Market Overview

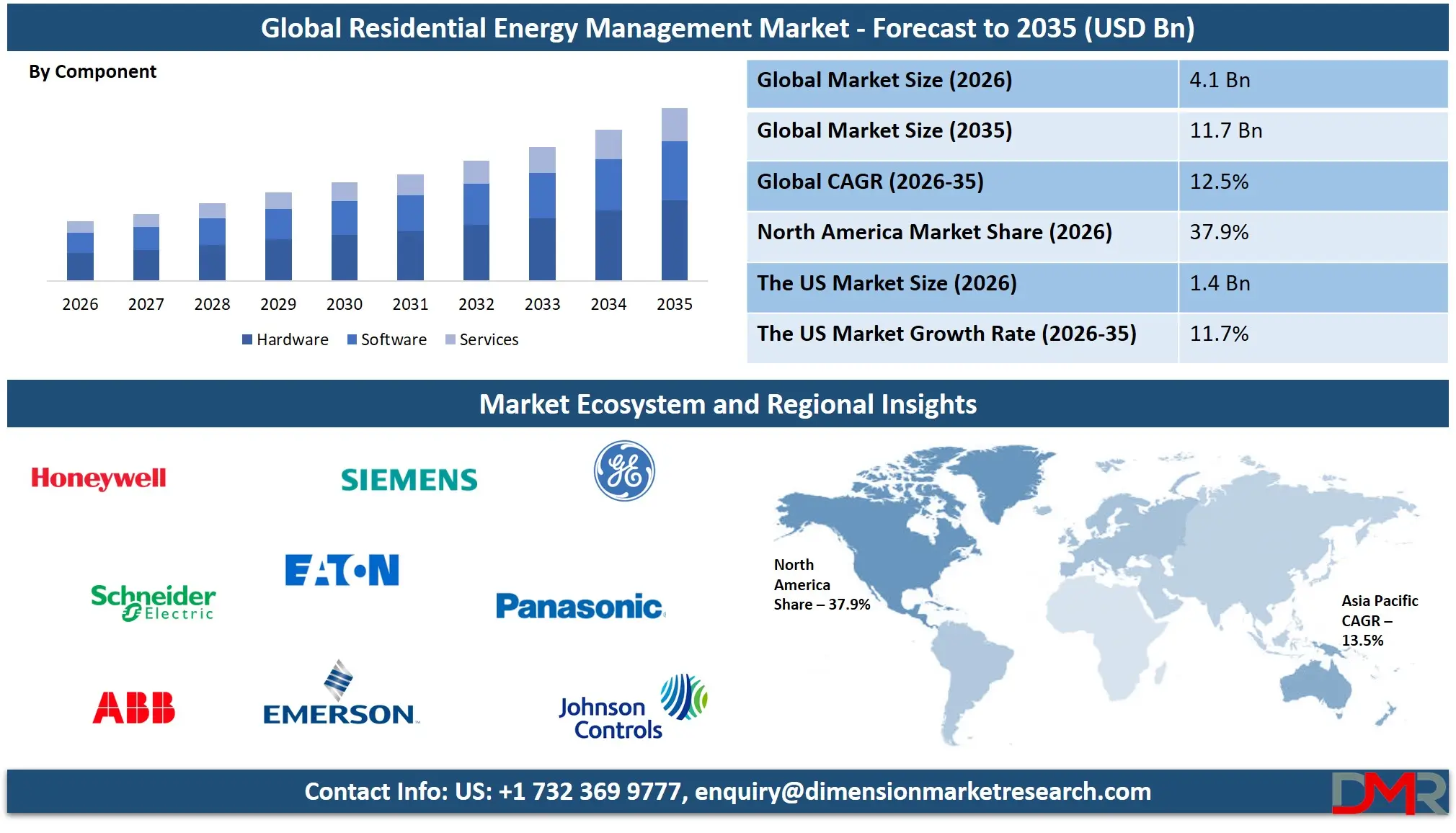

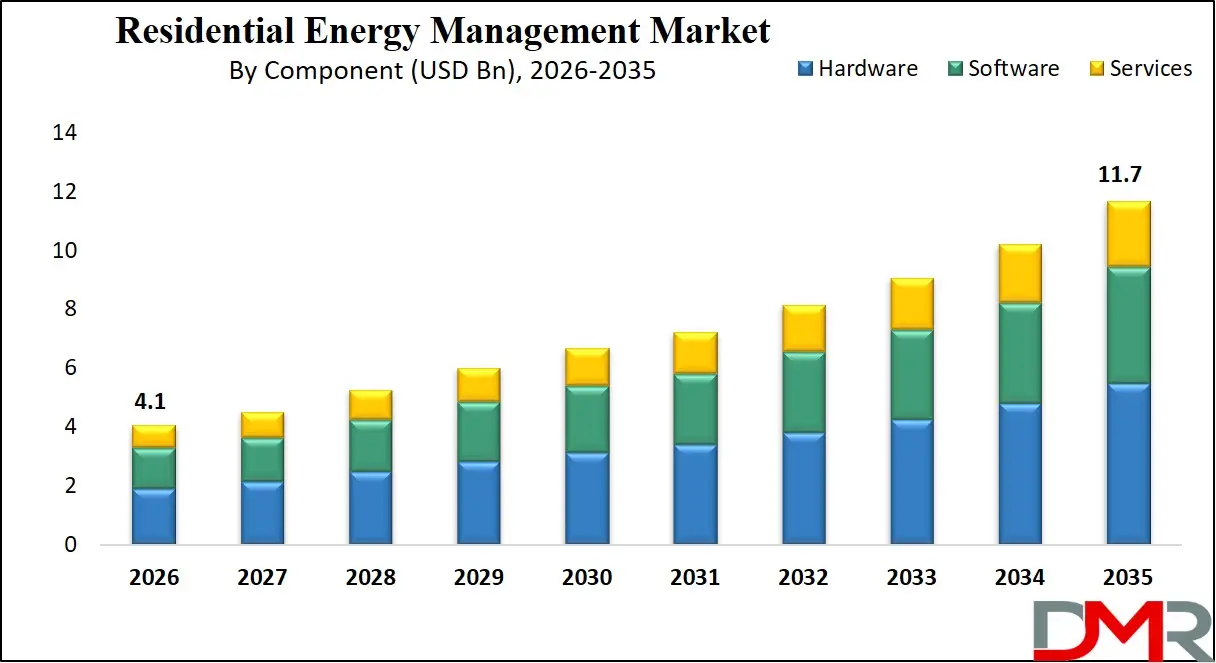

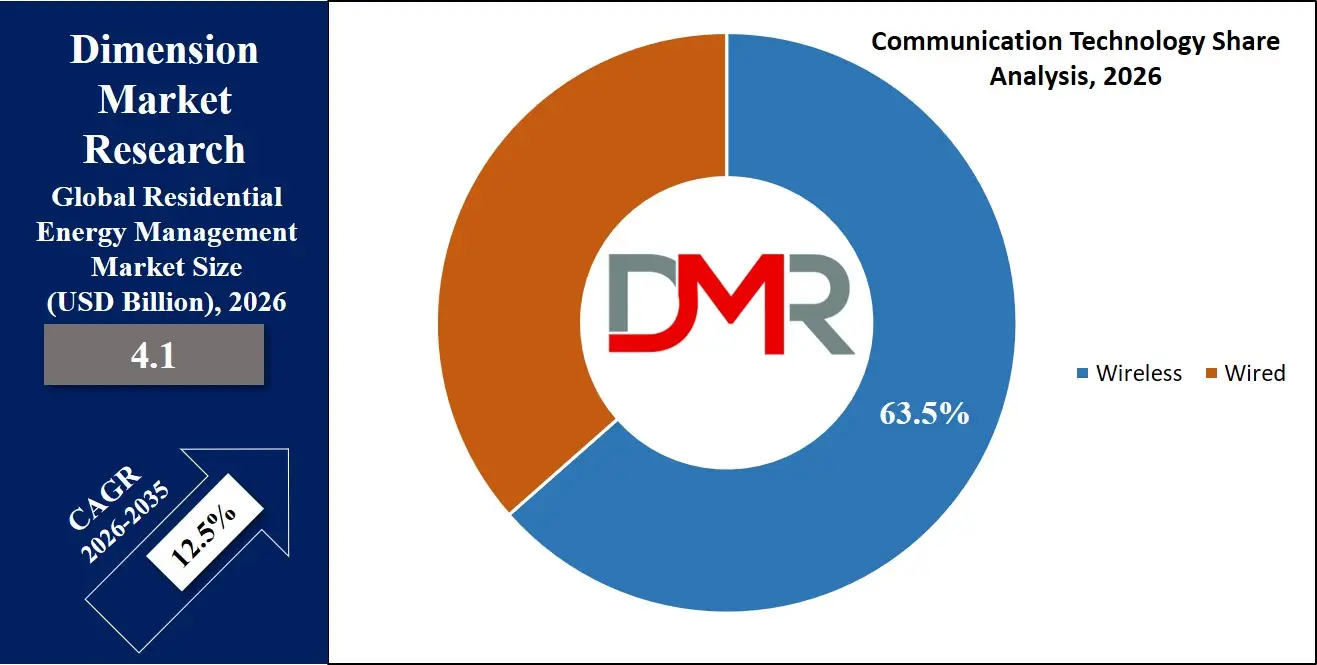

The Global Residential Energy Management Market size is projected to reach USD 4.1 billion in 2026 and grow at a compound annual growth rate of 12.5% to reach a value of USD 11.7 billion in 2035.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Residential Energy Management refers to a set of technologies, systems, and services designed to monitor, control, and optimize energy consumption within households. It integrates hardware devices such as smart meters, thermostats, sensors, and controllers with software platforms that analyze energy usage patterns and enable automated or user-driven control of appliances, lighting, heating, and cooling systems. Communication technologies including wireless protocols, wired connections, and cloud platforms allow seamless interaction between devices, utilities, and homeowners. These systems play a critical role in enhancing energy efficiency, reducing electricity costs, and supporting sustainable energy consumption in residential buildings.

