What is the Second-Life EV Battery Market Size?

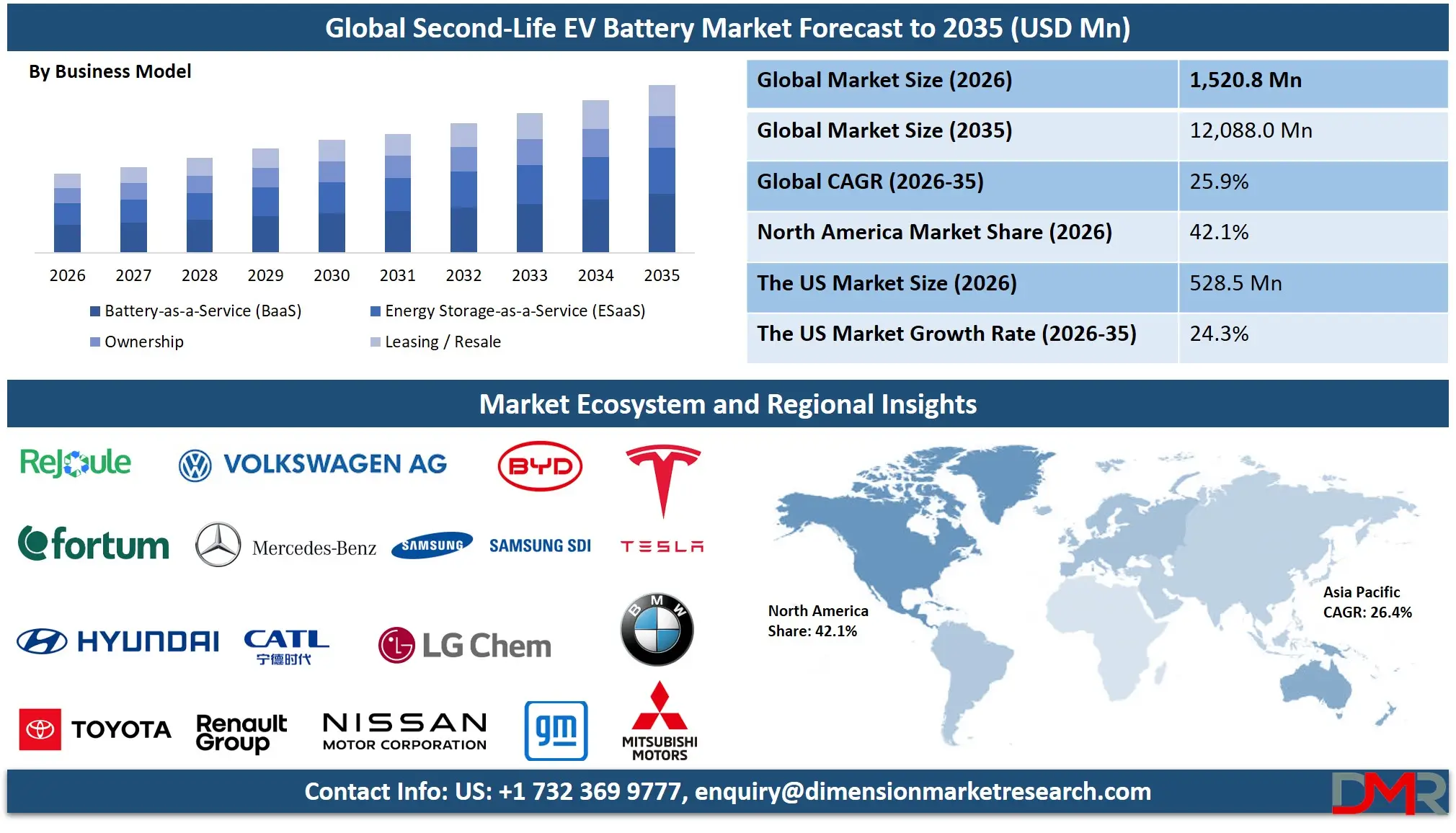

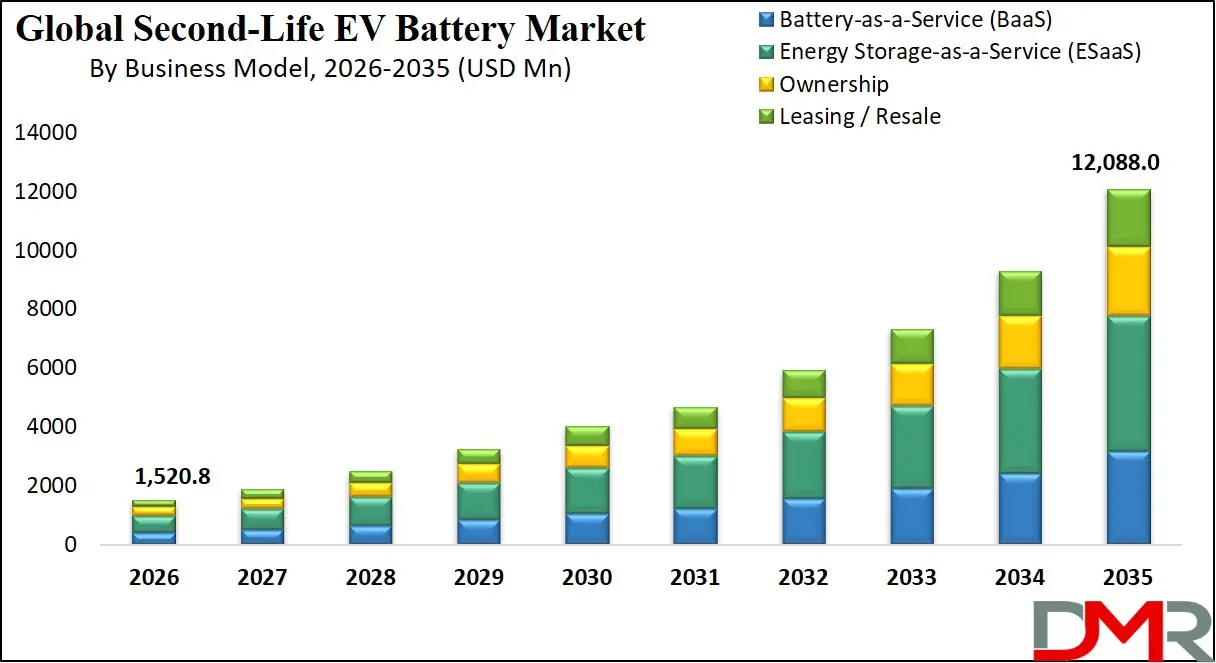

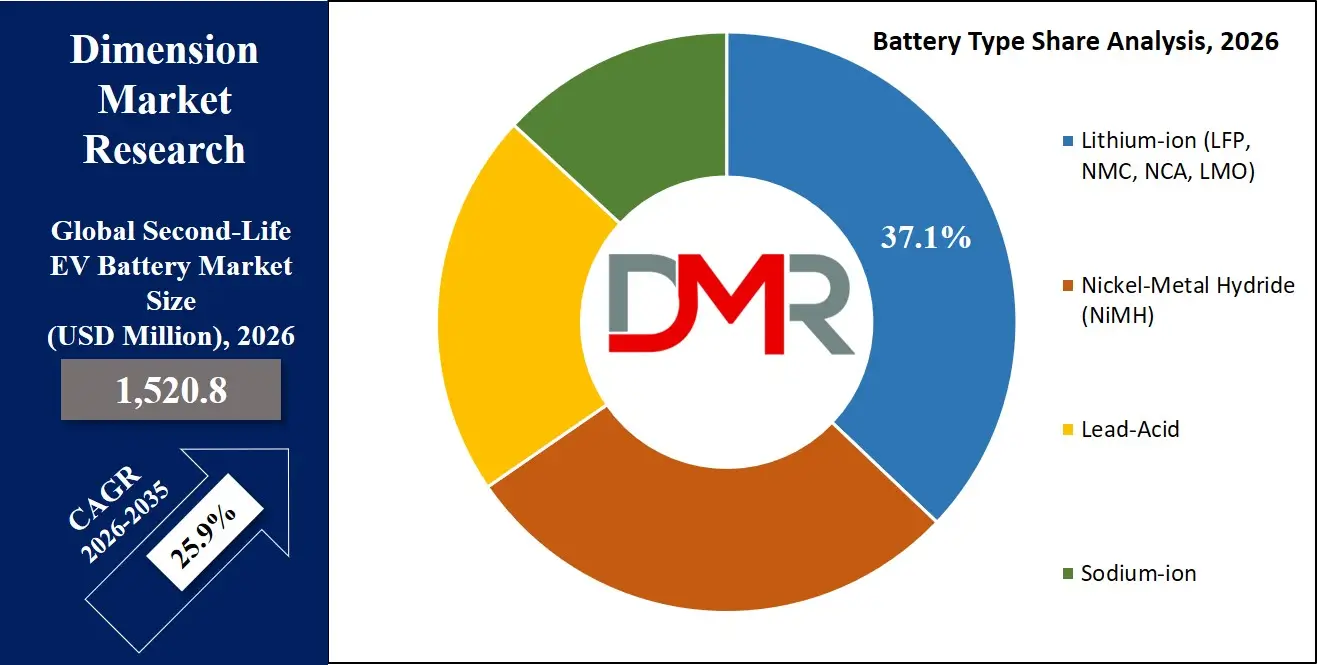

The Global Second-Life EV Battery Market is expected to reach a value of USD 1,520.8 million in 2026, and it is further anticipated to reach USD 12,088.0 million by 2035, growing at a CAGR of 25.9% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The second-life electric vehicle (EV) battery market has been growing exponentially as the first generation of electric vehicles reach their end of life and the need for a circular economy becomes more urgent. The market offers testing, repurposing, redeployment and repurposing services that break down end-of-life EV batteries and repurpose them in less critical stationary applications.

