What is the Rubber Processing Chemicals Market Size?

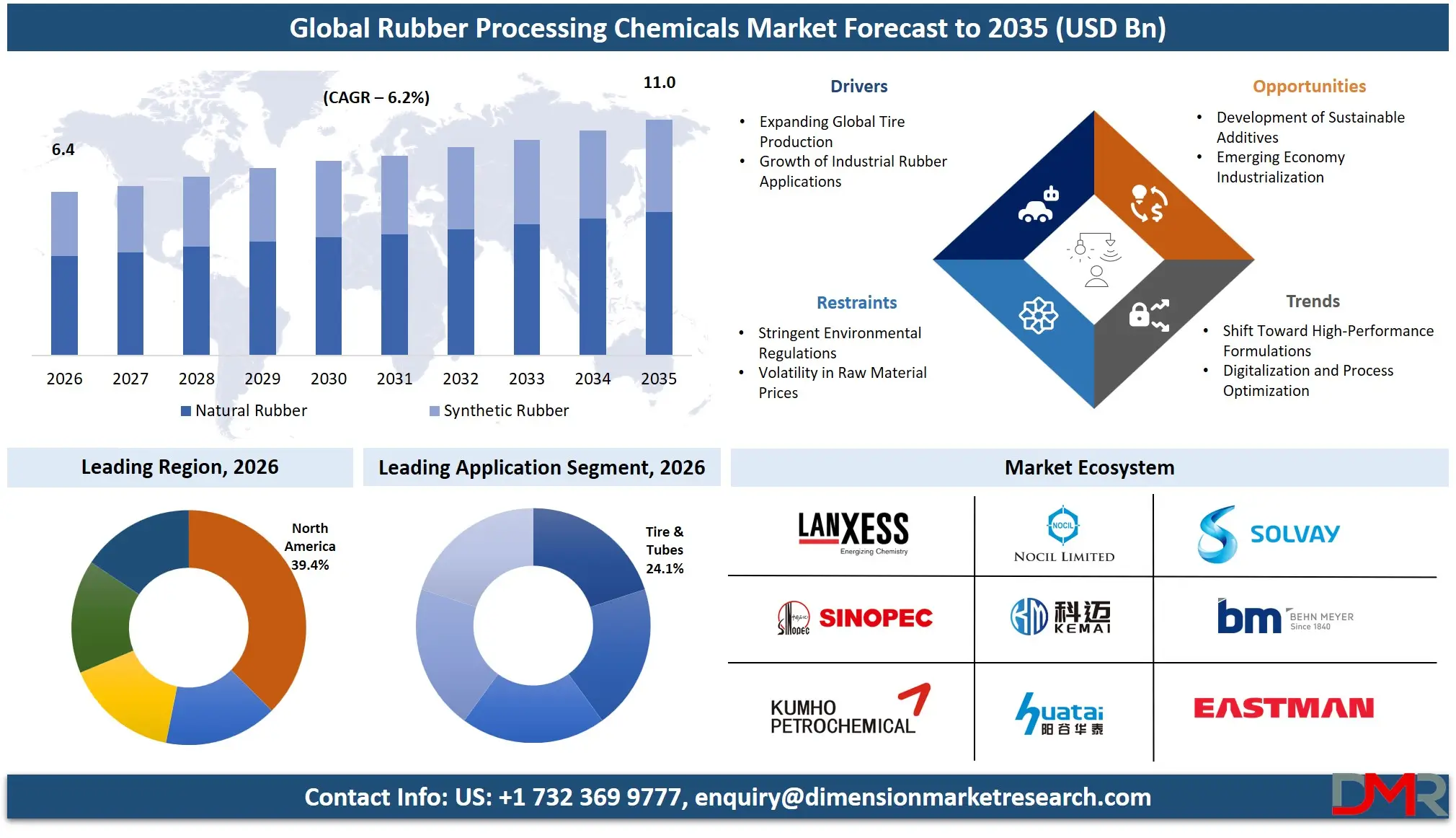

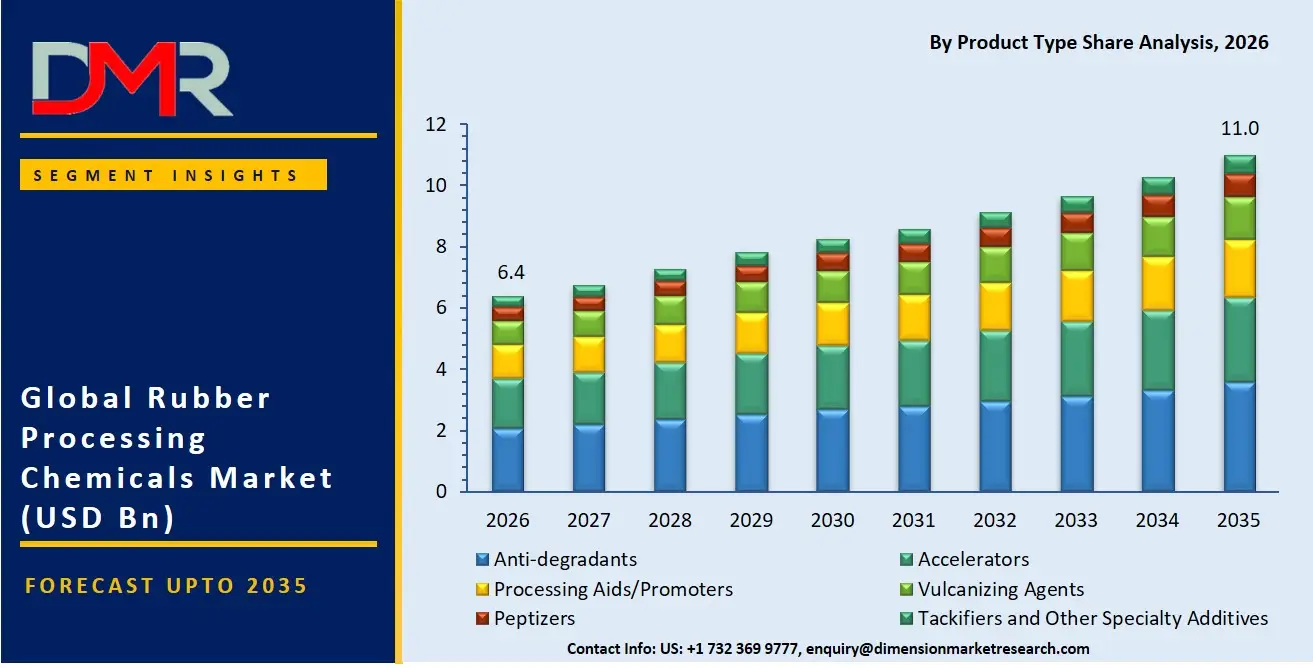

The Global Rubber Processing Chemicals Market is expected to reach a value of USD 6.4 billion in 2026, and it is further anticipated to reach USD 11.0 billion by 2035, growing at a CAGR of 6.2% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The rubber processing chemicals market has been growing at a steady rate, propelled by the relentless demand from the automotive and industrial manufacturing sectors. The market consists of specialty chemicals including anti-degradants, accelerators, and vulcanizing agents that are essential for enhancing the durability, elasticity, and thermal resistance of both natural and synthetic rubber. The increasing demand for high-performance tires, durable automotive components, and robust industrial rubber goods is driving the necessity for advanced chemical formulations. Tire and tube manufacturing remains the dominant application, with synthetic rubber derivatives being the most consumed due to their superior heat and abrasion resistance. The automotive, construction, and consumer products industries are key players as they require rubber compounds that can withstand extreme mechanical stress and environmental aging.

