What is the Global Self-Adhesive Labels Market Size?

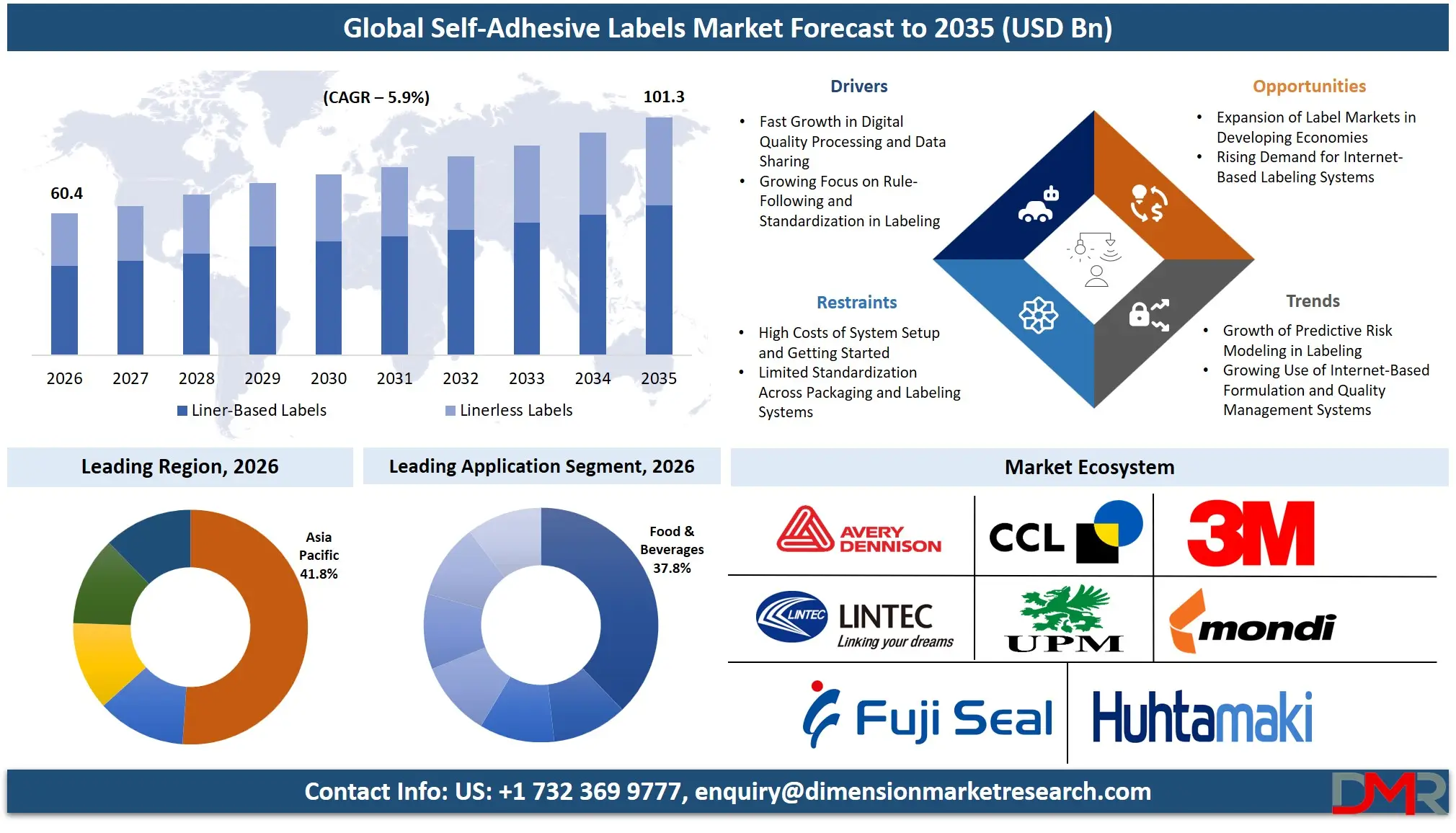

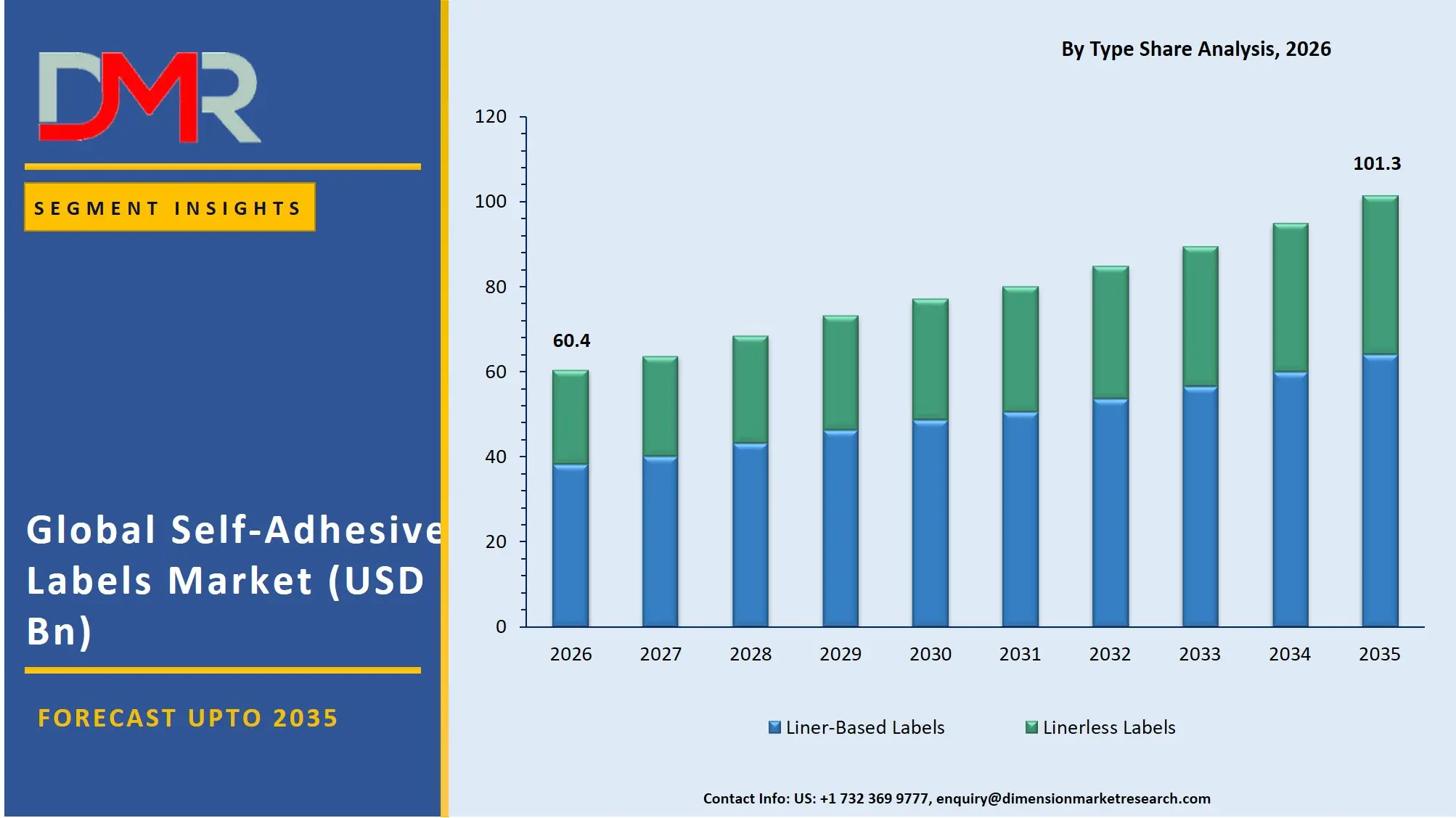

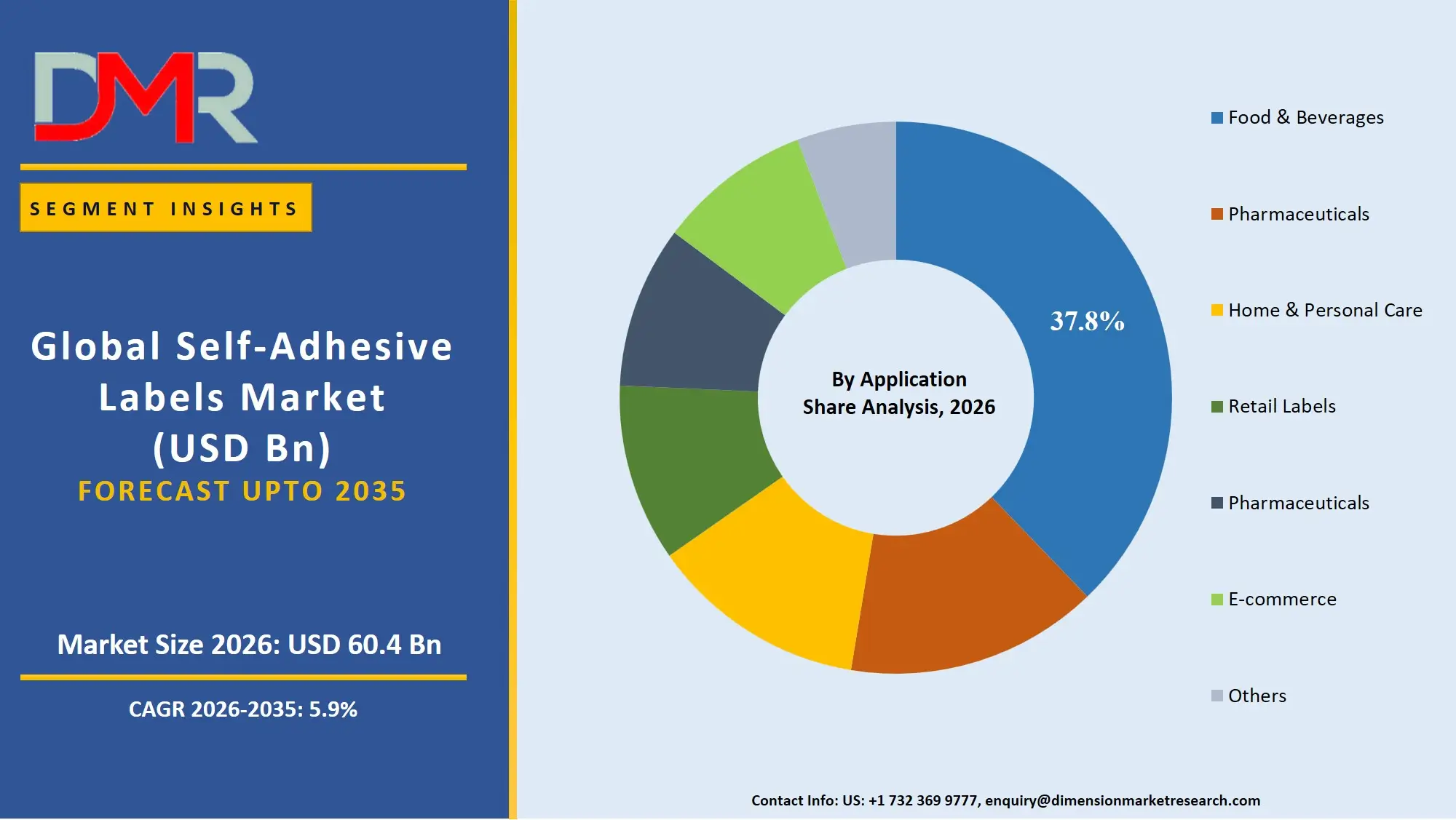

The Global Self-Adhesive Labels Market size is estimated at USD 60.4 billion in 2026 and is projected to reach USD 101.3 billion by 2035, exhibiting a CAGR of 5.9% during the forecast period, driven by the rising use of better data tools in smart packaging, automated quality checks in label converting, and connected supply chain management systems.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The Global Self-Adhesive Labels Market is expanding because of increasing use of smart software in detecting and analyzing consumer engagement patterns and label adhesive effectiveness; increasing approvals, which reduce the chance of rule-breaking during production and speed up the review process for new adhesive materials; and more funding in automating the use of label-related performance data.

Some other reasons for expansion in this market are new technologies in real-time quality assurance, material waste prediction through production markers, automated supply chain handling, and high-volume digital printing platforms, along with better data sharing rules. The digital shift in packaging and labeling companies has been helpful in speeding up product development and making label management easier. This includes shelf-life tracking research. In addition, government plans focusing on reducing packaging waste and the circular economy have ensured steady research in recyclable liners and eco-friendly adhesives.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