The growing emphasis on energy efficiency and carbon reduction has significantly accelerated the adoption of residential energy management technologies. Smart homes, distributed energy resources such as rooftop solar panels, and electric vehicle charging solutions are reshaping household energy consumption patterns. Digital platforms capable of real-time monitoring and predictive analytics allow homeowners to manage energy use more effectively while supporting grid stability. Utilities and technology providers are also integrating demand response capabilities, enabling residential users to adjust energy consumption during peak demand periods. This shift toward intelligent energy ecosystems is transforming how households interact with power infrastructure.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Recent advancements in smart grid infrastructure, connected devices, and digital energy platforms have strengthened the ecosystem supporting residential energy optimization. Utilities are increasingly deploying smart meters and connected systems that provide detailed consumption data to consumers. Strategic collaborations between technology developers, utilities, and energy service providers have accelerated innovation and integration of renewable energy and storage solutions in homes. Investments in cloud-based energy management platforms and advanced analytics tools are enabling better forecasting, automation, and control, paving the way for smarter and more efficient residential energy networks around the world.

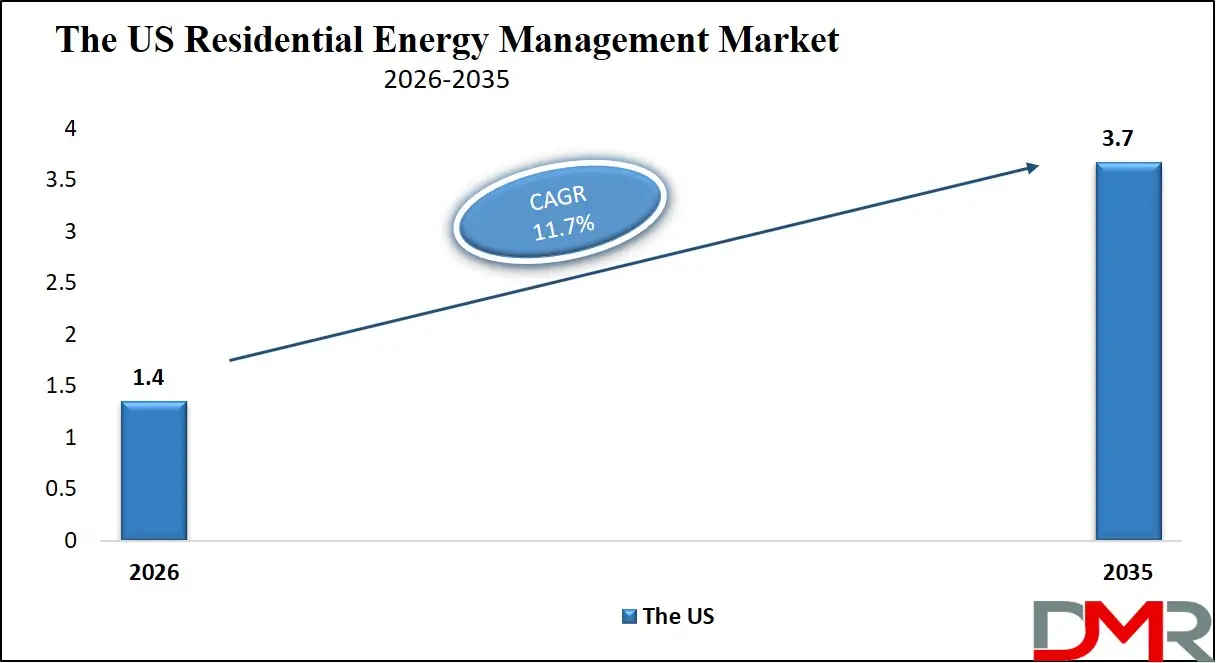

The US Residential Energy Management Market

The US Residential Energy Management Market size is projected to reach USD 1.4 billion in 2026 at a compound annual growth rate of 11.7% over its forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The US residential energy management market is strongly influenced by the rapid adoption of smart home technologies and advanced grid infrastructure. High penetration of smart meters, government initiatives promoting energy efficiency, and increasing residential electricity costs are encouraging homeowners to adopt energy monitoring and control systems. Utilities across the country are implementing demand response programs that incentivize households to adjust energy usage during peak periods. The expansion of rooftop solar installations and residential battery storage is also creating demand for integrated energy management platforms. Additionally, federal and state policies promoting energy efficiency standards and smart grid investments are strengthening the ecosystem for advanced residential energy technologies.

Europe Residential Energy Management Market

Europe Residential Energy Management Market size is projected to reach USD 902.0 million in 2026 at a compound annual growth rate of 11.9% over its forecast period.

Europe demonstrates strong momentum in residential energy optimization due to strict energy efficiency regulations and ambitious climate targets. Regional initiatives such as the European Green Deal and energy performance directives encourage households to adopt smart energy solutions that reduce carbon emissions and improve building efficiency. Smart meters are widely deployed across several European countries, providing real-time consumption data to homeowners. Increasing electricity prices and the growing adoption of renewable energy sources such as rooftop solar panels are further accelerating the integration of residential energy management systems. Digitalization of energy infrastructure and strong government support for energy-efficient buildings continue to foster innovation and large-scale adoption.

Japan Residential Energy Management Market

Japan Residential Energy Management Market size is projected to reach USD 287.0 million in 2026 at a compound annual growth rate of 12.2% over its forecast period.

