Market Overview

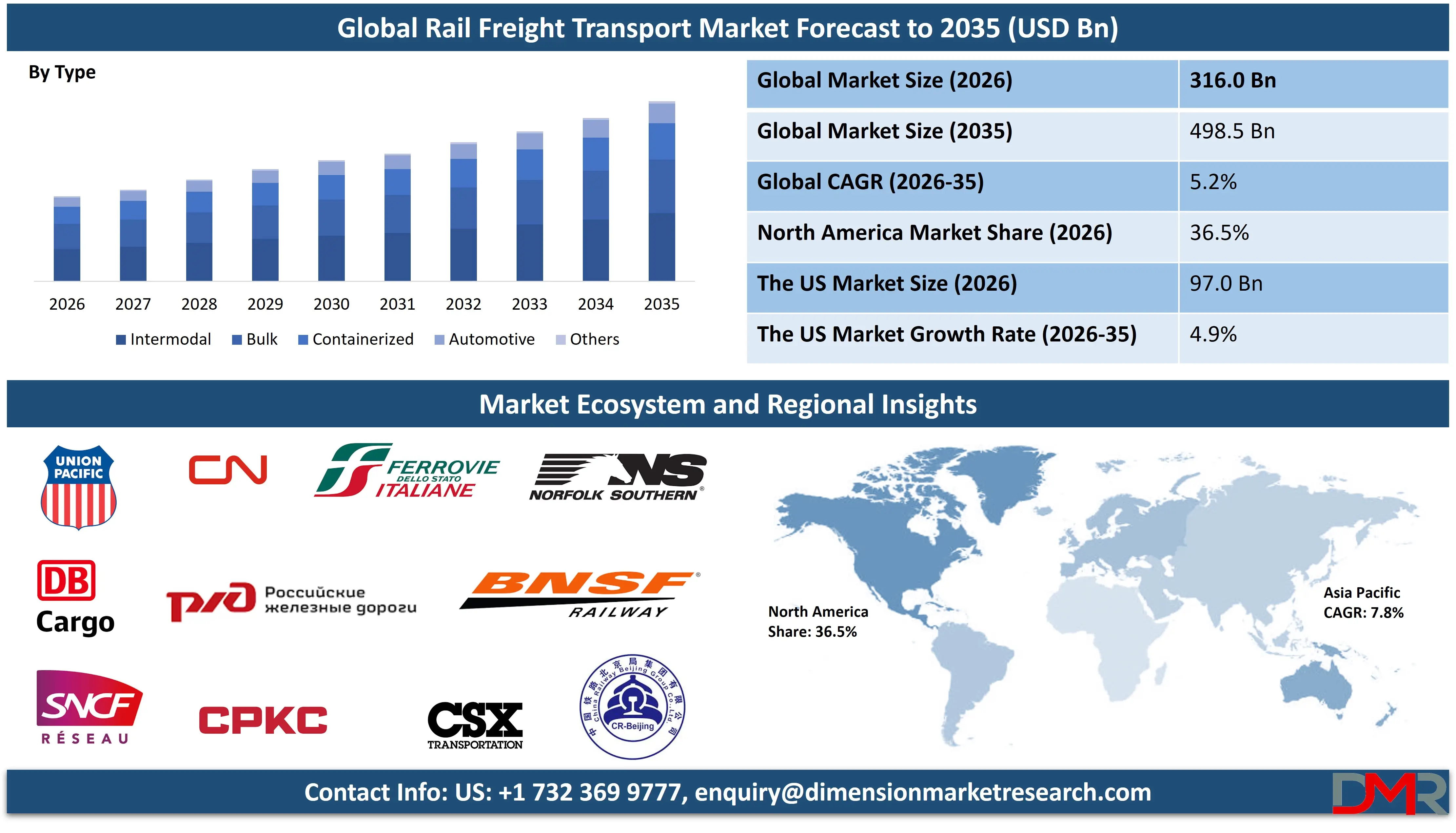

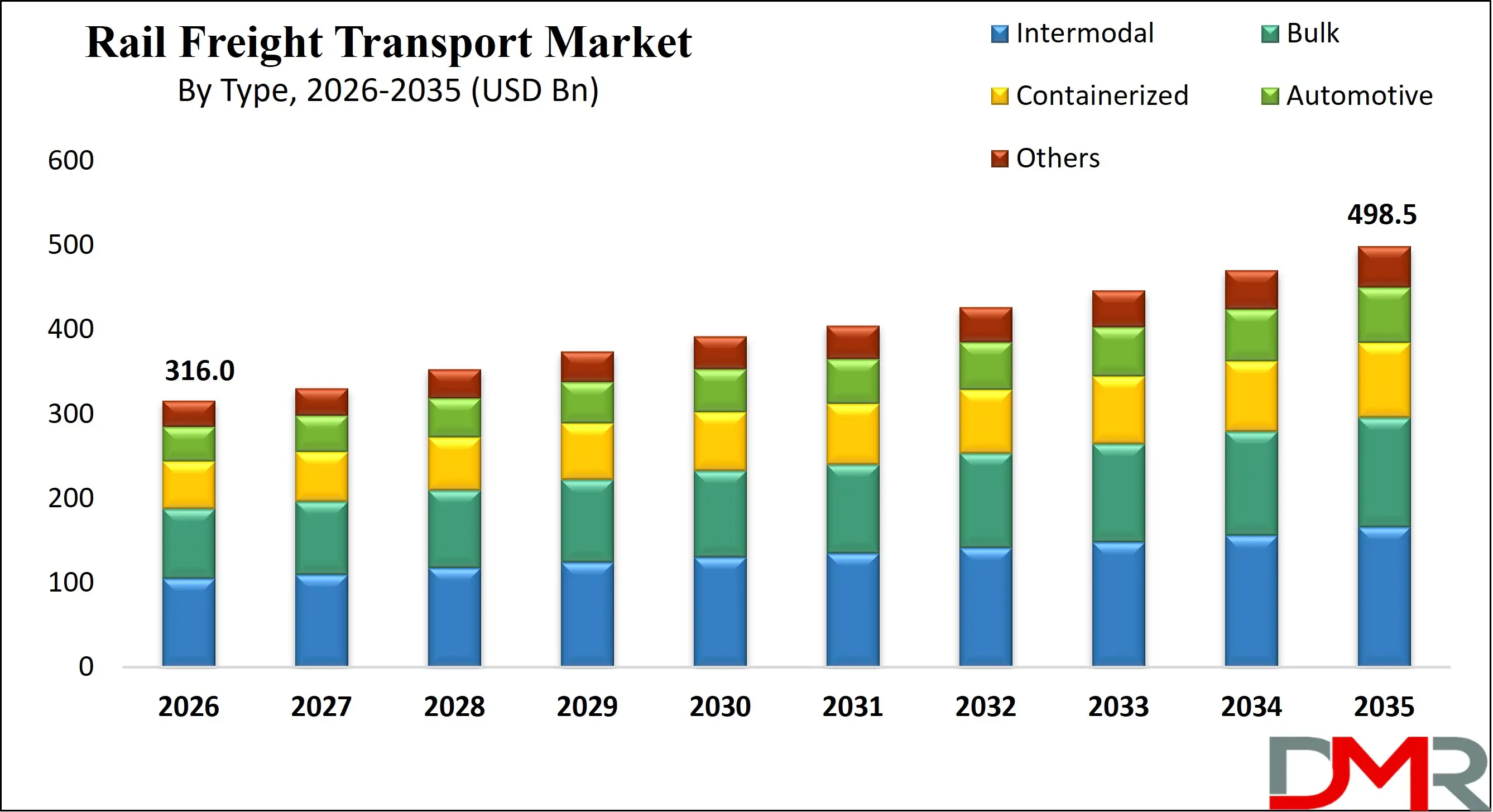

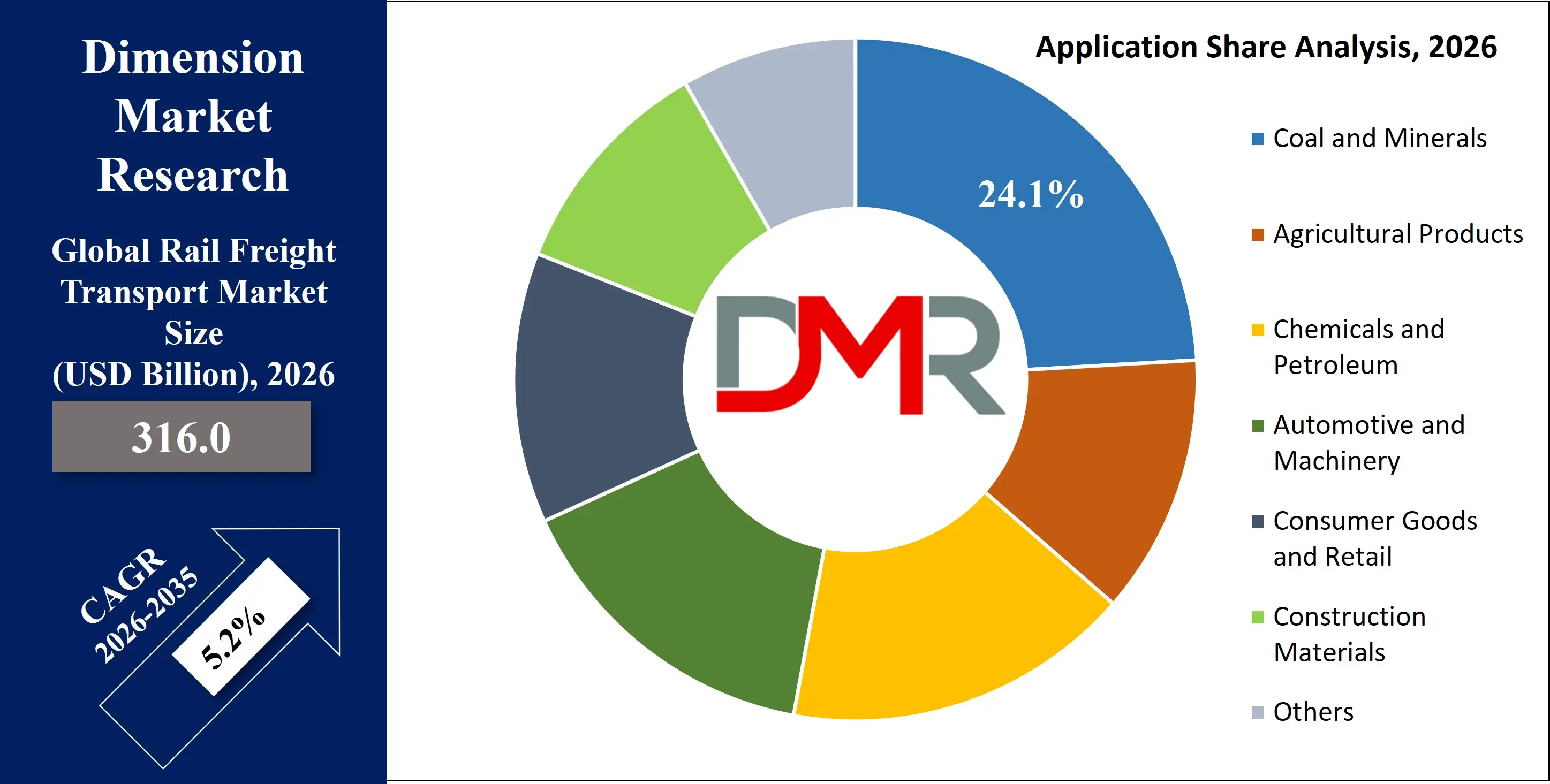

The Global Rail Freight Transport Market is projected to reach USD 316.0 billion in 2026 and is expected to grow at a CAGR of 5.2% from 2026 to 2035, attaining a value of USD 498.5 billion by 2035. The market's steady growth is driven by the increasing global demand for efficient, cost-effective, and sustainable bulk commodity transport, combined with the strategic shift toward decarbonizing logistics and strengthening supply chain resilience.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Rail freight enables the high-volume, long-distance movement of goods through automated yards, digital freight management, and integrated intermodal terminals, supporting industries in landlocked and remote regions where road infrastructure is congested or underdeveloped. The model addresses global challenges related to carbon emissions from transport and helps reduce logistics costs through optimized routing and scale.

Technological advancements, including automated train operations (ATO), Internet of Things (IoT) sensors, predictive maintenance AI, blockchain-enabled logistics, digital twin networks, and 5G-connected rail systems, are transforming the market into a smarter, more efficient, and highly integrated logistics backbone. Integration of machine learning algorithms for demand forecasting, fleet optimization, and dynamic pricing is reshaping operational economics.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Growing government initiatives promoting rail-centric freight corridors, green logistics policies, and public-private infrastructure investments further accelerate global adoption. However, barriers such as limited interoperability between national rail networks, high upfront capital costs, aging infrastructure in certain regions, and regulatory fragmentation remain. Despite these limitations, the convergence of digitalization, automation, and sustainability mandates positions rail freight as a central pillar of global supply chain modernization through 2035.

