Market Overview

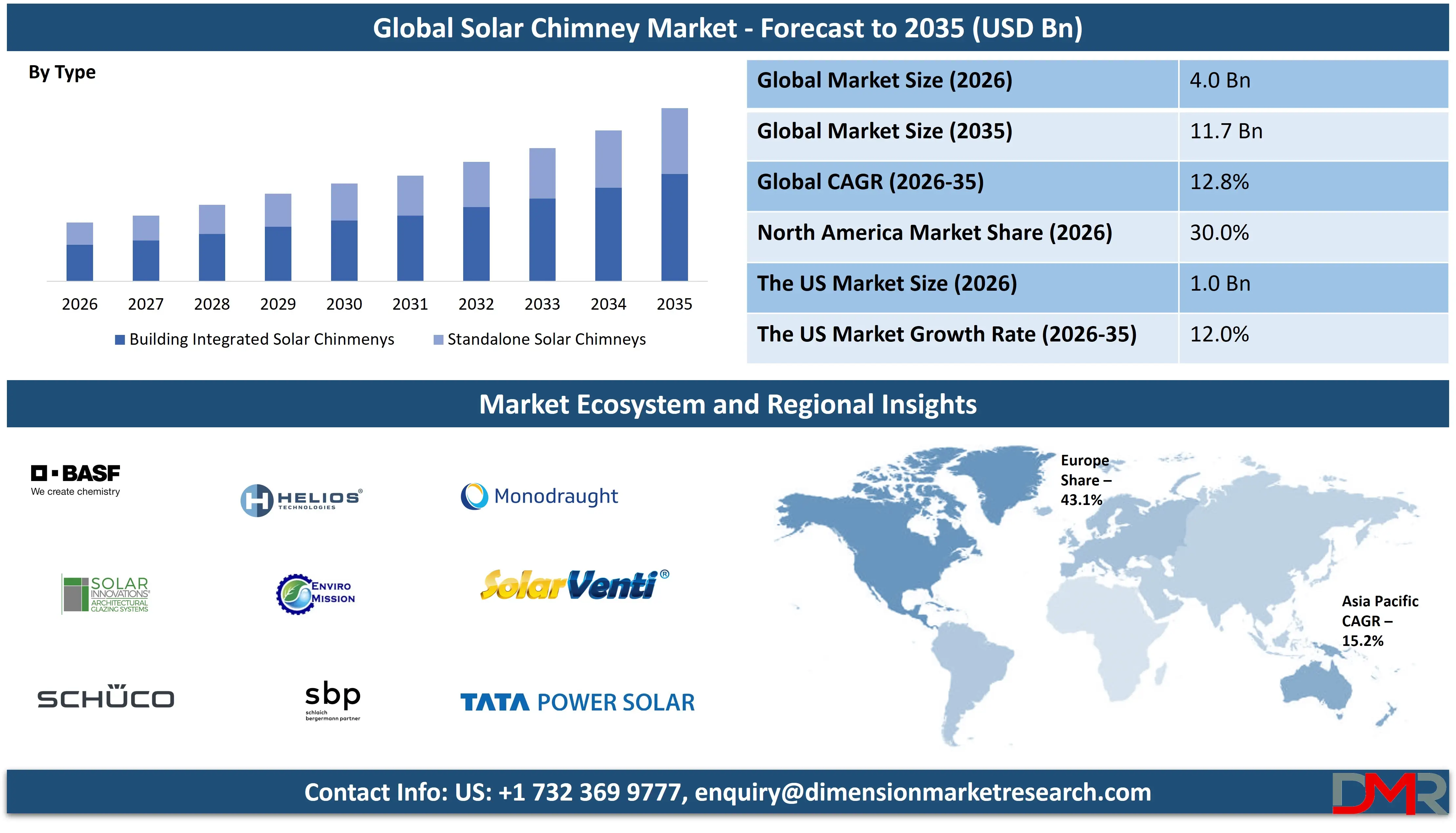

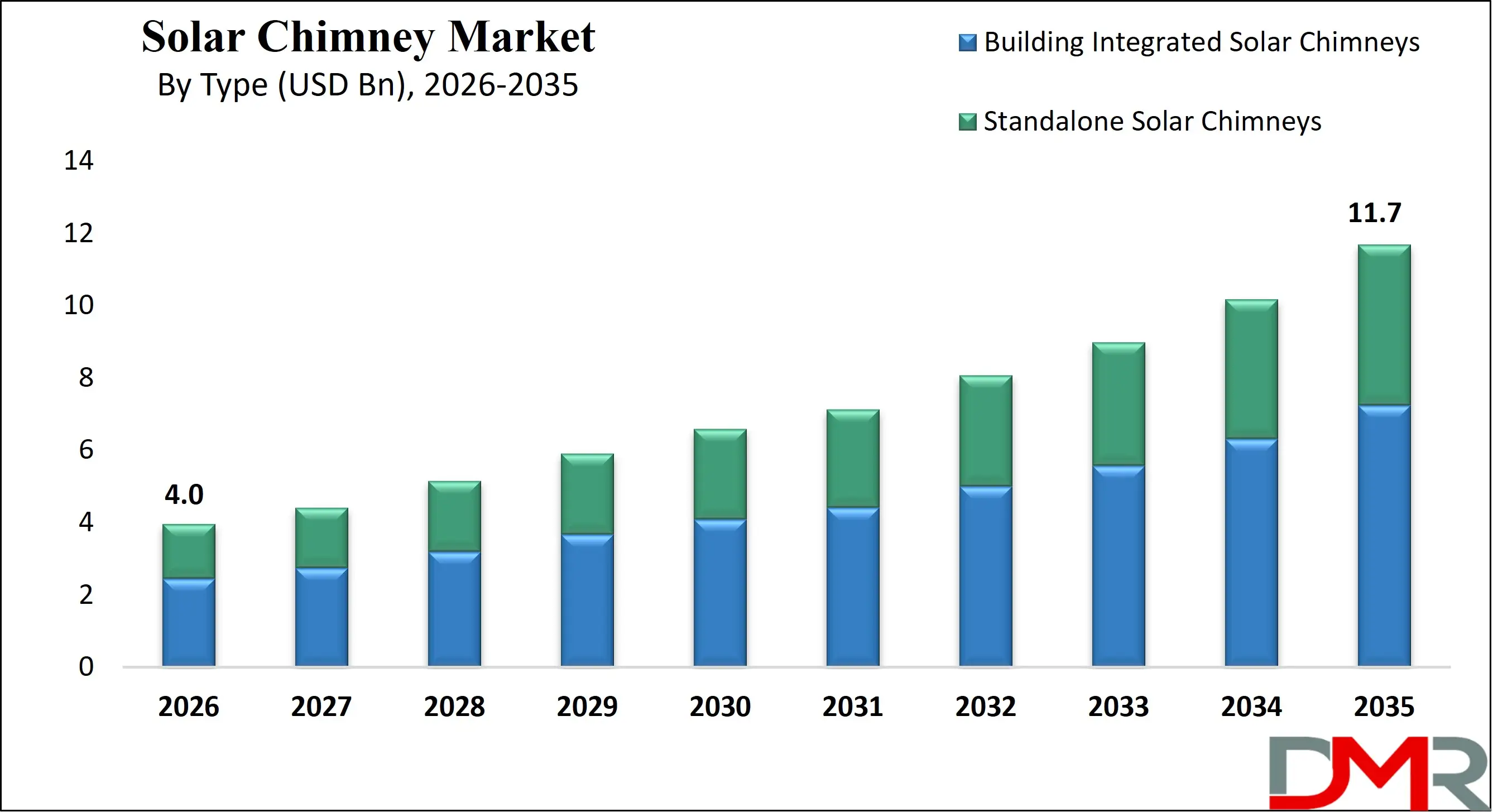

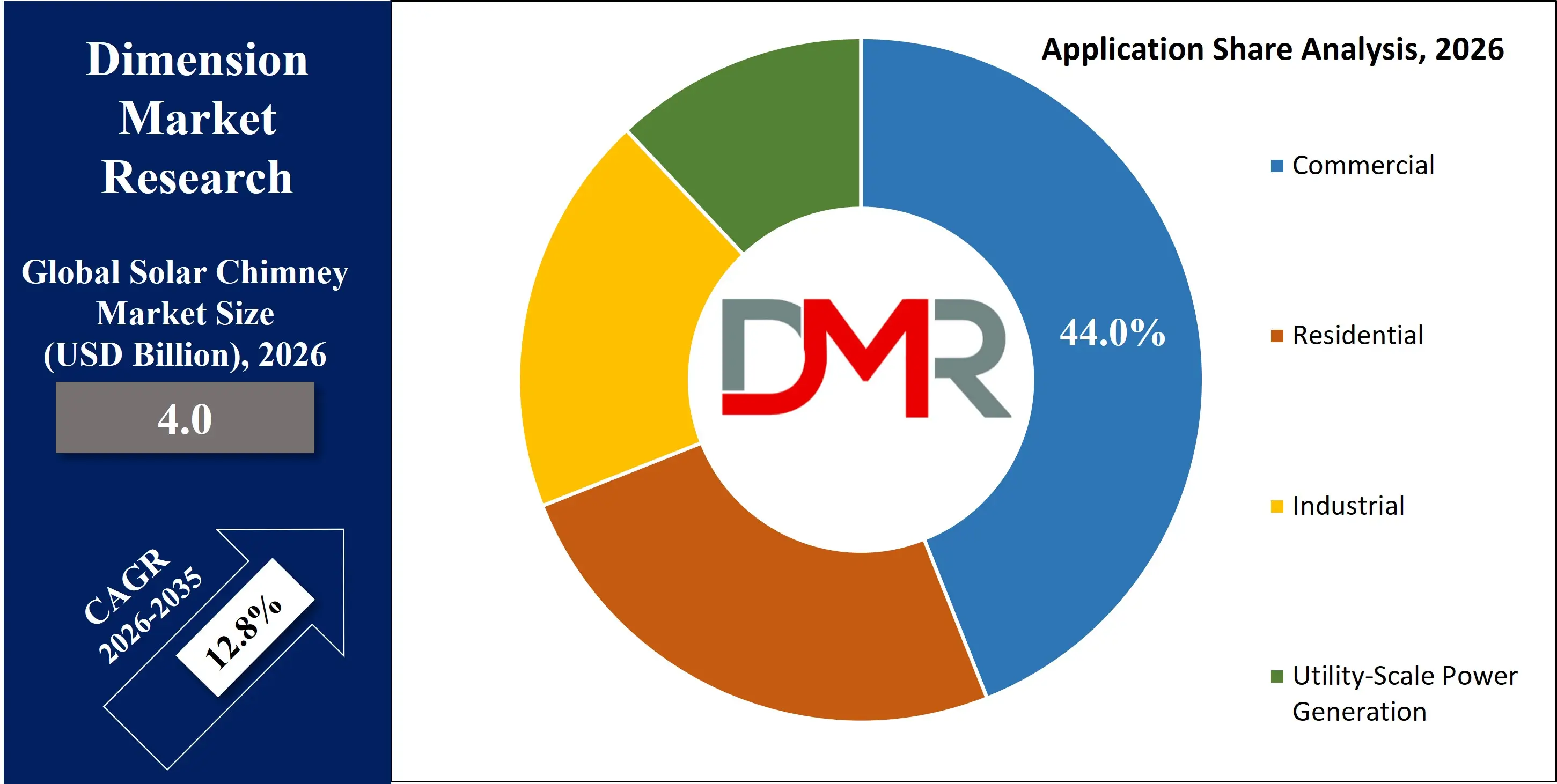

The Global Solar Chimney Market size is projected to reach USD 4.0 billion in 2026 and grow at a compound annual growth rate of 12.8% to reach a value of USD 11.7 billion in 2035.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Solar Chimney refers to a passive or hybrid architectural and energy-generation system that uses solar radiation to induce air movement for ventilation, cooling, or electricity production. It typically consists of a glazed collector area, a vertical or inclined chimney structure, and airflow channels that create a temperature differential to drive natural convection. In building applications, solar chimneys enhance indoor air circulation and reduce reliance on mechanical HVAC systems. In utility-scale configurations, they can be designed as solar chimney power plants that generate electricity through turbine-driven airflow. The concept integrates principles of thermodynamics, solar energy harvesting, and sustainable building design, positioning it within the broader renewable energy and green construction ecosystem.

The global emphasis on decarbonization, net-zero building standards, and energy-efficient construction has accelerated adoption. Advances in glazing materials, lightweight composites, and computational fluid dynamics modeling have improved performance predictability and cost efficiency. Growing interest in passive cooling solutions in hot climates and hybrid PV-integrated systems is shaping innovation pathways.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Further, significant activity includes pilot-scale power plants, integration with smart building management systems, and collaborations between architectural firms and renewable technology providers. Policy incentives for green buildings and sustainable infrastructure projects are also influencing investment patterns and commercialization strategies.

