Market Overview

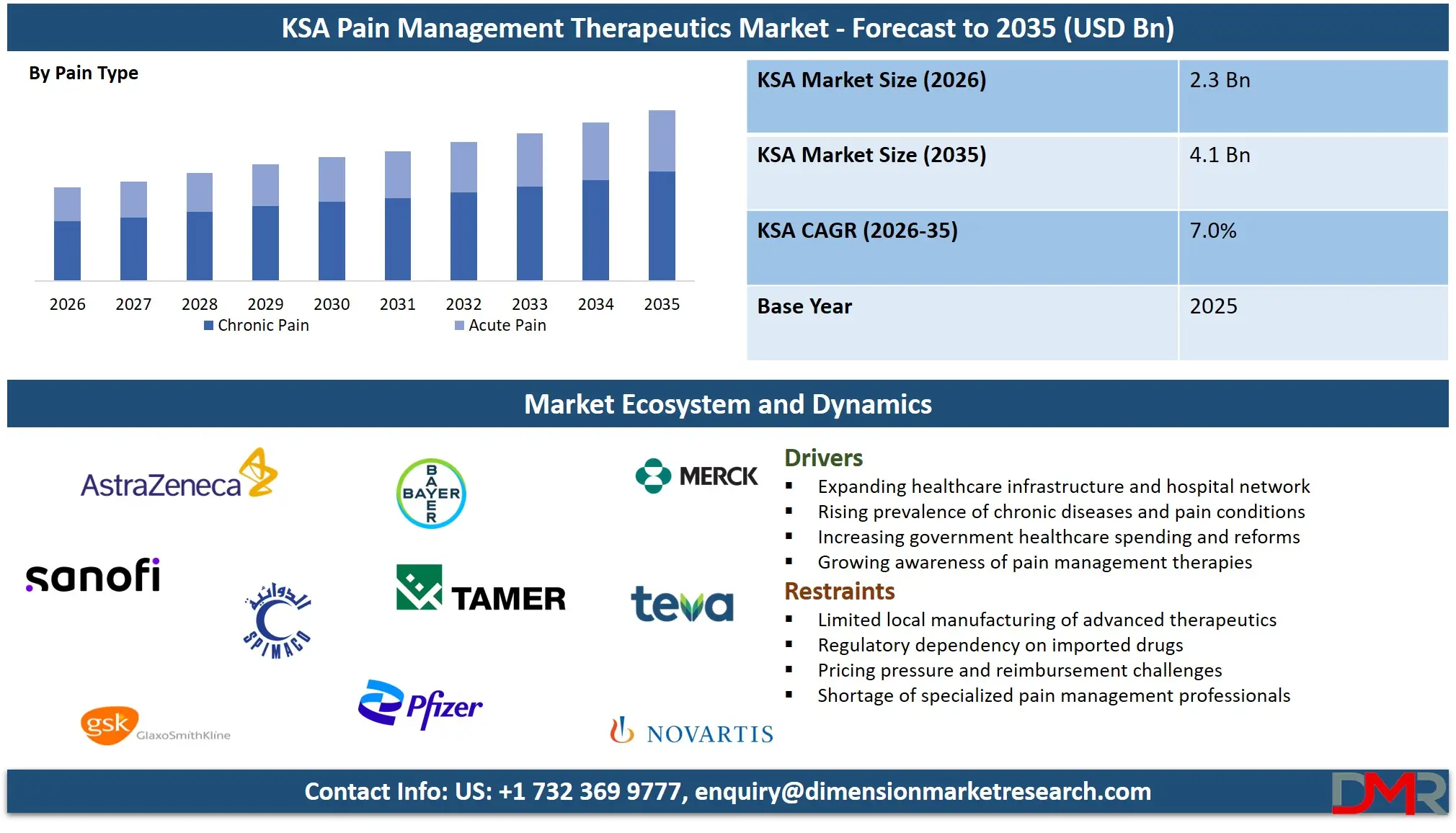

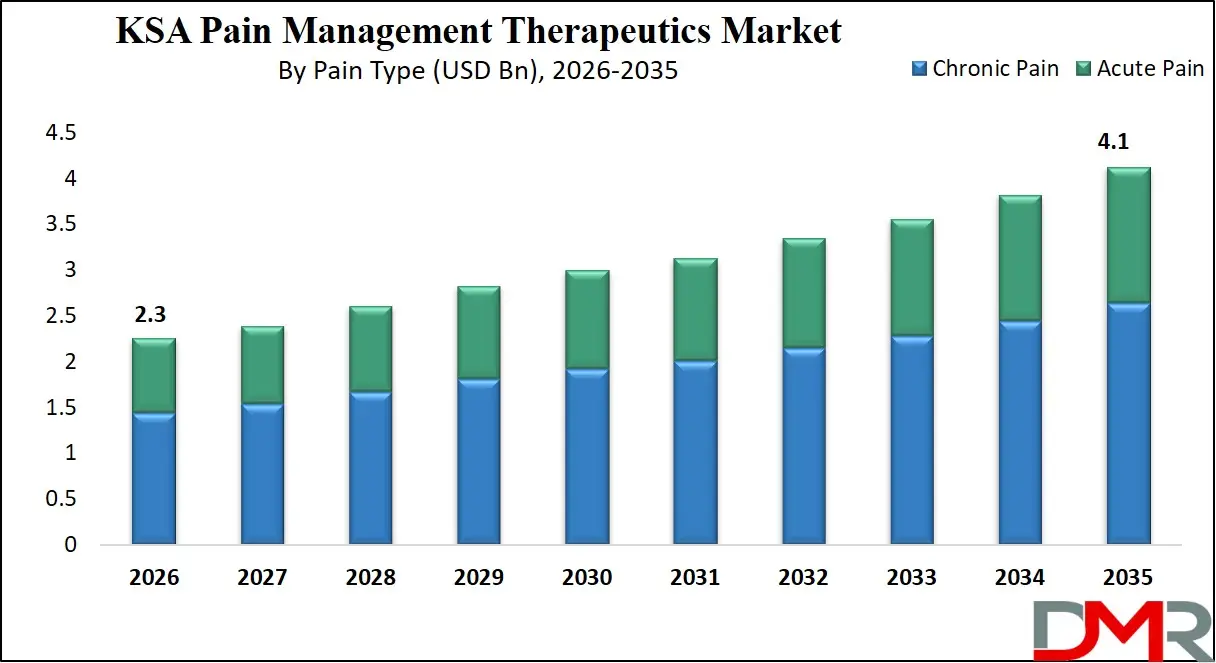

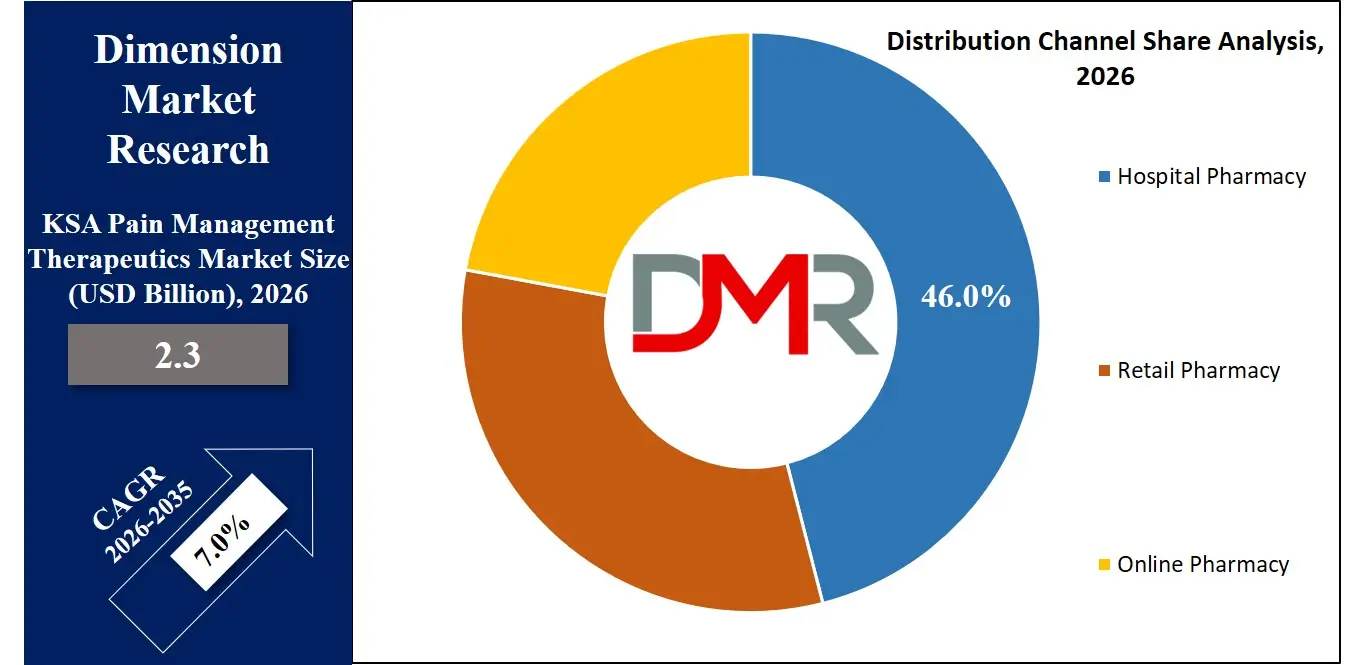

The KSA Pain Management Therapeutics Market size is projected to reach USD 2.3 billion in 2026 and grow at a compound annual growth rate of 7.0% to reach a value of USD 4.1 billion in 2035.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Pain Management Therapeutics refers to the range of pharmaceutical products, treatment approaches, and healthcare services used to alleviate acute and chronic pain conditions within Saudi Arabia. This includes drug classes such as non-steroidal anti-inflammatory drugs (NSAIDs), opioids, anesthetics, anticonvulsants, antidepressants, and anti-migraine medications, alongside various routes of administration like oral and parenteral delivery. These therapeutics are integral to improving patient quality of life, particularly for individuals suffering from conditions such as arthritis, cancer pain, neuropathic disorders, and post-operative discomfort.

The sector plays a vital role in the broader healthcare system, driven by increasing prevalence of chronic diseases, rising geriatric population, and expanding healthcare infrastructure under national transformation initiatives. The market is also influenced by advancements in drug formulations, targeted therapies, and growing awareness regarding pain management solutions. Integration of digital health tools and personalized medicine approaches is gradually reshaping treatment protocols.