What is the Global Solar Photovoltaic Glass Market Size?

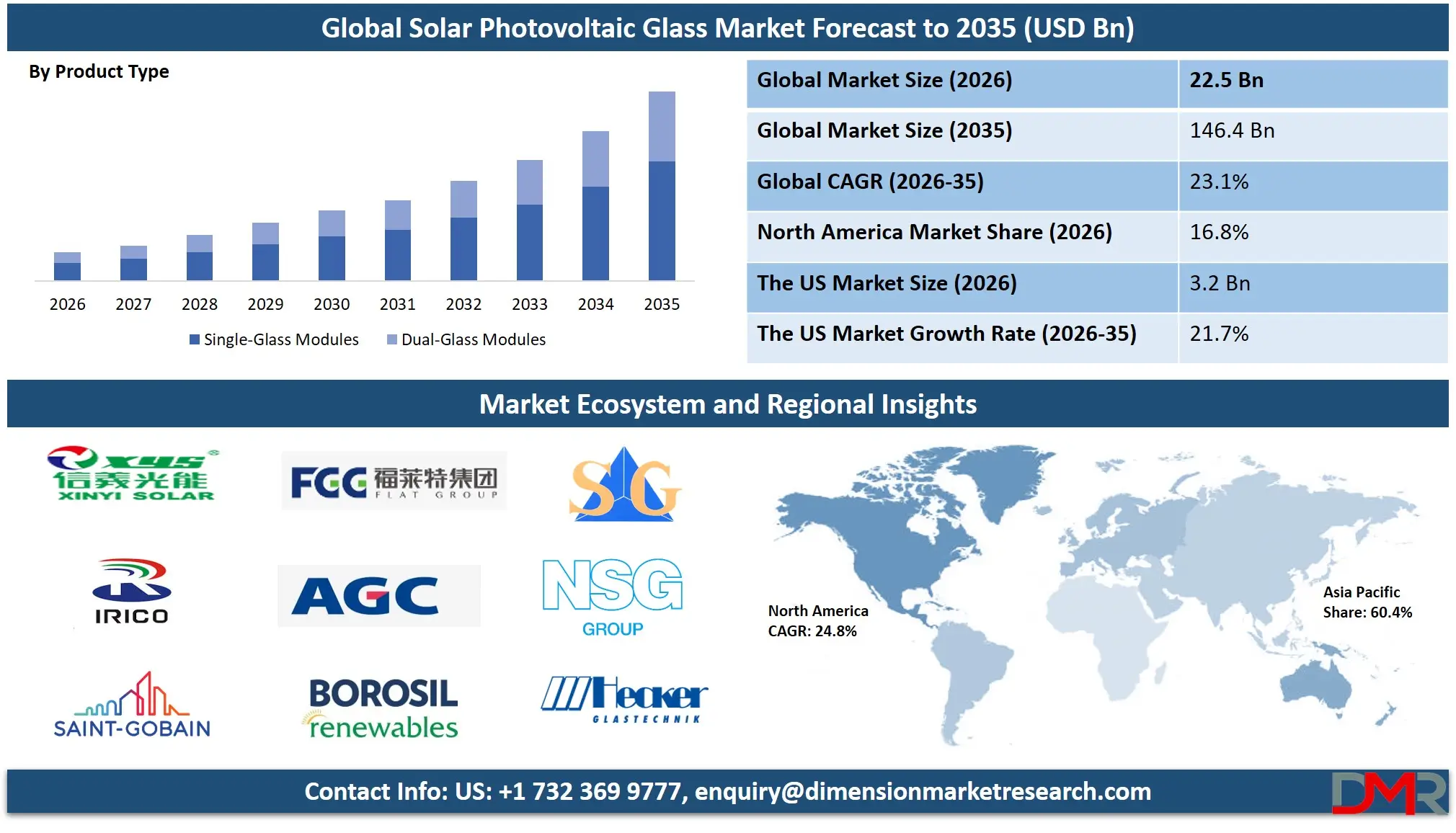

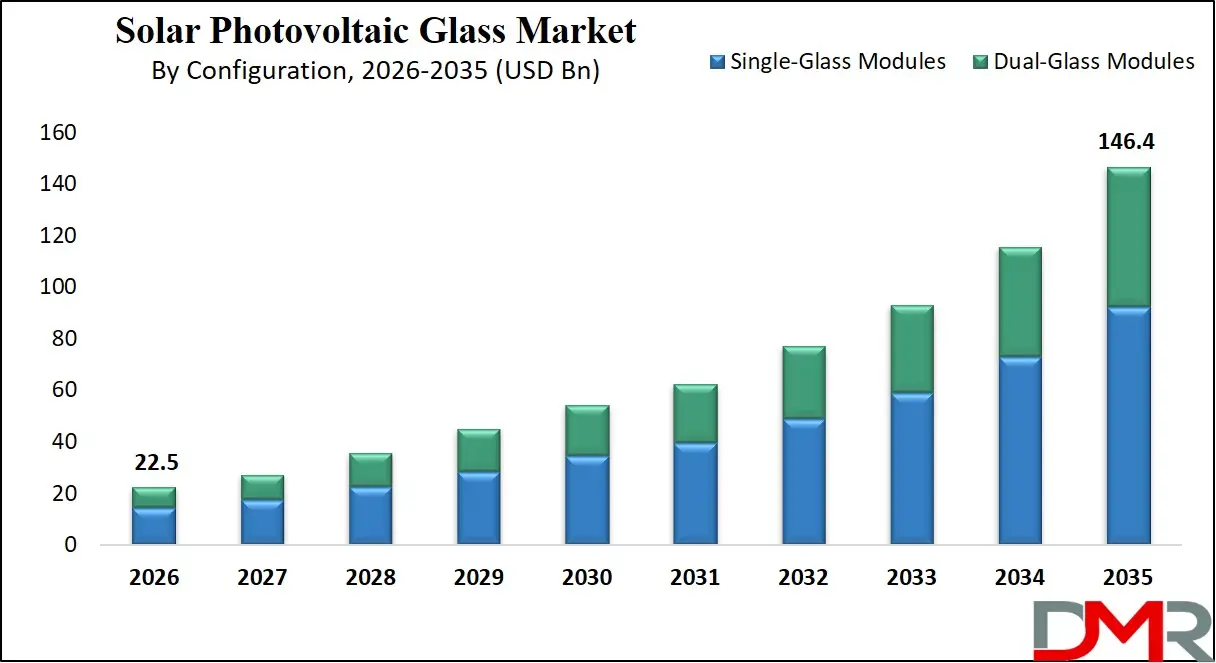

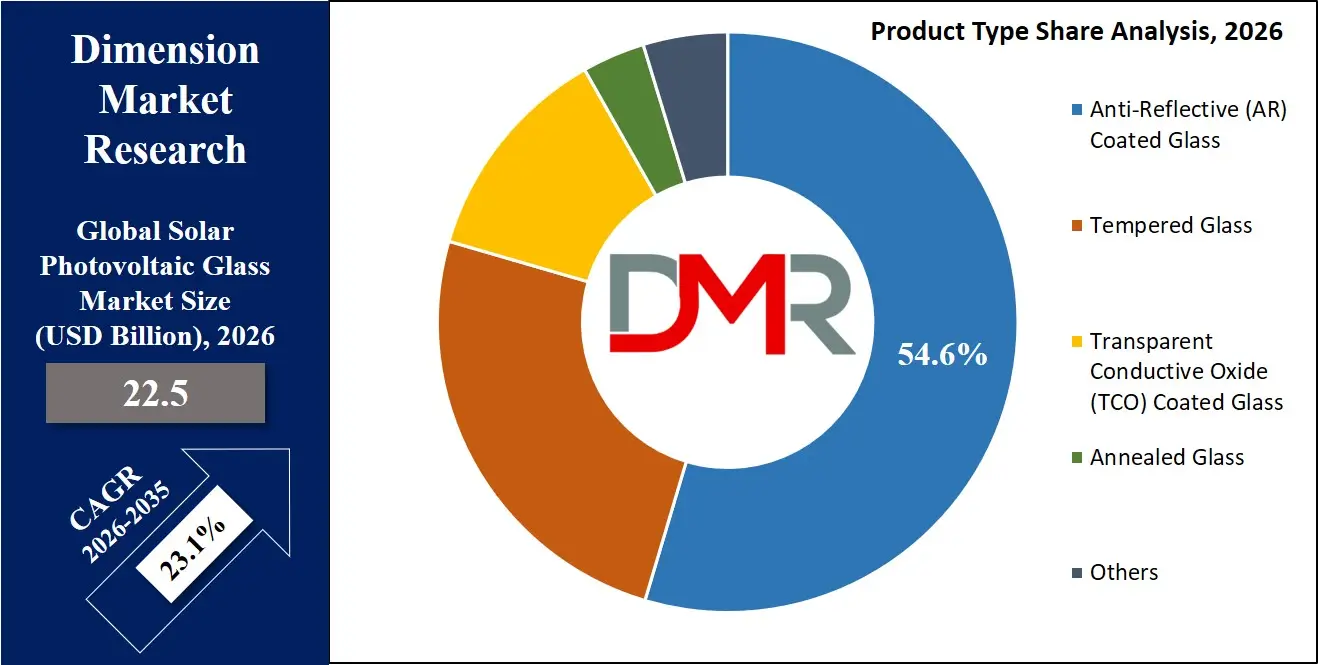

The Global Solar Photovoltaic Glass Market size is estimated at USD 22.5 billion in 2026 and is projected to reach USD 146.4 billion by 2035, growing at a CAGR of 23.1% during the forecast period, driven by AI-optimized glass manufacturing, automation, and integrated performance testing workflows in solar module production.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The growth of the Solar Photovoltaic Glass industry can be attributed to an increase in machine learning techniques for glass coating optimization and thermal management, government mandates that minimize the likelihood of failure of solar modules and shorten the timeline for the development of high-efficiency panels, and higher investment in automated glass production programs by private companies and governments.