The US Rail Freight Transport Market

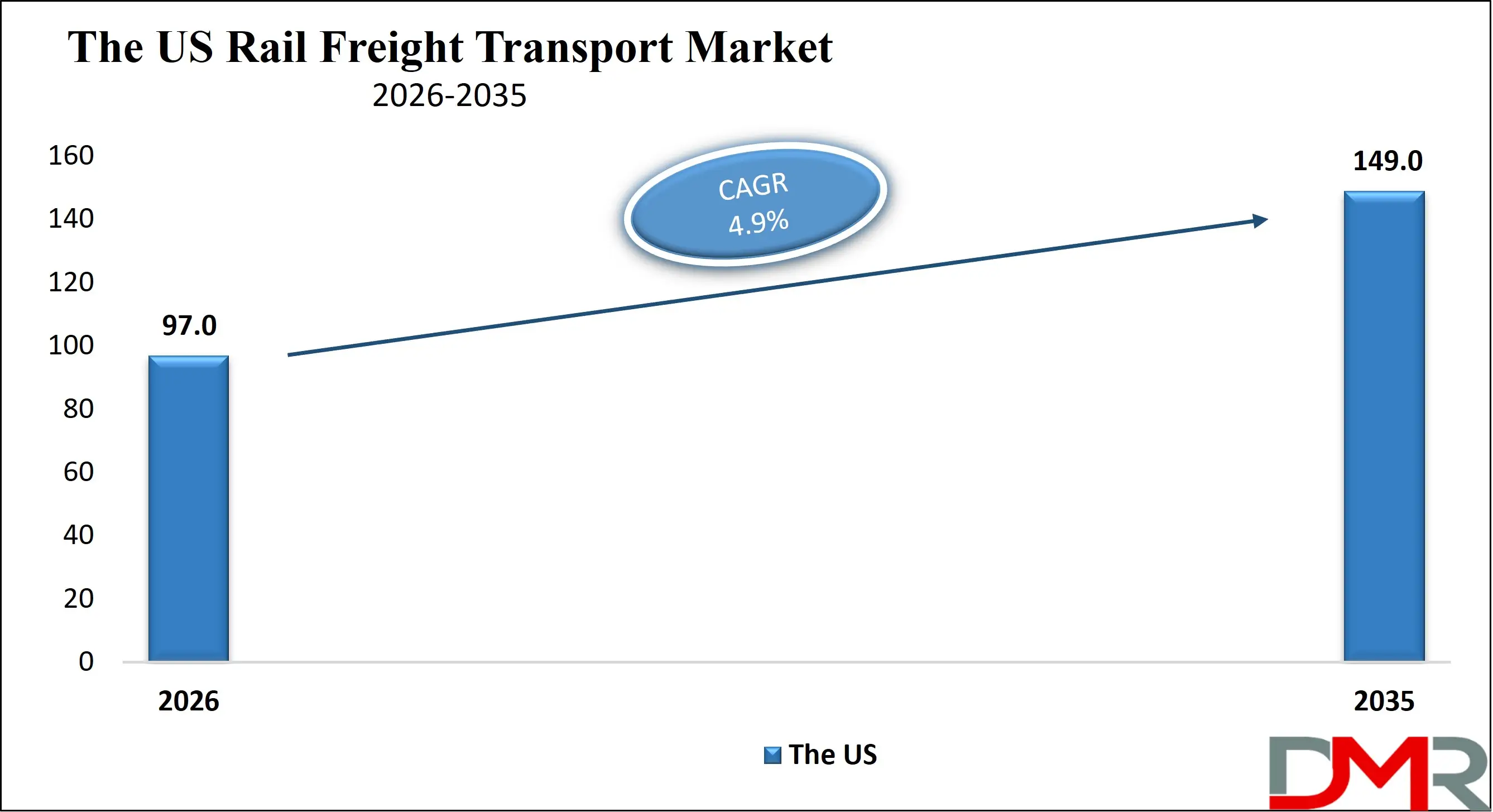

The U.S. Rail Freight Transport Market is projected to reach USD 97.0 billion in 2026 and grow at a CAGR of 4.9%, reaching USD 149.0 billion by 2035. The U.S. leads global volume due to its extensive rail network, dominance in bulk commodity transport, and large-scale intermodal integration with ports and trucking.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Major Class I railroads including Union Pacific, BNSF, CSX, and Norfolk Southern drive market growth through heavy investments in double-stack container corridors, precision scheduled railroading (PSR), and digital dispatch systems. The transport of coal, grains, chemicals, and intermodal containers constitutes the core revenue segments. Government support through the Bipartisan Infrastructure Law funds rail modernization, bridge upgrades, and congestion reduction projects.

The rapid rise of intermodal freight, fueled by e-commerce growth and port-to-hub efficiency, continues to redefine the U.S. logistics landscape. Integration of AI-driven predictive analytics for rolling stock health and automated classification yards further strengthens the country's leadership in technologically advanced freight rail operations.

The Europe Rail Freight Transport Market

The Europe Rail Freight Transport Market is projected to be valued at approximately USD 78.3 billion in 2026 and is projected to reach around USD 121.9 billion by 2035, growing at a CAGR of about 5.1% from 2026 to 2035. Europe's growth is anchored by strong EU policy support for modal shift from road to rail, cross-border rail interoperability initiatives, and Green Deal targets for transport decarbonization.

Countries such as Germany, France, Poland, Italy, and the Netherlands lead in rail freight volumes, driven by automotive, chemical, and intermodal flows. The EU's Trans-European Transport Network (TEN-T) and Digital Rail initiatives aim to enhance corridor capacity, standardize signaling (ERTMS), and streamline border crossings. Major operators like DB Cargo, SNCF, PKP Cargo, and Mercitalia are deploying digital freight platforms and electrified fleets.

Europe’s strong regulatory push for sustainable logistics, combined with road congestion and driver shortages, further drives rail freight uptake. Investment in combined transport terminals, dual-mode locomotives, and automated rail operations supports the region's position as an advanced and integrated rail freight market.

The Japan Rail Freight Transport Market

The Japan Rail Freight Transport Market is projected to be valued at USD 8.9 billion in 2026. It is further expected to witness subsequent growth in the upcoming period, holding USD 13.7 billion in 2035, expanding at a CAGR of 4.2% during the forecast period.

