Market Snapshot

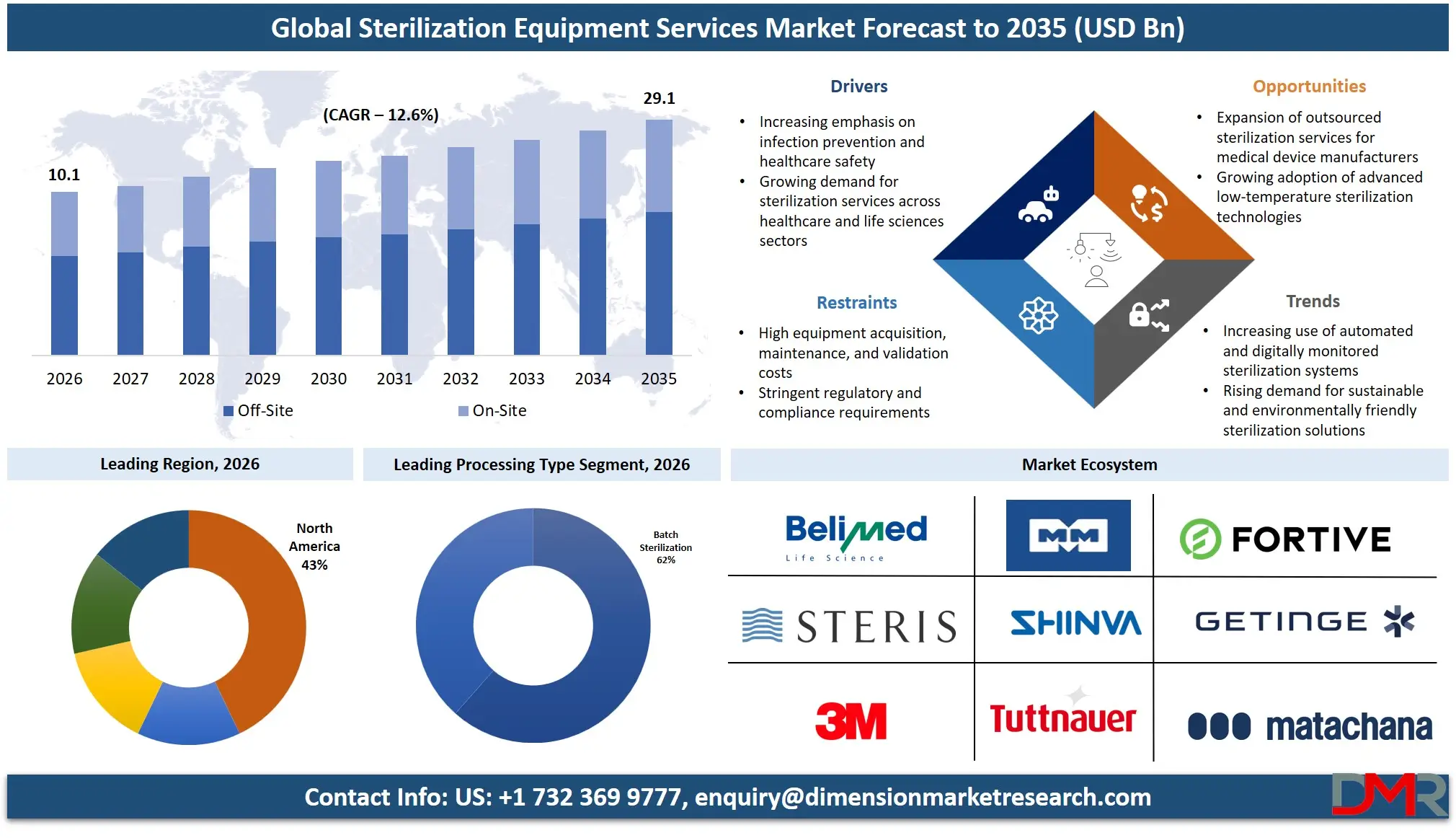

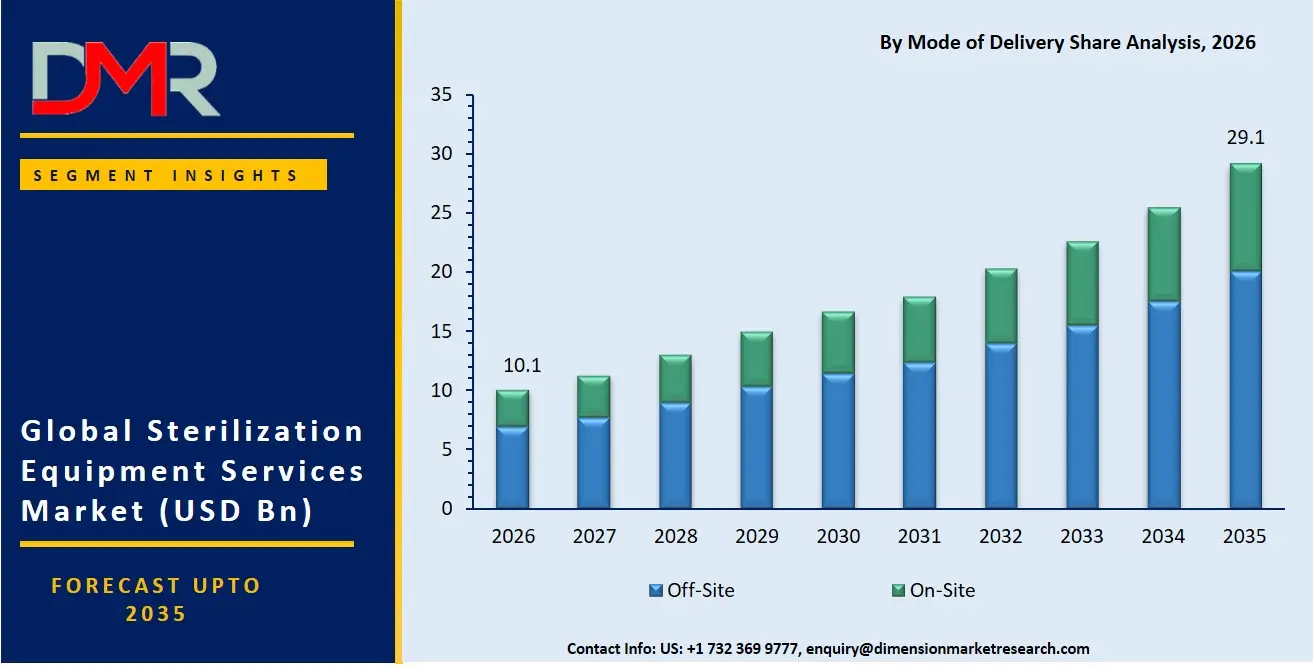

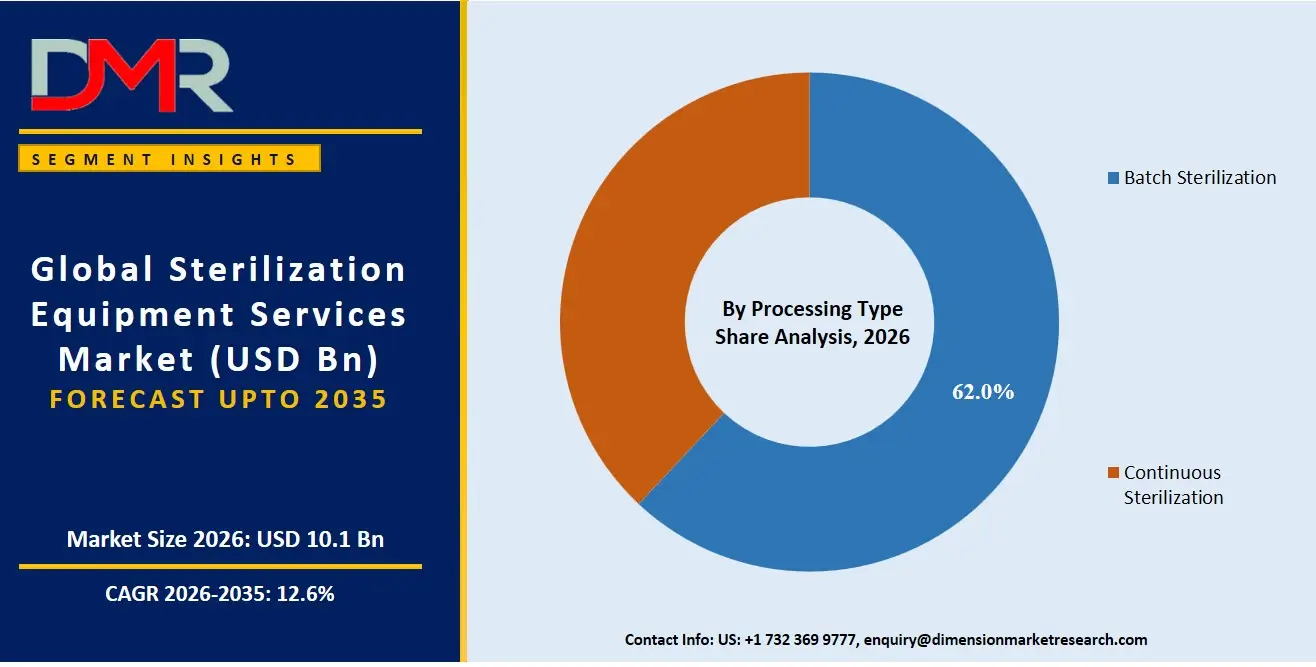

- The Sterilization Equipment Services market size was USD 8.9 Billion in 2025, reached USD 10.1 Billion in 2026, and is projected to hit USD 29.1 Billion by 2035 at a CAGR of 12.6%.

- Ethylene Oxide (EtO) Sterilization leads the By Method segment with a 53.6% revenue share, reflecting EO's unmatched compatibility with heat-sensitive medical device processing.

- Contract Sterilization Services holds a 80.2% share of the By Business Type segment, confirming a structural outsourcing shift among medical device manufacturers.

- Off-Site Sterilization Services commands a 68.7% share of the By Mode of Delivery segment, confirming third-party facility models outpace in-house processing.

