Market Overview

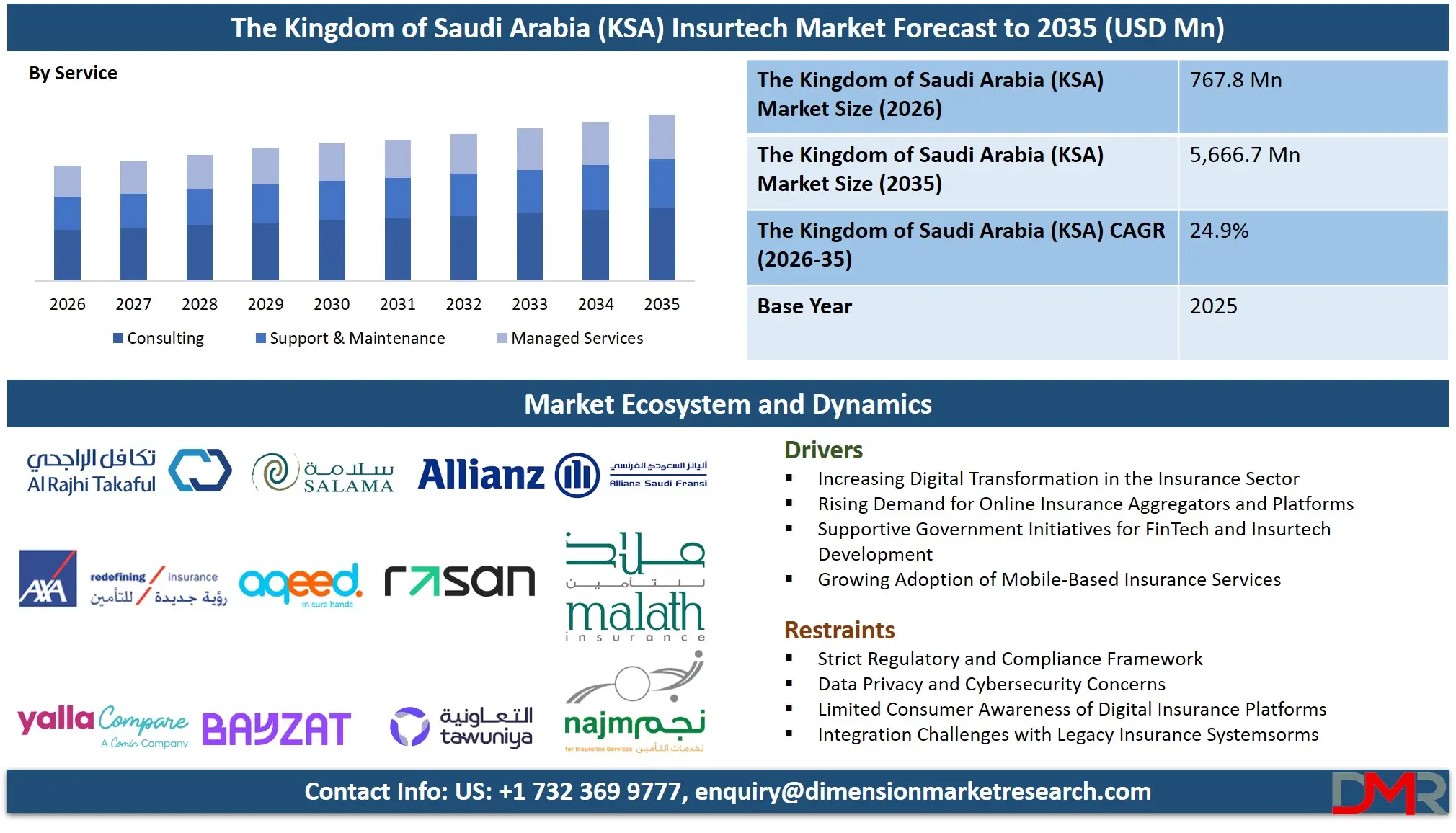

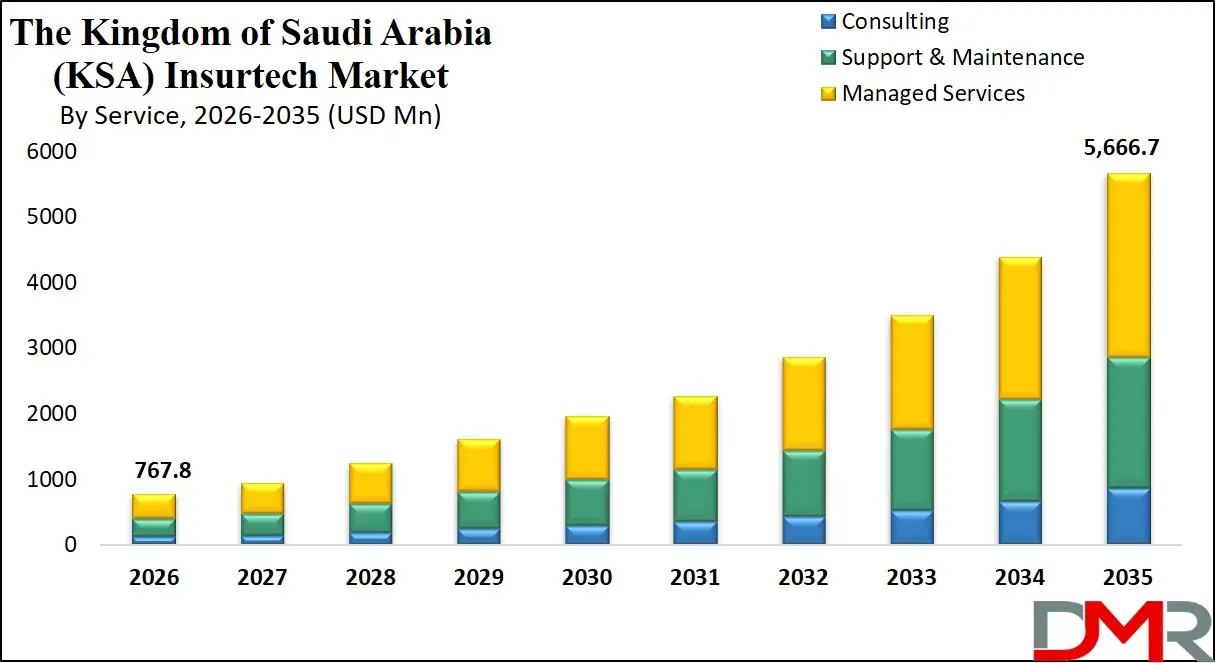

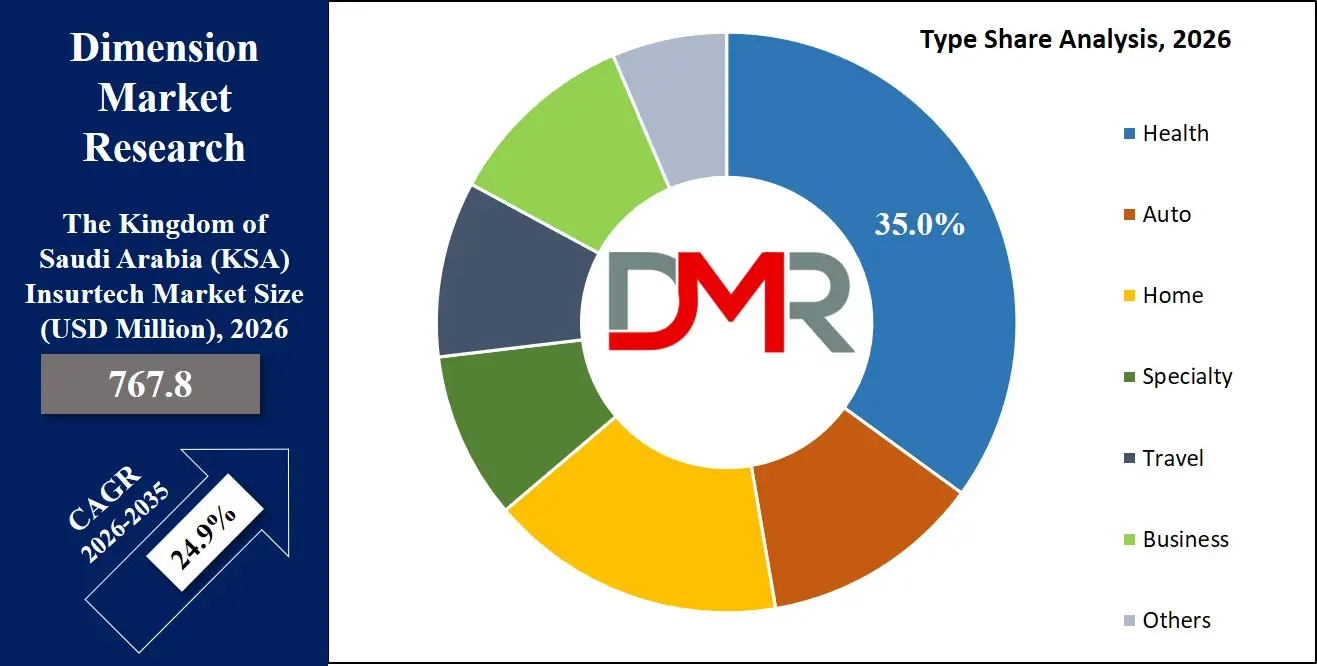

Saudi Arabia insurtech market is projected to reach USD 767.8 million in 2026 and is expected to expand significantly to USD 5,666.7 million by 2035, registering a strong CAGR of 24.9% during the forecast period. This rapid growth reflects the country’s broader digital transformation and financial sector modernization under Vision 2030, which aims to diversify the economy beyond oil while strengthening fintech and digital financial services.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Insurtech defined as the integration of advanced technologies into insurance operations has become a critical component of Saudi Arabia’s evolving financial ecosystem, supporting digital insurance distribution, automated underwriting, claims management platforms, and technology-driven risk assessment systems. These innovations are helping expand financial inclusion and improve access to insurance across sectors such as healthcare, mobility, logistics, and manufacturing.

The Saudi insurtech landscape has undergone a notable transformation with the integration of artificial intelligence, Internet of Things (IoT), big data analytics, and blockchain technologies. These tools enable real-time risk monitoring, predictive analytics, automated claims