Japan represents a technologically advanced environment for residential energy management systems due to its strong focus on energy efficiency and grid resilience. Following energy supply challenges in previous years, households have increasingly adopted energy monitoring systems and home energy management platforms. The government has promoted smart homes, distributed energy generation, and battery storage integration to strengthen energy security. Rapid urbanization and high electricity demand in densely populated areas are driving the adoption of automated control systems that optimize heating, cooling, and appliance energy consumption. Additionally, Japan's strong electronics and IoT manufacturing sector supports continuous innovation in connected home energy technologies.

Residential Energy Management Market: Key Takeaways

- Market Growth: The Residential Energy Management Market size is expected to grow by USD 7.2 billion, at a CAGR of 12.5%, during the forecasted period of 2027 to 2035.

- By Component: The hardware segment is anticipated to get the majority share of the Residential Energy Management market in 2026.

- By Communication Technology: The wireless segment is expected to get the largest revenue share in 2026 in the Residential Energy Management market.

- Regional Insight: North America is expected to hold a 37.9% share of revenue in the global Residential Energy Management market in 2026.

- Use Cases: Some of the use cases of Residential Energy Management include smart energy monitoring, smart HVAC optimization, and more.

Residential Energy Management Market: Use Cases:

- Smart Energy Monitoring: Homeowners can track real-time electricity consumption through smart meters and connected applications. This allows users to identify energy-intensive appliances and modify usage patterns to reduce electricity bills and improve efficiency.

- Demand Response Participation: Residential systems allow households to automatically adjust energy usage during peak grid demand periods. Utilities provide financial incentives to consumers who reduce or shift their electricity consumption.

- Smart HVAC Optimization: Advanced thermostats and sensors automatically regulate heating and cooling based on occupancy, temperature preferences, and weather conditions, reducing unnecessary energy consumption.

- Renewable Energy Integration: Energy management platforms coordinate rooftop solar panels, home batteries, and grid power to maximize renewable energy utilization and reduce reliance on conventional electricity sources.

- Electric Vehicle Charging Management: Systems can schedule EV charging during off-peak hours when electricity prices are lower, minimizing energy costs and reducing stress on the grid.

- Smart Lighting Automation: Connected lighting systems adjust brightness levels or switch off automatically based on occupancy or daylight conditions, improving energy efficiency in households.

- Appliance Load Control: Home energy systems can prioritize or delay operation of appliances such as washing machines, dishwashers, and water heaters to balance energy usage and reduce peak demand.

Stats & Facts

- U.S. Energy Information Administration (EIA) reported that approximately 119 million smart meters were installed in the United States by 2024, representing over 70% of all electricity customers.

- International Energy Agency (IEA) stated in 2024 that buildings account for nearly 30% of global final energy consumption and about 26% of global energy-related emissions.

- European Commission reported in 2025 that smart meter deployment across the European Union surpassed 200 million units installed in residential and commercial buildings.

- U.S. Department of Energy stated in 2024 that smart home technologies can reduce household electricity consumption by up to 10–15% through automation and monitoring.

- International Renewable Energy Agency (IRENA) reported in 2024 that global residential solar capacity exceeded 300 GW, significantly increasing the need for home energy management solutions.

- U.S. Environmental Protection Agency (EPA) reported in 2025 that energy-efficient homes can reduce energy consumption by approximately 20–30% compared with standard homes.

- Eurostat indicated in 2024 that households accounted for nearly 27% of final energy consumption in the European Union.

- Ministry of Economy, Trade and Industry Japan reported in 2025 that smart home energy management systems had been deployed in over 12 million Japanese households.

- International Energy Agency (IEA) estimated in 2025 that global electricity demand from residential buildings increased by approximately 3% annually.

- U.S. Department of Energy reported in 2024 that residential HVAC systems account for nearly 40% of household energy consumption in the United States.

- European Environment Agency stated in 2025 that improving building energy efficiency could reduce EU energy consumption by nearly 15%.

- National Renewable Energy Laboratory (NREL) reported in 2024 that integrating solar and battery storage in homes can reduce grid electricity consumption by up to 60%.

Market Dynamic

Driving Factors in the Residential Energy Management Market

Increasing Adoption of Smart Home Technologies

The growing popularity of smart homes is one of the most influential drivers of residential energy management systems. Smart thermostats, connected appliances, and automated lighting systems are becoming increasingly common in modern households. These technologies allow homeowners to monitor and control energy consumption through mobile applications and digital platforms. Integration with artificial intelligence and IoT devices enables real-time optimization of energy usage based on occupancy, weather conditions, and electricity prices. As consumers prioritize convenience, efficiency, and sustainability, smart home ecosystems are creating strong demand for comprehensive residential energy management solutions that improve comfort while minimizing energy waste.

Expansion of Renewable Energy and Distributed Energy Resources

The increasing adoption of rooftop solar panels, residential battery storage systems, and electric vehicles is accelerating the need for intelligent energy management platforms. These distributed energy resources require coordinated management to balance generation, storage, and consumption within households. Energy management systems allow homeowners to store excess solar energy, schedule appliance usage during peak generation periods, and reduce reliance on grid electricity. As governments and utilities promote renewable energy adoption through incentives and policy support, integrated home energy management solutions are becoming essential tools for maximizing energy efficiency and ensuring grid stability.

