What is the Security for AI Market Size?

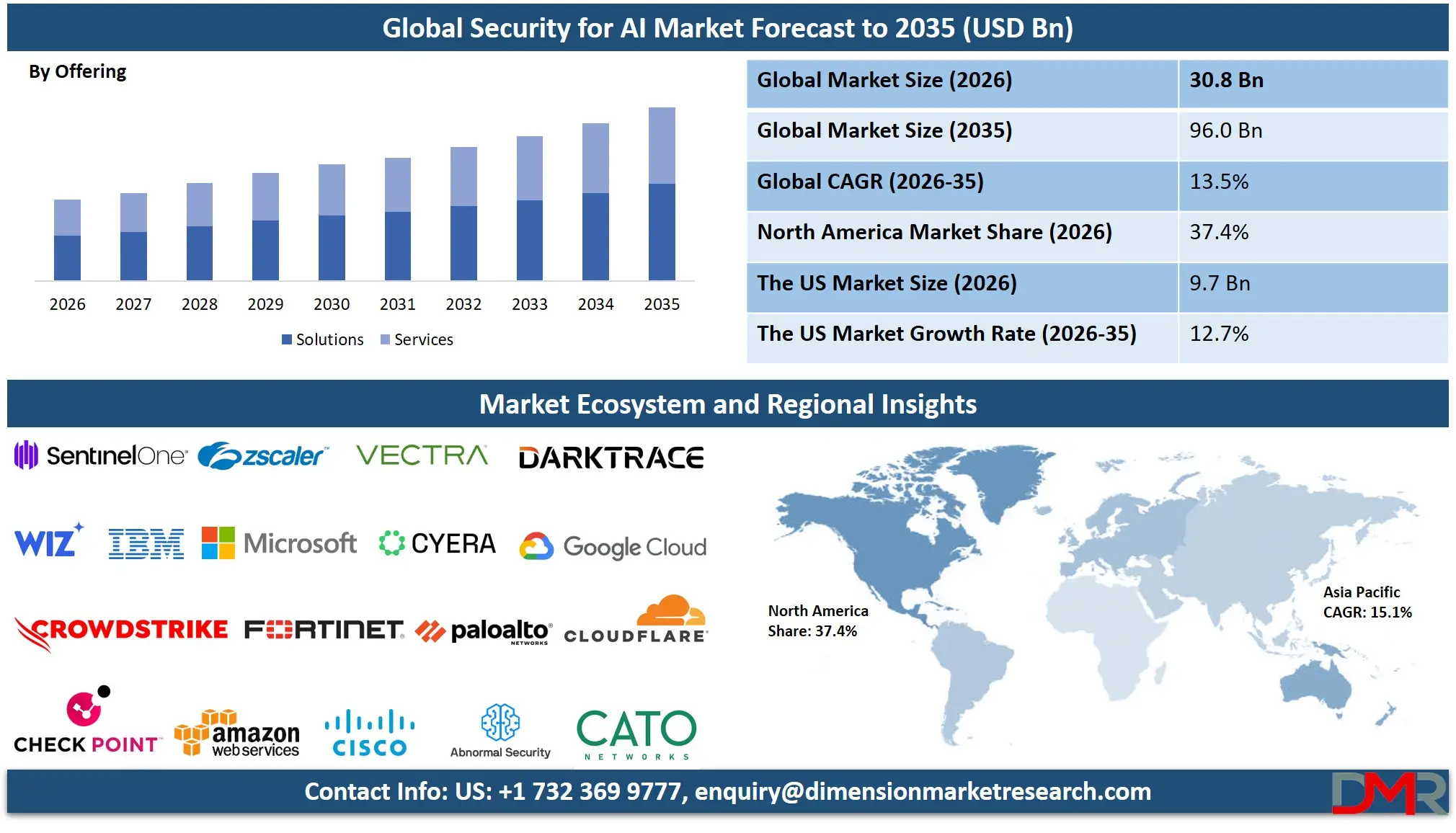

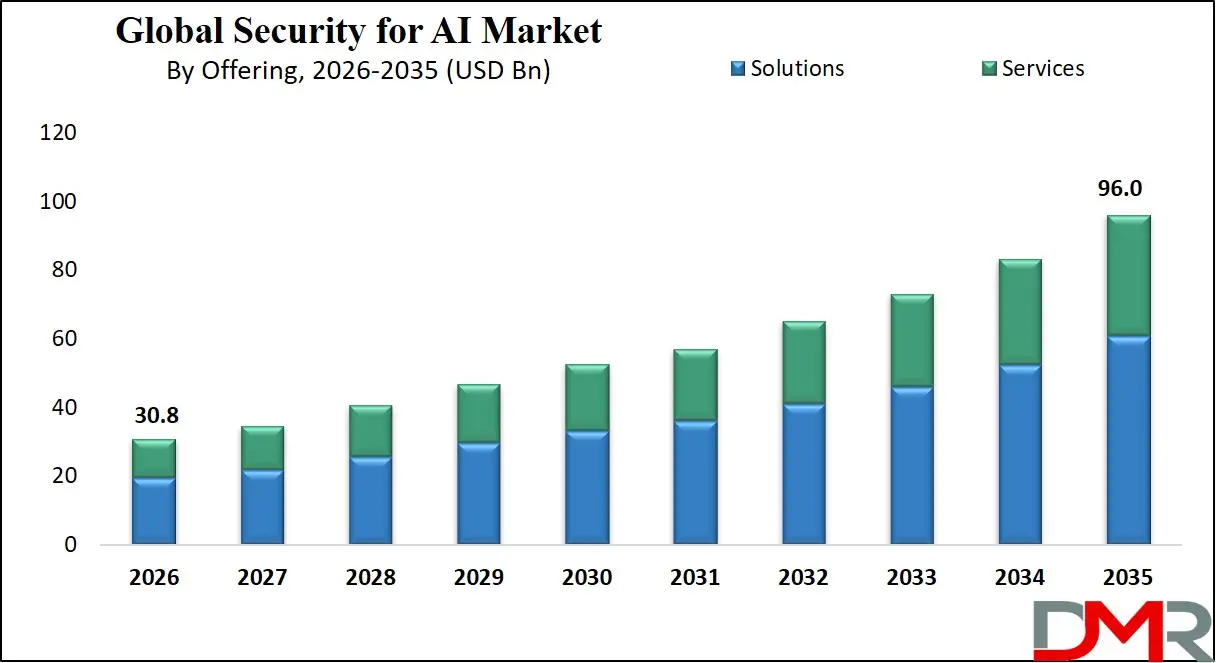

The Global Security for AI Market is expected to reach a value of USD 30.8 billion in 2026, and it is further anticipated to reach USD 96.0 billion by 2035, growing at a CAGR of 13.5% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The security for artificial intelligence (AI) market has been rapidly expanding as companies are rapidly embracing AI and at the same time increasingly facing a growing threat landscape against AI systems. This market includes products and services that secure AI models, data and the technology platforms they are trained on from specific threats such as adversarial attacks, model theft and data poisoning. The growing adoption of generative AI, large language models, and critical workloads powered by AI are creating the need for tailored security solutions.

Most common buyers are enterprises, with AI Threat Detection & Prevention Platforms and AI Governance, Risk & Compliance Tools still the most sought after products because of increasing regulation and reputational risks due to AI missteps. The BFSI, government & defense, and healthcare industries are prominent as they require secure, resilient and compliant AI systems.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The US Security for AI Market