The Japanese market is characterized by a highly disciplined and efficient system, operating within the unique geographic constraints of a mountainous archipelago. Rail freight faces intense competition from an exceptionally developed and efficient domestic coastal shipping network and an extensive road haulage system. As a result, its primary strength lies in specialized, high-value, and scheduled freight services, particularly on key trunk lines linking major industrial hubs like the Tokyo-Nagoya-Osaka corridor.

The market is driven by a strategic focus on intermodal transport to combat severe truck driver shortages and to support national environmental targets under Japan's Green Growth Strategy. The government actively promotes a modal shift from road to rail and sea through the Act on Promotion of Modal Shift in Freight Transportation. Major operators, led by Japan Freight Railway Company (JR Freight), are investing in advanced technologies such as Automated Gate Systems (AGS), GPS-enabled fleet management, and dedicated double-stack container trains to improve reliability and capacity.

Global Rail Freight Transport Market: Key Takeaways

- Steady Global Market Growth Outlook: The Global Rail Freight Transport Market is expected to be valued at USD 316.0 billion in 2026 and is projected to reach USD 498.5 billion by 2035, showcasing consistent expansion supported by global trade recovery, commodity demand, and modal shift policies.

- Moderate CAGR Driven by Sustainability and Digitalization: The market is expected to grow at a CAGR of 5.2% from 2026 to 2035, fueled by green logistics mandates, rail digitalization, intermodal integration, and rising cost competitiveness versus road transport.

- Strong Growth Trajectory in the United States: The U.S. Rail Freight Transport Market stands at USD 97.0 billion in 2026 and is projected to reach USD 149.0 billion by 2035, expanding at a CAGR of 4.9% due to robust intermodal growth and network optimization.

- Asia-Pacific Exhibits Highest Growth Potential: The Asia-Pacific region is expected to achieve the highest CAGR, driven by large infrastructure projects in China, India, and Southeast Asia, rising industrial output, and government-led rail corridor development.

- Technological Modernization Reshapes Operations: Innovations including automated train operations, IoT-based asset monitoring, AI-powered predictive maintenance, and digital freight platforms are significantly improving efficiency, reliability, and capacity utilization.

- Rising Focus on Supply Chain Resilience Boosts Adoption: Post-pandemic supply chain reconfiguration, coupled with volatility in fuel prices and road transport capacity, is driving sustained demand for reliable, high-capacity, and cost-stable rail freight solutions.

Global Rail Freight Transport Market: Use Cases

- Intermodal Container Transport: Seamless movement of shipping containers between ports, rail hubs, and inland terminals, reducing road congestion and enabling long-haul efficiency.

- Bulk Commodity Haulage: High-volume transport of coal, grains, ores, and chemicals from mines and farms to processing plants and ports via dedicated heavy-haul networks.