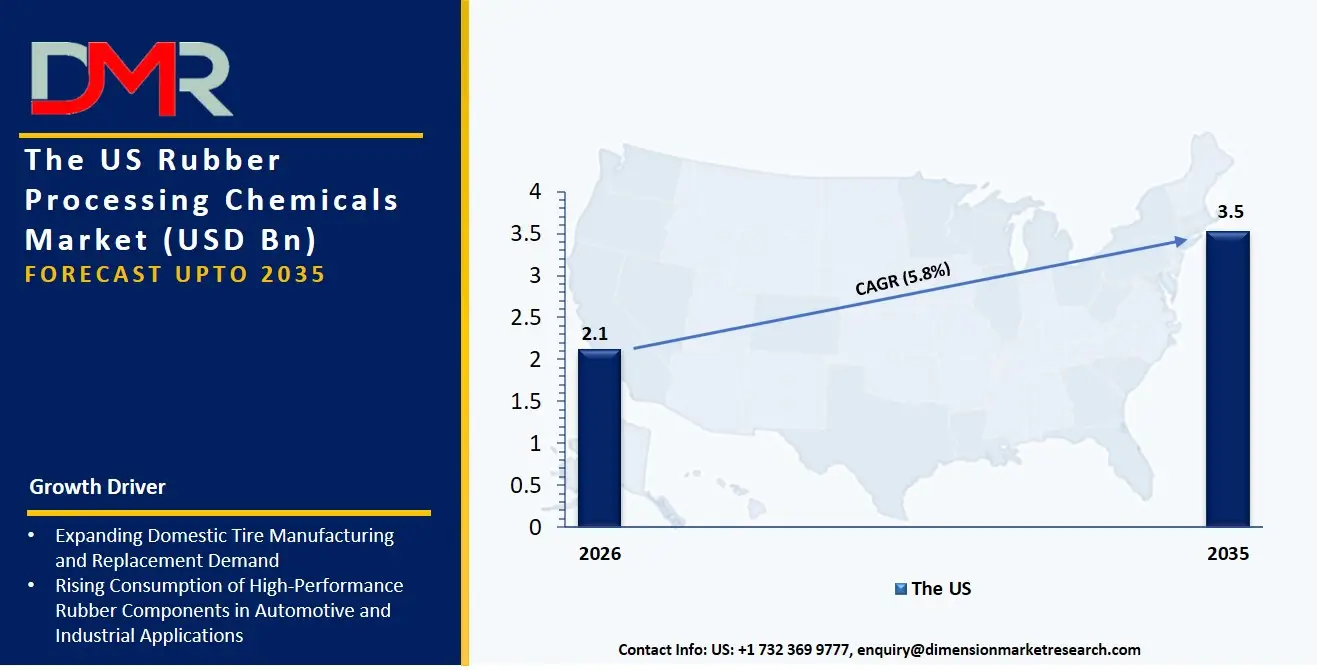

The US Rubber Processing Chemicals Market

The US Rubber Processing Chemicals Market is projected to reach USD 2.1 billion in 2026 at a compound annual growth rate of 5.8% over its forecast period, culminating in a value of USD 3.5 billion by 2035.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The US remains a pivotal market in rubber processing chemicals due to the aggressive modernization of domestic tire manufacturing and the robust demand for high-mileage, fuel-efficient tires. The market has been typified by high demand for advanced anti-degradants, whereby manufacturers are focused on extending the service life of rubber components exposed to severe oxidative and ozone-rich environments. Besides, the growing production of electric vehicles (EVs) is producing a similar need for specialty processing aids that manage the high-torque characteristics and increased weight of EV platforms, reducing rolling resistance and improving compound stability.

The Europe Rubber Processing Chemicals Market

The Europe Rubber Processing Chemicals Market is estimated to be valued at USD 1.9 billion in 2026 and is further anticipated to reach USD 3.1 billion by 2035 at a CAGR of 5.6%. Stringent regulatory frameworks including REACH and EU tire labeling regulations have a significant impact on the European market and drive the need to employ non-carcinogenic accelerators and sustainable antioxidants. Accelerated growth in bio-based processing oils and vulcanizing agents is also being experienced in the region as manufacturing hubs in Germany and Italy strive to balance industrial performance with circular economy mandates. In addition, initiatives to reduce volatile organic compound (VOC) emissions are challenging chemical suppliers to create dedicated, low-emission peptizers and tackifiers that ensure workplace safety and regulatory compliance across European rubber molding ecosystems.

The Japan Rubber Processing Chemicals Market

The Japan Rubber Processing Chemicals Market is projected to be valued at USD 353.2 million in 2026 at a CAGR of 5.1%. The Japanese market is unique, with a corporate drive to precision manufacturing in response to exacting quality standards for automotive OEMs and industrial robotics. High-performance vulcanizing agents and specialty accelerators make up a large part of the spending as large synthetic rubber producers optimize cure times and thermal stability for under-the-hood applications. There is also a strong need to integrate deeply with local automotive supply chains to bridge the performance gaps between traditional natural rubber compounds and advanced synthetic elastomers for high-tech belting and hose systems, which forms a niche in custom-formulated anti-ozonants and adhesion promoters.

Key Takeaways

- Market Size & Forecast: The Global Rubber Processing Chemicals market is projected to reach USD 6.4 billion in 2026, expanding to USD 11.0 billion by 2035, fueled by the dual drivers of rising vehicle production and the indispensable requirement for high-durability industrial rubber goods.

- Growth Rate & Outlook: Global market growth is expected at a CAGR of 6.2%, driven by a critical need for advanced anti-degradant systems and the escalating complexity of vulcanization processes for next-generation synthetic elastomers.