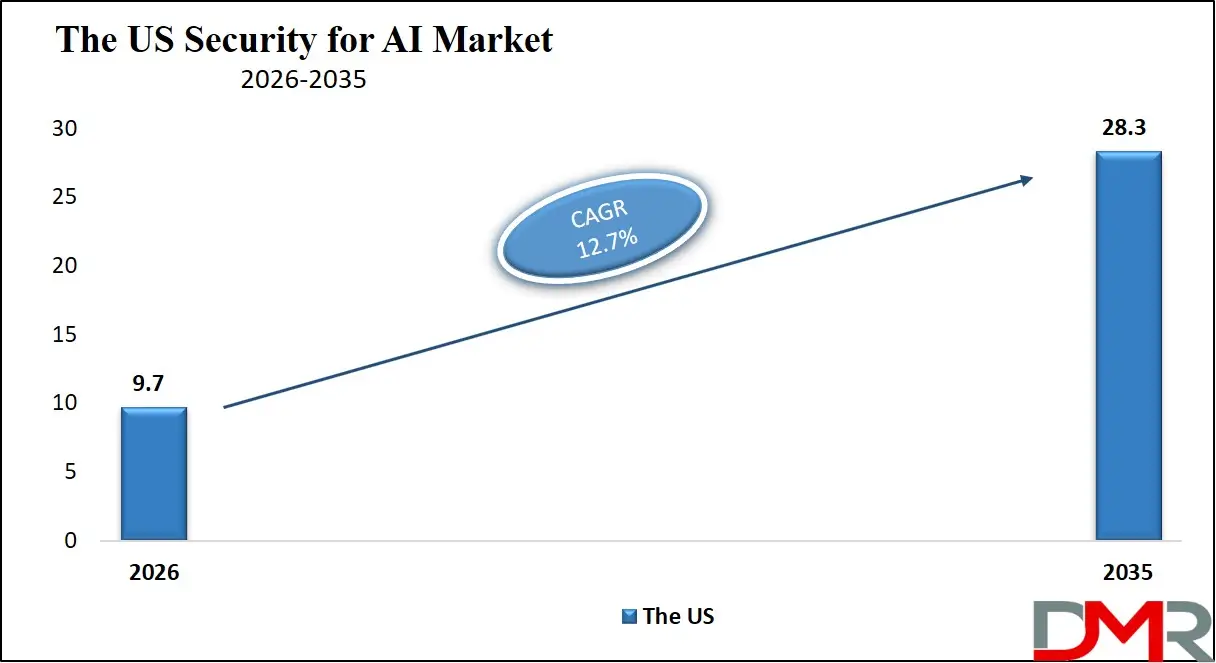

The US Security for AI Market is projected to reach USD 9.7 billion in 2026 at a compound annual growth rate of 12.7% over its forecast period, which is further forecasted to reach a value of USD 28.3 billion by 2035. The United States remains the most mature market for security in AI, owing to the rapid adoption of AI by the Fortune 500 companies and the emergence of state-based and proposed federal regulations.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The market has been characterised by significant demand for AI Model Security services, in which companies are actively working towards constructing resilient adversarial attack techniques and model verification to protect against model evasion and extraction. In addition, the deployment of generative AI in business operations is also resulting in a similar demand for Risk & Compliance Management services to govern data management and AI governance.

The Europe Security for AI Market

The Europe Security for AI Market is estimated to be valued at USD 9.0 billion in 2026 and is further anticipated to reach USD 27.2 billion by 2035 at a CAGR of 13.1%. The regulatory landscape in Europe including the EU AI Act and GDPR has a profound influence on the European market and necessitates the use of AI Governance, Risk & Compliance (AI GRC) Tools and Privacy-Preserving Machine Learning (PPML) models. There is also the rapid increase of Hybrid deployment of security solutions in the region as manufacturing and automotive sector in Germany and France seek to balance operational technology (OT) security and AI analytics. Furthermore, initiatives like GAIA-X are also pushing security providers to develop specialised Data Security & Privacy Protection services to support data sovereignty and secure AI model training in the European cloud.

The Japan Security for AI Market

The Japan Security for AI Market is projected to be valued at USD 3.3 billion in 2026. It is further expected to witness robust growth, holding USD 9.9 billion in 2035 at a CAGR of 13.0%. The Japanese market is unique, with a national corporate drive to leverage AI for societal challenges, including a declining workforce, which requires stringent security to protect critical automated systems. A significant portion of the expenditure is in security analytics and monitoring platforms and consulting services as large conglomerates implement AI in sensitive physical-world systems, such as industrial robotics and medical diagnostic technologies. Deeply integrated data loss prevention solutions are also in high demand to close the gaps between AI models, next-generation electronic medical record (EMR) systems, and industrial control systems, which makes up a niche in Behavioral Analytics and context-aware security.

Key Takeaways

- Market Size & Forecast: The Global Security for AI market is projected to reach USD 30.8 billion in 2026, which is further anticipated to be valued USD 96.0 billion by 2035, driven by the combination of high enterprise adoption rates of AI and the increasingly complex nature of AI cyber threats.

- Growth Rate & Outlook: Global market growth is expected at a CAGR of 13.5%, due to a severe lack of cybersecurity professionals with expertise in adversarial machine learning, and the increasing complexity of AI model security across the entire model lifecycle (design, development, deployment).

- Primary Growth Drivers: Major drivers include the need for mandatory compliance with new AI regulations, the escalation in the number of model poisoning and data leakage attacks, and the demand for Identity & Access Management (IAM) solutions tailored for non-human AI agent identities.

- Key Market Trends: Major trends include the emergence of dedicated AI Threat Detection & Prevention Platforms that use AI to secure AI, Context-Aware Computing to implement dynamic security policies for critical model parameters, and a shift towards Managed Security Services (MSS) as enterprises lack internal AI Security Operations Center (AI-SOC) capabilities.

- By Offering Analysis: Solutions are projected to dominate offering segment due to the preference for end-to-end solutions for AI threat detection, model protection, and model governance. These solutions offer scalability, automation, and proactive protection that allow proactive risk management with quicker return on investment than services.

- By Deployment Mode Analysis: Cloud-based deployments are poised to dominate this segment as companies favour cloud-based security for real-time analysis, automatic updates and cost-effectiveness, particularly for AI workloads that are increasingly developed and deployed in the cloud.

- By Organization Size Analysis: Large enterprises are expected to dominate this segment because of widespread use of AI, sophisticated systems, and larger cybersecurity budgets. They have complex security requirements and compliance needs, leading to substantial investment in AI security, unlike SMEs with constrained budgets.

