What is the Global Space Propulsion Market Size ?

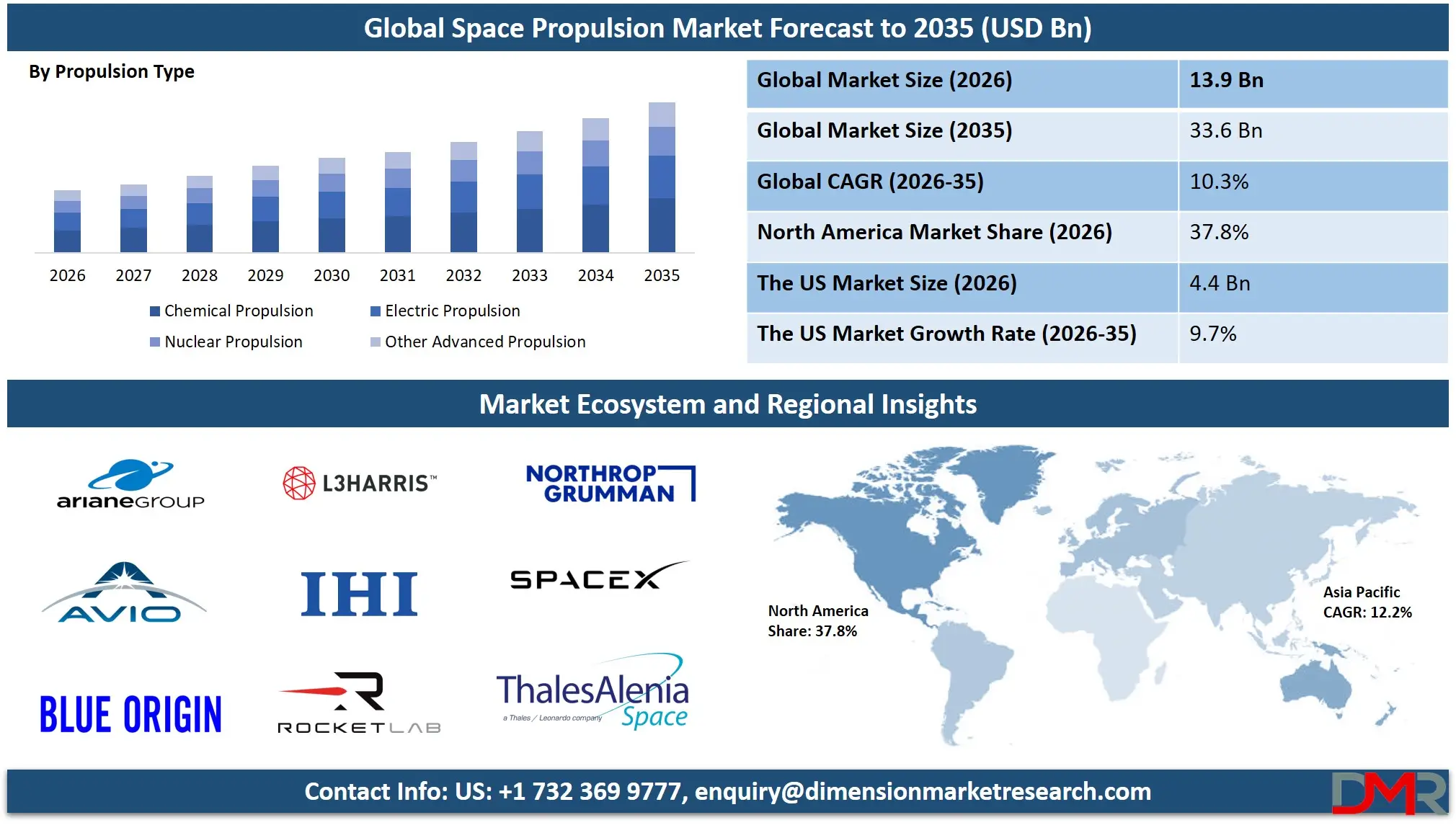

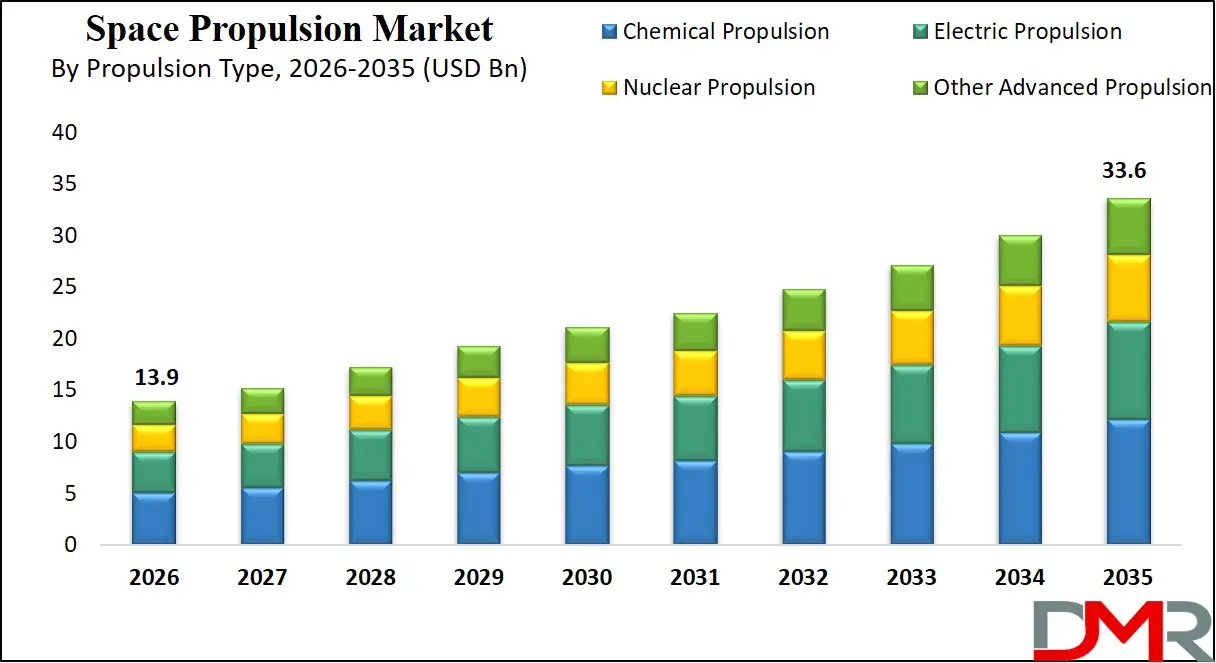

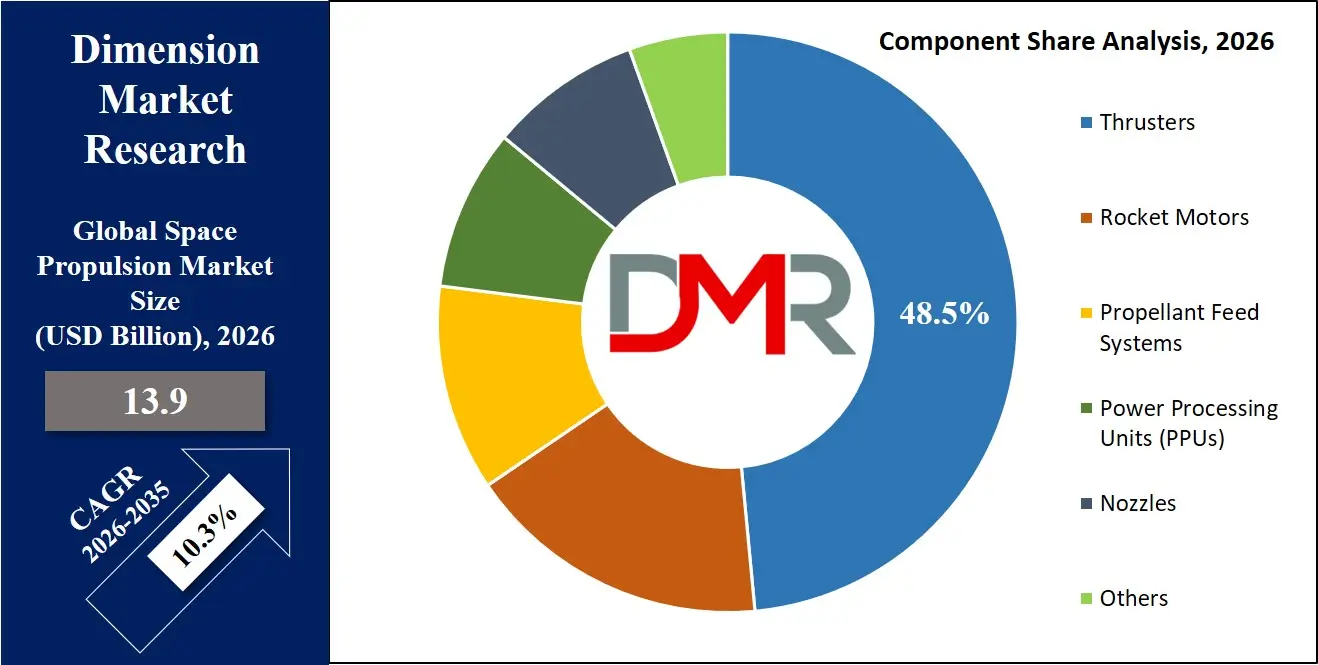

The Global Space Propulsion Market size in 2026 is estimated at USD 13.9 billion and grow at a compound annual growth rate (CAGR) of 10.3% to reach a value of USD 33.6 billion by 2035, due to advancements in electric propulsion, green propellants, 3D-printed nozzles and AI-controlled autonomous rendezvous.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The Space Propulsion Market has experienced an incremental growth due to the growing deployment of low-earth orbit mega-constellations, national security requirements of responsive space capabilities, and the need to allocate both government and commercial capital to lunar and Mars infrastructure in space agencies around the world. It also covers such new technologies as real-time ion thruster health monitoring, cloud-based propulsion telemetry analytics, and automated collision avoidance thrust mapping used in satellite propulsion projects.