- Primary Growth Drivers: Key forces include the expansion of the global automotive fleet, the shift toward high-performance tires that require sophisticated accelerators and antioxidants, and the need for robust processing aids to prevent premature failure in heavy-duty industrial rubber products.

- Key Market Trends: Major trends include the development of eco-friendly rubber chemicals to replace hazardous substances, the use of nanotechnology within anti-degradant systems to auto-remediate surface oxidation, and the shift toward pre-dispersed specialty additives as processors prioritize compounding accuracy and workplace hygiene.

- By Rubber Type Analysis: Synthetic Rubber is expected to dominate consumption due to its tailored properties and criticality in tire manufacturing. Professional chemical formulations are increasingly required to build an optimal crosslink density that connects polymer chains, enhancing abrasion resistance and dynamic mechanical properties.

- By Application Analysis: Tire & Tubes is the most lucrative application due to stringent performance and safety requirements. Automotive Components (non-tire) is the fastest-growing sector as electric vehicle sealing systems and vibration-dampening mounts require robust antioxidants and processing promoters for thermal endurance and acoustic optimization.

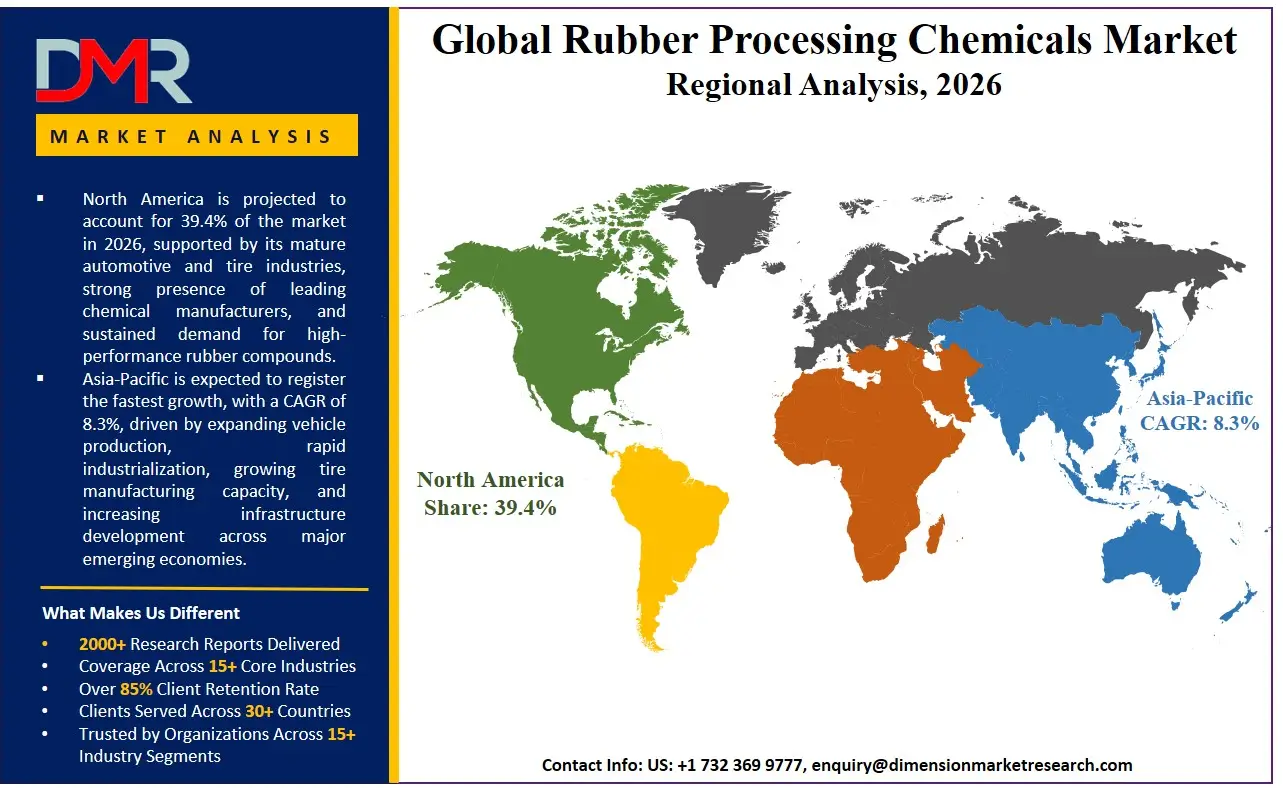

- Regional Leadership: North America is poised to dominate this market with 39.4% of the market share in 2026 due to its technologically advanced chemical sector that utilizes this infrastructure to its fullest, making it a leader in high-value specialty rubber additives.

