What is the Semiconductor Device for Processing Application Market Size?

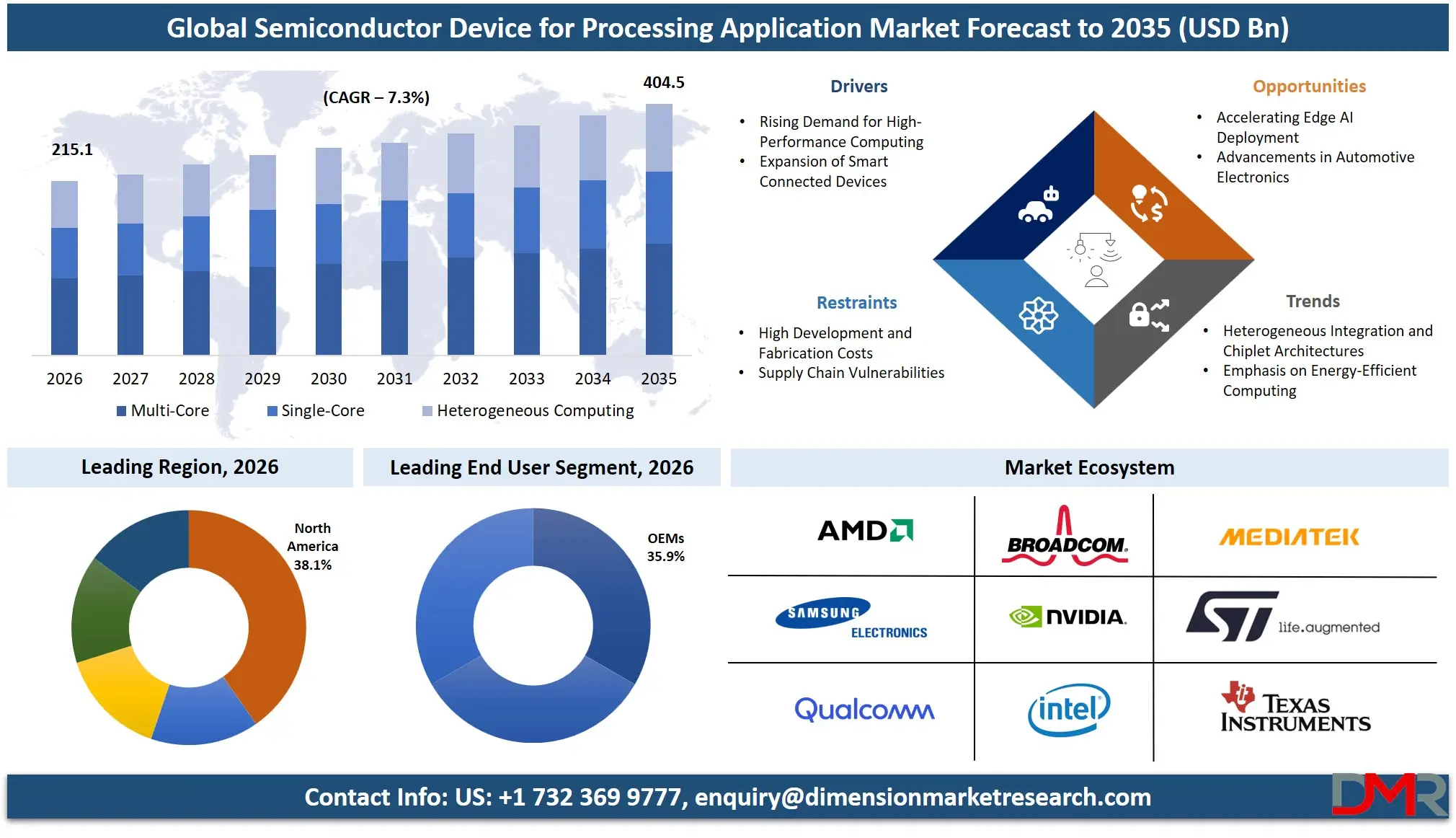

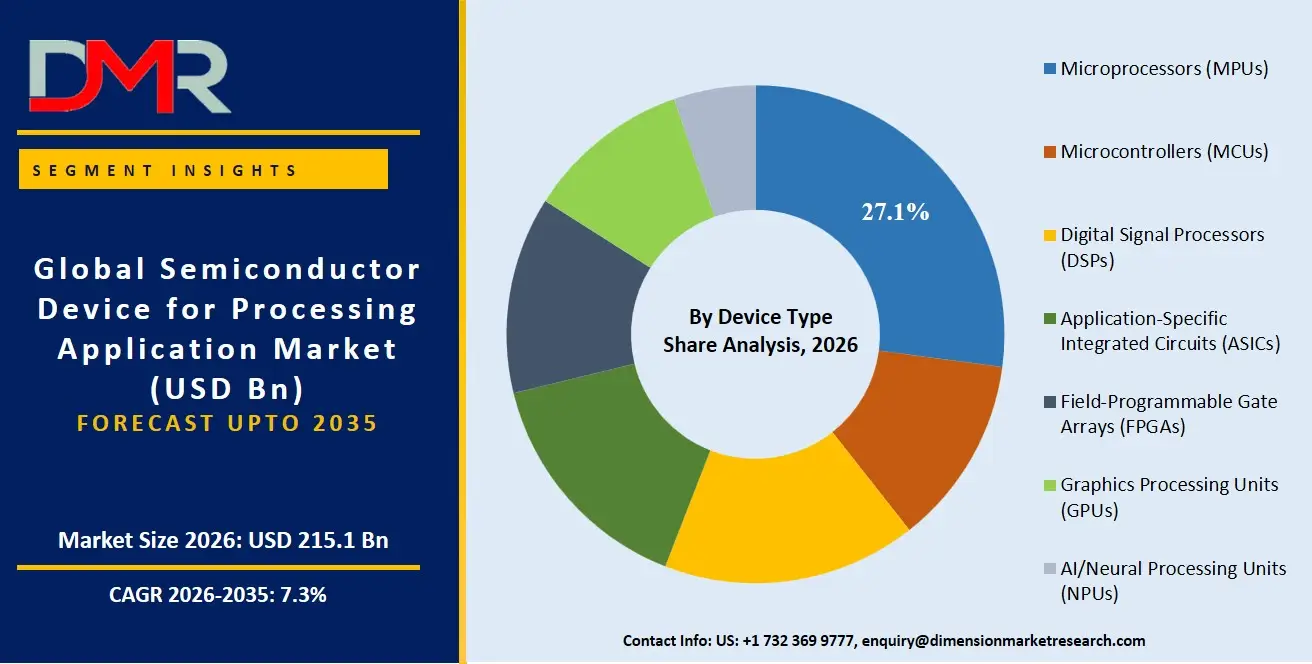

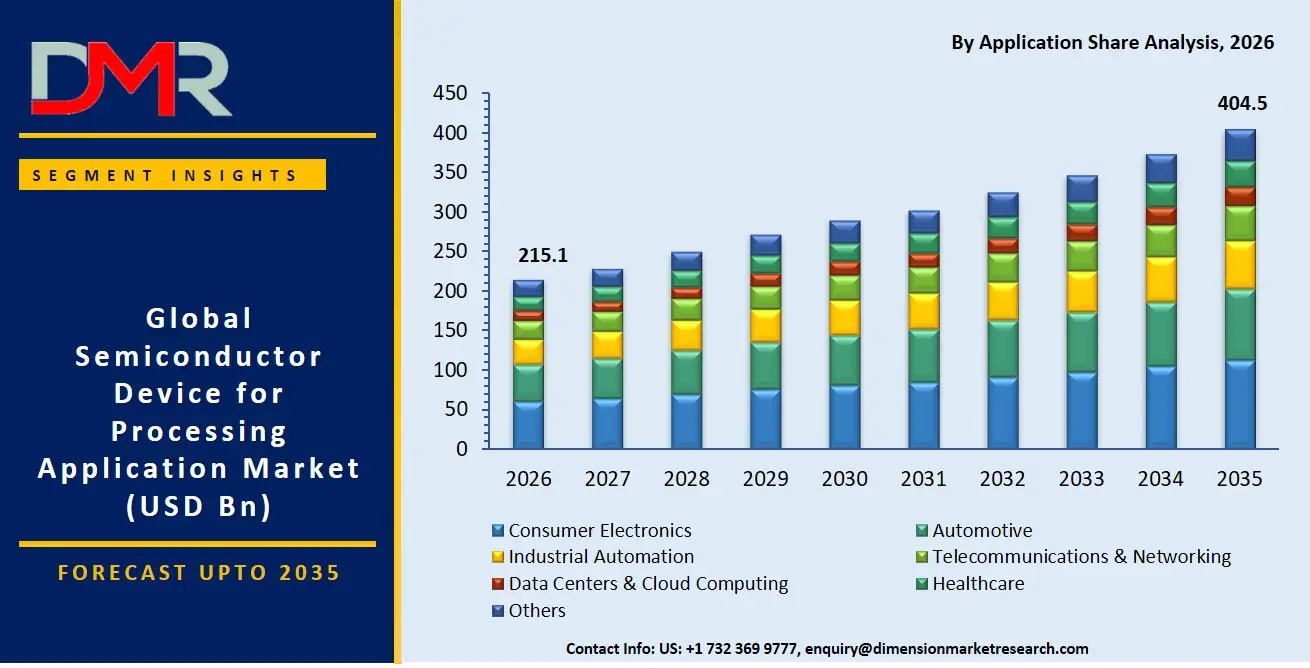

The Global Semiconductor Device for Processing Application Market is expected to reach a value of USD 215.1 billion in 2026, and it is further anticipated to reach USD 404.5 billion by 2035, growing at a CAGR of 7.3% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The semiconductor processing device market is experiencing robust growth as the digital backbone of the global economy expands, driven by the proliferation of AI, cloud computing, and autonomous systems. This market encompasses the design, manufacturing, and integration of core computational silicon, including Microprocessors (MPUs), Microcontrollers (MCUs), Graphics