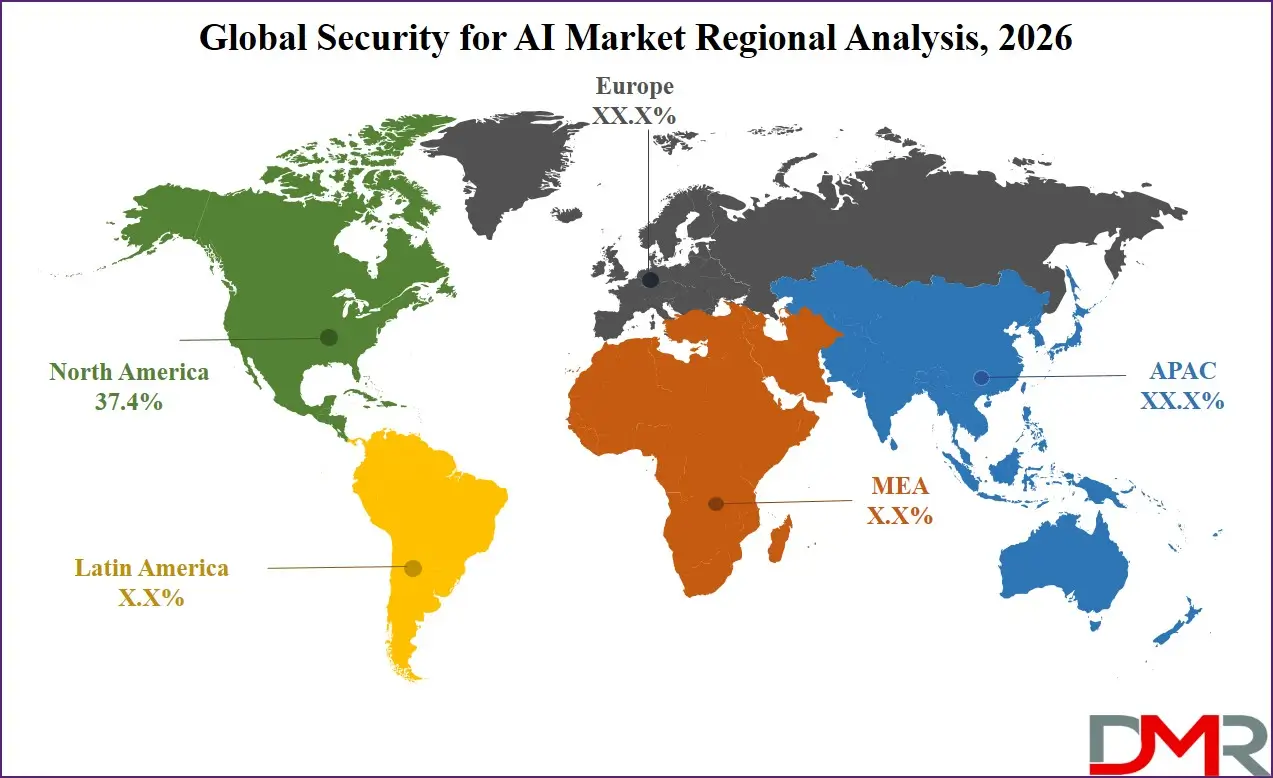

- Regional Leadership: North America is poised to dominate this market with 37.4% of the market share in 2026 because of widespread use of AI, sophisticated systems, and larger cybersecurity budgets. They have complex security requirements and compliance needs, leading to substantial investment in AI security, unlike SMEs with constrained budgets.

What is the Security for AI?

Security for AI encompasses the specialized tools, platforms, and advisory services offered by dedicated security vendors, cloud providers, and consultancies to assist organizations in protecting the entire AI lifecycle. These solutions, unlike off-the-shelf cybersecurity tools, are associated with how to secure AI. This includes AI Model Security tools to secure against adversarial machine learning attacks, AI Governance, Risk & Compliance solutions to ensure safe and responsible AI, and Security Analytics & Monitoring solutions to detect unusual patterns in model inputs and outputs that indicate an attack. Given that 90% of organizations will operate AI models in production by 2027, security for AI solutions are critical to enable trustworthy, safe and resilient AI operations to ensure that investments in AI translate to business value, rather than risk.

Use Cases

- Securing AI-Powered Fraud Detection in Banking: Financial institutions use AI Model Security solutions to safeguard their real-time fraud detection AI models from evasion attacks, where attackers manipulate transactions to defeat algorithms, protecting high-value payment networks.

- Patient Data Privacy in Healthcare AI: Hospital networks implement Data loss prevention and data security & privacy protection solutions to safeguard patient data used to train medical image AI models. This includes using privacy-enhancing technologies enabling AI training without revealing raw data, ensuring HIPAA compliance.

- National Security AI in Government: Defense agencies implement threat detection AI that meets strict data classification and sovereign deployment measures, ensuring that sensitive data used to train AI models is not leaked to the internet, using Consulting Services and on-premises AI GRC Tools.

- Securing Autonomous Vehicle AI in Manufacturing: Global car manufacturers deploy AI Threat Detection & Prevention Platforms to assess sensor data and AI decision-making pipelines in real-time, using context-aware network security to protect vehicle-to-everything (V2X) communications from spoofing and denial-of-service attacks.