Additional factors driving the growth include breakthroughs in real-time glass tempering tracking technologies, optical modeling and prediction, automated anti-reflective coating application, and high-throughput quality screening, among other developments in interoperability systems which facilitate PV glass integration in module manufacturing operations. Digital modernization in energy and industrial solar companies has helped optimize glass thickness design and improve process outcomes, including reduced time to production. Automation of the workflows, predictive processes, and artificial intelligence-enabled design-test-validate systems have accelerated adoption, and renewable energy national strategies have supported sustainability in solar manufacturing.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The US Solar Photovoltaic Glass Market

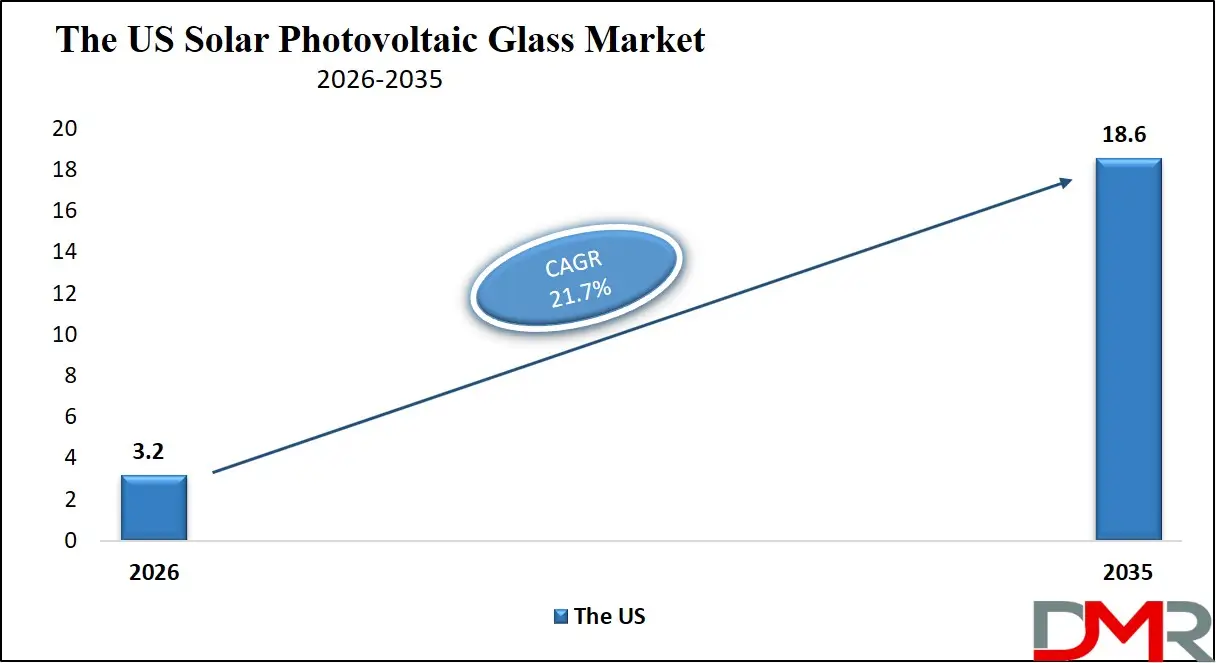

The US Solar Photovoltaic Glass Market is estimated to grow to USD 3.2 billion in 2026 with a compound annual growth rate of 21.7% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The US market is defined by the existence of significant federal funding schemes like the Solar Energy Technologies Office (SETO), the US Department of Energy's advanced manufacturing programs, the NREL-led PV module testing frameworks, all of which will help the development of the necessity of AI-driven glass engineering, real-time production telemetry of automated tempering lines and robotic handling systems, and predictive quality software. Automated PV glass manufacturing systems remain to be more rapidly adopted in the region, and the US needs highly developed interoperability frameworks, integration of real-world evidence using digital manufacturing logs, and verifiable PV glass AI assurance. Also, service providers are being pressured by initiatives like the Inflation Reduction Act (IRA) and national AI in manufacturing strategies to create dedicated integration and deployment services to guarantee data interoperability, quality assurance, and compliance across a variety of solar module manufacturing departments and academic research centers.

Europe Solar Photovoltaic Glass Market

The Europe Solar Photovoltaic Glass Market is estimated to be valued at USD 3.6 billion in 2026, witnessing growth at a CAGR of 20.6%, during the forecast period.