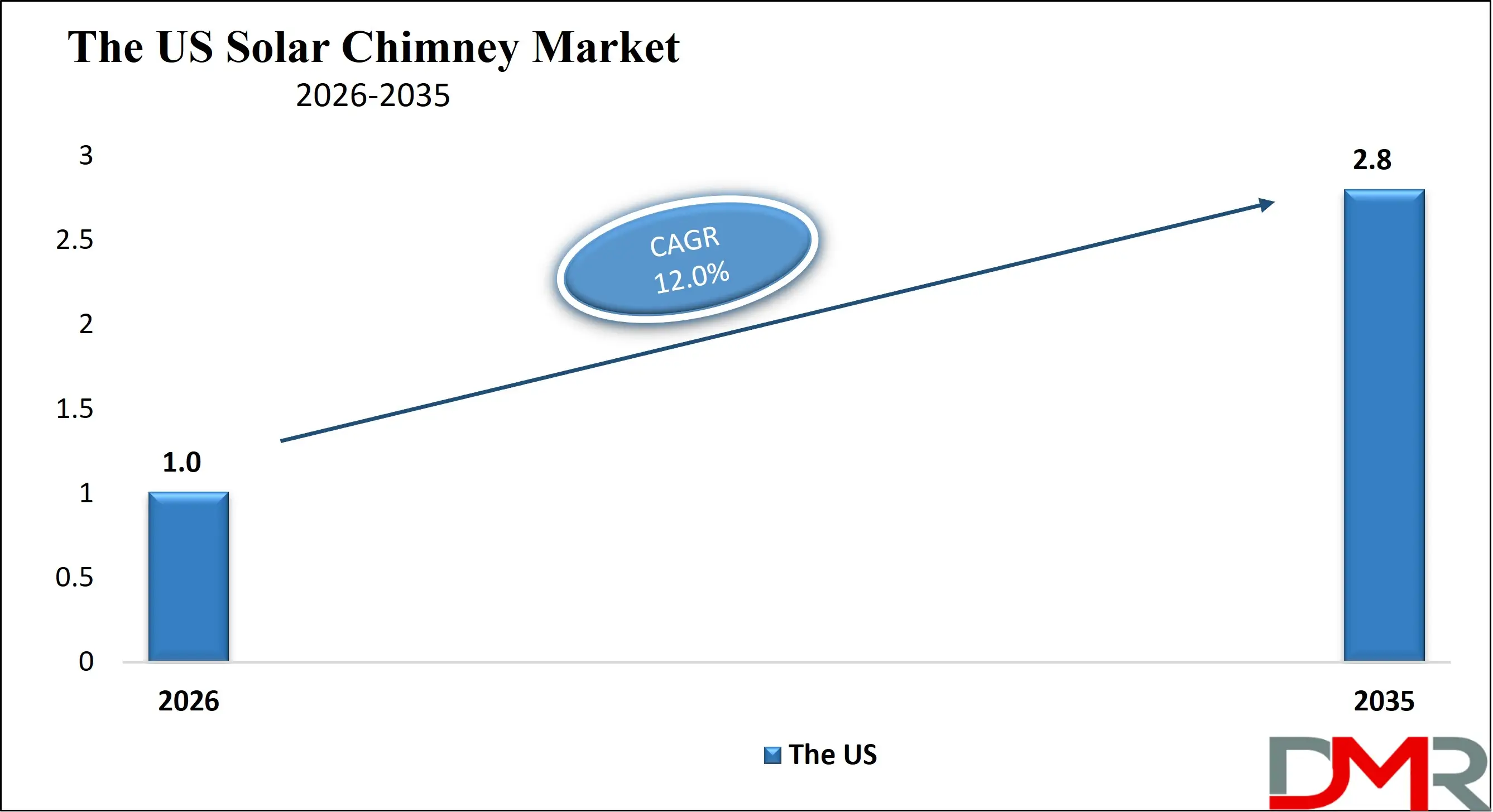

The US Solar Chimney Market

The US Solar Chimney Market size is projected to reach USD 1.0 billion in 2026 at a compound annual growth rate of 12.0% over its forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The US Solar Chimney Market is influenced by strong green building regulations, including state-level energy codes and federal tax incentives supporting renewable integration. Adoption is particularly visible in commercial buildings pursuing LEED certification and net-zero energy targets. Market growth is supported by the rising construction of energy-efficient schools, healthcare facilities, and government buildings. Key participants focus on hybrid systems integrating solar PV and HVAC technologies to enhance return on investment. Government-backed sustainability initiatives, research funding for passive cooling technologies, and climate resilience strategies in warmer states such as California, Texas, and Arizona further accelerate implementation.

Europe Solar Chimney Market

Europe Solar Chimney Market size is projected to reach USD 1.5 billion in 2026 at a compound annual growth rate of 11.8% over its forecast period.

Europe demonstrates steady progress due to stringent carbon reduction goals and frameworks such as the European Green Deal. The region’s emphasis on Nearly Zero-Energy Buildings (NZEB) supports passive ventilation systems like solar chimneys. Countries including Germany, France, and Spain are integrating these systems into public infrastructure and retrofitting projects. Strong regulatory backing, subsidies for renewable installations, and high public awareness of sustainable construction practices contribute to adoption. Innovation is also driven by architectural firms incorporating façade-integrated and hybrid solar chimney solutions into smart city initiatives.

Japan Solar Chimney Market

Japan Solar Chimney Market size is projected to reach USD 200.0 million in 2026 at a compound annual growth rate of 12.2% over its forecast period.

Japan’s Solar Chimney Market is shaped by energy security concerns, urban density, and a national commitment to carbon neutrality. Advanced building technologies and compact urban designs create opportunities for façade-integrated and vertical tower configurations. Government incentives promoting energy-efficient housing and sustainable commercial developments are key growth enablers. Industrial facilities are exploring medium-capacity systems for ventilation efficiency. However, space constraints and high installation costs present challenges. Continued R&D in lightweight materials and hybrid renewable integration is expected to support broader deployment.

Solar Chimney Market: Key Takeaways

- Market Growth: The Solar Chimney Market size is expected to grow by USD 7.3 billion, at a CAGR of 12.8%, during the forecasted period of 2027 to 2035.

- By Type: The building-integrated solar chimneys segment is anticipated to get the majority share of the Solar Chimney market in 2026.

- By Application: The commercial segment is expected to get the largest revenue share in 2026 in the Solar Chimney market.

