What is the Sovereign Cloud Market Size?

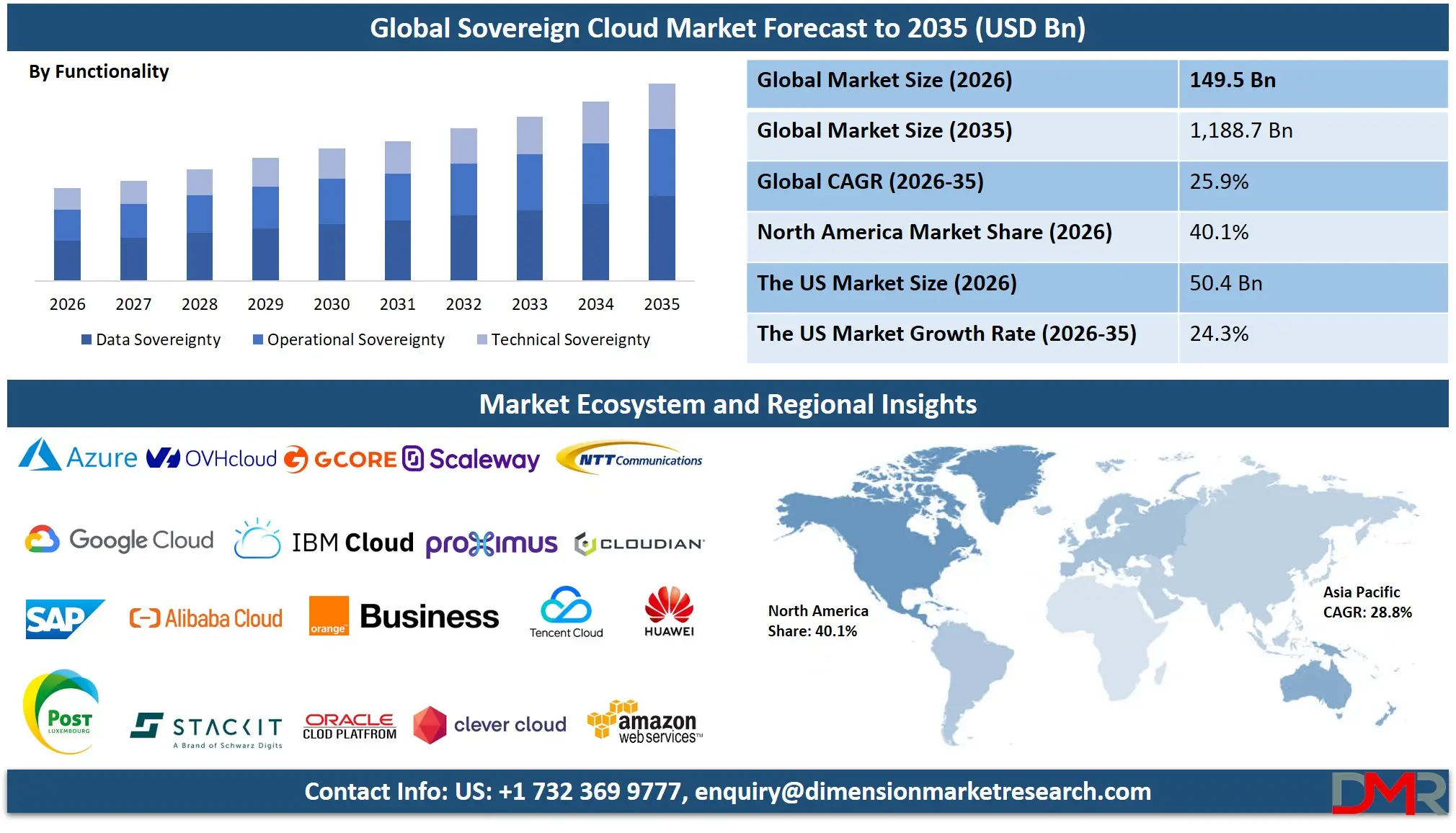

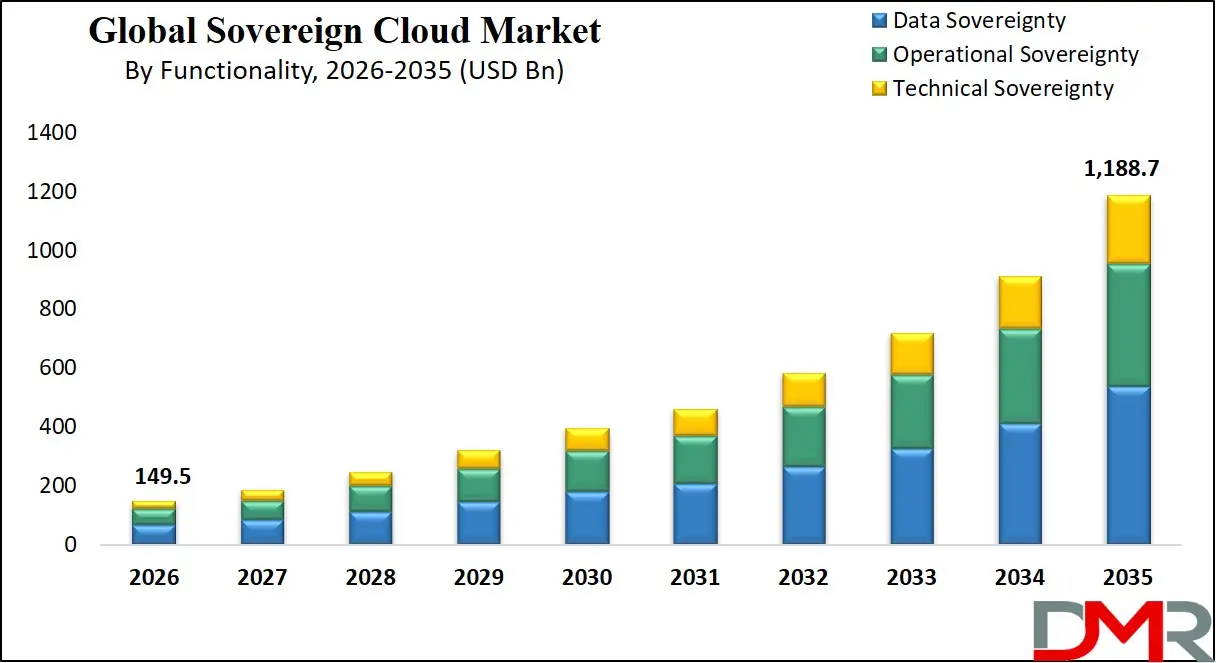

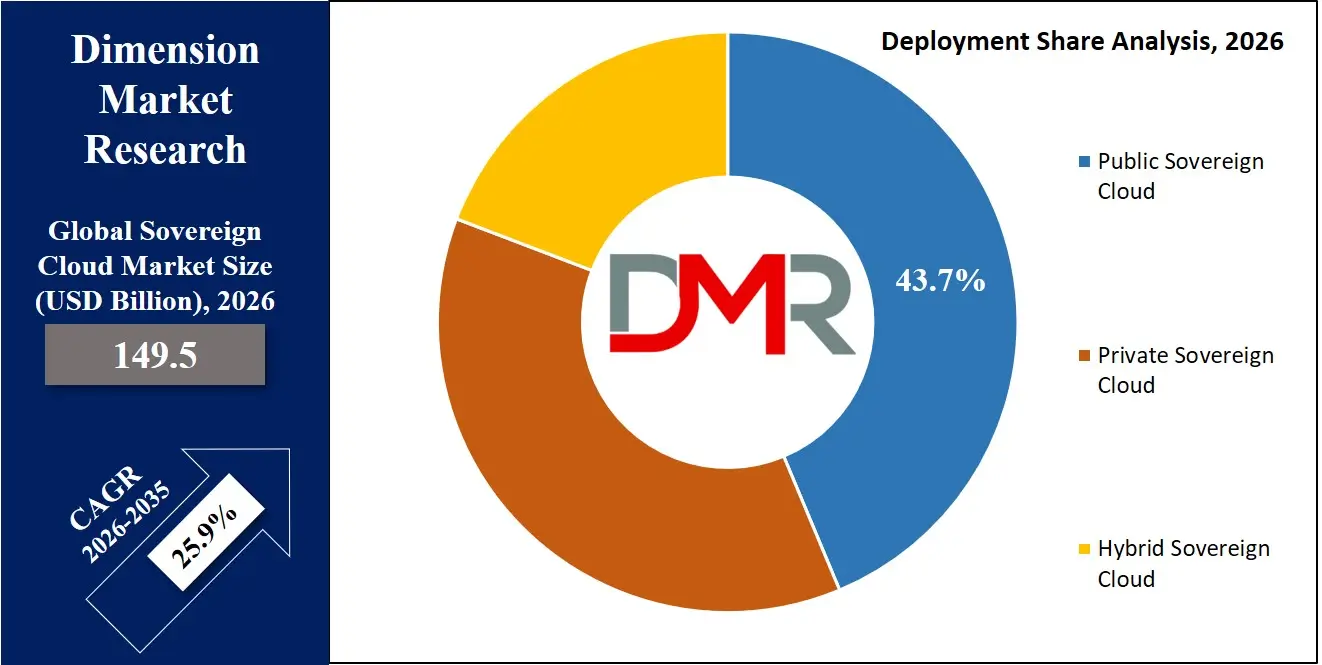

The Global Sovereign Cloud Market is expected to reach a value of USD 149.5 billion in 2026, and it is further anticipated to reach USD 1,188.7 billion by 2035, growing at a CAGR of 25.9% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Sovereign cloud market has been enjoying an exponential growth as countries and businesses are increasingly valuing data residency, jurisdictional control, and digital autonomy in a world characterized by growing geopolitical stresses and strict regulatory environments. The market includes cloud-based infrastructure and services that keep the data inside definite national or regional borders, and that are only under the jurisdiction of local laws and governance systems.