Modernization is a significant investment that launch providers, satellite OEMs, and defense contractors are pursuing to allow efficient propellant management, reduce the risk of orbital debris proliferation, and increase mission longevity. The move towards automation, predictive modeling of thruster erosion, and smart propulsion stacking (chemical for orbit raising + electric for station keeping) is increasing adoption. Moreover, the need to operationalize the Artemis Accords and the importance of sustainable space operations are driving digital changes in space transportation, and space propulsion systems have become an essential part of the future cislunar economy on a global scale.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

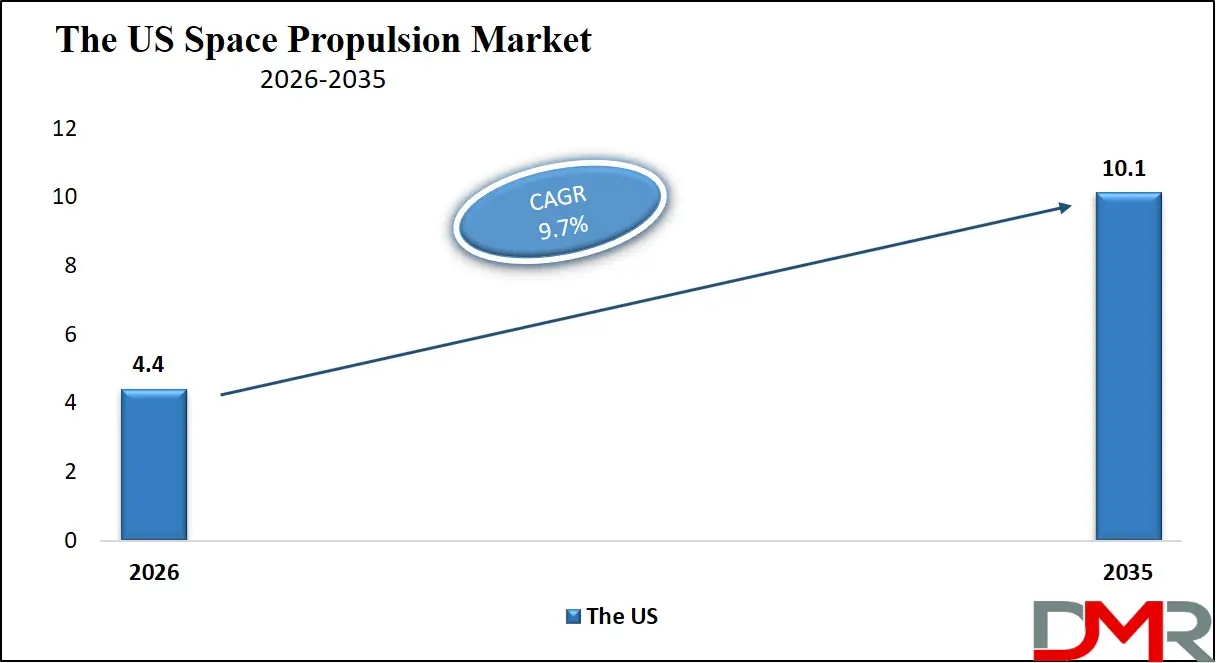

The US Space Propulsion Market

The US Space Propulsion Market is estimated to grow to USD 4.4 billion in 2026 with a compound annual growth rate of 9.7% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

In the US, the space propulsion market is motivated by commercial launch business (e.g., SpaceX, Blue Origin), national security (e.g., NSSL Phase 3), and the necessity of modernizing legacy hypergolic systems with safer, more high-performance solutions. Increasing investment is underway in autonomous thrust vector control systems, predictive life models of turbopumps using AI, and real-time engine telemetry to detect anomalies. Federal funding programs, including the NASA Artemis campaign and the constellation of Resilient Missile Warning and Tracking by the USSF, encourage the adoption. The Government and Defense, and Commercial segments dominate, and digital engineering tools enhance the performance of propulsion design and testing. Key players are focusing on propulsion reusability and supply chain partnerships to raise the launch frequency and reliability. The regulatory frameworks that promote space sustainability and verifiable mission assurance also facilitate the adoption of digital propulsion health monitoring, and the need to have real-time chamber pressure data and automated engine-out response further determines the growth of markets.

Europe Space Propulsion Market

The Europe Space Propulsion Market is estimated to be valued at USD 3.8 billion in 2026, witnessing growth at a CAGR of 10.1%, during the forecast period.

