Market Overview

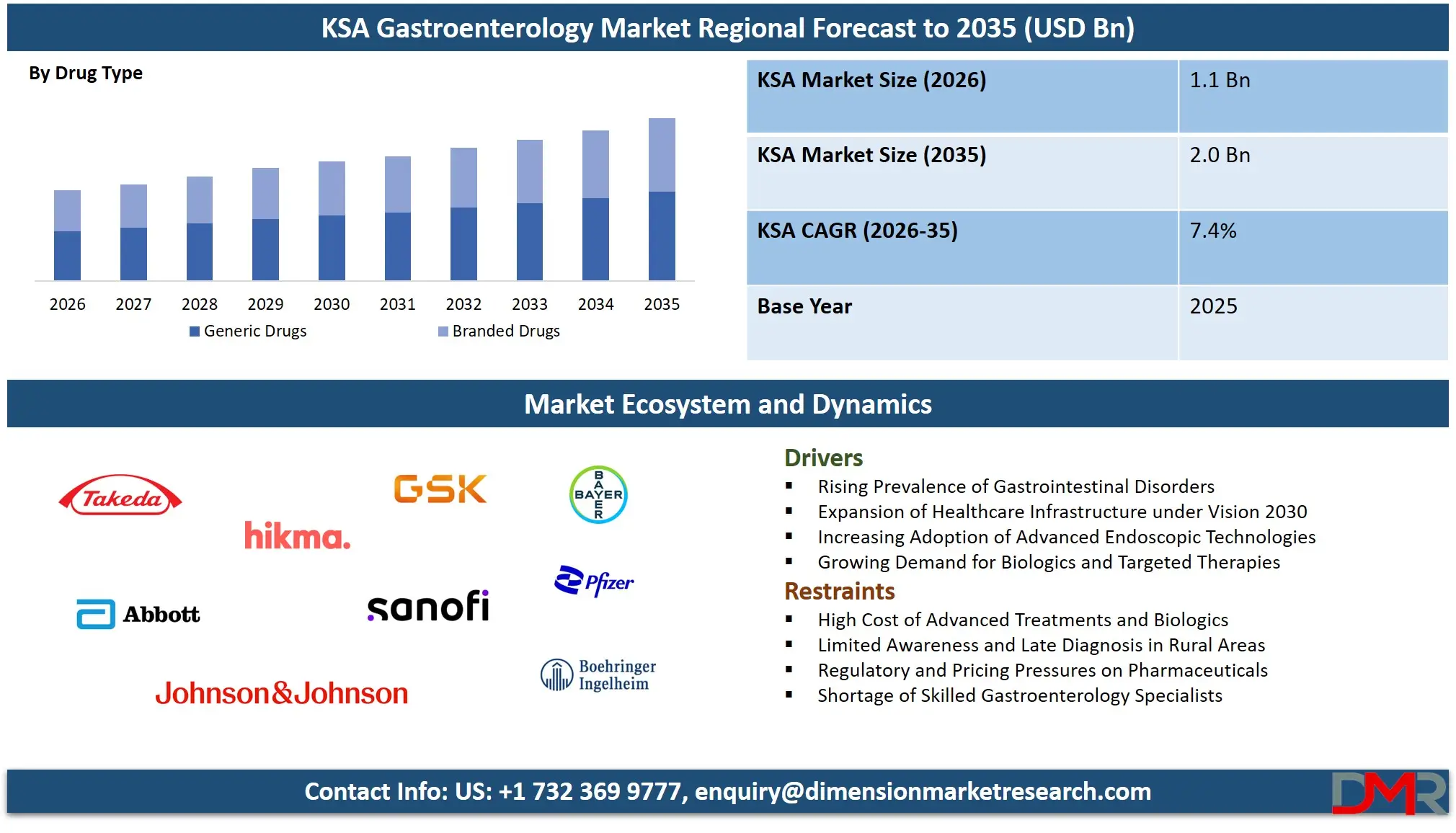

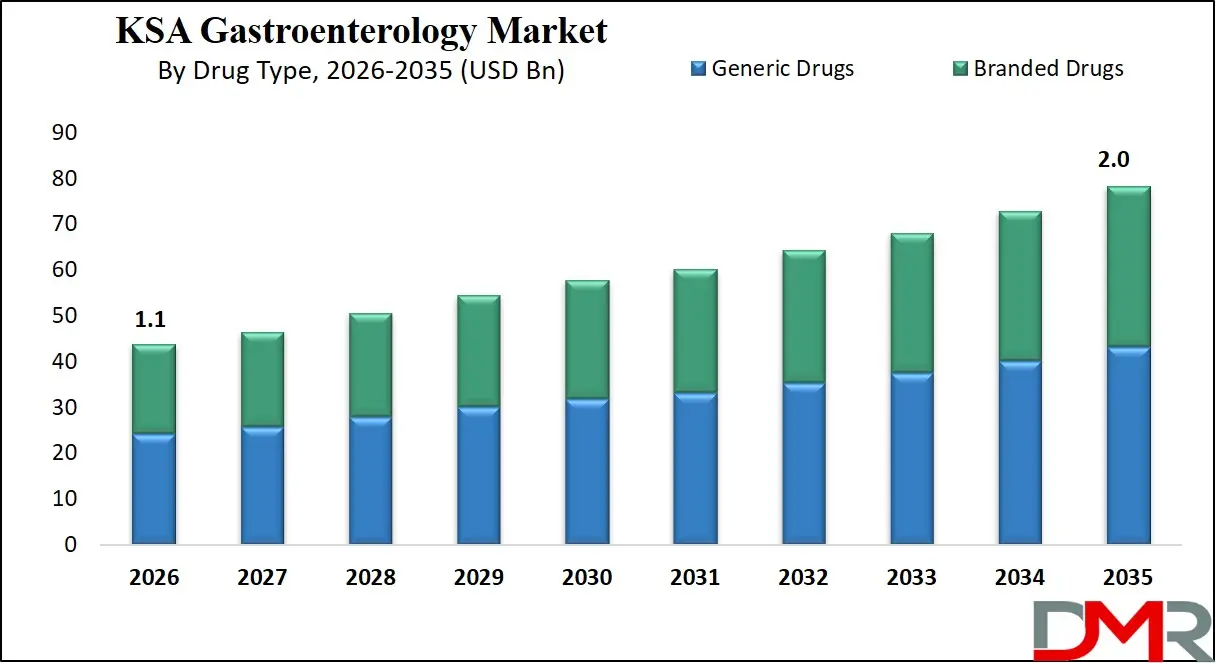

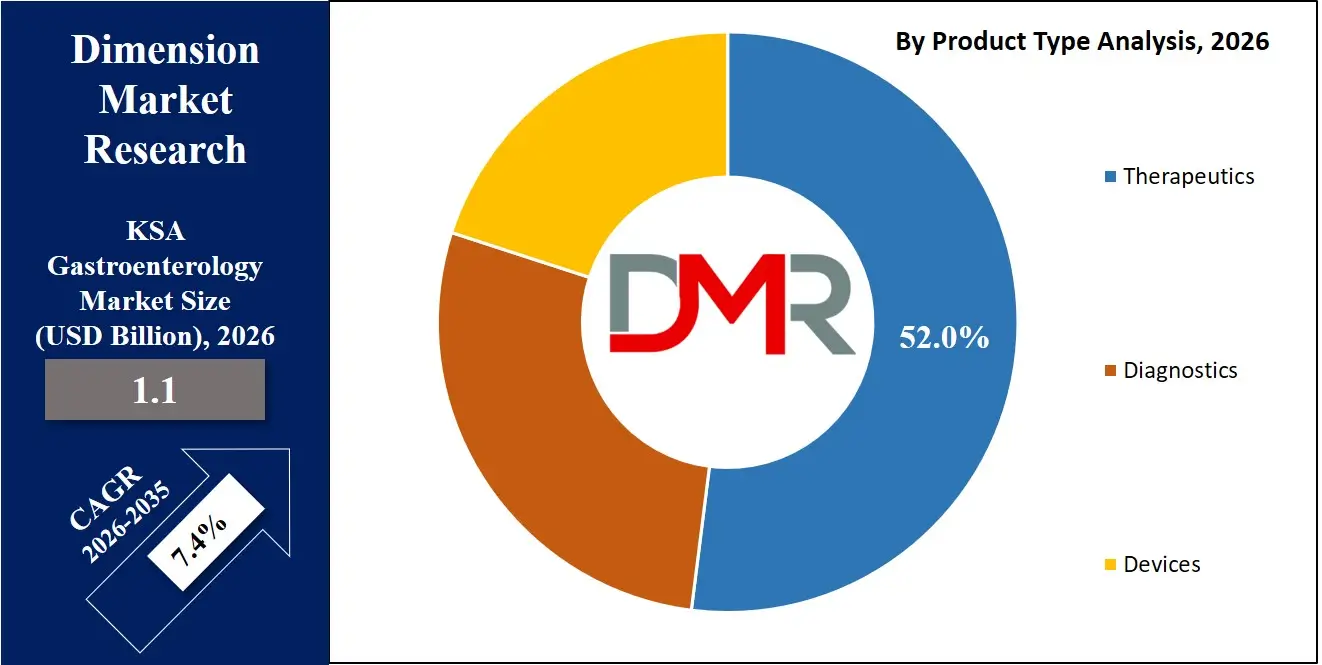

Saudi Arabia gastroenterology market is expected to reach USD 1.1 billion in 2026 and further grow to USD 2.0 billion by 2035, registering a CAGR of 7.4% during the forecast period, supported by rising gastrointestinal disease burden and increasing demand for advanced digestive care solutions.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Gastroenterology is a specialized branch of medicine focused on the structure, function, and disorders of the digestive system, including the esophagus, stomach, intestines, liver, pancreas, and gallbladder. It involves the diagnosis, treatment, and prevention of a wide range of gastrointestinal conditions such as acid reflux, peptic ulcers, irritable bowel syndrome, inflammatory bowel disease, and liver diseases. This field integrates clinical evaluation with advanced diagnostic procedures like endoscopy, colonoscopy, imaging techniques, and laboratory testing to assess digestive health. Gastroenterology also plays a critical role in managing chronic conditions, improving