Sovereign cloud solutions are a response to the urgent requirement of operational autonomy in relation to foreign jurisdiction, the protection of sensitive government data, information about citizens and other strategic corporate resources against extraterritorial jurisdiction. The rising pace of data localization legislation, increasing foreign intelligence surveillance fears, and the need to have continuous digital services in times of geopolitical upheavals are overwhelming the current demand in sovereign cloud architectures in all models of public, private, and hybrid deployments.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The US Sovereign Cloud Market

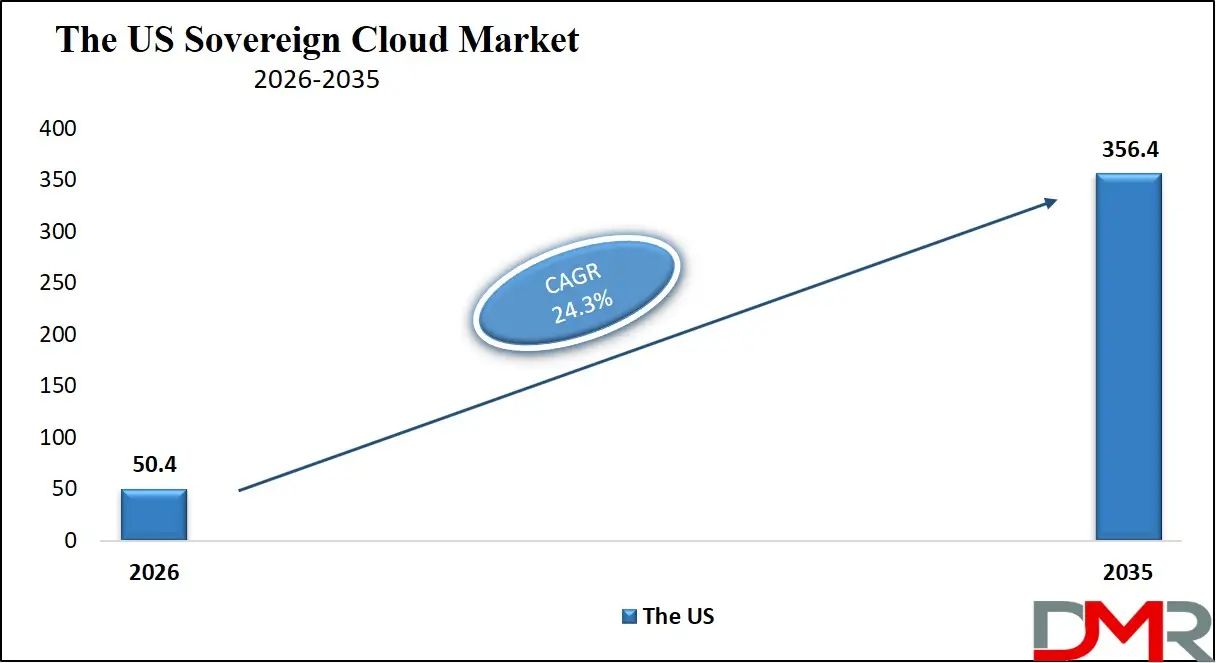

The US Sovereign Cloud Market is projected to reach USD 50.4 billion in 2026 at a compound annual growth rate of 24.3% over its forecast period, which is forecasted to be value of USD 356.4 billion by 2035. The US is a dominating player in the sovereign cloud environment, which is supported by the aggressive approach of the federal government on its Cloud Smart strategy and strict certification of the maturity model of cybersecurity by the Department of Defense.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

This market has been defined by significant investments in private sovereign cloud deployments of classified workloads and sensitive defense applications and increasing use of government-certified public sovereign cloud environments to FedRAMP High and DoD Impact Level 6 standards. Moreover, the growth of state in the form of data protection regulations and critical infrastructure security mandates is further generating parallel demand on sovereign cloud solutions in state and local government agencies as well as highly regulated private sector organizations in the defense contracting, aerospace, and financial services sectors.

The Europe Sovereign Cloud Market

The Europe Sovereign Cloud Market is estimated to be valued at USD 43.6 billion in 2026 and is further anticipated to reach USD 334.2 billion by 2035 at a CAGR of 25.4%.

Europe is the most mature and advanced regulatory-based sovereign cloud market in the world, basically influenced by the General Data Protection Regulation and the developing European Data Governance Act. The market dynamics of the region are inimably shaped by the initiatives like GAIA-X that aims to create a federated and interoperable European data infrastructure ecosystem that ensures data sovereignty and portability across member states. The deployment of Hybrid Sovereign Clouds is increasing faster with the German, French, and Nordic organizations striking a balance between the innovation potentials of the hyperscale cloud companies and the need to ensure that there is the control of the data to the European jurisdiction. The rise of cloud de-risking policies among European companies, aiming to reduce their exposure to extraterritorial law, is driving large volumes of investment in both domestic European cloud service providers and local examples of the global cloud solutions run by reputable European organizations.