The growing urgency to manage the ever-increasing number of decommissioned Lithium-ion packs, build sustainable energy storage value chains and postpone the large-scale battery recycling processes are creating a need for second-life services. The target users are utilities, commercial & industrial and residential, with Lithium-ion chemistries (LFP and NMC) the most common because of the residual capacity and costs. The renewable energy storage, grid-scale energy storage, and EV charging infrastructure markets are primary applications as they need economical, reliable and scalable storage ecosystems.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

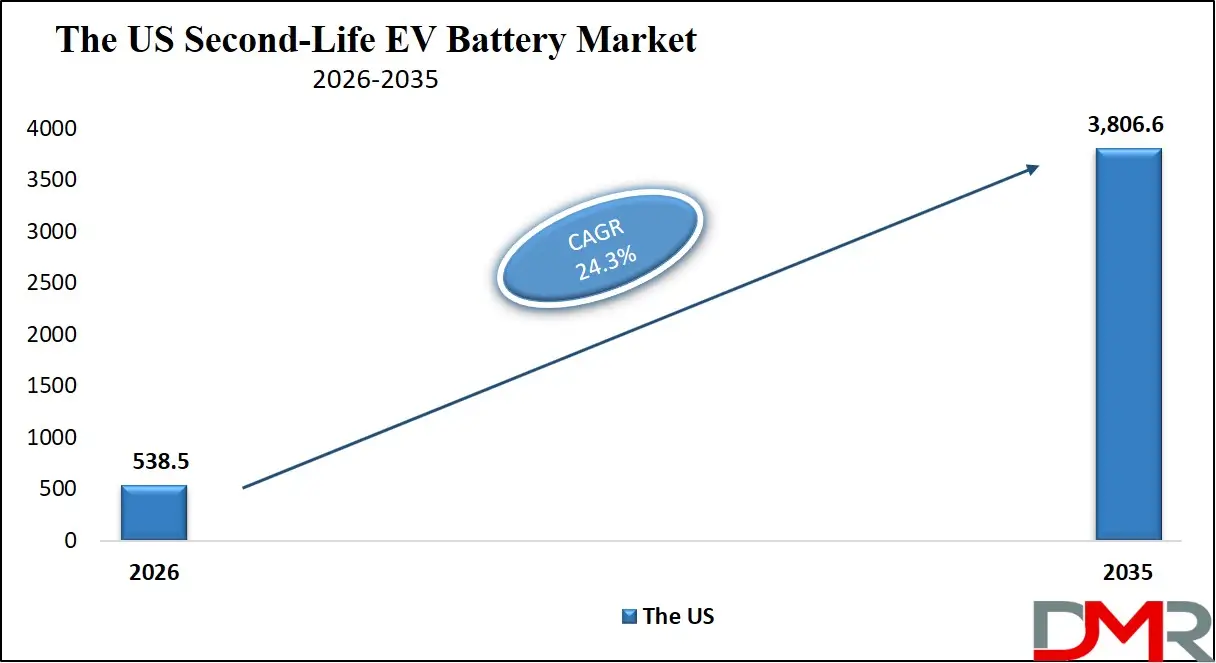

The US Second-Life EV Battery Market

The US Second-Life EV Battery Market is projected to reach USD 538.5 million in 2026 at a compound annual growth rate of 24.3% over its forecast period, which is further poised to reach a market value of USD 3,806.6 million by 2035.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The US remains the biggest and most mature market for second-life electric vehicle (EV) batteries as a result of the ambitious electrification goals of major fleets and the increasing pressure on the aging electricity grid. The market has been characterised by the strong demand for Software-managed Systems, for which companies are concerned with the deployment of artificial intelligence (AI) battery management systems to safely pool and manage hundreds of retired packs with varying levels of health. In addition, the deployment of large-scale Renewable Energy Storage projects is also creating the same demand for Energy Storage-as-a-Service (ESaaS) business models to jointly defer capital investment for grid operators and to integrate intermittent solar and wind generation.

The Europe Second-Life EV Battery Market

The Europe Second-Life EV Battery Market is estimated to be valued at USD 438.0 million in 2026 and is further anticipated to reach USD 3,403.5 million by 2035 at a CAGR of 25.6%.

The regulatory landscape such as the EU Battery Regulation and extended producer responsibility schemes have a profound influence on the European market and promote the need for advanced Battery-as-a-Service (BaaS) and leasing schemes to promote responsible product life cycle. The region also sees an accelerated roll-out of Hybrid Systems as Commercial & Industrial (C&I) customers in Germany and France attempt to combine on-site solar generation with second-life battery storage to counter price fluctuations. Also, the establishment of a pan-European circular battery economy is driving the need for service providers to build dedicated battery testing and grading centres to offer transparency and safety testing for a variety of second-life battery stocks.