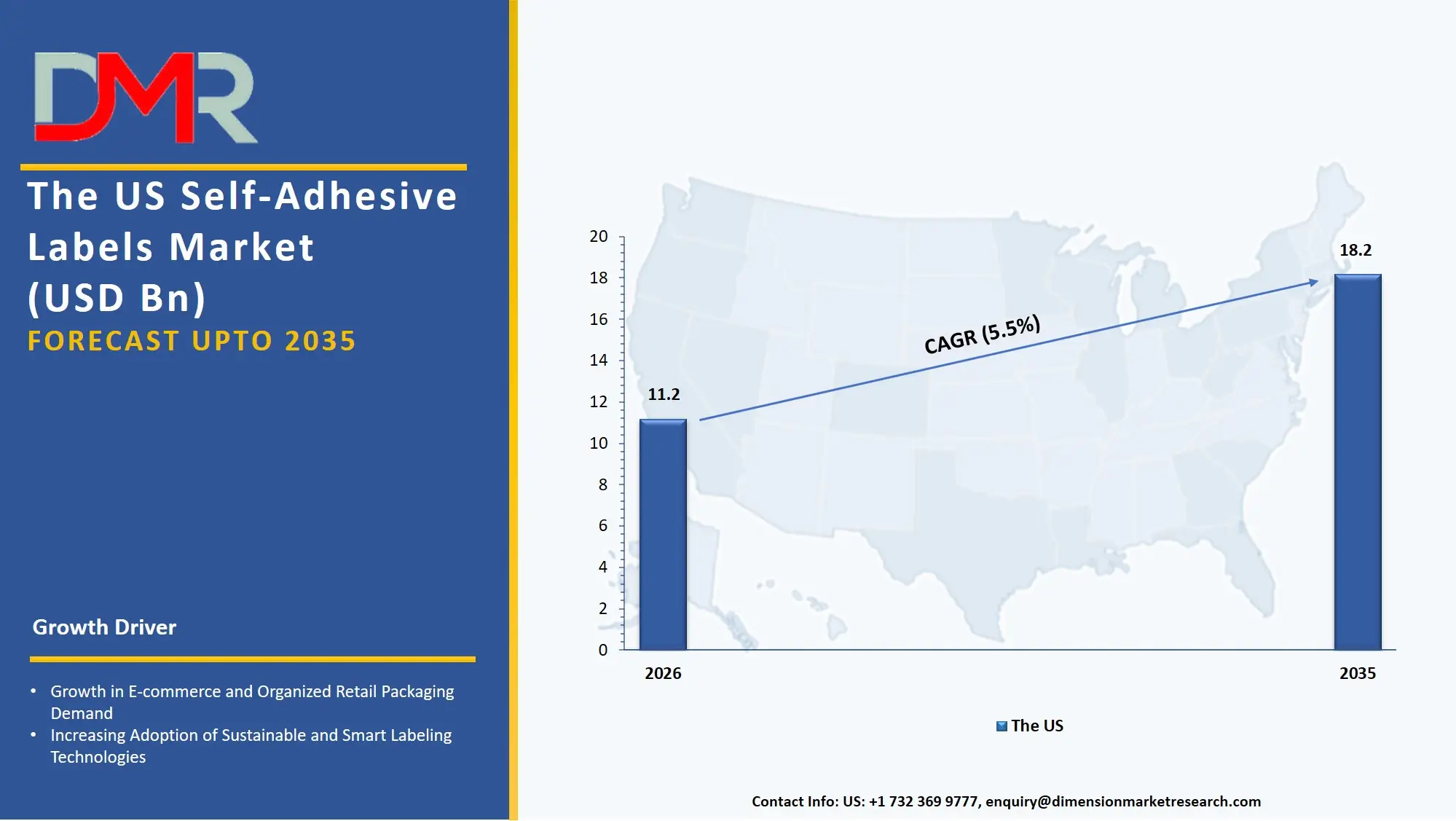

The US Self-Adhesive Labels Market

The US Self-Adhesive Labels Market is estimated to grow to USD 11.2 billion in 2026 with a compound annual growth rate of 5.5% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The US market is shaped by major federal and state-level programs promoting sustainable packaging, label affordability programs supported by the FDA, and EPA-led waste reduction initiatives. These programs encourage the use of smart quality testing, real-time customer data analysis, and predictive label formulation software. Automated compliance platforms are being rapidly adopted, and the US continues to invest in better data sharing between research labs, retail record systems, and reliable smart tools for self-adhesive labels. Service providers are also influenced by laws like the Truth in Labeling Act and national digital retail strategies to offer services that ensure data safety, rule-following, and smooth integration across product packaging and e-commerce portals.

Europe Self-Adhesive Labels Market

The Europe Self-Adhesive Labels Market is estimated to be valued at USD 16.6 billion in 2026, witnessing growth at a CAGR of 4.8%, during the forecast period.

Europe's self-adhesive labels market is well-established, shaped by EU-wide policies such as the EU Circular Economy Action Plan, the European Green Deal research program, and national policies to support digital packaging (e.g., Germany's national packaging reduction plans and France's anti-waste law 2030). Countries are also making label production processes more flexible to align producer and consumer demands and enable the sharing of recycling data across borders. The market grows due to new tools like software for real-time adhesive validation and scoring systems for linerless labels. Use is made easier by teamwork between public and private groups and shared data rules. Manufacturers have access to technologies such as cloud computing and secure record-keeping, and Europe is at the forefront of the digitisation of safe and efficient self-adhesive label operations.

Japan Self-Adhesive Labels Market

The Japan Self-Adhesive Labels Market is projected to be valued at USD 2.2 billion in 2026, progressing at a CAGR of 4.9%, during the period spanning from 2026 to 2035.

Japan's self-adhesive labels market is well developed, with high-quality digital printing platforms, connected inventory management systems, and a wide array of smart material waste analysis software tools. National focus on automation, efficiency and process honesty is delivered via predictive label performance models and smart production management. Growth opportunities are helped by government measures under the Society 5.0 program by Japan's Ministry of Economy, Trade and Industry (METI), and continued investment in digital smart packaging. Adhesive research, industrial performance analysis for product-specific label development and clinical packaging all need effective smart software to keep pace with data analysis. Higher costs for validating new label automation systems and connecting them with older production systems are significant, but there are opportunities for the export of Japanese self-adhesive label technologies to the Asian and Pacific markets.

Key Takeaways

- Market Size & Forecast: The Global Self-Adhesive Labels Market is estimated to be valued at USD 60.4 billion in 2026 and is expected to grow to USD 101.3 billion by 2035.

- Growth Rate & Outlook: The market is expected to witness growth at a compound annual growth rate of 5.9% in the forecast period.

- Primary Growth Drivers: The availability of new label formulation processing technologies that use smart software, the need to speed up sustainable packaging results and improve the success rates of adhesive-based labeling, and more government investment in national waste reduction infrastructure are key growth drivers.

- Key Market Trends: The predictive profiling of individual product labeling risks, real-time quality data handling, and the shift to internet-based label and product management platforms are key market trends.