The Japan Sovereign Cloud Market

The Japan Sovereign Cloud Market is projected to be valued at USD 15.2 billion in 2026. It is further expected to witness robust growth, holding USD 108.7 billion in 2035 at a CAGR of 24.4%.

The Japanese market demonstrates distinctive characteristics shaped by the nation's advanced technological infrastructure and acute sensitivity to data security following high-profile cyber incidents affecting government agencies and critical industries. The stipulated requirements of the Digital Agency on the procurement of cloud services by the Japanese government into the "Government Cloud" initiative and the aggressive investments in Technical Sovereignty capabilities, such as domestic encryption key management and indigenous identity and access management frameworks, have triggered the large investments. Japanese manufacturing, electronics, and automotive large conglomerates are moving towards sovereign cloud architectures to safeguard intellectual property and prevent disruptions in operations during geopolitical uncertainties in the region.

Key Takeaways

- Market Size & Forecast: The global sovereign cloud market will reach USD 149.5 billion in 2026 and surge to USD 1,188.7 billion by 2035, due to increased regulations, geo-political fragmentation, and need of national technological independence at global scale.

- Growth Rate & Outlook: The market is expected to grow at a CAGR of 25.9%, owing to the rising data localization regulations, the rise of geopolitical risks and the proliferation of sovereign-by-design cloud strategies in governments and regulated sectors around the world.

- Primary Growth Drivers: Growth is driven by extraterritorial surveillance laws, national security priorities, and demand for strict data sovereignty, ensuring sensitive information remains within domestic jurisdiction and protected from foreign government access and external control risks.

- Key Market Trends: The main trends driving the growth of this market are sovereign cloud as national infrastructure, development of technical sovereignty solutions, and development of regional cloud federations that make it possible to exchange data across the borders safely and securely using hybrid architectures without violating the jurisdictional compliance requirements.

- By Deployment Analysis: Public sovereign cloud are poised to dominate this market because of scalability, cost-efficiency, and compliance. It allows organizations to fulfill data residency needs and take advantage of hyperscale infrastructure. The high investments in local data centers and the increase in the demand of the services based on AI also stimulates adoption on a global scale.

- By Functionality Analysis: Data sovereignty is expected to lead this segment since it can guarantee that it is compliant with strict data localization and regulatory mandates. The security, foreign surveillance, and the legal risks are the key factors that drive organizations to retain sensitive data on national territory because it is the center of sovereign cloud strategies.

- By End-Use Industry Analysis: Government and defense are projected to dominate because sovereign cloud provides security of confidential data and enhances e-government projects, as well as reducing geopolitical and cyber threats, which would spur its rapid use across this industry.