- Automotive Logistics: Finished vehicle transport via specialized multilevel railcars, supporting just-in-time delivery from manufacturing plants to regional distribution centers.

- Cross-Block Train Operations: Regular scheduled long-distance container trains between continental economic zones, such as China-Europe rail services.

- Cold Chain Rail Logistics: Temperature-controlled transport of perishable goods (food, pharmaceuticals) using refrigerated railcars with real-time monitoring.

Global Rail Freight Transport Market: Stats & Facts

- The International Energy Agency (IEA) states that rail accounts for only 2% of transport energy use while moving 8% of global freight, underscoring its superior energy efficiency and critical role in decarbonizing logistics.

- The International Union of Railways (UIC) reports that over 70% of global rail freight ton-kilometers are hauled by just five countries (USA, China, Russia, India, and Canada), highlighting market concentration in large, resource-rich economies.

- The U.S. Department of Transportation notes that one freight train can carry the load of several hundred trucks, reducing highway wear, congestion, and emissions, validating rail as essential infrastructure for scalable, sustainable freight mobility.

- The European Environment Agency (EEA) notes rail freight emits approximately 75% less CO2 per ton-km than road haulage, intensifying policy support for modal shift under the European Green Deal.

- According to Global Rail Industry Surveys, digital freight management platforms are growing over 25% annually across major networks, as systems like RailData and CargoSmart optimize asset utilization where 30–40% of wagon capacity is often underused.

- The World Bank reports over 50% of landlocked developing countries lack integrated rail connectivity, causing high trade costs; rail freight corridor development mitigates this by enabling efficient port access for hundreds of millions in underserved regions.

Global Rail Freight Transport Market: Market Dynamic

Driving Factors in the Global Rail Freight Transport Market

Sustainability and Decarbonization Policies

Stringent global and regional carbon reduction targets are a major driver for modal shift from road to rail. Governments are implementing carbon pricing, road freight restrictions, and incentives for low-emission transport. Rail’s inherent energy efficiency and increasing electrification make it a cornerstone of green logistics strategies, boosting demand for rail freight services. Corporate sustainability goals are also pushing shippers to choose rail to reduce their Scope 3 emissions.

Technological Modernization and Digitalization

Rail freight benefits from rapid progress in automation, IoT, AI, and data analytics. Automated train operations, predictive maintenance systems, smart sensors, and digital freight platforms enhance operational efficiency, asset utilization, and service reliability. Integration with intermodal logistics through single digital windows reduces delays and improves customer visibility. Technologies like digital twins allow operators to simulate and optimize network performance before implementing changes in the real world.

Economic Efficiency and Scale for Bulk Haulage

For heavy, dense, and non-time-sensitive commodities transported over long distances, rail remains the most cost-effective land mode. The economies of scale achieved with unit trains and the lower fuel consumption per ton-mile provide a significant cost advantage over trucking, especially in markets like North America and Australia for coal, grain, and mineral transport.

Restraints in the Global Rail Freight Transport Market

High Capital Intensity and Infrastructure Gaps

Developing and maintaining rail infrastructure requires significant long-term investment. Many regions face challenges with aging tracks, limited electrification, and lack of last-mile connectivity. Interoperability issues between different national rail systems also hinder seamless cross-border freight movement, restricting market growth in fragmented regions. The capital required for new locomotives, wagons, and terminal equipment presents a high barrier to entry and expansion.

Regulatory and Competitive Fragmentation

The rail freight market is subject to varying national regulations, safety standards, and operational rules. Incumbent operators, new entrants, and state-owned entities often face uneven competitive landscapes. Moreover, intense competition from road transport on shorter routes and for time-sensitive goods pressures rail’s market share and pricing. In some regions, legacy labor agreements and complex access charges can also impede operational flexibility and cost competitiveness.

Last-Mile Connectivity Challenges

Rail is inherently a line-haul solution. The "first and last mile" often requires trucking, which adds cost, time, and complexity. The lack of sufficient sidings, transloading facilities, and seamless intermodal terminals in certain areas can negate rail's line-haul advantages, making door-to-door service less attractive compared to all-road alternatives.

Opportunities in the Global Rail Freight Transport Market

Expansion of International Rail Corridors

Development of transnational rail corridors such as the China-Europe Railway Express, the International North–South Transport Corridor, and Africa’s Trans-African Railway network creates major growth opportunities. These corridors enhance trade connectivity, reduce transit times compared to sea freight, and offer a reliable alternative to air and road for continental logistics. They also open new markets for rail operators and logistics providers.

Growth of Intermodal and Combined Transport

The rise of e-commerce and containerization fuels demand for integrated intermodal solutions. Expansion of inland container depots, rail-road terminals, and port-rail links enables seamless door-to-door logistics. Investments in standardized loading units and digital documentation present significant opportunities for rail to capture a larger share of the global containerized freight market, particularly in the medium-to-long-haul segment.

Adoption of Alternative Fuel Locomotives

The development and deployment of locomotives powered by batteries, hydrogen fuel cells, or biofuels present a significant opportunity to decarbonize rail freight further, especially on non-electrified or partially electrified lines. This can reduce dependence on diesel, lower operating costs, and enhance rail's environmental value proposition.

Trends in the Global Rail Freight Transport Market

Digital Freight Platforms and Integration

Cloud-based digital platforms are becoming central to rail freight operations, offering real-time tracking, capacity matching, automated billing, and integration with other transport modes. These platforms enhance transparency, optimize network planning, and improve customer engagement, driving the digital transformation of traditional rail logistics. The trend is toward creating one-stop digital marketplaces for rail capacity.