processing, and personalized insurance products, significantly enhancing operational efficiency and customer engagement. Additionally, the rapid growth of a digitally connected population, high smartphone penetration, and rising adoption of mobile financial services are accelerating demand for digital-first insurance solutions, embedded insurance products, and usage-based insurance models. The emergence of e-commerce ecosystems and digital marketplaces is also influencing insurers to develop flexible and on-demand coverage options tailored to modern consumer expectations.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Government-backed digital infrastructure investments and fintech innovation initiatives are creating strong opportunities for market expansion. Programs such as regulatory sandboxes, fintech accelerators, and large-scale development projects including smart city initiatives like NEOM and the Red Sea Project are strengthening the digital ecosystem necessary for insurtech growth. However, the sector still faces challenges including regulatory complexity, evolving compliance frameworks, cybersecurity concerns, and a shortage of specialized insurtech talent. Despite these constraints, increasing venture investments, strategic partnerships between insurers and technology firms, and supportive regulatory reforms are expected to accelerate innovation. As Saudi Arabia continues to build a digitally driven financial economy, the insurtech sector is poised to play a transformative role in reshaping the country’s insurance landscape and advancing its long-term economic diversification goals.

The Kingdom of Saudi Arabia (KSA) Insurtech Market: Key Takeaways

- Market Value: The Kingdom of Saudi Arabia Insurtech Market size is estimated to have a value of USD 767.8 million in 2026 and is expected to reach USD 5,666.7 million by the end of 2035.

- By Type Segment Analysis: Health insurance is anticipated to dominate this segment in this market as it will hold 35.0% of market share in 2026.

- By Technology Segment Analysis: Cloud computing is projected to dominate the technology segment in the KSA Insurtech Market with the highest market share in 2026.

- By Service Segment Analysis: The managed services segment is anticipated to dominate the KSA insurtech market with major market share in 2026.

- By End User Segment Analysis: Healthcare is projected to hold the leading position in the end-user segment of this market in 2026.

- Key Players: Some of the major key players in the Kingdom of Saudi Arabia Insurtech Market are Saudi Insurance Services, Tawuniya, MedGulf, Bupa Arabia, Walaa Cooperative Insurance, Alinma Tokio Marine Company, and many others.

- Market Growth Rate: The market is growing at a CAGR of 24.9 percent over the forecasted period.