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Recent progression reflects an evolving regulatory landscape, improved access to healthcare services, and rising investments in pharmaceutical innovation. Increased adoption of non-opioid alternatives, coupled with stricter opioid regulations, is shifting treatment patterns. The growing focus on patient-centric care and multidisciplinary pain management approaches continues to define the trajectory of this market.

KSA Pain Management Therapeutics Market: Key Takeaways

- Market Growth: The KSA Pain Management Therapeutics Market size is expected to grow by USD 1.7 billion, at a CAGR of 7.0%, during the forecasted period of 2027 to 2035.

- By Pain Type: The chronic pain segment is anticipated to get the majority share of the KSA Pain Management Therapeutics market in 2026.

- By Distribution Channel: The hospital pharmacy segment is expected to get the largest revenue share in 2026 in the KSA Pain Management Therapeutics market.

- Use Cases: Some of the use cases of pain management therapeutics include palliative care, cancer pain relief, and more.

KSA Pain Management Therapeutics Market: Use Cases

- Post-Surgical Recovery: Pain therapeutics are widely used after surgeries to ensure faster recovery and reduce complications. Hospitals rely on multimodal analgesia approaches combining opioids, NSAIDs, and anesthetics for effective outcomes.

- Chronic Disease Management: Patients with arthritis, cancer, and back pain require long-term medication plans. Therapeutics help maintain mobility and improve daily functioning.

- Neuropathic Pain Treatment: Specialized drugs like anticonvulsants and antidepressants are used to manage nerve-related pain conditions, enhancing patient comfort and neurological stability.

- Emergency Care Applications: Acute pain from injuries or trauma is managed using fast-acting analgesics in emergency departments. Rapid pain relief is critical in stabilizing patients.

- Cancer Pain Relief: Oncology patients rely on strong analgesics, including opioids and adjuvant therapies, to manage severe and persistent pain throughout treatment cycles.

- Migraine and Headache Management: Anti-migraine drugs such as triptans and CGRP inhibitors are increasingly used to control severe headaches and improve productivity.

- Palliative Care: Pain therapeutics play a crucial role in end-of-life care, ensuring comfort and dignity for patients with terminal illnesses.