- By Type: Liner-Based Labels are expected to take the largest revenue share in 2026 in the global self-adhesive labels market.

- By Technology: Flexography is expected to take the largest revenue share in 2026 in the self-adhesive labels market.

- By Application: Food & Beverages is estimated to take the lead in 2026 with the largest share in the self-adhesive labels market.

- Regional Leadership: Asia Pacific is estimated to take the lead in 2026 with 41.8% share in the self-adhesive labels market, owing to significant investment in automated labeling and smart packaging technologies.

What are Self-Adhesive Labels?

Self-adhesive labels are pressure-sensitive labels made from a combination of facestock, adhesive, and release liner, providing immediate bonding upon application without needing heat, water, or solvent activation. They include permanent, removable, and repositionable varieties. Self-adhesive labels use modern systems such as online quality checks, formulation management software, and remote tracking to manage, verify, and track labeling events and results. To improve supply chain outcomes, manage long-term product tracking and condition-specific labeling programs, and expand self-adhesive labels into personalized packaging coverage to support individual brand care and promote the development of sustainable labeling products.

Use Cases

- High-Speed Packaging for Daily Goods: Self-adhesive labels can provide high-bonding performance through advanced acrylic adhesives and liner-based facestocks to reduce label failure and support shelf-life tracking in days, compared to weeks that it would take with only traditional glue-applied labels.

- Long-Term Product Tracking: Long-term data on ongoing logistics issues, including temperature changes, humidity exposure, or transport damage, are studied to better understand label degradation and to help plan long-term durable labeling.

- Smart Inventory Management: Linerless label systems are handled through digital platforms and smart software in warehouse and retail settings to support real-time stock balance tracking.

- Community & Government Recycling Programs: Faster self-adhesive label development helps packaging innovation and development of recyclable labeling; government programs through smart monitoring of waste data advance national circular economy strategies and help the adoption of recycling standards.

How AI Is Transforming the Global Self-Adhesive Labels Market?

Artificial intelligence (AI) is being used more and more often in self-adhesive labels to improve adhesive formulation forecasting, find quality trends, and automatically spot unusual patterns in raw material sourcing data. It also allows faster quality checks because it can handle digital submissions on a large scale. Production records and electronic invoices are easier to study and help manufacturers find sourcing issues, reduce material waste, and improve the overall accuracy of label development. This has resulted in production being cost effective, quicker and more efficient than the old manual review method.

AI is also strengthening research and development by improving risk assessment and enabling more accurate label planning. It helps manufacturers predict how much label stock will be needed, find possible production delays, and monitor the performance of supplier networks more effectively. In addition, automation of routine checks and performance tracking is reducing operational workload, lowering administrative costs, and improving overall efficiency. This is leading to better financial results and more stable operations across the self-adhesive label production chain

Market Dynamics

Key Drivers of the Global Self-Adhesive Labels Market

Fast Growth in Digital Quality Processing and Data Sharing

The market is growing with the rise of digital tools to check and process label formulations, better management of production data, and a closer connection of electronic inventory records and labeling systems. Label management platforms provide real-time data that allows monitoring of the product workflow, helping to spot differences early and checking rules much faster. This has improved efficiency in operations and reduced human mistakes as well as administrative costs. At the same time, demand for more automated research and development is being helped by more activity in predictive analytics for the assessment of individual product labeling risks, as adhesive science further digitizes basic production tasks.

Growing Focus on Rule-Following and Standardization in Labeling

There is increasing emphasis on material openness, adhesive accuracy, and rule-following within the labeling system. Rules and frameworks such as the EU Circular Economy Action Plan and packaging modernization efforts in key markets are encouraging better data handling practices and more structured production processes. These advances are supporting the need for systems that can offer steady monitoring of adhesive formulations and standardized reporting. At the same time, active work to improve the sharing of recycling data and reduce mislabeling issues is strengthening the need for more effective management systems in both government and private label providers.

Restraints in the Global Self-Adhesive Labels Market

High Costs of System Setup and Getting Started

The rollout of self-adhesive label formulation platforms remains costly, requiring significant investment in system integration, testing, and alignment with packaging workflows. In addition, following data privacy rules such as GDPR and other regional laws adds to setup complexity. These factors increase upfront costs and can limit adoption, especially among smaller label converters and new companies entering the market.

Limited Standardization Across Packaging and Labeling Systems

There is still fragmentation in the market in terms of data formats and quality handling procedures. Although some areas have put in place organized label management systems, many manufacturers continue to work with both digital and manual systems. Lack of standard rules limits the ability to share data between packaging providers and label companies and results in inefficiencies in product development and system integration.

Growth Opportunities in the Global Self-Adhesive Labels Market

Expansion of Label Markets in Developing Economies

Newly developing economies such as Brazil, Indonesia, Nigeria, the UAE, and Vietnam are slowly building their packaging and labeling systems. These regions have long-term growth possibilities, with more people adopting branded consumer goods, and with more people becoming aware of smart packaging and slowly digitizing label care. These markets have few older production systems and can be used with new, technology-driven labeling systems that can grow over time.