Impact of the Iran Conflict on the Kingdom of Saudi Arabia (KSA) Insurtech Market

- Surge in Demand: Businesses are urgently seeking Political Violence and Cyber insurance to protect against missile strikes, riots, and state-backed hacking. This has created a new, high-demand niche for insurtechs offering rapid, digital underwriting for these complex risks.

- Market Repricing: Premiums for war-related covers have skyrocketed, with some increasing from 1% to 5% of asset value. Insurers are hardening terms and reducing capacity, forcing insurtechs to adapt pricing models and find new partners for high-risk coverage.

- Infrastructure Threats: Physical and cyber-attacks on regional data centers have disrupted cloud services that insurtechs rely on. This vulnerability is driving demand for robust cybersecurity solutions and testing "war exclusions" in cyber policies, creating potential coverage disputes.

- Investment Slowdown: The conflict has dampened international investor sentiment, threatening the venture capital funding that fuels insurtech growth. Extended conflicts risk creating longer fundraising cycles and a potential slowdown in innovation and market expansion for startups.

- Sector Disruption: Reduced global travel due to the conflict is directly dampening demand for travel insurance. Simultaneously, potential supply chain disruptions are increasing credit risks for SMEs, likely impacting trade credit insurance claims and related insurtech products.

The Kingdom of Saudi Arabia (KSA) Insurtech Market: Use Cases

- Digital Health Insurance: This is about optimization of policy issuance, claims processing, and telemedicine integration because of emerging demands for seamless healthcare coverage to offer fast, accurate, and cost-efficient insurance solutions across urban and rural areas.

- Usage-Based Auto Insurance: Automotive insurance would leverage telematics and IoT for real-time monitoring of driving behavior; state-of-the-art insurtech technology ensures that premiums are personalized and claims are handled most professionally with enhanced customer engagement.

- Parametric Insurance Solutions: Timely payouts for weather-related events, natural disasters, or business interruptions; blockchain-enabled smart contracts and real-time data feeds play a very critical role in automated claims settlement.

- Embedded Insurance in E-commerce: Streamlining policy administration, underwriting, and digital distribution to facilitate purchase protection and meet diverse consumer demands for on-demand coverage across different retail platforms.

The Kingdom of Saudi Arabia (KSA) Insurtech Market: Stats & Facts

Saudi Central Bank (SAMA)

- The Saudi insurance sector recorded gross written premiums of about USD 14.1 billion in 2022.

- The insurance sector grew by 26.9% in 2022.

- Insurance penetration in non-oil GDP reached 2.09% in 2022, up from 1.91% in 2021.

- The insurance loss ratio stood at 83.4% in 2022.

- Net profit of Saudi insurers reached about USD 183.4 million in 2022.

- The Saudization rate in the insurance sector reached 79% in 2022, up from 77% in 2021.

- The Saudi insurance industry generated over USD 14 billion in premiums.

Fintech Saudi (National Fintech Initiative)

- 6.4 million customers used insurtech services in 2024, growing 73% year-over-year.

- 8 million insurance policies were issued through insurtech platforms in 2024.

- The value of policies issued through insurtech platforms reached about USD 1.97 billion in 2024.

- Insurance aggregators issued 6.2 million policies in 2023.

- The value of policies issued by aggregators reached about USD 1.78 billion in 2023.

- 86% of aggregator policies were new policies in 2023.

- 14% of aggregator policies were renewals.

- Insurance aggregator platforms listed an average of 19.3 insurers in 2023.

- The conversion rate from inquiries to policy purchases was 6.1% in 2023.

- 15% of customers purchased multiple policies through aggregators.

Fintech Galaxy (Industry Fintech Ecosystem Tracking)

- Insurance aggregators issued 4.3 million policies in 2022.

- The value of policies issued through aggregators reached about USD 1.12 billion in 2022.

- 7.2 million customers were registered on insurance aggregator platforms in 2022.

- Aggregator users increased 33% compared with 2021.

- The number of policies issued by aggregators grew by 7.5% between 2021 and 2022.

- The value of aggregator-issued policies increased 40% year-over-year.

Vision 2030 / Saudi Digital Economy Programs

- Saudi Arabia aims for 70% of consumer payments to be non-cash by 2025.

- The government has invested over USD 1.5 billion in digital transformation initiatives supporting fintech and insurtech.

