What is the Saudi Arabia DG Ground-Mounted Solar PV Market Size?

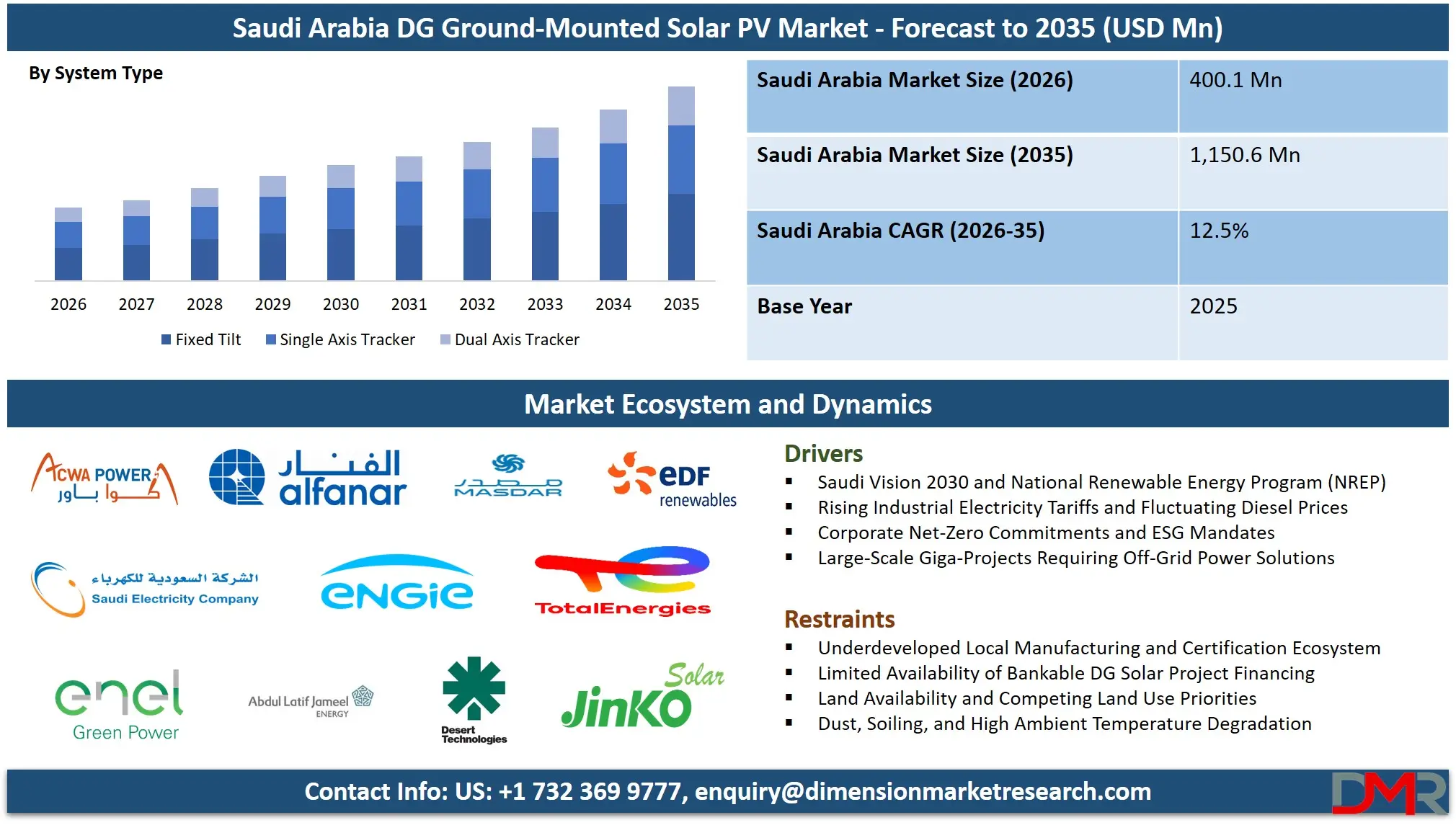

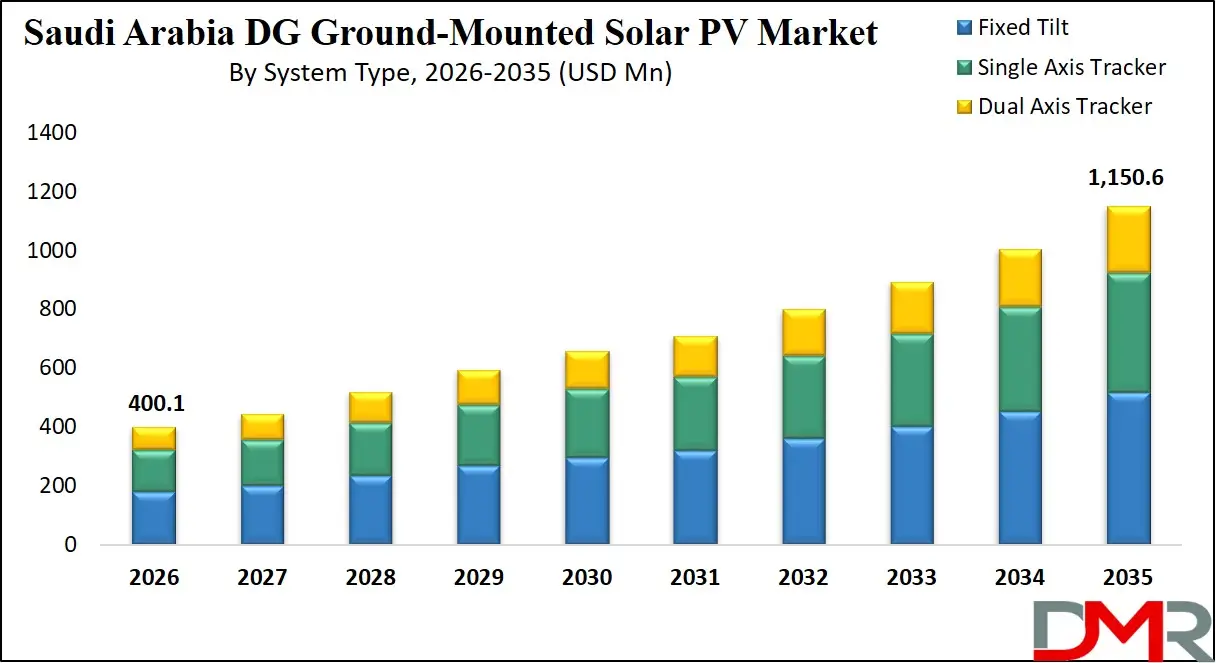

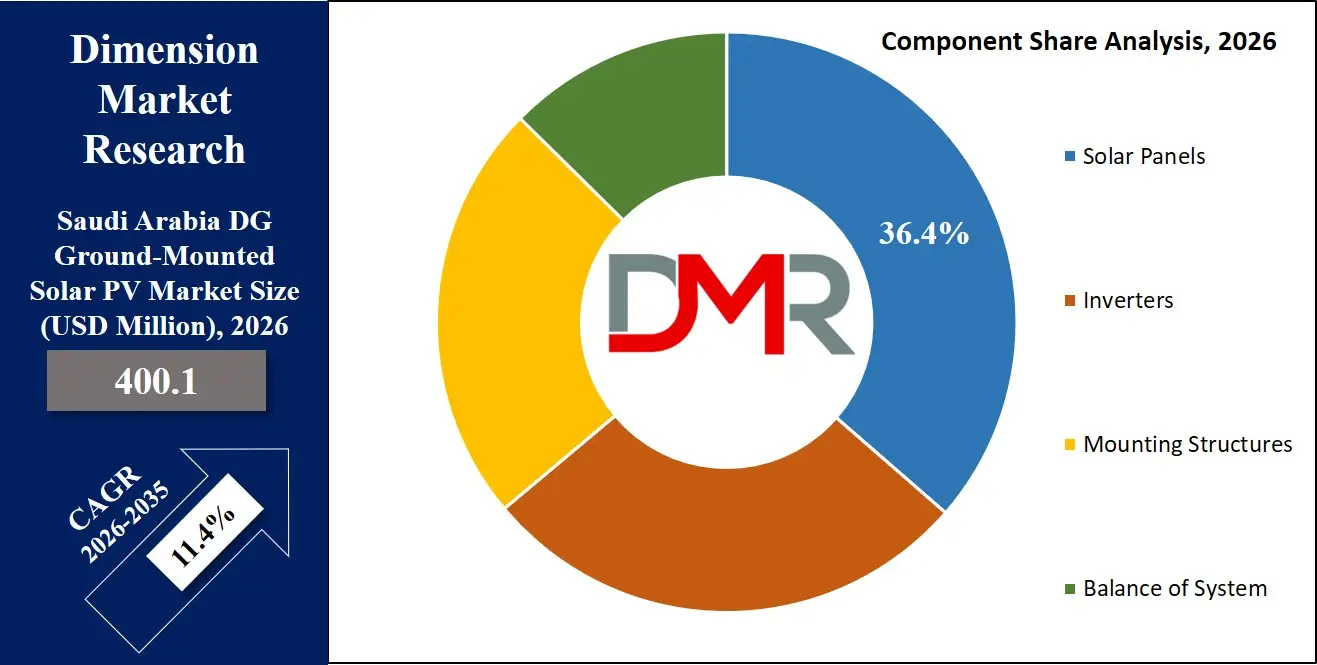

The Saudi Arabia DG Ground-Mounted Solar PV Market is estimated to be valued at USD 400.1 million in 2026 and is projected to reach USD 1,150.6 million by 2035, growing at a CAGR of 12.5% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The Saudi Arabia DG Ground-Mounted Solar PV Market is growing at a high pace, due to the introduction of numerous initiatives by the government, such as NIDLP and the Saudi Renewable Energy Initiative (SREI), which emphasize decentralized power production and energy self-sufficiency.

Growth is also being enhanced by increased attention to reducing the use of diesel to run off-grid facilities, a rise in electricity rates, and the use of unskilled labor to run the traditional sources of power. Many of these mega projects, such as NEOM Industrial City and King Salman Energy Park (SPARK), have created enormous demand for ground-mounted DG solar solutions to support captive and grid demand.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Key Takeaways

- Market Size & Forecast: The Saudi Arabia DG ground-mounted solar PV market is expected to grow from USD 400.1 million in 2026 to USD 1,150.6 million by 2035 due to increasing demand in decentralized renewable energy in industrial and commercial activities.

