What is the Semiconductor Devices for Electric Vehicle Market Size?

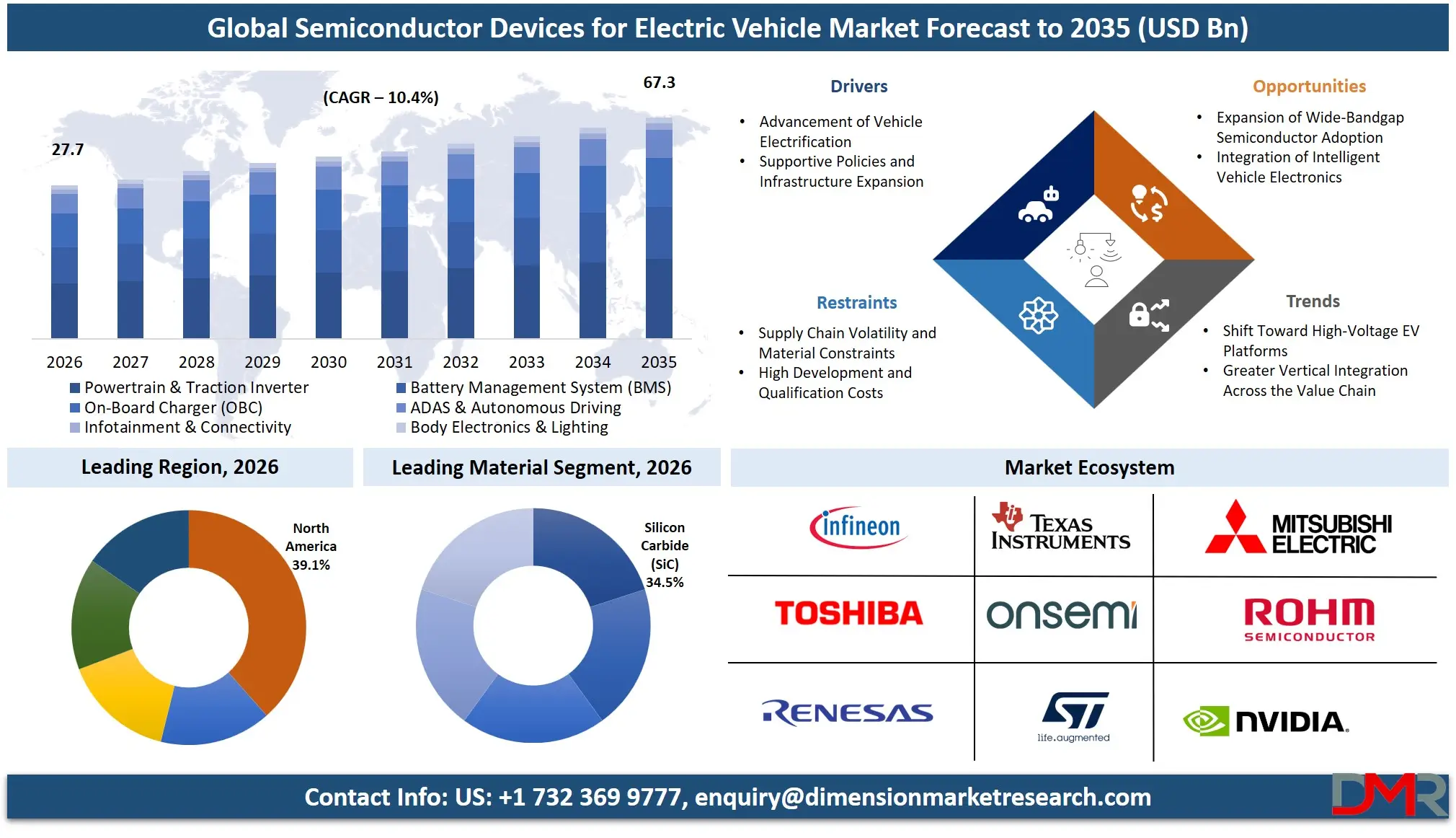

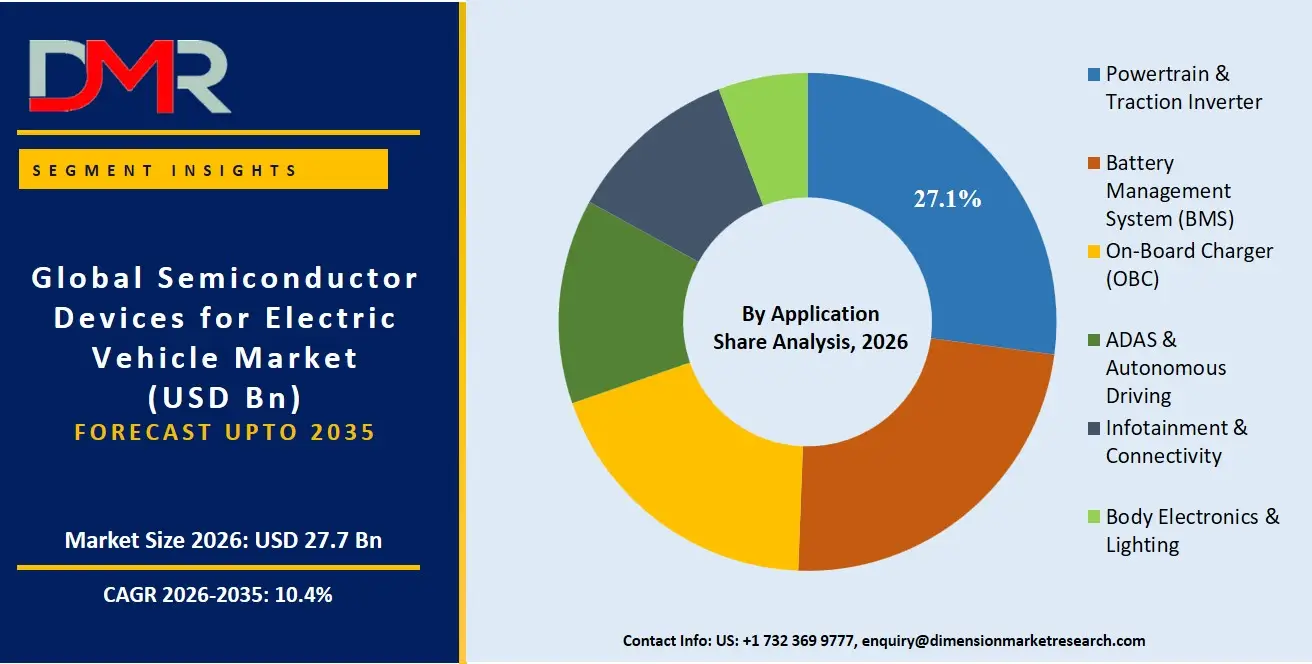

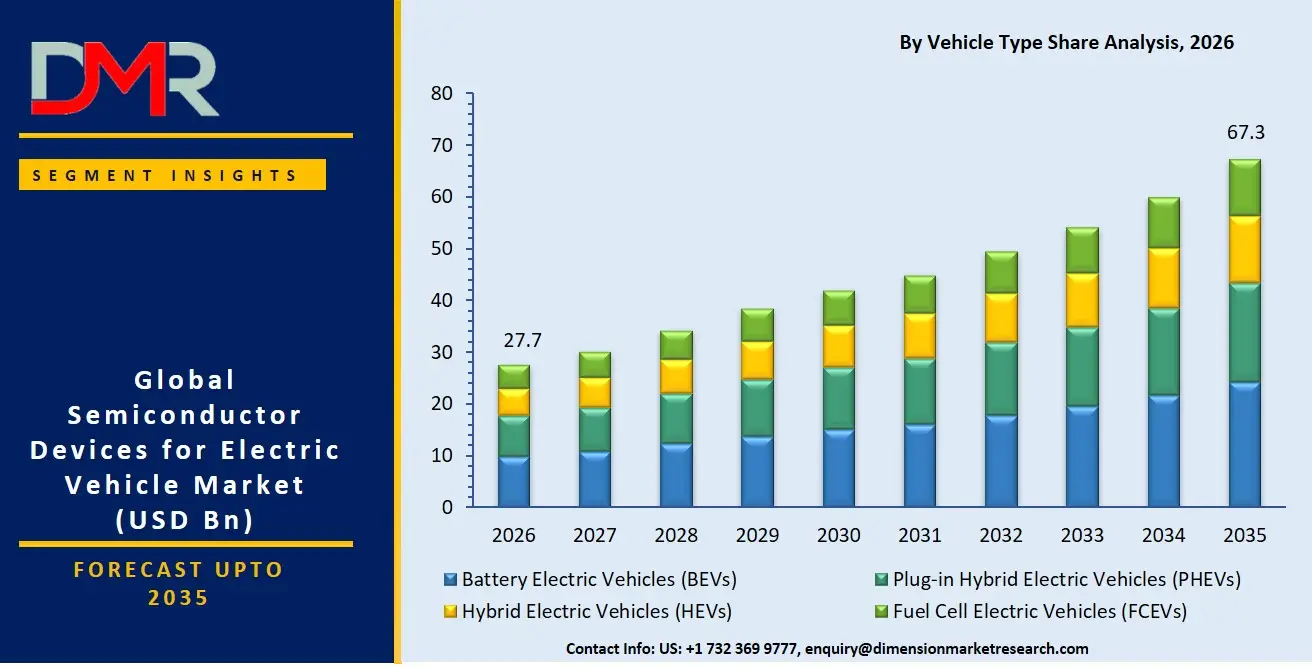

The Global Semiconductor Devices for Electric Vehicle Market is expected to reach a value of USD 27.7 billion in 2026, and is further anticipated to reach USD 67.3 billion by 2035, growing at a CAGR of 10.4% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The semiconductor devices market for electric vehicles is experiencing a structural transformation, driven by the rapid electrification of the automotive industry and the shift from internal combustion engines to software-defined, battery-powered architectures. This market encompasses power semiconductors, processing and control units, sensors, and memory devices that collectively manage energy conversion, autonomous driving functions, and in-vehicle connectivity. The surging demand for faster charging, extended driving range, and advanced driver-assistance systems (ADAS) is compelling automakers to innovate their powertrain and electrical/electronic (E/E) architectures, fueling the need for specialized semiconductor solutions. Battery Electric Vehicles (BEVs) and Plug-in Hybrids (PHEVs) are the primary platforms for this growth, with Silicon Carbide (SiC) and Gallium Nitride (GaN) emerging as critical materials for next-generation power efficiency.

