Market Overview

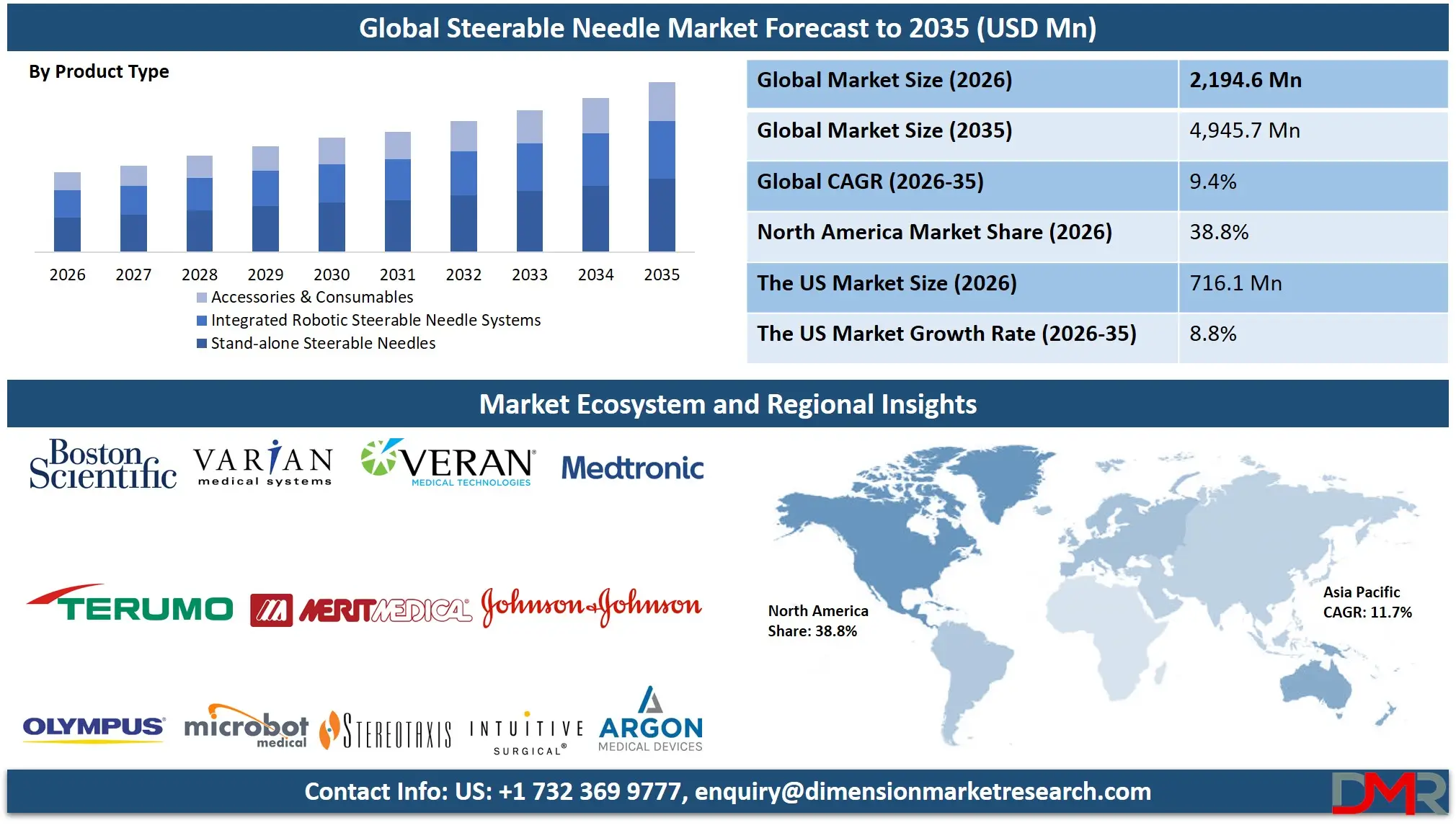

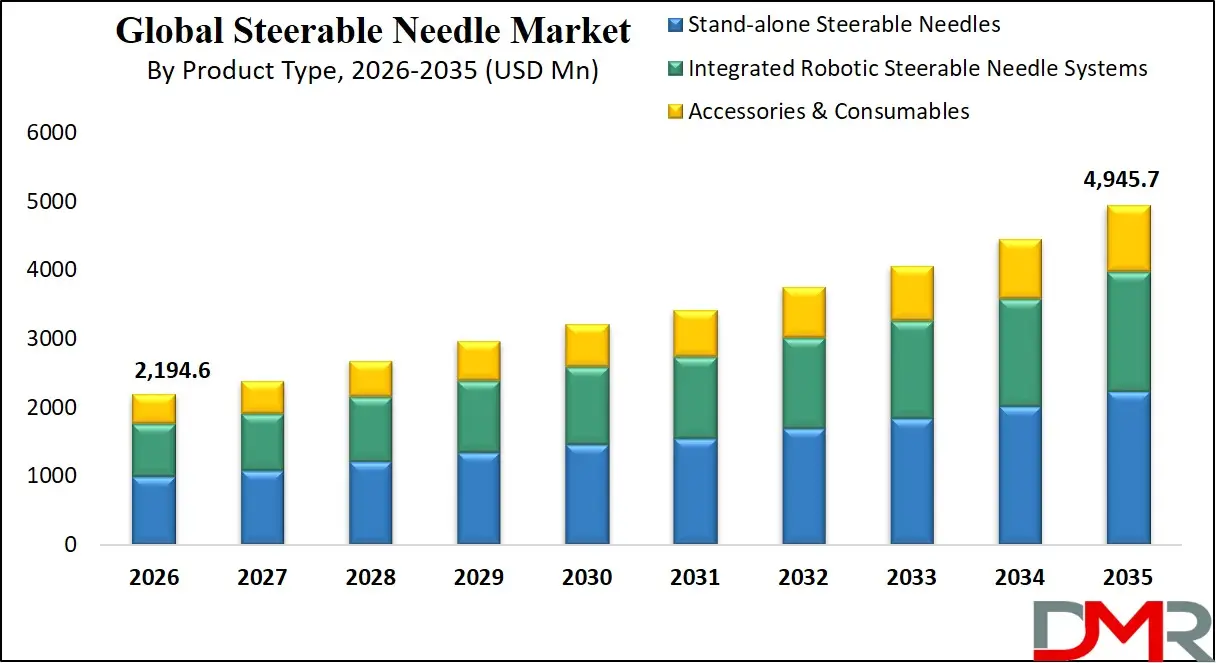

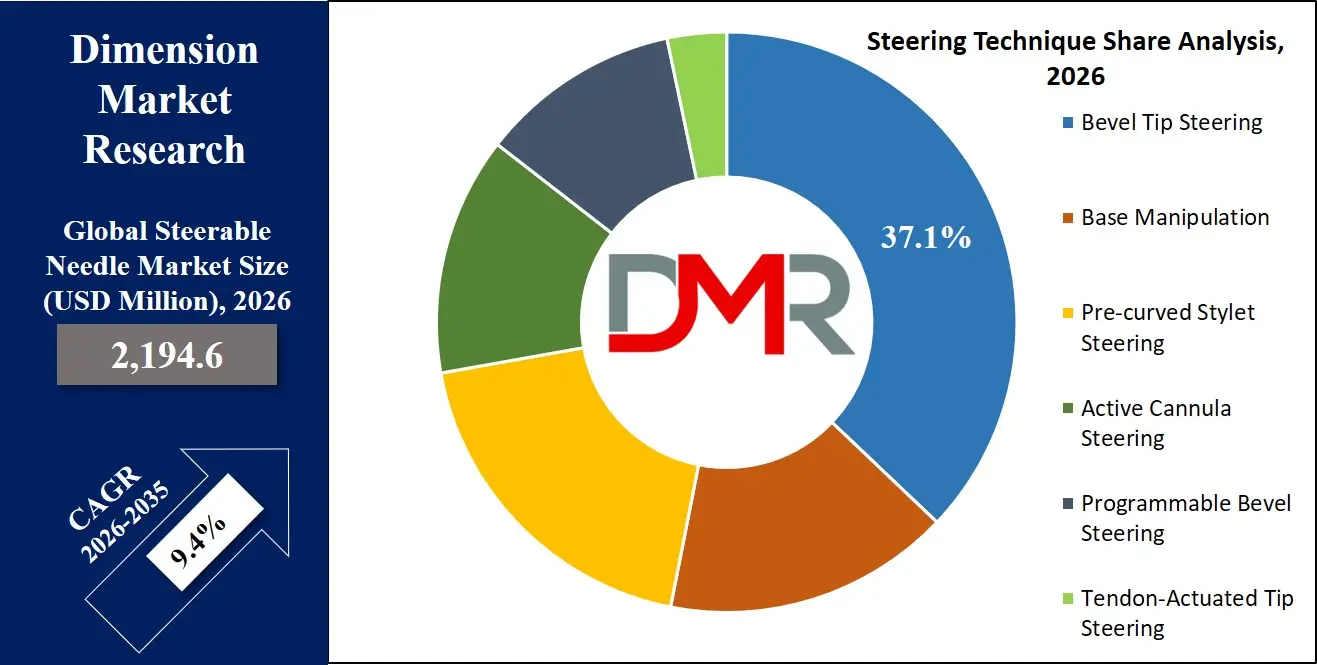

The Global Steerable Needle Market is poised for significant expansion, reaching an estimated USD 2,194.6 million in 2026 and projected to grow at a robust CAGR of 9.4% from 2026 to 2035, to a market value of USD 4,945.7 million by 2035. This strong growth trajectory is fueled by the increasing demand for minimally invasive surgeries (MIS), technological advancements in robotic-assisted systems, and the rising prevalence of cancer and chronic diseases requiring precise biopsy and ablation procedures.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The escalating global incidence of cancers (prostate, lung, liver, and breast), coupled with a growing preference for procedures that offer reduced patient trauma, faster recovery times, and lower healthcare costs, is compelling healthcare providers to adopt advanced precision instrumentation. The integration of real-time imaging guidance (MRI, CT, Ultrasound) with robotic systems is significantly increasing the demand for steerable needles that can navigate complex anatomical pathways to reach targeted tissue with sub-millimeter accuracy.

Furthermore, growing research funding and clinical validation for procedures like percutaneous ablation and targeted drug delivery are accelerating market adoption. Medical device companies and research institutions are increasingly developing articulated, bevel-tip, and magnetically-actuated needles with enhanced dexterity and control. These innovations enable physicians to perform complex interventions that were previously impossible with rigid, straight needles, thereby improving diagnostic yield and therapeutic outcomes.

The shift towards outpatient and office-based lab settings, combined with the development of single-use, disposable steerable needles, is enabling hospitals and ambulatory surgical centers (ASCs) to adopt these advanced technologies cost-effectively. As the global burden of chronic disease rises and healthcare systems prioritize value-based care, the Steerable Needle Market is expected to witness sustained double-digit growth through 2035, driven by the convergence of robotics, imaging, and interventional oncology.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Growing government and private sector investments in precision medicine and the development of advanced surgical robotics further accelerate global adoption. However, barriers such as the high cost of integrated robotic systems, the steep learning curve for clinicians, stringent regulatory approval processes (FDA, CE Mark), and challenges related to real-time image fusion and target motion (e.g., due to breathing) remain. Despite these limitations, the convergence of micro-engineering, control algorithms, and interventional imaging positions steerable needles as a critical tool for the future of minimally invasive interventions through 2035.