nutrient absorption, and supporting overall metabolic health, while continuously evolving through innovations in minimally invasive procedures, biologic therapies, and precision medicine.

The KSA gastroenterology market represents a rapidly developing segment of the healthcare industry, driven by the rising burden of digestive disorders and increasing healthcare investments across Saudi Arabia. The market encompasses a broad spectrum of products and services including gastrointestinal therapeutics, diagnostic procedures, and medical devices used for screening, monitoring, and treatment. Growth is supported by the increasing prevalence of lifestyle related conditions such as gastroesophageal reflux disease, obesity associated liver disorders, and colorectal cancer, along with improved access to healthcare services. The adoption of advanced technologies such as endoscopic imaging systems and minimally invasive surgical instruments is enhancing early diagnosis and treatment outcomes across hospitals and specialty clinics.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

In addition, the market is benefiting from ongoing healthcare transformation initiatives aligned with Vision 2030, which aim to strengthen healthcare infrastructure, promote private sector participation, and improve patient care standards. Pharmaceutical demand is witnessing a shift toward biologics, biosimilars, and targeted drug therapies, while diagnostic capabilities are expanding through digital health solutions and integrated laboratory networks. Increasing awareness regarding preventive healthcare and routine screening is further contributing to market expansion, particularly in urban centers. At the same time, the growing role of retail and online pharmacies is improving the accessibility of gastrointestinal medications, supporting the overall development of the gastroenterology ecosystem in Saudi Arabia.

KSA Gastroenterology Market: Key Takeaways

- Strong Market Expansion Outlook: The market is expected to grow from USD 1.1 billion in 2026 to USD 2.0 billion by 2035, reflecting steady long term expansion supported by rising GI disease burden.

- Therapeutics Segment Leadership: Therapeutics dominate with 52.0% market share, driven by high demand for biologics, small molecules, and long term gastrointestinal drug therapies.

