Market Overview

Global

Surgical Drainage Devices Market is projected to reach

USD 3.0 billion by the end of 2024 and grow exponentially until an anticipated value of

USD 5.3 billion in 2033 at a

CAGR of 6.6%.

Surgical Drains are implants designed to remove fluid and gas from body cavities or wounds. These drains are tubes placed near surgical sites that help eliminate pus, blood, or other fluids, preventing their accumulation in post-operative patients. They promote the healing process by removing inflammatory mediators, bacteria, foreign objects, and necrotic tissue.

They come in many forms, including passive drains like Penrose drains and active drains like vacuum-assisted or negative pressure systems. These are commonly used in hospitals, ambulatory surgical centers, and clinics following surgeries such as abdominal, orthopedic, and thoracic procedures.

The US Surgical Drainage Devices Market

The US Surgical Drainage Device Market is expected to reach USD 1.1 billion by the end of 2024 and is projected to grow significantly to an estimated USD 1.8 billion by 2033, with a CAGR of 6.2%.

The rising geriatric population in the US is prone to many surgical conditions, which significantly boosts the demand for surgical devices. Technological advancements in surgical drainage systems, improving their efficiency and patient comfort, further drive market growth.

Some of the key trends in the markets are the adoption of minimally invasive surgical techniques, and increasing the demand for advanced and efficient drainage systems.

Key Takeaways

- Market Growth: The global Surgical Drainage Device market is expected to grow by USD 2.1 billion, at a CAGR of 6.6%, during the forecasted period i.e. from 2025 to 2033.

- Market Definition: Surgical Drainage Devices are medical tools used to remove fluids, blood, or pus from surgical sites, preventing accumulation and promoting healing.

- Product Type Analysis: In terms of product, active drains are predicted to lead the global market with a high revenue share of 83.1% in 2024.

- Application Analysis: Thoracic and Cardiovascular Surgeries are forecasted to be one of the leading application segments in the global Surgical Drainage Device market with a market share of 30.4% in 2024.

