Market Overview

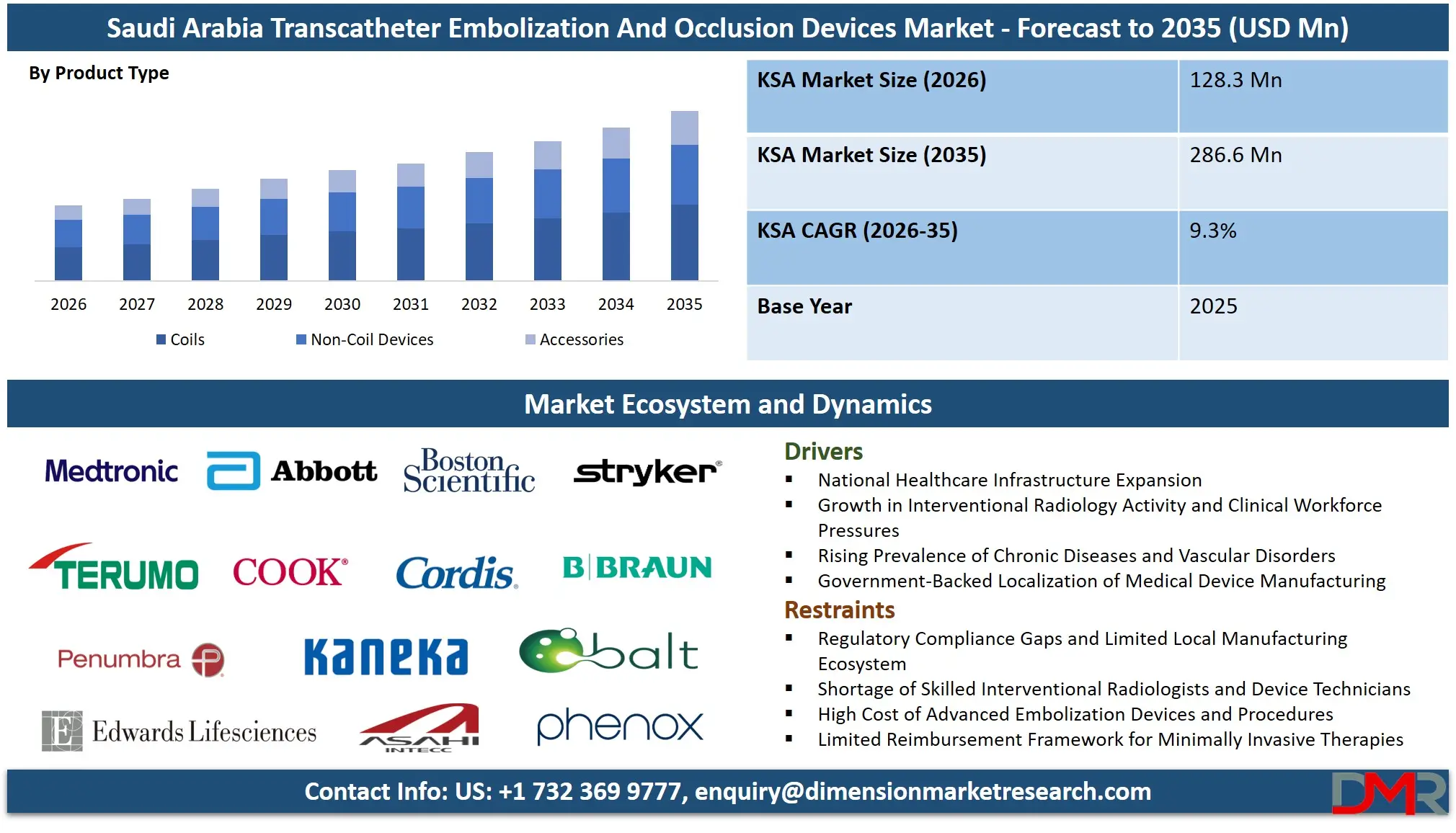

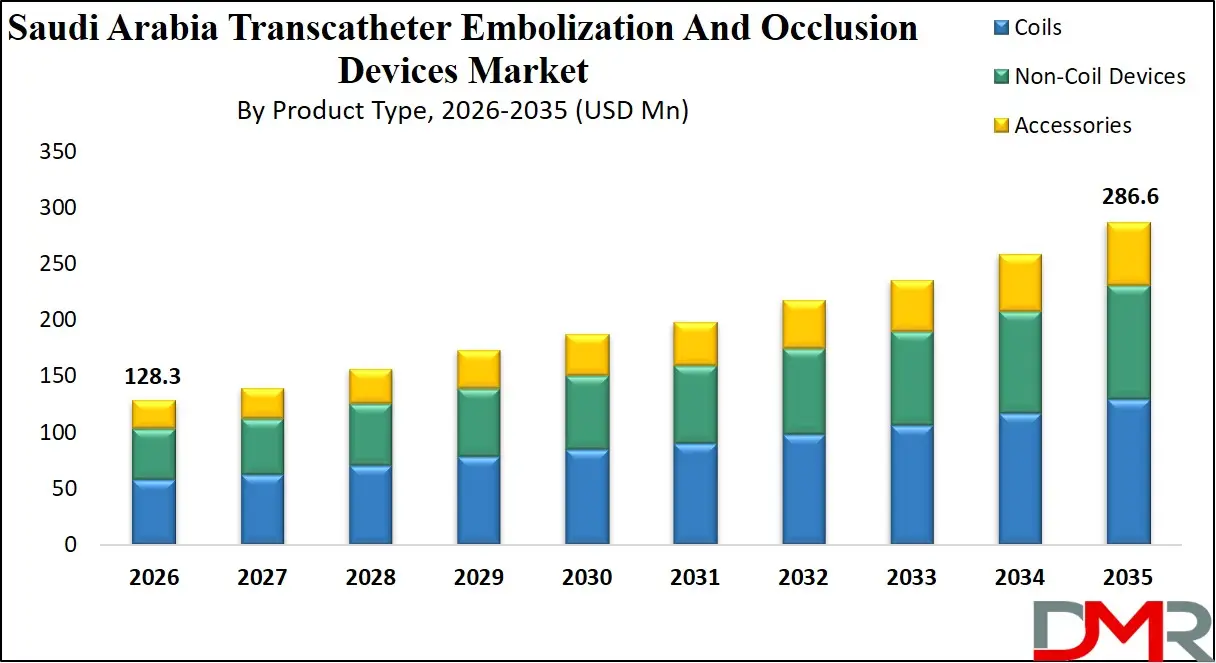

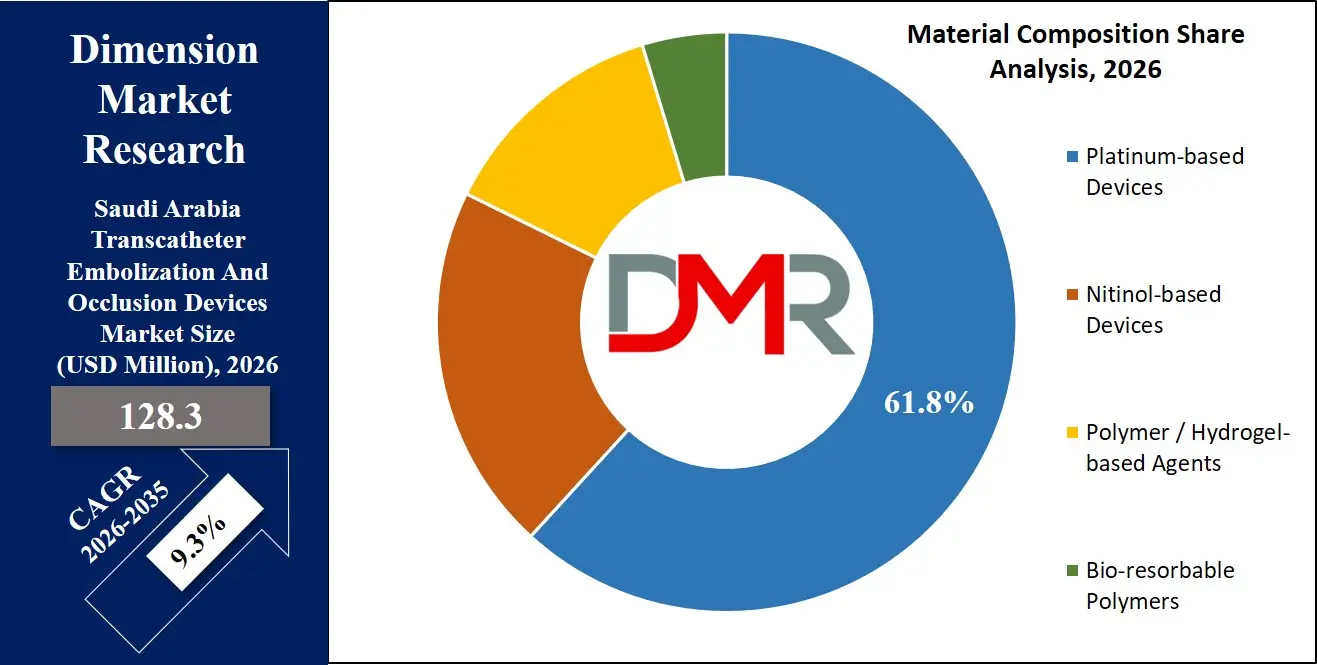

The Saudi Arabia Transcatheter Embolization And Occlusion Devices Market size is expected to reach a value of USD 128.3 million in 2026, and it is further anticipated to reach a market value of USD 286.6 million by 2035 at a CAGR of 9.3%.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Saudi Arabia Transcatheter Embolization and Occlusion Devices Market is one of the rapidly growing markets in the Middle East because the region has set ambitious industrial transformation objectives that should be reached by integrating the Vision 2030 and the National Industrial Development and Logistics Program (NIDLP). With the increase in automation demand attributed to labor cost optimization, e-commerce growth, and supply chain digitization, the public sector is responding to the need for providing sophisticated minimally invasive embolization and occlusion solutions, and so, are the individual healthcare organizations.

The issue of the transcatheter embolization device management in Saudi Arabia is evolving to a higher stage in the form of a national healthcare security scenario and economic diversification. The government initiative to localize the production of medical devices and the creation of the mega health zones, such as the King Salman Energy Park (SPARK) and NEOM Medical City, are placing a huge demand on transcatheter embolization devices and related interventional radiology services.