- Oral Medications Driving Treatment Demand: Oral route leads with 58.0% share, supported by widespread use of proton pump inhibitors and high patient preference for convenient drug administration.

- Generics Dominating Drug Landscape: Generic drugs account for 55.0% of total share, highlighting strong demand for cost effective gastrointestinal treatments across Saudi Arabia.

- High Disease Prevalence Supporting Demand: Over 30% of the population is affected by GI disorders, with GERD alone contributing 26.0% of application share, reinforcing sustained demand for diagnostics and therapeutics.

KSA Gastroenterology Market: Use Cases

- Advanced Endoscopic Diagnostics: Hospitals in Saudi Arabia are increasingly using endoscopy and colonoscopy for early detection of gastrointestinal disorders such as colorectal cancer and ulcers. This supports demand for minimally invasive procedures and improves diagnostic accuracy.

- Biologics for Chronic GI Diseases: Growing cases of inflammatory bowel disease are driving the use of biologics and targeted therapies. These treatments enhance disease management and support long term remission in digestive disorders.

- Management of Lifestyle Related GI Disorders: Rising incidence of GERD, IBS, and liver disorders due to lifestyle changes is increasing demand for gastrointestinal drugs and digestive health treatments across the KSA market.

- Expansion of Retail and Online Pharmacies: The growth of retail and online pharmacies is improving access to gastrointestinal medications, supporting drug distribution and enhancing patient convenience in Saudi Arabia.

Impact of US-Iran Conflict in the KSA Gastroenterology Market

- Economic Uncertainty and Cost Inflation: Escalating tensions between the US and Iran drive volatility in global oil prices, raising operating costs for healthcare providers in Saudi Arabia. This increases expenses for importing advanced gastroenterology equipment, diagnostics technologies, and therapeutic drugs, which rely on stable logistics and commodity pricing.

- Healthcare Budget Reallocations and Supply Chain Pressure: Geopolitical risks may prompt Saudi Arabia to prioritize defense and infrastructure spending over healthcare budgets, potentially affecting investment in specialized medical segments like gastroenterology. Disruptions in supply chains for medical devices and pharmaceuticals could slow the procurement of advanced diagnostics and treatment technologies.

- Investor Confidence and Long‑Term Healthcare Planning: Persistent US‑Iran conflict contributes to economic uncertainty that can reduce investor confidence in healthcare innovation and private gastroenterology initiatives. Slower foreign investment inflows may delay infrastructure expansion, digital health integration, and adoption of AI‑enabled diagnostics across the Saudi gastroenterology sector.

KSA Gastroenterology Market: Stats & Facts

- General Authority for Statistics (GASTAT) – Saudi Arabia (2024–2025)

- Obesity prevalence among adults aged 15+ reached 23.1% in 2024.

- Overweight population aged 15+ accounted for 45.1% in 2024.

- Childhood obesity among ages 2–14 stood at 14.6% in 2024.

- Around 33.3% of children were overweight in 2024.

- Only 10.2% of the population met recommended fruit and vegetable intake in 2024.

- Approximately 84.8% consumed only 1–4 servings daily in 2024.

- About 5% reported zero daily fruit and vegetable intake in 2024.

- National surveys during 2023–2024 indicate increasing lifestyle risk factors linked to digestive disorders.

- Saudi Ministry of Health & National Health Surveys (2023–2025)

- Nearly 32–33% of adults experience functional gastrointestinal disorders.

- Around 54.4% of GI patients seek medical consultation annually.

- Female prevalence of GI disorders reached 73.8% compared to 26.2% in males.

- Hospital visits related to digestive health conditions are increasing across regions.

- National screening programs have improved early detection of gastrointestinal diseases.

- Healthcare utilization for GI conditions showed steady growth between 2023 and 2025.

KSA Gastroenterology Market: Market Dynamic

Driving Factors in the KSA Gastroenterology Market

Rising Burden of Gastrointestinal and Liver Disorders

The increasing prevalence of gastrointestinal diseases such as GERD, irritable bowel syndrome, inflammatory bowel disease, and nonalcoholic fatty liver disease is a major growth driver in Saudi Arabia. Sedentary lifestyles, changing dietary patterns, and obesity are contributing to higher incidence rates, thereby boosting demand for digestive disease treatment, gastrointestinal drugs, and diagnostic procedures including endoscopy and colonoscopy.