Processing Units (GPUs), and specialized AI accelerators that power everything from hyperscale data centers to milliwatt-constrained edge sensors. The insatiable demand for heterogeneous computing architectures, which combine CPUs, GPUs, and NPUs on a single substrate to handle massive parallel processing workloads, is fundamentally reshaping the supplier landscape. Data centers, automotive OEMs, and consumer electronics manufacturers remain the most prolific consumers, with high-performance, energy-efficient, and domain-specific architectures becoming the primary competitive battlegrounds.

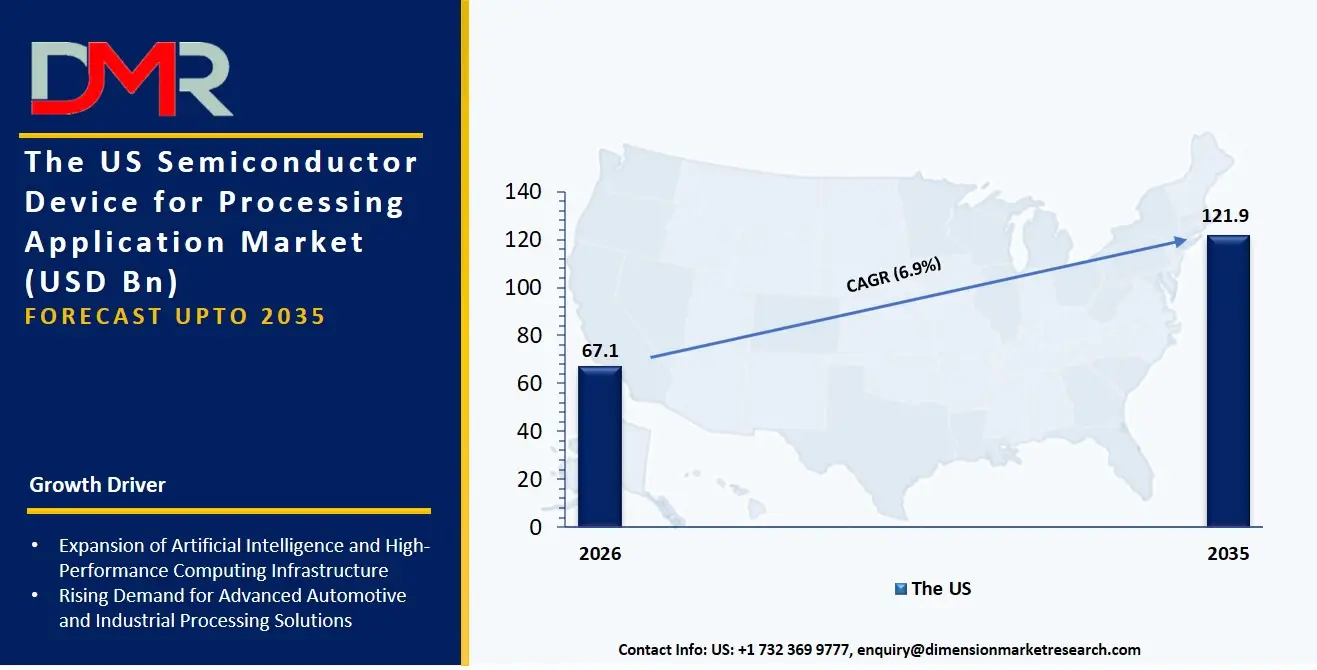

The US Semiconductor Device for Processing Application Market

The US Semiconductor Device for Processing Application Market is projected to reach USD 67.1 billion in 2026 at a compound annual growth rate of 6.9% over its forecast period, culminating in a value of USD 121.9 billion by 2035.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The US remains the epicenter of advanced processing design and innovation, driven by a fabless powerhouse ecosystem and aggressive onshoring initiatives for leading-edge manufacturing. The market is typified by soaring demand for Data Center AI Accelerators, where hyperscale cloud vendors are deploying custom ASICs and high-end GPUs to train large language models with trillions of parameters. Furthermore, the imposition of technology sovereignty measures and export controls is catalyzing significant investments in domestic foundries, with enterprises prioritizing the adoption of RISC-V and proprietary Arm-based Server Processors to secure their long-term supply chains.