- Growth Rate & Outlook: The market size is set to grow at a compound annual growth rate of 12.5% during the forecast period of 2026 to 2035.

- Primary Growth Drivers: Growth in this market is attributed to government mandates for localized power generation under Vision 2030 and NIDLP, along with the urgent need for reliable off-grid electricity for critical remote facilities.

- Key Market Trends: Integration of DG solar data into digital energy management platforms, transition to fixed tilt to single-axis trackers, and AI-based performance diagnostics are some of the key trends that indicate the high potential of this market.

- By Component Analysis: The solar panels segment is anticipated to get the majority share of the DG ground-mounted solar PV market in 2026.

- By System Type Analysis: The fixed tilt systems segment is expected to get the largest revenue share in 2026 in the market, primarily due to their lower capital costs, simpler maintenance, and ease of deployment in remote areas.

- By Technology Analysis: The monocrystalline silicon segment is likely to hold the largest share at approximately 66.2% of the technology segment in 2026, driven by high efficiency and space constraints in DG applications.

What is DG Ground-Mounted Solar PV?

Distributed Generation (DG) ground-mounted solar PV is a solar power system that is installed on the ground between 100 kW and 10 MW, which generates solar power that is consumed on-site or distributed locally rather than fed to a central utility. DG solar PV mounted on the ground assists in reducing transmission losses, the cost of electricity, providing a backup supply when the grid fails, and counteracting unstable fuel prices.

Use Cases

- Giga-Project Off-Grid Resilience for NEOM & SPARK: Make construction tools, temporary structures, and remote worker camps to become MEGA-project ready like NEOM and SPARK to eliminate diesel logistics and provide long-term operational security.

- Captive Power Across Industrial Value Chain: Examines the patterns of solar generation to industrial plants, such as factories, warehouses, and cold storage, where grid reliance can be minimized, and peak demand rates decreased as the predictability of energy costs is enhanced.

- Power Generation Reliability for Commercial & Agricultural Sites: Monitors PV performance in commercial complexes, greenhouse cooling systems, and water desalination units to streamline maintenance times, prevent costly diesel generator run times, and maximize energy production.