Rising Demand for Internet-Based Labeling Systems

The move to remote supply chain monitoring, spread-out manufacturing networks, and real-time quality checks is leading to the adoption of internet-based labeling systems. These systems allow centralized data access, better coordination between packaging providers and manufacturers, and faster product management. Internet-based setup is increasingly becoming a trend among modern label providers as operational efficiency becomes one of the competitive factors.

Global Self-Adhesive Labels Market Trends

Growth of Predictive Risk Modeling in Labeling

Self-adhesive label platforms are gradually adding data-driven technology to find risk trends and improve accuracy in product development. These systems allow manufacturers to study their customers' ordering behavior better, simplify the management of their product lines, and improve their overall performance. This move is slowly turning the industry more proactive and data-driven in label management instead of being purely reactive in packaging management.

Growing Use of Internet-Based Formulation and Quality Management Systems

The use of internet-based systems is currently becoming a basic part of today's label operations. These systems allow real-time quality checks, centralized product administration, and better network coordination among packaging providers. Internet-based platforms are improving the efficiency and responsiveness of self-adhesive label manufacturers that operate in different regions by removing the need to rely on physical infrastructure and allowing operations to grow more easily.

Research Scope and Analysis

The global self-adhesive labels market involves pressure-sensitive labeling solutions used across packaging, logistics, and branding applications. The study covers segmentation by type, composition, nature, technology, application, and end-use industry, driven by rising packaged goods demand, e-commerce expansion, sustainability trends, and advancements in smart labeling technologies.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Type Analysis

The Liner-Based Labels segment is likely to continue dominating the market in 2026, with 68.4% of the global self-adhesive labels market share. This is due to its key role in covering food packaging, consumer goods tracking, and long-term industrial labeling, and its usefulness in various manufacturing settings where complete adhesive protection is needed. The Linerless Labels segment is also growing rapidly, with increasing demand for sustainable packaging needed in eco-conscious consumer groups that require waste reduction and material efficiency. They are also helped by the improvement of coating processes, real-time quality checks, and flexibility through modular platforms that combine several material types for better usefulness and customer convenience.

By Composition Analysis

The Facestock segment is likely to continue dominating the market in 2026, with 52.7% of the global self-adhesive labels market share. This is due to its key role in providing printable surfaces for branding, barcodes, and product information, and its availability in paper, film, and specialty materials for various end-uses. The Adhesive segment is also critical, with permanent, removable, and repositionable formulations driving performance. The Release Liner segment, while smaller, is essential for protecting adhesive integrity during storage and dispensing; linerless technology is emerging as a sustainable alternative, reducing waste and lowering shipping costs for high-volume applications.

By Nature Analysis

The Permanent segment is the largest nature type in 2026, accounting for 62.3% share, driven by long-term bonding requirements for industrial and consumer durables. Removable labels are also a major segment, supported by established manufacturing processes and broad retail familiarity. The fastest-growing area is Repositionable labels, where consumers and brands prefer adjustable, residue-free alternatives to traditional adhesives.

By Technology Analysis

The Flexography segment is expected to account for 44.2% share in 2026, due to higher print speeds, cost-effectiveness for long runs, and greater substrate versatility compared to other printing types. The segment is also driven by growing adoption of water-based inks and combined printing options to increase value for converters in industrial and retail settings. Digital Printing is the fastest-growing segment in the self-adhesive labels market, due to the fast uptake of fully connected variable data workflows and short-run infrastructure. Lithography is the second-largest segment, followed by Screen Printing.

By Application Analysis

The Food & Beverages segment is expected to dominate with around 32.1% market share in 2026, driven by greater consumer focus on ingredient transparency, faster product turnover, and broader retail access compared to other applications. Food & beverage labels support customized packaging plans because they can offer multiple levels of moisture resistance, adhesive strengths, and shelf-life indicators, delivering fast results while keeping data within supply chain systems. The Pharmaceuticals segment, while smaller, is seeing strong growth in regions with government-sponsored drug authentication programs and serialized labeling requirements.

By End-Use Industry Analysis

The FMCG segment is the largest end-use industry in 2026, accounting for 44.5% share, driven by high-volume production, rapid shelf restocking, and the need for brand consistency across thousands of SKUs. Logistics is the second-largest segment, using durable labels for asset tracking and shipment identification. The fastest-growing area is Healthcare, where pharmaceutical and medical device labeling requires high durability, tamper evidence, and regulatory compliance.