What is the Rubber Processing Chemicals?

Rubber Processing Chemicals are the specialized compounding ingredients offered by chemical manufacturers and formulators to assist rubber processors throughout the entire product lifecycle. These additives, unlike the raw rubber polymers themselves, are related to the how of rubber compounding. This involves Anti-degradants to establish long-term protection against heat, oxygen, and ozone attack; Accelerators and Vulcanizing Agents to physically crosslink the polymer chains in a controlled and efficient manner without causing scorch; and Processing Aids and Peptizers to ensure that rubber compounds can effectively be mixed, extruded, and molded on existing shop-floor machinery. With 90% of all rubber consumed being crosslinked into a thermoset form, processing chemicals are needed to achieve cure efficiency, mechanical reinforcement, and environmental resistance, making rubber investments translate into tangible product longevity, as opposed to rapid component fatigue and failure.

Use Cases

- High-Speed Tire Durability: Tire manufacturers hire compound development specialists and use high-activity accelerators and anti-ozonants to formulate tread and sidewall compounds that resist cracking and blowouts under prolonged high-speed driving and exposure to atmospheric ozone.

- EV Vibration Dampening: Automotive component suppliers use specialty antioxidants and processing aids to manufacture engine mounts and sealing profiles that must endure higher thermal loads and torque-induced vibrations in electric vehicles, ensuring ride comfort and battery compartment integrity.

- Industrial Belt Longevity in Mining: Conveyor belt fabricators use advanced anti-fatigue agents and vulcanization cure systems to produce heavy-duty belts that resist catastrophic tearing and abrasive wear when transporting aggregate materials in harsh mining environments.

- Medical Device Safety: Medical device manufacturers use certified, high-purity accelerators and non-toxic plasticizers to create surgical tubing and seals that must maintain flexibility and biocompatibility under repeated steam sterilization cycles without leaching harmful byproducts.

How AI is Transforming the Rubber Processing Chemicals Market?

AI is changing the rubber processing chemicals sector by accelerating the development of novel formulations, as well as enhancing manufacturing precision. In material informatics, AI-based predictive modeling tools have the potential to automatically simulate the complex interactions between accelerators, anti-degradants, and filler systems, greatly minimizing the amount of physical lab testing and development timelines, and R&D project risk. Meanwhile, AI-powered features in compound mixing and quality control allow processors to better control batch-to-batch uniformity by detecting rheological anomalies, predicting cure kinetics, and suggesting real-time adjustments to peptizer or vulcanizing agent dosages to reinforce quality assurance protocols.

Chemical discovery and stability analysis are also revolving around AI. In the area of anti-degradant development, intelligent machine learning agents are used to virtually screen thousands of molecular structures and identify potential synergistic antioxidant blends that maximize thermal oxidative stability. Moreover, generative AI assistants are complementing rubber technologists by simulating compound aging processes and modeling long-term product performance to give stakeholders a visualization of a rubber component's service life before committing manufacturing resources.

Market Dynamics

Key Drivers in the Global Rubber Processing Chemicals Market

Expanding Global Tire Production

Rising passenger and commercial vehicle production, together with a robust replacement tire market, continues to fuel demand for rubber processing chemicals. Tires require a broad range of accelerators, anti-degradants, and vulcanizing agents to achieve durability, safety, and fuel efficiency. The growing adoption of electric vehicles further increases the need for advanced rubber compounds capable of handling higher torque and heavier battery loads. Urbanization and infrastructure development also stimulate demand for industrial and off-road tires. Consequently, tire manufacturers are steadily increasing their consumption of high-performance processing chemicals, making the automotive and transportation sectors the foremost drivers of market expansion worldwide.

Growth of Industrial Rubber Applications

Industrial sectors such as construction, mining, oil and gas, and manufacturing increasingly rely on belts, hoses, seals, and gaskets made from engineered rubber. These products require specialized chemical additives to improve processability and resistance to heat, abrasion, and chemicals. As industrial activity expands in emerging economies, the need for durable rubber components rises accordingly. Manufacturers are also adopting advanced formulations to extend service life and reduce maintenance costs. This broadening application base supports sustained consumption of rubber processing chemicals and encourages suppliers to develop innovative products tailored to demanding industrial environments, reinforcing long-term market growth.