Europe has a mature space propulsion market, and this has a significant influence on the regulatory requirements and regional policies such as the EU Space Programme, the Future Launchers Preparatory Programme of the ESA, and national sovereignty programs (e.g., Ariane 6 in France and Vega E in Italy). Countries are also striving for smart propulsion system modularization to harmonize commercial and institutional mission requirements and interoperability of the cross-border supply chain. Advanced manufacturing, like 3D-printed combustion chambers and laser ignition, and high-reliability electric propulsion units with in-built life-prediction algorithms, drives innovation. Public-private partnerships and harmonization of space traffic management standards facilitate adoption. Technologies like real-time plume monitoring and smart contract-based telemetry data sharing are commonly practiced as research-centric programs, and Europe is a frontrunner in terms of the digital transformation of green and bi-propellant propulsion.

Japan Space Propulsion Market

The Japan Space Propulsion Market is projected to be valued at USD 686.7 million in 2026, progressing at a CAGR of 11.1%, during the period spanning from 2026 to 2035.

Japan boasts a mature space propulsion market supported by high-performance solid rocket boosters (Epsilon S), ion engine technology (Hayabusa2), and a wide network of satellite servicing innovations. Automation, precision, and mission integrity are the priorities in the country and are achieved by AI-driven thruster wear prediction models (e.g., for magnetoplasmadynamic thrusters) and predictive thermal management systems for propulsion assets. Growth is stimulated by government actions under the Basic Plan on Space Policy and constant investment in in-orbit servicing infrastructure. The high volume of LEO observation satellites, lunar landers, and asteroid missions requires efficient propulsion systems for orbital insertion and station keeping. The difficulties are high validation costs for new propulsion chemistries and integration with existing satellite buses, yet the prospects are in exporting developed electric and chemical propulsion technologies to Asian and Pacific markets.

Key Takeaways

- Market Size & Forecast: The Global Space Propulsion Market is estimated to be valued at USD 13.9 billion in 2026 and is expected to grow to USD 33.6 billion by 2035.

- Growth Rate & Outlook: The market is expected to witness growth at a compound annual growth rate of 10.3% in the forecast period.

- Primary Growth Drivers: Technological progress in electric propulsion and green propellants to support mega-constellations, regulatory requirements, and commercial satellite deployment are some of the key drivers of growth in the market.

- Key Market Trends: The use of AI and data-driven decision making to optimize thrust and predict anomalies and transition to cloud-based propulsion telemetry and fleet management systems are some of the primary market trends.

- By Propulsion Type: The chemical propulsion segment is anticipated to get the majority share of the Space Propulsion market in 2026.

- By Component: The thrusters segment is expected to get the largest revenue share in 2026 in the Space Propulsion market.

- By Platform: The satellites segment is expected to get the largest revenue share in 2026 in the Space Propulsion market.