The Global Self-Adhesive Labels Market Report is segmented based on the following:

By Type

- Liner-Based Labels

- Linerless Labels

By Composition

- Facestock

- Adhesive

- Release Liner

By Nature

- Permanent

- Removable

- Repositionable

By Technology

- Flexography

- Digital Printing

- Lithography

- Screen Printing

- Gravure

- Letterpress

- Offset

By Application

- Food & Beverages

- Consumer Durables

- Pharmaceuticals

- Home & Personal Care

- Retail Labels

- E-commerce

- Others

By End-Use Industry

- FMCG

- Logistics

- Industrial

- Healthcare

- Others

Regional Analysis

Largest Region in the Self-Adhesive Labels Market

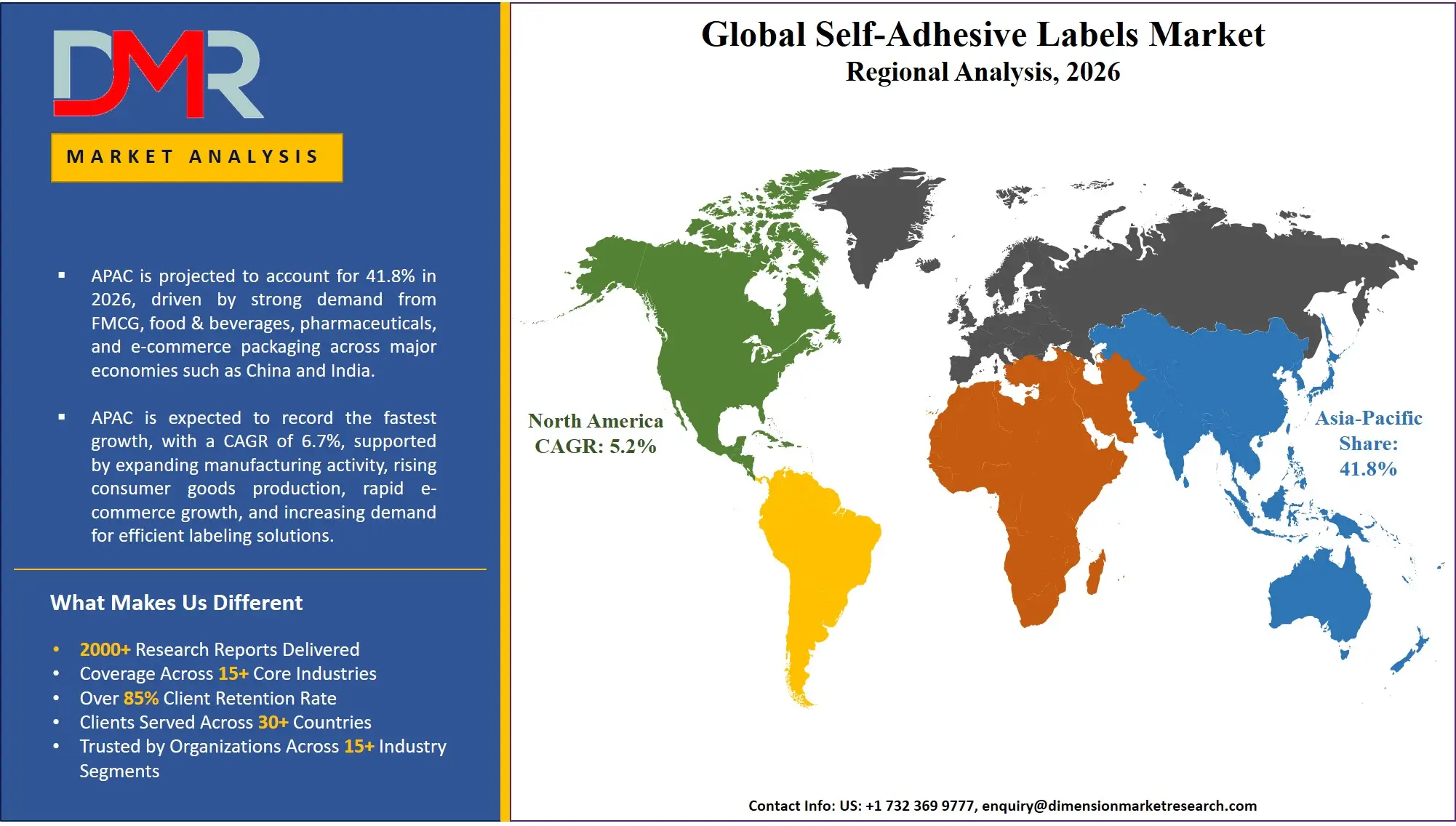

It is projected that the Asia-Pacific will take the lead in the global self-adhesive labels market (by value), covering a market share of about 41.8% in the year 2026. The region's dominance is driven by rapid expansion in FMCG and packaged goods demand, strong growth in e-commerce and logistics labeling, increasing pharmaceutical production and exports, and ongoing industrialization and urbanization across China, India, and Southeast Asia. The widespread adoption of advanced digital printing and automation for liner-based and linerless labels, along with cost-effective manufacturing capabilities, further strengthens Asia-Pacific's leading position. Additionally, ongoing investments in smart quality monitoring and system interoperability further reinforce the region's technology leadership. The presence of major label converters and raw material suppliers, coupled with favorable government policies supporting manufacturing exports, solidifies the region's dominance.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Fastest-Growing Region in the Self-Adhesive Labels Market