The solar PV glass market is mature in Europe, and it has a strong effect on the regulatory specifications and the regional policies including the EU Solar Energy Strategy, the European PV Manufacturing Pilot Lines, and national digital energy programs (e.g., the France-PV Glass Initiative and the German Energiewende 2030 strategy). Another area that countries are working towards is smart glass modularization in order to align research and production workload demands and interoperability of cross-border module manufacturing data supply chains. It is driven by advanced technologies, such as real-time optical design engines and high-reliability thermal stress scoring systems with an inbuilt predictive algorithm on the development of engineered glass coatings. Adoption is facilitated by the use of public-private partnerships and harmonization of PV glass standards. Technologies like real-time computational workload balancing and smart contract-based data sharing are commonly practiced as research-centric programs, and Europe is a frontrunner in terms of the digital transformation of safe and efficient PV glass-enabled solar manufacturing.

Japan Solar Photovoltaic Glass Market

The Japan Solar Photovoltaic Glass Market is projected to be valued at USD 720.1 million in 2026, progressing at a CAGR of 18.9%, during the period spanning from 2026 to 2035.

Japan boasts a mature solar PV glass market supported by high-performance automated glass coating systems, diagnostic integration technology, and a wide network of robotic glass processing AI innovations. Automation, precision, and process integrity are the priorities in the country and are achieved by predictive optical performance models and intelligent process management systems for glass tempering. Growth is stimulated by government actions under the Green Growth Strategy and constant investment in digital solar manufacturing infrastructure. The high volume of PV module R&D, industrial glass development for high-transmittance panels, and glass lab automation requires efficient AI for real-time evidence-based inference. The difficulties are high validation costs for new PV glass automation architectures and integration with legacy glass processing systems, yet the prospects are in exporting developed PV glass technologies to Asian and Pacific markets.

Key Takeaways

- Market Size & Forecast: The Global Solar Photovoltaic Glass Market is estimated to be valued at USD 22.5 billion in 2026 and is expected to grow to USD 146.4 billion by 2035.

- Growth Rate & Outlook: The market is expected to witness growth at a compound annual growth rate of 23.1% in the forecast period.

- Primary Growth Drivers: Technological progress in machine learning-based engineering of glass coatings for solar modules; regulatory requirements for faster module development and reduced failure rates; and industrial deployment of intelligent PV glass manufacturing platforms are some of the key drivers of growth in the market.

- Key Market Trends: The use of predictive optical outcome monitoring, real-time tempering optimization, and transition to cloud-based glass production telemetry and fleet management systems are some of the primary market trends.

- By Product Type: The Anti-Reflective (AR) Coated Glass segment is anticipated to get the majority share of the solar PV glass market in 2026.

- By Configuration: The Dual-Glass Modules segment is expected to occupy the largest revenue share in 2026 in the solar PV glass market.

- By Technology: The Crystalline Silicon Photovoltaic Technology segment (specifically Monocrystalline Silicon) is expected to get the largest revenue share in 2026 in the solar PV glass market.