The Japan Second-Life EV Battery Market

The Japan Second-Life EV Battery Market is projected to be valued at USD 164.2 million in 2026. It is further expected to witness robust growth, holding USD 1,199.6 million in 2035 at a CAGR of 24.7%.

Japan is special with a national corporate initiative to decarbonise society and prepare for disasters in the wake of the country's vulnerability to earthquakes and the shutdown of nuclear power plants. A significant part of the investment is in Standalone Systems for Power Backup and Residential Energy Storage as local governments and large conglomerates implement second-life packs from first-generation passenger electric vehicles for community microgrids. There is also a need to deeply engage in the local market to fill the gap between repurposed Nickel-Metal Hydride (NiMH) packs and new Lithium-ion (LFP) systems, which is a niche for Software-managed Systems and Energy Storage-as-a-Service.

Key Takeaways

- Market Size & Forecast: The Global Second-Life EV Battery market is projected to reach USD 1,520.8 million in 2026, expanding dramatically to USD 12,088.0 million by 2035, fueled by the dual drivers of a massive incoming wave of retired EV batteries and the mandatory creation of a circular battery materials supply chain.

- Growth Rate & Outlook: Global market growth is expected at a CAGR of 25.9%, because of the urgent need to lower the cost of energy storage systems and the increasing complexity of combining diverse battery chemistries and states of health in a single stationary system.

- Primary Growth Drivers: Major drivers driving this market growth include the global need to keep high-volume battery waste out of landfill, the economic need for low-cost grid-scale energy storage to integrate renewables, and the rollout of high-power EV charging infrastructure that must be buffered with second-life systems.

- Key Market Trends: Key trends include the emergence of testing and grading platforms for Li-ion (LFP, NMC) packs, the adoption of AI-powered tools in software-managed systems to automate the cell balancing and thermal runaway prevention, and the shift towards energy storage-as-a-service (ESaaS) as utilities are looking for CapEx-light approaches to grid stabilization.

- By Battery Type Analysis: Lithium-ion is projected to dominate this segment due to its high residual capacity and compatibility with energy storage systems makes it suitable for second-life applications, surpassing NiMH, lead-acid, and emerging sodium-ion technologies around the world.

- By System Type Analysis: Hybrid systems is poised to dominate system type segment as they merge second-life and new batteries to deliver stable, reliable energy. They address battery health variability, improve efficiency, and are preferred for large-scale and critical applications needing reliable and optimal energy output.

- By Vehicle Source Analysis: Passenger vehicles are the leading source of vehicle batteries due to increased EV uptake and production. Their batteries have uniform design, are easier to repurpose, and have adequate remaining capacity, thus providing a significant supply of batteries for second-life energy storage.