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Saudi Arabia Transcatheter Embolization And Occlusion Devices Market: Key Takeaways & Other Influencing Factors

- Market Growth Insights: The market is anticipated to reach approximately USD 128.3 million in 2026 and is projected to expand to around USD 286.6 million by 2035, registering a CAGR of 9.3% during the forecast period.

- By Product Type: The detachable coils segment is anticipated to get the majority share in the market as they offer precise placement and controlled release in complex vascular anatomies.

- By Material Composition Insights: Platinum-based devices are expected to take over the market in 2026 due to their widespread use in neurovascular and peripheral embolization procedures.

- By End User: Hospitals & clinics are popularized for high-volume interventional procedures, whereas ambulatory surgical centers are rapidly increasing because of their need for shorter procedure times and outpatient recovery.

- Cancer Incidence Burden: Saudi Arabia reports over 28,000 new cancer cases annually, with multiple indications (liver tumors, colorectal cancer, and metastases) requiring embolization-based interventional treatments.

- Interventional Radiology Workforce Gap: The country has approximately 140–150 radiologists per million population, but only around 2% specialize in interventional radiology, creating a supply gap that increases reliance on advanced embolization devices.

- Hospital Infrastructure Capacity: Saudi Arabia has more than 500 hospitals, with a growing number equipped with catheterization labs and angiography suites, supporting increasing volumes of embolization and occlusion procedures.

Impact of the Iran conflict on the Saudi Arabia Transcatheter Embolization And Occlusion Devices Market

The Iran crisis is a risk that has augmented supply chain and regulatory risks in the Transcatheter Embolization and Occlusion Devices Market in Saudi Arabia. The mounting tensions risk disruption of import pathways of catheter systems and microcoils, and accelerate the necessity to have localized production capacities, which include quality assurance and supply chain resilience. The players (NEOM Medical, SAUDI ARAMCO (medical technology division), and local distributors) are making investments in local manufacturing partners, e-commerce solutions, and quality certification solutions. The market is shifting towards vertically-integrated markets with a combination of local sourcing, ISO-certified production, and digital distribution. It will allow local producers, logistics companies, and certification organizations across the medical device programs in Saudi Arabia.