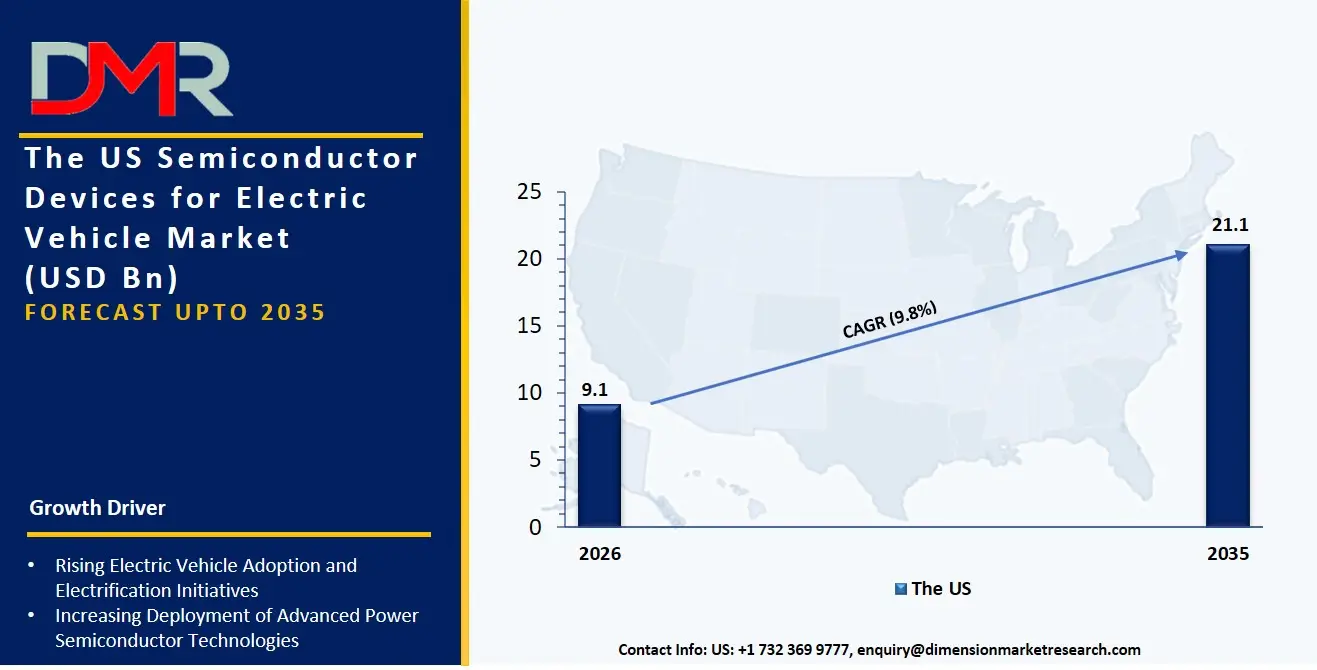

The US Semiconductor Devices for Electric Vehicle Market

The US Semiconductor Devices for Electric Vehicle Market is projected to reach USD 9.1 billion in 2026, growing at a compound annual growth rate of 9.8% over its forecast period, culminating in a value of USD 21.1 billion by 2035.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The US remains a pivotal innovation hub, driven by the aggressive electrification strategies of domestic automakers and the rapid expansion of domestic chip manufacturing capabilities. The market is characterized by a high-intensity demand for AI/Domain Controllers, as automakers seek to consolidate dozens of legacy electronic control units into centralized, high-performance computing platforms. Furthermore, the push for ultra-fast charging infrastructure is creating a parallel need for advanced Silicon Carbide (SiC) power modules that can operate reliably at high voltages and temperatures, making risk-mitigated supply chain consulting a critical value-add for OEMs.

The Europe Semiconductor Devices for Electric Vehicle Market

The Europe Semiconductor Devices for Electric Vehicle Market is estimated to be valued at USD 8.5 billion in 2026 and is further anticipated to reach USD 20.3 billion by 2035 at a CAGR of 10.1%. The European market is heavily influenced by stringent CO2 emission mandates under the "Fit for 55" package, which are compressing development timelines and forcing automakers to rapidly adopt 800V electrical architectures. This shift directly accelerates the demand for SiC-based Traction Inverters and On-Board Chargers (OBCs). The region's strong legacy in luxury and performance vehicles is also driving the integration of high-density Gallium Nitride (GaN) devices in compact power converters. Additionally, European OEMs are pioneering functional safety compliance, requiring sensor semiconductors and processing chips that meet the highest ASIL-D integrity levels for autonomous driving applications.