- Around 65% of Saudi consumers are interested in personalized digital insurance products.

- Approximately 50% of consumers are aware of insurtech solutions in the Kingdom.

- More than 35% of insurtech startups cite regulatory compliance as a key market challenge.

The Kingdom of Saudi Arabia (KSA) Insurtech Market: Market Dynamics

Driving Factors in the Kingdom of Saudi Arabia (KSA) Insurtech Market

Vision 2030 Financial Sector Development Program

Saudi Arabia's Vision 2030 underlines diversification away from dependence on oil and makes the insurtech and financial technology industry one of the mainstays of the economy. Huge investments in digital infrastructure projects like NEOM and the Red Sea Global have been driving growth. In addition, it also comprises fintech-friendly policies like establishing regulatory sandboxes and reducing barriers to digital insurance, which also attract foreign and local investments. This helps strengthen the nation's standing as a leading insurtech hub in the Middle East.

Increasing Young, Tech-Savvy Population

Saudi Arabia is also developing digital engagement actively with its young population demanding mobile-first insurance solutions, increasing the volumes of digital policy purchases, which in turn are raising demand for more sophisticated insurtech solutions. The upgrading of digital payment gateways, expansion of mobile networks, and the development of better customer experience platforms are easing the way to smoother insurance adoption. All these growth drivers increase the digital connectivity of the Kingdom in financial services and ensure the prosperity of the insurtech sector in the globalized digital economy.

Restraints in the Kingdom of Saudi Arabia (KSA) Insurtech Market

High Regulatory Compliance Costs

Advanced insurtech technologies and infrastructure development require significant capital investment for regulatory compliance, although governments are very supportive. Smaller enterprises can hardly afford comprehensive compliance systems or data protection integrations. This may impede market growth and further widen the gap between large corporations and SMEs in access to advanced insurance solutions.

Data Privacy Concerns

The insurtech industry will have concerns about data privacy and security that may affect customer adoption of digital insurance. While data protection frameworks are included in Vision 2030, the pace of digital adoption outpaces the development of comprehensive privacy regulations. Normally, companies rely on international standards, significantly increasing operational complexity. Getting over this restraint will involve considerable investments in cybersecurity and data protection programs meant to build consumer trust.

Opportunities in the Kingdom of Saudi Arabia (KSA) Insurtech Market

Integration of Emerging Technologies

The adoption of technologies such as AI, robotics, and big data analytics presents an excellent opportunity for insurtech optimization. Automated underwriting and predictive analytics cut down operational costs, while AI-powered systems enhance customer engagement capabilities. Startups and established firms alike are testing such integrations, which offers an excellent opportunity for technology providers and investors to reach the Saudi insurtech market.

Expansion of Parametric Insurance

With growing demand for the rapid payout of weather-related events and business interruptions, this parametric insurance is developing at a very fast pace. There is also more inflow of investments into IoT-enabled risk monitoring and automated claims settlement facilities. Additionally, infrastructure development in Saudi Arabia and changing climate patterns will further contribute to this segment and open doors for value-added service providers through innovative solution design.

Trends in the Kingdom of Saudi Arabia (KSA) Insurtech Market

Digital Transformation of Insurance

The insurtech sector in Saudi Arabia is also becoming a hub of digital transformation due to the initiatives laid down by Vision 2030 for integrating technology across all financial services. Companies are leveraging technologies such as IoT, AI, and blockchain for real-time underwriting, predictive analytics, and extended customer visibility. For example, IoT-enabled sensors provide timely insights into risk profiles, hence reducing any inefficiencies. Blockchain enhances data accuracy in complex insurance processes, building trust among stakeholders. This trend significantly improves operational efficiencies, besides being in tune with global smart insurance practices, and cements the Kingdom's status as a regional fintech hub.

Open Insurance and API Integration

This rapid growth has produced high demand in Saudi Arabia for the sector to implement open insurance and API-enabled solutions. Insurance providers such as Tawuniya and MedGulf have partnered with leading fintech platforms to try to meet today's demanding expectations around seamless coverage. The number of API-enabled distribution channels has been on the rise; there is an increasing level of product innovation, including the implementation of embedded insurance. As digital engagement is increasingly integral to consumer behavior, this trend is producing real investment in the hard infrastructure of insurance technology but also increasingly in digital platforms that then tie the operation together in one seamless interface for providers and customers alike.