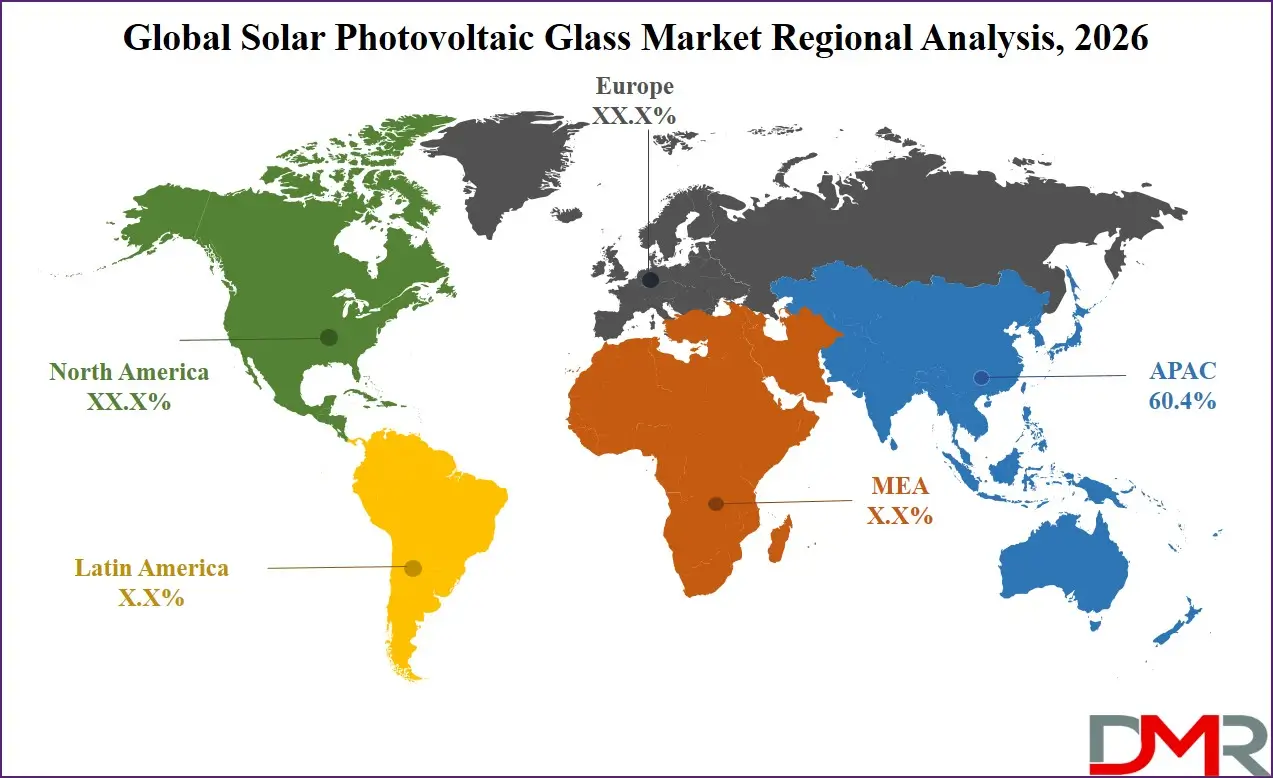

- Regional Leadership: Asia Pacific is predicted to dominate the market with an estimated 60.4% share in 2026.

What is Solar Photovoltaic Glass?

Solar Photovoltaic Glass refers to a specialized, high-transmittance glass product used as a protective cover or substrate in solar panels, combining thermal tempering, anti-reflective coatings, and conductive layers to maximize light absorption and electrical output. These products use automated cutting, tempering furnaces, coating application systems, and quality analytics to enable rapid module assembly, improved optical accuracy, and accelerated prototyping and scale-up of solar manufacturing. PV glass is increasingly used in utility-scale solar farms and building-integrated photovoltaics (BIPV) to enhance energy conversion efficiency, support sustainability, and advance the production of high-performance solar modules.

Use Cases

- Glass Optimization for High-Efficiency Modules: PV glass manufacturers are capable of designing high-throughput coating configurations in real-time to discover an optimal transmission glass for monocrystalline and bifacial modules with latency on the order of weeks, saving orders of magnitude over time compared with manual optical screening.

- Thermal & Optical Pathway Optimization: Long-term field exposure and performance data, such as cumulative light transmission and soiling accumulation, are modeled to give process adjustment recommendations and keep safely managing production runs without interruption to ensure module stability and manufacturing confidence.

- Tempering Line Monitoring & Control: Industrial deployments are employing machine learning and furnace analytics to perform on-device real-time strength prediction, process anomaly detection, and automated heat adjustment with quantifiable and proven accuracy.

- Population Health & Government Programs: More efficient PV glass manufacturing contributes to the success of solar energy innovation, grid decarbonization, and smart module surveillance, facilitates national renewable energy adoption, contributes to deployment reliability, and helps implement policies, such as the PV glass governance policy and solar manufacturing standards.

How AI Is Transforming the Global Solar Photovoltaic Glass Market?

Artificial intelligence is revolutionizing the field of PV glass manufacturing, allowing predictive modeling of the likelihood of optical performance success, automatic detection of anomalies in tempering data patterns, and optimization of glass coating parameters in a module-specific scenario. Furnace-generated telemetry and optical measurement data can be processed using AI algorithms to identify any degradation or performance drift and optimize production outcomes at scale. This saves time, is verifiable and cheaper than manual data analysis.

Moreover, AI enhances quality assurance through offering adaptive computational event-based scheduling, anticipating workflow threats to optical accuracy, and intelligent prioritization of glass line health monitoring. It is also involved in reducing the cost of baseline testing and ongoing performance tracking, allowing solar manufacturing IT operators to reduce the cost and physical footprint of on-prem test campaigns and improve the reliability of PV glass production workloads and their financial returns.

Market Dynamics

Key Drivers of the Global Solar Photovoltaic Glass Market

Rapid developments in Machine Learning and Real-Time Production Inference

The market is being pushed by a fast uptake of AI-driven glass and process optimization, high-efficiency manufacturing data processing, API-based interoperability with manufacturing execution systems (MES), and real-time telemetry analytics from tempering furnaces. These technologies enable monitoring of the performance of PV glass systems in real-time, identify process anomalies early, predict optical transmission rates, and simplify the process of experimental validation. Consequently, operational uptime and R&D efficiency are highly enhanced while minimizing the costs of manual data analysis. The growth of machine learning models for glass coating design, in particular, is also accelerating the need for intelligent PV glass automation, as solar manufacturers are increasingly adopting automation and workflow optimization based on production data.