Healthcare Transformation and Infrastructure Expansion

Ongoing healthcare reforms under Vision 2030 are significantly enhancing hospital infrastructure, specialty clinics, and diagnostic capabilities. Increased public and private investments are supporting the adoption of advanced medical devices, minimally invasive procedures, and digital health solutions, which in turn are driving growth in gastrointestinal diagnostics, therapeutics, and patient care services.

Restraints in the KSA Gastroenterology Market

High Cost of Advanced Therapies and Procedures

The cost associated with biologics, targeted therapies, and advanced endoscopic equipment remains high, limiting widespread adoption. This creates affordability challenges, particularly for long term treatment of chronic gastrointestinal disorders, impacting overall market penetration despite rising demand.

Shortage of Specialized Gastroenterology Professionals

Limited availability of skilled gastroenterologists and trained endoscopy professionals can restrict the expansion of specialized digestive care services. This gap affects timely diagnosis and treatment, especially in non-urban regions, thereby constraining market growth.

Opportunities in the KSA Gastroenterology Market

Growing Demand for Preventive Screening and Early Diagnosis

Increasing awareness regarding preventive healthcare is creating strong opportunities for routine screening programs such as colonoscopy for colorectal cancer detection. Expansion of diagnostic centers and screening initiatives is expected to drive demand for gastrointestinal diagnostics and laboratory testing services.

Expansion of Biosimilars and Generic Drug Market

The rising focus on cost effective treatment options is opening opportunities for biosimilars and generic gastrointestinal drugs. Local pharmaceutical manufacturers are strengthening their presence, improving drug accessibility and supporting the overall growth of the digestive health therapeutics market.

Trends in the KSA Gastroenterology Market

Shift toward Minimally Invasive and Endoscopic Procedures

There is a growing trend toward minimally invasive techniques such as advanced endoscopy and laparoscopic interventions. These procedures offer reduced recovery time, improved patient outcomes, and lower hospital stays, driving adoption across hospitals and specialty clinics.

Integration of Digital Health and AI in GI Diagnostics

The adoption of digital health platforms and artificial intelligence in gastrointestinal diagnostics is transforming disease detection and monitoring. AI powered imaging, electronic health records, and telemedicine solutions are enhancing diagnostic accuracy and enabling better management of digestive disorders in Saudi Arabia.

KSA Gastroenterology Market: Research Scope and Analysis

By Product Type Analysis

Therapeutics are expected to lead the product type segment in the KSA gastroenterology market, accounting for around 52.0% of the total market share in 2026, primarily driven by the growing burden of chronic gastrointestinal disorders such as GERD, inflammatory bowel disease, and liver conditions. The increasing reliance on pharmaceutical treatment for long term disease management, along with the rising adoption of biologics, biosimilars, and small molecule drugs, is significantly contributing to segment growth. Oral medications including proton pump inhibitors and antacids continue to witness high demand due to their widespread use in managing acid related disorders, while advanced biologic therapies are gaining traction for complex conditions like Crohn’s disease and ulcerative colitis. In addition, supportive government policies promoting access to cost effective generic drugs are further strengthening the therapeutics landscape in Saudi Arabia.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Diagnostics also hold a substantial share in the market, supported by the increasing focus on early disease detection and preventive healthcare. The demand for gastrointestinal diagnostics is rising with the growing adoption of endoscopic procedures such as colonoscopy and gastroscopy, which are essential for identifying conditions like colorectal cancer, ulcers, and inflammatory diseases at an early stage. Imaging techniques and laboratory testing are also playing a crucial role in accurate diagnosis and disease monitoring. The expansion of diagnostic centers, improvements in healthcare infrastructure, and integration of advanced imaging technologies are enhancing diagnostic capabilities across the country. As awareness regarding routine screening continues to increase, particularly for colorectal cancer, the diagnostics segment is expected to witness steady growth in the KSA gastroenterology market.