The Kingdom of Saudi Arabia (KSA) Insurtech Market: Research Scope and Analysis

By Type Analysis

Health insurance is projected to dominate the type segment in this market as it will hold 35.0% of market share in 2026. The dominance of health insurance in the type segment of the KSA Insurtech Market is owing to mandatory health insurance requirements and healthcare infrastructure growth in the country. Businesses in KSA are hugely investing in employee health benefits and digital health platforms; hence, advanced insurtech solutions are being used to smoothen health insurance operations, ranging from digital policy issuance and telemedicine integration to automated claims processing systems. Saudi Arabia's Vision 2030 underlines the emphasis on integrating technology for the smooth operation of healthcare financing. It therefore raises demand for IoT-enabled health monitoring devices, AI-powered underwriting systems, and digital claims platforms that help in tracking health outcomes with real-time visibility and building customer trust-critical to maintaining operational efficiency in this highly competitive market. Such huge healthcare projects spur demand for high-class digital health insurance solutions, including wellness programs and chronic disease management platforms.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

It will help in the complete interconnectivity of physical and digital components within a health insurance ecosystem, thus making its future in the market indispensable. AI, IoT, and the cloud completely depend on this basic digital infrastructure for gathering and synchronizing data within their systems. Growth in the digital health industry also adds to the contribution of advanced analytics platforms that optimize the processes of risk assessment. Government-backed healthcare initiatives advocate the use of the latest available technology to reduce operational bottlenecks, thus supporting the market of health insurance. Hence, health insurance remains an integral factor as it provides the actual coverage backbone for modern insurtech development in KSA.

By Technology Analysis

Cloud computing is anticipated to dominate the major share in the technology segment of the insurtech market in KSA, owing to the strategic reliance on scalable digital infrastructure for insurance operations. Saudi Arabia has vast digital transformation initiatives with cloud infrastructure connecting important economic regions for easier deployment of insurance platforms to regions such as Riyadh, Jeddah, and Dammam. Cloud computing offers flexibility and scalability no other technology can provide. Policy administration and claims processing, being very essential, do happen across all insurance types and also in banking and healthcare industries. There is an unparalleled growth in the number of digital insurance activities as, with a growing demand for seamless customer experiences, multiple times the same consumer would want to expect instant policy issuance.

The cloud infrastructure investments involve the expansion of data centers, adding regional cloud hubs, and furthering digital efficiency. This development also aligns with Vision 2030 in positioning Saudi Arabia as a global digital hub. The proximity of fintech clusters to cloud infrastructure further cements their position as the main technology for digital insurance distribution. Among many factors, cost-effectiveness comes forward. Compared with either on-premise or hybrid systems, it has cloud computing at lesser costs for scalability, thus making it perfectly fit for insurtech growth. The increased use of technologies for cloud security, like encryption and access management, improves the operational efficiency-cum-situation more in enhancing cloud dominance.

By Service Analysis

The managed services segment in the KSA Insurtech Market is projected to be dominated by service solutions, having become scalable, cost-effective, and fully capable of integrating smoothly with insurance operations. Due to the increased adoption of digital transformation strategies by businesses in Saudi Arabia, managed services offer flexible operational support for complex insurtech operations. This is also aligned with the aim of Vision 2030 toward modernizing industries and embracing technological innovation. Managed services make the operations available with real-time monitoring to make better decisions and collaborate with the different players along the insurance value chain. This becomes even more important in a geographically spread-out country like Saudi Arabia, where insurance coordination needs to be seamlessly performed. Moreover, managed services reduce direct costs associated with traditional in-house operations, such as staffing and training. The cost efficiency appeals to businesses of all sizes, especially small and medium enterprises-which are a growth segment in KSA's economy.

Not to say that the capability for advanced security and analytics of the managed service platforms stands in their favor, too. Predictive analytics, artificial intelligence, and machine learning capabilities integrated with these service platforms further enable businesses in insurance operations relevant to anticipating customer needs and mitigating risks. This dream is partly driven by initiatives from the KSA government aimed at improving digital infrastructure and partnering with major global technology providers. This will enable them to support dynamic market demands and ensure operational agility, hence remaining the dominant service method within the insurtech market.