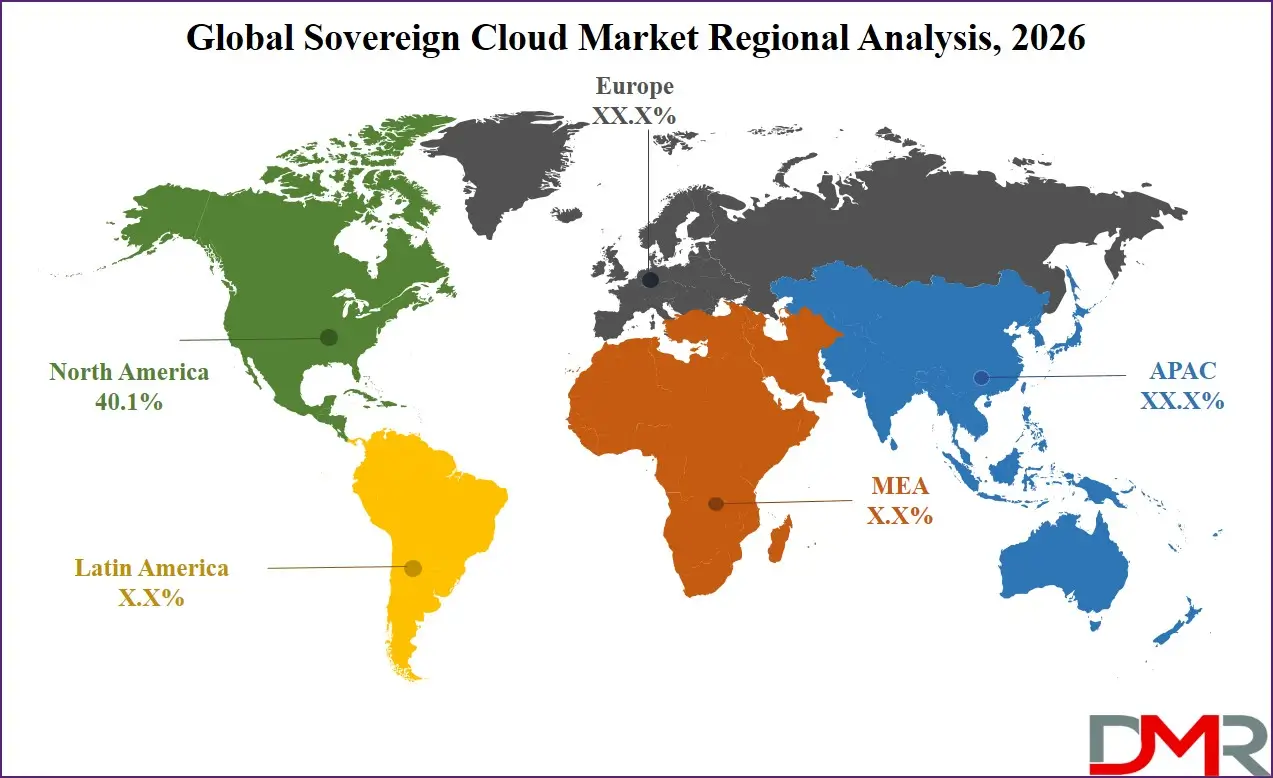

- Regional Leadership: North America leads with 40.1% share in 2026, due to robust government investments, defense modernization, and regulatory framework as well as regional demand, spread across both the public sector and highly regulated industries in need of secure sovereign cloud solutions.

What is the Sovereign Cloud?

Sovereign Cloud is a specialized form of cloud computing infrastructure and services designed with specific characteristics to provide that all data, metadata, operational controls fall under a specific nation or region jurisdiction, and that all laws, regulations, and governance frameworks of that land apply in full to it. Sovereign cloud implementations add several levels of jurisdictional isolation to the traditional cloud services which might send data around the world or expose it to extraterritorial jurisdiction, separation of legal entities so that foreign parent companies cannot compel data access, operational independence to ensure that administrative functions cannot be performed outside the jurisdiction, and cryptographic sovereignty to ensure that encryption keys and identity management systems are completely controlled nationally.

This architectural paradigm responds to the growing fear that traditional cloud models expose organizations to foreign surveillance legislation, introduce dependencies on infrastructure that is in the control of potential geopolitical rivals, and breach increasingly strict national information security and sovereignty regulations.

Use Cases

- National Digital Identity Management in Government & Defense: Government agencies implement Private Sovereign Cloud infrastructure to store national digital identity platforms and citizen authentication systems to make sure that biometric data, identity credentials, and authentication logs are only under the control of domestic jurisdiction and are not subject to foreign intelligence surveillance or foreign legal process.

- Cross-Border Financial Transaction Compliance in BFSI: Global financial institutions are using Hybrid Sovereign Cloud architectures to process and store transaction data that meets multiple country data localization requirements, storing customer financial records within prescribed geographic locations whilst also allowing global transaction processing using sovereign-compliant data federation models.

- Genomic Data Protection in Healthcare: Data Sovereignty-enabled sovereign cloud environments enable national health systems and research institutions to store and process sensitive genomic sequencing data, and comply with genetic privacy laws that bar the transfer of citizen genetic information across national boundaries and facilitate collaborative research by privacy-preserving analytics methods.

- Critical Infrastructure Operational Continuity in Energy & Utilities: Operational Sovereignty capabilities are deployed by energy grid operators to sovereign cloud deployments to ensure that essential operational capabilities cannot be disrupted or taken over by foreign actors through the enforcement of sanctions or in the event of a geopolitical crisis.

How AI is Transforming the Sovereign Cloud Market?

Artificial intelligence is fundamentally transforming the sovereign cloud environment by introducing new demands on the jurisdiction over training data, model weights and inference operations. The significance of AI models as national assets is propelling states and businesses to insist on sovereign cloud infrastructure that can host the training and deployment of large language models fully on national soil. In Data Sovereignty, AI tasks with sensitive government records, military intelligence, or corporate secrets must have iron-definitive assurances that training data will never exit the territory of the sovereignty and will not be open to foreign monitoring or seizure. This has spurred the creation of sovereign AI factories dedicated cloud infrastructure optimized to AI training and inference and with full jurisdictional isolation of data and the resultant model artifacts.

Market Dynamics

Key Drivers in the Global Sovereign Cloud Market

Proliferation of Data Localization Mandates

The most significant force behind sovereign cloud implementation is the growing pace of legislation of data residency and localization laws in over 100 countries. Countries such as India, with its Data Protection Act to Saudi Arabia, with its Personal Data Protection Law, are requiring that some types of information, specifically information about citizens, financial data, and health information, must remain stored and processed within the country. These rules have high formidable fines in case of non-compliance and offer legal liability to the organizations to use traditional cloud services that can transfer data across jurisdictions.

Geopolitical Weaponization of Digital Dependencies

The growing geopolitical tensions and the proven readiness of the nation-states to arm technology dependencies have changed enterprise and government risk calculus of cloud infrastructure fundamentally. The possibility of foreign state authorities to require cloud providers in their jurisdiction to deny service, reveal confidential information, or interfere with operations in the event of international conflict, has necessitated an immediate need to have Operational Sovereignty. Companies in strategically sensitive industries are increasingly focusing on cloud platforms that do not tie operational stability to any one of the foreign jurisdictions, whereby the businesses can continue their key operations despite geopolitical shifts.

