What is the Thermoplastic Polyurethane Films Market Size?

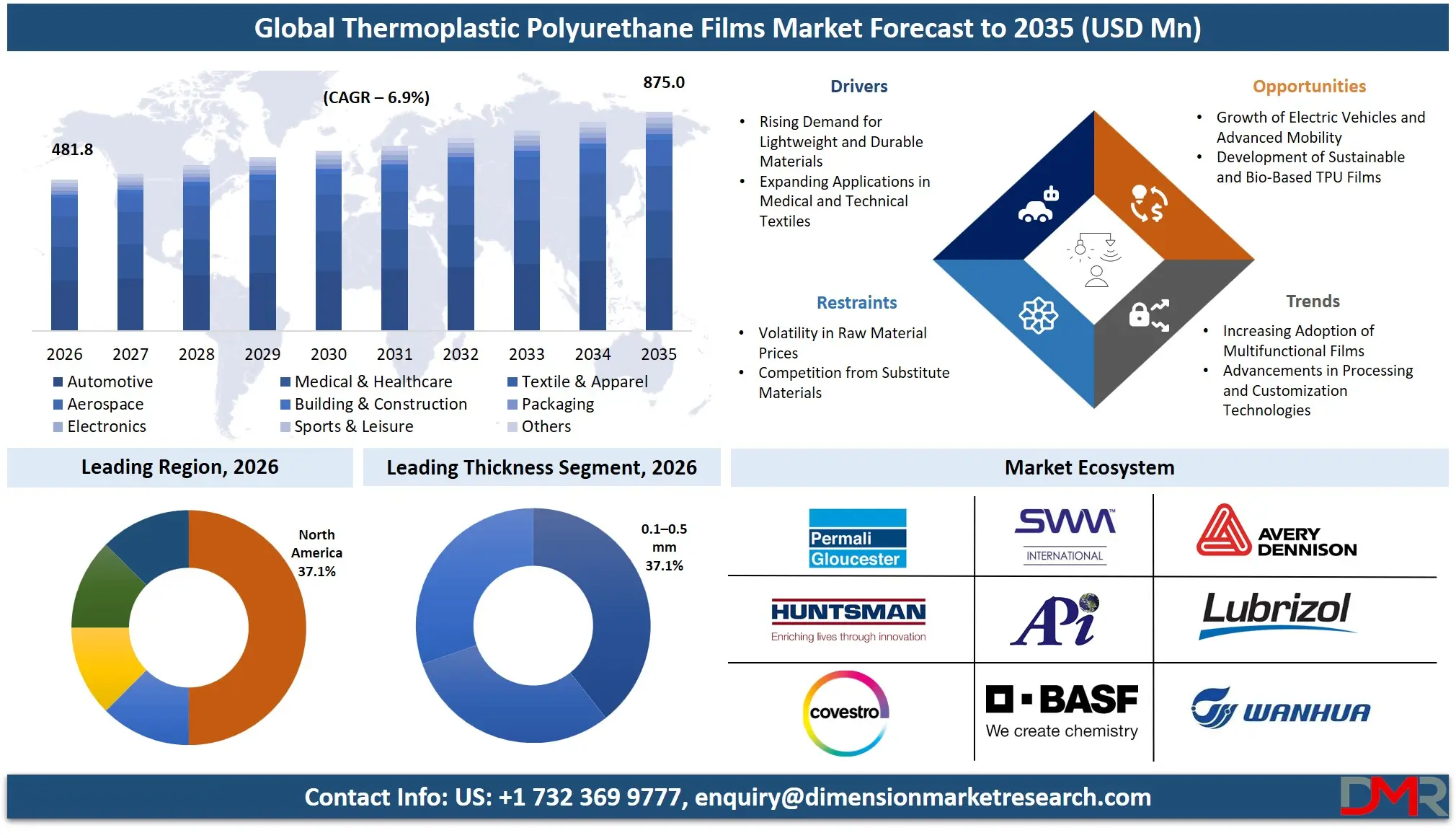

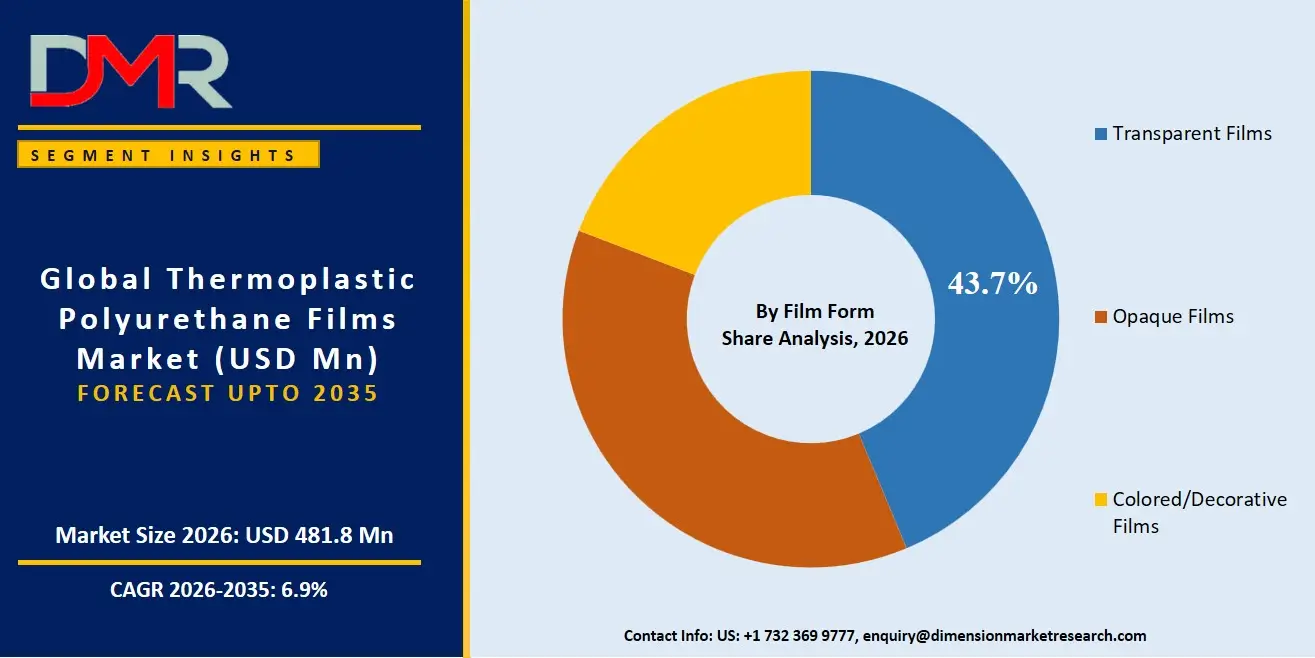

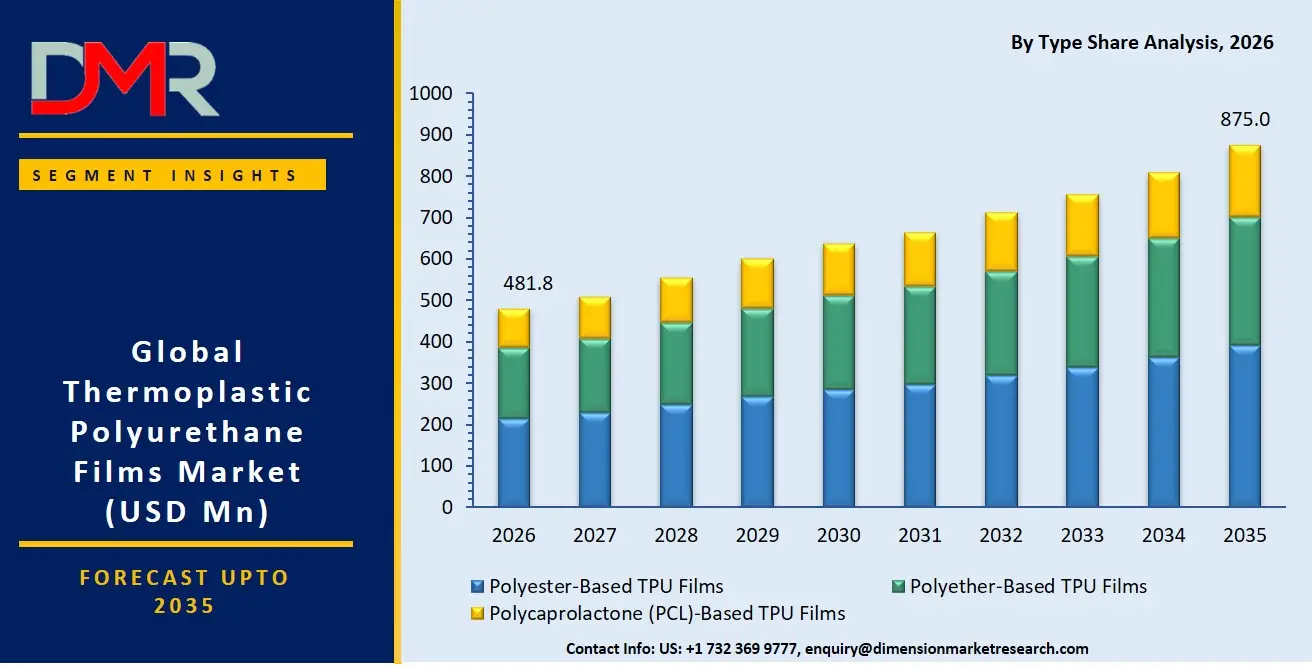

The Global Thermoplastic Polyurethane Films Market is expected to reach a value of USD 481.8 million in 2026, and it is further anticipated to reach USD 875.0 million by 2035, growing at a CAGR of 6.9% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The thermoplastic polyurethane films market has been experiencing sustained growth as industries increasingly prioritize lightweight, durable, and high-performance material solutions. The market encompasses films produced from polyester, polyether, and polycaprolactone-based TPU resins, which offer exceptional elasticity, abrasion resistance, chemical resistance, and optical clarity. These films are manufactured through various processing technologies including extrusion, calendering, and blown film processes, resulting in transparent, opaque, or colored variants with thicknesses ranging from ultra-thin films below 0.1 mm to robust films exceeding 0.5 mm. The growing demand for sustainable alternatives to PVC, the expansion of high-performance textile applications, and the rising adoption of TPU films in medical devices and automotive components are driving the necessity for innovative film formulations and advanced manufacturing capabilities.