By End User Analysis

The healthcare end-user segment is anticipated to dominate the KSA insurtech market due to several reasons such as mandatory health insurance requirements, extensive patient data, and advanced technology adoption. Healthcare providers are at the forefront of insurtech integration, driven by their operational need to invest in state-of-the-art digital infrastructure and insurance solutions. Saudi Arabia's Vision 2030 places a strong emphasis on the development of the healthcare and insurance sector factor that large healthcare groups in industries such as hospital management and pharmaceutical distribution are eyeing with great interest. These organizations could be operating very extensive patient care operations for which they need advanced software to track health outcomes in real-time, enable intelligent claims management, and improve risk assessment. Healthcare providers also boast scale for the adoption of innovative technologies like AI, IoT, and blockchain, paving ways to enhance efficiency and complete transparency in insurance operations. The reason healthcare organizations can negotiate better with insurance providers and deploy integrated insurtech solutions is because of their overall scale.

Healthcare providers have benefited from such initiatives funded by the government, examples of which are the programs under the Health Sector Transformation Program to provide different types of funds and digital infrastructure to extend the insurance functionalities of their organizations. In summary, this dominant position has also been enabled by driving the wheel of KSA's healthcare economics. At the forefront in the implementation of state-of-the-art insurtech best practices, leading healthcare organizations continue to help set new thresholds in terms of efficiency and innovative applications across the medical industry, therefore continuing their topmost market performance.

The Kingdom of Saudi Arabia (KSA) Insurtech Market Report is segmented on the basis of the following:

By Type

- Health

- Auto

- Home

- Specialty

- Travel

- Business

- Others

By Technology

- Blockchain

- Cloud Computing

- IoT

- Machine Learning

- Robo Advisory

- Others

By Service

- Consulting

- Support & Maintenance

- Managed Services

By End User

- BFSI

- Automotive

- Manufacturing

- Transportation

- Government

- Health

- Retail

- Others

Impact of Artificial Intelligence in the Kingdom of Saudi Arabia (KSA) Insurtech Market

- Enhanced Customer Experience: AI-powered virtual assistants and hyper-personalized portals provide instantaneous, round-the-clock service and tailored product recommendations, fundamentally elevating engagement and satisfaction levels for Saudi policyholders seeking modern digital convenience.

- Streamlined Operational Efficiency: Artificial intelligence automates core processes like underwriting, real-time claims adjudication, and sophisticated fraud detection, dramatically reducing overhead costs and processing delays for major Saudi insurers including Al Rajhi Takaful.

- Precision Risk Assessment: By harnessing big data and telematics, AI algorithms facilitate profoundly accurate underwriting and the development of dynamic, usage-based policies, enabling superior risk management and pricing precision across the local market.

- Proactive Fraud Mitigation: Sophisticated machine learning models continuously scrutinize claims data to instantly identify and prevent fraudulent patterns, thereby safeguarding profitability for providers and preserving the integrity of the Kingdom's financial ecosystem.

- Vision 2030 Strategic Alignment: The widespread integration of AI directly propels the nation's ambitious digital transformation agenda, fostering a cutting-edge Insurtech environment that benefits from supportive regulatory frameworks established by the Saudi Central Bank.

The Kingdom of Saudi Arabia (KSA) Insurtech Market: Competitive Landscape

The competitive landscape is fueled by participation, both domestic and international, in the Kingdom of Saudi Arabia Insurtech Market, with dissimilar capabilities across insurance, technologies, and digital infrastructure. Major companies, therefore, strategize to develop advanced technologies such as AI, IoT, and blockchain to enhance insurtech operations to better competitiveness. The leading players are Tawuniya, MedGulf, and Bupa Arabia in insurance services, while in cloud-based insurtech solutions, the leading players include SAP, Microsoft, and Oracle. These companies leverage Saudi Arabia's Vision 2030 initiatives by aligning their offerings with government priorities meant to attract investments and improve efficiency. It addresses both rising healthcare and automotive sectors where these focus more on niche capabilities: usage-based insurance and parametric insurance solutions, while Third-party insurtech providers have emerged, providing end-to-end solutions in policy administration and claims management.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Mergers and partnerships are common strategies that allow companies to expand service portfolios and reach. For instance, technology companies partnering with insurance providers enhance data-driven decision-making and operational agility. While the leading companies are competitive, innovation in the fields of automation, digital distribution, and predictive analytics separates the leaders. These opportunities are likely to come along with an intense competitive landscape for both established players and new entrants, with strong governmental support for developing fintech zones.

