Market Overview

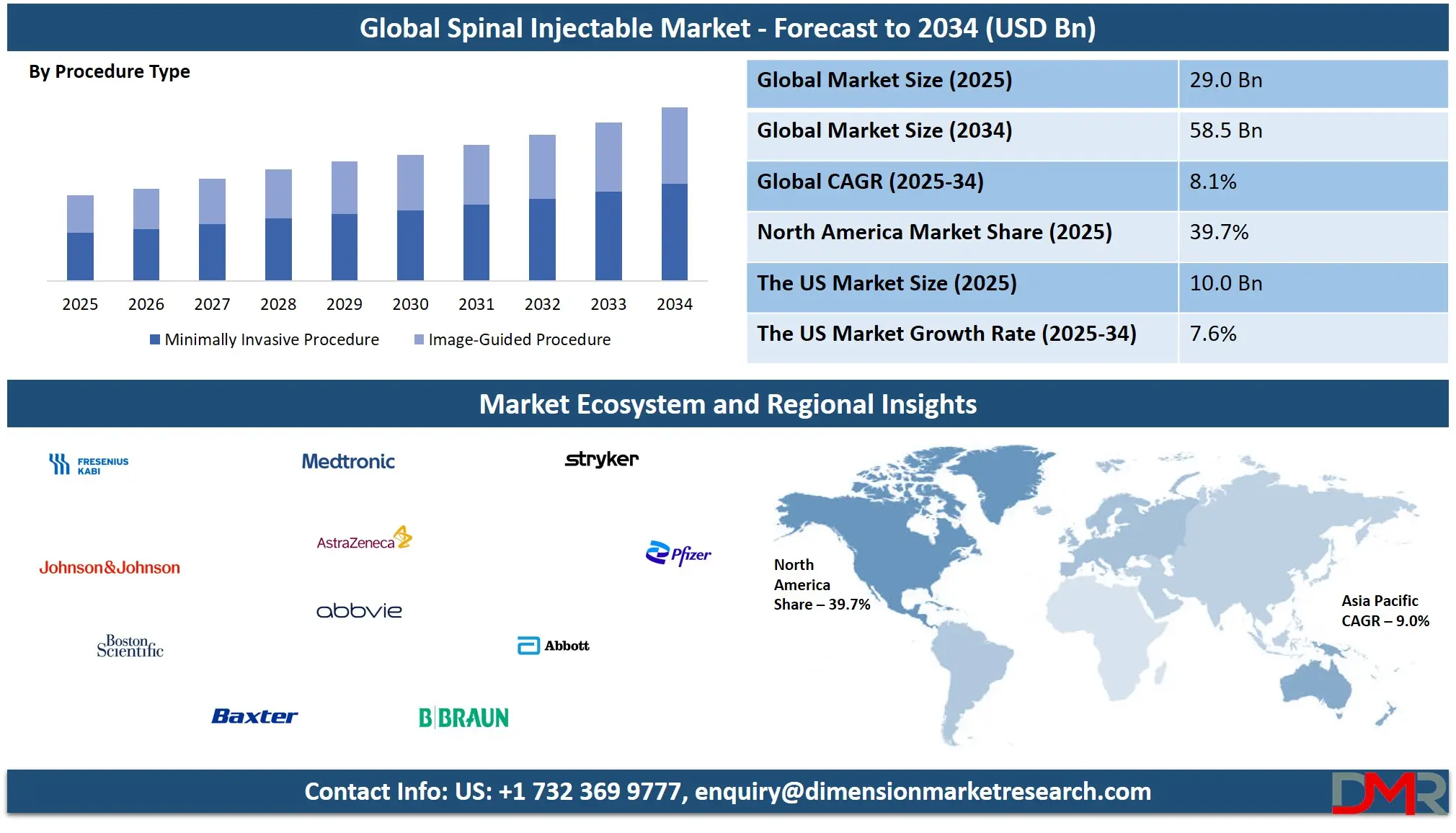

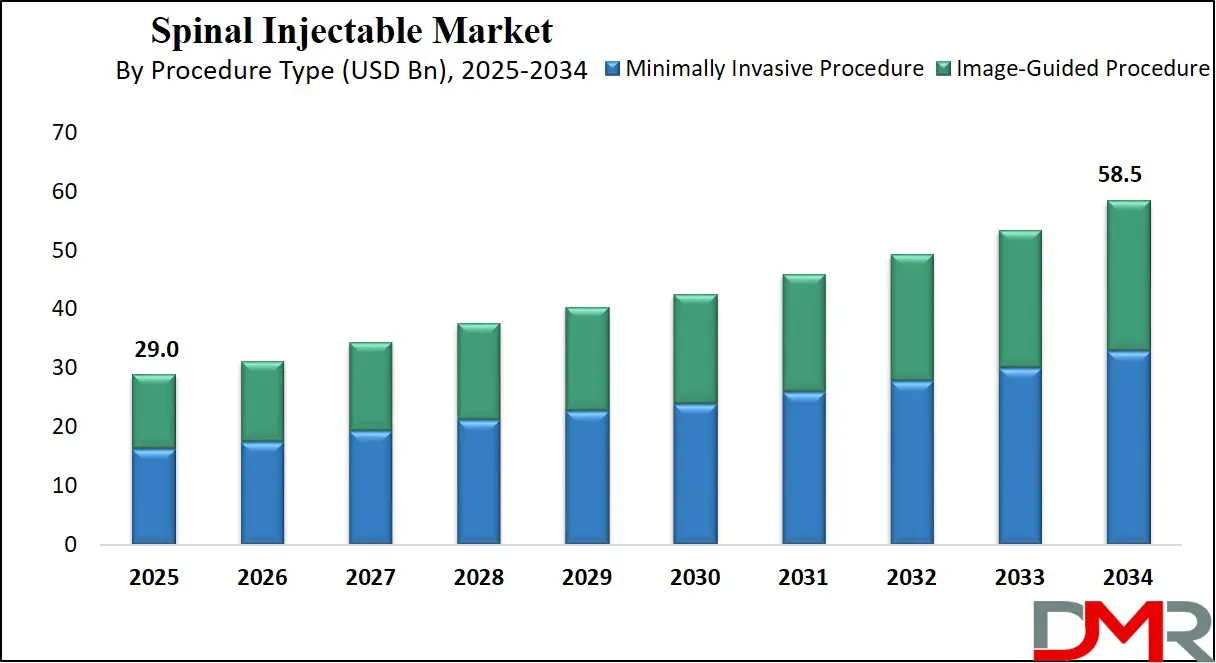

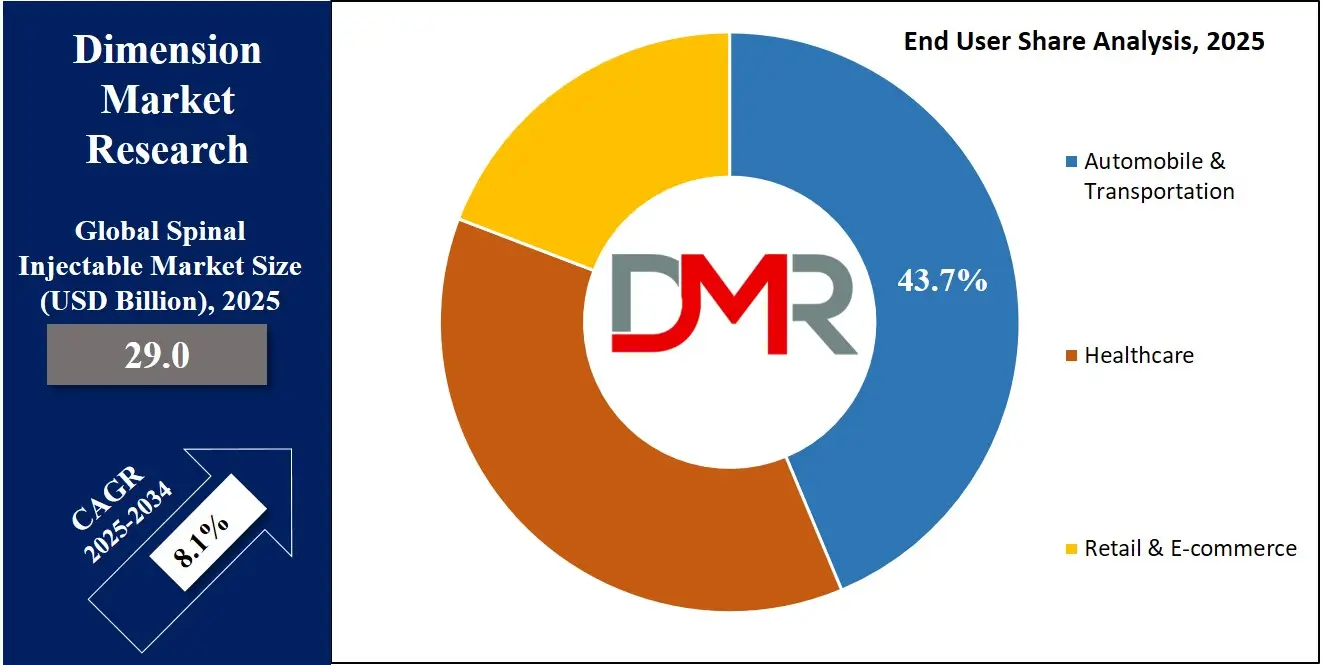

The Global Spinal Injectable Market size is projected to reach USD 29.0 billion in 2025 and grow at a compound annual growth rate of 8.1% to reach a value of USD 58.5 billion in 2034.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Spinal injectables refer to medicines injected directly into the spinal area to diagnose or treat pain, inflammation, and nerve-related conditions. These include corticosteroids, local anesthetics, hyaluronic acid–based injectables, biologic and regenerative therapies like platelet-rich plasma and stem cell injectables, opioid and non-opioid pain relievers, and combination formulations. Given through epidural, facet joint, intrathecal, or sacroiliac injections, spinal injectables are widely used in minimally invasive pain management. They support non-surgical treatment across orthopedics, neurology, and pain care, helping reduce hospital stays, recovery time, and procedural risks.

The rise in the cases of chronic spinal conditions such as lower back pain, degenerative disc disease, radiculopathy, and spinal stenosis are increasing the use of spinal injectables. Aging populations, sedentary lifestyles, and higher obesity rates are expanding the number of patients seeking pain relief. At the same time, advances in image-guided techniques like fluoroscopy, CT, and ultrasound are improving accuracy and safety, encouraging wider use in hospitals and specialty clinics.