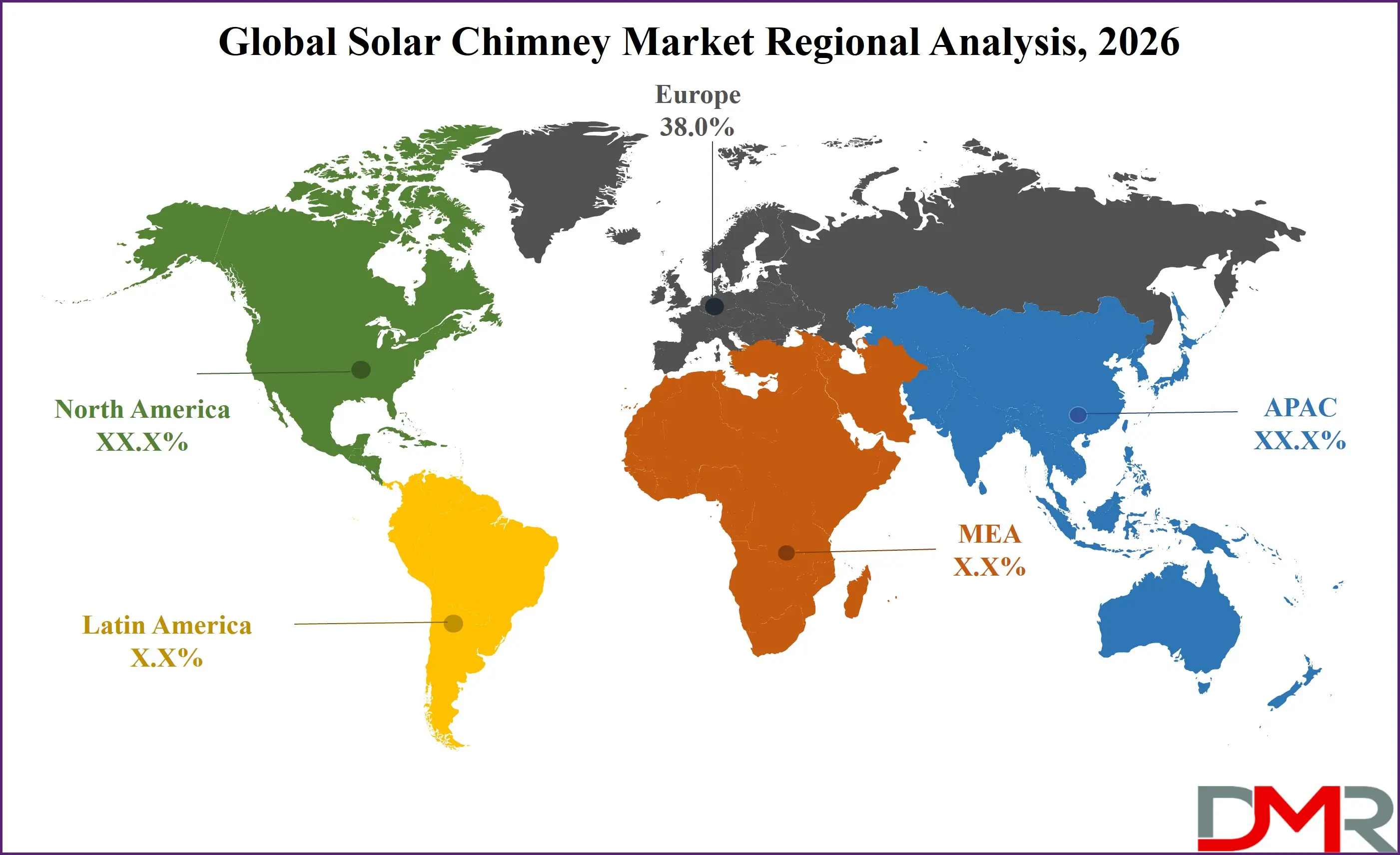

- Regional Insight: Europe is expected to hold a 38.0% share of revenue in the global Solar Chimney market in 2026.

- Use Cases: Some of the use cases of Solar Chimney include smart city infrastructure, hybrid renewable systems, and more.

Solar Chimney Market: Use Cases

- Passive Building Ventilation: Enhances natural airflow in residential and commercial buildings, reducing HVAC energy consumption.

- Industrial Heat Extraction: Removes excess heat from manufacturing plants and warehouses, improving worker safety and energy efficiency.

- Utility-Scale Power Generation: Large solar chimney towers generate electricity through turbine-driven airflow systems.

- Green Building Certification Support: Contributes to LEED and net-zero building performance metrics.

- Smart City Infrastructure: Integrated into sustainable urban planning for improved microclimate control.

- Educational & Healthcare Facilities: Ensures improved indoor air quality with reduced operational costs.

- Hybrid Renewable Systems: Combines with solar PV and HVAC for optimized energy performance.

Stats & Facts

- International Energy Agency reported in 2024 that global renewable electricity generation increased by 8% year-on-year.

- The US Department of Energy stated in 2024 that buildings account for nearly 40% of total energy consumption in the US.

- European Commission noted in 2025 that buildings contribute about 36% of EU carbon emissions.

- International Renewable Energy Agency recorded in 2024 that solar power capacity additions surpassed 300 GW globally.

- The US Energy Information Administration confirmed in 2025 that renewable energy accounted for approximately 24% of US electricity generation.

- Ministry of Economy, Trade and Industry Japan reported in 2024 that renewable energy represented over 22% of national electricity supply.

- United Nations Environment Programme highlighted in 2024 that energy-efficient buildings could reduce global emissions by up to 30% by 2030.

- World Bank stated in 2025 that green building investments are growing at over 10% annually worldwide.