Restraints in the Residential Energy Management Market

High Initial Installation Costs

Despite the long-term energy savings associated with residential energy management systems, high upfront costs remain a major barrier to adoption. Installing smart meters, connected sensors, energy monitoring devices, and automation platforms requires significant investment for many households. Additionally, integrating these systems with existing home infrastructure can involve complex installation processes and additional expenses. For consumers in developing markets or lower-income households, these financial barriers limit adoption rates. While prices for connected devices are gradually declining, the initial cost of deploying comprehensive residential energy management solutions continues to restrict market expansion.

Data Privacy and Cybersecurity Concerns

Residential energy management systems rely heavily on connected devices and cloud-based platforms that collect and analyze detailed household energy usage data. This connectivity raises concerns about data privacy and cybersecurity risks among consumers. Unauthorized access to smart home systems could potentially expose personal information or allow external manipulation of household devices. As a result, many consumers remain cautious about adopting connected energy technologies. Regulatory frameworks and robust cybersecurity standards are essential to address these concerns and build trust among users, but inconsistent regulations across regions continue to create challenges for technology providers.

Opportunities in the Residential Energy Management Market

Growth of Smart Grid Infrastructure

The global expansion of smart grid infrastructure presents significant opportunities for residential energy management technologies. Smart grids enable two-way communication between utilities and consumers, allowing households to receive real-time electricity pricing and consumption data. This connectivity makes it possible to implement automated demand response programs and optimize energy usage during peak periods. As governments and utilities invest in modernizing electricity networks, residential energy management systems can play a critical role in improving grid efficiency, reducing peak load pressures, and supporting the integration of renewable energy resources into residential power systems.

Increasing Demand for Energy-Efficient Buildings

Growing awareness about energy efficiency and environmental sustainability is encouraging homeowners to adopt advanced energy management technologies. Energy-efficient homes equipped with monitoring and automation systems can significantly reduce electricity consumption and carbon emissions. Real estate developers are increasingly integrating smart energy solutions into new residential projects to meet regulatory requirements and consumer expectations. As building codes become stricter and sustainability certifications gain importance, residential energy management platforms are expected to become standard features in modern housing developments.

Trends in the Residential Energy Management Market

Integration of AI and Predictive Energy Analytics

Advanced analytics and artificial intelligence are transforming residential energy management platforms by enabling predictive and automated decision-making. AI-driven systems analyze historical energy consumption patterns, weather forecasts, and user behavior to optimize energy usage in real time. Predictive analytics can anticipate peak demand periods and automatically adjust appliance usage to minimize energy costs. These technologies are also improving demand response participation by enabling automated responses to grid signals. As digital technologies continue to evolve, AI-powered energy management platforms are becoming increasingly sophisticated and efficient.

Growth of Cloud-Based Energy Management Platforms

Cloud computing is playing a crucial role in the expansion of residential energy management systems. Cloud-based platforms allow homeowners to access energy data remotely through mobile applications and web interfaces. These platforms provide advanced analytics, automated device control, and seamless integration with smart home ecosystems. Cloud infrastructure also enables utilities and service providers to deliver software updates, new features, and predictive maintenance services without requiring on-site modifications. As cloud adoption increases, energy management platforms are becoming more scalable, flexible, and accessible to a wider range of residential users.

Impact of Artificial Intelligence in Residential Energy Management Market

- Smart Energy Forecasting: AI algorithms analyze historical consumption patterns and weather conditions to predict household energy demand and optimize energy usage.

- Automated Appliance Scheduling: AI-enabled platforms automatically schedule energy-intensive appliances during off-peak hours to reduce electricity costs and grid pressure.

- Predictive Maintenance: Machine learning models monitor device performance and detect anomalies in energy consumption, helping prevent system failures.

- Energy Consumption Insights: AI-powered analytics provide homeowners with detailed insights into energy usage patterns and recommendations for reducing electricity consumption.

- Demand Response Optimization: AI systems automatically adjust household energy usage during peak grid demand periods, improving grid stability and reducing electricity costs.

- Smart HVAC Optimization: AI integrates with thermostats and environmental sensors to regulate heating and cooling based on occupancy and temperature patterns.

- Renewable Energy Optimization: AI algorithms manage energy flow between solar panels, batteries, and the grid to maximize renewable energy utilization.

- Personalized Energy Recommendations: AI platforms provide customized energy-saving suggestions based on user behavior and household energy patterns.

- Grid Interaction Intelligence: AI allows homes to interact dynamically with smart grids, adjusting energy consumption based on real-time pricing signals.

Research Scope and Analysis

By Component Analysis

Hardware components are the backbone of residential energy management systems, enabling the physical monitoring, control, and communication of household energy consumption. This segment includes smart meters, smart thermostats, load control switches, in-home displays, and various sensors and communication devices that collect real-time data about electricity usage within residential buildings. In 2026, the hardware segment is expected to hold approximately 46.8% of the total market share, making it the dominant component category. The widespread installation of smart meters by utilities and the rapid adoption of smart thermostats are major factors supporting the segment's leadership. Hardware devices enable homeowners to visualize energy consumption patterns and automate appliance operation, which significantly improves energy efficiency. In addition, the increasing penetration of smart homes and connected IoT devices is strengthening demand for advanced monitoring hardware. Continuous innovation in wireless communication technologies and cost reductions in smart devices are further encouraging adoption, particularly in developed economies where smart grid infrastructure is already established.