The US Thermoplastic Polyurethane Films Market

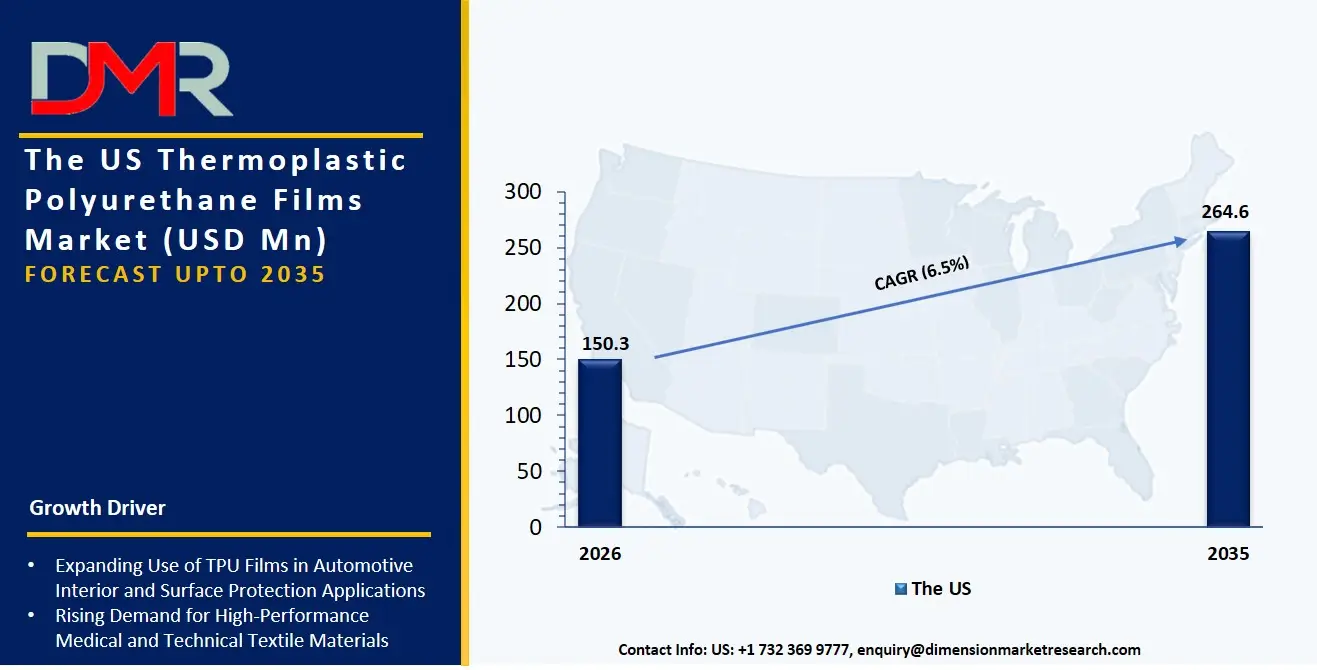

The US Thermoplastic Polyurethane Films Market is projected to reach USD 150.3 million in 2026 at a compound annual growth rate of 6.5% over its forecast period, culminating in a value of USD 264.6 million by 2035.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The United States continues to be the largest and most technologically advanced market for TPU films, driven by the robust medical device manufacturing sector and the aggressive lightweighting initiatives of the automotive industry. The market has been characterized by high demand for polyether-based TPU films, particularly in medical and healthcare applications where superior hydrolysis resistance and biocompatibility are essential for wound care dressings, surgical drapes, and implantable device components. Furthermore, the growing adoption of transparent TPU films in paint protection applications for premium vehicles is creating a parallel demand for UV-stabilized, optically clear film formulations that maintain aesthetic integrity while providing durable surface protection.

The Europe Thermoplastic Polyurethane Films Market

The Europe Thermoplastic Polyurethane Films Market is estimated to be valued at USD 153.2 million in 2026 and is further anticipated to reach USD 272.5 million by 2035 at a CAGR of 6.6%. The European market is significantly influenced by stringent regulatory frameworks including REACH and the EU Medical Device Regulation, which drive the need for bio-compatible polyester-based TPU films and environmentally sustainable manufacturing processes. Accelerated growth of textile and apparel applications is being experienced in the region as sportswear manufacturers in Germany and Italy seek to incorporate breathable, waterproof TPU membranes into high-performance activewear. In addition, the circular economy initiatives under the European Green Deal are compelling film manufacturers to develop recyclable and bio-based TPU film formulations that maintain performance characteristics while reducing environmental footprint across the product lifecycle.

The Japan Thermoplastic Polyurethane Films Market