The US Steerable Needle Market

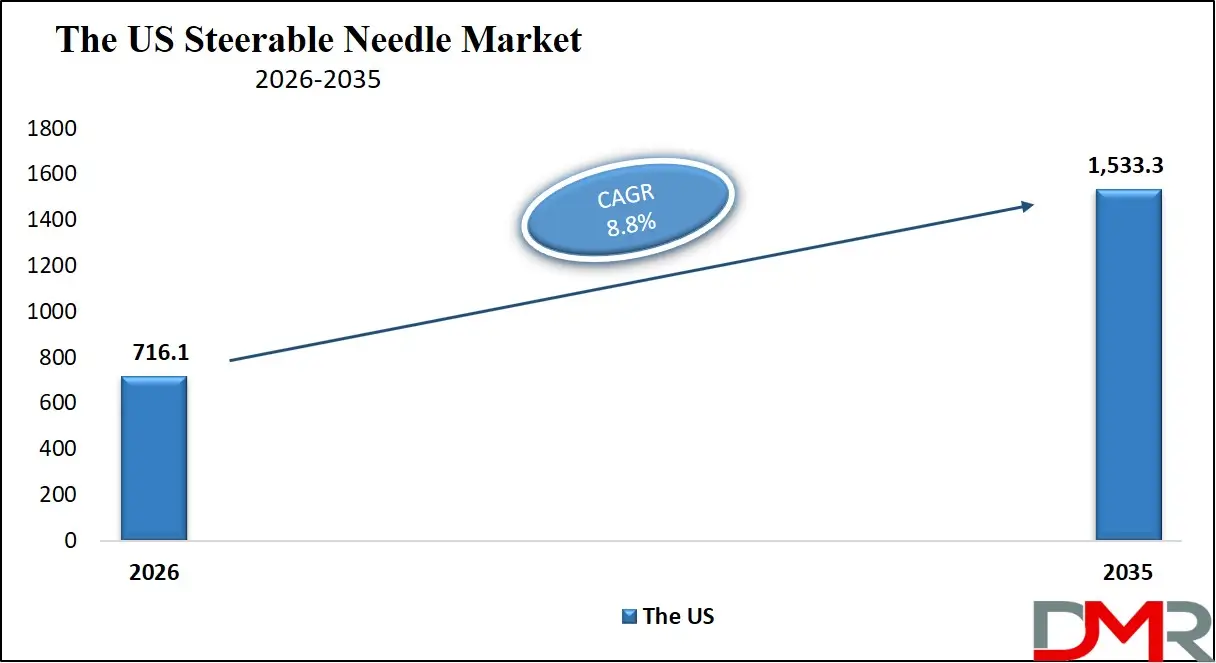

The U.S. Steerable Needle Market is projected to reach USD 716.1 million in 2026 and grow at a CAGR of 8.8%, reaching approximately USD 1,533.3 million by 2035. The U.S. leads global adoption due to its advanced healthcare infrastructure, high healthcare expenditure, and being a primary hub for the development and early adoption of surgical robotics and image-guided therapy systems.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The high prevalence of cancer, particularly prostate and lung cancer, combined with a strong patient preference for minimally invasive diagnostic and therapeutic options, fuels demand. Major cancer centers and academic medical institutions, such as the Mayo Clinic and MD Anderson Cancer Center, are actively involved in clinical research and adoption of these technologies, often in partnership with leading medical device companies like Medtronic and Johnson & Johnson.

U.S. regulatory support from the FDA, including breakthrough device designation pathways, encourages rapid innovation and market entry for novel steerable catheter and needle technologies. The market is witnessing a shift towards integrated robotic platforms (like the Monarch Platform or Ion Endoluminal System) that combine bronchoscopy with steerable instrumentation for peripheral lung nodule biopsy. The focus on early cancer detection and precision ablation techniques has intensified the need for highly accurate, controllable needles, positioning the U.S. as the epicenter of innovation in this space.

The Europe Steerable Needle Market

The Europe Steerable Needle Market is projected to reach an estimated USD 598.7 million in 2026 and is expected to grow at a CAGR of 8.7% from 2026 to 2035, reaching approximately USD 1,260.4 million by 2035. Europe's growth is anchored by its strong medical technology sector, a rapidly aging population, and increasing adoption of advanced surgical techniques under stringent Medical Device Regulation (MDR) oversight.

Countries such as Germany, France, the U.K., and Italy are widely adopting these technologies, driven by well-established public healthcare systems and a high concentration of leading research hospitals. The U.K.'s National Health Service (NHS) and Germany's network of university hospitals are key adopters, focusing on improving cancer survival rates through precision diagnostics.

Europe's strong industrial base in precision engineering and medical imaging, with key players like Siemens Healthineers, supports the development and integration of steerable needle systems. Funding from the EU for research in areas like "minimally invasive diagnostics" encourages cross-border collaboration and clinical studies validating the cost-effectiveness of these technologies. With a sophisticated medical community and a regulatory landscape demanding high levels of clinical evidence, Europe remains a highly advanced and essential region for steerable needle adoption.

The Japan Steerable Needle Market

The Japan Steerable Needle Market is estimated to reach USD 146.3 million in 2026 and is forecast to grow at a CAGR of 7.9% from 2026 to 2035, reaching around USD 289.5 million by 2035. Japan's aging population ("super-aged society") and its government's focus on advanced healthcare innovation under initiatives like "Japan Vision: Health Care 2035" are driving the adoption of technologies that improve quality of life and reduce the burden on caregivers.

The Ministry of Health, Labour and Welfare (MHLW) actively supports the adoption of robotic surgery and advanced imaging to improve treatment outcomes for its growing elderly population, particularly for prevalent conditions like liver, stomach, and lung cancers. Japan's leadership in robotics and precision engineering provides a robust foundation for domestic development and adoption of sophisticated medical devices.

Major Japanese corporations and medical institutions are collaborating to integrate steerable needle technologies into operating rooms, aiming to enhance the precision of biopsies and localized cancer treatments. The cultural emphasis on technical excellence and high-quality medical care, combined with a proactive government strategy for medical innovation, positions Japan as a high-growth, quality-focused market for steerable needle solutions.

Global Steerable Needle Market: Key Takeaways

- Strong Global Market Growth Outlook: The Global Steerable Needle Market is expected to be valued at USD 2,194.6 million in 2026 and is projected to reach USD 4,945.7 million by 2035, showcasing rapid expansion supported by the global shift towards minimally invasive procedures.

- High CAGR Driven by Precision Oncology Demand: The market is expected to grow at an impressive CAGR of 9.4% from 2026 to 2035, fueled by rising cancer incidence, technological advancements in robotic guidance, and the need for more accurate tissue sampling.

- Strong Growth Trajectory in the United States: The U.S. Steerable Needle Market stands at USD 716.1 million in 2026 and is projected to reach USD 1,533.3 million by 2035, expanding at a CAGR of 8.8% due to high healthcare spending and a dominant medical robotics industry.

- Regional Dominance: North America is expected to capture approximately 38.8% of the global market share in 2026, supported by a well-established healthcare system, high rate of technology adoption, and the presence of key robotic surgery platform developers.

- Rapid Advancement in Needle Technologies: Innovations including MRI-compatible needles, robotic steerable sheaths, optical shape-sensing, and bio-inspired needle designs are significantly enhancing accuracy, control, and safety in percutaneous interventions.

- Growing Demand for Biopsies Boosts Adoption: The rising global volume of suspicious lesion detections (e.g., lung nodules via CT screening), coupled with the need for high-quality tissue samples for genomic analysis, is driving sustained demand for precise, reliable steerable biopsy needles.