Market Dynamics

Key Drivers in the Global Security for AI Market

The Global AI Security Skills Gap

Multinational corporations are struggling to get hands-on experts with skills in adversarial machine learning, AI model audit, secure MLOps pipelines, and AI threat modelling. The demand is growing faster than supply of skilled professionals which has resulted in a market gap. As a consequence, there is a trend for companies to outsource to Managed Security Services (MSS) for AI rather than hiring locally. MSS providers help with critical functions such as ongoing model monitoring, AI artifact vulnerability testing and incident response for model integrity issues. This helps organisations to speed up AI deployment cycles and reduce the cost of a successful adversarial attack on AI due to a lack of in-house AI security expertise.

Complexity of Securing the AI Supply Chain

Large companies also often source multiple AI models (usually proprietary models, third-party APIs, and fine-tuned foundation models from open-source communities) to speed up development. However, managing the security of a multi-source AI supply chain is extremely complex. Enterprises have to check for malware in the serialized model files, secure the data feed for training, and certify the security of third-party models. This might lead to significant vulnerabilities in the supply chain, and covert data exfiltration channels without expert guidance. Therefore, enterprises are in need of the AI Model Security and Security Analytics products that can help them navigate through these environments.

Restraints in the Global Security for AI Market

Inertia of Legacy Security Architecture Debt

The majority of companies still operate security operations centers and tools built in the pre-AI era and are highly adapted to network and endpoint security, rather than AI models. The legacy systems are major barriers to transformation, even though they need to be replaced by a dedicated AI system. Re-architecting security processes and incorporating dedicated tools for AI pipeline monitoring and response can be expensive, risky, and cause disruption. The fear of operational disruptions, alert fatigue, and loss of visibility across the board is what keeps organizations away. As a result, technical debt associated with legacy architecture slows the implementation of specialized AI security tools and often delays and even prevents holistic security for AI systems.

Economic Uncertainty and Budget Scrutiny

The uncertain economic and business environment has led to organizations being more cautious about investing in specialised and cutting-edge security technologies, particularly for risks they haven't experienced. Despite the emerging interest in AI risk management at the board level, security leaders are feeling the pressure to explain the need for investments in new AI GRC Tools and Managed Security Services. The service charges and duration of professional services firms are likely to be scrutinised. Companies are now moving towards "turnkey" short-term projects with quick pass/fail compliance or integration with current SIEM platforms. This is forcing the AI security vendors to be more outcome-oriented and show a reduced AI risk.

Growth Opportunities in the Global Security for AI Market

Building Trustworthy AI by Design

A major opportunity for growth in the security for AI market is helping companies build secure-by-design AI systems from the beginning of model development. Many organisations have rushed to use tools like ChatGPT, but are now experiencing the consequences of data leakage and prompt injection attacks, and would now like to have their own AI development processes secure by design. The creation of such secure-by-design environments requires expertise in integrating AI Model Security scanning into CI/CD pipelines, automating bias detection and providing strong Data Security & Privacy Protection to training data. The AI security service companies can help companies build secure and scalable AI environments to enable secure and compliant innovation.

Vertical-Specific AI Security Compliance

Combining technical expertise in AI security with knowledge of various industry-specific regulations is fuelling professional services growth as industries develop regulations on how to adopt AI. These include AI diagnostic rules for medical, algorithmic trading rules for finance and functional safety rules for AI-powered manufacturing robots. Healthcare, life sciences and financial companies in the BFSI industry have to follow strict guidelines and specific operational requirements. So, they need to work with those who understand the principles of adversarial defense and industry regulations such as HIPAA and PCI DSS. To enhance value proposition, security vendors and services providers may consider customizing AI GRC Tools per vertical needs, and creating playbooks for automated enforcement of security policies.

Trends in the Global Security for AI Market

The Rise of AI Security Platform Engineering

Platform engineering is increasingly being embraced in enterprise as an alternative to legacy, silo-based security operations. Organizations are developing AI Security Platforms that provide self-service and guardrailed security tests to data scientists and software developers, rather than security, data science and operations being managed by different teams with separate and competing controls. These make it easy to automate model privacy, input sanitization and run-time threat detection. In response, security for AI vendors are offering platform architecture support, MLOps security automation, and playbook development for AI related security incidents.

Red Teaming for AI as a Service

Testing the security of AI models for adversarial threats is also a growing area in AI security as organisations need to demonstrate the resilience of their models to regulators and stakeholders. Companies are now looking for security approaches that not only align to policy but also mimic the capabilities of a determined hacker. This has brought about the need for automated AI Red Teaming platforms and services. Security for AI vendors help companies to test models for prompt injection, jailbreaks, training data extraction and decision boundary evasion to identify key vulnerability risks before they are exploited in the real world.

Research Scope and Analysis

By Offering Analysis

The Global Security for AI market is projected to be led by solutions as companies focus on implementing integrated platforms that protect AI models, data, and decision-making systems. Companies are embracing solutions such as AI threat monitoring, model security, and AI governance to address threats such as adversarial attacks and data poisoning. These solutions offer monitoring, response, and compliance capabilities, essential in regulated sectors. Solutions are more scalable, repeatable and deliver quicker return-on-investment (ROI) compared to services, becoming the preferred option for enterprise-wide adoption of AI. With rapid adoption of AI in industries, the need for comprehensive security solutions is growing faster than services, cementing their market leadership.