Restraints in the Global Rubber Processing Chemicals Market

Stringent Environmental Regulations

Many conventional rubber processing chemicals face growing scrutiny due to concerns regarding toxicity, persistence, and workplace exposure. Compliance with evolving environmental and occupational safety regulations increases testing, reformulation, and production costs for manufacturers. Some legacy additives are being phased out, requiring investment in alternative chemistries and process modifications. Smaller producers may find these transitions particularly challenging, potentially limiting capacity expansion. While such regulations ultimately foster safer products, they can temporarily constrain market growth and reduce margins. The need to balance performance with sustainability remains a significant challenge for participants across the global rubber processing chemicals value chain.

Volatility in Raw Material Prices

The market is sensitive to fluctuations in the costs of petrochemical feedstocks and specialty intermediates used in additive production. Price swings driven by crude oil movements, supply disruptions, or geopolitical factors can compress margins and complicate long-term planning. Manufacturers often struggle to pass increased costs to customers immediately, particularly under fixed-price supply agreements. This uncertainty may delay investments and encourage end users to optimize formulations to reduce chemical usage. Persistent feedstock volatility therefore acts as a restraint, affecting profitability and creating operational challenges throughout the supply chain for rubber processing chemical producers.

Growth Opportunities in the Global Rubber Processing Chemicals Market

Development of Sustainable Additives

Demand is rising for environmentally friendly processing chemicals that maintain high performance while reducing ecological impact. Producers that successfully commercialize bio-based, low-toxicity, or recyclable additive systems can access new markets and strengthen customer relationships. Sustainability initiatives among tire manufacturers and industrial users are accelerating adoption of such solutions. In addition to regulatory compliance, greener chemistries can enhance brand value and support circular economy objectives. Continued research and collaboration across the value chain create substantial opportunities for innovation, enabling companies to differentiate their offerings and capture premium segments within the evolving rubber processing chemicals market.

Emerging Economy Industrialization

Rapid industrialization and vehicle ownership growth in Asia, Africa, and parts of Latin America are creating significant new demand for rubber goods. Expanding infrastructure projects and manufacturing capacity require large volumes of tires, belts, hoses, and seals, all of which depend on processing chemicals. Establishing local production facilities and distribution networks in these regions offers suppliers access to high-growth customer bases and lower logistics costs. Strategic partnerships with regional manufacturers can further accelerate market penetration. These favorable demographic and economic trends present compelling long-term expansion opportunities for companies operating in the global rubber processing chemicals industry.

Trends in the Global Rubber Processing Chemicals Market

Shift Toward High-Performance Formulations

End users increasingly seek rubber compounds with superior durability, lower rolling resistance, and enhanced resistance to extreme operating conditions. This is driving the development of advanced processing chemicals that enable precise control of curing and material properties. Multifunctional additives that improve efficiency while reducing formulation complexity are gaining traction. The trend is especially pronounced in premium tires and specialized industrial applications, where performance differentials directly influence purchasing decisions. Suppliers are therefore investing heavily in research and development to create next-generation chemistries that meet increasingly stringent technical requirements and deliver measurable value to customers.

Digitalization and Process Optimization

Rubber manufacturers are adopting digital tools, automation, and data analytics to improve consistency and reduce waste in compounding operations. This transformation encourages the use of processing chemicals designed for predictable behavior and compatibility with highly controlled manufacturing environments. Suppliers are increasingly offering technical support, formulation modeling, and data-driven services alongside their products. Enhanced process monitoring enables customers to optimize additive usage and achieve tighter quality specifications. As smart manufacturing practices spread throughout the industry, digital integration is becoming a defining trend that shapes product development and customer engagement strategies in the rubber processing chemicals market.

Research Scope and Analysis

The global rubber processing chemicals market is segmented by product type into anti degradants including antiozonants and antioxidants, accelerators, processing aids and promoters, vulcanizing agents, peptizers, and tackifiers with other specialty additives. It is further segmented by rubber type into natural and synthetic rubber, by application into tires and tubes, automotive components, industrial rubber goods, footwear, belts and hoses, consumer goods, and others, and by end user into automotive, industrial manufacturing, construction, consumer products, and others.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Product Type Analysis

Anti-degradants are projected to dominate the product landscape because protecting rubber from oxidation, heat, ozone, and weathering is essential for maintaining durability and safety. Their extensive use in tires, automotive seals, hoses, and industrial products ensures consistently high demand. Antiozonants and antioxidants significantly extend service life, reduce maintenance requirements, and improve performance under harsh operating conditions.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Regulatory emphasis on product reliability and manufacturers' focus on longer-lasting rubber goods further reinforce their leadership. Continuous advancements in anti-degradant chemistry that enhance compatibility with modern elastomers and support high-performance applications have solidified this segment's position as the largest and most indispensable category within the global rubber processing chemicals market.