Some of the prominent players in The Kingdom of Saudi Arabia (KSA) Insurtech Market are:

- Rasan

- Tawuniya

- Malath

- Al Rajhi Takaful

- Bupa Arabia

- Saudi Takaala / SALAMA

- Najm

- Aqeed

- Bayzat

- YallaCompare

- AXA Saudi Arabia

- Allianz Saudi Fransi

- MedGulf Insurance

- Zavi Technologies

- Takaful Emirates

- Daman Insurance

- Yasmina

- Shory Group

- Hala

- Mozn

- Other Key Players

Recent Developments in the Kingdom of Saudi Arabia (KSA) Insurtech Market

- October 2025: Tawuniya introduced an AI-powered claims processing platform designed to enhance customer experience efficiency. The platform uses machine learning algorithms to reduce claims settlement times, optimize document verification, and minimize manual intervention, addressing challenges in urban and rural insurance operations.

- September 2025: Bupa Arabia entered a strategic partnership with a prominent Saudi health tech company to integrate IoT technologies into its regional health insurance operations. The collaboration focuses on automating health monitoring, reducing fraud, and enabling real-time data sharing across insurance networks.

- August 2025: The Saudi Arabian government inaugurated the Riyadh Fintech Hub, a state-of-the-art facility designed to improve insurtech connectivity across critical industries such as healthcare, automotive, and retail.

- November 2024: Oracle launched a blockchain-based solution to enhance transparency and security in insurance management for Saudi enterprises. The solution facilitates seamless collaboration across stakeholders, ensuring the authenticity of policies, reducing fraud, and enhancing regulatory compliance.

- July 2024: SAP unveiled cloud-based predictive analytics innovations aimed at improving decision-making in insurtech operations. These solutions leverage big data to forecast claims patterns, optimize underwriting, and streamline policy administration processes, empowering businesses to adapt to market dynamics.

- April 2024: MedGulf, a leader in health insurance, expanded its digital distribution channels, increasing capacity for direct-to-consumer policy sales. This move supports the growing insurtech demand and strengthens Saudi Arabia's position in global digital insurance.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 767.8 Mn |

| Forecast Value (2035) |

USD 5,666.7 Mn |

| CAGR (2026–2035) |

24.9% |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors and etc. |

| Country Coverage |

The Kingdom of Saudi Arabia (KSA) |

| Segments Covered |

By Type (Health, Auto, Home, Specialty, Travel, Business, and Others), By Technology (Blockchain, Cloud Computing, IoT, Machine Learning, Robo Advisory, and Others), By Service (Consulting, Support & Maintenance, and Managed Services), By End User (BFSI, Automotive, Manufacturing, Transportation, Government, Health, Retail, and Others) |

| Prominent Players |

Rasan, Tawuniya, Malath, Al Rajhi Takaful, Bupa Arabia, Saudi Takaful / SALAMA, Najm, Aqeed, Bayzat, YallaCompare, AXA Saudi Arabia, Allianz Saudi Fransi, MedGulf Insurance, Zavi Technologies, Takaful Emirates, Daman Insurance, Yasmina, Shory Group, Hala, Mozn, and Other Key Players |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users) and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days and 5 analysts working days respectively. |

Frequently Asked Questions

How big is the Kingdom of Saudi Arabia's Insurtech Market?

▾ The Kingdom of Saudi Arabia Insurtech Market size is estimated to have a value of USD 767.8 million in 2026 and is expected to reach USD 5,666.7 million by the end of 2035.

Who are the key players in the Kingdom of Saudi Arabia Insurtech Market?

▾ Some of the major key players in the Kingdom of Saudi Arabia Insurtech Market are Saudi Insurance Services, Tawuniya, MedGulf, Bupa Arabia, Walaa Cooperative Insurance, Alinma Tokio Marine Company, and many others.

What is the growth rate in the Kingdom of Saudi Arabia Insurtech Market?

▾ The market is growing at a CAGR of 24.9 percent over the forecasted period.