The Japan Semiconductor Devices for Electric Vehicle Market

The Japan Semiconductor Devices for Electric Vehicle Market is projected to be valued at USD 2.1 billion in 2026 at a CAGR of 9.5%. The Japanese market is unique, driven by a powerful consortium-led approach to electrification and a deep heritage in power electronics manufacturing. Major conglomerates are heavily investing in next-generation MOSFETs and IGBTs to reclaim global leadership in power semiconductor efficiency. There is also a distinct niche in developing ultra-compact, highly reliable microcontrollers (MCUs) for Body Electronics and Battery Management Systems (BMS), which bridge the gap between legacy 12V systems and new high-voltage EV platforms, demanding seamless integration and real-time precision.

Key Takeaways

- Market Size & Forecast: The Global Semiconductor Devices for EV market is projected to reach USD 27.7 billion in 2026, expanding to USD 67.3 billion by 2035, fueled by the dual engines of xEV proliferation and the architectural shift to centralized, software-defined vehicle platforms.

- Growth Rate & Outlook: Global market growth is expected at a CAGR of 10.4%, driven by the critical need to eliminate charging anxiety through 800V fast-charging systems and the escalating semiconductor content per vehicle required for Level 3+ autonomous driving.

- Primary Growth Drivers: Key forces include the transition from silicon-based IGBTs to wide-bandgap SiC power devices for superior powertrain efficiency, the consolidation of ECUs into AI/Domain Controllers, and the exponential increase in sensor redundancy for functional safety compliance.

- Key Market Trends: Major trends include the industrialization of 200mm SiC wafers to lower device costs, the integration of multi-sensor fusion algorithms directly onto processing chips, and the shift toward smart, predictive Battery Management Systems using advanced MCUs.

- By Material Analysis: Silicon Carbide (SiC) is expected to dominate material innovation conversations due to its ability to unlock 5-10% greater powertrain efficiency. Silicon (Si)-based IGBTs will retain high volume in cost-sensitive segments, while GaN devices gain traction in auxiliary low-power converters and LiDAR systems.

- By Application Analysis: Powertrain & Traction Inverter is the most lucrative application, representing the largest bill-of-materials share. ADAS & Autonomous Driving is the fastest-growing segment as vehicle safety architectures demand redundant processing and high-bandwidth memory devices to handle sensor fusion data.

- Regional Leadership: North America is poised to dominate this market with 39.1% of the market share in 2026, driven by a strong domestic EV design ecosystem and strategic federal investments in advanced semiconductor manufacturing and packaging capabilities.

What is the Semiconductor Devices for Electric Vehicle?

Semiconductor devices for electric vehicles are the specialized electronic components that serve as the foundational building blocks for all high-voltage power management, intelligent processing, and safety-critical sensing within electrified vehicles. Unlike generic consumer-grade chips, these devices are engineered for extreme automotive reliability, temperature tolerance, and functional safety standards. This market encompasses Power Semiconductors (like SiC MOSFETs and IGBTs) that switch high currents in the traction inverter, Processing & Control Semiconductors (like AI domain controllers) that interpret sensor data to make real-time decisions, Sensor Semiconductors that provide precise current and position feedback, and Memory Devices that store firmware and driving data. With the average EV containing roughly twice the semiconductor content of a traditional combustion vehicle, these components are the core enablers of range, performance, and intelligence, transforming battery chemistry into a controllable, high-performance driving experience.

Use Cases

- High-Voltage Fast Charging in BEVs: Premium electric vehicles utilize Silicon Carbide (SiC) power modules within their On-Board Chargers (OBC) and traction inverters to efficiently convert AC grid power to DC battery voltage, enabling 800V architectures that halve charging times compared to 400V systems.

- Predictive Battery Management: Advanced Battery Management Systems (BMS) deploy high-precision microcontrollers (MCUs) and isolated current sensors to monitor voltage and temperature at the cell level, employing complex algorithms to predict state-of-health and prevent thermal runaway across thousands of Li-ion cells.

- Centralized Autonomous Driving Processing: Purpose-built AI/Domain Controllers fuse inputs from camera, radar, and LiDAR sensors in a centralized computing node, executing high-fidelity environmental perception models to enable real-time path planning and Level 3+ hands-free driving on highways.

- Electric Powertrain for Heavy Loads: In commercial electric trucks and buses, parallel arrays of high-power IGBTs and SiC MOSFETs in the traction inverter convert DC battery power into AC current to drive high-torque motors, ensuring reliable performance under continuous high-load conditions.

How AI is Transforming the Semiconductor Devices for Electric Vehicle Market?

AI is reshaping the semiconductor landscape for electric vehicles by demanding a new class of neural processing units and physically-aware edge computing architectures. In the domain of AI/Domain Controllers, system-on-chips (SoCs) are being designed with dedicated deep-learning accelerators that process sensor fusion data in real-time, enabling vehicles to navigate complex urban environments with minimal latency. This pushes the need for high-bandwidth, automotive-grade DRAM (LPDDR) to ensure the AI model's weight data flows without bottlenecks.