Stats & Facts

- Saudi Ministry of Health reported that over 60% of elderly patients in 2024 experienced chronic pain conditions requiring medical intervention.

- General Authority for Statistics (Saudi Arabia) indicated that the population aged above 60 years reached 7.4% in 2025, driving demand for pain therapeutics.

- World Health Organization stated in 2024 that musculoskeletal disorders affect nearly 30% of adults in the Middle East region.

- Saudi Food and Drug Authority reported a 12% increase in approvals for analgesic drugs in 2025.

- International Diabetes Federation estimated in 2024 that 17.7% of Saudi adults have diabetes, often linked with neuropathic pain.

- World Bank data (2025) showed Saudi healthcare expenditure accounted for approximately 6.6% of GDP.

- Saudi Ministry of Health recorded a 15% rise in surgical procedures in 2024, increasing demand for post-operative pain management.

- WHO reported in 2025 that cancer incidence in Saudi Arabia is growing at 3% annually, boosting need for pain therapeutics.

- OECD Health Statistics 2024 highlighted increasing adoption of non-opioid pain therapies globally, including Saudi Arabia.

- Saudi Vision 2030 healthcare initiatives increased private healthcare participation by over 25% in 2025.

- Gulf Health Council reported in 2024 that migraine prevalence in Saudi Arabia exceeds 25% among adults.

- Saudi FDA noted a 10% rise in demand for generic pain medications in 2025.

Market Dynamic

Driving Factors in the KSA Pain Management Therapeutics Market

Rising Burden of Chronic Diseases

The increasing prevalence of chronic conditions such as arthritis, diabetes, and cancer significantly drives the demand for pain management therapeutics in Saudi Arabia. Chronic diseases often result in persistent pain, requiring long-term pharmacological intervention. As the population ages and lifestyle-related illnesses rise, the need for effective pain control solutions becomes more critical. Healthcare providers are focusing on integrated treatment approaches combining multiple drug classes to improve outcomes. Additionally, growing awareness among patients regarding pain management options encourages early diagnosis and treatment, further supporting market expansion and sustained demand for advanced therapeutics.

Healthcare Infrastructure Expansion and Policy Support

Saudi Arabia’s ongoing healthcare transformation under Vision 2030 is a major growth catalyst. Increased government spending, expansion of hospitals, and rising private sector involvement have improved access to advanced pain management therapies. Regulatory support for faster drug approvals and investments in pharmaceutical manufacturing also contribute to market growth. Enhanced healthcare accessibility ensures that more patients receive timely pain management treatments. Moreover, digital health integration and telemedicine platforms are enabling better patient monitoring and follow-up care, strengthening the overall adoption of pain therapeutics across urban and semi-urban regions.

Restraints in the KSA Pain Management Therapeutics Market

Stringent Regulations on Opioid Usage

Strict regulatory controls on opioid prescriptions present a significant challenge for the market. While opioids are highly effective for severe pain, concerns over addiction and misuse have led to tighter monitoring and restricted access. Physicians are often cautious in prescribing these drugs, which may limit treatment options for patients with intense pain conditions such as cancer. Compliance with regulatory frameworks also increases administrative burdens for healthcare providers and pharmaceutical companies. As a result, reliance on alternative therapies grows, but these may not always provide equivalent efficacy, potentially affecting patient outcomes.

Limited Awareness and Treatment Gaps

Despite advancements, awareness regarding comprehensive pain management remains limited among certain patient populations. Many individuals delay seeking treatment or rely on over-the-counter medications without proper medical guidance. This leads to underdiagnosis and undertreatment of chronic pain conditions. Additionally, disparities in healthcare access between urban and rural areas contribute to inconsistent treatment adoption. Lack of specialized pain management centers and trained professionals further exacerbates the issue. These gaps hinder the full potential of the market by restricting timely intervention and reducing overall therapeutic effectiveness.

Opportunities in the KSA Pain Management Therapeutics Market

Shift Toward Non-Opioid and Innovative Therapies

The growing preference for non-opioid pain management solutions presents a significant opportunity. Pharmaceutical companies are investing in the development of safer alternatives such as biologics, CGRP inhibitors, and targeted therapies. These innovations address safety concerns while maintaining efficacy, making them attractive options for both patients and healthcare providers. Increased research and development activities, coupled with supportive regulatory policies, are accelerating the introduction of novel treatments. This shift not only diversifies the therapeutic landscape but also enhances long-term sustainability by reducing dependency on controlled substances.