- Workforce Safety and Automated Remote Operations: Reduces frontline fuel handling risks and repetitive generator servicing of an aging workforce, and allows remote diagnostics and data-informed energy choices across industrial facilities.

How AI Is Transforming the Saudi Arabia DG Ground-Mounted Solar PV Market

The Saudi Arabia DG Ground-Mounted Solar PV Market is witnessing a revolutionary change with the adoption of artificial intelligence for predictive energy analytics and automated decision-making. PV data technology leverages machine learning to review historical generation data, soiling patterns, and weather trends to dynamically predict potential performance degradation ahead of time, allowing for preventive cleaning and maintenance rather than reactive loss recovery. AI further helps in demand forecasting of replacement inverters and panels, slashing inventory costs and making the supply chain efficient. In mega-projects like NEOM, AI models simulate multiple failure scenarios for large-scale DG assets to optimize their maintenance.

In addition, AI helps ensure the transparency of sourcing and quality assurance of PV components. There, computer vision and analytics can verify the authenticity of solar panels and inverters, as well as detect micro-cracks or defects with greater accuracy than manual inspection without human judgment errors. Another prediction made it possible to predict sourcing disruption based on geopolitical and environmental data, which is pivotal for Saudi Arabia, ensuring that compliance and reliability are in place, along with reduced dependence on manual testing and reliance on international suppliers.

Market Dynamics

Key Drivers of the Saudi Arabia DG Ground-Mounted Solar PV Market

Saudi Vision 2030 and National Renewable Energy Program (NREP)

The Vision 2030 of the Saudi government, along with the National Renewable Energy Program (NREP) that requires the growth of renewable energy capacity, lessening the use of liquid fuels to generate power, and the localization of solar PV production in all industrial sectors, is the most significant driver of the DG Ground-Mounted Solar PV Market. These government plans established certain goals to produce 58.7 GW of renewable energy by 2030, establishing top-down demand on distributed ground-mounted solar systems and energy performance reporting across the industrial economy, including factories and commercial complexes.

Rising Industrial Electricity Tariffs and Fluctuating Diesel Prices

As the subsidies on energy become phased out faster and the cost of grid electricity to commercial and industrial users rises, the urgent requirement is at the moment for decentralized generation of solar energy, so that vital facilities can continue to work at a reasonable price without any unexpected interruptions in the power supply. The growing instability of the prices of diesel as a backup generation in Saudi Arabia requires efficient DG solar systems to avoid interruptions in production and to ensure against the impacts of changes in fuel prices.

Restraints in Saudi Arabia DG Ground-Mounted Solar PV Market

Underdeveloped Local Manufacturing and Certification Ecosystem

Saudi Arabia does not have a mature local supply chain of certified solar panels, inverters, and mounting structures as compared to China and Europe, meaning that they are forced to rely on extended import logistics. There are no local certification institutions of IEC standards and quick quality assurance, so large-scale DG projects are associated with a delay in procurement and a higher working capital requirement, and hence, it is impossible to achieve rapid adoption without supply chain buffers.

Limited Availability of Bankable DG Solar Project Financing

There is also a shortage of local financial institutions with proven underwriting expertise for distributed solar projects below 10 MW, thus making it necessary to rely on more costly international lenders or corporate balance sheets. This financing gap results in a higher cost of capital and reduced deployment velocity for small and medium enterprises seeking to install DG ground-mounted solar systems.

Growth Opportunities in Saudi Arabia DG Ground-Mounted Solar PV Market

Local Assembly and Manufacturing Under the Saudi Content Program

The development of local panel assembly lines, tracker manufacturing, and inverter integration facilities would be beneficial in decreasing dependency on imports and enabling the Kingdom to achieve the 40% local content requirement for renewable energy projects under the Saudi Content Program. The presence of local manufacturing facilities, automated assembly, and trained technicians would cater to unique market needs prevalent in the Gulf region, including sand-resistant coatings and high-ambient temperature designs.

Wheeling and Corporate PPA Regulatory Reforms

As Saudi Arabia embraces competitive electricity markets, there is an increasing need for wheeling regulations that allow DG solar developers to sell power to multiple off-takers across different locations. Any DG solar installation must be able to export surplus power to the grid and receive fair compensation, creating a huge market for corporate power purchase agreements (PPAs) and energy services companies (ESCOs).