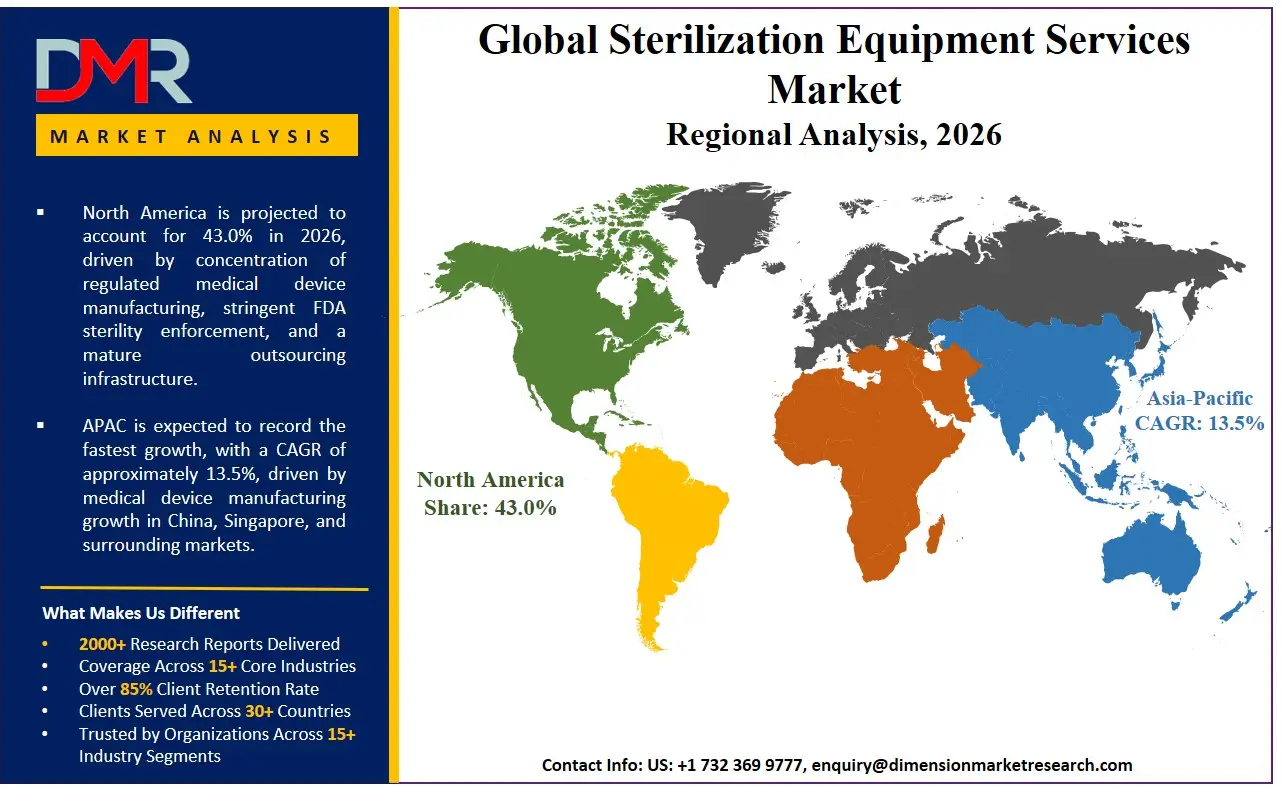

- North America holds the largest regional share at 43.0% of global market revenue, valued at approximately USD 4.3 Billion in 2026.

- The U.S. market is set tp valued at USD 3.7 Billion in 2026 and is projected to reach USD 10.8 Billion by 2035, growing at a CAGR of 12.1%.

- Medical Device Companies represent the largest end-user group, with the U.S. FDA confirming over 20 billion medical devices sterilized annually using EO alone.

Market Overview

The sterilization equipment services market covers the full range of commercial and outsourced services used to eliminate microbial contamination from medical devices, pharmaceutical products, and regulated packaging. This includes contract sterilization, validation services, and consulting, delivered through EO, radiation, steam, and low-temperature technologies. The market excludes the sale of sterilization hardware as standalone capital equipment.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

This market sits at the intersection of healthcare compliance, medical device manufacturing, and infection prevention infrastructure. Every sterile medical device reaching a patient requires certified processing, making sterilization services a non-discretionary input cost rather than a discretionary procurement decision. That structural reality insulates the market from cyclical pressures affecting other healthcare segments, and it is precisely why operators with validated capacity consistently generate recurring contracted volume regardless of broader economic conditions.

Contract sterilization has displaced in-house processing as the dominant service model across the industry. Healthcare providers and device manufacturers are choosing managed service relationships over owned infrastructure, concentrating processing volume with large-scale operators who can absorb regulatory compliance costs and capital upgrade requirements that smaller or internal operations cannot sustain economically.

Key Statistics

- Getinge AB reported a 63% increase in adjusted EBITA to 2.14 billion Swedish crowns in Q4 2024, reflecting strong European demand for sterile reprocessing systems. As reported by Getinge AB.

- STERIS plc's AST segment operating income reached USD 131.1 million in Q4 FY2026, compared with USD 122.2 million in the prior year, driven by pricing improvements alongside volume growth. As reported by STERIS plc.

- Advanced Sterilization Products reported more than 23,000 STERRAD sterilization systems installed globally by 2024, supporting low-temperature hydrogen peroxide workflows for heat-sensitive instruments. As confirmed by ASP.

- China exported sterilization equipment valued at USD 156.39 million in 2024, representing 858,091 units, approximately 50% of global medical sterilizer production volume by units. As reported by the World Bank WITS database.

- Sotera Health operated 48 sterilization locations worldwide as of May 2025, spanning EO, gamma, electron beam, and X-ray processing from a single service network. As confirmed by Sotera Health.

Market Size and Forecast

The Global Sterilization Equipment Services Market size is estimated at USD 10.1 Billion in 2026 from USD 8.9 Billion in 2025, and is projected to reach USD 29.1 Billion by 2035, exhibiting a CAGR of 12.6% during the forecast period.

The U.S. segment is forecast to outpace the global average at a CAGR of 12.1%, reaching USD 10.8 Billion by 2035 from USD 3.7 Billion in 2026. That premium growth rate reflects regulatory enforcement intensity and the concentration of medical device manufacturing in the country, where sterility compliance is non-negotiable and outsourcing adoption continues to deepen. STERIS plc's AST segment posted 9% revenue growth to USD 289.2 million in Q4 FY2026, confirming that both pricing power and volume expansion are active contributors to service revenue trajectory, not just market-level demand growth.

An upside scenario is credible if Asia-Pacific sterilization infrastructure investments scale faster than current projections reflect. If manufacturers accelerate device production shifts to Asia-Pacific markets, regional service volume could pull the global CAGR above 12.6%. A downside scenario emerges if EO emissions regulations force unplanned facility closures faster than transitional enforcement policies permit, compressing processing capacity until alternative sterilization methods reach comparable commercial scale.

Market Dynamics

Non-Discretionary Device Processing Volume Anchors Sustained Service Demand

The U.S. FDA confirmed in 2024 that more than 20 billion medical devices sold annually in the United States are sterilized using ethylene oxide. This volume does not fluctuate with economic cycles. As global device manufacturing capacity expands, the corresponding sterilization service requirement scales proportionally, creating a compounding base of contracted processing volume that established operators convert into long-term revenue.