The Japan Thermoplastic Polyurethane Films Market is projected to be valued at USD 49.7 million in 2026. It is further expected to witness steady growth, holding USD 86.3 million in 2035 at a CAGR of 6.3%. The Japanese market is distinct, characterized by precision engineering requirements from the electronics and automotive sectors that demand exceptionally uniform film thickness and consistent surface quality. Polyester-based TPU films and transparent film variants make up a substantial portion of the spending as electronics manufacturers incorporate TPU films into flexible printed circuit protection, display lamination, and wearable device components. There is also a strong need for deeply customized film solutions that bridge the gap between traditional rigid protective materials and the emerging flexible electronics form factors, creating a specialized niche in ultra-thin blown films and high-clarity extrusion films for advanced electronic applications.

Key Takeaways

- Market Size & Forecast: The Global Thermoplastic Polyurethane Films market is projected to reach USD 481.8 million in 2026, expanding steadily to USD 875.0 million by 2035, fueled by the dual drivers of PVC replacement initiatives and the growing demand for high-performance, lightweight materials across automotive, medical, and textile industries.

- Growth Rate & Outlook: Global market growth is expected at a CAGR of 6.9%, driven by increasing regulatory restrictions on phthalate-based plasticizers, the expanding application scope of breathable membranes in sportswear, and the critical need for durable surface protection solutions in premium automotive segments.

- Primary Growth Drivers: Key forces include the widespread transition from conventional PVC films to TPU alternatives in medical applications requiring biocompatibility, the growing need for high-abrasion-resistant films in industrial and automotive protective applications, and the expanding adoption of TPU films in inflatable structures and outdoor recreational equipment.

- Key Market Trends: Major trends include the development of bio-based TPU film formulations derived from renewable feedstocks, the rise of multi-layer composite films combining TPU with other functional polymers, the increasing use of advanced extrusion technologies for ultra-thin film production, and the growing emphasis on recyclable TPU film systems aligned with circular economy principles.

- By Type Analysis: Polyester-based TPU films are expected to dominate the market due to their superior mechanical strength, excellent chemical resistance, and cost-effectiveness across diverse industrial applications. Polyether-based variants are experiencing the fastest growth in medical and healthcare applications where hydrolysis resistance and microbial stability are paramount.