Beyond autonomy, AI is embedding intelligence directly into power management. Generative AI models are being used to design and simulate next-generation SiC and GaN device structures, optimizing thousands of microscopic transistor trench patterns to achieve maximum power density with minimal switching losses. In Battery Management Systems, tiny on-chip inference engines within advanced MCUs are beginning to predict lithium-ion cell degradation patterns, dynamically adjusting charging curves to extend battery longevity without physical intervention.

Market Dynamics

Key Drivers in the Global Semiconductor Devices for Electric Vehicle Market

Advancement of Vehicle Electrification

Rapid electrification of passenger and commercial vehicles is significantly increasing demand for power semiconductors, sensors, and control ICs. These components enable efficient traction inverters, battery management systems, and onboard charging units, supporting higher driving range and improved vehicle performance. As governments strengthen emission regulations and consumers increasingly adopt electric mobility, automakers are integrating sophisticated semiconductor architectures to enhance energy efficiency and reliability. The transition toward higher-voltage platforms and fast-charging capabilities further intensifies the need for advanced silicon carbide and gallium nitride devices, making semiconductor content per vehicle substantially greater than in conventional automobiles and reinforcing sustained market expansion.

Supportive Policies and Infrastructure Expansion

Government incentives, fuel-economy mandates, and investments in charging infrastructure are accelerating EV deployment worldwide. Expanding charging networks encourage consumer confidence and stimulate vehicle sales, directly increasing semiconductor consumption. Simultaneously, public funding for domestic chip manufacturing and automotive supply-chain resilience is fostering innovation and production capacity. Regulatory emphasis on safety, connectivity, and energy efficiency also drives adoption of advanced semiconductor solutions for powertrain control and intelligent vehicle systems. Together, policy support and infrastructure development create a favorable ecosystem that sustains long-term demand for automotive-grade semiconductor devices and encourages manufacturers to invest in next-generation technologies tailored to electric vehicles.

Restraints in the Global Semiconductor Devices for Electric Vehicle Market

Supply Chain Volatility and Material Constraints

The industry remains vulnerable to supply disruptions involving wafers, specialty gases, and critical raw materials. Lengthy fabrication cycles and concentrated manufacturing capacity can create shortages, increasing lead times and costs for automakers. Dependence on advanced substrates for silicon carbide devices further compounds procurement challenges. Such volatility complicates production planning and may delay vehicle launches or limit output. In addition, geopolitical tensions and trade restrictions can affect component availability, prompting manufacturers to maintain larger inventories and diversify sourcing strategies, actions that elevate operational expenses and reduce the pace at which semiconductor technologies are deployed across the electric vehicle sector.

High Development and Qualification Costs

Automotive semiconductors require rigorous testing and qualification to meet stringent safety and reliability standards. Developing devices capable of operating under extreme temperatures and demanding electrical conditions necessitates substantial investments in research, specialized equipment, and certification. Smaller suppliers may face barriers to entry due to these costs, while automakers encounter higher component prices during early adoption stages. The transition to wide-bandgap technologies adds further expenditure related to manufacturing processes and packaging innovations. Consequently, elevated development costs can slow commercialization timelines and constrain widespread deployment, particularly in cost-sensitive vehicle segments and emerging EV markets.

Growth Opportunities in the Global Semiconductor Devices for Electric Vehicle Market

Expansion of Wide-Bandgap Semiconductor Adoption

Silicon carbide and gallium nitride technologies offer substantial efficiency gains, reduced energy losses, and compact system designs. Their increasing integration into inverters, charging systems, and power converters presents significant growth potential for suppliers. As production scales and costs decline, these materials are expected to penetrate mass-market electric vehicles, enabling longer ranges and faster charging. Manufacturers investing in dedicated fabrication capacity and innovative packaging solutions can secure competitive advantages. The growing preference for high-voltage architectures further strengthens this opportunity, positioning wide-bandgap semiconductors as a cornerstone of future EV platforms and a major avenue for market value creation.

Integration of Intelligent Vehicle Electronics

Electric vehicles increasingly incorporate advanced driver assistance, connectivity, and predictive energy-management functions. This evolution creates opportunities for semiconductor companies to provide high-performance processors, sensors, and communication chips that complement power electronics. Software-defined vehicle architectures require scalable computing platforms capable of supporting over-the-air updates and data-intensive applications. Suppliers offering integrated solutions that combine power efficiency with processing capability can capture additional revenue streams. Collaboration between chipmakers and automakers in developing customized semiconductor ecosystems is likely to accelerate, expanding the addressable market and fostering innovation across both premium and mainstream electric vehicle segments.

Trends in the Global Semiconductor Devices for Electric Vehicle Market

Shift Toward High-Voltage EV Platforms

Automakers are increasingly adopting 800-volt and higher electrical architectures to improve charging speed and drivetrain efficiency. This trend is boosting demand for semiconductors with superior voltage handling, thermal performance, and switching characteristics. Advanced power modules and optimized packaging technologies are becoming standard design priorities. The resulting reduction in cable weight and charging times enhances overall vehicle appeal while encouraging broader use of silicon carbide components. As high-voltage systems proliferate across diverse vehicle classes, semiconductor suppliers are adapting product portfolios to meet evolving performance requirements and to support next-generation electric mobility solutions.