Saudi Arabia Transcatheter Embolization And Occlusion Devices Market: Use Cases

- Interventional Oncology Expansion in Tertiary Hospitals: Rising cancer burden is driving the adoption of embolization procedures such as transarterial chemoembolization (TACE) and radioembolization across tertiary care centers, increasing demand for advanced embolization devices in liver and tumor management.

- Neurovascular Intervention for Stroke and Aneurysm Management: Growing incidence of stroke and cerebral aneurysms is accelerating the use of coil embolization and flow diversion procedures in specialized neurovascular units, supporting higher utilization of detachable coils and liquid embolics.

- Public-Private Partnership (PPP) Driven Cath Lab Expansion: Collaborations led by the Ministry of Health and private sector are expanding hybrid operating rooms and catheterization labs, enhancing access to minimally invasive embolization procedures across major hospitals.

- Minimally Invasive Treatment Adoption in Vascular Disorders: Increasing preference for minimally invasive techniques in treating peripheral vascular diseases, uterine fibroids, and AV malformations is boosting embolization device usage due to shorter recovery times and reduced hospital stays.

Saudi Arabia Transcatheter Embolization And Occlusion Devices Market: Market Dynamics

Driving Factors in Saudi Arabia Transcatheter Embolization And Occlusion Devices Market

National Healthcare Infrastructure Expansion

The most important driving forces of the transcatheter embolization device market are the Vision 2030 National Industrial Development and Logistics Program (NIDLP) and the National Transformation Program. These initiatives of the government impose the quality of healthcare output and patient safety and localization of medical device technologies that give a top-down demand on the purchase of transcatheter embolization devices and the provision of performance reporting and predictive maintenance services throughout the healthcare economy.

Growth in Interventional Radiology Activity and Clinical Workforce Pressures

The rising volume of interventional oncology procedures, neurovascular interventions, and trauma care which are caused by chronic disease prevalence, supply chain volatility, and specialist shortages are major drivers of the market. These are the conditions that require advanced embolization device interventions and long-term inventory management plans, which will equip providers with the capability to decrease operational costs and ensure long-term clinical sustainability.

Restraints in Saudi Arabia Transcatheter Embolization And Occlusion Devices Market

Regulatory Compliance Gaps and Limited Local Manufacturing Ecosystem

The system of regulatory accelerated approval of new transcatheter embolization devices, which is built in Saudi Arabia through the Saudi Food and Drug Authority (SFDA), is not as developed as in Europe and the US. Lack of rapid pathways for bio-resorbable embolics and lack of localized production of catheters and micro-guidewires can lead to dependence on supply chain and will not allow the mass adoption and cost-cutting of the market.

Shortage of Skilled Interventional Radiologists and Device Technicians

The local interventional radiologists and device technicians are not sufficient in the special field of complex embolization procedures, particularly in such fields as flow diversion and liquid embolics handling. This reliance on international clinical experts can increase costs and slow down the experience of instilling new embolization device skills into homeland hospitals.

Opportunities in Saudi Arabia Transcatheter Embolization And Occlusion Devices Market

Expansion of Local Manufacturing and Supply Chain Self-Reliance

The possibility of developing local expertise in the fields of transcatheter device assembly, coil calibration, and catheter-based tooling has a strong chance of growth and development. Localized manufacturing plants, AI-based inventory systems, and cold chain logistics (for temperature-sensitive liquid embolics), specific to the demands of the Gulf area, can address some of the most important market demands and help the Kingdom become self-sufficient in this important sphere of interventional medical devices.

Shift Toward Performance-Based Service Models and Uptime Contracts

With Saudi Arabia coming up with a value-based healthcare framework, the transcatheter embolization device performance management services have a huge prospect. Demand in both the public hospital networks and the private interventional centers will be high as a result of the necessity to independently verify device uptime, risk assess embolization lines in the system registry, and be compliant with international medical device safety guidelines.

Trends in Saudi Arabia Transcatheter Embolization And Occlusion Devices Market

Integration of Digital Monitoring and Smart Hospital Platforms

The fact that embolization device intelligence is being integrated into the basic design and operational model of digital hospital platforms in Saudi Arabia is one of the significant trends in this market. System data are being fed into hospital information systems (HIS) and remote monitoring applications and into cath lab command centers to allow real-time procedure downtime detection and automatic inventory reordering.