By Route of Administration Analysis

Oral medications are expected to dominate the route of administration segment in the KSA gastroenterology market, accounting for approximately 58.0% of the total market share in 2026, primarily due to their convenience, cost effectiveness, and widespread use in managing common gastrointestinal disorders. A large patient population suffering from conditions such as gastroesophageal reflux disease, irritable bowel syndrome, and peptic ulcers relies heavily on oral drugs including proton pump inhibitors, antacids, and antispasmodics for long term symptom control. The ease of administration, strong availability through retail and online pharmacies, and high patient compliance are key factors supporting the dominance of oral formulations. Additionally, the growing preference for generic gastrointestinal drugs is further boosting the adoption of oral medications across Saudi Arabia.

Injectables also represent a significant segment, particularly for the treatment of severe and chronic gastrointestinal diseases that require rapid or targeted therapeutic action. Biologics and advanced drug therapies administered through injections are increasingly used for conditions such as inflammatory bowel disease and certain liver disorders, where oral treatments may be less effective. These injectable therapies offer higher efficacy and improved disease control, especially in hospital settings and specialty clinics. Although their usage is comparatively lower due to higher costs and the need for clinical supervision, the demand for injectable gastrointestinal treatments is rising with the increasing adoption of biologics and the expansion of advanced healthcare services in the KSA market.

By Drug Type Analysis

Generic drugs are expected to dominate the drug type segment in the KSA gastroenterology market, accounting for approximately 55.0% of the total market share in 2026, mainly due to their affordability and widespread availability. The increasing focus on cost containment within the Saudi healthcare system, along with supportive government policies encouraging the use of low cost alternatives, is driving strong demand for generic gastrointestinal medications. These drugs are widely used in the treatment of common digestive disorders such as GERD, irritable bowel syndrome, and peptic ulcers, particularly in long term therapy where cost efficiency is critical. The presence of local pharmaceutical manufacturers and the expansion of retail and online pharmacies are further strengthening the accessibility and adoption of generic drugs across the country.

Branded drugs also hold a significant share in the market, particularly in the treatment of complex and chronic gastrointestinal conditions that require advanced therapeutic solutions. These include innovative biologics and targeted therapies used for inflammatory bowel disease, colorectal cancer, and severe liver disorders, where higher efficacy and specialized formulations are essential. Branded gastrointestinal drugs are often preferred in hospital settings and specialty care due to their established clinical outcomes and strong research backing. Although their higher cost limits widespread use compared to generics, the demand for branded drugs is supported by increasing healthcare spending, improved access to advanced treatments, and the growing need for effective management of severe digestive diseases in Saudi Arabia.

By Application Analysis

Gastroesophageal reflux disease is expected to dominate the application segment in the KSA gastroenterology market, accounting for approximately 26.0% of the total market share in 2026, primarily due to its high prevalence and recurring nature. Factors such as unhealthy dietary habits, rising obesity rates, and sedentary lifestyles in Saudi Arabia are significantly contributing to the growing incidence of acid related disorders. This has led to sustained demand for gastrointestinal drugs including proton pump inhibitors, antacids, and H2 receptor blockers for long term symptom management. The ease of diagnosis, high patient awareness, and continuous need for maintenance therapy are key elements supporting the dominance of GERD within the digestive disease treatment landscape.

Irritable bowel syndrome also represents a notable share in the market, driven by increasing cases linked to stress, dietary patterns, and lifestyle changes. The condition requires ongoing management through a combination of gastrointestinal medications, dietary modifications, and supportive therapies, which contributes to steady demand for treatment solutions. Although IBS is less severe compared to other chronic gastrointestinal disorders, its high prevalence and impact on quality of life are encouraging patients to seek medical attention and long term care. The growing availability of targeted therapies and improved diagnostic approaches is further supporting the expansion of the IBS segment within the KSA gastroenterology market.