By Deployment Mode Analysis

Cloud-based deployment is poised to dominate this segment due to its scalability, agility and capacity to manage ever-changing AI workloads. As companies increasingly host AI models in the cloud, they need flexible security solutions. Cloud-based AI security solutions offer real-time monitoring, automatic upgrades, and integration with AI development workflows, making them appealing. Moreover, the growing trend towards multi-cloud and hybrid environments has reinforced the need for centralized, cloud-based security management. Affordability and simplicity of deployment also play a role, especially for small and medium-sized enterprises (SMEs) and rapidly growing companies. With AI innovation happening in the cloud, cloud security solutions are still the primary deployment method, allowing enterprises to protect their distributed AI assets.

By Organization Size Analysis

Large enterprises is poised to be dominate this segment given their widespread use of AI, larger spending on cybersecurity, and sophisticated IT ecosystems. These companies use AI in their core processes, making them attractive targets for advanced cyber-attacks, thus requiring advanced AI security measures. They also have strict governance, risk, and compliance (GRC) requirements, leading to advanced GRC solutions. Large enterprises typically invest in enterprise-grade, comprehensive platforms with sophisticated analytics and automation features. However, SMEs can be more constrained in terms of budget and expertise, hindering uptake. Therefore, large enterprises are still at the forefront of adopting holistic AI security frameworks, and remain the key market segment.

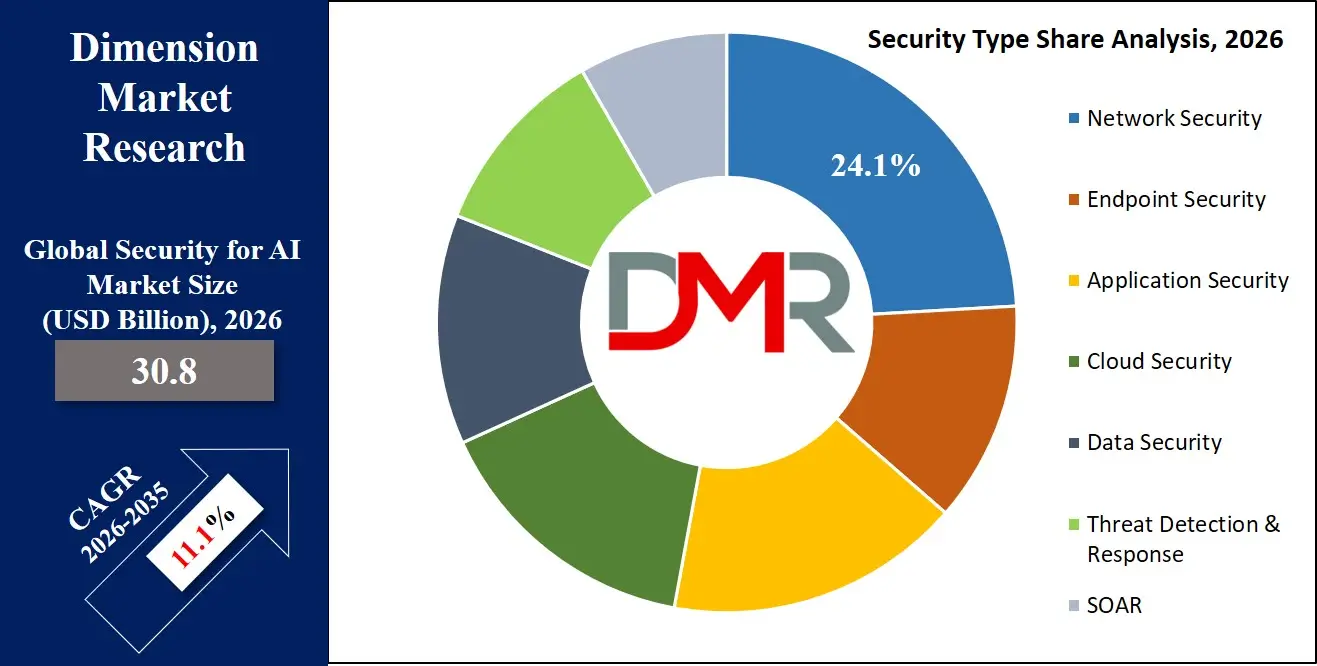

By Security Type Analysis

Network security is expected to dominate this segment because it provides the underlying security for AI systems and infrastructure. AI systems and applications heavily depend on connected networks for data exchange, training models, and real-time decision-making, making them susceptible to cyber attacks, such as data interception and denial-of-service.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Companies focus on network perimeter, traffic, and communication channel security to maintain the integrity and availability of AI systems. AI-based network security solutions provide real-time detection and response capabilities. With the broadening of AI ecosystems into cloud and edge computing, strong network security is critical, affirming its position as the most prominent security layer in the Global Security for AI market.