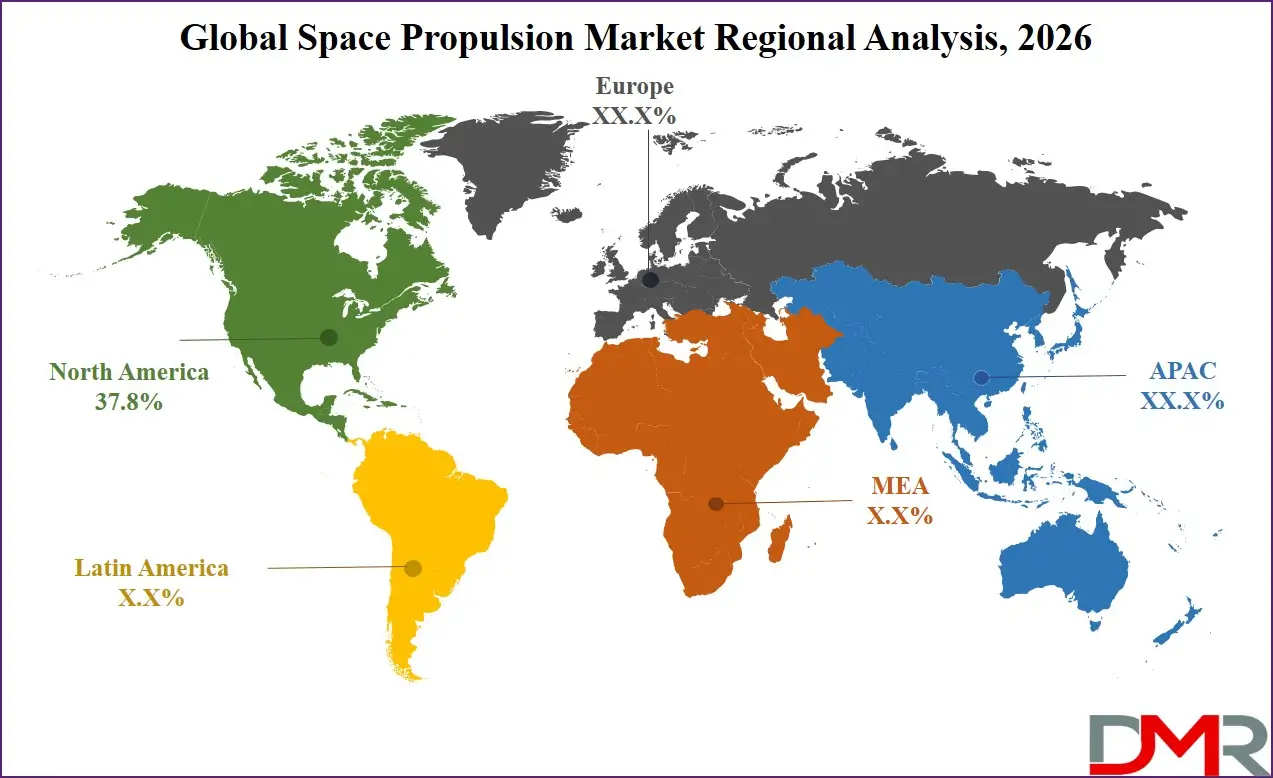

- Regional Leadership: North America is predicted to dominate the market with an estimated 37.8% share in 2026, with high launch frequency and defense spending.

Use Cases

- LEO Mega-Constellation Deployment and Maintenance: Propulsion systems support orbit raising, collision avoidance maneuvers, and end-of-life deorbiting that reduce the risks of the generation of debris and improve the mission life, regulatory compliance, and space safety.

- Thruster Life Prediction Modeling (Reliability Risk): Mission information, including cumulative firing hours or cathode erosion is modeled to provide redundancy margins and continue the mission without failure to maintain operational stability over the long term and investor trust.

- Commercial Satellite Services: Commercial satellite providers are employing electric and chemical propulsion to perform station keeping, end-of-life disposal, and orbital repositioning to provide communications, Earth observation, and broadband services with quantifiable and proven maneuver performance.

- Deep-Space and Government Programs: More effective propulsion systems contribute to the success of lunar landers, Mars rovers, and asteroid probes, facilitate national exploration, contribute to launch reliability, and help implement policies, such as the space traffic coordination policy and orbital debris mitigation policy.

What is the Space Propulsion?

Space propulsion is a technology that propels spacecrafts and satellites to accomplish orbit insertion, station keeping, attitude control, orbital transfer, and interplanetary trajectory correction. It employs chemical burning, acceleration of ionized gases, nuclear thermal, or new technologies (solar sails, electrospray thrusters) to provide propulsion. The contemporary systems have real-time telemetry, additive-manufactured parts, and AI-assisted navigation to ensure transparency, efficiency, and reliability. These propulsion systems are capable of supporting efficient mission planning, sustainable space operations, and help direct the funds of commercial and government and research stakeholders towards scalable, long-period space infrastructure. They also facilitate accountability by making sure that propulsion performance data is quantified, tracked, and in line with global space sustainability objectives.

How AI Is Transforming the Global Space Propulsion Market

The artificial intelligence is transforming space propulsion systems by having been able to model the thruster erosion predictively, anomalies in the turbopump vibration data can be automatically identified, and thrust vectoring can be optimized in real-time. Telemetry and environmental data can be analysed with AI algorithms to determine any degradation or performance drift and scale-optimise mission results. This saves time, is verifiable and cheaper than manual data analysis.

Moreover, AI enhances mission assurance through offering adaptive burn planning, anticipating thermal threats to engine components, and intelligent prioritization of propulsion system health monitoring. It is also involved in reducing the cost of baseline testing and ongoing performance tracking, allowing mission operators to reduce the cost and physical footprint of ground-based test campaigns and improve the reliability of space maneuvers and their financial returns.

Market Dynamics

Key Drivers of the Global Space Propulsion Market

Rapid developments in Electric Propulsion and Autonomous Systems

The market is being pushed by a fast uptake of AI, high-efficiency Hall-effect thrusters (HETs), additive manufacturing (3D-printed injectors and nozzles), and real-time telemetry analytics. These technologies will allow monitoring of the health of thrusters in real-time, identify performance anomalies early, predict the end-of-life, and simplify the process of ground verification. Consequently, operational uptime and mission efficiency are highly enhanced as well as minimizing expenses of manual analysis of telemetry. The growth of the commercial satellite constellations like Starlink and OneWeb, in particular, is also accelerating the need in intelligent propulsion systems as space operators are more inclined towards automation and mission optimization based on data.

Growing Focus on Space Regulation and Orbital Sustainability

The world is becoming more and more involved in policies of orbital debris mitigation, with governments and international bodies proposing deorbit mitigation policies, like the Zero Debris Charter of ESA and the deorbit mitigation policies proposed by the FCC. These structures are driving a high demand of sound propulsion systems that can be used to carry out controlled deorbiting and end-of-life maneuvers. In parallel, global initiatives such as the UN COPUOS Long-term Sustainability Guidelines are encouraging the adoption of cleaner propulsion technologies and green propellants. The increasing calls on transparency in the disposal of satellites and orbital behavior are also enhancing the necessity of verifiable and efficient propulsion systems in both commercial and government missions.