Shift Toward Bio-resorbable and Image-Guided Embolization Systems

Taking into account the saliency of long-term device complications, the focus on managing the risks associated with the use of embolization systems is one of the trends that should be considered, which also presupposes the introduction of the next-generation systems. Such technologies as image-guided flow-directed embolics and bio-resorbable polymer devices are highly important in terms of investments, and their application is becoming the norm in large medical centers as post-market surveillance of such new systems.

Saudi Arabia Transcatheter Embolization And Occlusion Devices Market: Research Scope and Analysis

By Product Type Analysis

The Saudi Arabia market is led by the Coils segment, driven by Detachable Coils, which account for approximately 59.3% of the total market share in 2026. As a subcategory of coils, they are preferred for precise, controlled deployment, high conformability, and suitability for complex procedures. Pushable Coils are mainly used in less complex cases. The fastest-growing segment is Non-Coil Devices, particularly Liquid Embolics, due to rising focus on reducing reintervention rates and treating complex vascular conditions, despite risks like non-target embolization and flow control challenges. Accessories ensure efficient device delivery across procedures.

By Material Composition Analysis

The most prominent segment is Platinum-based Devices, accounting for approximately 61.8% of the market share in 2026, since it provides the basic operational radiopacity and flexibility for neurovascular and peripheral procedures on the basis of which all the other configurations work.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

This is ease of deployment, lower capital requirement, and modularity. The segment with the highest CAGR is Bio-resorbable Polymers because of the need for temporary occlusion and better long-term vessel healing. Nitinol-based devices will still be an important part of peripheral vascular applications, and the Polymer/Hydrogel-based agents will still be needed in hypervascular tumor embolization.

By Application Analysis

This segment is poised to be dominated by Oncology, accounting for approximately 37.8% of the market share in 2026, because it is recommended that the least non-target embolization solutions should serve the high-throughput interventional oncology requirements as well as be compatible with the 24/7 cancer centers currently being established. The segment with the highest CAGR is Neurology, due to the increasing need for cerebral aneurysm and AVM embolization. Also important is the Peripheral Vascular Disease segment for small vessel occlusion, where complex, critical flow traceability is of paramount importance due to the complete validation and durability required.

By End-User Analysis

Hospitals & Clinics is the dominating segment, accounting for approximately 58.3% of the market share in 2026, since the majority of high-value device procurements are represented by the large number of tertiary care clients who have long-term contracts, interventional suite integration needs, and after-sales support requirements. The segment with the highest CAGR is Ambulatory Surgical Centers, largely due to healthcare sector digitization and general improvement in outpatient measures, and is becoming more and more used for same-day embolization procedures. Others (including specialty institutes and research centers), working with complex R&D and critical care cases, are also another end user, although a less important one.

Saudi Arabia Transcatheter Embolization And Occlusion Devices Market Report is segmented on the basis of the following:

By Product Type

- Coils

- Pushable Coils

- Detachable Coils

- Non-Coil Devices

- Flow Diverting Devices

- Embolization Particles

- Liquid Embolics

- Other Non-Coil Devices

- Accessories

By Material Composition

- Platinum-based Devices

- Nitinol-based Devices

- Polymer / Hydrogel-based Agents

- Bio-resorbable Polymers

By Application

- Oncology

- Peripheral Vascular Disease

- Neurology

- Urology

- Others

By End User

- Hospitals & Clinics

- Ambulatory Surgical Centers

- Others

Impact of Artificial Intelligence in Saudi Arabia Transcatheter Embolization And Occlusion Devices Market

The integration of machine learning algorithms enhances AI-powered analytics platforms in the Saudi Arabia Transcatheter Embolization and Occlusion Devices Market. With predictive models, demand forecasting, and inventory optimization, providers can anticipate market changes and align supply chains, reducing inventory levels and improving hospital efficiency.

The incorporation of AI also assists in sourcing transparency and quality assurance of embolization devices. AI-based vision inspection devices and supply chain analytics can verify device materials, identify production flaws or contamination, and forecast sourcing disruptions based on environmental and geopolitical conditions. This is particularly important for healthcare plans in Saudi Arabia, including NEOM Medical City, where device purity, sterility, and regulatory quality can be ensured with reduced reliance on manual testing.