By Technology Analysis

Machine learning is anticipated to dominate technology segment as it allows systems to recognize abnormalities, threats, and take real-time action based on massive amounts of data. Machine learning models are employed for behavior analysis, fraud prevention and predictive threat intelligence, and are essential components of a cybersecurity strategy. Machine learning is scalable and flexible, adapting to the changing threat environment better than other technologies. It learns and enhances detection accuracy over time, offering a key edge over traditional rule-based approaches. With the growing use of self-organizing and cognitive security systems, machine learning technology continues to dominate AI security.

By Application Analysis

Threat detection and prevention are expected to dominate the technology segment as enterprises focus on proactive security against AI-based cyber threats. As cyber threats, including adversarial inputs and model poisoning, evolve in complexity, businesses need powerful systems to detect threats in real time. AI-based detection systems monitor user behavior, network traffic, and data irregularities to detect potential threats. Prevention systems also bolster defense with automated response and mitigation. This is a vital application across sectors, and the most commonly employed use case. The need for advanced threat prevention and detection systems will continue to grow as cybersecurity threats and AI technologies evolve.

By End-User Analysis

The BFSI sector is poised to lead this segment because of its extensive use of AI for key operations like fraud management, risk management and customer analytics. BFSI companies manage large volumes of data, making them an attractive target for cyber criminals and driving the need for enhanced AI security. The need for compliance with regulatory standards also drives the use of governance and risk management solutions. BFSI companies heavily invest in securing AI models and data flows for operational resilience and customer confidence. Moreover, the sector's pioneering use of AI technologies speeds up the requirement for AI security. Thus, BFSI continues to be the top end-user in the Global Security for AI market.

The Global Security for AI Market Report is segmented on the basis of the following:

By Offering

- Solutions

- AI Threat Detection & Prevention Platforms

- AI Model Security (Adversarial Defense, Model Integrity)

- Data Security & Privacy Protection

- Identity & Access Management (IAM)

- Cloud & Network Security Solutions

- Security Analytics & Monitoring Platforms

- AI Governance, Risk & Compliance (AI GRC) Tools

- Services

- Consulting Services

- Integration & Deployment Services

- Support & Maintenance

- Managed Security Services (MSS)

By Deployment Mode

- On-Premises

- Cloud-Based

- Hybrid

By Organization Size

By Security Type

- Network Security

- Endpoint Security

- Application Security

- Cloud Security

- Data Security

- Threat Detection & Response

- SOAR

By Technology

- Machine Learning

- Natural Language Processing

- Computer Vision

- Context-Aware Computing

- Behavioral Analytics

By Application

- Identity & Access Management

- Fraud Detection & Prevention

- Intrusion Detection & Prevention

- Data Loss Prevention

- Risk & Compliance Management

- Security Analytics

- AI Model Security

- Other Application

By End-User

- BFSI

- Government & Defense

- IT & Telecommunications

- Healthcare

- Retail & E-commerce

- Manufacturing

- Automotive & Transportation

- Energy & Utilities

- Other End-User

Regional Analysis

Leading Region by Market Share

North America is poised to dominate the global security for AI market as it is projected to hold 37.4% of the market share by the end of 2026. North America, led by the United States, has the largest share in the security for AI market because of the unrivalled density of hyperscale AI cloud computing platforms and the ambitious AI deployment plans of the Fortune 500 enterprises. It has a well-established network of global systems integrators, niche AI security startups and talent in adversarial machine learning and AI security engineering. Corporate investment in generative AI, autonomous systems, and the overall death of rule-based automation drives the need for AI Threat Detection & Prevention Platforms, AI Model Security, and continuous security monitoring. Furthermore, a positive venture capital environment continues to fund emerging, AI-specfic companies that require professional services to enable rapid development and security assurance for their new model structures.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Fastest-Growing Regional Market

Asia-Pacific is expected to be the most rapidly expanding security for AI market, due to the government-run large-scale AI adoption programs in India, China, Japan and Southeast Asia. The rapid development of the economy, the growing tech-savvy middle-income group and the thriving digital economy are driving large conglomerates and government agencies to quickly protect their AI investments against cybercriminals and advanced persistent threats. Risk & Compliance Management and Consulting Services are highly sought after by large enterprises to help them develop national and corporate AI security strategies. The region also lacks skilled AI security professionals and it is essential to engage with Managed Security Services (MSS) to monitor AI models, threat monitoring and respond to incidents to fill the skills gap and ensure quicker, safer deployment of AI projects.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The global security landscape for AI has become more dynamic with a rich diversity of multinational cybersecurity giants acquring AI capabilities, the professional security subsidiaries of the major hyperscalers, and AI-first speciality security vendors. The success factors will be the deep partnerships with foundational model providers and MLOps platforms as they will enable the required "embedded security" channels and access to emerging models that need security. The movement towards market consolidation is rapidly progressing with traditional network security companies acquiring AI model security and Security Analytics & Monitoring Platform specialized boutiques to stay afloat. Custom intellectual property capabilities such as automated red-teaming libraries, model-neutral threat detection, model-specific AI Governance Risk & Compliance (GRC) reporting accelerators are more critical in the ability to differentiate rather than just connect to generic SIEM or SOAR solutions.