The Saudi Arabia DG Ground-Mounted Solar PV Market Trends

Integration of Solar Forecasting into Industrial Energy Management

PV generation intelligence is being fed into building management systems (BMS) and industrial energy management platforms, enabling real-time load shifting and automatic battery dispatch based on cloud cover predictions. System data on irradiance, module temperature, soiling loss, and inverter performance are being transmitted to factory command centers for centralized energy decision-making and demand charge reduction workflow automation.

Shift from Capex-Heavy Ownership to Solar-as-a-Service Models

Commercial and industrial energy consumers are increasingly adopting leasing models and third-party ownership structures over traditional upfront purchase of DG solar systems to achieve immediate operational expenditure savings and eliminate maintenance responsibilities. This trend is particularly strong in mid-sized industrial facilities and agricultural operations where capital preservation is mission-critical for business continuity.

Research Scope and Analysis

By Component Analysis

The Saudi Arabia market is currently dominated by Solar Panels, accounting for approximately 48.2% of the market share in 2026, reflecting the country's high-volume deployment of DG systems for industrial and commercial assets. These panels offer high-efficiency monocrystalline technology, bifacial options, and full degradation warranties. Their usage is vital to decrease unexpected power shortfalls, maintain production line efficiency, and optimize operational economics.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The segment with the highest CAGR is Inverters due to the country's commitment to maximizing energy harvest and meeting real-time grid compliance needs for DG projects. This segment involves smart inverter reliability management, reactive power control, and proper anti-islanding protocols. Mounting Structures and Balance of System (cables, combiner boxes, monitoring hardware) are gaining traction among project developers for rapid deployment, while Other Components form a smaller but essential supporting segment.

By System Type Analysis

The most prominent segment is Fixed Tilt, accounting for approximately 68.7% of the market share in 2026, as it provides foundational operational simplicity upon which other configurations are built. This segment offers ease of installation, lower capital requirements, and modularity suitable for existing maintenance workflows. The segment with the highest CAGR is Single Axis Tracker because of the growing need for higher energy yield and better integration with afternoon peak demand profiles. Single Axis Trackers will become increasingly important for continuous process factories, while Fixed Tilt will remain essential for small and medium enterprise production cells and pilot lines requiring lower initial investment. Both system types are critical for comprehensive DG solar strategies across different asset classes and operational environments.

By Technology Analysis

The Monocrystalline Silicon segment holds the largest share, representing approximately 71.5% of the market in 2026, as it directly addresses the primary requirement of DG applications, including space constraints, higher efficiency, and better low-light performance. This technology includes PERC cells, half-cut designs, and bifacial architectures to maximize yield per square meter. The Thin Film segment is growing at the highest CAGR due to increasing demand for lightweight, flexible modules for specific applications like carports and low-load-bearing roofs. Multicrystalline silicon remains fundamental for price-sensitive applications, though its share is declining due to the efficiency advantages of mono technology.

By Application Analysis

The Industrial sector accounts for the largest share at approximately 44.2% in 2026, driven by factories, process industries, and logistics hubs requiring captive power to reduce electricity costs and ensure production continuity. The highest CAGR segment is Utility (DG edge-of-grid), as operators of remote distribution networks and grid-support applications prioritize energy reliability and peak shaving. Commercial follows, needing solar for office complexes, retail centers, and hospitality facilities. Residential includes villas and housing compounds, each with specific rooftop and small ground-mount requirements.

Saudi Arabia DG Ground-Mounted Solar PV Market Report is segmented based on the following:

By Component

- Solar Panels

- Inverters

- Mounting Structures

- Balance of System

By System Type

- Fixed Tilt

- Single Axis Tracker

- Dual Axis Tracker

By Technology

- Monocrystalline Silicon

- Thin Film

- Multicrystalline Silicon

By Application

- Residential

- Commercial

- Industrial

- Utility

Competitive Landscape

The Saudi Arabia DG Ground-Mounted Solar PV Market is characterized by large government-backed industrial zones, international PV manufacturers, and local EPC contractors. Competition will focus on supporting Vision 2030 goals through sustainable, localized renewable energy solutions. Anchor stakeholders include the Ministry of Energy, Saudi Aramco, NEOM Industrial City, and SABIC, in addition to global industry leaders for PV technology and technical training programs.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The emerging industrial economy and small-to-medium enterprises are served by local installers and regional distributors. Competition is heating up around AI-driven analytics, performance guarantees, and local manufacturing capabilities. Expect a fragmented market with lots of local startups alongside ongoing international investments in giga-projects and the NIDLP framework.