- Eurostat recorded in 2024 that construction output in sustainable building segments rose by 5% year-on-year.

- National Renewable Energy Laboratory reported in 2025 that passive solar cooling technologies can reduce building cooling loads by up to 20%.

Market Dynamic

Driving Factors in the Solar Chimney Market

Growing Demand for Energy-Efficient Buildings

The rising global emphasis on energy-efficient and low-carbon buildings is a major force accelerating the Solar Chimney Market. Increasing electricity prices and stricter building energy regulations are encouraging developers to adopt passive ventilation solutions. Solar chimneys reduce reliance on mechanical cooling systems, cutting operational costs and lowering carbon emissions. Corporate ESG commitments and green building certifications further support adoption. Expanding urbanization in warm regions strengthens the economic and environmental value of passive cooling technologies.

Integration with Hybrid Renewable Systems

The integration of solar chimneys with photovoltaic panels and HVAC systems enhances overall system performance and commercial viability. Hybrid configurations improve airflow efficiency while generating supplemental electricity, strengthening return on investment. Smart sensors and automated building management systems allow real-time airflow optimization. These solutions are increasingly applied in commercial and industrial facilities. Advances in modular construction and performance simulation tools reduce engineering complexity, enabling smoother deployment and broader acceptance across diverse infrastructure projects.

Restraints in the Solar Chimney Market

High Initial Capital Investmen

tSolar chimney installations, especially utility-scale towers, require significant upfront investment. Costs related to structural frameworks, specialized glazing materials, and engineering design often exceed those of conventional ventilation systems. In developing economies, limited access to sustainable financing mechanisms can delay adoption. Extended payback periods may discourage private stakeholders in regions with lower electricity tariffs. These financial challenges can restrict rapid scalability and slow widespread market penetration, particularly in cost-sensitive construction environments.

Technical and Space Constraints

Urban density and architectural limitations can restrict the feasibility of installing solar chimney systems. Vertical tower designs may require structural reinforcements and compliance with strict zoning laws. In colder climates, seasonal temperature variations can reduce operational efficiency. Limited technical expertise in certain regions further complicates design and implementation. These constraints may slow commercialization efforts and increase project complexity, particularly in retrofitting existing buildings or densely populated urban settings.

Opportunities in the Solar Chimney Market

Expansion in Emerging Economies

Rapid urbanization across Asia-Pacific, the Middle East, and Africa presents strong expansion potential. Hot climatic conditions in these regions enhance the effectiveness of passive solar ventilation systems. Government-supported smart city programs and sustainable housing initiatives create favorable conditions for adoption. Increasing awareness of energy efficiency and long-term operational savings strengthens demand. Growing infrastructure development further supports deployment, positioning emerging economies as high-potential growth areas for solar chimney technologies.

Green Infrastructure Investments

Growing investments in sustainable infrastructure projects provide significant growth prospects. Solar chimneys are increasingly integrated into public buildings, transportation hubs, and institutional facilities to meet decarbonization objectives. Climate finance mechanisms and government incentives help offset installation expenses, improving project feasibility. Public-private partnerships also encourage innovation and scalability. As nations prioritize resilient and energy-efficient infrastructure, solar chimney solutions are expected to gain stronger consideration in long-term development planning.

Trends in the Solar Chimney Market

Digital Modeling and Simulation

Advanced computational fluid dynamics tools are transforming solar chimney design and optimization. These digital solutions allow engineers to simulate airflow patterns, thermal performance, and structural efficiency before construction. Accurate modeling reduces project risks and enhances customization for diverse building types. Integration with digital twin platforms improves ongoing monitoring and maintenance efficiency. Such technologies are strengthening investor confidence and accelerating innovation in performance-driven sustainable building solutions.

Hybrid and Multifunctional Designs

There is growing emphasis on multifunctional solar chimney systems that combine ventilation, daylighting, and renewable energy generation. Photovoltaic-integrated and HVAC-linked configurations improve value propositions for commercial projects. Modular and prefabricated components reduce construction timelines and installation costs. Designers are also incorporating aesthetic architectural elements to enhance building appeal. These multifunctional innovations are expanding application scope and supporting broader adoption across residential, commercial, and institutional infrastructure projects.

Impact of Artificial Intelligence in Solar Chimney Market

- Predictive Performance Modeling: AI-driven simulations optimize chimney height, collector size, and airflow rates for maximum efficiency.

- Smart Climate Control: AI integrates with building systems to regulate airflow based on occupancy and temperature patterns.

- Energy Output Forecasting: Machine learning predicts power generation in utility-scale systems.

- Maintenance Optimization: AI-based diagnostics detect airflow blockages or structural stress early.

- Design Automation: Generative AI supports architects in creating energy-efficient chimney configurations.

- Demand Forecasting: AI analyzes construction and climate data to estimate regional demand.

- Operational Efficiency: Real-time analytics enhance hybrid PV-HVAC system coordination.

- Cost Reduction Strategies: AI-driven supply chain optimization reduces material and logistics expenses.