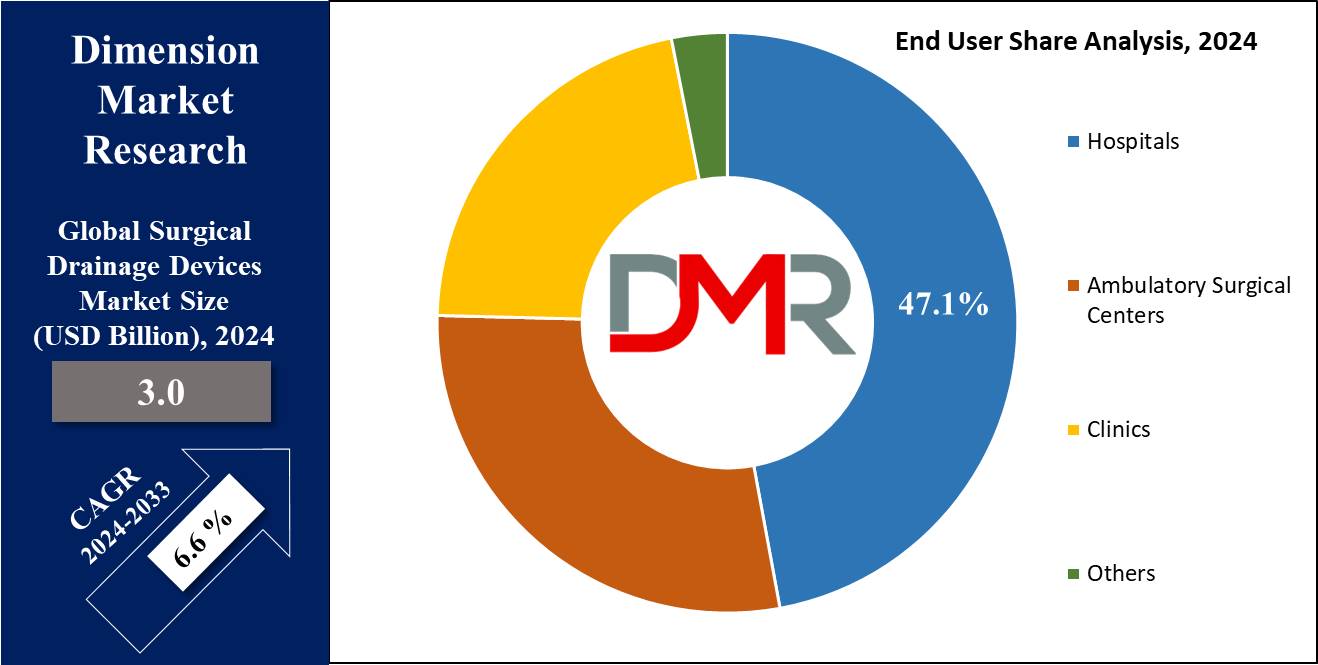

- End User Analysis: Hospitals are projected to lead the global Surgical Drainage Device market in terms of revenue, with a 47.1% market share in 2024.

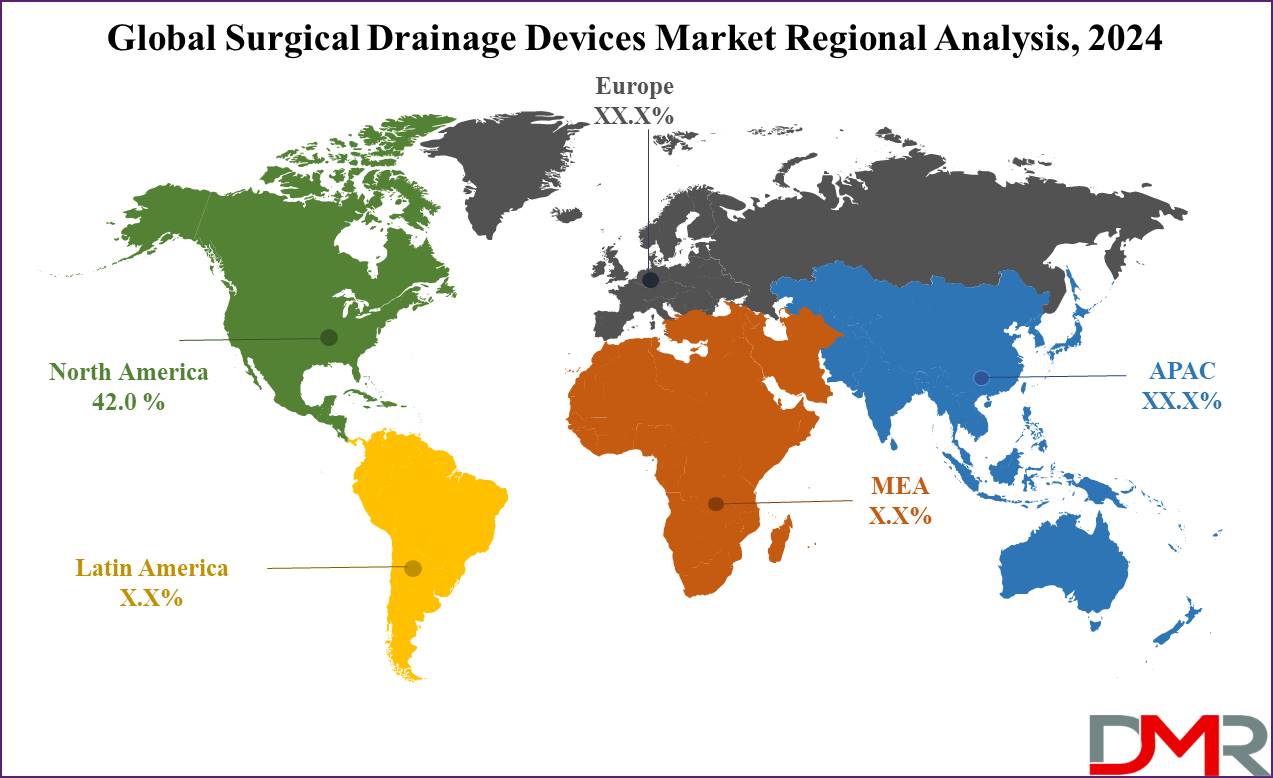

- Regional Analysis: North America is predicted to dominate the global Surgical Drainage Device market with the highest market share of 42.0 % in 2024.