Some of the prominent players in the Saudi Arabia DG Ground-Mounted Solar PV Market are:

- ACWA Power Company

- Alfanar Company

- Abu Dhabi Future Energy Company (Masdar)

- Saudi Electricity Company

- ENGIE SA

- EDF Renewables

- TotalEnergies SE

- Enel Green Power S.p.A.

- Abdul Latif Jameel Energy Company Limited

- Desert Technologies Industries Factory Company

- Nesma & Partners Contracting Company Ltd.

- Sterling and Wilson Renewable Energy Limited

- Larsen & Toubro Limited

- Power Construction Corporation of China, Ltd.

- JinkoSolar Holding Co., Ltd.

- LONGi Green Energy Technology Co., Ltd.

- Trina Solar Co., Ltd.

- Canadian Solar Inc.

- First Solar, Inc.

- JA Solar Technology Co., Ltd.

- Other Key Players

Recent Developments

- November 2025: EDF Renewables secured financing for two large solar PV projects (1.4 GW total capacity) in Saudi Arabia, supported by long-term PPAs and expected to be operational by 2027.

- November 2025: Total Energies SE, in partnership with Toyota Tsusho and Altaaqa Renewable Energy (Zahid Group), commenced commercial operations of a 112 MW solar PV plant in Wadi Ad-Dawasir, marking its first operational renewable energy project in Saudi Arabia under the National Renewable Energy Program.

- October 2025: Saudi Electricity Company and EDF Renewables signed a 25-year Power Purchase Agreement (PPA) for the 600 MW Samtah solar PV project, marking a major milestone in Saudi Arabia’s renewable expansion pipeline.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 400.1 Mn |

| Forecast Value (2035) |

USD 1,150.6 Mn |

| CAGR (2026–2035) |

12.5% |

| Historical Period |

2021 – 2025 |

| Forecast Period |

2027 – 2035 |

| Base Year |

2025 |

| Estimated Year |

2026 |

| Segments Covered |

By Component (Solar Panels, Inverters, Mounting Structures, Balance of System), By System Type (Fixed Tilt, Single Axis Tracker, Dual Axis Tracker), By Technology (Monocrystalline Silicon, Thin Film, Multicrystalline Silicon), By Application (Residential, Commercial, Industrial, Utility) |

| Country Coverage |

Saudi Arabia |

Frequently Asked Questions

How big is the Saudi Arabia DG Ground-Mounted Solar PV Market?

▾ The Saudi Arabia DG Ground-Mounted Solar PV Market size is estimated to have a value of USD 400.1 million in 2026 and is expected to reach USD 1,150.6 million by the end of 2035.

What is the CAGR of the Saudi Arabia DG Ground-Mounted Solar PV Market from 2026 to 2035?

▾ The market is growing at a CAGR of 12.5% over the forecasted period.

What factors are driving the growth of the Saudi Arabia DG Ground-Mounted Solar PV Market?

▾ The rising industrial electricity tariffs and diesel cost volatility requiring localized renewable generation, along with Saudi Vision 2030 and the National Renewable Energy Program (NREP), are the key factors driving the market growth.

What are the major trends in the Saudi Arabia DG Ground-Mounted Solar PV Market?

▾ Major trends include integration of solar forecasting into industrial energy management systems and a significant shift from Capex-heavy ownership to Solar-as-a-Service (leasing/PPA) models.

Who are the key players in the Saudi Arabia DG Ground-Mounted Solar PV Market?

▾ Some of the major key players in the Saudi Arabia DG Ground-Mounted Solar PV Market are Abu Dhabi Future Energy Company (Masdar), Saudi Electricity Company, ENGIE SA, TotalEnergies SE, Enel Green Power S.p.A., JinkoSolar Holding Co., Ltd., and many others.

How is the Saudi Arabia DG Ground-Mounted Solar PV Market segmented?

▾ The market is segmented by Component, System Type, Technology, and Application.