By End-User Analysis

Hospitals are expected to dominate the end user segment in the KSA gastroenterology market, accounting for approximately 48.0% of the total market share in 2026, primarily due to their advanced healthcare infrastructure and ability to provide comprehensive gastrointestinal care. These facilities handle a high volume of patients requiring complex procedures such as endoscopy, colonoscopy, and minimally invasive surgeries, along with the administration of biologics and injectable therapies. Hospitals also offer integrated services including diagnostics, treatment, and post procedure care, making them the preferred choice for managing chronic and severe gastrointestinal disorders such as inflammatory bowel disease, colorectal cancer, and liver diseases. Continuous investments under healthcare modernization initiatives are further strengthening hospital capabilities and driving their dominance in the market.

Diagnostic centers also play a crucial role in the market by focusing on early detection and routine screening of gastrointestinal conditions. These centers are increasingly equipped with advanced imaging technologies, laboratory testing services, and specialized endoscopic procedures, supporting accurate and timely diagnosis of disorders such as GERD, ulcers, and colorectal cancer. The growing emphasis on preventive healthcare and rising awareness about regular screening are driving patient inflow to diagnostic facilities. Additionally, the expansion of standalone diagnostic centers and their accessibility in urban areas are contributing to the steady growth of this segment within the KSA gastroenterology market.

The KSA Gastroenterology Market Report is segmented on the basis of the following:

By Product Type

- Therapeutics

- Biologics

- Biosimilars

- Small Molecules

- Diagnostics

- Endoscopic Procedures

- Imaging

- Lab Tests

- Devices

- Biopsy Tools

- Surgical Instruments

By Route of Administration

- Injectables

- Oral Medications

- Others

By Drug Type

- Branded Drugs

- Generic Drugs

By Application

- Inflammatory Bowel Disease (IBD)

- Gastroesophageal Reflux Disease (GERD)

- Irritable Bowel Syndrome (IBS)

- Colorectal Cancer

- Liver Disorders

By End-User

- Hospitals

- Diagnostic Centers

- Retail Pharmacies

- Online Pharmacies

Impact of Artificial Intelligence in the KSA Gastroenterology Market

Artificial intelligence is playing a transformative role in the KSA gastroenterology market by enhancing the accuracy and efficiency of gastrointestinal diagnostics. AI powered imaging systems are increasingly being integrated with endoscopy and colonoscopy procedures to improve the detection of abnormalities such as polyps, early stage colorectal cancer, and inflammatory lesions. These advanced systems assist clinicians in real time decision making, reducing the risk of missed diagnoses and improving patient outcomes. In addition, AI driven data analytics and electronic health records are enabling better disease prediction, patient stratification, and personalized treatment planning, supporting the overall advancement of digestive disease management in Saudi Arabia.

Beyond diagnostics, artificial intelligence is also influencing treatment optimization and healthcare delivery across the gastroenterology ecosystem. AI based tools are helping in monitoring chronic gastrointestinal conditions such as inflammatory bowel disease and liver disorders by analyzing patient data and predicting disease progression. Telemedicine platforms integrated with AI are improving access to specialized gastroenterology care, particularly in remote areas, while also enhancing patient engagement and follow up care. As healthcare digitalization continues to expand under national transformation initiatives, the adoption of AI in gastrointestinal therapeutics, diagnostics, and workflow management is expected to significantly drive innovation and operational efficiency in the KSA market.

KSA Gastroenterology Market: Competitive Landscape

The KSA gastroenterology market exhibits a moderately competitive landscape characterized by the presence of both multinational corporations and established regional players competing across therapeutics, diagnostics, and medical devices segments. Global companies such as Medtronic, Fujifilm, Stryker, and Smith and Nephew dominate the advanced endoscopy and minimally invasive device space through continuous innovation and technology upgrades, while pharmaceutical giants including Pfizer, GSK, and AstraZeneca lead in branded gastrointestinal therapeutics.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

At the same time, local manufacturers such as SPIMACO, Tabuk Pharmaceuticals, and Jamjoom Pharma strengthen the market through cost effective generic drug production and strong distribution networks. Competition is largely driven by product innovation, expansion of healthcare infrastructure, pricing strategies, and partnerships with government healthcare entities, with increasing focus on biologics, biosimilars, and advanced diagnostic solutions shaping the competitive dynamics in Saudi Arabia.