Automation and Autonomous Rail Operations

The industry is progressively adopting higher levels of automation, from automated yards and robotic inspection to mainline autonomous train operations (ATO Grades 2-4). These technologies reduce human error, increase network capacity and safety, and lower operational costs, positioning rail freight for a more competitive and efficient future. Trials of fully autonomous freight trains are already underway in several countries.

Sustainability-Linked Financing and Partnerships

There is a growing trend of green bonds and sustainability-linked loans being used to finance rail freight infrastructure and rolling stock. Furthermore, strategic partnerships between rail operators, ports, shipping lines, and major shippers are forming to create end-to-end green logistics corridors, with rail as the central low-carbon pillar.

Global Rail Freight Transport Market: Research Scope and Analysis

By Type Analysis

Intermodal Rail Freight is projected to dominate the global market due to its alignment with global containerized trade growth, e-commerce logistics, and port-hinterland connectivity. It involves the efficient transfer of standardized containers between ships, trucks, and trains. This segment benefits from strong investment in dedicated intermodal corridors, double-stack networks, and terminal automation. Its scalability and efficiency in moving consumer goods over long distances secure its leading market position through 2035. The growth of e-commerce, which requires reliable movement of a high volume of smaller shipments consolidated into containers, is a primary tailwind for this segment.

Bulk Rail Freight ranks as the second-largest type segment, essential for transporting high-volume, low-value commodities like coal, minerals, grains, and chemicals. Its dominance is tied to the continuous demand from energy, mining, and agricultural sectors, particularly in large economies such as the U.S., China, Russia, and Australia. While its growth is steadier and more cyclical, tied to commodity prices, it remains a fundamental revenue pillar for rail operators worldwide. The long-term trend toward renewable energy may pressure coal transport, but demand for other bulk commodities like grains, potash, and metals is expected to remain robust.

By Application Analysis

Coal and Minerals Transport is poised to be the largest application segment, driven by enduring global energy and industrial demand. Rail is the most cost-effective mode for moving massive volumes of coal from mines to power plants and ports. Despite energy transition pressures, coal transport remains a key application, especially in Asia-Pacific and North America, supporting base-load power generation and steel production.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Containerized/Intermodal Goods is the fastest-growing application segment, fueled by manufacturing trade, e-commerce, and the need for reliable, scheduled land transport. The expansion of continental rail services for finished and semi-finished goods ensures this segment's increasing market share and strategic importance. It encompasses a wide range of goods from electronics and retail merchandise to auto parts and machinery.

Agricultural Products constitutes a major and stable application, involving the movement of grains, fertilizers, and foodstuffs from agricultural heartlands to processing centers, ports, and population centers. Rail provides the necessary capacity, especially during harvest seasons, and is critical for national and international food security logistics.

By End User Analysis

Mining and Energy industries are anticipated to dominate as end users due to their reliance on heavy-haul rail for bulk raw material logistics. Rail provides the scale and cost structure necessary for moving commodities from remote extraction sites to processing facilities and export points. This includes coal, metallic ores, crude oil, and liquefied natural gas (where applicable).

Manufacturing and Automotive is the second-largest end-user segment. Rail is critical for moving components, finished vehicles, and industrial products across supply chains. The segment benefits from specialized rolling stock, scheduled train services, and integration with just-in-time production models. Automotive manufacturers are among the most significant customers for finished vehicle transport services.

Agriculture is a core end-user sector, relying on rail for the efficient, large-scale movement of grain, feed, and fertilizer. Railroads provide essential market access for farmers, often through long-term contracts and strategic investments in grain loading facilities.

The Global Rail Freight Transport Market Report is segmented on the basis of the following

By Type

- Intermodal

- Bulk

- Containerized

- Automotive

- Others

By Application

- Coal and Minerals

- Agricultural Products

- Chemicals and Petroleum

- Automotive and Machinery

- Consumer Goods and Retail

- Construction Materials

- Others

By End User

- Mining and Energy

- Manufacturing and Automotive

- Agriculture

- Retail and Consumer Goods

- Chemicals and Pharmaceuticals

- Construction

- Logistics and Freight Forwarding Companies

Impact of Artificial Intelligence in the Global Rail Freight Transport Market

- AI for Predictive Maintenance: AI analyzes sensor data from locomotives and wagons to predict failures before they occur, reducing downtime, extending asset life, and improving fleet availability. This transforms maintenance from schedule-based to condition-based, optimizing costs and reliability.

- Automated Train Operations (ATO): ATO systems enable driver-assist or fully automated train movements, increasing network capacity, optimizing energy consumption, and enhancing safety on dedicated freight corridors. This allows for more precise scheduling and denser train operations.

- Digital Freight Management Platforms: Cloud-based platforms provide end-to-end shipment visibility, automated documentation, dynamic pricing, and capacity management, streamlining operations for operators and customers. They create a digital ecosystem connecting shippers, carriers, and terminals.

- IoT-Based Asset Tracking: IoT sensors on rolling stock and containers provide real-time location, condition (e.g., temperature, shock), and load status, enabling proactive logistics management and security. This data is crucial for high-value, sensitive, or perishable cargo.

- Blockchain for Supply Chain Transparency: Blockchain technology secures and automates waybills, customs documentation, and payments, reducing fraud, delays, and administrative costs in cross-border rail freight. It creates an immutable, shared ledger for all transaction parties.

- Digital Twins for Network Optimization: Virtual replicas of rail networks allow operators to simulate traffic, test scheduling scenarios, and plan infrastructure projects with minimal disruption, leading to better asset utilization and strategic planning.