Global Steerable Needle Market: Use Cases

- Lung Nodule Biopsy: Pulmonologists and interventional radiologists use robotic bronchoscopy platforms with steerable catheters to navigate the tortuous airways of the lung and accurately biopsy small, peripheral nodules for early-stage lung cancer diagnosis.

- Prostate Cancer Diagnosis and Focal Therapy: Urologists use MRI-ultrasound fusion-guided steerable needles for targeted biopsy of suspicious prostate lesions. They are also increasingly used for focal laser or cryo-ablation, treating cancer while preserving healthy tissue.

- Liver Tumor Ablation: Interventional radiologists use steerable needles to access liver tumors, often located near major blood vessels or under the diaphragm, for precise delivery of microwave or radiofrequency ablation energy.

- Deep Brain Stimulation (DBS): Neurosurgeons utilize ultra-thin steerable probes to navigate the delicate structures of the brain and precisely place electrodes for the treatment of Parkinson's disease and essential tremor.

- Fetal Surgery: In specialized centers, surgeons use small-gauge steerable needles to perform in-utero procedures, such as shunting for lower urinary tract obstruction or treating twin-to-twin transfusion syndrome, guided by ultrasound.

Global Steerable Needle Market: Stats & Facts

U.S. National Institutes of Health (NIH) / National Center for Biotechnology Information (NCBI)

- CT-guided needle biopsy procedures have reported diagnostic accuracy rates ranging from 65% to 96% for pulmonary lesions.

- Interventional radiology guidelines report average diagnostic success rates of approximately 93.1% for percutaneous needle biopsies.

- Clinical studies show non-diagnostic biopsy results occur in roughly 2.16% of CT-guided lung biopsy cases.

- Pneumothorax occurs in approximately 31.7% of CT-guided lung biopsy procedures across some clinical cohorts.

- In large pulmonary biopsy studies, bleeding complications occur in about 22.9% of procedures.

- CT-guided lung biopsy diagnostic accuracy is reported at 94.6% for malignancy detection in small pulmonary lesions.

- Sensitivity for malignancy detection using CT-guided core needle biopsy is about 92.0%.

- Specificity of CT-guided needle biopsy for pulmonary malignancies can reach 98.6%.

American Journal of Neuroradiology

- A clinical evaluation of 184 CT-guided core needle biopsies reported an initial diagnostic yield of 93%.

- Adjusted diagnostic yield after follow-up testing was approximately 91%.

- The false-negative rate for CT-guided biopsies was around 2%.

- Diagnostic yield for lesions larger than 10 mm reached about 93%.

Radiological Society of North America (RSNA)

- A clinical analysis of 846 transthoracic needle biopsy procedures reported pneumothorax in 226 patients (26.7%).

- Pneumothorax occurred in 38% of procedures using 18-gauge needles.

- Pneumothorax occurred in 23% of procedures using 19-gauge needles.

- Diagnostic accuracy reached 96% for biopsies performed with 18-gauge needles.

- Diagnostic accuracy reached 92% for biopsies performed with 19-gauge needles.

Technol Cancer Research & Treatment (Clinical Study on Lung Biopsy Techniques)

- A study involving 307 patients undergoing CT-guided lung biopsy reported a 100% technical success rate.

- Diagnostic accuracy was 95.4% for freehand biopsy procedures.

- Diagnostic accuracy increased to 96.8% when guidance devices were used.

- The average procedure time ranged from about 10.8 to 12.8 minutes depending on technique.

- Hemoptysis occurred in approximately 9.7% to 10.5% of lung biopsy procedures.

Society of Interventional Radiology (SIR) / American College of Radiology (ACR)

- Quality improvement guidelines recommend a minimum diagnostic success rate threshold of 82% for percutaneous needle biopsies.

- Earlier guidelines recommended minimum diagnostic yields of about 75% for thoracic needle biopsies.

- Most thoracic needle biopsies typically require 1–3 needle passes to obtain adequate tissue samples.

Society of Abdominal Radiology (SAR)

- Surveys of radiology institutions show 18-gauge needles are the most commonly used size for solid-organ biopsy procedures.

- Among surveyed radiologists, automatic firing biopsy needles are used in the majority of solid organ biopsy procedures.

- 25-gauge needles are the most commonly used size for thyroid fine-needle aspiration procedures.

Oncology Interventional Radiology Clinical Studies

- CT-guided pancreatic biopsy studies show technical success rates of 100% in some clinical cohorts.

- Initial diagnostic accuracy for CT-guided pancreatic biopsies is reported at 92.2%.

- Major complications occur in approximately 1.1% of pancreatic biopsy procedures.

- Minor complications occur in around 2.2% of procedures.

Clinical Oncology & Radiology Research

- Tumor seeding following CT-guided lung biopsy occurs in less than 0.01% of procedures, indicating extremely low risk.

- CT-guided head and neck biopsies represent about 1% of all CT-guided interventional procedures.

Global Steerable Needle Market: Market Dynamic

Driving Factors in the Global Steerable Needle Market

Escalating Global Burden of Cancer and Chronic Disease

The rising global incidence of cancer, particularly in deep-seated and hard-to-reach organs like the lungs, liver, and prostate, is the primary driver for the steerable needle market. Accurate diagnosis via biopsy is the cornerstone of cancer care, and the demand for minimally traumatic, precise tissue sampling is growing. Steerable needles allow physicians to navigate around critical anatomical structures (bone, major vessels) to access these targets, directly addressing the clinical challenge of diagnosing and staging cancer. This capability is also vital for delivering localized therapies, such as ablation, directly to tumors.

Technological Convergence of Robotics and Imaging

The synergy between advanced medical robotics, real-time imaging (CT, MRI, Ultrasound fusion), and needle design is a powerful driver. Robotic systems eliminate hand tremor and enable precise, planned trajectories, while steerable needles provide the necessary dexterity to follow those paths. Integration with imaging allows for closed-loop control, where the needle's position can be tracked and adjusted in real-time relative to the target. This convergence enables entirely new classes of procedures, making previously inoperable or unreachable lesions treatable.

Restraints in the Global Steerable Needle Market

High Acquisition and Procedural Costs

The cost of robotic platforms capable of using steerable needles can be prohibitive (often $500,000 to $2 million), placing them out of reach for many smaller hospitals and clinics, especially in price-sensitive markets. Additionally, the single-use, disposable steerable needle devices themselves carry a significant per-procedure cost compared to standard needles. Justifying this expense requires a clear demonstration of improved patient outcomes and potential long-term cost savings, which can be a barrier to widespread adoption.