Expansion of Private Healthcare and Medical Tourism

The rapid growth of private healthcare facilities and rising medical tourism in Saudi Arabia create new avenues for market expansion. International collaborations and investments are improving the quality of care and introducing advanced pain management solutions. Patients traveling for specialized treatments contribute to increased demand for high-quality therapeutics. Furthermore, private hospitals often adopt cutting-edge technologies and personalized treatment approaches, driving innovation in pain management practices. This expansion strengthens the market ecosystem and encourages continuous improvement in therapeutic offerings.

Trends in the KSA Pain Management Therapeutics Market

Adoption of Multimodal Pain Management Approaches

Healthcare providers are increasingly adopting multimodal strategies that combine different drug classes and treatment techniques to achieve better pain control. This approach reduces reliance on single-drug therapies, particularly opioids, and minimizes side effects. Integration of pharmacological and non-pharmacological treatments, such as physiotherapy and behavioral therapy, enhances patient outcomes. The trend reflects a shift toward holistic care, where individualized treatment plans are designed based on patient needs and conditions, improving overall satisfaction and recovery rates.

Growing Role of Digital Health and Telemedicine

Digital health technologies are transforming pain management practices in Saudi Arabia. Telemedicine platforms enable remote consultations, allowing patients to access specialists without geographical barriers. Wearable devices and mobile health applications are being used to monitor pain levels and treatment responses in real time. These innovations improve patient engagement and adherence to treatment plans. Additionally, data-driven insights help healthcare providers optimize therapies and predict patient needs, contributing to more efficient and personalized pain management solutions.

Impact of Artificial Intelligence in KSA Pain Management Therapeutics Market

- Predictive Pain Assessment: AI algorithms analyze patient data to predict pain patterns, enabling proactive treatment planning and improved outcomes.

- Personalized Treatment Plans: AI helps tailor drug combinations based on individual patient profiles, enhancing effectiveness and reducing side effects.

- Drug Discovery Acceleration: Machine learning accelerates identification of new analgesic compounds, reducing development timelines.

- Clinical Decision Support: AI-powered systems assist physicians in selecting optimal therapies based on real-time data and clinical guidelines.

- Remote Patient Monitoring: AI integrates with wearable devices to track patient pain levels continuously, improving adherence and response tracking.

- Optimization of Dosage: AI models determine optimal dosing schedules, minimizing risks associated with overuse or underuse of medications.

- Early Detection of Adverse Effects: AI systems identify potential side effects early, enabling timely intervention and safer treatment.

- Operational Efficiency: Automation of administrative processes reduces workload for healthcare providers and improves service delivery.

Research Scope and Analysis

By Pain Type Analysis

Chronic pain dominates the KSA pain management therapeutics market and is projected to hold approximately 64% market share in 2026. This dominance is driven by the high prevalence of long-term conditions such as arthritis, diabetes-related neuropathy, and cancer. Chronic pain requires continuous management, leading to sustained demand for multiple drug classes, including antidepressants and anticonvulsants. The aging population further strengthens this segment’s growth, as older individuals are more susceptible to chronic illnesses. Increased awareness, improved diagnosis rates, and the adoption of comprehensive treatment approaches continue to support consistent expansion of this segment.

Acute pain represents the fastest-growing segment due to the rising number of surgeries, injuries, and emergency medical cases across Saudi Arabia. Demand for fast-acting analgesics and anesthetics is increasing significantly, particularly in hospitals and trauma centers where immediate pain relief is essential. Advancements in surgical procedures and improved healthcare infrastructure are contributing to this segment’s rapid expansion. Additionally, the growing preference for short-term pain management solutions with fewer side effects is influencing treatment choices, while increasing healthcare accessibility ensures timely intervention and supports the continued growth of acute pain therapeutics.

By Drug Class Analysis

NSAIDs lead the market with an estimated 32% share in 2026, primarily due to their widespread use in treating mild to moderate pain conditions such as musculoskeletal disorders and post-operative discomfort. Their affordability, easy availability, and proven effectiveness make them a preferred first-line treatment option among healthcare providers. Increasing incidence of chronic conditions and injuries further drives demand for NSAIDs. Additionally, the availability of generic versions and continuous product innovations enhance accessibility, ensuring sustained market dominance while supporting cost-effective pain management strategies across diverse patient populations.