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The market is gradually shifting from traditional corticosteroid injections toward biologic, regenerative, and long-acting formulations that focus on longer-term pain relief and recovery. Better reimbursement support, clearer clinical guidelines, and improved physician training are supporting this transition. Together, these changes show a maturing market moving toward more personalized, effective, and integrated spinal pain management solutions.

The US Spinal Injectable Market

The US Spinal Injectable Market size is projected to reach USD 10.0 billion in 2025 at a compound annual growth rate of 7.6% over its forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The United States represents the most established market for spinal injectables, driven by high prevalence of chronic spinal pain and strong adoption of interventional pain management practices. Advanced healthcare infrastructure, widespread availability of trained pain specialists, and extensive use of image-guided procedures contribute significantly to market strength. Favorable reimbursement frameworks encourage utilization across hospitals, ambulatory surgical centers, and specialty pain clinics. Continuous investment in research, physician training, and biologic therapies further reinforces the US market’s leadership, with strong demand across both diagnostic and therapeutic applications.

Europe Spinal Injectable Market

Europe Spinal Injectable Market size is projected to reach USD 7.3 billion in 2025 at a compound annual growth rate of 8.0% over its forecast period.

Europe’s spinal injectable market is influenced by aging demographics, rising spinal disorder incidence, and strong emphasis on minimally invasive therapies. Regional healthcare systems prioritize cost-effective interventions that reduce hospitalization and long-term disability. Regulatory harmonization across European countries supports standardized adoption of spinal injectables. The region also benefits from increased investment in regenerative medicine research and adoption of advanced imaging-guided procedures. Steady innovation, combined with public healthcare funding and expanding clinical protocols, continues to drive adoption across major European economies.

Japan Spinal Injectable Market

Japan Spinal Injectable Market size is projected to reach USD 1.5 billion in 2025 at a compound annual growth rate of 7.9% over its forecast period.

Japan’s spinal injectable market is shaped by its rapidly aging population and high prevalence of degenerative spinal conditions. Demand is increasing for non-surgical pain management solutions that preserve mobility and quality of life. Government healthcare initiatives support minimally invasive interventions to reduce surgical burden. Advanced diagnostic infrastructure and physician expertise contribute to steady market growth. However, stringent regulatory approval processes for biologics present challenges, while opportunities exist in expanding regenerative injectable therapies and outpatient pain management services.

Spinal Injectable Market: Key Takeaways

- Market Growth: The Spinal Injectable Market size is expected to grow by USD 27.4 billion, at a CAGR of 8.1%, during the forecasted period of 2026 to 2034.

- By Procedure Type: The minimally invasive procedure segment is anticipated to get the majority share of the Spinal Injectable Market in 2025.

- By End User: Hospitals segment is expected to get the largest revenue share in 2025 in the Spinal Injectable Market.