Regulatory enforcement has further strengthened the outsourcing case. The FDA expanded its 2024 sterility guidance and issued multiple warning letters across sterile processing markets. Manufacturers facing compliance risk cannot absorb internal processing failures. Outsourcing to validated service providers transfers operational and regulatory liability to specialists with established track records, which is why STERIS plc reported total revenues of USD 5.46 Billion from continuing operations for fiscal year 2025, a 6.2% increase compared to fiscal 2024, as reported by Reuters.

EO Emissions Regulations and Product Failures Raise Operational Risk

The U.S. FDA released transitional enforcement policies in November 2024 to prevent medical device supply disruptions during EO facility upgrade periods. This policy intervention signals that regulatory pressure is sufficient to threaten processing capacity, and that the compliance timeline is tightening regardless of transitional relief. Operators must absorb capital expenditure for emissions control upgrades while maintaining throughput commitments to contracted manufacturers.

Product quality failures add a second pressure layer. The FDA issued 2024 safety alerts and recall actions involving multiple Getinge sterile packaging and cardiovascular systems. For a sector where sterility assurance is the core value proposition, any recall event erodes customer confidence and creates switching behavior that disrupts established service relationships. Smaller service providers without the balance sheet scale of dominant operators face a structural disadvantage absorbing both cost pressures simultaneously, which is accelerating consolidation toward larger, better-capitalized contract sterilization operators.

Asia-Pacific Expansion and Annex 1 Compliance Open New Revenue Streams

Asia-Pacific sterilization infrastructure represents a clear expansion opportunity for operators already positioned near high-growth device manufacturing hubs. Life Science Outsourcing doubled its in-house EO sterilization capacity through three new 3M Steri-Vac chamber deployments as of January 2024, targeting mid-sized medical device manufacturers who cannot access large-operator volume minimums. The mid-market segment is a structurally underserved tier where second-tier service providers can build defensible volume without competing directly against the two dominant operators.

EU GMP Annex 1 compliance requirements create a distinct revenue driver in the validation and consumables segment. Regulatory-driven product adoption cycles, where compliance mandates purchasing decisions rather than discretionary procurement, represent the most predictable revenue opportunity in the market. Operators with validated documentation and inspection-enabled consumable lines are best positioned to capture pharmaceutical-sector volume as Annex 1 enforcement activity continues to expand across European markets.

Market Trends

X-Ray Adoption and FDA Oversight Intensity Are Reshaping Sterilization Infrastructure

X-ray sterilization is moving from a niche alternative to a mainstream processing platform within commercial contract sterilization networks. Parallel investment by two of the three largest operators in the same technology and timeframe confirms this is a high-conviction infrastructure shift, not an experimental deployment. For early movers that have already invested in validated multi-technology processes and inspection-enabled consumables, the intensifying FDA oversight environment functions as a competitive barrier rather than an operational burden, locking in customers who cannot afford to switch to unvalidated alternatives mid-compliance cycle.

Method / Technique Type Analysis

In 2026, Ethylene Oxide (EtO) Sterilization held a dominant market position in the By Method / Technique Type segment of the Sterilization Equipment Services Market, with a 53.6% share. No competing method currently replicates EO's penetration capability across complex polymer and electronic device geometries at commercial scale, which is why its revenue leadership is structurally anchored rather than cyclically driven.

Gamma Sterilization serves as the primary radiation-based alternative for high-volume device processing, though isotope supply constraints and growing regulatory preference for non-isotope alternatives are shifting long-term investment toward X-ray and electron beam platforms.

Electron Beam Radiation Sterilization operates without radioactive isotopes, removing cobalt-60 supply chain risk, and is increasingly positioned as a complementary platform within multi-technology service networks. Steam Sterilization retains its standard position for heat-stable reusable surgical instruments in hospital central sterile processing departments, where its low per-cycle cost and established validation frameworks sustain volume despite unsuitability for heat-sensitive devices.

Hydrogen Peroxide Sterilization, including vaporized and plasma variants, addresses heat-sensitive device reprocessing in hospital and surgical center settings, with the FDA clearance of the ULTRA GI™ sterilization cycle for duodenoscopes in August 2024 expanding its clinical application range into complex GI endoscopy reprocessing.

X-Ray Irradiation Sterilization is the fastest-expanding radiation modality in commercial contract networks, with investment from both leading operators confirming it is transitioning to a core platform within technology-agnostic service portfolios.

Business Type Analysis

With a 80.2% share, Contract Sterilization Services holds the strongest position in the By Business Type / Service Type segment of the Sterilization Equipment Services Market in 2026. Medical device manufacturers are actively substituting owned infrastructure with contracted processing relationships, concentrating recurring volume with third-party operators and reducing their fixed capital exposure in the process.

Sterilization Validation Services operate alongside contract processing but address a distinct regulatory requirement, carrying higher technical barriers than standard processing contracts and creating margin differentiation for operators with established regulatory expertise.

Sterilization Consulting Services provide regulatory strategy and compliance documentation support to manufacturers navigating sterility assurance requirements across multiple jurisdictions. Consulting revenues are smaller in absolute scale but generate high-value engagements that frequently convert into long-term contract sterilization agreements, making them a strategic customer acquisition channel rather than a standalone revenue line.

Mode of Delivery Analysis

Off-Site Sterilization Services captures 68.7% of segment demand in the By Mode of Delivery segment of the Sterilization Equipment Services Market in 2026, as the economics of centralized processing, shared infrastructure, validated equipment, and pooled regulatory expertise, consistently outperform in-house alternatives for mid-to-large volume device producers.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

On-Site Sterilization Services address manufacturers and healthcare systems that require processing within or adjacent to their own facilities for throughput, logistics, or contamination control reasons. On-site models are growing in relevance where supply chain disruptions have exposed the operational risks of single-location off-site dependency, creating a structurally motivated demand base for modular and portable processing solutions that did not exist at comparable scale five years ago.