The software segment is emerging as the fastest-growing component category in the residential energy management ecosystem. Energy management platforms, energy analytics software, and customer engagement applications allow homeowners and utilities to analyze energy consumption patterns, optimize device performance, and manage energy resources efficiently. Software solutions provide centralized dashboards, predictive analytics, and automated control capabilities that enhance energy optimization across multiple connected devices. With increasing deployment of cloud platforms and digital energy services, software systems are becoming critical for managing distributed energy resources such as rooftop solar panels and residential battery storage. As the smart home ecosystem expands, demand for advanced energy analytics tools and integrated energy management platforms is expected to grow rapidly.

By Communication Technology Analysis

Wireless communication technologies dominate residential energy management systems due to their flexibility, scalability, and ease of installation. Technologies such as Wi-Fi, Zigbee, Z-Wave, Bluetooth, and cellular communication enable seamless connectivity between smart devices, energy management platforms, and utility networks. In 2026, wireless technologies are expected to account for around 63.5% of the overall market share in communication technologies. The increasing adoption of IoT-enabled devices in smart homes is the primary driver of this segment's growth. Wireless communication eliminates the need for extensive wiring, making it suitable for both new residential buildings and retrofitting existing homes. Additionally, advancements in low-power communication protocols allow energy devices to operate efficiently for extended periods. The growing ecosystem of connected appliances, sensors, and automation systems is further strengthening the demand for reliable wireless communication solutions in residential energy management applications.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Wired communication technologies, including Ethernet and power line communication (PLC), continue to play an important role in residential energy management networks where reliability and stable connectivity are essential. PLC technology allows energy management devices to transmit data using existing electrical wiring infrastructure, reducing the need for additional communication lines. Although wired systems are not as flexible as wireless solutions, they offer advantages such as lower interference and higher data stability. These systems are particularly useful in large residential complexes or multi-unit buildings where stable communication between devices and central controllers is required. The adoption of wired communication remains relevant in environments where consistent connectivity and security are critical.

By Application Analysis

Energy monitoring and control represent the largest application segment in the residential energy management market. These systems allow homeowners to track electricity consumption in real time and automatically control appliances, lighting, and heating systems to improve energy efficiency. In 2026, this segment is projected to account for approximately 34.2% of the market share. The increasing availability of smart meters and mobile-based energy monitoring applications is driving the adoption of this technology. Real-time energy visibility enables households to identify energy-intensive appliances and modify consumption patterns accordingly. Additionally, automation features allow devices to switch off or reduce power consumption during periods of low usage. Utilities are also encouraging consumers to adopt monitoring platforms through incentive programs and demand response initiatives. As electricity prices continue to rise globally, households are becoming more proactive in managing energy usage, further strengthening the demand for monitoring and control systems.

Electric vehicle charging management is the fastest-growing application segment within residential energy management systems. As electric vehicle adoption accelerates globally, households require intelligent charging solutions that optimize energy consumption and minimize electricity costs. Energy management platforms allow EV owners to schedule charging sessions during off-peak electricity periods or when renewable energy generation is highest. These systems can also integrate with rooftop solar installations and home battery storage to maximize renewable energy utilization. With governments encouraging electric mobility through subsidies and infrastructure investments, demand for residential EV charging optimization solutions is expected to expand rapidly in the coming years.

By Deployment Analysis

Cloud-based deployment models are rapidly becoming the preferred architecture for residential energy management platforms. In 2026, cloud deployment is expected to represent around 58.7% of the market share due to its scalability, remote accessibility, and advanced analytics capabilities. Cloud systems allow homeowners to monitor and control energy consumption through mobile applications and web dashboards from anywhere. Utilities and service providers also benefit from cloud platforms by delivering software updates, energy analytics, and automated services without requiring physical infrastructure upgrades in homes. Additionally, cloud computing supports large-scale data analysis that enables predictive energy management and demand response optimization. As internet connectivity and IoT device adoption continue to expand, cloud-based energy management platforms are expected to dominate residential energy optimization solutions.

On-premise deployment remains relevant for households that prioritize data privacy, local data storage, and direct device control. In these systems, energy management software and control platforms operate within the home network without relying heavily on cloud infrastructure. On-premise solutions offer enhanced security and lower dependence on internet connectivity, making them suitable for regions with limited broadband infrastructure. Although growth in this segment is slower compared with cloud deployment, certain residential communities and smart home enthusiasts continue to prefer localized control systems for improved customization and data protection.

By Residence Type Analysis

Single-family homes represent the largest residential category for energy management systems due to their higher energy consumption levels and greater flexibility for installing smart devices. In 2026, this segment is expected to hold approximately 61.3% of the overall market share. Homeowners in single-family residences often have greater control over infrastructure upgrades, making it easier to install smart thermostats, solar panels, energy storage systems, and monitoring devices. Rising electricity prices and growing awareness about sustainability are encouraging homeowners to invest in energy optimization technologies. Additionally, the increasing popularity of smart home ecosystems is accelerating adoption in standalone houses where multiple connected devices can be integrated within a centralized energy management platform.