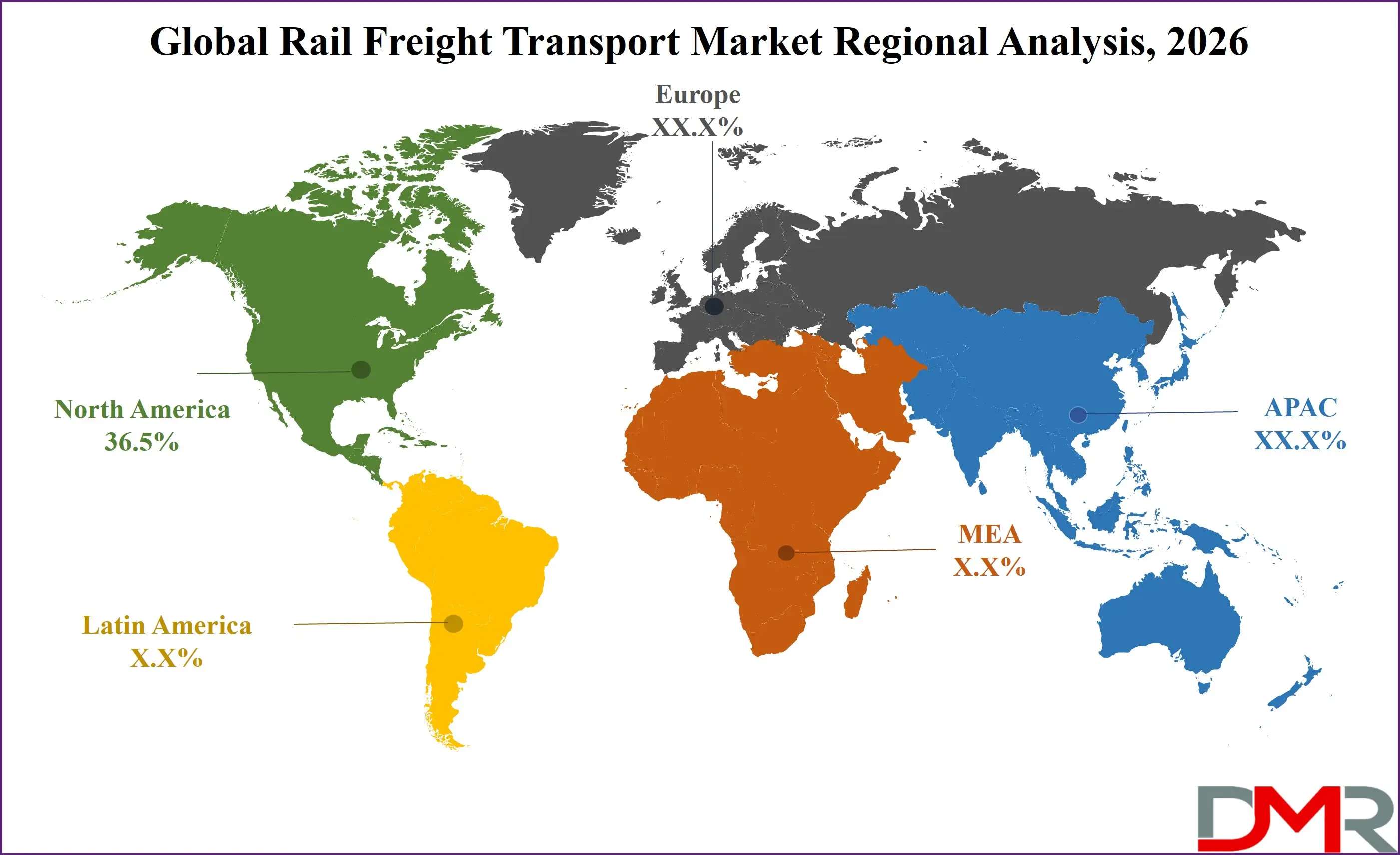

Global Rail Freight Transport Market: Regional Analysis

Region with the Largest Revenue Share

North America is projected to dominate the Global Rail Freight Transport Market with over 36.5% of market share by the end of 2026, owing to its extensive and mature private rail network, dominance in bulk commodity transport, and highly developed intermodal sector. The United States, with its powerful Class I railroads, moves immense volumes of coal, grain, and intermodal containers. Strong regulatory frameworks, significant private investment in network technology, and integration with continental supply chains underpin regional leadership. The market is characterized by long-haul, heavy-weight trains, high asset productivity, and a strong focus on shareholder returns, which drives continuous operational innovation.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Region with the Highest CAGR

Asia-Pacific holds the highest CAGR and is poised for the fastest growth, driven by massive infrastructure investments, rising industrial production, and strategic government rail corridor projects. China's Belt and Road rail links and India's dedicated freight corridor (DFC) program are transforming regional logistics. The large population base, growing middle class, and expansion of manufacturing and trade create enormous, sustained demand for rail freight capacity. Unlike the privately-driven North American model, growth in Asia-Pacific is often state-led, with significant public investment aimed at achieving broader economic and strategic goals, including reducing logistics costs as a percentage of GDP.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Global Rail Freight Transport Market: Competitive Landscape

The Global Rail Freight Transport Market is moderately consolidated, featuring a mix of state-owned operators, private Class I railroads, and niche intermodal/logistics players. Leading operators such as Union Pacific, BNSF Railway, CSX, and Norfolk Southern (North America), DB Cargo, Russian Railways, and SNCF (Europe), and China State Railway Group (Asia) dominate volume and network coverage. Competition varies by region: it is primarily between a few large private carriers in North America, between state-owned and private operators in Europe's open access environment, and is largely state-dominated in many Asian markets.