Greater Vertical Integration Across the Value Chain

Leading automakers and semiconductor manufacturers are pursuing closer partnerships, long-term supply agreements, and in some cases in-house chip development. Vertical integration enhances supply security, accelerates innovation, and enables optimization of semiconductor designs for specific vehicle platforms. Companies are also investing in localized manufacturing and advanced packaging capabilities to reduce dependency on external suppliers. This collaborative trend promotes faster commercialization cycles and more resilient supply chains. As electric vehicles become increasingly electronics-centric, integrated development strategies are expected to play a defining role in shaping competitive dynamics within the global semiconductor device market.

Research Scope and Analysis

The global semiconductor devices for electric vehicle market is segmented by device type into power, processing and control, sensor, and memory semiconductors; by material into silicon, silicon carbide, and gallium nitride; by vehicle type, application, and sales channel, encompassing OEM and aftermarket distribution to comprehensively assess demand across the EV value chain.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Device Type Analysis

Power semiconductors is projected to dominate the market because they are indispensable for energy conversion and control in traction inverters, onboard chargers, and auxiliary power systems. Every electric vehicle requires multiple high-power devices to efficiently manage battery energy and propulsion, resulting in significantly higher semiconductor content than other device categories. The transition toward higher-voltage architectures and faster charging further increases demand for advanced power devices, particularly silicon carbide components. Their direct impact on driving range, efficiency, and vehicle performance makes power semiconductors the largest revenue contributor. Continuous innovation in switching speed, thermal management, and packaging further reinforces their leading position within the electric-vehicle semiconductor ecosystem.

By Material Analysis

Silicon carbide (SiC) is poised to be the dominant material in value terms due to its superior efficiency, high-temperature capability, and ability to support high-voltage operation. EV manufacturers increasingly adopt SiC devices in traction inverters and fast-charging systems to extend driving range and reduce energy losses. Although silicon remains widely used, the performance advantages of SiC justify its premium pricing and rapid penetration into next-generation platforms. Expanding production capacity and ongoing cost reductions are accelerating adoption across vehicle segments. As automakers prioritize efficiency and charging performance, silicon carbide has emerged as the material of choice for advanced electric-vehicle semiconductor applications.

By Vehicle Type Analysis

Battery electric vehicles (BEVs) is expected to dominate semiconductor demand because they rely entirely on electrical propulsion and therefore require the highest semiconductor content per vehicle.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Their powertrains incorporate sophisticated inverters, battery management systems, charging electronics, and advanced computing platforms. Strong consumer adoption, supportive government policies, and expanding charging infrastructure continue to boost BEV production worldwide. Compared with hybrids and fuel-cell vehicles, BEVs necessitate larger batteries and more powerful power electronics, translating directly into greater semiconductor value. The ongoing shift toward fully electric mobility ensures that BEVs remain the principal driver of growth in the electric-vehicle semiconductor market.

By Application Analysis

Powertrain and traction inverter applications are projected to account for the largest share because they are central to converting battery energy into propulsion. These systems require high-performance power semiconductors capable of handling substantial currents and voltages with minimal losses. Improvements in inverter efficiency directly enhance vehicle range and performance, making this area a focal point for innovation and investment. The increasing adoption of high-voltage platforms and silicon carbide technology further elevates semiconductor content within the powertrain. Since every electric vehicle depends on these critical functions, powertrain and traction inverter applications consistently represent the dominant segment.

By Sales Channel Analysis

OEMs are projected to dominate sales as they procure semiconductors directly for integration into new electric vehicles during manufacturing. Their large production volumes, long-term sourcing agreements, and close collaboration with chip suppliers enable early access to advanced technologies and customized solutions. The aftermarket remains comparatively limited because semiconductor replacements are infrequent and often tied to specialized service networks. OEM-driven design decisions determine the majority of semiconductor content and value within vehicles. As global EV production continues to expand, original equipment manufacturers will remain the primary purchasing channel, solidifying their leadership in the semiconductor devices for electric vehicles market.

The Global Semiconductor Devices for Electric Vehicle Market Report is segmented on the basis of the following:

By Device Type

- Power Semiconductors

- IGBTs

- MOSFETs

- Silicon Carbide (SiC) Devices

- Gallium Nitride (GaN) Devices

- Processing & Control Semiconductors

- Microcontrollers (MCUs)

- Microprocessors (MPUs)

- AI/Domain Controllers

- Sensor Semiconductors

- Current Sensors

- Temperature Sensors

- Position Sensors

- Memory Devices

By Material

- Silicon Carbide (SiC)

- Silicon (Si)

- Gallium Nitride (GaN)

By Vehicle Type

- Battery Electric Vehicles (BEVs)

- Plug-in Hybrid Electric Vehicles (PHEVs)

- Hybrid Electric Vehicles (HEVs)

- Fuel Cell Electric Vehicles (FCEVs)

By Application

- Powertrain & Traction Inverter

- Battery Management System (BMS)

- On-Board Charger (OBC)

