detectors operate reliably at room temperature across a broad energy range, and their established manufacturing base and wide regulatory acceptance make them the default technology choice for most procurement programs where cost and operational simplicity outweigh energy resolution requirements.

Solid State and Semiconductor Detectors are the fastest-growing technology type, gaining share in applications requiring high energy resolution and compact form factors. The CERN DRD3 collaboration demonstrated a silicon carbide detector achieving energy resolution of 30 keV at 5.8 MeV alpha particles with timing resolution under 1 ns in 2025, establishing SiC as a technically validated alternative to silicon in demanding research and clinical environments where performance requirements exceed what scintillation systems can deliver.

End-User Analysis

Medical and Healthcare

Medical and Healthcare captures 37.8% of the By End-User segment, as mandatory dosimetry compliance across nuclear medicine and radiotherapy makes procurement non-discretionary across hospital networks. France's SISERI system covers more than 350,000 workers monitored annually for ionizing radiation exposure, with 386,080 workers monitored in 2022, of whom 92.7% received annual doses below 1 mSv, per France's nuclear safety authority. Compliance infrastructure of this scale means every employer in France's medical sector is a mandated buyer of certified dosimetry services and equipment regardless of budget cycle conditions.

Energy and Power/Nuclear Power Plants represent the fastest-growing end-user segment in absolute revenue terms. Mirion Technologies Nuclear and Safety segment generated revenue of USD 614.6 million in FY2025, up from USD 549.4 million in FY2024, per SEC filings, driven by life-extension spending and early SMR instrumentation contracts. China's nuclear power investment in construction and engineering reached a record CNY 146.9 Billion in 2024, per the China Nuclear Energy Association, confirming that new-build procurement will sustain this segment's revenue base through the end of the decade.

Deployment Analysis

Fixed/Installed Systems

Fixed/Installed Systems account for 40.0% of the By Deployment segment in 2026, reflecting their critical role in continuous radiation monitoring across nuclear power plants, hospitals, research laboratories, industrial facilities, and border security infrastructure. These systems are embedded within fixed operational environments where uninterrupted monitoring, regulatory compliance, and real-time radiation surveillance are mandatory. The segment benefits from long asset lifecycles and recurring replacement demand as operators modernize monitoring networks to meet increasingly stringent radiation safety standards. Large-scale investments in nuclear power expansion, radiotherapy facilities, and critical infrastructure protection continue to reinforce procurement of permanently installed radiation detection systems.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Wearable/Personal Systems represent the fastest-growing deployment segment, supported by tightening occupational safety regulations and the expanding workforce exposed to ionizing radiation. Nuclear energy operators, healthcare providers, industrial inspection companies, and emergency response organizations are increasingly equipping personnel with individual radiation monitoring devices to ensure real-time dose tracking and regulatory compliance. Growth is further supported by advances in miniaturization, wireless connectivity, and digital dose management platforms, enabling organizations to monitor worker exposure more effectively. Rising emphasis on worker safety across nuclear decommissioning projects, radiopharmaceutical production facilities, and next-generation reactor programs is expected to accelerate adoption of personal radiation monitoring technologies throughout the forecast period.

Key Market Segments

By Product Type

- Detection and Monitoring Solutions

- Safety Equipment

- Personal Dosimeters

- Area Process Monitors

- Environmental Radiation Monitors

- Surface Contamination Monitors

- Radioactive Material Monitors

By Detector/Technology Type

- Scintillation Systems

- Gas-Filled Detectors

- Solid State/Semiconductor Detectors

- Photographic Film

By End-User/Industry Vertical

- Medical and Healthcare

- Industrial

- Homeland Security and Defense

- Energy and Power/Nuclear Power Plants

- Research and Academia

- Environmental Monitoring

By Deployment

- Fixed/Installed Systems

- Portable/Handheld Systems

- Wearable/Personal Systems

Regional Analysis

North America holds the leading regional position with a 30.5% revenue share, valued at approximately USD 1.6 Billion in 2026, with the United States contributing 70% of that regional total. The U.S. nuclear workforce employed 58,517 workers in 2023, a 2.8% increase from 2022, per world-nuclear-news.org, sustaining occupational dosimetry demand. CBP's ongoing radiation screening mandate across all U.S. ports of entry and NIST's April 2025 documentary standards update for security screening equipment anchor federal procurement of detection systems across border, aviation, and defense applications that competitors in other regions cannot access without U.S. regulatory certification.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Asia Pacific is the fastest-structurally-expanding region, driven by China and India's nuclear build programs. China had 57 to 58 operational reactors with approximately 60,000 megawatts of installed capacity at end-2024, with India's current nuclear capacity standing at 8,180 megawatts against a national target of 100,000 megawatts by 2047, creating a more than tenfold expansion requiring proportional radiation monitoring infrastructure at every new installation across the forecast period.