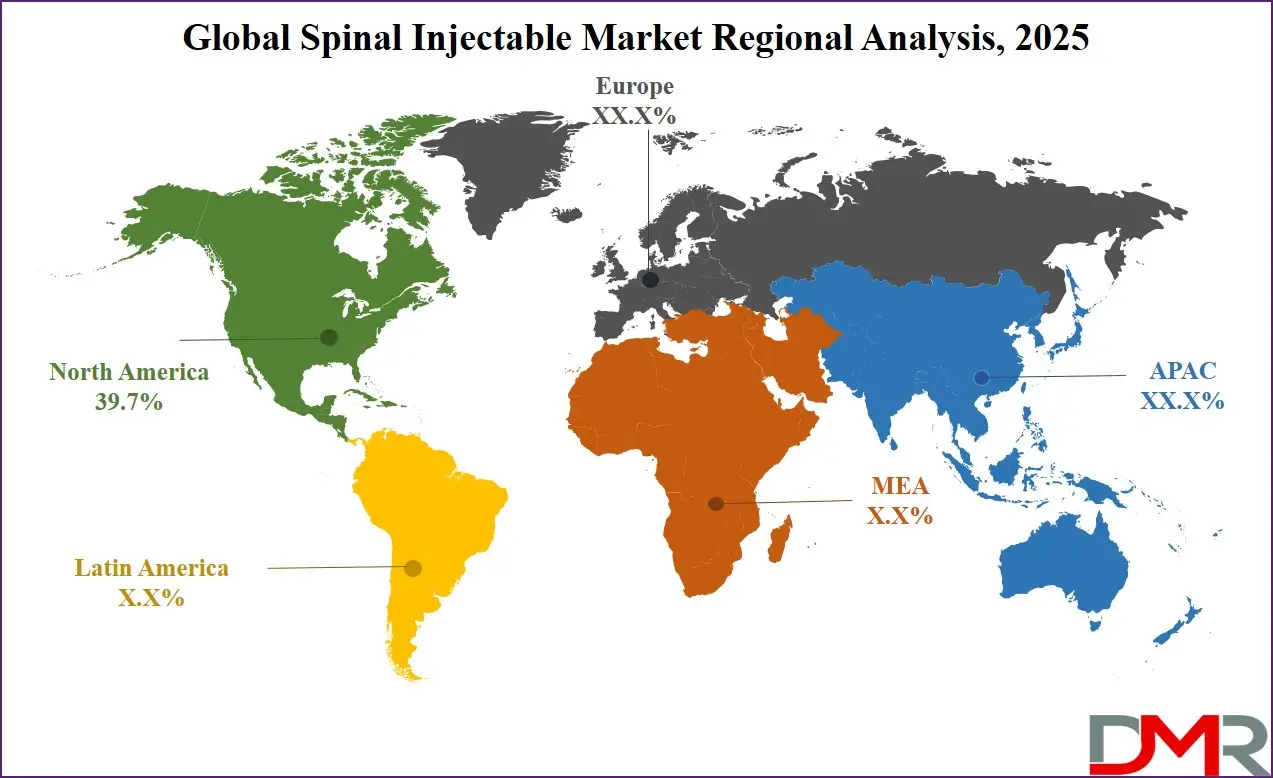

- Regional Insight: North America is expected to hold a 39.7% share of revenue in the Global Spinal Injectable Market in 2025.

- Use Cases: Some of the use cases of Spinal Injectable include diagnostic pain localization, post-surgical pain management, diagnostic pain localization, and more.

Spinal Injectable Market: Use Cases

- Chronic Lower Back Pain Management: Targeted injections reduce inflammation and nerve irritation, improving mobility and daily function.

- Radiculopathy and Sciatica Treatment: Epidural and transforaminal injections alleviate nerve compression-related pain.

- Post-Surgical Pain Management: Injectables manage inflammation and residual pain following spinal procedures.

- Diagnostic Pain Localization: Selective nerve blocks help identify precise pain sources before definitive treatment.

Stats & Facts

- Centers for Disease Control and Prevention reported that over 39% of U.S. adults experienced back pain in 2024.

- National Institutes of Health estimated spinal disorders account for more than USD 134 billion in annual healthcare costs in 2024.

- U.S. Department of Health and Human Services stated minimally invasive pain procedures increased by 11% in 2024.

- European Commission reported musculoskeletal disorders as the leading cause of disability in Europe in 2024.

- World Health Organization identified lower back pain as the top global cause of years lived with disability in 2024.

- Ministry of Health, Labour and Welfare Japan reported spinal degenerative disorders among the top three causes of chronic pain in 2024.

- Centers for Medicare & Medicaid Services recorded a 9% increase in reimbursement claims for spinal injections in 2024.

- National Health Service UK reported reduced surgical referrals due to increased injectable pain interventions in 2024.

- Organisation for Economic Co-operation and Development projected continued growth in interventional pain management through 2025.

- U.S. Bureau of Labor Statistics noted rising demand for pain management specialists in 2025.