The Europe Semiconductor Device for Processing Application Market

The Europe Semiconductor Device for Processing Application Market is estimated at USD 52.4 billion in 2026 and is forecast to expand at a CAGR of 8.3%, reaching USD 107.7 billion by 2035. Growth is propelled by the region's leadership in automotive electronics, where stringent functional safety standards drive demand for advanced 32-bit MCUs and high-compute domain controllers. Accelerating industrial automation adoption, particularly within Germany's smart factory ecosystems, necessitates robust Embedded Processors and real-time Heterogeneous Computing architectures. Furthermore, ambitious government semiconductor initiatives, notably the EU Chips Act, are catalyzing a pivot toward advanced-node ASIC manufacturing and FD-SOI technologies. Rising R&D spending by European OEMs and IDMs, coupled with growing regional manufacturing capacity aimed at supply chain sovereignty, collectively reinforce the continent's strategic position in energy-efficient processing for green mobility and intelligent manufacturing.

The Japan Semiconductor Device for Processing Application Market

The Japan Semiconductor Device for Processing Application Market is projected to be valued at USD 18.7 billion in 2026. It is further expected to witness robust growth, holding USD 32.3 billion in 2035 at a CAGR of 6.3%. The Japanese market is characterized by a deep competitive moat in precision manufacturing and materials, now augmented by a corporate drive to revive domestic logic and foundry capabilities. Discrete GPUs for high-performance gaming and workstation applications, alongside specialized MCUs for factory automation, constitute a large share of the ecosystem. Furthermore, there is a strategic pivot toward developing next-generation AI accelerators and High-End FPGAs for telecommunications infrastructure, bridging the gap between Japan's traditional strength in device physics and the emerging demands of 5G Advanced and autonomous systems.

Key Takeaways

- Market Size & Forecast: The Global Semiconductor Device for Processing Application market is projected to reach USD 215.1 billion in 2026, expanding to USD 404.5 billion by 2035, fueled by the dual engines of generative AI deployment and the architectural shift from scalar to spatial computing.

- Growth Rate & Outlook: Global market growth is expected at a CAGR of 7.3%, driven by the extinction of Dennard scaling and the resulting shift from monolithic single-core designs to complex, domain-specific multi-die packaging and chiplets.

- Primary Growth Drivers: Key forces include the exponential growth of parametric AI models requiring massive clusters of GPUs and NPUs, the automotive industry's transition to software-defined vehicles reliant on high-compute domain controllers, and the pervasive IoT demanding ultra-low-power 32-bit MCUs with integrated security.

- Key Market Trends: Major trends include the rapid adoption of chiplet-based architectures for Heterogeneous Computing, the surge in custom ASICs for hyper-scale data center operators bypassing traditional merchant silicon, and the battle between x86, Arm, and RISC-V instruction set architectures (ISAs) across all device types.

- By Device Type Analysis: AI/Neural Processing Units (NPUs) represent the explosive growth vector, as distinct architectural paradigms like systolic arrays and near-memory compute become mandatory for Edge AI Accelerators and Data Center AI Accelerators, decoupling AI inference and training from legacy GPU shader cores.

- By Application Analysis: Data Centers & Cloud Computing and Automotive are the most lucrative verticals. The former demands uncompromised performance-per-watt for general-purpose CPUs and custom ASICs, while the latter fuses functional safety with high-bandwidth sensor processing, driving demand for automotive-qualified MPUs and MCUs.

- Regional Leadership: North America is poised to dominate this market with 38.1% of the global market share in 2026, anchored by its commanding leadership in fabless semiconductor design, electronic design automation (EDA) software, and the capital-intensive architecture licensing that defines the value chain.

What is the Semiconductor Device for Processing Application?

Semiconductor devices for processing applications are the specialized silicon engines the "brains" that execute logical and mathematical operations, distinguishing them from memory or power management chips. These products, unlike simple passive components, are defined by their architectural blueprint and instruction set architecture (ISA). This market encompasses the gamut from General-Purpose CPUs that orchestrate operating systems in servers and personal computers, to tightly integrated 32-bit MCUs that manage real-time control loops in automotive braking systems. With the collapse of Moore's Law's simple cadence, the market has pivoted to domain-specific acceleration, where Data Center AI Accelerators, custom Standard-Cell ASICs, and adaptive High-End FPGAs provide orders-of-magnitude efficiency gains for specific workloads, translating complex software into tangible hardware performance.

Use Cases

- Real-Time Ray Tracing in Consumer Electronics: Gaming console and discrete GPU manufacturers utilize advanced Graphics Processing Units to perform real-time ray tracing and AI-enhanced frame generation, turning cinematic visual rendering into an interactive consumer experience.

- Level-3 Autonomous Driving in Automotive: Automotive OEMs employ high-performance Server Processor-class MPUs with integrated NPUs on a single chip to perform real-time sensor fusion, object classification, and path planning inside a strict, safety-certified power envelope.

- Smart Manufacturing Predictive Maintenance: Industrial automation providers use deterministic 16-bit and 32-bit MCUs alongside low-power AI Edge AI Accelerators to analyze vibration and thermal data directly at the machine tool, predicting bearing failures without cloud latency.

- Massive MIMO Beamforming in Telecommunications: Telecommunication infrastructure vendors deploy high-speed DSPs and High-End FPGAs in 5G base stations to execute complex beamforming algorithms in the sub-millisecond time frames required by 3GPP standards.