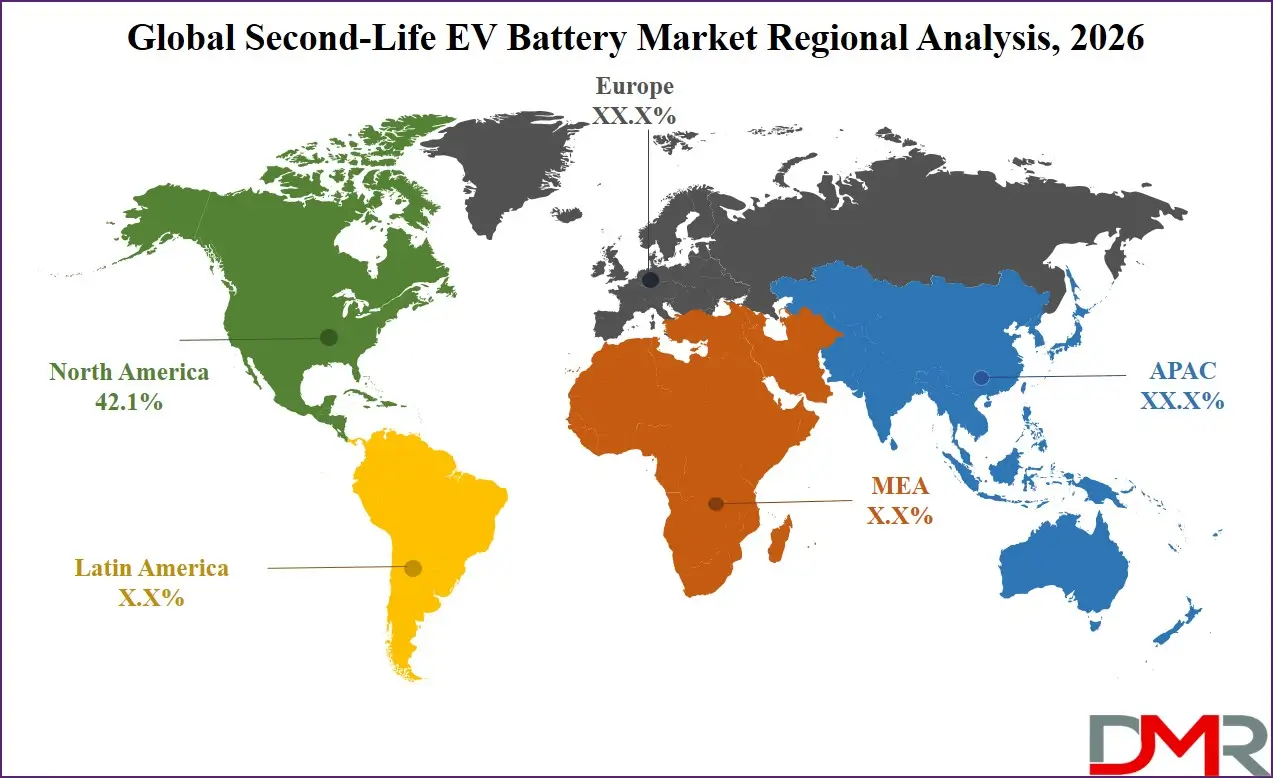

- Regional Leadership: North America is poised to dominate this market with 42.1% of the market share in 2026 due to its well-developed electric vehicle ecosystem and proactive state-level clean energy storage mandates that make it a leader in this market.

What is the Second-Life EV Battery?

Second-Life EV Battery Services refer to the specialised testing, reuse and controlled integration services provided by industry players, battery lifecycle managers and energy services companies to help organisations traverse the whole post-vehicle battery value chain. These services are not connected with the manufacturing of new batteries, but with the how of deploying an asset safely and profitably. This is with Battery-as-a-Service (BaaS) to develop a strategic roadmap of per-kWh usage, Ownership and Leasing models to physically place assets onto the site of an end-user and integrate them without causing disruption to their business, and Software-managed Systems to ensure that thousands of retired cells with varying impedances can communicate and work as a single reliable energy storage plant. As millions of EV batteries will retire each year, professional lifecycle services will be required to attain safe operation, regulatory compliance, and performance guarantees, and a second-life investment will turn into a real grid resilience, rather than a risky waste liability.

Use Cases

- Sodium-ion Readiness in Telecom: Telecom tower operators employ leasingbusiness models and Software-controlled Systems to deploy second-life packs to replace diesel generators in place of new fire-safe and ultra-low-cost hybrid backup system, with emerging Sodium-ion batteries now being tested.

- Peak Shaving for Data Centers: Data center operators apply Energy Storage-as-a-Service (ESaaS) and hybrid systems, which combine retired NMC packs out of the commercial cars along with on-site solar to cut peak energy use and engage in grid frequency markets without capital investment.

- Community Microgrid Resilience: Off-grid and remote communities utilize Standalone Systems made up of repurposed passenger vehicle LFP batteries to form resilient microgrids, which substitute costly and carbon-dense diesel generation with predictable, clean energy and can be operated with local ownership models.

- Fast-Charging Buffering for Highways: EV charging station operators use systems based on second-life as an integrated buffer to ultra-fast charging hubs that enables power to be pulled off a stationary Hybrid System of retired batteries instead of directly off a limited local grid connection.

How AI is Transforming the Second-Life EV Battery Market?

By eliminating the sorting and grading process in the second-life battery market and improving the safety of the operations, AI is transforming the market. In Systems controlled by software, AI-driven diagnostic systems can be used to automatically examine the electrochemical history of a battery to estimate the remaining cycle life and significantly reduce the time spent on manually testing a battery and deployment schedules, as well as project risk. In the meantime, AI-based capabilities in Energy Storage-as-a-Service enable aggregators to more effectively manage battery cycling policies by identifying abnormal cells, forecasting future degradation trends, and recommending solutions such as dynamic state-of-charge limits to implement controls and influence economic life.

Market Dynamics

Key Drivers in the Global Second-Life EV Battery Market

The Incoming Tsunami of Retired EV Batteries

The amount of these retired assets is increasing much more rapidly than the recycling industry or new energy storage production can accommodate. This is establishing a structural necessity to re-use and not to destroy. This is resulting in a trend of utilities and C&I entities collaborating with second-life integrators as opposed to relying on new battery supply alone. These firms help in vital activities such as gathering, dismantling, electrochemical assortment, repacking and controlled functioning. By using such services, organizations can get cheap storage capacity to integrate renewable energy and reduce the impact of poor disposal of batteries on the environment.

Unfavorable Economics of New Grid-Scale Storage

Large-scale energy developers and utilities are eagerly shut out of the exclusive use of first-life Lithium-ion systems, especially where maximum energy density is not needed, such as load shifting and solar firming. A new storage project is sensitive to the fluctuating prices of raw materials and lengthy manufacturing lead times. This economic force of this cost and supply chain complexity results in a strong economic motivation towards alternative sources. Therefore, the Ownership and Leasing models of second-life systems have increased demand and could provide a 30-50% cost savings over new systems when used in stationary applications with a highly skilled operational management.