Energy management adoption in multi-family housing and apartment complexes is growing rapidly as property developers integrate smart building technologies into residential infrastructure. Centralized energy monitoring platforms allow building managers to optimize electricity consumption across multiple units while providing tenants with visibility into individual energy usage. Smart lighting systems, centralized HVAC management, and automated appliance controls can significantly improve energy efficiency in large residential complexes. As urbanization increases and high-density housing becomes more common, the demand for scalable energy management solutions in apartment buildings is expected to grow substantially.

The Residential Energy Management Market Report is segmented on the basis of the following:

By Component

- Hardware

- Smart Meters

- Smart Thermostats

- Load Control Switches / Controllers

- In-Home Displays (IHD)

- Sensors & Communication Devices

- Software

- Energy Management Platforms

- Energy Analytics Software

- Customer Engagement Platforms

- Services

- Consulting & System Design

- Installation & Integration

- Monitoring & Maintenance

By Communication Technology

- Wired

- Ethernet

- Power Line Communication (PLC)

- Wireless

- Wi-Fi

- Zigbee

- Z-Wave

- Bluetooth

- Cellular / RF

By Application

- Energy Monitoring & Control

- Demand Response Management

- Load Management / Peak Load Shaving

- Smart HVAC Control

- Smart Lighting Control

- Renewable Energy Integration (Solar & Storage)

- EV Charging Management

By Deployment

By Residence Type

- Single-Family Homes

- Multi-Family Homes / Apartments

Regional Analysis

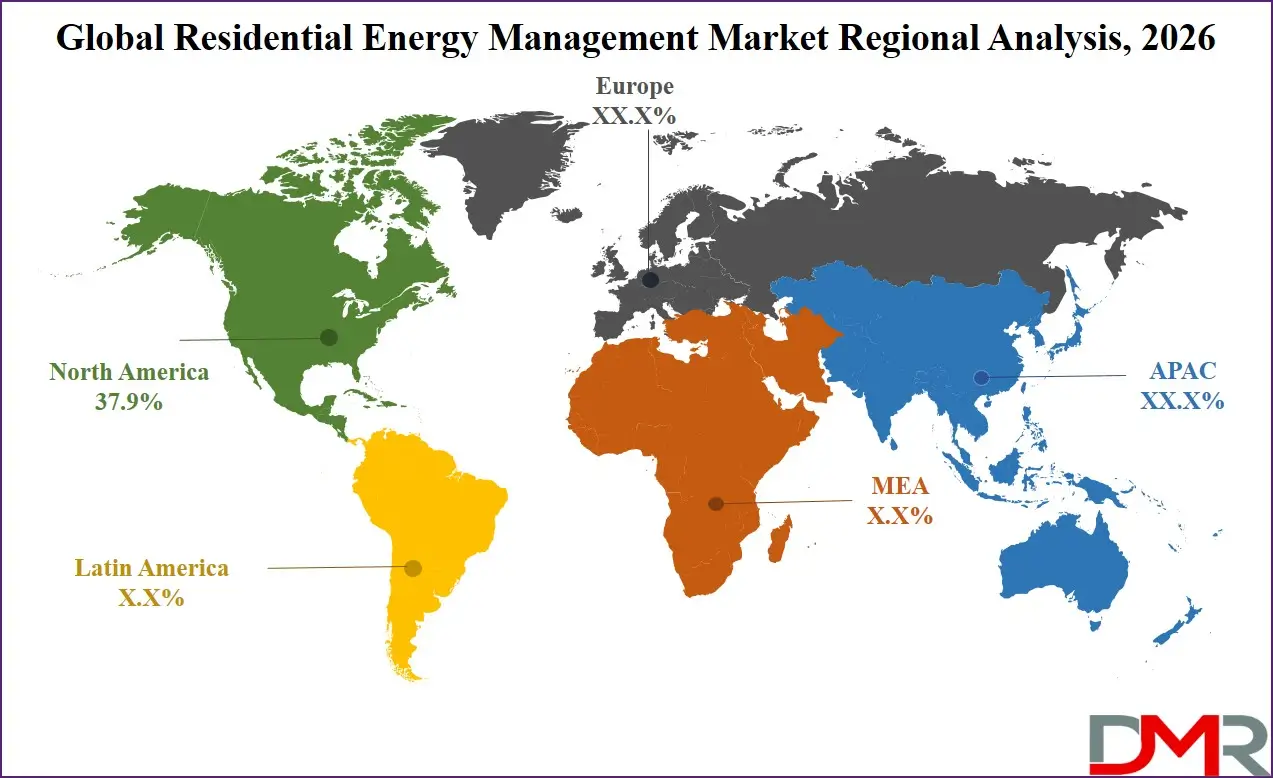

Leading Region in the Residential Energy Management Market

North America is expected to remain the leading region in the residential energy management market due to strong smart grid infrastructure, high smart home adoption, and supportive regulatory frameworks. In 2026, the region is projected to account for approximately 37.9% of the global market share. The United States plays a dominant role due to widespread smart meter deployment and increasing adoption of connected home technologies. Utilities across the region actively promote demand response programs that encourage households to manage electricity usage during peak demand periods.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Additionally, the growing penetration of rooftop solar installations, home battery storage, and electric vehicles is creating demand for integrated energy management platforms. Government initiatives promoting energy efficiency, sustainability, and grid modernization are also contributing to regional growth. Advanced digital infrastructure and the presence of technology innovators continue to support the development of sophisticated residential energy optimization solutions across North America.