Restraints in the Global Sovereign Cloud Market

Premium Cost Economics and Limited Scale

The nature of sovereign cloud implementations is that they are more expensive to operate than the traditional hyperscale cloud services because of inherent economic limitations. The need to have a data center infrastructure that is specific to jurisdiction constrains the economies of scale that the global cloud providers get due to their giant, multi-tenant facilities. The deployment of Private Sovereign Clouds imply higher costs and the presence of specific infrastructure, specialized security mechanisms, and most of the time air-gapped systems that do not allow the operational efficiency of public cloud automation. Public Sovereign Cloud solutions are cheaper than private implementations and yet still carry a premium based on higher overhead costs due to the need to preserve legal entity separation, local support services, and jurisdiction-specific compliance certifications.

Innovation Lag and Feature Parity Gaps

Domestic cloud environments, especially air-gapped or sovereign environments (sometimes run by national or local providers), often lag the innovation pace and breadth of feature of hyperscale cloud environments worldwide. The physical and logical seclusion of sovereign architectures may act as a barrier to the flow of continuous stream of new services, higher AI functions, and state-of-the-art developer tools that global cloud providers offer their main areas of commerce. Companies that use sovereign cloud solutions frequently face challenging tradeoffs between obtaining Technical Sovereignty and the entire range of cloud-native innovation that is the source of digital transformation.

Growth Opportunities in the Global Sovereign Cloud Market

National Digital Infrastructure Modernization

The worldwide trend of government transformation projects through digitalization is offering an unprecedented expansion potential to sovereign cloud service providers. Countries across the globe are actively modernizing citizen service delivery platforms, digital identity systems and e-governance infrastructure, and sovereign cloud forms the basis of these strategic efforts. Government & Defense agencies dealing with sensitive citizen information, national security information, and vital citizen services must have cloud infrastructure that ensures Data Sovereignty and is capable of delivering the agility and innovative velocity of modern digital government.

Regulated Industry Compliance Enablement

The private sector industries that are highly regulated and are experiencing increasing data sovereignty and operational resilience requirements are a huge and under-served market opportunity of sovereign cloud solutions. BFSI organizations that operate in a complex web of national financial data localization requirements, cross-border transaction reporting requirements, and business continuity requirements need sovereign cloud structures that can both meet a variety of jurisdictional compliance regimes and also support global business functions. Equally, Healthcare organizations with sensitive patient data governed by strict privacy rules like HIPAA in the United States and GDPR in Europe, in addition to new genetic data protection legislation, will need sovereign cloud environments that will ensure that patient data is only exposed to domestic legal protection.

Trends in the Global Sovereign Cloud Market

Emergence of Regional Sovereign Cloud Federations

One of the major market trends is the emergence of federated sovereign cloud architectures that allow the sharing of trusted data across national borders and still maintain jurisdictional sovereignty. Other frameworks like the GAIA-X initiative in Europe and new frameworks in Southeast Asia and the Gulf Cooperation Council aim to develop standards of interoperability and governance in such a way that allows cross-border data flows within a specific trust community. These federated Hybrid Sovereign Cloud models resolve the tension that exists between the need to ensure data sovereignty and the economic necessity to integrate data on a regional level, allowing the collaborative research, the facilitation of trade, and the coordinated provision of services to the involved countries.

Supply Chain Sovereignty and Hardware Trust

The increasing understanding that Technical Sovereignty does not just require the control of software and data to be effectively achieved to sovereign, but that overall technology supply chain is also a necessary component in sovereign cloud implementations, is leading to a renewed interest in hardware provenance and integrity checking in sovereign cloud deployments. Companies and governments are now requiring transparency of the manufacturing provenance of components of cloud infrastructure, especially hardware security modules, cryptographic processors and networking equipment which form trust anchors of sovereign cloud systems.

Research Scope and Analysis

Research Scope and Analysis covers deployment, functionality, service type, enterprise size, and end-use industries, highlighting public sovereign cloud dominance driven by scalability, compliance, data sovereignty, and government-led digital transformation.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Deployment Analysis

This segment is poised to dominated by public sovereign cloud because it has the capacity of integrating scalability, cost-efficiency, and compliance with regulations. Public sovereign infrastructure provided by hyperscalers in collaboration with domestic organizations has become increasingly popular in governments and enterprises because it offers scalable infrastructure and data residency and adherence to the law. In contrast to privately deployed clouds, government-sovereign clouds will decrease capital outlay and hasten digital transformation efforts. Hybrid models are becoming popular yet they still demand complexity of integration. Increasing AI, analytics, and digital public services demand is another factor contributing to the dominance because these require scalable infrastructure. Also, hyperscale providers remain heavy users of localized data centers and sovereign offerings, and thus, the easyest and fastest to implement offering to organizations hoping to be compliant without having to sacrifice performance is public sovereign cloud.