Restraints in the Global Second-Life EV Battery Market

Heterogeneity and Safety Validation Costs

The majority of retired battery streams are a complicated combination of cathode chemistries (LFP, NMC, NCA, LMO), physical formats (cylindrical, pouch, prismatic), and health of state, all of various original equipment manufacturers. Their low cost of material is a major problem to standardization because of these heterogenous systems. Test, sorting and grading of thousands of individual packs can be expensive and technologically challenging to certify that they will be safe in operation when they are put into service. It requires careful logistical planning, tailor-made power electronics and fire suppression systems to deploy.

Uncertain and Evolving Regulatory Frameworks

The lack of stable and consistent regulatory conditions among jurisdictions has led to organizations being reluctant to invest in energy storage projects based on repurposed automotive batteries. Although sustainability is a strategic focus, executives are under pressure to explain to them why a product of unclear status of waste-to-product deserves to be safe and compliant. The transport permits and site fire codes, as well as the extended producer responsibility requirements of systems relying on a second-life asset category, are all under more and more scrutiny. Companies have moved to smaller pilot projects that are easily approved and prove their safety and reliability.

Growth Opportunities in the Global Second-Life EV Battery Market

Direct-to-APU Re-deployment in EV Charging Hubs

Among the large growth opportunities in the second-life battery market is the value of helping charge point operators develop integrated, buffered fast-charging islands. Many charging firms have been faced with demand charges, yet they now want their own low-cost on-site storage which does not tie them to their grid connection nor their peak power delivery. These advanced high-power energy stores are developed with expert capabilities in Hybrid System assembly, DC-coupled-power electronics, and dynamic load management software.

Off-grid Power for Telecom Tower Diesel Displacement

The necessity to combine technical expertise and knowledge in particular operational conditions is fueling the development of second-life services, as telecom vendors develop ESG-compliant solutions to energize remote infrastructure. They are tower locations in South Asia, Africa and in Latin America where grid reliability is bad. The telecom companies must comply with stringent decarbonization requirements and operation cost cutting requirements. Therefore, they need implementation partners that understand battery electrochemistry and the severe tropical deployment conditions.

Trends in the Global Second-Life EV Battery Market

The Rise of the Independent Battery Health Passport

Digital traceability is a growingly popular trend in organizations that uses alternative forms of old-fashioned and obscure salvage transactions. Companies are building indelible records of data blocks about individual battery modules, with the pack history not being lost between the vehicle dismantler and the second-life integrator. These digital passports will offer a self-service, verifiable history of state of health, thermal events and warranty status to prospective buyers. In response, second-life service providers are offering experience in cloud-based data analytics, API integration, and automated valuation.

Sustainability Monetization via Carbon Credits

Environmental impact is also becoming a prominent consideration in energy storage choices as firms are being pressured to accomplish net-zero targets and report their contributions to a circular economy. Companies have now taken an interest in second-life strategies that can be used to improve the measure of sustainability and reduce project costs and create verified carbon avoidance credits. This has led to the requirement of lifecycle auditing services. The Second-life providers help companies to record the displacement of the diesel generation, measure the emissions that the new battery manufacturing will avoid and get their project registered to generate carbon credits.

Research Scope and Analysis

By Battery Type Analysis

The second-life EV battery market is poised to be dominated by Lithium-ion batteries in this segment because of their high energy density, longer lifecycle, and high usage in electric vehicles. Chemistries like LFP, NMC, NCA and LMO have a high remaining capacity when used in automotive applications and are therefore very suitable in a second application such as in the stationary energy storage. Large-scale repurposing is further encouraged by their standardized production and established supply chain.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Moreover, lithium-ion batteries are more efficient, less self-discharge, and can be used with advanced battery management systems which can facilitate dependable operation in second-life applications. By comparison, NiMH and lead-acid batteries are less efficient and have shorter lifespan, and sodium-ion is yet to be developed.

By System Type Analysis

Hybrid systems are projected to dominate the system type segment because they merge second-life batteries with new batteries or other energy storage technologies to achieve optimal performance and reliability. This method assists in eliminating variability in residual capacity and health of used EV batteries, which guarantees a consistent energy output. Hybrid configurations also increase the lifespan and efficiency of systems due to the balance in loads on new and repurposed units. Critical applications in which high reliability is required are popular with utilities and commercial operators as they opt to use hybrid systems. Moreover, it can be integrated with powerful software and battery management systems to monitor and optimize in real-time. The hybrid models offer more flexibility and lower operational risks compared to standalone systems, and thus are the preferred type of system in large-scale deployments.

By Vehicle Source Analysis

Passenger vehicles are expected to dominate as the primary source of second-life EV batteries since their output and adoption volumes are much larger than commercial vehicles. The increase in passenger EV sales across the globe has resulted in a substantial and steady stream of used batteries entering the secondary market. These batteries are usually used up to 70-80% capacity and hence are easily repurposed. The use of battery packs that are standardized in passenger EVs also makes the task of collection, testing, and refurbishing easier. Conversely, commercial vehicle batteries are very diverse in size and usage patterns, which restricts scalability. With the use of passenger EVs becoming increasingly popular worldwide, the segment will also continue to provide the largest portion of second-life battery supply.