Stringent Regulatory and Reimbursement Hurdles

Navigating the regulatory landscape for these combination products (hardware, software, disposable device) is complex and time-consuming. Obtaining FDA or CE Mark approval requires extensive clinical data to prove safety and efficacy. Simultaneously, securing adequate reimbursement from public and private payers is critical for commercial success. Coding and payment for novel procedures often lag behind technological development, creating financial uncertainty for providers and slowing market uptake.

Opportunities in the Global Steerable Needle Market

Expansion into High-Volume Interventional Pulmonology and Radiology

The largest near-term opportunity lies in high-volume procedures like lung nodule biopsy. With the expansion of CT screening for lung cancer, the number of detected suspicious nodules is skyrocketing. Developing user-friendly, cost-effective steerable systems that can be adopted not just by specialized surgeons but also by interventional pulmonologists and radiologists in community hospital settings represents a massive growth opportunity. Partnerships with group purchasing organizations (GPOs) and value analysis committees will be key to penetrating this volume-driven market.

Development of MRI-Compatible and Therapeutic Needles

The opportunity to combine steerable technology with therapeutic delivery is significant. Developing needles that are fully MRI-compatible allows for procedures to be performed under the superior soft-tissue contrast of MRI without moving the patient. Furthermore, integrating therapeutic capabilities, such as delivering focal ablation (cryo, microwave, laser) or targeted drug therapies (e.g., immunotherapy agents) directly into a tumor through the same steerable needle used for diagnosis, creates a powerful "see and treat" platform. This convergence of diagnosis and therapy (theranostics) can create significant new value and improve patient care pathways.

Trends in the Global Steerable Needle Market

Robotic-Assisted Bronchoscopy for Lung Nodules

The rise of platforms like Intuitive's Ion and Medtronic's Monarch is a dominant trend. These systems combine ultra-thin, articulating catheters (steerable sheaths) with shape-sensing technology or electromagnetic navigation to access the peripheral lung. This trend is rapidly shifting the standard of care for lung nodule evaluation from a "watch and wait" approach to a minimally invasive biopsy, driving significant demand for compatible steerable instruments.

Optical Shape-Sensing and Electromagnetic Tracking

Moving away from purely mechanical steering, there is a clear trend towards integrating advanced tracking technologies. Fiber-optic shape-sensing allows the system to know the precise 3D shape and location of the needle in real-time, without radiation. Similarly, electromagnetic tracking integrates with pre-operative CT scans for fusion-guided navigation. These trends enable "closed-loop" control, where the physician can see the needle's exact position relative to the target on a screen, dramatically improving accuracy and confidence.

Global Steerable Needle Market: Research Scope and Analysis

By Product Type Analysis

Among the product-type segments, stand-alone steerable needles are expected to dominate the global steerable needle market. These devices are widely adopted across hospitals and interventional radiology centers because they provide a cost-effective and practical solution for minimally invasive procedures without requiring complex robotic systems. Manual steerable needles and electromagnetically tracked needles allow physicians to navigate anatomical pathways with improved precision while maintaining familiarity with traditional procedural workflows. Compared with integrated robotic systems, stand-alone devices require lower capital investment and minimal infrastructure upgrades, making them accessible to a larger number of healthcare facilities, particularly in emerging healthcare markets.

The increasing prevalence of cancer and the growing demand for image-guided biopsy procedures have further accelerated the adoption of stand-alone steerable needles. Physicians frequently use these devices in procedures such as lung, liver, and prostate biopsies, where navigating around critical structures is essential for accurate tissue sampling. Additionally, the integration of electromagnetic tracking technology in some stand-alone systems has improved needle visualization during imaging-guided procedures, further enhancing procedural accuracy.

While integrated robotic steerable needle systems are gaining attention due to their advanced navigation capabilities and automation, their adoption remains limited by high installation costs and the need for specialized training. As a result, most healthcare facilities continue to rely on stand-alone steerable needles for routine clinical procedures. Ongoing technological improvements in needle flexibility, steerability, and compatibility with imaging systems are expected to sustain the dominance of this segment in the coming years.

By Needle Design Analysis

The bevel-tip flexible needle segment is projected to hold the largest share of the global steerable needle market based on needle design. These needles are widely used because their asymmetrical beveled tip naturally generates lateral forces during insertion, allowing physicians to steer the needle through soft tissue by rotating and adjusting insertion angles. This inherent steering capability makes bevel-tip needles highly effective for navigating complex anatomical pathways and reaching difficult-to-access lesions.

Bevel-tip flexible needles are commonly used in minimally invasive procedures such as tumor biopsies, targeted drug delivery, and ablation therapies. Their flexibility allows them to bend gradually while advancing through tissue, enabling clinicians to avoid critical structures such as blood vessels, nerves, and organs. This capability is particularly important in procedures involving the lungs, liver, and prostate, where precision is crucial for both diagnostic accuracy and patient safety.

Another key factor supporting the dominance of bevel-tip needles is their compatibility with existing imaging guidance systems such as ultrasound, CT, and MRI. Physicians can easily incorporate these needles into current clinical workflows without requiring additional equipment or specialized training. Furthermore, bevel-tip designs are relatively simple to manufacture, making them more cost-effective compared with advanced tendon-actuated or robotic needle systems.

As healthcare providers continue to prioritize minimally invasive procedures and precision medicine, bevel-tip flexible needles remain the preferred choice due to their balance of maneuverability, reliability, and affordability. Continuous improvements in materials and design are expected to further enhance their performance and maintain their strong market position.

By Steering Technique Analysis

Among the various steering techniques used in steerable needle systems, bevel tip steering currently are expected to dominate the market. This technique relies on the asymmetric geometry of the needle tip, which creates differential forces during tissue insertion and enables the needle to follow a curved path when rotated. The simplicity and effectiveness of this approach have made it one of the most widely used steering methods in minimally invasive medical procedures.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Bevel tip steering is particularly valuable in image-guided interventions such as biopsies, ablations, and targeted drug delivery. Physicians can adjust the direction of the needle in real time by rotating the needle shaft, allowing precise navigation toward lesions or treatment sites while avoiding critical anatomical structures. This capability significantly improves procedural accuracy and reduces the risk of complications.

Another factor driving the dominance of bevel tip steering is its compatibility with both manual and robotic systems. Unlike more complex steering mechanisms such as tendon-actuated tips or active cannula systems, bevel tip steering does not require sophisticated mechanical components or additional control systems. This simplicity reduces device costs and facilitates easier integration into existing clinical workflows.