Market Dynamic

Driving Factors in the Spinal Injectable Market

Rising Prevalence of Spinal Disorders

The growing incidence of chronic lower back pain, degenerative disc disease, and spinal stenosis is a major factor driving the spinal injectable market. Aging populations, sedentary lifestyles, obesity, and occupational stress are increasing the global burden of spinal conditions. Spinal injectables provide targeted pain relief and inflammation control without invasive surgery, often delaying or eliminating the need for surgical intervention. Their effectiveness, convenience, and reduced recovery times make them a preferred choice for both patients and healthcare providers, sustaining high procedural demand across hospitals and specialty clinics.

Technological Advancements in Image-Guided Procedures

Innovations in fluoroscopy, CT, and ultrasound-guided injection techniques are enhancing the safety, precision, and effectiveness of spinal injectable procedures. Improved visualization allows accurate delivery of medications to affected nerve roots, reducing complications and improving clinical outcomes. Healthcare facilities increasingly invest in these advanced imaging systems to support minimally invasive interventions. These technological advancements boost physician confidence, increase adoption in both hospitals and outpatient centers, and enable expansion of complex procedures such as facet joint and epidural injections, driving overall market growth.

Restraints in the Spinal Injectable Market

High Procedure and Equipment Costs

The high costs of advanced imaging equipment, specialized injectables, and skilled personnel limit market adoption, especially in smaller healthcare facilities and emerging economies. Upfront investments for fluoroscopy, CT, or ultrasound-guided procedures can be prohibitive. Cost-sensitive patients may also delay or avoid treatment due to affordability concerns. This financial barrier restricts accessibility and slows growth in regions with limited healthcare budgets. Despite clinical benefits, high procedural and equipment expenses remain a significant restraint for widespread adoption of spinal injectable therapies globally.

Regulatory and Safety Concerns

Stringent regulations for biologic and regenerative injectables increase approval timelines and development expenses. Safety concerns, including infection risks, steroid overuse, and inconsistent clinical outcomes, further limit adoption. Manufacturers must conduct extensive clinical validation to meet regulatory standards, delaying product commercialization. Healthcare providers also exercise caution in using newer biologic therapies without long-term outcome data. These regulatory and safety challenges slow market expansion, particularly for advanced regenerative and combination injectables, creating hurdles for both new entrants and established players.

Opportunities in the Spinal Injectable Market

Growth in Regenerative and Biologic Injectables

Biologic and regenerative therapies, including PRP and stem cell injectables, offer strong growth potential by addressing underlying tissue damage rather than only managing symptoms. Rising patient preference for long-term, non-steroidal solutions is increasing adoption. Expanding clinical research, improved treatment protocols, and favorable outcomes enhance physician confidence. These therapies also provide manufacturers with opportunities for premium pricing and product differentiation. As evidence supporting regenerative efficacy grows, the segment is expected to capture an increasing share of the spinal injectable market in hospitals and specialty pain management clinics.

Expansion in Emerging Healthcare Markets

Emerging regions present significant opportunities due to rapid urbanization, rising disposable incomes, and expanding healthcare infrastructure. Increased awareness of minimally invasive spinal treatments and investment in specialty clinics further support adoption. Government healthcare initiatives, insurance coverage expansion, and improved access to trained clinicians are accelerating procedural volumes. These markets offer untapped potential for both conventional and advanced biologic injectables. As healthcare systems in Asia-Pacific, Latin America, and the Middle East continue to modernize, demand for spinal injectables is expected to grow strongly in both hospital and outpatient settings.

Trends in the Spinal Injectable Market

Shift Toward Minimally Invasive Pain Management

Healthcare systems increasingly prioritize minimally invasive procedures to reduce costs, shorten hospital stays, and accelerate patient recovery. Spinal injectables are becoming preferred alternatives to surgery for chronic and post-surgical spinal pain. Hospitals and specialty clinics are adopting epidural, facet joint, and intrathecal injections to manage nerve and musculoskeletal pain efficiently. The trend toward minimally invasive approaches aligns with patient preferences for faster, lower-risk treatments. This shift is driving higher procedural adoption and increased investment in advanced imaging technologies to support precise, targeted delivery of spinal injectables.

Adoption of Combination and Sustained-Release Injectables

Combination formulations and sustained-release injectables are gaining popularity due to improved efficacy and longer-lasting pain relief. These products enhance treatment adherence by reducing the frequency of injections while delivering consistent therapeutic effects. Sustained-release and combination injectables also support personalized care by addressing multiple pain pathways simultaneously. Growing physician confidence, favorable patient outcomes, and evidence-based treatment protocols are encouraging wider adoption in hospitals and outpatient clinics. This trend reflects a focus on patient convenience, treatment efficiency, and long-term spinal health, further driving market growth.

Impact of Artificial Intelligence in Spinal Injectable Market

- AI-Assisted Imaging Guidance: Enhances injection precision and reduces procedural errors.