Key Regions and Countries

North America

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Competitive Landscape

The radiation detection and monitoring market is consolidating rapidly around a small number of scaled vendors with multi-segment product portfolios and direct presence in major nuclear markets. Mirion Technologies reported a total backlog of USD 1,104.3 million at December 31, 2025, up from USD 811.9 million at December 31, 2024, per SEC filings. In April 2026, Mirion secured a USD 35 million SMR instrumentation and control systems order from a single leading SMR developer, following USD 50 million in SMR-related orders in Q1 2026, confirming that first-mover SMR commercial positioning is converting into multi-year contracted revenue that competitors cannot easily displace from a standing start.

The security screening segment saw its leading vendor report revenue of GBP 963 million in the financial year ended July 2025, up 12.1% from GBP 859 million in FY2024, per Financial Times market data, before agreeing to a sale valuing the business at GBP 2.0 billion at a 16.3x operating profit multiple in December 2025. A private equity acquisition at this valuation multiple signals that sophisticated capital markets view radiation detection as a high-quality recurring-revenue business with defensible government contract relationships. IBA reported net sales of EUR 498.2 million in FY2024, up 7% from EUR 466.7 million in FY2023, with equipment order intake up 11% year-over-year and backlog stable at an all-time high of EUR 1.5 Billion, confirming that hospital capital cycles for radiation therapy equipment remain robust and sustain ancillary dosimetry procurement well into the late 2020s.

Company Profiles

Thermo Fisher Scientific holds a strategically important position across both government defense and commercial medical markets. In May 2026, Thermo Fisher launched the PackEye XS Radiation Detection Backpack, a next-generation covert radiation detection, identification, and assessment system for field security and emergency response applications, demonstrating active investment in portable detection platforms that expand its addressable market beyond fixed and institutional systems into field security applications where incumbent vendors have limited product presence.

Mirion Technologies, Inc. is the market's most strategically aggressive operator, combining organic SMR instrumentation growth with transformative M&A. Q1 2026 total revenue reached USD 258 million, up 28% year-over-year, with SMR-related orders reaching USD 85 million across Q1 2026 and April 2026 combined and a USD 1.1 Billion backlog providing multi-year revenue visibility that most competitors cannot match.

Key Players

- Thermo Fisher Scientific

- Mirion Technologies, Inc.

- Fortive Corporation

- Fuji Electric Co., Ltd.

- Ludlum Measurements, Inc.

- Arktis Radiation Detectors Ltd

- Landauer, Inc.

- Centronic Limited

- Radiation Monitoring Devices, Inc.

- SE International Inc.

- Amray Radiation Protection

Supply Chain and Value Chain Analysis

The radiation detection and monitoring value chain begins with specialized raw material and component suppliers providing scintillator crystals, semiconductor substrates including CdZnTe and silicon carbide, photomultiplier tubes, and gas-filled detector housings. These materials require highly controlled manufacturing environments and limited global supply bases. Detector fabrication represents the highest-value-add step in the chain, where proprietary performance differentiation is established and market leaders invest most heavily in R&D to maintain product advantages that command premium pricing and long qualification cycles from buyers.

System integration and calibration assembles detector components into complete monitoring platforms, where nuclear safety certification creates switching cost barriers that protect revenue once a system is installed. Paragon Energy Solutions' embedded presence across 100% of North American reactors, now part of Mirion Technologies following the December 2025 acquisition, illustrates how certification at this layer creates captive revenue streams.

Bertin Technologies structures approximately one-third of its 208 VF Nuclear employees as permanently seconded to four Central European nuclear plants at Dukovany, Temelin, Mochovce, and Jaslovske Bohunice, converting installation presence into long-term service contracts that are effectively insulated from competitive retendering. France's SISERI system centralizes dosimetric data for 386,080 workers monitored in 2022, with vendors providing both hardware and regulatory data reporting platforms capturing a second recurring revenue stream beyond equipment sales that grows in strategic importance as AI-enabled analytics create opportunities for predictive monitoring as a differentiated service offering.