Fastest Growing Region in the Residential Energy Management Market

Asia-Pacific is projected to be the fastest-growing region in the residential energy management market due to rapid urbanization, increasing energy demand, and expanding smart city initiatives. Countries such as China, Japan, South Korea, and India are investing heavily in smart grid infrastructure and energy-efficient residential developments. Rising electricity consumption in urban areas is encouraging governments to promote energy monitoring technologies that help households optimize energy use. The expansion of renewable energy installations, particularly rooftop solar systems, is also supporting the adoption of home energy management platforms. In addition, increasing smartphone penetration and the rapid growth of IoT ecosystems in Asia-Pacific are enabling households to adopt connected energy management technologies at a faster pace.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The residential energy management market is characterized by intense competition and continuous technological innovation. Companies operating in this space focus on developing advanced smart devices, cloud-based platforms, and integrated energy solutions to strengthen their market position. Strategic collaborations with utilities, technology providers, and smart home platform developers play a critical role in expanding product ecosystems and improving interoperability between devices. Research and development investments are increasing as companies aim to introduce AI-enabled analytics, predictive energy optimization tools, and advanced automation capabilities. Market participants are also focusing on expanding service offerings, including installation, monitoring, and maintenance services, to create long-term customer relationships. High initial technology costs and interoperability challenges act as entry barriers, favoring established players with strong technological capabilities and extensive distribution networks.

Some of the prominent players in the global Residential Energy Management are:

- Schneider Electric

- Honeywell International

- Siemens

- Johnson Controls

- ABB

- Eaton

- General Electric

- Panasonic

- Emerson Electric

- Itron

- Landis+Gyr

- Cisco Systems

- LG Electronics

- Samsung Electronics

- Leviton Manufacturing

- Lutron Electronics

- Tesla

- Google Nest (Alphabet)

- Ecobee

- Vivint Smart Home

- Other Key Players

Recent Developments

- In March 2026, Solis has introduced a new range of residential energy storage systems under its SolisStorage brand, signaling a move beyond inverters toward integrated energy storage solutions. The systems use long-life LiFePO₄ batteries, offering over 6,000 cycles, more than 90% depth of discharge, and up to 10 years of reliable operation. The portfolio includes three series, including the IntelliHome low-voltage system with 5.1 kWh, 10.2 kWh, and 16 kWh capacities designed for residential solar-plus-storage and backup power needs.

- In January 2026, ABB launched ReliaHome™ Flex, a modular residential energy management system designed to help homeowners add electric appliances without expensive electrical service upgrades. Compatible with any load center, the system installs quickly and can scale for both retrofits and new homes. Managed through the ReliaHome app, it provides real-time energy insights and automation features. The solution enables households to integrate EV chargers, HVAC systems, water heaters, and induction cooktops while avoiding costly infrastructure upgrades.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 4.1 Bn |

| Forecast Value (2035) |

USD 11.7 Bn |

| CAGR (2026–2035) |

12.5% |

| The US Market Size (2026) |

USD 1.4 Bn |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors and etc. |

| Segments Covered |

By Component (Hardware, Software, Services), By Communication Technology (Wired, Wireless), By Application (Energy Monitoring & Control, Demand Response Management, Load Management / Peak Load Shaving, Smart HVAC Control, Smart Lighting Control, Renewable Energy Integration (Solar & Storage), EV Charging Management), By Deployment (On-Premise, Cloud-Based), By Residence Type (Single-Family Homes, Multi-Family Homes / Apartments) |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

| Prominent Players |

Schneider Electric, Honeywell International, Siemens, Johnson Controls, ABB, Eaton, General Electric, Panasonic, Emerson Electric, Itron, Landis+Gyr, Cisco Systems, LG Electronics, Samsung Electronics, Leviton Manufacturing, Lutron Electronics, Tesla, Google Nest (Alphabet), Ecobee, Vivint Smart Home, and Other Key Players |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users) and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days and 5 analysts working days respectively. |

Frequently Asked Questions

How big is the Global Residential Energy Management Market?

▾ The Global Residential Energy Management Market size is expected to reach USD 4.1 billion by 2026 and is projected to reach USD 11.7 billion by the end of 2035.

Which region accounted for the largest Global Residential Energy Management Market?

▾ North America is expected to have the largest market share in the Global Residential Energy Management Market, with a share of about 37.9% in 2026.

How big is the Residential Energy Management Market in the US?

▾ The US Residential Energy Management market is expected to reach USD 1.4 billion by 2026.

Who are the key players in the Residential Energy Management Market?

▾ Some of the major key players in the Global Residential Energy Management Market include ABB, Eaton, Siemens, and others.

What is the growth rate in the Global Residential Energy Management Market?

▾ The market is growing at a CAGR of 12.5 percent over the forecasted period.