- ADAS & Autonomous Driving

- Infotainment & Connectivity

- Body Electronics & Lighting

By Sales Channel

Regional Analysis

Leading Region by Market Share

ℹ

To learn more about this report –

Download Your Free Sample Report Here

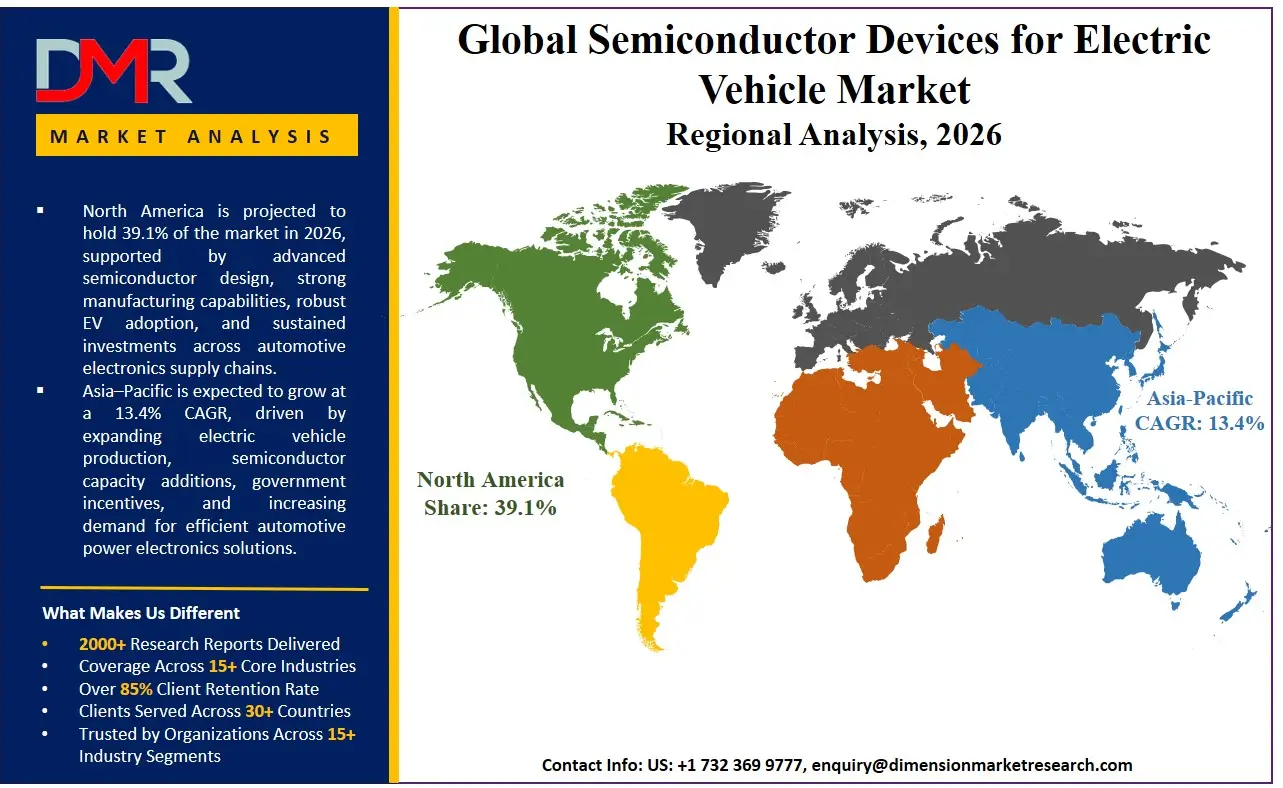

North America is poised to dominate the global semiconductor devices for electric vehicle market, holding an estimated 39.1% of the market share by the end of 2026. This leadership is anchored by a powerful convergence of Tesla's vertical integration strategy and the electrification roadmaps of legacy Detroit automakers, which creates an insatiable demand for advanced Power Semiconductors and AI/Domain Controllers. The region benefits from a robust fabless design ecosystem and substantial CHIPS Act-funded investment in domestic, leading-edge manufacturing and advanced packaging facilities. The heavy emphasis on Level 3 and 4 autonomous driving features among US automakers makes it the single largest addressable market for high-compute processing platforms and sensor fusion chips, pushing the frontier of automotive semiconductor innovation.

Fastest-Growing Regional Market

Asia-Pacific is expected to be the most rapidly expanding market, propelled by an unparalleled manufacturing scale and aggressive government-driven electrification policies, particularly in China. The region is not just the largest producer of EVs but is rapidly moving up the value chain to dominate the design and fabrication of automotive-grade SiC substrates and battery management ICs. The intense competition among Chinese domestic OEMs to differentiate in-cabin experience and autonomous driving capabilities is fueling a voracious appetite for high-performance Microprocessors (MPUs) and memory devices. Furthermore, the rapid investment in high-voltage charging infrastructure across Southeast Asia and China is directly catalyzing the deployment of 800V architectures, accelerating the substitution of legacy Si IGBTs with next-generation Silicon Carbide (SiC) power modules.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The competitive environment of global semiconductor devices for the EV market is a high-stakes arena defined by a technological arms race in material science and system-level integration. The landscape is characterized by a clear split between traditional silicon IGBT giants who command high-volume, lower-cost segments, and pure-play wide-bandgap innovators who are capturing the high-growth, high-margin SiC and GaN inverter sockets. Strategic control over the substrate supply chain, particularly the bottleneck of crystalline SiC boule production, has become the primary determinant of market power and capacity fulfillment. Vertical system integration is blurring competitive lines, with leading OEMs designing their own custom AI/Domain Controllers to control their software destiny, forcing traditional component suppliers to offer more deeply integrated "smart module" solutions. The ability to deliver functional safety certification packages seamlessly alongside silicon is rapidly becoming a non-negotiable ticket to compete.