Regulatory Landscape

The IAEA establishes the foundational international framework governing radiation monitoring across all sectors. Its 2025 Nuclear Technology Review highlighted new reactor builds including Russia's Kola NPP test facility, confirming that the agency's oversight remit is expanding alongside the global reactor construction pipeline. National regulators in 31 operating countries must continuously update their domestic adoption of IAEA standards as new reactor configurations, including SMRs enter commissioning phases that existing regulatory frameworks were not originally designed to cover.

NIST's Documentary Standards project, updated April 10, 2025, develops national performance standards for X-ray and gamma-ray screening equipment across checkpoint, cargo, vehicle, and whole-body applications serving TSA, FPS, DNDO, and CBP as primary DHS customers. Vendors supplying U.S. government screening programs must meet these evolving NIST benchmarks as a procurement qualification requirement that functions as a market entry filter for non-certified competitors.

Investment and White Space Analysis

Investment is concentrated in two high-conviction areas: SMR instrumentation and medical dosimetry compliance infrastructure. Mirion Technologies SMR-related revenue is expected to exceed 3% of total company revenue by year-end 2026, confirming that SMR instrumentation has moved beyond pilot stage into commercial procurement where early-positioned vendors are converting first-mover advantage into multi-year backlog that competitors cannot easily displace.

The environmental radiation monitoring segment represents a white space where investment lags behind regulatory and infrastructure demand. The EU Digital Decade national roadmaps committed EUR 288.6 Billion in 2025, funding cross-border sensor networks including environmental radiation monitoring nodes, with ML-optimized sensor networks achieving R2 scores of 0.95 versus 0.85 for conventional layouts and RMSE 30% lower. Vendors offering AI-integrated environmental monitoring platforms aligned with EU digital infrastructure standards can access government procurement channels that bypass traditional nuclear utility procurement cycles entirely.

Asia Pacific presents the highest-growth regional white space, with India's nuclear capacity target of 100,000 megawatts by 2047 compared to its current 8,180 megawatts implying a more than tenfold expansion requiring proportional radiation monitoring infrastructure at every new installation. Personal dosimetry services for the mid-market industrial workforce represent an underserved segment with recurring revenue characteristics. Approximately 52% of the 24 million monitored workers globally are exposed to natural radiation sources, with many employed in industrial radiography, oil and gas, and construction sectors where dosimetry compliance infrastructure is less mature than in nuclear or medical settings. Mirion's backlog reached USD 1.1 Billion in Q1 2026, up 38% including acquisitions and 19% excluding M&A, representing multi-year contracted revenue that pre-occupies customer procurement budgets and means new entrants must target greenfield SMR builds, environmental monitoring networks, and industrial dosimetry as entry points rather than attempting to displace embedded vendors in operating reactor fleets where relationships span up to 60 years under Japan's life-extension framework.

Recent Developments

- December 2025: Smiths Detection. Acquisition Agreed. Reached an agreed sale to CVC Capital Partners at an enterprise valuation of GBP 2.0 Billion, representing a 16.3x headline operating profit multiple, signaling high institutional conviction in radiation detection as a recurring-revenue government contract business.

- October 2025: SPC Doza. Product Launch. Launched a dedicated SMR monitoring suite featuring continuous air and environmental sensors, marking the first commercially available monitoring platform purpose-built for the SMR reactor format.

- September 2025: Mirion Technologies. Acquisition Agreement. Announced a definitive agreement to acquire Paragon Energy Solutions from Windjammer Capital Investors for approximately USD 585 million in cash, targeting expansion in nuclear power and SMR instrumentation markets.

- August 2025: Kromek Group. Defense Award. Announced a new biosecurity award from the UK MoD's Defence Science and Technology Laboratory along with additional CBRN orders totaling approximately GBP 860,000, broadening its defense detection contract base.

- July 2025: Kromek Group. Government Contract. Won a GBP 1.7 million contract under a UK Government Framework, with revenue expected to be mostly recognized within the current financial year, reinforcing its position in government-backed detection programs.