By Business Model Analysis

Energy Storage-as-a-Service (ESaaS) is anticipated to dominate this segment since it eliminates initial capital expenditure and operational risks to end users. With this model, installations, maintenance and performance are handled by the providers, and the customers can enjoy energy storage solutions in either a subscription or pay-per-use model. This is especially appealing to utilities and commercial users who want flexibility and predictability of costs. ESaaS is also beneficial to the lifecycle management of second-life batteries, which is necessary to ensure optimal use and performance. In comparison to ownership models, ESaaS is faster to adopt with reduced financial hurdles and easy deployment. With the transition of energy markets towards service-based approaches and distributed energy systems, ESaaS is gaining momentum as the business model of choice.

By Application Analysis

Grid-scale energy storage is projected to dominate this segment as the energy requirement grows towards balancing, peak shaving, and integration of renewable energy. The second-life EV batteries offer a cost-effective alternative to new batteries in large-scale storage systems, which is very appealing to utilities. Such systems assist in stabilizing the power grids by storing the surplus energy in low-demand times and discharging it during peak times. The increased adoption of renewable energy sources like solar energy and wind power also contributes to the need for grid-scale storage. Also, governments and regulators are encouraging the implementation of energy storage to improve grid resilience. Consequently, grid-scale applications have the greatest and most significant application of second-life EV batteries.

By End User Analysis

The utilities and grid operators are poised to lead this segment because they implement large-scale energy storage systems to improve grid stability, reliability, and efficiency. Large storage space is needed by these entities to support the variability in energy supply and demand, especially as more renewable energy is incorporated. EV batteries in the second life provide a cost-effective method to enable utilities to increase storage capacity as well as help achieve sustainability objectives. Also, utilities enjoy the benefits of long-term operation and centralised control, and therefore are the best consumers of used batteries. Utilities are run on a scale that is much larger compared to residential or telecom sectors, which increases demand. They are the most dominant end-user segment due to their strategic role in energy systems.

The Global Second-Life EV Battery Market Report is segmented on the basis of the following:

By Battery Type

- Lithium-ion (LFP, NMC, NCA, LMO)

- Nickel-Metal Hydride (NiMH)

- Lead-Acid

- Sodium-ion

By System Type

- Standalone Systems

- Hybrid Systems

- Software-managed Systems

Vehicle Source

- Passenger Vehicles

- Commercial Vehicles

By Business Model

- Battery-as-a-Service (BaaS)

- Energy Storage-as-a-Service (ESaaS)

- Ownership

- Leasing / Resale

By Application

- Grid-Scale Energy Storage

- Renewable Energy Storage

- EV Charging Infrastructure

- Power Backup Systems

- Residential Energy Storage

- Off-grid / Microgrid Systems

By End User

- Utilities & Grid Operators

- Commercial & Industrial (C&I)

- Residential

- Telecom

- Data Centers

Regional Analysis

Leading Region by Market Share

North America is poised to dominate the global second-life EV battery market as it is projected to hold 42.1% of the market share by the end of 2026. This is the largest share of the second-life battery market due to the unprecedented density of end-of-life Tesla and other first-generation EV packs and the aggressive energy storage purchasing requirements of states such as California and New York. The region boasts an established ecosystem of automotive dismantlers, battery lifecycle management startups, and a highly skilled talent base in power systems engineering.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The utility investment in mitigating wildfires, solar firming, and the general transition to gas-fired peaker plants towards the phase-out is helping maintain the need to use cost-effective second-life grid resources and ongoing optimization. In addition, a positive federal investment tax credit on standalone storage keeps funding innovative ESaaS business models requiring a low-cost, secure source of storage to attain rapid deployment and stable revenue stacking.

Fastest-Growing Regional Market

Asia-Pacific is expected to be the most rapidly expanding second-life EV battery market, due to the sweeping circular economy requirements led by the government in China, India, Japan, and South Korea. The accelerated decommissioning of early electric buses and two-wheelers, the emergence of a digitally-satiated energy-hungry economy, and the dynamic growth of off-grid rural regions are pushing state utilities and telecom operators to turn to ultra-low-cost repurposed storage. The Leasing/Resale business models are highly sought after to enable these large organizations to shift to opex-based, circular energy storage operating models with no capital overhang. Another emerging and growing regulatory need in the area is producer responsibility, which is nascent and needs to be outsourced to second-life aggregation to test, reuse, and handle retired packs to fill in the recycling backlog and implement clean energy projects more quickly.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

Global second-life EV battery market has developed a very dynamic competitive environment with a diverse mix of global automotive OEMs, pure-play battery science startups, and large energy infrastructure developers. Deep strategic partnerships with dismantlers and OEMs will be the key to success since the ability to obtain a steady, traceable supply of retired packs is the key to the joint development of economic projects and access to project financing. Market consolidation is already going on fast gearing towards the purchase of specialist second-life integration companies by traditional electric utilities in an effort to guarantee a pipeline of affordable storage to modernize the grid. Proprietary intellectual property such as battery-agnostic power conversion platforms and AI-driven diagnostic and balancing algorithms is increasingly playing a greater role as a foundation of competitive difference than mere low-cost material sourcing or generic project development strategies.