Some of the prominent players in the Global Semiconductor Devices for Electric Vehicle Market are:

- Infineon Technologies AG

- STMicroelectronics N.V.

- NXP Semiconductors N.V.

- Texas Instruments Incorporated

- ON Semiconductor Corporation (onsemi)

- Renesas Electronics Corporation

- ROHM Co., Ltd.

- Mitsubishi Electric Corporation

- Toshiba Electronic Devices & Storage Corporation

- Wolfspeed, Inc.

- Qualcomm Incorporated

- NVIDIA Corporation

- Intel Corporation

- Analog Devices, Inc.

- Microchip Technology Incorporated

- Samsung Electronics Co., Ltd.

- SK hynix Inc.

- Bosch GmbH

- Hitachi Astemo, Ltd.

- Other Key Players

Recent Developments

- June 2026: Leading SiC innovator Wolfspeed announced customer samples of its next-generation Gen 5 200mm SiC MOSFET technology, optimized for 1200V and 750V automotive and industrial applications including 800V-class traction inverters, promising up to a 27% reduction in specific on-resistance (RSP) versus competing 1200V SiC solutions for premium Battery Electric Vehicles (BEVs).

- May 2026: Infineon Technologies introduced a new 1300V SiC power module within its HybridPACK Drive family, the first in the line capable of continuous operation at 205°C (versus the 175°C industry standard), enabling up to 15% higher output current in traction inverter applications while retaining the same footprint for drop-in compatibility with existing designs.

- January 2026: NXP Semiconductors unveiled its S32N7 series of 5nm super-integration processors, designed for centralized, software-defined vehicle architectures that digitalize core functions propulsion, vehicle dynamics, body, gateway, and safety domains into a single hub, with Bosch as the first partner to deploy the chip in its vehicle integration platform.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 27.7 Bn |

| Forecast Value (2035) |

USD 67.3 Bn |

| CAGR (2026–2035) |

10.4% |

| The US Market Size (2026) |

USD 9.1 Bn |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Device Type, By Material, By Vehicle Type, By Application, and By Sales Channel |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Global Semiconductor Devices for Electric Vehicle Market?

▾ The Global Semiconductor Devices for Electric Vehicle market is poised to be valued at USD 27.7 billion in 2026 and is projected to reach USD 67.3 billion by 2035, driven by the universal transition to electric powertrains and the increasing intelligence of software-defined vehicles.

What is the CAGR of the Global Semiconductor Devices for Electric Vehicle Market from 2026 to 2035?

▾ The market is expected to grow at a CAGR of 10.4% from 2026 to 2035, reflecting the accelerating semiconductor content per vehicle and the high-value transition from silicon to Silicon Carbide (SiC) materials in high-voltage systems.

What factors are driving the growth of the Global Semiconductor Devices for Electric Vehicle Market?

▾ Key drivers include global CO2 emission regulations forcing rapid EV adoption, the efficiency advantages of SiC and GaN materials in unlocking faster charging and longer range, and the architectural shift to centralized AI/Domain Controllers for autonomous driving features.

Which region held the largest share of the Semiconductor Devices for Electric Vehicle Market in 2026?

▾ North America is projected to hold 39.1% of the market share in 2026, driven by a strong concentration of EV design leadership, aggressive deployment of Level 3+ autonomy, and substantial federal investment in advanced chip manufacturing infrastructure.

Which region is expected to grow the fastest in the Semiconductor Devices for Electric Vehicle Market?

▾ The Asia-Pacific region is expected to grow the fastest, fueled by massive production scales in China and South Korea, alongside rapid local innovation in electric powertrains and autonomous driving technology.

What are the major trends in the Global Semiconductor Devices for Electric Vehicle Market?

▾ Major trends include the industrialization of 200mm SiC wafer manufacturing to reduce costs, the integration of AI inference accelerators directly into automotive MCUs, and the development of smart sensor modules with embedded processing for redundant, fail-operational E/E architectures.

Who are the key players in the Global Semiconductor Devices for Electric Vehicle Market?

▾ Key players include global power semiconductor leaders like Infineon, STMicroelectronics, Wolfspeed, and ON Semiconductor, as well as high-compute processor architects like NVIDIA, Qualcomm, and NXP Semiconductors, who are driving the intelligence layer of the EV revolution.

How is the Global Semiconductor Devices for Electric Vehicle Market segmented?

▾ The market is segmented by Device Type, Material, Vehicle Type, Application, and Sales Channel.