Research Scope and Analysis

By Type Analysis

Building-Integrated Solar Chimneys are projected to account for 62% of the market share in 2026, maintaining dominance due to strong alignment with green building standards and urban sustainability goals. Roof-mounted, wall-integrated, and façade-integrated systems are widely adopted in residential and commercial buildings where space efficiency is essential. These systems are incorporated during the architectural design phase, reducing incremental costs and enhancing structural compatibility. Their ability to lower HVAC energy consumption and support net-zero commitments makes them highly attractive. Growing demand for energy-efficient construction and stricter building codes further solidifies their leadership position globally.

Standalone Solar Chimneys are anticipated to be the fastest-growing type segment, supported by increasing interest in solar chimney power plants and large-scale industrial ventilation applications. These systems operate independently of building structures, making them suitable for industrial zones and utility-scale renewable projects. Advancements in turbine efficiency, airflow optimization, and composite structural materials are improving commercial feasibility. Research initiatives focusing on large-capacity electricity generation models are strengthening long-term prospects. As governments explore alternative renewable technologies for energy diversification, standalone installations are expected to gain stronger momentum across emerging economies and energy-intensive regions.

By Material Analysis

Glass glazing is projected to hold 55% market share in 2026 within the material category due to its superior durability, high solar transmittance, and long operational lifespan. Tempered and low-iron glass variants improve heat absorption efficiency while maintaining structural reliability. Glass is widely preferred in commercial and institutional projects where long-term performance and minimal degradation are critical. Although initial costs are higher than polycarbonate alternatives, lifecycle benefits and recyclability enhance its appeal. Growing emphasis on sustainable construction materials and fire-resistant properties further contributes to glass maintaining dominance in solar chimney installations.

Polycarbonate glazing is expected to be the fastest-growing material segment due to its lightweight structure, flexibility, and lower installation costs. It offers impact resistance and easier handling during construction, making it suitable for residential and retrofitting applications. Technological improvements in UV resistance and thermal performance are enhancing its viability. Developers seeking cost-effective solutions in emerging markets increasingly favor polycarbonate systems. As modular solar chimney installations expand, the demand for lightweight and adaptable glazing materials is projected to accelerate steadily.

By Design Configuration Analysis

Vertical tower designs are projected to capture 48% of the market share in 2026, driven by their strong airflow generation capacity and suitability for both building-integrated and standalone systems. These configurations maximize convection efficiency by increasing height differentials, making them highly effective in warm climates. They are commonly deployed in commercial complexes and pilot power generation projects. Structural advancements in steel and composite reinforcements have improved feasibility and safety compliance. Their scalability and proven thermodynamic efficiency continue to position vertical towers as the dominant configuration across global installations.

Hybrid systems are emerging as the fastest-growing configuration segment, combining solar chimney ventilation with photovoltaic panels or HVAC integration. These systems enhance energy output while optimizing indoor climate control. Growing adoption of smart building technologies and real-time energy management platforms supports their expansion. Hybrid solutions provide stronger financial returns by delivering dual functionality—ventilation and electricity generation. Increasing demand for multifunctional renewable systems in commercial and institutional infrastructure is accelerating innovation and deployment of hybrid configurations worldwide.

By Capacity Analysis

Low-capacity systems are expected to hold 51% market share in 2026, largely due to widespread application in residential and small commercial buildings. These systems focus on passive ventilation and cooling, offering cost-effective and energy-saving alternatives to mechanical HVAC units. Their simpler design and shorter payback period make them attractive for homeowners and property developers. Growing awareness of indoor air quality and sustainable housing further supports demand. As urban housing projects increase globally, low-capacity installations are anticipated to maintain dominant adoption levels.

High-capacity systems represent the fastest-growing capacity segment, primarily driven by research into utility-scale solar chimney power plants. These installations aim to generate renewable electricity alongside ventilation benefits. Technological advancements in turbine integration and collector efficiency are improving commercial viability. Governments exploring diversified renewable portfolios are supporting pilot projects. As demand for alternative clean energy solutions rises, high-capacity systems are expected to witness accelerated investment and technological refinement.

By Application Analysis

Commercial applications are projected to account for 44% of the market share in 2026, driven by office buildings, shopping malls, hospitality establishments, educational institutions, and healthcare facilities. These structures require efficient ventilation systems to maintain occupant comfort and regulatory compliance. Integration with building management systems enhances operational control and energy savings. Corporate sustainability commitments and green certifications are major growth catalysts. Increasing construction of energy-efficient commercial complexes globally reinforces this segment’s leadership position.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Residential applications are the fastest-growing segment due to rising consumer awareness of energy savings and sustainable living practices. Solar chimneys are increasingly integrated into single-family homes and multi-family housing projects. Growing government incentives for green housing and passive design solutions further stimulate demand. Urban heat concerns and rising electricity costs encourage homeowners to adopt natural ventilation technologies. This segment is expected to expand steadily, particularly in warm and densely populated regions.