By Rubber Type Analysis

Synthetic rubber is poised to be the dominant rubber type owing to its superior consistency, tailored properties, and widespread adoption in tire manufacturing and industrial applications. It offers enhanced resistance to heat, abrasion, chemicals, and aging compared with many natural rubber grades, making it ideal for demanding environments. The ability to engineer specific performance characteristics and ensure stable supply at large scale further supports its prevalence. Rapid growth in automotive production, infrastructure development, and advanced industrial goods has accelerated the consumption of synthetic elastomers, thereby driving the use of processing chemicals specifically formulated for these materials and cementing synthetic rubber's leading market position.

By Application Analysis

Tire and tube manufacturing is projected to represent the leading application segment because it consumes the largest volume of rubber processing chemicals worldwide. Modern tires require sophisticated additive packages to achieve optimal curing, durability, rolling resistance, and safety performance. Expanding vehicle fleets, replacement tire demand, and the increasing production of electric vehicles continue to stimulate consumption. Processing chemicals are indispensable for ensuring uniformity and extending tire life under diverse operating conditions. Continuous innovation in high-performance and sustainable tire compounds further strengthens this segment's dominance, making tire and tube applications the principal demand center for rubber processing chemicals across both mature and emerging markets.

By End User Analysis

The automotive industry is poised to dominate the end-user demand due to its extensive consumption of tires, seals, gaskets, hoses, vibration dampers, and numerous other rubber components. Stringent requirements for safety, fuel efficiency, durability, and comfort necessitate the use of advanced rubber formulations incorporating a wide range of processing chemicals. Rising global vehicle production, coupled with the transition toward electric and hybrid vehicles, sustains strong demand for high-performance elastomeric materials. Automotive manufacturers' focus on reliability and extended component life further amplifies chemical usage, securing the sector's position as the foremost end user and the primary driver of innovation within the global rubber processing chemicals market.

The Global Rubber Processing Chemicals Market Report is segmented on the basis of the following:

By Product Type

- Anti-degradants

- Antiozonants

- Antioxidants

- Accelerators

- Processing Aids/Promoters

- Vulcanizing Agents

- Peptizers

- Tackifiers and Other Specialty Additives

By Rubber Type

- Natural Rubber

- Synthetic Rubber

By Application

- Tire & Tubes

- Automotive Components (non-tire)

- Industrial Rubber Goods

- Footwear

- Belts & Hoses

- Consumer Goods

- Others

By End User

- Automotive

- Industrial Manufacturing

- Construction

- Consumer Products

- Others

Regional Analysis

Leading Region by Market Share

ℹ

To learn more about this report –

Download Your Free Sample Report Here

North America is poised to dominate the global rubber processing chemicals market as it is projected to hold 39.4% of the market share by the end of 2026. The United States, which dominates North America, has the highest share in the rubber processing chemicals market because of the unmatched concentration of large-scale tire and automotive OEM manufacturing plants and the aggressive material modernization agendas of domestic automotive manufacturers. The area has an established ecosystem of global chemical conglomerates, boutique specialty formulators, and a rich pool of talent in polymer science and chemical engineering. Enterprise investment in advanced mobility, smart manufacturing, and the overall replacement of legacy elastomeric parts contribute to the continued demand for next-generation anti-degradants and vulcanizing agents along with continuous compound optimization. Moreover, a stringent NHTSA safety compliance climate persistently finances upcoming rubber technologies that need expert chemical processing to achieve expeditious development and product reliability.

Fastest-Growing Regional Market

Asia-Pacific is expected to be the most rapidly expanding rubber processing chemicals market, driven by sweeping industrialization and infrastructure development in China, India, and Southeast Asia. The fast-paced economic growth, the rise of the consumer class, and the dynamic expansion of the automotive production sector is compelling established tire manufacturers and state-run industrial firms to expand their synthetic rubber and compounding capabilities. Rubber compound optimization is in high demand to help these large organizations head in the direction of high-output, zero-defect operating models. There is also a growing need to outsource specialty chemical innovation to bridge the gap between local raw material variations and global OEM quality requirements, fostering faster investments in domestic accelerator and peptizer manufacturing projects.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The competitive environment of the global rubber processing chemicals market has become highly dynamic with a heterogeneous array of multinational petrochemical giants, specialized antioxidant and accelerator producers, and regional formulation houses. The key to success will be profound strategic alliances with major tire and automotive OEMs because they will open the necessary co-development opportunities and early access to next-generation vehicle platform requirements. The movement towards market consolidation is rapidly progressing with traditional chemical conglomerates acquiring niche green chemistry and bio-based additive specialists to stay afloat. Proprietary intellectual property, including non-blooming anti-degradant systems and single-package cure systems, is becoming a more important basis of competitive differentiation than just bulk commodity pricing or generic distribution networks.