Some of the prominent players in the KSA Gastroenterology Market are:

- Takeda Pharmaceutical Company

- Hikma Pharmaceuticals PLC

- Abbott Laboratories

- Johnson & Johnson Services, Inc.

- GlaxoSmithKline PLC

- Sanofi S.A.

- Bayer AG

- Boehringer Ingelheim International GmbH

- Pfizer Inc.

- AstraZeneca PLC

- Saudi Pharmaceutical Industries & Medical Appliances Corporation (SPIMACO)

- Tabuk Pharmaceuticals Manufacturing Company

- Jamjoom Pharmaceuticals Company

- Avalon Pharma (Middle East Pharmaceutical Industries Co.)

- Gulf Pharmaceutical Industries (Julphar)

- Medtronic PLC

- Stryker Corporation

- KARL STORZ SE & Co. KG

- Fujifilm Holdings Corporation

- Smith & Nephew PLC

- Other Key Players

Recent Developments in the KSA Gastroenterology Market

- February 2026: Medtronic announced the launch and CE Mark approval of its next generation GI Genius module with ColonPRO software, enhancing AI assisted colonoscopy with real time polyp detection and improved diagnostic accuracy in gastrointestinal procedures.

- April 2025: Medtronic entered into a strategic agreement with Dragonfly Endoscopy to distribute advanced pancreaticobiliary endoscopy technology, enhancing precision and therapeutic capabilities in gastrointestinal procedures.

- April 2024: Medtronic unveiled advanced AI driven innovations for endoscopic care including upgraded ColonPRO software for the GI Genius system, improving workflow efficiency and polyp detection capabilities in gastroenterology diagnostics.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 1.1 Bn |

| Forecast Value (2035) |

USD 2.0 Bn |

| CAGR (2026–2035) |

7.4% |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors and etc. |

| Segments Covered |

By Product Type (Therapeutics, Diagnostics, Devices), By Route of Administration (Injectables, Oral Medications, Others), By Drug Type (Branded Drugs, Generic Drugs), By Application (Inflammatory Bowel Disease, Gastroesophageal Reflux Disease, Irritable Bowel Syndrome, Colorectal Cancer, Liver Disorders), By End-User (Hospitals, Diagnostic Centers, Retail Pharmacies, Online Pharmacies) |

| Country Coverage |

Saudi Arabia |

| Prominent Players |

Takeda Pharmaceutical Company, Hikma Pharmaceuticals PLC, Abbott Laboratories, Johnson & Johnson Services Inc., GlaxoSmithKline PLC, Sanofi S.A., Bayer AG, Boehringer Ingelheim International GmbH, Pfizer Inc., AstraZeneca PLC, Saudi Pharmaceutical Industries & Medical Appliances Corporation (SPIMACO), Tabuk Pharmaceuticals Manufacturing Company, Jamjoom Pharmaceuticals Company, Avalon Pharma, Gulf Pharmaceutical Industries (Julphar), Medtronic PLC, Stryker Corporation, KARL STORZ SE & Co. KG, Fujifilm Holdings Corporation, Smith & Nephew PLC, and Other Key Players |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users) and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days and 5 analysts working days respectively. |

Frequently Asked Questions

How big is the KSA Gastroenterology Market?

▾ The KSA Gastroenterology Market size is estimated to have a value of USD 1.1 billion in 2026 and is expected to reach USD 2.0 billion by the end of 2035.

What is the growth rate in the KSA Gastroenterology Market in 2026?

▾ The market is growing at a CAGR of 7.4% over the forecasted period of 2026.

Who are the key players in the KSA Gastroenterology Market?

▾ Some of the major key players in the KSA Gastroenterology Market are Takeda Pharmaceutical Company, Hikma Pharmaceuticals PLC, Abbott Laboratories, Johnson & Johnson Services Inc., GlaxoSmithKline PLC, Sanofi S.A., Bayer AG, Boehringer Ingelheim International GmbH, Pfizer Inc., AstraZeneca PLC, Saudi Pharmaceutical Industries & Medical Appliances Corporation (SPIMACO), Tabuk Pharmaceuticals Manufacturing Company, and many others.