By End Use Analysis

Green buildings are anticipated to hold 46% market share in 2026, as solar chimneys directly contribute to energy efficiency certifications and carbon reduction goals. Architects and developers incorporate these systems to meet environmental standards and improve building performance ratings. Retrofitting existing structures with passive ventilation solutions also supports segment growth. Policy incentives and ESG reporting requirements further drive demand. As sustainable construction becomes mainstream, green buildings remain the primary end-use sector for solar chimney adoption.

Renewable energy installations represent the fastest-growing end-use segment, supported by increasing exploration of solar chimney power plants and hybrid renewable systems. Integration with photovoltaic arrays and energy storage solutions enhances overall efficiency. Governments seeking diversified clean energy options are funding research and demonstration projects. Technological innovation and scalability improvements are strengthening feasibility. This segment is expected to witness accelerated development as renewable portfolios expand globally.

The Solar Chimney Market Report is segmented on the basis of the following

By Type

- Building-Integrated Solar Chimney

- Roof-Mounted

- Wall-Integrated

- Façade-Integrated

- Standalone Solar Chimney

- Detached Ventilation Structures

- Solar Chimney Power Plants

By Material

- Glazing Material

- Structural Material

- Steel

- Aluminum

- Concrete

- Composite Materials

By Design Configuration

- Vertical Tower Design

- Inclined/Sloped Collector Design

- Hybrid Systems

- Solar PV Integrated

- HVAC Integrated

By Capacity

- Low Capacity (Ventilation-Focused Systems)

- Medium Capacity (Commercial/Industrial Systems)

- High Capacity (Power Generation Systems)

By Application

- Residential

- Single-Family Homes

- Multi-Family Housing

- Commercial

- Office Buildings

- Shopping Malls

- Hotels & Hospitality

- Educational Institutions

- Healthcare Facilities

- Industrial

- Manufacturing Units

- Warehouses

- Processing Plants

- Utility-Scale Power Generation

By End-Use

- Green Buildings

- Sustainable Infrastructure Projects

- Renewable Energy Installations

- Smart City Projects

Regional Analysis

Leading Region in the Solar Chimney Market

Europe is projected to account for 38% of the global market share in 2026, maintaining its leading position due to strong regulatory frameworks and sustainability commitments. Energy efficiency directives and Nearly Zero-Energy Building mandates drive adoption across residential and commercial sectors. Public infrastructure retrofitting and green construction incentives further stimulate deployment. High awareness of passive cooling benefits and access to climate financing enhance market maturity. Continued investments in renewable integration and smart city initiatives reinforce Europe’s dominant role in advancing solar chimney technologies.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Fastest Growing Region in the Solar Chimney Market

Asia-Pacific is expected to be the fastest-growing region, supported by rapid urbanization, rising temperatures, and expanding sustainable infrastructure investments. Countries such as China, India, and Southeast Asian economies are prioritizing energy-efficient housing and industrial development. Favorable climatic conditions improve solar chimney performance, strengthening cost-effectiveness. Government-backed smart city programs and renewable energy targets further accelerate adoption. Increasing construction activity and environmental awareness position Asia-Pacific as a high-growth region in the global solar chimney landscape.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The Solar Chimney Market is moderately fragmented, with companies competing on technological innovation, cost efficiency, and customization capabilities. Strategic partnerships with architectural firms and construction companies enhance project integration. High capital requirements and engineering expertise create entry barriers. Firms invest in R&D to improve hybrid integration and structural materials. Long-term contracts in public infrastructure and green building projects support revenue stability.

Some of the prominent players in the global Solar Chimney are

- EnviroMission Ltd.

- Solar Innovations, Inc.

- Schlaich Bergermann Partner

- Solarventi Ltd.

- Monodraught Ltd.

- Tata Power Solar Systems Ltd.

- Schüco International KG

- HelioDynamics Ltd.

- BASF SE

- Kingspan Group plc

- Solatube International, Inc.

- SolarChimney.com

- Sunvent Industries

- SolarWall (Conserval Engineering Inc.)

- Greenvent Solar

- Solar Air Systems

- Solar Breeze

- Solar Chimney Technologies, Inc.

- Solarfan Systems

- Other Key Players

Recent Developments

- In February 2026, Tesla, Inc. is gaining attention for manufacturing American-built solar panels that strengthen its fully integrated clean energy ecosystem. The development is being described as a major step toward seamless integration of hardware, software, and energy management solutions. Tesla’s solar panels now complement its Powerwall batteries and electric vehicle lineup, allowing the company to offer a comprehensive energy solution while reducing its previous reliance on third-party solar panel suppliers.

- In September 2025, Cologne Bonn Airport launched a pilot photovoltaic project featuring 80 adhesive solar panels installed on the 27-meter chimney of its co-generation plant, covering approximately 70 square meters with south-facing modules mounted along the curved surface. Developed by Heliatek, the lightweight panels use rear-side adhesive technology that removes the need for a substructure and generate up to 4,400 kWh annually, roughly equivalent to a household’s yearly electricity consumption. The HeliaSol 436-2000-CFF modules deliver 50–55 W each at 7.2%–8.0% efficiency, contributing to a total system capacity of about 4 kW, while their ultra-thin and low-weight design makes them suitable for structurally sensitive roofs and facades.