CGRP inhibitors are the fastest-growing segment, driven by increasing migraine prevalence and rising demand for targeted and advanced therapies. These drugs provide improved efficacy with fewer side effects compared to traditional treatment options, making them highly attractive for patients with chronic migraines. Growing awareness among healthcare professionals and patients regarding innovative therapies is accelerating their adoption. Furthermore, ongoing research and development activities are expanding their application scope, while improved access to specialized care in Saudi Arabia supports the rapid growth and future potential of this segment.

By Route of Administration Analysis

The oral segment holds around 58% market share in 2026 due to its convenience, ease of administration, and high patient compliance. Tablets and capsules are widely prescribed for both chronic and acute pain conditions, making them the most preferred route among patients and healthcare providers. Cost-effectiveness and widespread availability further strengthen this segment’s position in the market. Additionally, advancements in oral drug formulations, including extended-release and combination therapies, enhance treatment effectiveness and patient adherence, contributing to the continued dominance of oral administration in pain management practices.

Parenteral administration is witnessing rapid growth, particularly in hospital settings where immediate pain relief is required for severe conditions. Injectable formulations are commonly used during surgeries, emergency treatments, and critical care situations, ensuring faster onset of action compared to oral medications. Increasing number of surgical procedures and trauma cases in Saudi Arabia is driving demand for parenteral therapeutics. Additionally, advancements in injectable drug technologies and improved healthcare infrastructure are supporting this segment’s expansion, making it an essential component of modern pain management strategies.

By Indication Analysis

Arthritic pain dominates with a projected 27% share in 2026, driven by the rising prevalence of osteoarthritis and rheumatoid arthritis in Saudi Arabia. The increasing geriatric population and sedentary lifestyles contribute significantly to higher incidence rates of joint-related disorders. Continuous use of NSAIDs, biologics, and supportive therapies plays a key role in managing symptoms and improving patient mobility. Additionally, growing awareness about early diagnosis and treatment options encourages more patients to seek medical care, supporting sustained growth and reinforcing the dominance of this segment.

Cancer pain is the fastest-growing segment due to increasing cancer incidence and improved access to oncology treatments in Saudi Arabia. Patients undergoing cancer therapies often experience severe and persistent pain, requiring strong analgesics and combination treatment approaches. Advances in oncology care and supportive pain management therapies are driving demand for specialized medications. Additionally, rising awareness about palliative care and improved healthcare infrastructure are enhancing treatment accessibility, ensuring better quality of life for patients and contributing to the rapid expansion of this segment.

By Distribution Channel Analysis

Hospital pharmacies account for approximately 46% market share in 2026, supported by high patient inflow and availability of specialized medications for pain management. These pharmacies play a critical role in dispensing prescription drugs, particularly for severe, chronic, and post-operative pain conditions. The presence of skilled healthcare professionals ensures proper drug administration and monitoring. Additionally, increasing hospital admissions and surgical procedures contribute to higher demand for hospital pharmacy services, reinforcing their dominant position in the market.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Online pharmacies are expanding rapidly due to increasing digitalization and changing consumer preferences for convenience and accessibility. Patients are mainly opting for online platforms to purchase medications, driven by ease of ordering and home delivery services. Growth in e-commerce, along with the rise of telemedicine, is significantly supporting this segment’s expansion. Additionally, improved internet penetration and digital healthcare initiatives in Saudi Arabia are enhancing accessibility, making online pharmacies an increasingly important distribution channel in the pain management therapeutics market.