How AI is Transforming the Semiconductor Device for Processing Application Market?

AI is fundamentally re-architecting the semiconductor processing landscape by making data the first-order constraint and forcing a departure from general-purpose computing. In the Data Center AI Accelerators segment, massive systolic array architectures, which excel at dense matrix multiplication, are replacing traditional superscalar CPU approaches, creating a new merchant silicon royalty hierarchy distinct from the PC era. Meanwhile, at the edge, NPUs designed as Edge AI Accelerators are being fused onto the die of standard MCUs, enabling always-on keyword spotting and gesture recognition in battery-powered devices with sub-milliwatt energy budgets.

The design methodology of silicon itself is also being transformed by AI. In the realm of Full-Custom ASICs and Standard-Cell ASICs, reinforcement learning agents are being deployed by foundries and IDMs to optimize floor-planning, reducing physical design timelines from months to weeks. Moreover, generative AI models are simulating complex Heterogeneous Computing traffic patterns, allowing architects to calibrate NoC (Network-on-Chip) fabrics and memory controller bandwidth precisely before tape-out, mitigating expensive re-spins.

Market Dynamics

Key Drivers in the Global Semiconductor Device for Processing Application Market

Rising Demand for High-Performance Computing

The proliferation of cloud computing, artificial intelligence, big-data analytics, and advanced simulation workloads is fueling the need for increasingly powerful processing semiconductors. Enterprises and service providers are investing heavily in processors capable of delivering superior computational density and energy efficiency. This demand extends from hyperscale data centers to edge devices, encouraging continuous innovation in microprocessors, GPUs, and AI accelerators. As digital transformation accelerates across industries, processing devices with enhanced parallelism, faster interconnects, and optimized architectures remain essential, making high-performance computing one of the strongest growth catalysts for the global market.

Expansion of Smart Connected Devices

The rapid adoption of smartphones, IoT equipment, connected vehicles, and industrial automation systems significantly increases the requirement for processing semiconductors. These devices depend on advanced chips to execute complex algorithms, manage connectivity, and support real-time decision-making. Manufacturers are therefore integrating more capable processors and accelerators into products across consumer and industrial domains. Growing consumer expectations for seamless digital experiences and the rising deployment of intelligent infrastructure worldwide further stimulate demand. The resulting increase in unit shipments and processing complexity continues to drive sustained expansion of the semiconductor device market for processing applications.

Restraints in the Global Semiconductor Device for Processing Application Market

High Development and Fabrication Costs

Designing state-of-the-art processing semiconductors requires substantial investments in research, electronic design automation tools, and advanced manufacturing facilities. Transitioning to smaller process nodes further escalates capital expenditures and technical complexity. These costs create significant barriers to entry and may constrain innovation among smaller firms. Additionally, lengthy development cycles and the risk of low manufacturing yields can affect profitability and delay product launches. Consequently, only a limited number of companies possess the resources needed to compete at the leading edge, restraining broader market participation and potentially slowing the pace of technological diversification.

Supply Chain Vulnerabilities

The semiconductor ecosystem relies on a highly globalized supply chain encompassing raw materials, fabrication equipment, packaging, and logistics. Disruptions arising from geopolitical tensions, natural disasters, or transportation bottlenecks can lead to shortages and production delays. Processing devices are particularly affected because many depend on specialized manufacturing capabilities concentrated in a few regions. Such vulnerabilities increase costs and create uncertainty for both suppliers and customers. Companies are therefore compelled to maintain larger inventories and diversify sourcing strategies, actions that may reduce operational efficiency and temporarily hinder market growth during periods of supply instability.

Growth Opportunities in the Global Semiconductor Device for Processing Application Market

Accelerating Edge AI Deployment

The migration of artificial intelligence capabilities from centralized data centers to edge devices presents substantial opportunities for processing semiconductor suppliers. Smart cameras, autonomous machines, and industrial sensors increasingly require local inference to reduce latency and enhance privacy. This trend creates demand for specialized AI accelerators and energy-efficient processors optimized for edge environments. Vendors that deliver compact, high-performance solutions stand to benefit from expanding deployments across healthcare, manufacturing, retail, and transportation. As organizations prioritize real-time analytics and autonomous operation, edge AI is expected to unlock significant new revenue streams throughout the processing semiconductor value chain.

Advancements in Automotive Electronics

Modern vehicles incorporate an expanding array of processing-intensive functions, including advanced driver-assistance systems, infotainment, connectivity, and electrified powertrains. These capabilities require powerful and reliable semiconductor devices capable of operating under demanding conditions. The transition toward software-defined and autonomous vehicles further increases processing requirements, creating opportunities for suppliers of high-performance CPUs, GPUs, and AI processors. Long product lifecycles and stringent quality standards also support stable demand and premium pricing. As automotive manufacturers continue to integrate digital technologies, this sector is poised to become an increasingly important avenue for market expansion.