Use Cases

- Post-Operative care: Surgical drainage devices are crucial in post-operative care to remove accumulated fluids, blood, or pus from the surgical site. This helps prevent complications such as hematomas, seromas, and infections, ensuring the wound heals properly.

- Treatment of Abscesses: These drainage devices are extensively used in the treatment of abscesses, which are localized collections of pus caused by infections which is inserted to drain the pus, reduce swelling, and alleviate pain.

- Thoracic Surgery: In thoracic surgery, surgical drainage devices are used to remove air, blood, or fluid from the pleural space, which is the area between the lungs and the chest wall.

- Management of Chronic Wounds: In managing chronic wounds like diabetic ulcers or pressure sores, surgical drainage devices are used to eliminate exudates that can hinder the healing process.

Market Dynamic

Driver

Increasing Number of SurgeriesAs more surgeries become necessary to care for our aging population and to treat sports and road traffic injuries, more surgeries require surgical drainage devices than ever. Further, smoking and alcohol consumption increase surgical treatment requirements driving demand. Furthermore, surgical drainage devices offer numerous advantages like less pain, increased effectiveness, lower infection risks, and drain blockage risk reductions, which further boost their popularity and market demand.

Emergence of Chronic Illnesses

Chronic diseases, such as diabetes, cardiovascular conditions, genetic disorders, inflammation, and cancer significantly exacerbate the need for surgical drainage devices. Surgery may often be required to address complications caused by chronic diseases affecting extraintestinal organs as well as the digestive tract requiring medical drainage devices for effective management.

Restraints

Increased Risk of Bacterial Infection

Surgical drains used for removing fluids and preventing accumulation at surgical sites, can provide a conduit for bacteria to enter the body which can elevate the risk of bacterial infection. This can lead to serious complications, extended hospital stays, and increased medical costs. Infections associated with surgical drains are a significant concern, as they compromise patient outcomes and overall safety. The high incidence of surgical site infections due to drain usage undermines confidence in these devices, thereby hindering their market growth.

Opportunities

Technological Advancements in Drainage Systems

The use of advanced technologies like smart sensors, wireless connectivity, and automated drainage systems presents a significant opportunity in the surgical drainage device market. These innovations can improve patient outcomes by enabling real-time monitoring, reducing the risk of infections, and providing precise fluid management.

Increasing Demand for Minimally Invasive Procedures

There is an increased demand for specialized surgical drainage devices that are compatible with these procedures with the growing preference for minimally invasive surgeries. This trend is driven by the benefits of minimally invasive techniques, including reduced recovery times, lower risk of complications, and smaller scars.

Trends

Regulatory Approvals and Reimbursement Policies

Favorable regulatory approvals and reimbursement policies for surgical procedures and related devices are impacting the market. Governments and healthcare organizations are increasingly recognizing the importance of effective post-operative care, leading to supportive policies that encourage the use of advanced surgical drainage devices.

Research Scope and Analysis

By Product Type

Active Drains is predicted to dominate the global surgical drainage devices market with a revenue share of 83.1 % in 2024. This dominance is due to its efficiency in evacuating fluids and preventing air buildup at the surgical site through suction mechanisms such as vacuum or wall suction. They offer customizable suction settings, improved drainage efficiency, and a lower risk of blockage. These active drains employ negative pressure wound therapy to drain fluid from the surgical site.