End User Analysis

In 2026, Medical Device Companies held the largest revenue share in the By End User / Industry Vertical segment of the Sterilization Equipment Services Market. Every finished sterile device requires certified processing before market release, making sterilization services a non-discretionary input cost embedded in device manufacturing economics rather than a variable procurement decision.

Hospitals and Clinics represent the largest healthcare facility end-user group, operating central sterile processing departments that reprocess reusable surgical instruments between procedures. Pharmaceutical and Biotechnology Companies require sterility assurance for injectable drug products and biologics, where contamination carries direct patient safety consequences drive demand for premium documented service tiers.

Food and Beverage processors and Cosmetics and Personal Care manufacturers apply sterilization services primarily to packaging decontamination under less stringent regulatory frameworks than medical applications, while Research Laboratories maintain stable sterilization demand tied to funding cycles rather than production volumes.

The Packaging Industry operates as a high-volume, specification-driven sub-market that scales directly with pharmaceutical and medical device production output, with Ahlstrom receiving FDA 510(k) clearance in January 2024 for its Reliance® Fusion sterilization wrap as a direct example of how packaging validation intersects with sterilization service requirements.

Processing Type Analysis

In 2026, Batch Sterilization held the largest market share in the By Processing Type segment of the Sterilization Equipment Services Market. Batch processing allows operators to validate a defined load configuration, run full biological and chemical indicator protocols, and release product with complete traceability documentation, a regulatory acceptance standard that continuous processing systems cannot yet replicate across major markets at equivalent credibility levels.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Continuous Sterilization offers throughput advantages for high-volume, uniform product streams where load configuration is consistent and validation can be established for an ongoing process rather than discrete cycles. Adoption is growing in high-volume contract sterilization facilities handling large medical device production runs, particularly on electron beam and X-ray platforms where product moves through an irradiation field at controlled speed and dose rather than in discrete batch configurations.

Contract Service Type Analysis

In 2026, Terminal Sterilization held the largest market share in the By Contract Service Type segment of the Sterilization Equipment Services Market. Regulatory agencies including the FDA and EMA strongly prefer terminal sterilization over aseptic processing where product characteristics permit, which structurally biases contract volume toward terminal methods and insulates this segment from competitive displacement by aseptic alternatives.

Aseptic Processing applies to products whose active ingredients cannot survive terminal sterilization conditions, primarily biologics, certain injectables, and heat-labile pharmaceutical formulations. The complexity and cost of aseptic processing create higher per-unit service fees compared to terminal sterilization, supporting margin differentiation for qualified contract operators who can meet the documentation burden that Annex 1 now demands.

Sterilization Technology Generation Analysis

In 2026, Conventional / Established Technologies held the dominant position in the By Sterilization Technology Generation segment of the Sterilization Equipment Services Market. EO, gamma, steam, and standard hydrogen peroxide systems represent the validated, globally accepted technology base carrying decades of regulatory precedent, established biological indicator protocols, and broad customer familiarity, barriers that next-generation alternatives must overcome before displacing them at scale.

Emerging / Next-Generation Technologies encompass alternative sterilization platforms targeting the limitations of conventional methods, particularly EO's environmental profile and gamma's isotope supply dependency. Supercritical Carbon Dioxide sterilization, Cold Plasma, Pulsed Light and UV-C, and Accelerator-Based Radiation systems each address specific application niches. Aptar's ActivShield™ technology, which received a U.S. federal government contract in October 2024, represents early-stage commercial development within this group, targeting portable sterilization without EO or external power requirements, a positioning that directly addresses two of the most commercially significant constraints in the current technology base.

Key Market Segments

By Method / Technique Type

- Ethylene Oxide (EtO) Sterilization

- Gamma Sterilization (Gamma Irradiation)

- Electron Beam (E-Beam) Radiation Sterilization

- Steam Sterilization

- Hydrogen Peroxide Sterilization (including Vaporized Hydrogen Peroxide / Plasma)

- X-Ray Irradiation Sterilization

- Nitrogen Dioxide (NO₂) Sterilization

- Chlorine Dioxide Gas Sterilization

- Dry Heat Sterilization

By Business Type / Service Type

- Contract Sterilization Services

- Sterilization Validation Services

- Sterilization Consulting Services

By Mode of Delivery

- Off-Site Sterilization Services

- On-Site Sterilization Services

By End User / Industry Vertical

- Medical Device Companies

- Hospitals & Clinics

- Pharmaceutical & Biotechnology Companies

- Food & Beverage

- Cosmetics & Personal Care

- Research Laboratories

- Packaging Industry

By Processing Type

- Batch Sterilization

- Continuous Sterilization

By Contract Service Type

- Terminal Sterilization

- Aseptic Processing

By Sterilization Technology Generation

- Conventional / Established Technologies

- Emerging / Next-Generation Technologies

- Supercritical Carbon Dioxide (scCO₂) Sterilization

- Cold Plasma Sterilization

- Pulsed Light / UV-C Sterilization

- Accelerator-Based Radiation (non-isotope) Sterilization

By Automation Level

- Manual / Conventional Processing

- Semi-Automated Sterilization

- Fully Automated & IoT-Integrated Sterilization

- AI-Driven / Predictive Sterilization Process Management

By Sterilization Service Scope

- Standalone Sterilization-Only Services

- Sterilization + Packaging Integrity Testing

- End-to-End Sterilization + Logistics & Supply Chain Services

- Sterilization + Regulatory Compliance & Documentation Support

By Facility / Service Center Ownership Model

- Dedicated Third-Party Contract Sterilization Facility

- Shared / Tolling Sterilization Facility

- Mobile / Modular On-Site Sterilization Unit

- Hospital / Healthcare Facility-Owned Central Sterile Processing Department (CSPD)

Regional Analysis

In 2026, North America held a dominant position with a 43.0% share, valued at USD 4.3 Billion. The region's leadership reflects the concentration of regulated medical device manufacturing, stringent FDA sterility enforcement, and a mature outsourcing infrastructure that channels processing volume to large-scale contract operators. North America's premium growth trajectory relative to the global CAGR signals that U.S. regulatory tightening and manufacturer outsourcing adoption are compounding each other rather than operating as separate forces.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Europe's sterilization services market is being reshaped by EU GMP Annex 1 compliance requirements, which generated measurable commercial activity throughout 2024 and created documented demand for validation services and inspection-enabled consumables across the region.