Some of the prominent players in the Global Rubber Processing Chemicals Market are:

- Lanxess

- Eastman Chemical Company

- Arkema

- Solvay

- Kumho Petrochemical

- China Petroleum & Chemical Corporation (Sinopec)

- NOCIL Limited

- Behn Meyer

- Shandong Yanggu Huatai Chemical

- Kemai Chemical

- Agrofert

- Duslo

- PMC Group

- Emery Oleochemicals

- Vanderbilt Chemicals

- King Industries

- Akrochem Corporation

- Rhein Chemie

- OUCHI SHINKO CHEMICAL INDUSTRIAL

- Performance Additives Division of SI Group

- Other Key Players

Recent Developments

- March 2026: Lanxess showcased sustainable tire additives at Tire Technology Expo 2026, including Vulkanox 4060 as a potential replacement for 6PPD, Aflux SD silica-dispersion aid, and talc-free Rhenogran/Rhenoslab grades supporting evolving European sustainability and product-traceability requirements.

- November 2025: BASF commissioned a new dispersant production line in Nanjing, China, employing controlled free-radical polymerization technology. The facility strengthens local supply of advanced additive solutions for automotive and industrial coatings customers throughout the rapidly growing Chinese market.

- January 2026: NXP Semiconductors introduced its 5 nm S32N7 vehicle processors at CES. Collaborating with Bosch, the platform centralizes key vehicle functions for software-defined vehicles and is expected to reduce total ownership costs by approximately twenty percent.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 6.4 Bn |

| Forecast Value (2035) |

USD 11.0 Bn |

| CAGR (2026–2035) |

6.2% |

| The US Market Size (2026) |

USD 2.1 Bn |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Product Type, By Rubber Type, By Application, and By End User |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Global Rubber Processing Chemicals Market?

▾ The Global Rubber Processing Chemicals market is poised to be valued at USD 6.4 billion in 2026 and is projected to reach USD 11.0 billion by 2035, driven by the universal need for specialized chemistry in tire durability, EV component development, and industrial rubber goods.

What is the CAGR of the Global Rubber Processing Chemicals Market from 2026 to 2035?

▾ The market is expected to grow at a CAGR of 6.2% from 2026 to 2035, reflecting the accelerating complexity of elastomeric material science and the persistent demand for higher-performance, longer-life rubber products.

What factors are driving the growth of the Global Rubber Processing Chemicals Market?

▾ Key drivers include the pervasive demand for high-performance tires, the mandatory push to reduce rolling resistance and emissions, the management of extreme heat in electric vehicle components, and the surge in demand for sustainable, non-carcinogenic additives amid evolving chemical safety laws.

Which region held the largest share of the Rubber Processing Chemicals Market in 2026?

▾ North America is poised to hold 39.4% of the market share in 2026, driven by a mature automotive and tire manufacturing ecosystem and aggressive investment in advanced anti-degradant and specialty accelerator development.

Which region is expected to grow the fastest in the Rubber Processing Chemicals Market?

▾ The Asia-Pacific region is expected to grow the fastest, fueled by rapid industrialization and vehicle production in China and India, where compound optimization and cost-effective vulcanization systems are critical for transitioning mass manufacturing plants to high-output quality standards.

What are the major trends in the Global Rubber Processing Chemicals Market?

▾ Major trends include the integration of artificial intelligence into chemical formulation discovery, the rise of pre-dispersed and dust-free additive masterbatches, the demand for custom cure systems for EV battery sealing, and the focus on bio-based processing oils within circular economy frameworks.

Who are the key players in the Global Rubber Processing Chemicals Market?

▾ Key players include global chemical conglomerates like Lanxess, BASF, and Sumitomo Chemical, as well as specialized leaders like NOCIL and Kumho Petrochemical, alongside a growing number of niche green chemistry innovators and regional compounders.

How is the Global Rubber Processing Chemicals Market segmented?

▾ The market is segmented by Product Type, Rubber Type, Application, and End User.