These are also known as close drains which are used in deep wounds with significant fluid drainage needs that are connected to a suction device to create negative pressure. The use of negative pressure therapy in active drains effectively removes fluid from the surgical site, ensuring the wound remains dry and minimizing the risk of infection. These are preferred by the surgeon due to their closed system, which prevents exposure to the atmosphere and inhibits bacterial growth.

There are different types of active drains including Blake drain, Jackson-Pratt drain, Redivac drain, EVD & Lumbar drain, Negative pressure wound therapy, Chest tube, and others. Meanwhile, the passive drains segment is projected to be the fastest-growing segment in the surgical drainage devices market. Passive drains are open drains that are inserted into the wound with open ends exposed to the air to facilitate fluid removal. These drains depend on gravity and natural body pressure to remove fluids without the use of suction.

By Application

Thoracic and Cardiovascular Surgeries are projected to hold 30.4% market share by 2024 due to their complexity and riskiness. As cardiovascular diseases increase, their number also increases with it. To properly remove fluid from chest areas more efficiently and reduce risks from medical issues such as pneumonia. Chest drainage systems play a vital role. Due to an increase in surgeries, more surgical drainage devices designed specifically for cardiovascular procedures were implemented into standard operating practices.

These drainage devices play a crucial role in handling any excess fluid or bodily substances that accumulate before, during or post-surgery. Neurosurgeries rank second after thoracic and cardiovascular surgeries due to an increasing prevalence of neurological conditions like stroke and Alzheimer's, which often necessitate surgical intervention. With increased cases comes an increased need for effective drainage solutions during and post neurosurgical operations which fuels the demand for surgical drainage devices market.

By End User

The surgical drainage devices market can be divided by end user into hospitals, ambulatory surgical centers, clinics, and others. Of these categories of end-use, hospitals are projected to account for 47.1% of revenue share by 2024 as they are the primary users of drainage devices. Prioritize patient safety while continuously improving surgical treatments and drainage technologies, they are driving the growth of the market. They adopt new drainage equipment techniques quickly while adhering to guidelines set by regulatory bodies.

As such, surgical drainage devices have become an in-demand item within hospitals; healthcare providers and surgeons choose specific devices based on their effectiveness and experience to offer optimal patient care in many surgical specialties within hospitals. Furthermore, such surgical drainage devices have become the standard of care. Hospitals perform numerous surgical cases from routine to complex operations each year, necessitating an array of surgical drainage solutions to manage post-operation complications effectively and drive market expansion.

Hospitals boasting advanced medical infrastructure and experienced surgical teams are equipped to use high-grade drainage devices that meet current industry standards, while ambulatory surgical centers have experienced explosive growth as they specialize in less complex procedures that don't necessitate extensive drainage, offering outpatient services where patients are released the same day from care.

The Global Surgical Drainage Device Market Report is segmented based on the following

By Product

- Active Drains

- Jackson-Pratt Drain

- Hemovac Drain

- Blake Drain

- Negative Pressure Wound Therapy

- Redivac Drain

- EVD & Lumbar Drain

- Chest Tube

- Others

- Passive Drains

By Application

- Thoracic and Cardiovascular Surgeries

- Neurosurgical Procedures

- Abdominal Surgery

- Orthopedics

- Others

By End User

- Hospitals

- Ambulatory Surgical Centers

- Clinics

- Others

Regional Analysis

North America is expected to dominate the surgical drainage device market with a market

share of 42.0% in 2024, due to intense R&D investments and favorable government policies aimed at combating chronic diseases. Advanced healthcare infrastructure attributed to this region's strong market presence supports extensive research and development activities, which drives the growth of this market.

Central agencies and governments of this region invest heavily in innovative technologies and advanced surgical drainage solutions, driving the development of new and more effective devices. This region is benefitted by its strong healthcare system that includes many hospitals and surgical centers with the capability to utilize and integrate advanced drainage devices into patient care protocols.