Asia Pacific is the highest-investment expansion region for global sterilization operators, driven by medical device manufacturing growth in China, Singapore, and surrounding markets, with both STERIS plc and Sterigenics committing capital to new processing facilities in the region within a 12-month window.

Latin America remains a secondary growth market supported by expanding pharmaceutical manufacturing capacity in Brazil and Mexico, with Medline's strategic supply agreement reaffirmed with Solvita in August 2024 through its Mexicali facility confirming supply chain investment activity in the region.

The Middle East and Africa represent an early-stage market underpinned by healthcare facility expansion across GCC countries and South Africa, with global operators including MMM Group and Matachana maintaining active distribution across more than 100 countries by 2024 to serve developing market healthcare system demand.

Key Regions and Countries

North America

Europe

- Germany

- France

- The UK

- Spain

- Italy

- Rest of Europe

Asia Pacific

- China

- Japan

- South Korea

- India

- Australia

- Rest of APAC

Latin America

- Brazil

- Mexico

- Rest of Latin America

Middle East & Africa

- GCC

- South Africa

- Rest of MEA

Competitive Landscape

The sterilization equipment services market is moderately consolidated at the top, with two operators controlling a disproportionate share of global contract sterilization volume. Below this tier, the market fragments significantly across regional specialists, hospital-focused system suppliers, and niche technology operators. Competitive positioning is shifting away from single-technology leadership toward multi-modal platform capability, as device manufacturers standardize on service partners who can process across EO, gamma, electron beam, and X-ray from a single network relationship.

Geographic expansion and acquisitions are the two primary competitive moves reshaping market structure. Mid-tier operators are building scale through acquisition rather than organic growth, as demonstrated by Instrumentum's expansion across four U.S. states in July 2025 and Getinge's partnership with SteriPro International in November 2025. Capital equipment revenue declines across the sector confirm that manufacturers are exiting the equipment ownership model entirely. Operators that invest in service network scale and validation depth will capture share from those still oriented toward equipment sales, as the structural direction of outsourcing adoption is not reversible at this stage of the market cycle.

Company Profiles

STERIS plc holds the dominant position in the global sterilization equipment services market through its Applied Sterilization Technologies segment, which generated USD 273.9 million in Q4 FY2025 revenue, a 9% year-over-year increase. The company's multi-technology processing expansion across geographies creates a network scale advantage that smaller operators cannot replicate without equivalent capital deployment timelines, making STERIS the default partner for manufacturers seeking validated processing across multiple sterilization methods from a single contracted operator.

Sotera Health Company operates through its Sterigenics contract sterilization segment, which generated USD 198 million in Q4 2025 revenue, a 10.6% year-over-year increase. Its technology-agnostic platform spanning EO, gamma, electron beam, and X-ray positions it as the preferred partner for medical device manufacturers seeking processing flexibility across product lines. Full-year 2025 net revenues of USD 1.164 billion, a 5.7% increase from 2024, confirm that Sotera's multi-location, multi-technology model is capturing outsourcing volume faster than the broader market is growing.

Key Players

- STERIS plc

- Sotera Health Company

- Servizi Italia S.p.A.

- E-BEAM Services, Inc.

- BGS Beta-Gamma-Service GmbH & Co. KG

- Medistri SA

- H.W. Andersen Products Ltd.

- Cretex Companies (Cretex Medical)

- Life Science Outsourcing, Inc.

- Microtrol Sterilisation Services Pvt. Ltd.

- Noxilizer, Inc.

- MMM Group

- B. Braun Medical Ltd

- Stryker Corporation

- Ecolab Inc.

- Fortive Corporation (Advanced Sterilization Products, ASP)

- Belimed AG (Metall Zug AG)

- 3M Company

- SteriPack Group

- Cosmed Group Inc.

- Medline Industries Inc.

- SteriTek, Inc.

- Europlaz Technologies Limited

- Prince Sterilization Services, LLC

- Steripure SAS

- Blue Line Sterilization Services, LLC

- Midwest Sterilization Corporation

- C.G. Laboratories, Inc.

- ClorDiSys Solutions Inc.

- Crothall Healthcare

- SGS SA

- Sterilization Technology, Inc. (STI)

- Getinge AB

- Cardinal Health

- Teva Pharmaceutical Industries Ltd.

- Becton, Dickinson and Company

- Avantti Medi Clear MBP

- CWS International GmbH

- Taisei Kako Co., Ltd.

- NextBeam

- Pro-Tech Design and Manufacturing Inc.

- Doyen Medipharm

- Berkshire Sterile Manufacturing

Supply Chain and Value Chain Analysis

The sterilization equipment services value chain begins with raw material and consumable inputs including sterilization agents such as ethylene oxide gas, cobalt-60 isotopes for gamma irradiation, and hydrogen peroxide formulations, alongside packaging materials including sterilization wrap and pouches. The maximum value in the chain is created at the contract sterilization processing stage, where validated throughput, regulatory documentation, and traceability systems command price premiums over commodity processing. Operators without validated service capacity cannot access this value layer regardless of facility scale.