By Functionality Analysis

Data sovereignty is projected to be leading functionality segment as it directly addresses regulatory and legal requirements of data storage and processing. As more data localization laws are put into practice in other regions, organizations are required to make sure that sensitive data is not moved out of the country and under local authority. Particularly important in this respect is the case of such areas as government, BFSI and healthcare, in which compliance breach may result in hefty fines. Operational and technical sovereignty are important, but usually secondary layers that are constructed around data sovereignty needs. The increasing anxieties over foreign surveillance, cross-border data transfer and the cyber risks further buttress the significance of data sovereignty. As a result, most sovereign cloud strategies are fundamentally designed around ensuring data control, making it the cornerstone and dominant functionality in this market.

By Service Type Analysis

Infrastructure as a Service (IaaS) is expected to take the leading position in the sovereign cloud market since it is the base layer on which other services are developed. Organizations are attracted to IaaS due to the ability to control computing, storage, and networking resources and comply with sovereignty requirements simultaneously. It enables governments and businesses to tailor environments based on national policies and security provisions. IaaS is more flexible and controllable than PaaS and SaaS, which is essential in sensitive workloads. Moreover, numerous sovereign cloud implementations start with infrastructure modernization, which enhances the use of IaaS. With the digital transformation pace increasing and the need to provide secure infrastructure on the rise, IaaS remains leading because of its contribution as the foundation of sovereign cloud ecosystems.

By Enterprise Size Analysis

The sovereign cloud market is expected to be dominated by large enterprises because they have a high level of exposure to regulation, operate globally, and have large amounts of data. These organizations have to work in a variety of jurisdictions and have to abide with different data protection laws, which is why sovereign cloud solutions are necessary. They also have the financial resources to invest in modern cloud architectures and collaboration with hyperscalers. Moreover, in large businesses, there is always a high probability that the data is very sensitive (financial, customer, and intellectual property) and therefore, requires greater security and sovereignty measures. SMEs are progressively switching to sovereign cloud solutions, but their constrained budgets and fewer regulatory obligations limit their adoption.

By End-Use Industry Analysis

The government and defense sector is poised to be dominated the sovereign cloud market as they require data security, national control, and adherence to stringent regulatory frameworks. Governments need cloud infrastructure that would provide them with full control of sensitive information such as information about the citizens, defense intelligence and administration systems. Sovereign cloud services reduce the risks related to foreign access, cyber-attacks, and geopolitical conflicts. There are also national digital transformation efforts, smart governance and e-governance platforms, which are driving adoption. Although industries such as BFSI and healthcare are also very demanding, they tend to be controlled by regulatory measures instituted by the governments. The government and defense sector thus is the largest and most influential end-user, and is fueling the uptake and development of sovereign cloud technologies around the world.

The Global Sovereign Cloud Market Report is segmented on the basis of the following:

By Deployment

- Public Sovereign Cloud

- Private Sovereign Cloud

- Hybrid Sovereign Cloud

By Functionality

- Data Sovereignty

- Operational Sovereignty

- Technical Sovereignty

By Service Type

- Infrastructure as a Service (IaaS)

- Platform as a Service (PaaS)

- Software as a Service (SaaS)

By Enterprise Size

- Large Enterprises

- Small & Medium Enterprises (SMEs)

By End-Use Industry

- Government & Defense

- BFSI (Banking, Financial Services & Insurance)

- Healthcare

- Telecommunications

- Energy & Utilities

- Manufacturing

- Others

Regional Analysis

Leading Region by Market Share

North America is poised to dominate the global sovereign cloud market, projected to hold 40.1% of the market share by the end of 2026. The North American sovereign cloud activity anchored by the United States has been market leadership because of convergence of the largest government cloud procurement programs in the world, the availability of leading sovereign cloud technology services, and broad adoption within regulated private sector markets. The presence of federal programs such as FedRAMP High authorization schemes, the impact-level 6 requirements in the Department of Defense classified workloads, and the intelligence community Commercial Cloud Enterprise program are significant and enduring demand of sovereign cloud services under public sovereign cloud, private sovereign cloud, and hybrid sovereign cloud deployment models. In addition to federal procurement, state-led data protection efforts and critical infrastructure protection requirements are generating concurrent sovereign cloud demand among state and local government entities, state-funded healthcare and governmental defense industrial base contractors.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Fastest-Growing Regional Market

Asia-Pacific is expected to be the most rapidly expanding sovereign cloud market, is fueled by the convergence of national aggressive digital sovereignty projects, the rising pace of localization data requirements in key economies, and significant government investment in local cloud infrastructures. The demand that China has on critical data and personal information to stay within national borders has led to the development of a massive domestic sovereign cloud ecosystem that is led by national cloud leaders. The data protection policy and the community cloud program in India are leading to significant investments in sovereign cloud infrastructure to enable digital public services and regulated industry compliance. The Government Cloud program of Japan and the Digital Agency specifications of sovereign cloud procurement by the government are rapidly driving sovereign cloud uptake by government and strategic sectors.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The global sovereign cloud market is characterized by intense competition between global hyperscalers and regional providers. Major players like Amazon Web Services, Microsoft Azure, Google Cloud Platform, and Oracle Cloud Infrastructure are leading with robust infrastructure, high-level AI and powerful enterprise ecosystems. However, regional players including OVHcloud, T-Systems, and Alibaba Cloud are gaining ground by emphasizing data sovereignty, regulatory compliance, and local trust.