Additionally, the favorable reimbursement landscape in the U.S. promotes the use of surgical drainage devices by healthcare providers, enhancing their availability and accessibility for patients. Asia-Pacific is predicted to show notable growth due to the rising penetration of healthcare companies that encourage the commercialization of new medical products, including surgical drainage devices.

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The surgical drainage device market is characterized by intense competition among large and small players alike, offering software and services in domestic as well as international markets. At present, its fragmentation level remains moderate but this trend appears likely to intensify going forward. Major market players have taken steps such as innovating products and services and engaging in mergers and acquisitions to expand the functionality of their portfolios and remain competitive.

Development in this market has focused on surgical devices utilizing negative pressure and vacuum technology for fluid removal and wound healing, such as those from Medtronic, B. Braun Holding GmbH, Acelity Cardinal Health Inc., and Dickinson Company & ConvaTec among many others.

Some of the prominent players in the global surgical drainage devices market are:

- Acelity

- Teleflex Incorporated

- Cardinal Health

- Medtronic

- Cook Medical

- Stryker

- Johnson and Johnson

- B. Braun Melsungen AG

- Smith & Nephew plc

- Becton Dickinson

- Centese

- Others

Recent Development

- In July 2024, BioInteractions’ Commercial Director introduced surface active therapeutics that are being used for the prevention and protection of medical devices against infections which is becoming more and more important, as the number of healthcare-associated infections rises.

- In March 2024, The U.S. Food and Drug Administration issued a Class I recall, the agency’s most serious, for a Medtronic device used to temporarily drain spinal fluid from patients after surgery for a thoracic aortic aneurysm. Medtronic’s Duet External Drainage and Monitoring System Catheter Tubing carries the potential risk of the catheter becoming disconnected, which could cause infections or other problems for patients.

- In November 2023, Argon Medical Devices announced the launch of the Kodiak™ Dual Port Coaxial Introducer Kit for precise and streamlined introduction of diagnostic and therapeutic devices into the vasculature.

- In January 2023, Zimmer Biomet announced to acquisition of Embody, a soft tissue healing development company valued at around USD 275 million which enabled the company to provide advanced solutions to its customers, thus improving its sales prospects.

Report Details

| Report Characteristics |

| Market Size (2024) |

USD 3.0 Bn |

| Forecast Value (2033) |

USD 5.3 Bn |

| CAGR (2024-2033) |

6.6 % |

| Historical Data |

2018 – 2023 |

| The US Market Size (2024) |

USD 1.1 Bn |

| Forecast Data |

2025 – 2033 |

| Base Year |

2023 |

| Estimate Year |

2024 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors and etc. |

| Segments Covered |

By Product (Active Drains, and Passive Drains), By Application (Thoracic and Cardiovascular Surgeries, Neurosurgical Procedures, Abdominal Surgery, Orthopedics, and Others), By End User (Hospitals, Ambulatory Surgical Centers, Clinics, and Others) |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia- Pacific– China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA

|

| Prominent Players |

Acelity, Teleflex Incorporated, Cardinal Health, Medtronic, Cook Medical, Stryker, Johnson and Johnson, B. Braun Melsungen AG, Smith & Nephew plc, Becton Dickinson, Centese, and Other Key Players |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users) and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days and 5 analysts working days respectively. |

Frequently Asked Questions

The Global Surgical Drainage Device Market size is estimated to have a value of USD 3.0 billion in 2024 and is expected to reach USD 5.3 billion by the end of 2033.

North America is expected to be the largest market share for the Global Surgical Drainage Device Market with a share of about 42.0 % in 2024.

Some of the major key players in the Global Surgical Drainage Device Market are Medtronic, B. Braun Holding GmbH, Acelity, Cardinal Health, Inc., Becton, Dickinson and Company, and ConvaTec. and many others.

The market is growing at a CAGR of 6.6 percent over the forecasted period.

The US Surgical Drainage Device Market size is estimated to have a value of USD 1.1 billion in 2024 and is expected to reach USD 1.8 billion by the end of 2033.