The KSA Pain Management Therapeutics Market Report is segmented on the basis of the following:

By Pain Type

By Drug Class

- Non-steroidal Anti-inflammatory Drugs (NSAIDs)

- Opioids

- Oxycodone

- Hydrocodones

- Tramadol

- Morphine

- Fentanyl

- Others

- Anesthetics

- Anti-Migraine Drugs

- Triptans

- Ergot Alkaloids

- CGRP Inhibitors

- Antidepressants

- Anticonvulsants

- Other Drug Class

By Route of Administration

By Indication

- Arthritic Pain

- Neuropathic Pain

- Chronic Back Pain

- Post-Operative Pain

- Cancer Pain

- Fibromyalgia

- Other Indication

By Distribution Channel

- Online Pharmacy

- Retail Pharmacy

- Hospital Pharmacy

Competitive Landscape

The KSA pain management therapeutics market is characterized by intense competition driven by innovation, regulatory compliance, and evolving patient needs. Market participants focus on research and development to introduce safer and more effective drugs, particularly non-opioid alternatives. Strategic collaborations with healthcare providers and distributors enhance market reach and accessibility.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

High entry barriers, including stringent regulatory approvals and significant investment requirements, limit new entrants. Companies also invest in localized manufacturing and supply chain optimization to reduce costs and improve efficiency. Continuous product differentiation, patient-centric approaches, and adoption of digital health technologies are key strategies to maintain competitive advantage.

Some of the prominent players in the KSA Pain Management Therapeutics are:

- Pfizer

- Novartis

- GlaxoSmithKline

- Sanofi

- Bayer

- AstraZeneca

- Johnson & Johnson

- Merck & Co.

- Teva Pharmaceutical Industries

- Boehringer Ingelheim

- Abbott Laboratories

- Hikma Pharmaceuticals

- Julphar

- SPIMACO

- Jamjoom Pharma

- Tabuk Pharmaceuticals

- Al-Andalus Pharmaceuticals

- Avalon Pharma

- Saudi Pharmaceutical Industries & Medical Appliances Corp

- Tamer Group

- Other Key Players

Recent Developments

- In March 2025, Novartis announced a significant investment to expand its pain management portfolio in Saudi Arabia. The initiative included partnerships with local healthcare institutions and increased funding for research on targeted therapies, particularly for migraine and cancer pain. The company also focused on enhancing distribution networks and digital health integration. This move strengthens Novartis’ presence in the region and supports the broader shift toward advanced and personalized pain management solutions.

- In January 2025, Pfizer introduced an advanced non-opioid pain management drug in Saudi Arabia aimed at reducing dependency on traditional opioid treatments. The launch focused on patients suffering from chronic musculoskeletal and neuropathic pain. The drug demonstrated improved safety profiles and fewer side effects during clinical trials. Pfizer collaborated with regional healthcare providers to ensure rapid adoption and accessibility.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 2.3 Bn |

| Forecast Value (2035) |

USD 4.1 Bn |

| CAGR (2026–2035) |

7.0% |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors and etc. |

| Segments Covered |

By Pain Type (Chronic Pain, Acute Pain), By Drug Class (Non-steroidal Anti-inflammatory Drugs (NSAIDs), Opioids, Anesthetics, Anti-Migraine Drugs, Antidepressants, Anticonvulsants, Other Drug Class), By Route of Administration (Oral, Parenteral), By Indication (Arthritic Pain, Neuropathic Pain, Chronic Back Pain, Post-Operative Pain, Cancer Pain, Fibromyalgia, Other Indication), By Distribution Channel (Online Pharmacy, Retail Pharmacy, Hospital Pharmacy) |

| Country Coverage |

Saudi Arabia |

| Prominent Players |

Pfizer, Novartis, GlaxoSmithKline, Sanofi, Bayer, AstraZeneca, Johnson & Johnson, Merck & Co., Teva Pharmaceutical Industries, Boehringer Ingelheim, Abbott Laboratories, Hikma Pharmaceuticals, Julphar, SPIMACO, Jamjoom Pharma, Tabuk Pharmaceuticals, Al-Andalus Pharmaceuticals, Avalon Pharma, Saudi Pharmaceutical Industries & Medical Appliances Corp, Tamer Group, and Other Key Players |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users) and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days and 5 analysts working days respectively. |

Frequently Asked Questions

How big is the KSA Pain Management Therapeutics Market?

▾ The KSA Pain Management Therapeutics Market size is expected to reach USD 2.3 billion by 2026 and is projected to reach USD 4.1 billion by the end of 2035.

Who are the key players in the KSA Pain Management Therapeutics Market?

▾ Some of the major key players in the KSA Pain Management Therapeutics Market include Pfizer, Merck, Sanofi and others.

What is the growth rate in the KSA Pain Management Therapeutics Market?

▾ The market is growing at a CAGR of 7.0 percent over the forecasted period.