Strategic partnerships, government collaborations, and sovereign cloud alliances are used as a motivating factor in competition because they aim to address stringent national regulations. Organizations are making a big investment in localized data centers, encryption systems, and compliance systems. With geopolitical tensions escalating, and laws on data localization growing tougher, differentiation is growing more and more based on the capacity to trade-off between global scalability and rigorous jurisdictional control and security assurance.

Some of the prominent players in the Global Sovereign Cloud Market are:

- Amazon Web Services

- Microsoft Azure

- Google Cloud Platform

- Alibaba Cloud

- Oracle Cloud

- IBM Cloud

- OVHcloud

- Gcore

- Scaleway

- Clever Cloud

- Cloudian

- Yotta Data Services

- Proximus

- StackIT

- Post Telecom

- SAP

- Tencent Cloud

- Huawei Cloud

- NTT Communications

- Orange Business

- Other Key Players

Recent Developments

- December 2025: AWS added new Impact Level 6 authorized regions to its GovCloud offerings, to support classified Department of Defense workloads, and expanded technical sovereignty capabilities with domestic hardware security modules and verified supply chain integrity to process top secret/sensitive compartmented information.

- October 2025: The Indian government used the National Sovereign Cloud Initiative to award a consortium of local technology providers with significant contracts to build indigenous cloud infrastructure to host citizen data, digital public services and sensitive government workloads under exclusive Indian jurisdictional control.

- September 2025: OVHcloud and Deutsche Telekom OVHcloud and Deutsche Telekom declared a strategic sovereign cloud collaboration forming a federated European sovereign cloud platform allowing Hybrid Sovereign Cloud deployments across France and Germany without the loss of national jurisdiction and compliance with GAIA-X.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 149.5 Bn |

| Forecast Value (2035) |

USD 1,188.7 Bn |

| CAGR (2026–2035) |

25.9% |

| The US Market Size (2026) |

USD 50.4 Bn |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Deployment (Public Sovereign Cloud, Private Sovereign Cloud, and Hybrid Sovereign Cloud), By Functionality (Data Sovereignty, Operational Sovereignty, and Technical Sovereignty), By Service Type (Infrastructure as a Service (IaaS), Platform as a Service (PaaS), and Software as a Service (SaaS)), By Enterprise Size (Large Enterprises, and Small & Medium Enterprises (SMEs)), By End-Use Industry (Government & Defense, BFSI (Banking, Financial Services & Insurance), Healthcare, Telecommunications, Energy & Utilities, Manufacturing, and Others) |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Global Sovereign Cloud Market?

▾ The Global Sovereign Cloud market is poised to be valued at USD 149.5 billion in 2026 and is projected to reach USD 1,188.7 billion by 2035, driven by accelerating data localization mandates, geopolitical imperatives for digital sovereignty, and national investments in strategic cloud infrastructure.

What is the CAGR of the Global Sovereign Cloud Market from 2026 to 2035?

▾ The market is expected to grow at a CAGR of 25.9% from 2026 to 2035, reflecting the structural shift toward sovereignty-by-design cloud architectures across government, defense, and regulated industries, coupled with the proliferation of national data protection frameworks globally.

What factors are driving the growth of the Global Sovereign Cloud Market?

▾ Key drivers include the enactment of data localization laws across 100+ countries, geopolitical weaponization of digital dependencies creating operational sovereignty imperatives, national strategic autonomy initiatives in critical technology infrastructure, and the convergence of AI sovereignty with cloud sovereignty requirements.

Which region held the largest share of the Sovereign Cloud Market in 2026?

▾ North Americais projected to dominate this market with 40.1% of market share in 2026, driven by substantial federal government sovereign cloud procurement for defense, intelligence, and civilian agency modernization, coupled with state-level data protection initiatives and regulated industry adoption.

Which region is expected to grow the fastest in the Sovereign Cloud Market?

▾ The Asia-Pacific region is expected to grow the fastest, fueled by aggressive national digital sovereignty initiatives in China, India, and Japan, accelerating data localization mandates across Southeast Asia, and substantial government investment in indigenous sovereign cloud infrastructure.

What are the major trends in the Global Sovereign Cloud Market?

▾ Major trends include the emergence of regional sovereign cloud federations enabling trusted cross-border data sharing, intensified focus on supply chain sovereignty and hardware trust verification, and the convergence of operational and technical sovereignty dimensions into comprehensive sovereign cloud frameworks.

Who are the key players in the Global Sovereign Cloud Market?

▾ Key players include specialized sovereign cloud instances of global hyperscalers (AWS GovCloud, Azure Government, Google Cloud Sovereign Solutions), indigenous European providers (OVHcloud, Deutsche Telekom, Orange), Asian national champions (Alibaba Cloud, Huawei Cloud), and systems integrators with sovereign cloud practices (Capgemini, Atos, Thales).

How is the Global Sovereign Cloud Market segmented?

▾ The market is segmented by Deployment, Functionality, Service Type, Enterprise Size, and End-Use Industry.