Technology providers like Siemens Mobility, Alstom, Wabtec, and Hitachi Rail drive innovation in rolling stock, signaling, and digital solutions. Their role is increasingly critical as railroads modernize fleets and control systems. Digital freight platforms and intermodal service integrators such as Hub Group, XPO Logistics, and Deutsche Bahn's DB Schenker are increasingly influential in shaping customer-facing services and multimodal connectivity. They compete by offering seamless, data-rich logistics solutions that abstract the complexity of dealing directly with rail carriers.

The competitive dynamic is evolving from pure asset-based competition to include competition based on digital service quality, sustainability credentials, and reliability. Strategic alliances between operators on international corridors are also a key feature of the competitive landscape.

Some of the prominent players in the Global Rail Freight Transport Market are

- Union Pacific Railroad

- BNSF Railway

- CSX Transportation

- Norfolk Southern Railway

- Canadian National Railway (CN)

- Canadian Pacific Kansas City (CPKC)

- China State Railway Group Co., Ltd. (CR)

- Russian Railways (RZD)

- DB Cargo

- SNCF Réseau / Fret

- Ferrovie dello Stato Italiane (FS)

- Siemens Mobility

- Alstom

- Wabtec Corporation

- Hitachi Rail

- Kawasaki Heavy Industries

- CRRC Corporation

- Hyundai Rotem

- Kuehne+Nagel (Rail Logistics)

- Hub Group

- Other Key Players

Recent Developments in the Global Rail Freight Transport Market

- November 2025: CPKC inaugurated a fully digitized cross-border rail corridor between Canada and the U.S., featuring automated interchange and AI-driven traffic management, significantly reducing transit times for automotive and intermodal freight.

- October 2025: Siemens Mobility and DB Cargo presented a new hybrid diesel-battery locomotive for non-electrified lines, aimed at reducing emissions and fuel costs in European rail freight operations.

- September 2025: CRRC supplied autonomous locomotives for mineral transport, integrating onboard AI for terrain adaptation and convoy operation, marking a step-change in remote area rail freight.

- August 2025: The complete opening of India's 1,500 km Western DFC enhanced connectivity between Delhi and Mumbai ports, doubling average train speed and capacity for containerized and bulk freight.

- July 2025: A consortium of European and Asian rail operators launched a blockchain-based platform to digitize waybills and customs processes for China-Europe rail freight, cutting border crossing times by up to 40%.

- June 2025: Wabtec and Google Cloud extended their collaboration to deploy advanced AI models across North American fleets, aiming to reduce unplanned downtime by 20% through enhanced failure prediction.

- May 2025: A state-of-the-art rail-connected intermodal terminal commenced operations at the Port of Rotterdam, increasing rail-based container handling capacity by 15% and strengthening rail's role in port hinterland logistics.

- April 2025: BNSF unveiled a plan to acquire a fleet of Wabtec FLXdrive battery-electric locomotives for use in yard and local service in California, marking a significant step toward zero-emission switching operations.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 316.0 Bn |

| Forecast Value (2035) |

USD 498.5 Bn |

| CAGR (2026–2035) |

5.2% |

| The US Market Size (2026) |

USD 97.0 Bn |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors, etc. |

| Segments Covered |

By Type (Intermodal, Bulk, Containerized, Automotive, and Others), By Application (Coal and Minerals, Agricultural Products, Chemicals and Petroleum, Automotive and Machinery, Consumer Goods and Retail, Construction Materials, and Others), By End User (Mining and Energy, Manufacturing and Automotive, Agriculture, Retail and Consumer Goods, Chemicals and Pharmaceuticals, Construction, and Logistics and Freight Forwarding Companies) |

| Regional Coverage |

North America – US, Canada; Europe – Germany, UK, France, Russia, Spain, Italy, Benelux, Nordic, Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, Rest of MEA |

| Prominent Players |

Union Pacific Railroad, BNSF Railway, CSX Transportation, Norfolk Southern Railway, Canadian National Railway (CN), Canadian Pacific Kansas City (CPKC), China State Railway Group Co., Ltd. (CR), Russian Railways (RZD), DB Cargo, SNCF Réseau / Fret, Ferrovie dello Stato Italiane (FS), Siemens Mobility, Alstom, Wabtec Corporation, Hitachi Rail, Kawasaki Heavy Industries, CRRC Corporation, Hyundai Rotem, Kuehne+Nagel (Rail Logistics), Hub Group, and Other Key Players |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users), and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days, and 5 analysts working days respectively. |

Frequently Asked Questions

How big is the Global Rail Freight Transport Market?

▾ The Global Rail Freight Transport Market size is estimated to have a value of USD 316.0 billion in 2026 and is expected to reach USD 498.5 billion by the end of 2035

What is the growth rate in the Global Rail Freight Transport Market?

▾ The market is growing at a CAGR of 5.2 percent over the forecasted period of 2026 to 2035.

What is the size of the US Rail Freight Transport Market?

▾ The US Rail Freight Transport Market is projected to be valued at USD 97.0 billion in 2026. It is expected to reach USD 149.0 billion in 2035, growing at a CAGR of 4.9%.

Which region accounted for the largest Global Rail Freight Transport Market?

▾ North America is expected to have the largest market share in the Global Rail Freight Transport Market, with a share of over 36.5% in 2026.

Who are the key players in the Global Rail Freight Transport Market?

▾ Some of the major key players in the Global Rail Freight Transport Market are Union Pacific Railroad, BNSF Railway, CSX Transportation, China State Railway Group, DB Cargo, Siemens Mobility, Alstom, and Wabtec Corporation, among others.