Restraints in the Global Space Propulsion Market

High Costs of Testing and Space Qualification

Space propulsion systems are costly and time-consuming to validate, needing to test in a vacuum chamber, qualify vibrations, test long-term thruster life cycle, and sophisticated telemetry facilities. Moreover, export control laws and regulations like ITAR and EAR further complicate and increase expenses. All these pose serious obstacles to new entrants and small satellite developers, tend to lengthen deployment time, and raise initial capital needs.

Limited Standardization Across Propulsion Systems

The industry still depends on several propulsion systems that include chemical (hypergolic and bipropellant), and electric propulsion systems that include ion and hall-effect propulsion systems. Nevertheless, the absence of standard interfaces between propulsion units and satellite platforms is a significant challenge. Space systems lack universal plug-and-play standards, unlike the automotive or aviation industries, which complicates and makes integration very expensive. This division expands the time of development and restricts the wide-ranging interoperability of the satellite constellation.

Growth Opportunities in the Global Space Propulsion Market

Expansion of Emerging Space Programs

Developing space nations such as Brazil, Indonesia, Nigeria, the UAE, and Vietnam are investing heavily in space infrastructure and propulsion capability development. These regions present strong growth potential due to increasing demand for satellite-based communication, Earth observation, and navigation services. With fewer legacy system constraints, these markets provide opportunities for modern, cost-efficient propulsion technologies tailored for small satellite and LEO constellation deployment.

Rising Demand for In-Orbit Services

The increased requirement of advanced propulsion systems is being generated by the growth of in-orbit servicing (IOS), satellite refueling, and active debris removal (ADR). The technologies play a vital role in satellite repositioning, life extension, and controlled re-entry functions. With the rising importance of sustainability as a major industry concern, in-orbit mobility and servicing capabilities are likely to be fundamental to future space infrastructure.

Global Space Propulsion Market Trends

AI-Driven Propulsion Monitoring and Predictive Analytics

Propulsion systems are being monitored and anomalies detected in real time and component wear predicted using artificial intelligence. The use of digital twin models and machine learning algorithms is enhancing the burn planning, the life of the system, and the reliability of the mission. This shift is transforming propulsion management from manual telemetry review to fully automated, continuously optimized system monitoring.

Cloud-Based Telemetry and Fleet Management System

Cloud computing and digital twin technologies are taking the centre stage in the operations of propulsion systems. These platforms enable real-time storage and analysis of engine performance data, centralized fleet management, as well as remote monitoring of satellite propulsion systems. Cloud-based systems enhance transparency, lower ground infrastructure expenses, and quicker responses to missions across constellations of satellites, as experienced by operators of large satellites.

Research Scope and Analysis

By Propulsion Type Analysis

The chemical propulsion segment is expected to remain the largest in 2026, accounting for about 52.3% of the global space propulsion market, driven by its dominant use in launch vehicles, upper-stage operations, and high-thrust, time-critical missions such as lunar landers and crewed spacecraft, where rapid orbital insertion and maximum thrust are essential. Meanwhile, the electric propulsion segment is witnessing strong growth, driven by rising demand for high specific impulse in LEO station-keeping, orbit raising of small satellites, and deep-space missions where fuel efficiency is critical. Adoption is further supported by AI-based plume monitoring, real-time thruster efficiency diagnostics, and modular hybrid configurations that integrate electric and chemical systems for improved mission flexibility and endurance.

By Component Analysis

The thrusters segment is expected to dominate with approximately 48.5% market share in the year 2026, owing to its critical role in generating actual ΔV, high replaceability, and co-benefits with reusable systems (e.g., SpaceX Merlin thrusters, Starlink Hall thrusters). Commercial and government buyers are shifting to higher-performance thruster designs in order to have greater fuel efficiency and improve mission longevity.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Thruster solutions are adaptable, making it easy to deploy and integrate with other components (e.g., PPUs, feed systems). Rocket motors can still be used, though, in places where high initial thrust is required (e.g., launch vehicle boosters, missile systems). The multi-component usage with thrusters, propellant feed systems, and power processing units simultaneously has the quickest development, and the propulsion system portfolios are more flexible to different thrust classes and mission contexts.

By Platform Analysis

It is predicted that the satellites segment will have the highest share of around 48.7% in 2026, considering its pivotal role in hosting electric and chemical propulsion for orbit maintenance, deorbiting, and collision avoidance. The integrated telemetry and control systems provide continuous maneuver tracking, which improves the efficiency and safety of constellation operations. Constellation scale and burn frequency are determined by the platform type, and the most common are small satellites with Hall effect thrusters. The launch vehicles segment controls large-thrust, short-duration missions, such as first and second stage propulsion. The fastest growing area is the space tugs / orbital transfer vehicles segment, which enhances the power to automate payload delivery and standardize propulsion interfaces by means of modular thruster arrays and refueling ports. The fusion of platform integration and AI is generating smarter orbital mobility markets, which results in innovation and expands the technological market.