Moreover, extensive clinical research and technological development have been conducted around bevel tip steering, resulting in improved modeling, simulation, and navigation algorithms. These advancements have enhanced the predictability and reliability of needle trajectories during procedures. As a result, bevel tip steering remains the most commonly implemented steering technique in both research and clinical applications within the global steerable needle market.

By Technology Analysis

Based on technology, mechanical steerable needles is forecasted to dominate the global steerable needle market. These devices rely on mechanical design elements such as flexible shafts, bevel tips, and controlled insertion techniques to achieve steering capability within biological tissues. Their reliability, simplicity, and ease of use make them the most widely adopted technology in clinical settings.

Mechanical steerable needles are commonly used in minimally invasive diagnostic and therapeutic procedures, including biopsies, tumor ablation, and targeted drug delivery. Physicians prefer these systems because they provide predictable control over needle direction without requiring complex external equipment or magnetic fields. Additionally, mechanical designs are compatible with standard medical imaging modalities such as CT scans, ultrasound, and fluoroscopy, allowing physicians to guide the needle in real time during procedures.

Another key advantage of mechanical steerable needles is their cost efficiency. Compared with advanced technologies such as magnetic navigation systems or hybrid robotic platforms, mechanical devices are significantly more affordable and easier to manufacture. This affordability allows healthcare facilities, particularly in developing regions, to adopt steerable needle technology without substantial capital investment.

Although magnetic and hybrid steerable needle technologies are emerging and offer promising capabilities for remote navigation and enhanced precision, they remain primarily in research or early clinical adoption stages. Consequently, mechanical steerable needles continue to dominate the market due to their proven performance, accessibility, and widespread acceptance among medical professionals.

By Needle Gauge Analysis

The 19–22 gauge segment is projected to dominate the steerable needle market based on needle gauge. This gauge range is widely preferred in clinical practice because it offers an optimal balance between needle flexibility, maneuverability, and tissue sampling capability. Needles within this size range are commonly used in both diagnostic and therapeutic procedures, particularly in image-guided biopsies.

In biopsy procedures, 19–22 gauge needles allow physicians to obtain sufficient tissue samples for histopathological analysis while minimizing patient discomfort and procedural complications. These needles are thin enough to reduce tissue trauma yet strong enough to maintain structural integrity during insertion and steering. As a result, they are widely used in procedures involving organs such as the lungs, liver, prostate, and breast.

Additionally, this gauge range is compatible with various imaging guidance techniques, including ultrasound-guided and CT-guided interventions. The moderate size of 19–22 gauge needles allows clinicians to maintain precise control over needle trajectory while navigating through soft tissues. This capability is particularly important in steerable needle systems, where accurate control is required to reach target lesions.

Although smaller gauges (greater than 22) are sometimes used for fine needle aspiration and larger gauges (less than 19) are used for certain therapeutic procedures, the versatility of the 19–22 gauge range makes it the most widely adopted option. Its ability to support a broad range of diagnostic and therapeutic interventions continues to drive its dominance in the market.

By Application Analysis

Among the application segments, diagnostic applications are expected to dominate the global steerable needle market, with biopsy procedures representing the largest share within this category. The growing global burden of cancer and other chronic diseases has significantly increased the demand for accurate and minimally invasive diagnostic techniques. Steerable needles enable physicians to reach difficult-to-access lesions and obtain tissue samples with higher precision compared with conventional straight needles.

Biopsy procedures such as lung, liver, prostate, and breast biopsies are particularly dependent on precise needle placement. In many cases, tumors are located near vital structures such as blood vessels or nerves, making accurate navigation essential. Steerable needles allow clinicians to adjust the needle trajectory during insertion, improving the likelihood of reaching the target lesion while minimizing the risk of complications.

Fine needle aspiration procedures also contribute to the growth of diagnostic applications. These procedures are widely used for evaluating thyroid nodules, lymph nodes, pancreatic lesions, and lung nodules. The ability of steerable needles to adjust direction in real time enhances the accuracy of sample collection, reducing the need for repeat procedures.

Furthermore, the increasing adoption of advanced imaging technologies and image-guided interventions in hospitals and diagnostic centers is supporting the growth of diagnostic applications. As early disease detection continues to become a priority in healthcare systems worldwide, the demand for steerable needle technologies in diagnostic procedures is expected to remain strong.

By End-User Analysis

Hospitals are projected to represent the largest end-user segment in the global steerable needle market. These institutions perform a high volume of complex diagnostic and therapeutic procedures that require advanced medical devices and specialized clinical expertise. Steerable needles are commonly used in hospital departments such as interventional radiology, oncology, and minimally invasive surgery.

One of the primary factors driving hospital dominance is the availability of advanced imaging infrastructure. Hospitals are equipped with sophisticated diagnostic technologies such as CT scanners, MRI systems, and ultrasound imaging platforms that are essential for guiding steerable needle procedures. The integration of these imaging systems with steerable needle technologies enables clinicians to perform highly precise interventions.

Hospitals also benefit from multidisciplinary medical teams that include radiologists, surgeons, oncologists, and specialized technicians who collaborate in complex procedures. This collaborative environment supports the adoption of advanced medical technologies such as steerable needle systems. Additionally, hospitals often receive higher patient inflow for cancer diagnostics, biopsies, and interventional treatments, further increasing the demand for these devices.

Although ambulatory surgical centers and specialty clinics are gradually adopting minimally invasive technologies, hospitals continue to dominate due to their comprehensive healthcare infrastructure, greater financial resources, and ability to handle complex cases.