Saudi Arabia Transcatheter Embolization And Occlusion Devices Market: Competitive Landscape

The Saudi Arabia market of transcatheter embolization and occlusion devices is a dynamic place, with large government-funded healthcare zones, top international medical device manufacturers, and an additional ecosystem of local distributors. The focus of competition lies in the realization of the Vision 2030 healthcare goals.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Anchors, key consumers, and innovators are state-owned hospital networks and project developers, including the Ministry of Health, Saudi Aramco Medical Development, NEOM Medical City, and SABIC Medical. They are associated with the largest companies worldwide such as Medtronic, Boston Scientific, Terumo, Stryker Neurovascular, and Siemens Healthineers on embolization technologies and clinical training. The developing healthcare sector is served by local and regional distributors such as Tamer Group and Al Rushaid Medical.

Some of the prominent players in Saudi Arabia Transcatheter Embolization And Occlusion Devices Market are:

- Medtronic plc

- Boston Scientific Corporation

- Abbott Laboratories

- Stryker Corporation

- Terumo Corporation

- Johnson & Johnson (Cerenovus division)

- Penumbra, Inc.

- Cook Group Incorporated

- Merit Medical Systems, Inc.

- Cordis Corporation

- B. Braun Melsungen AG

- Edwards Lifesciences Corporation

- Balt Extrusion SAS (Balt Group)

- phenox GmbH

- Acandis GmbH

- Asahi Intecc Co., Ltd.

- Kaneka Corporation

- Other Key Players

Recent Developments in Saudi Arabia Transcatheter Embolization And Occlusion Devices Market

- January 2026: Boston Scientific Corporation announced a definitive agreement to acquire Penumbra Inc., strengthening its position in neurovascular and embolization technologies and expanding its portfolio in thrombectomy and vascular intervention segments.

- October 2025: Penumbra Inc. announced the launch of its SwiftSET neuroembolization coil, strengthening its neurovascular embolization portfolio for treating complex aneurysms and supporting minimally invasive procedures globally, including Middle East markets.

- May 2025: Terumo Corporation announced commercial availability of its SOFIA 88 neurovascular support catheter, expanding its stroke and embolization treatment ecosystem and strengthening its interventional portfolio.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 128.3 Mn |

| Forecast Value (2035) |

USD 286.6 Mn |

| CAGR (2026–2035) |

9.3% |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors and etc. |

| Segments Covered |

By Product Type (Coils, Non-Coil Devices, Accessories), By Material Composition (Platinum-based Devices, Nitinol-based Devices, Polymer / Hydrogel-based Agents, Bio-resorbable Polymers), By Application (Oncology, Peripheral Vascular Disease, Neurology, Urology, Others), By End User (Hospitals & Clinics, Ambulatory Surgical Centers, Others) |

| Country Coverage |

The Kingdom of Saudi Arabia (KSA) |

| Prominent Players |

Medtronic plc, Boston Scientific Corporation, Abbott Laboratories, Stryker Corporation, Terumo Corporation, Johnson & Johnson (Cerenovus division), Penumbra, Inc., Cook Group Incorporated, Merit Medical Systems, Inc., Cordis Corporation, B. Braun Melsungen AG, Edwards Lifesciences Corporation, Balt Extrusion SAS (Balt Group), phenox GmbH, Acandis GmbH, Asahi Intecc Co., Ltd., Kaneka Corporation, and Other Key Players |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users), and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days and 5 analysts working days respectively. |

Frequently Asked Questions

How big is the Saudi Arabia Transcatheter Embolization And Occlusion Devices Market?

▾ The Saudi Arabia Transcatheter Embolization And Occlusion Devices Market size is estimated to have a value of USD 128.3 million in 2026 and is expected to reach USD 286.6 million by the end of 2035.

What is the growth rate in the Saudi Arabia Transcatheter Embolization And Occlusion Devices Market?

▾ The market is growing at a CAGR of 9.3% over the forecasted period.

Who are the key players in the Saudi Arabia Transcatheter Embolization And Occlusion Devices Market?

▾ Some of the major key players in the Saudi Arabia Transcatheter Embolization And Occlusion Devices Market are Boston Scientific Corporation, Terumo Corporation, Penumbra, Inc., Stryker Corporation, and Johnson & Johnson (Ceronovus), and many others.