Trends in the Global Semiconductor Device for Processing Application Market

Heterogeneous Integration and Chiplet Architectures

Manufacturers are increasingly combining multiple specialized processing elements within a single package to improve performance, flexibility, and yield. Chiplet-based designs enable the integration of CPUs, GPUs, memory, and accelerators using optimized process technologies, reducing development costs while enhancing scalability. This approach addresses the limitations of traditional monolithic scaling and allows faster introduction of innovative features. The growing adoption of advanced packaging techniques reflects a broader industry shift toward modular system design, making heterogeneous integration one of the most influential technological trends shaping the future of processing semiconductors.

Emphasis on Energy-Efficient Computing

Power efficiency has become a primary design objective as data centers, mobile devices, and edge systems seek to balance performance with sustainability. Semiconductor companies are introducing architectures that deliver greater computational output per watt through optimized instruction sets, power-management techniques, and specialized accelerators. Regulatory pressures and corporate sustainability goals further reinforce this focus. Energy-efficient processing not only reduces operating costs but also enables new applications in battery-powered and thermally constrained environments. Consequently, innovations that maximize efficiency while maintaining high performance are emerging as a defining trend across the global processing semiconductor market.

Research Scope and Analysis

The global semiconductor device for processing application market encompasses microprocessors, microcontrollers, DSPs, ASICs, FPGAs, GPUs, and NPUs, categorized by processing architecture into single-core, multi-core, and heterogeneous designs. Key applications include consumer electronics, automotive, industrial, telecom, data centers, and healthcare, serving OEMs, foundries and IDMs, enterprises, and research institutions worldwide.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Device Type Analysis

Microprocessors (MPUs) are poised to dominate this segment owing to their indispensable role in general-purpose computing, servers, and embedded systems. Their unmatched software compatibility, high processing performance, and continuous architectural advancements sustain widespread adoption across personal computing, enterprise infrastructure, and industrial applications. The rapid expansion of cloud services, artificial intelligence workloads, and edge computing further reinforces demand for high-performance MPUs. Moreover, leading semiconductor manufacturers consistently invest in process-node scaling and power-efficiency improvements, enhancing MPU capabilities and extending their market leadership. The broad application base and mature ecosystem surrounding microprocessors ensure that they remain the largest revenue-generating device category in processing applications worldwide.

By Processing Architecture Analysis

Multi-core architectures are anticipated to hold the leading position as they provide superior computational throughput, energy efficiency, and scalability compared with single-core designs. The growing complexity of software applications, alongside rising requirements for parallel processing in AI, analytics, and multimedia workloads, has accelerated their adoption across virtually all end-use sectors. Multi-core designs enable manufacturers to increase performance without proportionally raising clock speeds and power consumption, making them ideal for modern computing platforms. Their prevalence in smartphones, servers, automotive electronics, and industrial systems, combined with ongoing advancements in heterogeneous integration and interconnect technologies, firmly establishes multi-core architectures as the dominant processing paradigm.

By Application Analysis

Consumer electronics is expected to account for the largest share due to the enormous global volumes of smartphones, laptops, tablets, wearables, gaming devices, and smart home products.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

These devices require increasingly sophisticated processing capabilities to support advanced features, connectivity, and artificial intelligence functions. Frequent product refresh cycles and rising consumer expectations for performance continuously stimulate semiconductor demand. Additionally, the proliferation of IoT-enabled consumer products and high-resolution multimedia applications further expands processing requirements. The sheer scale of consumer electronics manufacturing, coupled with sustained innovation from device makers, ensures that this application segment remains the primary driver of semiconductor devices used for processing applications.

By End User Analysis

OEMs is projected to dominate because they integrate processing semiconductors directly into finished products spanning consumer, automotive, industrial, and communication markets. Their large production volumes and close collaboration with chip suppliers enable early adoption of cutting-edge technologies and customized solutions. OEMs drive demand by continuously introducing new features and performance enhancements into their products, necessitating advanced processors and accelerators. Furthermore, global supply chains and long-term procurement agreements provide OEMs with significant purchasing power, reinforcing their position as the leading end-user group. Their central role in transforming semiconductor components into market-ready systems secures their dominance within the processing-device ecosystem.

The Global Semiconductor Device for Processing Application Market Report is segmented on the basis of the following:

By Device Type

- Microprocessors (MPUs)

- General-Purpose CPUs

- Server Processors

- Embedded Processors

- Microcontrollers (MCUs)

- 8-bit MCUs

- 16-bit MCUs

- 32-bit MCUs

- Digital Signal Processors (DSPs)

- Fixed-Point DSPs

- Floating-Point DSPs

- Application-Specific Integrated Circuits (ASICs)

- Standard-Cell ASICs

- Full-Custom ASICs

- Semi-Custom ASICs

- Field-Programmable Gate Arrays (FPGAs)

- Low-End FPGAs

- Mid-Range FPGAs

- High-End FPGAs

- Graphics Processing Units (GPUs)