Growing Focus on Module Regulation and Sustainable Manufacturing

The world is increasingly focused on solar module safety and quality, with governments and regulatory bodies introducing manufacturing efficiency frameworks, such as the EU Solar Strategy provisions and the US DOE's Advanced Manufacturing Technologies framework for solar panels. These structures are driving demand for efficient PV glass automation capable of supporting real-time process monitoring and continuous learning. In parallel, global initiatives promoting solar manufacturing standardization and workforce development are encouraging the adoption of evidence-based PV glass architectures. The increasing focus on transparency in glass design and reduction in production failure rates is also enhancing the necessity of reliable and scalable PV glass automation in both public and private solar manufacturing systems.

Restraints in the Global Solar Photovoltaic Glass Market

High Costs of Integration and Process Validation

PV glass platforms are expensive and time-intensive to implement, need to be heavily tested in production settings, and process logic reliability is tested, and long-term performance evaluation of new components is needed. Also, regulatory limitations and data privacy regulations (e.g., trade secret protections for coating formulas) add to the complexity and cost of deployment. These aspects pose barriers to entry, lengthen deployment, and raise initial capital investments.

Limited Standardization Across Manufacturing Data and Workflows

The industry continues to rely on multiple PV glass automation architectures, including robotics-based handling, AI-based for thermal optimization, and computer vision-based for defect detection. However, the lack of standardized glass manufacturing data interfaces remains a key challenge. PV glass lacks universal plug-and-play standards compared to traditional glass processing modules, making integration complex and limiting interoperability of PV glass models across different R&D and production systems.

Growth Opportunities in the Global Solar Photovoltaic Glass Market

Expansion of Emerging Solar Manufacturing Programs

Developing solar markets such as Brazil, Indonesia, Nigeria, the UAE, and Vietnam are investing in digital renewable energy infrastructure and advanced PV glass capabilities. These regions present strong growth potential due to increasing demand for automated glass coating development, tempering monitoring, and remote production consultation applications. With limited legacy glass processing infrastructure, they provide opportunities for the deployment of modern PV glass automation optimized for R&D and manufacturing environments.

Rising Demand for Cloud-Based PV Glass Deployment

The increased requirement for advanced PV glass automation is being generated by the growth of remote R&D collaboration, distributed solar manufacturing, and real-time production control applications. These technologies play a vital role in virtual PV glass platforms, remote production facilities, and solar innovation hubs. With the rising importance of sub-hour process latency as a major production concern, cloud-based PV glass inference capabilities are likely to be fundamental to future solar manufacturing and renewable energy IT infrastructure.

Global Solar Photovoltaic Glass Market Trends

Predictive Optical Outcome Monitoring and Computational Analytics

PV glass platforms are being monitored and process logic anomalies are detected in real time, and performance degradation patterns are predicted using on-system learning. The use of digital twin models of optical transmission and machine learning algorithms is enhancing production workflow scheduling, system lifespan, and deployment reliability. This shift is transforming PV glass management from manual data review to a fully automated, continuously optimized system for monitoring.

Cloud-Based Telemetry and Fleet Management Systems

Cloud computing and digital twin technologies are taking centre stage in the operations of PV glass manufacturing clusters. These platforms enable real-time storage and analysis of production performance data, centralized fleet management of automated processing lines, and remote monitoring of glass line health. Cloud-based systems enhance transparency, lower on-prem infrastructure expenses, and provide quicker responses to workflow changes across manufacturing sites, as experienced by operators of large PV glass networks.

Research Scope and Analysis

By Product Type Analysis

The Anti-Reflective (AR) Coated Glass segment is expected to remain the largest in 2026, accounting for about 54.6% of the global solar PV glass market, driven by its dominant use in large-scale utility modules, seamless manufacturing integration, and flexibility across diverse solar frameworks where real-time light transmission data and coating ecosystem maturity are essential.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Meanwhile, the Tempered Glass segment is witnessing strong growth, driven by rising demand for high-strength protective covers in R&D and production settings where real-time impact resistance and process reproducibility are critical. Adoption is further supported by workflow optimization, real-time efficiency improvements, and modular configurations that integrate multiple process logic types for improved workflow flexibility and operator satisfaction.

By Configuration Analysis

The Dual-Glass Modules segment is expected to account for 58.4% share in 2026, as solar manufacturers heavily rely on dual-glass structures for bifacial cells and enhanced durability. The segment is further supported by increasing deployment of lightweight glass sheets, anti-soiling coatings, and integrated weatherproofing platforms that enhance energy yield and operational efficiency across utility and BIPV applications. It is also among the fastest-growing segments in the PV glass market, driven by rapid adoption of bifacial module architectures and scalable glass lamination infrastructure.

By Technology Analysis

The Crystalline Silicon Photovoltaic Technology segment is expected to dominate with around 68.5% market share in 2026, driven by the critical need for high-transmittance glass for PERC and TOPCon cells in solar manufacturing. PV glass supports monocrystalline scenarios due to its ability to provide consistent optical performance, delivering rapid light capture while maintaining process data within production systems. The Thin-Film Photovoltaic Technology segment (specifically Cadmium Telluride), while smaller, is witnessing strong growth, driven by specialized glass requirements where lower upfront costs and integration with existing substrate infrastructure are required. The Perovskite Photovoltaic Technology segment has the fastest development due to emerging encapsulation needs.