The most significant supply chain bottleneck sits in isotope supply for gamma sterilization, where pricing leverage and supply tightness create structural input cost risk for gamma-dependent operators that EO and accelerator-based radiation operators do not face. Downstream, the value chain connects sterilization operators to medical device manufacturers, pharmaceutical companies, and hospital systems through long-term service contracts, and Medline's strategic supply agreement reaffirmed with Solvita in August 2024 illustrates how integrated supply chain commitments lock in volume and reduce customer switching behavior. Midland Memorial Hospital's temporary diversion of trauma surgeries in February 2026 due to sterilization equipment issues illustrates the operational consequences of single-source dependency, reinforcing why manufacturers and healthcare systems are building redundancy into their sterilization networks, a trend that benefits multi-technology, multi-location operators over single-facility specialists.

Regulatory Landscape

The sterilization equipment services market operates under one of the most intensive regulatory oversight frameworks in the healthcare sector. The U.S. FDA serves as the primary enforcement authority in North America, having expanded its sterility guidance in 2024 and issued multiple warning letters across sterile processing markets. These enforcement actions carry operational consequences including facility shutdowns and product recalls that directly interrupt sterilization service revenue, making regulatory compliance a core business continuity requirement rather than a peripheral cost center.

Ethylene oxide emissions regulation represents the most commercially significant regulatory pressure reshaping the market. The FDA's transitional enforcement policies released in November 2024 acknowledge the structural dependency of the U.S. healthcare system on EO processing and signal that regulators will balance environmental compliance timelines against patient access risk. Operators that complete emissions upgrades during the transitional window will face fewer operational interruptions than those that delay. In Europe, EU GMP Annex 1 mandates contamination control strategies, aseptic processing validation, and sterility assurance documentation at a level of specificity that requires direct investment in inspection-enabled consumables and validated service partners. Operators without Annex 1-compliant service documentation cannot access European pharmaceutical manufacturer accounts, making compliance a market access requirement rather than a quality preference.

Investment and White Space Analysis

Investment is currently concentrating in two areas: X-ray sterilization infrastructure and Asia-Pacific processing capacity. Both leading operators committing capital to the same technology and geography within a 12-month window confirms that X-ray is the highest-conviction infrastructure bet in the market, driven by the need to reduce gamma isotope dependency and meet EO emissions reduction requirements simultaneously. Asia-Pacific represents the clearest geographic white space in the global sterilization services network, where medical device manufacturing is growing but validated sterilization processing infrastructure remains underdeveloped relative to production volume. Operators that establish validated capacity in Singapore, China, and adjacent markets before regional competitors scale will capture long-term contractual volume from manufacturers building Asia-Pacific supply chains.

The mid-sized medical device manufacturer segment is structurally underserved by the current market, as the volume minimums of dominant operators exclude a meaningful tier of manufacturers who require validated outsourced processing but cannot meet large-operator thresholds. The on-site and modular sterilization segment offers a white space for operators targeting hospital systems and surgery centers unable to rely on off-site processing due to throughput or logistics constraints, with Midland Memorial Hospital's February 2026 trauma surgery diversion illustrating the documented operational cost of inadequate on-site redundancy.

Recent Developments

- April 2026, Sterigenics, a subsidiary of Sotera Health, opened a new X-ray sterilization facility in the Southeast United States, adding irradiation processing capacity for medical device, pharmaceutical, and biopharmaceutical manufacturers.

- April 2026, Getinge AB launched the GSS67N sterilizer platform with validated load capacity of up to 24 trays and 600 pounds at the HSPA conference, enabling sterile processing departments to increase throughput without expanding physical infrastructure.

- February 2026, Midland Memorial Hospital temporarily diverted trauma surgeries due to sterilization equipment issues while working with STERIS to restore operations, highlighting the operational risk of sterilization service disruptions in acute care settings.

- November 2025, Getinge and SteriPro International announced a strategic partnership focused on scalable sterile processing optimization services across North America.

- October 2025, Terumo completed the acquisition of OrganOx to expand into organ preservation and transplantation technologies with relevance to sterile processing workflows.

- August 2025, STERIS plc completed the expansion of its Suzhou, China facility to include X-ray sterilization processing, adding radiation capacity for medical device and pharmaceutical customers across Asia-Pacific.

- July 2025, Sartorius completed its acquisition of MatTek Corp and Visikol Inc. to strengthen cell technology and laboratory services capabilities relevant to sterile bioprocessing workflows.

- July 2025, Instrumentum acquired Sterile Processing Express and Sterile Processing Services of America, expanding off-site sterile processing operations across four U.S. states.

- May 2025, Sterigenics announced expansion investment in a new X-ray sterilization facility in Haw River, North Carolina, to increase irradiation processing capacity for medical devices and biopharma products.

- November 2024, Advanced Sterilization Products received four Medical Device Network Excellence Awards recognizing innovation and environmental impact in sterilization technology.

- October 2024, Aptar received a U.S. federal government contract to advance its ActivShield™ sterilization technology targeting portable sterilization without ethylene oxide or external power sources.

- September 2024, Advanced Sterilization Products expanded commercialization of its ULTRA GI™ Cycle for STERRAD™ sterilizers, enabling terminal sterilization of compatible GI scopes.

- August 2024, STERIS plc announced new EO facility operations in Singapore through a strategic partnership with TOMOE SHOKAI CO., Ltd., securing proximity to Asia-Pacific device manufacturing growth.

- June 2024, Getinge launched the Poladus 150 low-temperature sterilizer, representing continued investment in vaporized hydrogen peroxide systems for heat-sensitive surgical instruments.

- April 2024, Medline announced an agreement to acquire Ecolab's global surgical solutions business, including the Microtek sterile drape product line.

- March 2024, Belimed and RAD Technology Medical Systems completed the FlexSPD portable sterile processing department solution, providing modular sterilization capacity for hospitals and surgery centers.