- Integrated GPUs

- Discrete GPUs

- AI/Neural Processing Units (NPUs)

- Edge AI Accelerators

- Data Center AI Accelerators

By Processing Architecture

- Multi-Core

- Single-Core

- Heterogeneous Computing

By Application

- Consumer Electronics

- Automotive

- Industrial Automation

- Telecommunications & Networking

- Data Centers & Cloud Computing

- Healthcare

- Others

By End User

- OEMs

- Foundries & IDMs

- Enterprises

- Government & Research Institutions

Regional Analysis

Leading Region by Market Share

ℹ

To learn more about this report –

Download Your Free Sample Report Here

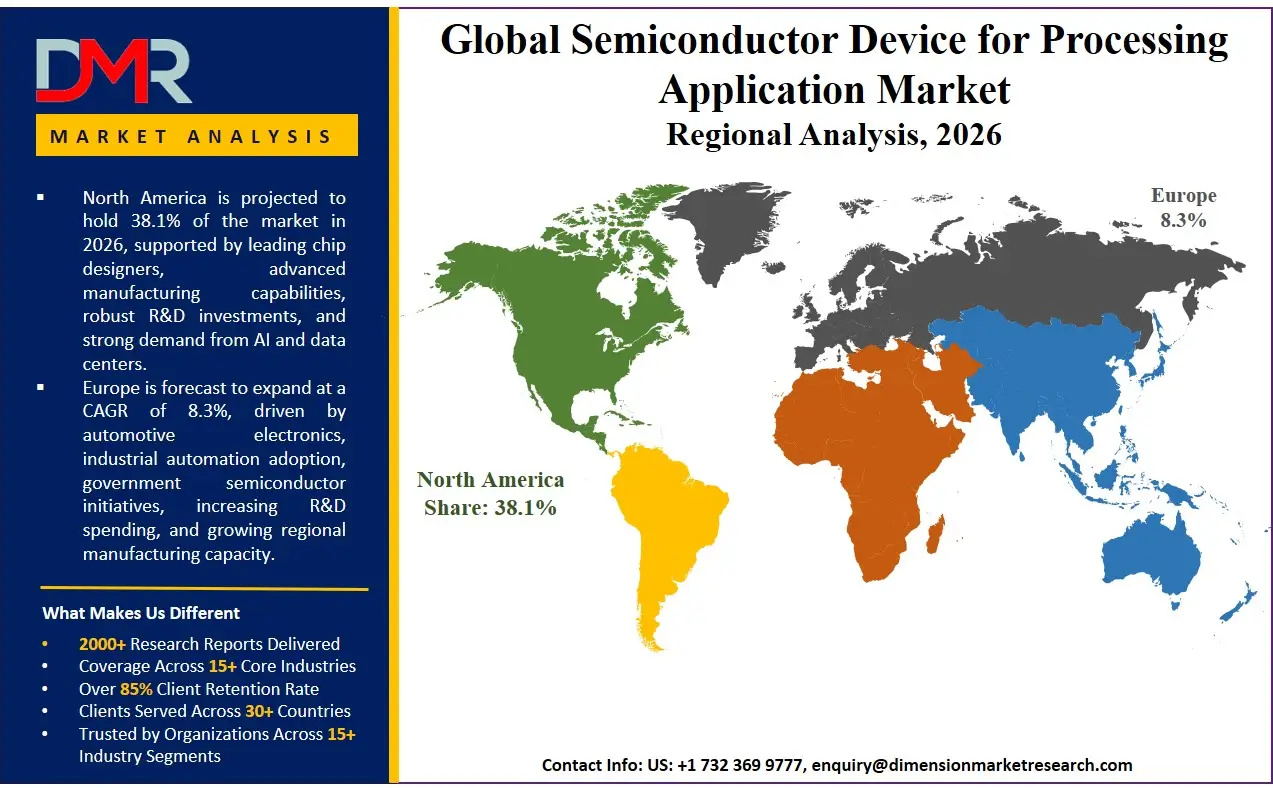

North America is poised to dominate the global semiconductor device for processing application market, holding a projected 38.1% of the market share by the end of 2026. The United States anchors this dominance through an unmatched intellectual property moat, housing the world's leading fabless design firms, GPU and CPU architecture licensors, and EDA software tool vendors. The region benefits from a flywheel effect: the deployment of large capital pools into AI-native startups drives the demand for silicon, which funds the R&D for next-generation Data Center AI Accelerators, which in turn enables new AI capabilities. Moreover, the CHIPS Act is successfully catalyzing a physical onshoring of leading-edge foundry capabilities, creating a tight innovation loop between system architects and semiconductor manufacturing that is hard to replicate globally.