By Application Analysis

The Utility-Scale Solar Installations segment represents the largest application in 2026, accounting for 51.1% share, driven by large-scale projects requiring highly durable, high-transmittance glass for maximum energy yield and long-term reliability. Residential Rooftop Installations form the second-largest segment, utilizing lightweight tempered glass for ease of installation and safety. The fastest-growing area is Building-Integrated Photovoltaics (BIPV) (specifically Facades), adopting PV glass for architectural aesthetics and energy generation. Commercial & Industrial (C&I) Rooftop Installations are emerging for cost-effective solar deployment.

By End-Use Analysis

The Solar Energy Industry segment represents the largest end-user in 2026, accounting for 70.3% share, driven by high-volume demand for PV glass in module assembly for utility, residential, and commercial projects. The Building & Construction Industry forms the second-largest segment, utilizing PV glass for BIPV applications such as curtain walls and skylights. The fastest-growing area is Infrastructure Development, adopting PV glass for solar-powered transportation and public infrastructure. The Automotive Industry is emerging for solar glass in electric vehicle rooftops and auxiliary power systems.

The Global Solar Photovoltaic Glass Market Report is segmented based on the following:

By Product Type

- Anti-Reflective (AR) Coated Glass

- Tempered Glass

- Transparent Conductive Oxide (TCO) Coated Glass

- Annealed Glass

- Others

By Configuration

- Single-Glass Modules

- Dual-Glass Modules

By Technology

- Crystalline Silicon Photovoltaic Technology

- Monocrystalline Silicon

- Polycrystalline Silicon

- Thin-Film Photovoltaic Technology

- Cadmium Telluride (CdTe)

- Amorphous Silicon (a-Si)

- Copper Indium Gallium Diselenide (CIGS)

- Perovskite Photovoltaic Technology

- Other Emerging Technologies

By Application

- Utility-Scale Solar Installations

- Residential Rooftop Installations

- Commercial & Industrial (C&I) Rooftop Installations

- Building-Integrated Photovoltaics (BIPV)

- Facades

- Curtain Walls

- Skylights

- Others

By End Use

- Solar Energy Industry

- Building & Construction Industry

- Automotive Industry

- Infrastructure Development

- Others

Regional Analysis

Leading Region in the Solar Photovoltaic Glass Market

It is projected that Asia-Pacific will take the lead in the global solar PV glass market, covering a market share of about 60.4% in the year 2026. The region's dominance is driven by massive solar module production capacity concentrated in China, India, and Southeast Asia, strong government support through national solar missions and manufacturing subsidies, low-cost production advantages for tempered and coated glass, and the presence of key PV glass vendors and solar cell manufacturers.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The widespread adoption of advanced automation and high-throughput glass processing lines for utility-scale, residential, and BIPV applications further strengthens Asia-Pacific's leading position in the market. Additionally, continuous investments in expanding domestic glass manufacturing capacity and integrated solar supply chains are further reinforcing regional dominance.

Fastest-Growing Region in the Solar Photovoltaic Glass Market

North America is the fastest-growing region, supported by aggressive re-shoring of solar manufacturing under the Inflation Reduction Act (IRA), strong domestic content bonus incentives for U.S.-made PV glass, increasing investments in new glass production facilities in the U.S. and Mexico, and growing adoption of automated glass coating systems. The region benefits from well-established industrial glass manufacturing expertise for high-performance products, increasing commercial participation from domestic and foreign suppliers, and alignment with national energy security roadmaps. Countries across the region are actively deploying new PV glass lines to reduce import dependence and strengthen domestic solar infrastructure. Growing emphasis on advanced AR coating technology and structured process logic development further accelerates market expansion in the region. Moreover, increasing federal tax credits and commercial solar commitments are expected to sustain high growth momentum.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The solar photovoltaic glass market is highly competitive, with innovation and strategic alliances shaping the competitive environment. In order to achieve a competitive advantage, companies and research labs are focused on the development of advanced automation architectures (e.g., AI-based coating design, robotics for high-throughput handling, and machine learning for tempering optimization), AI-powered production telemetry, and digital twin-enabled process monitoring platforms. There are high barriers to entry due to capital-intensive process validation infrastructure, specialized glass engineering expertise, and the need for mature software ecosystems and solar manufacturing regulatory and procurement compliance.

Strategic approaches in the market to increase market presence include partnerships with solar module manufacturers and energy companies, mergers between automation solution providers and system integrators, and long-term supply contracts with R&D labs and academic institutions. Moreover, research and development in interoperability frameworks and scalable software architectures are important factors in maintaining competitiveness and addressing the evolving needs of the solar energy community.

Some of the prominent players in the Global Solar Photovoltaic Glass Market are:

- Xinyi Solar Holdings Limited

- Flat Glass Group Co., Ltd.