The Global Steerable Needle Market Report is segmented on the basis of the following:

By Product Type

- Stand-alone Steerable Needles

- Manual Steerable Needles

- Electromagnetically Tracked Needles

- Integrated Robotic Steerable Needle Systems

- Robotic Platforms

- Navigation & Guidance Software

- Disposable Steerable Needles/Kits

- Accessories & Consumables

By Needle Design

- Bevel-Tip Flexible Needles

- Symmetric-Tip Needles

- Tendon-Actuated Tip Needles

By Steering Technique

- Bevel Tip Steering

- Base Manipulation

- Pre-curved Stylet Steering

- Active Cannula Steering

- Programmable Bevel Steering

- Tendon-Actuated Tip Steering

By Technology

- Mechanical Steerable Needles

- Magnetic Steerable Needles

- Hybrid Steerable Needles

By Needle Gauge

- 19 – 22 Gauge

- Less than 19 Gauge

- Greater than 22 Gauge

By Application

- Diagnostic Applications

- Biopsy

- Lung Biopsy

- Prostate Biopsy

- Liver Biopsy

- Breast Biopsy

- Other Biopsies

- Fine Needle Aspiration (FNA)

- Thyroid Nodule Diagnosis

- Lymph Node Evaluation

- Lung Nodule Assessment

- Pancreatic Lesion Diagnosis

- Therapeutic Applications

- Ablation

- Microwave

- Radiofrequency

- Cryoablation

- Targeted Drug / Brachytherapy Delivery

- Drainage & Aspiration

- Other Applications

By End-User

- Hospitals

- Ambulatory Surgical Centers (ASCs)

- Specialty Clinics & Diagnostic Imaging Centers

Impact of Artificial Intelligence in the Global Steerable Needle Market

- AI for Procedure Planning: AI algorithms analyze pre-operative 3D images (CT/MRI) to automatically segment organs, identify lesions, and map out optimal, collision-free needle pathways, accounting for critical structures and suggesting the best entry point and trajectory.

- AI-Driven Real-Time Guidance: AI acts as a co-pilot during the procedure, fusing pre-operative plans with real-time imaging (ultrasound). It can automatically track the needle tip, predict its future path, and provide auditory or visual cues to the physician if the needle deviates from the plan.

- AI for Target Motion Prediction: AI models can learn and predict organ motion caused by patient breathing or heartbeat. This predictive capability allows the robotic system to dynamically adjust the needle's position or recommend the optimal moment for tissue sampling, improving accuracy in moving targets like lung and liver lesions.

- AI for Diagnostic Image Analysis: AI can be used to analyze the tissue sample images in real-time (e.g., using optical coherence tomography through the needle) to provide immediate feedback to the physician, confirming that the targeted tissue (e.g., cancerous lesion) has been successfully sampled, reducing the need for repeat biopsies.

- Learning from Procedural Outcomes: AI systems aggregate anonymized data from thousands of procedures to identify which planning strategies, needle types, and techniques lead to the highest diagnostic yield and lowest complication rates, continuously refining best-practice guidelines for physicians.

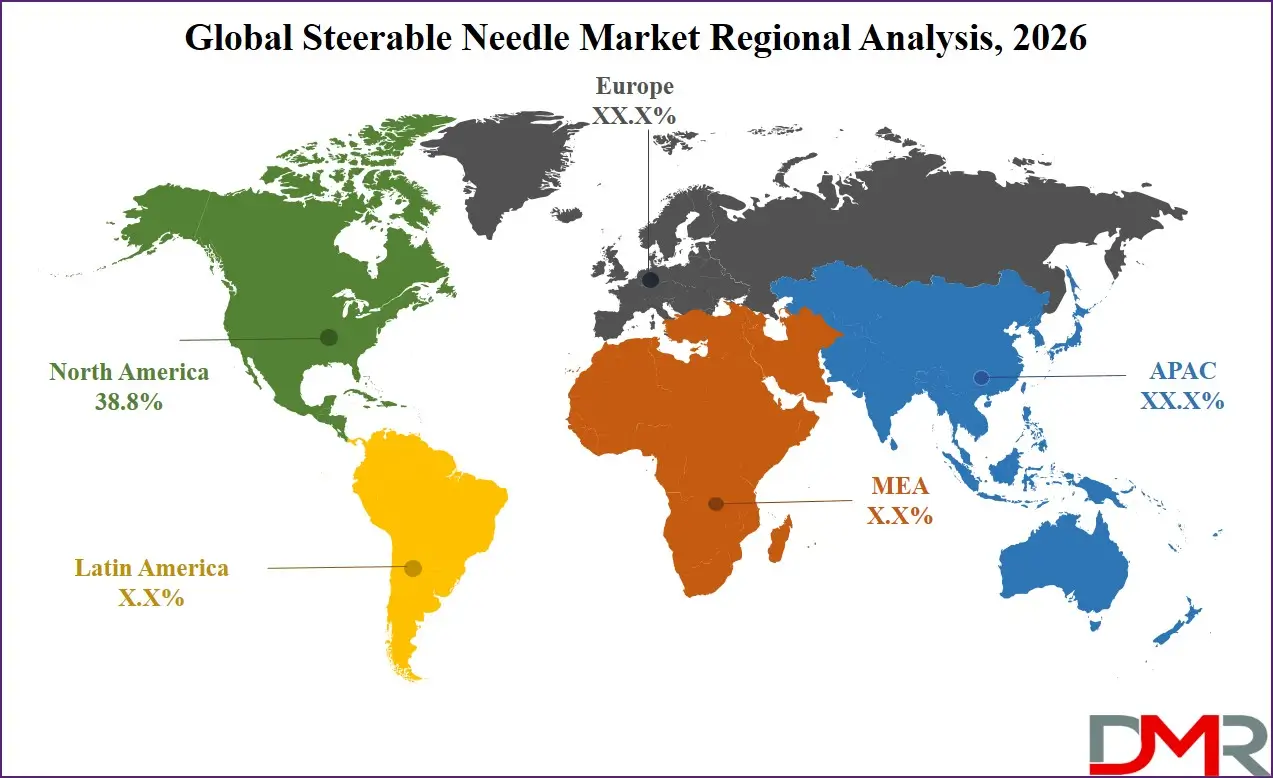

Global Steerable Needle Market: Regional Analysis

Region with the Largest Revenue Share

North America is projected to dominate the regional segment with the highest market share, as it is anticipated to hold 38.8% of the total market revenue by the end of 2026. This leadership is due to its advanced healthcare infrastructure, high per capita healthcare spending, and being the primary hub for leading medical robotics companies like Intuitive Surgical and Medtronic. The region's strong venture capital ecosystem fuels innovation and start-up activity in this space.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The United States, in particular, accounts for the largest share within North America due to its large, well-insured patient population, high prevalence of cancer screening, and a favorable reimbursement landscape for new technologies compared to other regions. Although Asia Pacific is the fastest-growing region, North America continues to hold the largest revenue share due to early adoption of surgical robotics and strong investment in precision medicine.