- Predictive Patient Selection: Identifies patients most likely to benefit from injectable.

- Procedure Planning Optimization: Improves treatment planning and outcome predictability.

- Clinical Decision Support: Assists physicians in selecting optimal injectable types.

- Workflow Automation: Reduces procedural time and operational inefficiencies.

- Outcome Monitoring: Tracks patient response and treatment effectiveness.

- Research Acceleration: Supports data analysis in biologic injectable development.

Research Scope and Analysis

By Product Type Analysis

Corticosteroids remain the leading product type in the spinal injectable market, holding an estimated 38.4% share in 2025 due to their strong anti-inflammatory and pain-relief properties. They are widely used in epidural, facet joint, and sacroiliac joint injections for treating conditions such as spinal stenosis, herniated discs, radiculopathy, and chronic lower back pain. Their fast onset of action, cost-effectiveness, and long history of clinical use make them a preferred first-line treatment among physicians. Standardized dosing protocols, broad availability, and consistent reimbursement support further reinforce their dominance, particularly in hospitals and pain management clinics managing high patient volumes.

Biologic and regenerative injectables are the fastest-growing product segment, driven by rising demand for therapies that address the underlying causes of spinal pain rather than temporary symptom relief. Treatments such as platelet-rich plasma and stem cell–based injectables promote tissue repair, reduce inflammation, and support long-term functional recovery. Increasing patient preference for non-steroidal options and growing clinical evidence supporting regenerative outcomes are accelerating adoption. Although higher treatment costs and regulatory complexity remain challenges, expanding clinical trials, physician training programs, and technological improvements are expected to significantly increase the use of biologic and regenerative injectables across specialty clinics and advanced care centers.

By Indication Analysis

Spinal pain disorders represent the largest indication segment, accounting for a projected 41.6% market share in 2025. Conditions such as chronic lower back pain and degenerative disc disease generate high demand for spinal injectable treatments, especially among aging populations. These injectables help reduce inflammation, relieve nerve compression, and improve mobility, often delaying or eliminating the need for surgery. The segment benefits from well-established clinical guidelines, consistent patient inflow, and strong reimbursement coverage. Widespread awareness among physicians and patients further supports continued dominance, making spinal pain disorders a core contributor to overall market revenue.

Radiculopathy and sciatica are the fastest-growing indications due to rising diagnosis rates and increased demand for targeted nerve pain relief. Epidural and transforaminal injections are commonly used to reduce nerve irritation and provide rapid symptom improvement. Improved diagnostic imaging, greater patient awareness, and earlier intervention are contributing to higher treatment volumes. As sedentary lifestyles and spinal degeneration become more prevalent, demand for injectable therapies addressing nerve-related pain is expected to continue growing, particularly in outpatient and specialty care settings.

By Route of Administration Analysis

Epidural injections dominate the route of administration segment, holding an estimated 47.9% market share in 2025. Their ability to deliver medication directly to inflamed nerve roots makes them highly effective for treating spinal stenosis, herniated discs, and radicular pain. Strong physician familiarity, broad clinical applicability, and consistent patient outcomes support widespread use. The increasing adoption of image-guided epidural techniques further enhances procedural accuracy and safety, reinforcing clinician confidence and sustaining the segment’s leadership across hospitals and specialty clinics.

Facet joint injections are experiencing rapid growth as awareness of facet-related spinal pain increases. Improved diagnostic accuracy allows clinicians to better identify facet joint dysfunction as a pain source. These injections are increasingly used in chronic pain management, particularly for patients unsuitable for surgery. Rising use in outpatient and ambulatory settings, along with growing patient preference for targeted, minimally invasive therapies, is driving strong expansion in this segment.

By Procedure Type Analysis

Minimally invasive procedures account for approximately 56.2% of the spinal injectable market in 2025, driven by lower complication rates, reduced recovery times, and decreased healthcare costs. These procedures align with healthcare system priorities focused on efficiency, patient safety, and faster return to daily activities. Increasing adoption across hospitals, specialty clinics, and ambulatory surgical centers reflects growing confidence in minimally invasive pain management approaches. Their ability to deliver effective outcomes without the risks associated with open surgery continues to fuel widespread acceptance.

Image-guided procedures are the fastest-growing segment, supported by advancements in fluoroscopy, CT, and ultrasound technologies. These techniques improve injection precision, reduce procedural errors, and enhance patient safety. As healthcare facilities invest in advanced imaging systems and clinician training, image-guided procedures are becoming the preferred approach, particularly for complex spinal conditions and high-risk patients.