- January 2024, Ahlstrom received FDA 510(k) clearance for Reliance® Fusion sterilization wrap, improving efficiency and drying performance in surgical instrument sterilization.

- January 2024, Midmark announced that its M11 Steam Sterilizer received the Dental Advisor 2024 Top Product Award for tabletop autoclave performance and sterilization workflow efficiency.

Report Details

| Report Characteristics |

| Market Value (2025) |

USD 8.9 Billion |

| Market Value (2026) |

USD 10.1 Billion |

| Forecast Revenue (2035) |

USD 29.1 Billion |

| CAGR (2026–2035) |

12.6% |

| Base Year for Estimation |

2025 |

| Historic Period |

2020–2024 |

| Forecast Period |

2026–2035 |

| Report Coverage |

Revenue Forecast, Market Dynamics, Competitive Landscape, Recent Developments |

| Segments Covered |

By Method / Technique Type (Ethylene Oxide, Gamma Sterilization, Electron Beam, Steam Sterilization, Hydrogen Peroxide, X-Ray Irradiation, Nitrogen Dioxide, Chlorine Dioxide Gas, Dry Heat), By Business Type / Service Type (Contract Sterilization Services, Sterilization Validation Services, Sterilization Consulting Services), By Mode of Delivery (Off-Site Sterilization Services, On-Site Sterilization Services), By End User / Industry Vertical (Medical Device Companies, Hospitals & Clinics, Pharmaceutical & Biotechnology Companies, Food & Beverage, Cosmetics & Personal Care, Research Laboratories, Packaging Industry), By Processing Type (Batch Sterilization, Continuous Sterilization), By Contract Service Type (Terminal Sterilization, Aseptic Processing), By Sterilization Technology Generation (Conventional / Established Technologies, Emerging / Next-Generation Technologies), By Automation Level (Manual / Conventional Processing, Semi-Automated, Fully Automated & IoT-Integrated, AI-Driven / Predictive), By Sterilization Service Scope (Standalone, Sterilization + Packaging Integrity Testing, End-to-End + Logistics, Sterilization + Regulatory Compliance), By Facility / Service Center Ownership Model (Dedicated Third-Party, Shared / Tolling, Mobile / Modular, Hospital / Healthcare Facility-Owned CSPD) |

| Regional Analysis |

North America – US and Canada; Europe – Germany, France, The UK, Spain, Italy, and Rest of Europe; Asia Pacific – China, Japan, South Korea, India, Australia, and Rest of APAC; Latin America – Brazil, Mexico, and Rest of Latin America; Middle East & Africa – GCC, South Africa, and Rest of MEA |

| Competitive Landscape |

STERIS plc, Sotera Health Company, Servizi Italia S.p.A., E-BEAM Services Inc., BGS Beta-Gamma-Service GmbH & Co. KG, Medistri SA, H.W. Andersen Products Ltd., Cretex Companies, Life Science Outsourcing Inc., Microtrol Sterilisation Services Pvt. Ltd., Noxilizer Inc., MMM Group, B. Braun Medical Ltd, Stryker Corporation, Ecolab Inc., Fortive Corporation (ASP), Belimed AG, 3M Company, SteriPack Group, Cosmed Group Inc., Medline Industries Inc., SteriTek Inc., Europlaz Technologies Limited, Prince Sterilization Services LLC, Steripure SAS, Blue Line Sterilization Services LLC, Midwest Sterilization Corporation, C.G. Laboratories Inc., ClorDiSys Solutions Inc., Crothall Healthcare, SGS SA, Sterilization Technology Inc., Getinge AB, Cardinal Health, Teva Pharmaceutical Industries Ltd., Becton Dickinson and Company, Avantti Medi Clear MBP, CWS International GmbH, Taisei Kako Co. Ltd., NextBeam, Pro-Tech Design and Manufacturing Inc., Doyen Medipharm, Berkshire Sterile Manufacturing |

| Customization Scope |

Customization for segments, region/country-level will be provided. Additional customization can be done based on the requirements. |

| Purchase Options |

We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

Frequently Asked Questions

What is the biggest investment opportunity in this market?

▾ X-ray sterilization infrastructure and Asia-Pacific processing capacity are the two highest-conviction investment areas based on current operator behavior. The market is projected to expand from USD 8.9 Billion in 2026 to USD 29.1 Billion by 2035, representing an incremental revenue opportunity of over USD 20 Billion across the forecast period. Sterilization validation services tied to EU GMP Annex 1 and FDA compliance requirements represent an additional premium-margin opportunity that existing operators are only partially addressing.

Who are the top companies in this market?

▾ STERIS plc and Sotera Health Company are the two dominant operators by revenue and network scale. Getinge AB, Life Science Outsourcing, and Advanced Sterilization Products are among the significant players across contract processing, equipment, and validation service lines.

Which segment is growing fastest in Sterilization Equipment Services Market and why?

▾ Contract Sterilization Services, holding a 80.2% share of the By Business Type segment, is the fastest-expanding tier. Medical device manufacturers are substituting owned sterilization infrastructure with contracted processing relationships to reduce fixed capital exposure and transfer regulatory compliance liability to validated specialists.

Which region is growing fastest in Sterilization Equipment Services Market and why?

▾ The United States, within North America, carries the highest confirmed CAGR at 12.1%, compared to the global rate of 12.6%. Asia-Pacific is the most active region for new facility investment, as validated sterilization processing infrastructure remains underdeveloped relative to the region's device manufacturing output growth.

What is the biggest challenge holding Sterilization Equipment Services Market back?

▾ EO emissions regulations represent the most immediate operational challenge, with facility upgrade costs and compliance timelines creating pressure on processing capacity across North America. Product safety failures, including FDA safety alerts and recall actions involving sterile packaging systems in 2024, add reputational and regulatory risk that can disrupt contracted service relationships and accelerate customer switching toward better-capitalized operators.