Region with the Highest CAGR

Asia-Pacific is projected to hold the highest CAGR and is poised to achieve rapid market share growth due to its massive and aging population, rapidly developing healthcare infrastructure, and increasing healthcare expenditure in countries like China, India, and South Korea. The rising incidence of cancer in the region is creating an urgent need for advanced diagnostic and treatment technologies. Governments are investing heavily in modernizing major hospitals and medical research centers.

Local manufacturing initiatives and partnerships between global medtech firms and regional distributors are making these technologies more accessible. The sheer patient volume in countries like China and India provides a compelling economic incentive for the adoption of technologies that can improve procedural efficiency and outcomes. This, combined with a growing middle class seeking access to high-quality medical care, positions APAC as the fastest-growing market for steerable needle systems.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Global Steerable Needle Market: Competitive Landscape

The Global Steerable Needle Market is moderately consolidated, characterized by a mix of large medical device conglomerates, specialized surgical robotics companies, and innovative start-ups. Leading players like Medtronic (with the Monarch Platform) and Johnson & Johnson (through its subsidiary Auris Health, with the Monarch platform) leverage their extensive sales networks and portfolio of complementary technologies to drive adoption. Pure-play robotics innovators such as Intuitive Surgical (with the Ion platform) are driving market dynamics with specialized, high-precision systems focused on specific clinical indications like lung biopsy.

Other significant players include Stereotaxis (for cardiac applications), Hansen Medical (now part of Auris Health), and various emerging companies developing niche steerable technologies for neurosurgery and other specialties. The market also includes component suppliers and manufacturers of advanced materials and imaging software that are critical to the supply chain.

Some of the prominent players in the Global Steerable Needle Market are:

- Medtronic plc

- Johnson & Johnson (Auris Health, Inc.)

- Intuitive Surgical, Inc.

- Stereotaxis, Inc.

- Microbot Medical Ltd.

- Veran Medical Technologies

- Varian Medical Systems, Inc.

- Merit Medical Systems

- Argon Medical Devices

- Elesta S.r.l. (part of BSIC Group)

- Gallery Digital Surgical Technologies

- AngioDynamics, Inc.

- Pajunk GmbH Medizintechnologie

- Cook Medical

- Boston Scientific Corporation

- Terumo Corporation

- Olympus Corporation

- Other Key Players

Recent Developments in the Global Steerable Needle Market

- November 2025: Intuitive Surgical announced an upgrade to its Ion endoluminal system, featuring enhanced shape-sensing technology that improves navigation accuracy in challenging peripheral lung segments, supported by new clinical data presented at a major oncology conference.

- October 2025: Medtronic demonstrated its next-generation Monarch platform at a leading gastroenterology and pulmonology congress, highlighting new capabilities for bronchoscopic ablation of lung tumors, expanding the platform's utility beyond biopsy.

- September 2025: Johnson & Johnson MedTech announced a strategic research collaboration with a top-tier AI imaging company to integrate advanced real-time image fusion algorithms into its robotic surgery platforms, aiming to enhance needle guidance for liver procedures.

- August 2025: A novel start-up, "Flexion Medical," secured USD 50 million in Series C funding to advance its clinical trials for a new MRI-compatible steerable needle designed for precise drug delivery in glioblastoma brain cancer.

- July 2025: A major European consortium received funding to develop a standardized training and certification curriculum for robotic-assisted bronchoscopy, aiming to shorten the learning curve and ensure safe adoption of steerable needle technologies across the continent.

- June 2025: Microbot Medical received CE Mark approval for its LIBERTY robotic system, a single-use, fully disposable platform for neurovascular, peripheral vascular, and urology procedures, signaling a trend towards smaller, more affordable robotic systems.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 2,194.6 Mn |

| Forecast Value (2035) |

USD 4,945.7 Mn |

| CAGR (2026–2035) |

9.4% |

| The US Market Size (2026) |

USD 716.1 Mn |

| Historical Data |

2020 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors and etc. |

| Segments Covered |

By Product Type (Stand-alone Steerable Needles, Integrated Robotic Steerable Needle Systems, Accessories & Consumables), By Needle Design (Bevel-Tip Flexible Needles, Symmetric-Tip Needles, Tendon-Actuated Tip Needles), By Steering Technique (Bevel Tip Steering, Base Manipulation, Pre-curved Stylet Steering, Active Cannula Steering, Programmable Bevel Steering, Tendon-Actuated Tip Steering), By Technology (Mechanical Steerable Needles, Magnetic Steerable Needles, Hybrid Steerable Needles), By Needle Gauge (19–22 Gauge, Less than 19 Gauge, Greater than 22 Gauge), By Application (Diagnostic Applications, Therapeutic Applications), By End-User (Hospitals, Ambulatory Surgical Centers (ASCs), Specialty Clinics & Diagnostic Imaging Centers) |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

| Prominent Players |

Medtronic plc, Johnson & Johnson (Auris Health, Inc.), Intuitive Surgical, Inc., Stereotaxis, Inc., Microbot Medical Ltd., Veran Medical Technologies, Varian Medical Systems, Inc., Merit Medical Systems, Argon Medical Devices, Elesta S.r.l. (part of BSIC Group), Gallery Digital Surgical Technologies, AngioDynamics, Inc., Pajunk GmbH Medizintechnologie, Cook Medical, Boston Scientific Corporation, Terumo Corporation, Olympus Corporation, and Other Key Players |

| Purchase Options |

We have three licenses to opt for (Single User License (Limited to 1 user), Multi-User License (Up to 5 Users) and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days and 5 analysts working days respectively. |

Frequently Asked Questions

How big is the Global Steerable Needle Market?

▾ The Global Steerable Needle Market size is estimated to have a value of USD 2,194.6 million in 2026 and is expected to reach USD 4,945.7 million by the end of 2035.

What is the growth rate in the Global Steerable Needle Market?

▾ The market is growing at a CAGR of 9.4 percent over the forecasted period of 2026-2035.

What is the size of the US Steerable Needle Market?

▾ The US Steerable Needle Market is projected to be valued at USD 716.1 million in 2026. It is expected to witness subsequent growth as it holds USD 1,533.3 million in 2035 at a CAGR of 8.8%.

Which region accounted for the largest Global Steerable Needle Market?

▾ North America is expected to have the largest market share in the Global Steerable Needle Market with a share of about 38.8% in 2026.

Who are the key players in the Global Steerable Needle Market?

▾ Some of the major key players in the Global Steerable Needle Market are Medtronic plc, Johnson & Johnson (Auris Health), Intuitive Surgical, Inc., Stereotaxis, Inc., Microbot Medical Ltd., and many others.