By End User Analysis

Hospitals dominate the spinal injectable end-user segment with an estimated 44.8% market share in 2025, supported by advanced medical infrastructure, high patient inflow, and access to multidisciplinary clinical teams. They serve as primary centers for complex spinal procedures, image-guided injections, and post-surgical pain management. Hospitals benefit from specialized equipment, trained interventional pain specialists, and integrated pharmacy services that ensure safe and timely administration of injectables. Strong reimbursement support and the ability to manage high-risk and chronic cases further reinforce hospitals’ leading position in the spinal injectable market.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Specialty clinics are experiencing rapid growth as they focus specifically on pain management, orthopedics, and spine care. These clinics attract patients seeking quicker access to treatment, shorter waiting times, and personalized care in outpatient settings. Increasing demand for minimally invasive spinal procedures and targeted injectable therapies supports expansion. Improved diagnostic capabilities and rising patient awareness are further driving adoption. As healthcare systems shift toward outpatient care models, specialty clinics are becoming an increasingly important channel for spinal injectable treatments.

By Distribution Channel Analysis

Hospital pharmacies lead the distribution channel with a projected 49.3% market share in 2025, driven by their close integration with clinical operations and high procedural volumes. They ensure immediate availability of spinal injectables for both inpatient and outpatient procedures, supporting efficient treatment workflows. Centralized procurement systems, strict quality control standards, and coordination with medical teams enhance safety and reliability. Their ability to manage specialized and time-sensitive injectable products strengthens their dominant role within the spinal injectable distribution network.

Online and specialty pharmacies represent the fastest-growing distribution channel due to increased digital adoption and improved pharmaceutical logistics. These channels support the growing demand for specialty, biologic, and regenerative injectables by offering efficient supply management and direct delivery to healthcare providers. Advances in cold-chain storage, inventory tracking, and regulatory compliance are improving reliability. As healthcare providers seek flexible sourcing options and cost efficiencies, online and specialty pharmacies are becoming an increasingly important part of the spinal injectable supply ecosystem.

The Spinal Injectable Market Report is segmented on the basis of the following:

By Product Type

- Corticosteroids

- Methylprednisolone

- Triamcinolone

- Betamethasone

- Local Anesthetics

- Bupivacaine

- Lidocaine

- Ropivacaine

- Hyaluronic Acid–Based Injectables

- Biologic & Regenerative Injectables

- Platelet-Rich Plasma (PRP)

- Stem Cell–Based Injectables

- Opioid & Non-Opioid Analgesics

- Combination Injectables

By Indication

- Spinal Pain Disorders

- Chronic Lower Back Pain

- Degenerative Disc Disease

- Radiculopathy & Sciatica

- Spinal Stenosis

- Herniated / Bulging Disc

- Post-Surgical Pain Management

- Inflammatory Spinal Conditions

By Route of Administration

- Epidural Injections

- Interlaminar

- Transforaminal

- Intrathecal Injections

- Facet Joint Injections

- Sacroiliac Joint Injections

By Procedure Type

- Minimally Invasive Procedures

- Image-Guided Procedures

- Fluoroscopy-Guided

- CT-Guided

- Ultrasound-Guided

By End User

- Hospitals

- Specialty Clinics

- Pain Management Clinics

- Orthopedic Clinics

- Spine Centers

- Ambulatory Surgical Centers

By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online / Specialty Pharmacies

- Direct Sales to Healthcare Providers

Regional Analysis

Leading Region in the Spinal Injectable Market

North America leads the spinal injectable market with an estimated 39.7% share in 2025, supported by a high prevalence of spinal disorders and well-established healthcare infrastructure. The region demonstrates strong adoption of minimally invasive pain management techniques across hospitals and specialty clinics. Favorable reimbursement policies, widespread access to trained interventional pain specialists, and early integration of advanced imaging technologies drive consistent demand. Continuous investment in biologic and regenerative therapies, along with active clinical research and product innovation, further strengthens North America’s leadership and positions the region for sustained market dominance.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Fastest Growing Region in the Spinal Injectable Market

Asia-Pacific is the fastest-growing region in the spinal injectable market, driven by rapid urbanization and expanding access to healthcare services. Increasing awareness of minimally invasive spinal treatments, rising disposable incomes, and a growing elderly population are accelerating demand. Government investments in healthcare infrastructure and pain management services support wider adoption. The expansion of specialty clinics, improvements in diagnostic capabilities, and increasing use of image-guided procedures are further strengthening regional growth. Together, these factors position Asia-Pacific as a key growth engine for the spinal injectable market in the coming years.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The spinal injectable market is moderately competitive, characterized by ongoing product innovation, investment in clinical research, and strategic partnerships. Market participants focus on expanding biologic portfolios, enhancing formulation safety, and improving delivery accuracy. Entry barriers include regulatory compliance, clinical validation requirements, and physician training needs. Companies emphasize differentiation through regenerative therapies, combination injectables, and integration with imaging technologies. Strategic collaborations with healthcare providers and R&D investments are key approaches to strengthening market positioning and sustaining competitive advantage.