Asia-Pacific is also the fastest-growing region, supported by strong digital packaging infrastructure goals in China, India, Japan, and ASEAN nations, increasing sustainable packaging awareness efforts, rising investments in local label manufacturing capabilities, and growing adoption of automated quality analysis systems. The region benefits from well-established digital payment systems for packaged goods, increasing business activity, and alignment with national circular economy roadmaps. Countries across the region are actively setting up self-adhesive label platforms to improve formulation efficiency and strengthen packaging infrastructure. Growing focus on label research and structured data development further speeds up market expansion.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The self-adhesive labels market is highly competitive, with new ideas and strategic partnerships shaping the competitive environment. To gain an advantage, companies and manufacturers are focused on developing better digital platforms (such as smart adhesive formulation engines, automated coating systems, and mobile apps for label inventory management), smart data analysis, and digital platform-based quality monitoring. There are high barriers to entering the market due to the large amount of money needed for material approval, specialized adhesive knowledge, and the need for mature software systems and rule-following.

Strategic approaches to increase market presence include partnerships with packaging research groups and retail chains, mergers between label converters and technology providers, and long-term support contracts with customers and logistics institutions. Additionally, research and development in data-sharing rules and flexible software designs are important for staying competitive and meeting the changing needs of the self-adhesive label community.

Some of the prominent players in the Global Self-Adhesive Labels Market are:

- Avery Dennison Corporation

- CCL Industries Inc.

- 3M Company

- UPM-Kymmene Corporation

- LINTEC Corporation

- Mondi plc

- Coveris Management GmbH

- Multi-Color Corporation

- Fuji Seal International, Inc.

- HERMA GmbH

- Huhtamaki Oyj

- SATO Holdings Corporation

- All4Labels Group GmbH

- Optimum Group B.V.

- Skanem AS

- Schreiner Group GmbH & Co. KG

- Torraspapel Adestor S.A.

- H.B. Fuller Company

- Constantia Flexibles Group GmbH

- Asteria Group

- Other Key Players

Recent Developments

- March 2026: CCL Industries Inc. signed a binding agreement to acquire Sleever International, expanding its shrink sleeve labeling portfolio and strengthening its global presence in sustainable packaging solutions.

- February 2026: Avery Dennison Corporation introduced the AD IdentiFresh RFID inlay series, enabling enhanced inventory tracking, improved freshness monitoring, and reduced food waste across retail supply chains through advanced smart labeling technology solutions.

- March 2025: LINTEC Corporation launched a removable hot-melt adhesive labelstock (“CHILL AT / Re Chill”) designed for low-temperature applications, enabling easy removal, recyclability, and reduced environmental impact in food and industrial packaging.

- March 2025: UPM-Kymmene Corporation showcased its new Carbon Action label portfolio at Labelexpo Mexico 2025, highlighting sustainable label materials designed to reduce carbon footprint and support circular packaging solutions across global packaging applications.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 60.4 Bn |

| Forecast Value (2035) |

USD 101.3 Bn |

| CAGR (2026–2035) |

5.9% |

| The US Market Size (2026) |

USD 11.2 Bn |

| Historical Period |

2021 – 2025 |

| Forecast Period |

2027 – 2035 |

| Base Year |

2025 |

| Estimated Year |

2026 |

| Segments Covered |

By Type, By Composition, By Nature, By Technology, By Application, By End-Use Industry |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Global Self-Adhesive Labels Market?

▾ The Global Self-Adhesive Labels Market size is estimated to have a value of USD 60.4 billion in 2026 and is expected to reach USD 101.3 billion by the end of 2035.

Which region held the largest share of the Global Self-Adhesive Labels Market in 2026?

▾ Asia Pacific is expected to account for the largest market share in 2026, with a share of about 41.8%.

Which region is expected to grow the fastest in the Global Self-Adhesive Labels Market?

▾ Asia Pacific is the fastest-growing region in the market during the forecast period.

Who are the key players in the Global Self-Adhesive Labels Market?

▾ Some of the major key players in the Global Self-Adhesive Labels Market are Avery Dennison Corporation, CCL Industries Inc., 3M Company, UPM Raflatac, Mondi Group, H.B. Fuller Company, and many others.

What is the CAGR of the Global Self-Adhesive Labels Market from 2026 to 2035?

▾ The market is growing at a CAGR of 5.9% over the forecasted period.

What factors are driving the growth of the Global Self-Adhesive Labels Market?

▾ The market is driven by advances in smart software-based adhesive formulation processing, regulatory pressure to speed up sustainable packaging results and reduce material waste, and increased government investment in national circular economy infrastructure.

What are the major trends in the Global Self-Adhesive Labels Market?

▾ The key market trends include the adoption of predictive label performance tracking and real-time quality data analysis, along with a growing shift toward internet-based label management platforms and data-enabled packaging management systems.

How is the Global Self-Adhesive Labels Market segmented?

▾ The market is segmented by type, composition, nature, technology, application, and end-use industry.