By Satellite Mass Class Analysis

The 51–500 kg (Micro) satellite segment is likely to take the lead with an estimated share of 35.4% in 2026, driven by strong adoption in Earth observation, communication, and LEO constellation deployments. However, the broader Nano and Micro satellite categories together account for the dominant propulsion demand base due to high deployment volumes. Large satellites (greater than 1 ton) continue to require robust propulsion systems for GEO missions, orbit maintenance, and end-of-life disposal. The Nano satellite segment supports lightweight propulsion technologies such as electrospray and cold gas systems. The fastest-growing category is the 501 kg–1 ton (Mini) segment, driven by flexible mission requirements and increasing commercial satellite deployments.

By Orbit Class Analysis

The Low Earth Orbit (LEO) segment represents the largest orbit class in 2026, accounting for approximately 62.3% share of the market, driven by rising mega-constellation deployments collision avoidance requirements, and end-of-life deorbiting regulations. Geostationary Orbit (GEO) forms the second-largest segment, utilizing propulsion for orbital insertion, station keeping, and life extension missions. Medium Earth Orbit (MEO) end users, particularly in navigation constellations (GPS, Galileo), are adopting electric propulsion for precise orbit maintenance. Beyond GEO represents a steadily growing segment, leveraging nuclear and advanced propulsion for lunar, Mars, and deep-space missions. The diversification across orbit classes highlights the broadening adoption of space propulsion technology beyond traditional commercial communications.

By End-User Analysis

The commercial segment represents the largest end-user segment in 2026, accounting for approximately 54.3% share of the market, driven by rising LEO mega-constellation deployments, demand for orbital transfer vehicles, and cost pressures requiring efficient electric propulsion for station keeping and deorbiting. Government & Defense forms the second-largest segment, utilizing propulsion for national security satellites, missile systems, lunar and Mars exploration (NASA Artemis, ESA's Terrae Novae), and space domain awareness missions. Research Institutions end users, particularly in deep-space probes and science missions, are adopting advanced propulsion (nuclear thermal, ion thrusters) for long-duration, high-ΔV requirements where conventional propellants are insufficient. The fastest-growing area is the commercial segment, driven by the need to have low-cost, high-reliability propulsion for small satellite constellations, in-orbit servicing, and space logistics. With increasing launch frequency and orbital congestion, commercial, defense, and research agencies have been spending more on autonomous propulsion systems to improve mission success rates and space operations efficiency.

The Global Space Propulsion Market Report is segmented based on the following:

By Propulsion Type

- Chemical Propulsion

- Electric Propulsion

- Nuclear Propulsion

- Other Advanced Propulsion

By Component

- Thrusters

- Rocket Motors

- Propellant Feed Systems

- Nozzles

- Power Processing Units (PPUs)

- Others

By Platform

- Satellites

- Small Satellites

- Medium Satellites

- Large Satellites

- Launch Vehicles

- Space Tugs / Orbital Transfer Vehicles

- Interplanetary Spacecraft & Deep-Space Probes

- Rovers & Spacecraft Landers

- Capsules / Cargo Spacecraft

By Satellite Mass Class

- Less than or equal to 50 kg (Nano)

- 51–500 kg (Micro)

- 501 kg–1 ton (Mini)

- Greater than 1 ton (Large)

By Orbit Class

- Low Earth Orbit (LEO)

- Medium Earth Orbit (MEO)

- Geostationary Orbit (GEO)

- Beyond GEO

By End-User

- Commercial

- Government & Defense

- Research Institutions

Regional Analysis

Leading Region in the Space Propulsion Market

It is projected that North America will take the lead in the global space propulsion market (by value), covering a market share of about 37.8% in the year 2026. The region's dominance is driven by strong commercial launch cadence (US-based launch providers), high propulsion system prices relative to other regions, a mature supply chain for liquid and solid rocket motors, and the presence of key propulsion system integrators and component suppliers. The widespread adoption of advanced electric and reusable chemical propulsion systems for constellation deployment, defense missions, and NASA deep-space programs further strengthens North America's leading position in the market. Additionally, continuous investments in AI-enabled engine health monitoring and additive manufacturing capabilities are further reinforcing regional technological leadership.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Fastest-Growing Region in the Space Propulsion Market

Asia-Pacific is the fastest-growing region, supported by strong satellite deployment targets (China, India, Japan), increasing space exploration initiatives, rising investments in domestic launch capabilities, and growing adoption of electric propulsion systems. The region benefits from well-established manufacturing capacity, increasing commercial participation, and alignment with national space roadmaps. Countries across the region are actively deploying propulsion systems to enhance mission efficiency and strengthen space infrastructure. Growing emphasis on space R&D and structured propulsion development further accelerates market expansion in the region. Moreover, increasing government support and commercial constellation commitments are expected to sustain high growth momentum.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The space propulsion market is very competitive, with innovation and strategic alliances being the order of the day. In order to achieve a competitive advantage, companies and government labs are oriented towards the creation of new advanced propulsion technologies (e.g., nuclear thermal, dual-mode, green monopropellants), AI-powered engine telemetry, and digital twin-enabled health monitoring platforms. There are high barriers to entry because of capital-intensive testing infrastructure, technical propulsion know-how, and the need for flight heritage and supply chain certifications. Strategic approaches in the market to increase market presence include partnerships with satellite OEMs, mergers between thruster developers and launch integrators, and long-term propulsion supply contracts with constellation operators. Moreover, research and development in additive manufacturing and high-temperature materials are important factors in staying competitive and meeting the changing needs of the space industry.