Some of the prominent players in the Global Second-Life EV Battery Market are:

- Nissan Motor Co., Ltd.

- BMW AG

- BYD Company Ltd.

- LG Chem Ltd.

- Samsung SDI Co., Ltd.

- Tesla, Inc.

- Contemporary Amperex Technology Co., Limited (CATL)

- General Motors Company

- Volkswagen AG

- Renault Group

- Hyundai Motor Company

- Mitsubishi Motors Corporation

- Mercedes-Benz Group AG

- Toyota Motor Corporation

- Fortum Oyj

- BELECTRIC

- Connected Energy Ltd.

- B2U Storage Solutions

- ReJoule Incorporated

- Enel X S.r.l.

- Other Key Players

Recent Developments

- January 2026: General Motors announced a significant growth of its stationary storage business and a new ESaaS program to reassign commercial vehicle LFP packs to grid-scale energy storage systems, including a specific leasing channel with utility clients.

- November 2025: TotalEnergies reinforced its partnership with Toyota and unveiled a particular practice of software-controlled systems and at-home energy stores to assist end-users make smooth home backup systems out of retired NiMH hybrid batteries and remain in full regulatory compliance.

- October 2025: Lohum bought a Nordic battery analytics businesses like ReLion Battery Analytics to expand its BaaS and leasing/resale offerings to the telecom industry to fulfill the complex needs of tower operators in diesel displacement and remote power generation in a tropical environment with a microgrid.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 1,520.8 Mn |

| Forecast Value (2035) |

USD 12,088.0 Mn |

| CAGR (2026-2035) |

25.9% |

| The US Market Size (2026) |

USD 538.5 Mn |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Battery Type (Lithium-ion (LFP, NMC, NCA, LMO), Nickel-Metal Hydride (NiMH), Lead-Acid, and Sodium-ion), By System Type (Standalone Systems, Hybrid Systems, and Software-managed Systems), By Vehicle Source (Passenger Vehicles, Commercial Vehicles), By Business Model (Battery-as-a-Service (BaaS), Energy Storage-as-a-Service (ESaaS), Ownership, and Leasing/Resale), By Application (Grid-Scale Energy Storage, Renewable Energy Storage, EV Charging Infrastructure, Power Backup Systems, Residential Energy Storage, and Off-grid/Microgrid Systems), By End User (Utilities & Grid Operators, Commercial & Industrial (C&I), Residential, Telecom, and Data Centers) |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Global Second-Life EV Battery Market?

▾ The Global Second-Life EV Battery market is poised to be valued at USD 1,520.8 million in 2026 and is projected to reach USD 12,088.0 million by 2035, driven by the universal need for sustainable and low-cost energy storage for grid stabilization and renewable integration.

What is the CAGR of the Global Second-Life EV Battery Market from 2026 to 2035?

▾ The market is expected to grow at a CAGR of 25.9% from 2026 to 2035, reflecting the accelerating volume of retiring EV batteries and the persistent economic advantage of a repurposing-first strategy before material recycling.

What factors are driving the growth of the Global Second-Life EV Battery Market?

▾ Key drivers include the tsunami of retired EV batteries, the unfavorable economics of new grid-scale storage assets, the complexity of managing heterogeneous battery streams, and the surge in demand for ESaaS models amid volatile energy prices.

Which region held the largest share of the Second-Life EV Battery Market in 2026?

▾ North America is poised to dominate this market with 42.1% of the market share in 2026, driven by a mature EV ecosystem and aggressive utility investment in Solar Firming and Power Backup Systems using cost-effective second-life lithium-ion assets.

Which region is expected to grow the fastest in the Second-Life EV Battery Market?

▾ The Asia-Pacific region is expected to grow the fastest, fueled by rapid circular economy mandates in China and India, where Leasing/Resale models are critical for transitioning off-grid towers and communities to reliable, second-life based energy systems.

What are the major trends in the Global Second-Life EV Battery Market?

▾ Major trends include the creation of digital battery health passports, the integration of AI into Software-managed Systems for safety, the rise of sustainability monetization through carbon credits, and the focus on Sodium-ion as a future second-life-ready chemistry.

Who are the key players in the Global Second-Life EV Battery Market?

▾ Key players include automotive OEMs like Tesla and BMW, pure-play integrators like B2U Storage Solutions and Connected Energy, and energy infrastructure developers like Enel X and Eaton, alongside specialized diagnostics and lifecycle management startups.

How is the Global Second-Life EV Battery Market segmented?

▾ The market is segmented by Battery Type, System Type, Vehicle Source, Business Model, Application, and End User.