Some of the prominent players in the Global Security for AI Market are:

- Microsoft Corporation

- CrowdStrike Holdings, Inc.

- Palo Alto Networks, Inc.

- Check Point Software Technologies Ltd.

- Fortinet, Inc.

- Cloudflare, Inc.

- Netskope, Inc.

- Cato Networks

- Darktrace plc

- Cyera Ltd.

- Zscaler, Inc.

- SentinelOne, Inc.

- Snyk Ltd.

- Wiz, Inc.

- Vectra AI, Inc.

- Prompt Security

- Remedio

- Abnormal Security

- IBM Corporation

- Cisco Systems, Inc.

- Other Key Players

Recent Developments

- January 2026: AWS announced it will undertake a substantial expansion of its AI security services, a professional services program to help Healthcare and Life Sciences and Manufacturing customers adopt AI Model Security for their sensitive domain-specific models with automated adversarial robustness testing and runtime integrity monitoring.

- November 2025: IBM Consulting expanded its partnership with Microsoft and launched a dedicated practice, Risk & Compliance Management and AI Model Security, to help BFSI clients securely transfer AI scoring workloads to Microsoft Azure, and help them comply with global financial model risk management requirements.

- October 2025: Accenture acquired a European AI security startup to enhance its AI GRC Tools and Cloud & Network Security Solutions for sovereign AI cloud data centers, to address the intricate data sovereignty and AI security needs of Government & Defense and public sector clients.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 30.8 Bn |

| Forecast Value (2035) |

USD 96.0 Bn |

| CAGR (2026–2035) |

13.5% |

| The US Market Size (2026) |

USD 9.7 Bn |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Offering (Solutions, and Services), By Deployment Mode (On-Premises, Cloud-Based, and Hybrid), By Organization Size (Large Enterprises, and SMEs), By Security Type (Network Security, Endpoint Security, Application Security, Cloud Security, Data Security, Threat Detection & Response, and SOAR), By Technology (Machine Learning, Natural Language Processing, Computer Vision, Context-Aware Computing, and Behavioral Analytics), By Application (Identity & Access Management, Fraud Detection & Prevention, Intrusion Detection & Prevention, Data Loss Prevention, Risk & Compliance Management, Security Analytics, AI Model Security, and Other Application), By End-User (BFSI, Government & Defense, IT & Telecommunications, Healthcare, Retail & E-commerce, Manufacturing, Automotive & Transportation, Energy & Utilities, and Other End-User) |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Global Security for AI Market?

▾ The Global Security for AI market is poised to be valued at USD 30.8 billion in 2026 and is projected to reach USD 96.0 billion by 2035, driven by the universal need for specialized skills and tools to protect AI models, data, and infrastructure from emerging and unique threats.

What is the CAGR of the Global Security for AI Market from 2026 to 2035?

▾ The market is expected to grow at a CAGR of 13.5% from 2026 to 2035, reflecting the accelerating reliance on AI for critical operations and the persistent shortage of internal expertise in adversarial machine learning and AI security operations.

What factors are driving the growth of the Global Security for AI Market?

▾ Key drivers include the global AI security skills gap, the imperative to comply with emerging AI governance regulations like the EU AI Act, the escalating complexity of securing multi-model AI supply chains, and the surge in demand for AI GRC Tools amid growing concerns over data sovereignty and model provenance.

Which region held the largest share of the Security for AI Market in 2026?

▾ North America is expected to dominate this market with 37.4% of market share in 2026, driven by a mature hyperscaler ecosystem and aggressive enterprise investment in securing mission-critical AI workloads and building Trustworthy AI frameworks.

Which region is expected to grow the fastest in the Security for AI Market?

▾ The Asia-Pacific region is expected to grow the fastest, fueled by rapid AI integration in digital economies in India, China, and Japan, where Consulting Services and Managed Security Services are critical for building secure national AI infrastructure.

What are the major trends in the Global Security for AI Market?

▾ Major trends include the integration of AI-powered security analytics into AI workflows, the rise of automated AI Red Teaming platforms as a service, the demand for vertical-specific AI GRC solutions, and the focus on Identity & Access Management for non-human AI identities in complex agentic environments.

Who are the key players in the Global Security for AI Market?

▾ Key players include cybersecurity leaders like CrowdStrike and Palo Alto Networks, AI-native security startups like HiddenLayer and Robust Intelligence, AI infrastructure leaders like NVIDIA, and the professional services divisions of hyperscalers like Microsoft and AWS, alongside global consultancies like Accenture and Deloitte.

How is the Global Security for AI Market segmented?

▾ The market is segmented by Offering, Deployment Mode, Organization Size, Security Type, Technology, Application, and End-User.