Report Details

| Report Characteristics |

| Market Value (2025) |

USD 4.6 Billion |

| Market Value (2026) |

USD 5.1 Billion |

| Forecast Revenue (2035) |

USD 13.6 Billion |

| CAGR (2026 to 2035) |

11.4% |

| Base Year for Estimation |

2025 |

| Historic Period |

2020 to 2024 |

| Forecast Period |

2026 to 2035 |

| Report Coverage |

Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered |

By Product Type (Detection and Monitoring Solutions, Safety Equipment, Personal Dosimeters, Area Process Monitors, Environmental Radiation Monitors, Surface Contamination Monitors, Radioactive Material Monitors), By Detector/Technology Type (Scintillation Systems, Gas-Filled Detectors, Solid State/Semiconductor Detectors, Photographic Film), By End-User/Industry Vertical (Medical and Healthcare, Industrial, Homeland Security and Defense, Energy and Power/Nuclear Power Plants, Research and Academia, Environmental Monitoring), By Deployment (Fixed/Installed Systems, Portable/Handheld Systems, Wearable/Personal Systems) |

| Regional Analysis |

North America (US and Canada), Europe (Germany, France, The UK, Spain, Italy, and Rest of Europe), Asia Pacific (China, Japan, South Korea, India, Australia, and Rest of APAC), Latin America (Brazil, Mexico, and Rest of Latin America), Middle East & Africa (GCC, South Africa, and Rest of MEA) |

| Competitive Landscape |

Thermo Fisher Scientific, Mirion Technologies Inc., Fortive Corporation, Fuji Electric Co. Ltd., Ludlum Measurements Inc., Arktis Radiation Detectors Ltd, Landauer Inc., Centronic Limited, Radiation Monitoring Devices Inc., SE International Inc., Amray Radiation Protection |

| Customization Scope |

Customization for segments and region or country level will be provided. Additional customization can be done based on requirements. |

| Purchase Options |

Three license options: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited Users and Printable PDF) |

Frequently Asked Questions

What is the biggest investment opportunity in Radiation Detection and Monitoring Market?

▾ SMR instrumentation represents the clearest near-term opportunity, with Mirion Technologies' SMR-related revenue expected to exceed 3% of total company revenue by year-end 2026. Environmental radiation monitoring aligned with the EU's EUR 288.6 Billion Digital Decade roadmap and industrial mid-market dosimetry for the underserved portion of the 24 million globally monitored workforce represent the two highest-potential white spaces beyond the nuclear utility tier.

Who are the top companies in Radiation Detection and Monitoring Market?

▾ Leading companies include Thermo Fisher Scientific, Mirion Technologies Inc., Fortive Corporation, Fuji Electric Co. Ltd., Ludlum Measurements Inc., Arktis Radiation Detectors Ltd, Landauer Inc., Centronic Limited, Radiation Monitoring Devices Inc., SE International Inc., and Amray Radiation Protection. Mirion Technologies leads in nuclear instrumentation with a backlog of USD 1,104.3 million at December 31, 2025.

Which segment is growing fastest in Radiation Detection and Monitoring Market and why?

▾ Solid State and Semiconductor Detectors are gaining share fastest within technology type due to superior energy resolution in compact form factors. Energy and Power/Nuclear Power Plants represent the fastest-growing end-user segment in absolute revenue terms, with China's nuclear power investment reaching a record CNY 146.9 Billion in 2024 and more than 30 reactors under construction adding approximately 34,000 megawatts.

Which region is growing fastest in Radiation Detection and Monitoring Market and why?

▾ Asia Pacific is the fastest-structurally-expanding region, driven by China and India's nuclear build programs. India targets 100,000 megawatts of nuclear capacity by 2047 against a current base of 8,180 megawatts, implying a more than tenfold expansion requiring proportional radiation monitoring infrastructure investment at every new installation across the forecast period.

What is the biggest challenge holding Radiation Detection and Monitoring Market back?

▾ Multi-jurisdictional regulatory approval cycles lengthen product commercialization timelines as IAEA standards require country-level adoption before monitoring devices can be deployed. High capital costs for nuclear-grade detection hardware, as identified in Mirion Technologies' FY2024 10-K filing, concentrate market access among large tier-1 operators and constrain penetration among smaller utilities, research institutions, and emerging-market facilities that cannot absorb full compliance infrastructure costs without government grant support.