Fastest-Growing Regional Market

Europe is poised to command the highest CAGR of 8.3% because it is starting from a position of catch-up, creating a pronounced growth leap as it aggressively builds sovereign chip capabilities. Unlike mature manufacturing hubs, Europe is channeling massive, unprecedented investments through the EU Chips Act to onshore advanced-node ASIC production and FD-SOI fabrication, directly amplifying regional output. Simultaneously, the region's global leadership in automotive electronics and industrial automation is undergoing a fundamental architectural overhaul, shifting from legacy 8-bit MCUs to complex, high-value heterogeneous SoCs that merge AI inference with deterministic control. This confluence of a low baseline manufacturing capacity now being rapidly scaled, combined with soaring R&D spending by OEMs transitioning to software-defined vehicles, generates a steeper expansion trajectory than already-saturated, high-volume production regions.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The competitive landscape of the global semiconductor processing device market is a high-stakes, winner-take-most arena defined by extreme capital intensity and the battle over architectural lock-in. The market is dominated by a few integrated design-and-marketing giants in the MPU and GPU segments and a diversified cadre of fabless specialists in MCUs and FPGAs. Success hinges on the control of the instruction set architecture (x86, Arm, RISC-V) and the proprietary interconnects that bundle accelerators into a coherent Heterogeneous Computing system. The trend toward vertical integration is accelerating, with hyper-scale End Users bypassing traditional OEMs to commission their own Semi-Custom ASICs and Foundries & IDMs offering pre-verified chiplet building blocks. Consolidation is rampant as incumbents acquire specialized NPU and interconnect IP firms to bolster their chiplet portfolios and prevent architectural obsolescence in the AI era.

Some of the prominent players in the Global Semiconductor Device for Processing Application Market are:

- Intel

- AMD

- NVIDIA

- Qualcomm

- Broadcom

- MediaTek

- Samsung Electronics

- Texas Instruments

- NXP Semiconductors

- STMicroelectronics

- Infineon Technologies

- Renesas Electronics

- Marvell Technology

- Microchip Technology

- Analog Devices

- ON Semiconductor

- SK hynix

- Apple

- IBM

- HiSilicon Technologies

- Other Key Players

Recent Developments

- March 2024: NVIDIA unveiled its Blackwell AI platform, featuring dual-reticle GPUs connected by a high-speed chip-to-chip interconnect and optimized for training and inference of large AI models.

- April 2024: Intel introduced its second-generation AI-enhanced software-defined vehicle SoC, the automotive industry's first chiplet-based architecture for scalable compute, graphics, and AI in vehicles.

- January 2025: Qualcomm expanded the Snapdragon X Series beyond notebooks to desktop and mini-PC form factors, leveraging integrated NPUs to deliver advanced on-device AI experiences for Windows PCs.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 215.1 Bn |

| Forecast Value (2035) |

USD 404.5 Bn |

| CAGR (2026–2035) |

7.3% |

| The US Market Size (2026) |

USD 67.1 Bn |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Device Type, By Processing Architecture, By Application, and By End User |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Global Semiconductor Device for Processing Application Market?

▾ The Global Semiconductor Device for Processing Application market is poised to be valued at USD 215.1 billion in 2026 and is projected to reach USD 404.5 billion by 2035, driven by the universal insertion of silicon intelligence into data centers, vehicles, and edge devices.

What is the CAGR of the Global Semiconductor Device for Processing Application Market from 2026 to 2035?

▾ The market is expected to grow at a CAGR of 7.3% from 2026 to 2035, reflecting the accelerating architectural complexity and capital intensity required to advance computational performance beyond traditional Moore’s Law scaling.

What factors are driving the growth of the Global Semiconductor Device for Processing Application Market?

▾ Key drivers include the exponential computing demand of generative AI, the architectural transformation of the automobile into a software-defined platform, and the global imperative to secure semiconductor supply chains through localized manufacturing.

Which region held the largest share of the Semiconductor Device for Processing Application Market in 2026?

▾ North America is projected to hold 38.1% of the market share in 2026, driven by its unassailable leadership in advanced processor design, EDA intellectual property, and the deep partnership between hyperscale cloud platforms and silicon architects.

Which region is expected to grow the fastest in the Semiconductor Device for Processing Application Market?

▾ The Europe region is expected to grow the fastest, fueled by sovereign semiconductor investments in China, the massive consumer electronics manufacturing base, and the rapid electrification of the regional automotive fleet.

What are the major trends in the Global Semiconductor Device for Processing Application Market?

▾ Major trends include the disaggregation of monolithic SoCs into chiplet-based architectures, the open-standard RISC-V ISA challenging proprietary architectures, and the structural pivot toward in-memory and near-memory compute to break the data-transfer bottleneck.

Who are the key players in the Global Semiconductor Device for Processing Application Market?

▾ Key players include architectural leaders like Intel, AMD, NVIDIA, and Qualcomm, who drive the CPU, GPU, and AI accelerator landscape, alongside specialized processing firms like Texas Instruments, STMicroelectronics, and NXP for the embedded and automotive sectors.

How is the Global Semiconductor Device for Processing Application Market segmented?

▾ The market is segmented by Device Type, Processing Architecture, Application , and End User.