Some of the prominent players in the global Spinal Injectable are:

- Pfizer Inc.

- AbbVie Inc.

- AstraZeneca

- Johnson & Johnson

- Medtronic plc

- Stryker Corporation

- Baxter International Inc.

- B. Braun Melsungen AG

- Boston Scientific Corporation

- Abbott Laboratories

- Zimmer Biomet Holdings

- Hikma Pharmaceuticals PLC

- Sun Pharmaceutical Industries Ltd.

- Teva Pharmaceutical Industries Ltd.

- Fresenius Kabi

- Novartis AG

- Sanofi

- Merck & Co., Inc.

- Eli Lilly and Company

- Amgen Inc.

- GSK plc

- Other Key Players

Recent Developments

- In August 2025, Spinal Simplicity announced that IntraLink, an injectable device technology developed to treat symptomatic disc degradation, that has been granted Breakthrough Device Designation from the U.S. Food and Drug Administration (FDA), that accelerates regulatory review and may also provide reimbursement pathways to bring this novel technology to market. Also, it utilizes plant-derived compounds that self-polymerize and attach to collagen fibrils throughout the spinal disc, which mechanically supports the disc to inhibit excessive motion and stabilize the spinal joint.

- In July 2025, Amphix Bio announced its leading treatment for spinal cord injuries (SCI), Amfx-200, received the Orphan Drug designation from the U.S. Food and Drug Administration (FDA). An estimated 18,000 cases of SCI are reported annually in the U.S. and are labeled as a devastating health condition often resulting in permanent paralysis. Amphix Bio elected to fight this with its SCI treatment Amfx-200.

Report Details

| Report Characteristics |

| Market Size (2025) |

USD 29.0 Bn |

| Forecast Value (2034) |

USD 58.5 Bn |

| CAGR (2025–2034) |

8.1% |

| The US Market Size (2025) |

USD 10.0 Bn |

| Historical Data |

2019 – 2024 |

| Forecast Data |

2026 – 2034 |

| Base Year |

2024 |

| Estimate Year |

2025 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors and etc. |

| Segments Covered |

By Product Type (Corticosteroids, Local Anesthetics, Hyaluronic Acid–Based Injectables, Biologic & Regenerative Injectables, Opioid & Non-Opioid Analgesics, Combination Injectables), By Indication (Spinal Pain Disorders, Radiculopathy & Sciatica, Spinal Stenosis, Herniated / Bulging Disc, Post-Surgical Pain Management, Inflammatory Spinal Conditions), By Route of Administration (Epidural Injections, Intrathecal Injections, Facet Joint Injections, Sacroiliac Joint Injections), By Procedure Type (Minimally Invasive Procedures, Image-Guided Procedures), By End User (Hospitals, Specialty Clinics, Ambulatory Surgical Centers), By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online / Specialty Pharmacies, Direct Sales to Healthcare Providers) |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

| Prominent Players |

Pfizer Inc., AbbVie Inc., AstraZeneca, Johnson & Johnson, Medtronic plc, Stryker Corporation, Baxter International Inc., B. Braun Melsungen AG, Boston Scientific Corporation, Abbott Laboratories, Zimmer Biomet Holdings, Hikma Pharmaceuticals PLC, Sun Pharmaceutical Industries Ltd., Teva Pharmaceutical Industries Ltd., Fresenius Kabi, Novartis AG, Sanofi, Merck & Co., Inc., Eli Lilly and Company, Amgen Inc., GSK plc, and Other Key Players |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users) and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days and 5 analysts working days respectively. |

Frequently Asked Questions

How big is the Global Spinal Injectable Market?

▾ The Global Spinal Injectable Market size is expected to reach USD 29.0 billion by 2025 and is projected to reach USD 58.5 billion by the end of 2034.

Which region accounted for the largest Global Spinal Injectable Market?

▾ North America is expected to have the largest market share in the Global Spinal Injectable Market, with a share of about 39.7% in 2025.

How big is the Spinal Injectable Market in the US?

▾ The US Spinal Injectable market is expected to reach USD 10.0 billion by 2025.

Who are the key players in the Spinal Injectable Market?

▾ Some of the major key players in the Global Spinal Injectable Market include Pfizer, AbbVie, Johnson & Johnson, and others.

What is the growth rate in the Global Spinal Injectable Market?

▾ The market is growing at a CAGR of 8.1 percent over the forecasted period.