Some of the prominent players in the Global Space Propulsion Market are:

- L3Harris Technologies, Inc.

- Northrop Grumman Corporation

- ArianeGroup

- IHI Corporation

- Avio S.p.A.

- Space Exploration Technologies Corp.

- Blue Origin, LLC

- Mitsubishi Heavy Industries, Ltd.

- Rocket Lab USA, Inc.

- Airbus SE

- Thales Alenia Space

- Lockheed Martin Corporation

- The Boeing Company

- OHB SE

- Moog Inc.

- Busek Co. Inc.

- Accion Systems Inc.

- Exotrail SA

- Dawn Aerospace Limited

- Nammo AS

- Other Key Players

Recent Developments

- January 2026: L3Harris Technologies, Inc. announced the sale of a 60% stake in its space propulsion division to AE Industrial Partners for USD 845.0 million, while retaining ownership of key engines such as RS-25 used in NASA’s Artemis program.

- January 2026: Rocket Lab USA, Inc. achieved a record number of Electron launches with consistent mission success and continued development of its Neutron rocket, expanding its propulsion capabilities.

- November 2025: Blue Origin, LLC successfully launched and landed its New Glenn rocket booster, marking a major milestone in reusable propulsion systems and strengthening competition with SpaceX.

- July 2024: ArianeGroup successfully supported the inaugural launch of the Ariane 6 rocket, strengthening Europe’s independent access to space with advanced cryogenic propulsion systems.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 13.9 Bn |

| Forecast Value (2035) |

USD 33.6 Bn |

| CAGR (2026–2035) |

10.3% |

| The US Market Size (2026) |

USD 4.4 Bn |

| Historical Period |

2021 – 2025 |

| Forecast Period |

2027 – 2035 |

| Base Year |

2025 |

| Estimated Year |

2026 |

| Segments Covered |

By Propulsion Type (Chemical Propulsion, Electric Propulsion, Nuclear Propulsion, Other Advanced Propulsion), By Component (Thrusters, Rocket Motors, Propellant Feed Systems, Nozzles, Power Processing Units (PPUs), Others), By Platform (Satellites, Launch Vehicles, Space Tugs / Orbital Transfer Vehicles, Interplanetary Spacecraft & Deep-Space Probes, Rovers & Spacecraft Landers, Capsules / Cargo Spacecraft), By Satellite Mass Class (Less than or equal to 50 kg (Nano), 51–500 kg (Micro), 501 kg–1 ton (Mini), Greater than 1 ton (Large)), By Orbit Class (Low Earth Orbit (LEO), Medium Earth Orbit (MEO), Geostationary Orbit (GEO), Beyond GEO), By End-User (Commercial, Government & Defense, Research Institutions) |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Global Space Propulsion Market?

▾ The Global Space Propulsion Market size is estimated to have a value of USD 13.9 billion in 2026 and is expected to reach USD 33.6 billion by the end of 2035.

What is the CAGR of the Global Space Propulsion Market from 2026 to 2035?

▾ The market is growing at a CAGR of 10.3% over the forecasted period.

What factors are driving the growth of the Global Space Propulsion Market?

▾ Technological advancements in electric propulsion and green propellants, regulatory mandates for orbital debris mitigation and government funding for lunar and Mars exploration are the factors driving the growth of the space propulsion market, globally.

What are the major trends in the Global Space Propulsion Market?

▾ Adoption of AI and data-driven telemetry for anomaly prediction and engine health monitoring, and a shift toward cloud-based propulsion telemetry and fleet management platforms are the major trends in the market.

Which region held the largest share of the Global Space Propulsion Market in 2026?

▾ North America is expected to account for the largest market share in 2026, with a share of about 37.8%.

Which region is expected to grow the fastest in the Global Space Propulsion Market?

▾ Asia Pacific is the fastest-growing region in the market during the forecast period.

Who are the key players in the Global Space Propulsion Market?

▾ Some of the major key players in the Global Space Propulsion Market are SpaceX, Blue Origin, Northrop Grumman Corporation, Rocket Lab USA, Inc., IHI Corporation, and many others.

How is the Global Space Propulsion Market segmented?

▾ The market is segmented by propulsion type, component, platform, satellite mass class, orbit class, and end-user.