- CSG Holding Co., Ltd.

- IRICO Group New Energy Company Limited

- AGC Inc.

- Nippon Sheet Glass Co., Ltd.

- Compagnie de Saint-Gobain S.A.

- Guardian Industries Holdings (Koch Industries Company)

- Taiwan Glass Industry Corporation

- Borosil Renewables Limited

- Jinjing Group Co., Ltd.

- Qingdao Jinxin Glass Co., Ltd.

- Anhui Anci Hi-Tech Co., Ltd.

- AVIC Sanxin Co., Ltd.

- Guangdong Golden Glass Technologies Limited

- Henan Huamei Cinda Industrial Co., Ltd.

- Interfloat Corporation

- Hecker Glastechnik GmbH & Co. KG

- Şişecam Flat Glass Sanayi ve Ticaret A.Ş.

- Onyx Solar Group LLC

- Other Key Players

Recent Developments

- January 2026: Xinyi Solar Holdings Limited successfully commissioned a new 1,200 T/D photovoltaic glass furnace in Indonesia to expand Southeast Asia supply and reduce regional solar module bottlenecks, strengthening its global leadership in ultra-clear PV glass manufacturing.

- October 2025: AGC Inc. initiated a strategic circular economy collaboration with NPC Incorporated to recycle solar panel cover glass into architectural flat glass, advancing sustainability and closed-loop PV glass production systems.

- June 2025: Compagnie de Saint-Gobain S.A. announced a strategic partnership with a leading solar module manufacturer to co-develop laminated photovoltaic glass for building-integrated photovoltaics (BIPV), enhancing efficiency and aesthetic solar building solutions.

- March 2025: Nippon Sheet Glass Co., Ltd. began commercial production of advanced transparent conductive oxide (TCO) coated solar glass at its Pilkington North America facility, strengthening its high-performance PV glass supply chain for global solar manufacturers.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 22.5 Bn |

| Forecast Value (2035) |

USD 146.4 Bn |

| CAGR (2026-2035) |

23.1% |

| The US Market Size (2026) |

USD 3.2 Bn |

| Historical Period |

2021 – 2025 |

| Forecast Period |

2027 – 2035 |

| Base Year |

2025 |

| Estimated Year |

2026 |

| Segments Covered |

By Product Type (Anti-Reflective (AR) Coated Glass, Tempered Glass, Transparent Conductive Oxide (TCO) Coated Glass, Annealed Glass, Others), By Configuration (Single-Glass Modules, Dual-Glass Modules), By Technology (Crystalline Silicon Photovoltaic Technology (Monocrystalline Silicon, Polycrystalline Silicon), Thin-Film Photovoltaic Technology (Cadmium Telluride (CdTe), Amorphous Silicon (a-Si), Copper Indium Gallium Diselenide (CIGS)), Perovskite Photovoltaic Technology, Other Emerging Technologies), By Application (Utility-Scale Solar Installations, Residential Rooftop Installations, Commercial & Industrial (C&I) Rooftop Installations, Building-Integrated Photovoltaics (BIPV) (Facades, Curtain Walls, Skylights), Others), By End Use (Solar Energy Industry, Building & Construction Industry, Automotive Industry, Infrastructure Development, Others) |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Global Solar Photovoltaic Glass Market?

▾ The Global Solar Photovoltaic Glass Market size is estimated to have a value of USD 22.5 billion in 2026 and is expected to reach USD 146.4 billion by the end of 2035.

What is the CAGR of the Global Solar Photovoltaic Glass Market from 2026 to 2035?

▾ The market is growing at a CAGR of 23.1% over the forecasted period.

What factors are driving the growth of the Global Solar Photovoltaic Glass Market?

▾ The market is driven by advances in machine learning-based glass coating and optical engineering and real-time manufacturing data generation, regulatory pressure to accelerate module development and reduce production failure rates, and increasing government investment in national renewable energy infrastructure.

What are the major trends in the Global Solar Photovoltaic Glass Market?

▾ The key market trends include the adoption of predictive optical outcome monitoring and real-time tempering control, along with a growing shift toward cloud-based PV glass platforms and telemetry-enabled workflow management systems.

Which region held the largest share of the Global Solar Photovoltaic Glass Market in 2026?

▾ Asia-Pacific is expected to account for the largest market share in 2026, with a share of about 60.4%.

Which region is expected to grow the fastest in the Global Solar Photovoltaic Glass Market?

▾ North America is the fastest-growing region in the market during the forecast period.

Who are the key players in the Global Solar Photovoltaic Glass Market?

▾ Some of the major key players in the Global Solar Photovoltaic Glass Market are Xinyi Solar Holdings Limited, Saint-Gobain S.A., AGC Inc., Borosil Renewables Limited, Nippon Sheet Glass Co., Ltd., and many others.

How is the Global Solar Photovoltaic Glass Market segmented?

▾ The market is segmented by product type, configuration, technology, application, and end use.