- By Application Analysis: Automotive and Medical & Healthcare represent the most lucrative application segments due to stringent performance requirements and regulatory compliance needs. Textile & Apparel is the fastest-growing sector as breathable TPU membranes become integral to high-performance sportswear, outdoor gear, and athleisure fashion categories.

- Regional Leadership: North America is poised to dominate this market with 37.1% of the market share in 2026 due to its well-established medical device manufacturing ecosystem, advanced automotive sector, and strong research and development infrastructure that continually pushes the boundaries of TPU film technology and application development.

What is the Thermoplastic Polyurethane Films?

Thermoplastic Polyurethane Films are specialized polymer films manufactured from thermoplastic polyurethane resins that combine the processing advantages of thermoplastics with the performance characteristics of crosslinked polyurethane elastomers. These films, unlike conventional plastic films such as PVC or polyethylene, are distinguished by their exceptional combination of elasticity, transparency, abrasion resistance, and chemical durability. The market encompasses various film types including polyester-based TPU films that offer superior mechanical properties and chemical resistance for industrial applications, polyether-based TPU films that provide excellent hydrolysis resistance and microbial stability for medical uses, and polycaprolactone-based TPU films that deliver unique biodegradability profiles for specialized applications. With industries increasingly seeking sustainable, high-performance material alternatives, TPU films have become essential for applications ranging from automotive paint protection and medical wound care to waterproof-breathable textiles and flexible electronics encapsulation, making advanced film technologies translate into tangible product performance advantages rather than mere material substitution.

Use Cases

- Automotive Paint Protection Films: Automotive manufacturers and aftermarket specialists utilize transparent polyester-based TPU films ranging from 0.15 to 0.2 mm thickness as paint protection solutions, providing self-healing surface properties, UV resistance, and stone chip protection that preserve vehicle aesthetics while maintaining optical clarity over extended service lifetimes.

- Medical Wound Care and Surgical Applications: Medical device companies employ polyether-based TPU films in transparent wound dressings, surgical incise drapes, and negative pressure wound therapy interfaces where biocompatibility, moisture vapor transmission, and conformable elastic properties are essential for patient comfort and clinical efficacy.

- High-Performance Sportswear Membranes: Sportswear brands integrate ultra-thin blown TPU films below 0.05 mm as waterproof-breathable membranes in performance outerwear, running shoes, and athletic accessories, providing moisture management and weather protection without compromising the flexibility and lightweight characteristics demanded by athletes.

- Flexible Electronics Protection: Electronics manufacturers apply ultra-thin, optically clear TPU films in flexible display lamination, touchscreen protection, and wearable device encapsulation where film uniformity, optical clarity, and mechanical durability are critical for maintaining device functionality under repeated flexing and environmental exposure.

How AI is Transforming the Thermoplastic Polyurethane Films Market?

Artificial intelligence is transforming the thermoplastic polyurethane (TPU) films market by accelerating material discovery, optimizing production, and enhancing quality control. Machine-learning algorithms analyze formulation data to identify resin combinations that deliver targeted properties such as flexibility, abrasion resistance, and transparency, reducing development time and cost. In manufacturing, AI-enabled process controls continuously adjust extrusion and lamination parameters to improve yield, consistency, and energy efficiency while minimizing scrap. Computer-vision systems inspect films in real time, detecting defects that might otherwise escape conventional methods. AI-driven demand forecasting and supply-chain analytics also help producers align inventories with customer requirements and respond rapidly to market shifts. Collectively, these capabilities enable TPU film manufacturers to innovate faster, operate more sustainably, and provide highly customized products for automotive, medical, textile, and other high-value applications.

Market Dynamics

Key Drivers in the Global Thermoplastic Polyurethane Films Market

Rising Demand for Lightweight and Durable Materials

Industries such as automotive, aerospace, and consumer goods increasingly seek materials that reduce weight without compromising performance. TPU films provide an excellent combination of strength, flexibility, abrasion resistance, and low mass, making them ideal for replacing heavier conventional materials. Their use contributes to improved fuel efficiency in vehicles and enhanced product durability in numerous applications. As manufacturers continue to prioritize sustainability and operational efficiency, the adoption of TPU films is accelerating. This trend is further supported by advances in film processing and formulation technologies that enable customized properties for diverse end uses, reinforcing TPU films as a preferred material across multiple industries.

Expanding Applications in Medical and Technical Textiles

The medical and technical textile sectors are significant growth engines for TPU films. Their biocompatibility, softness, and resistance to chemicals and microorganisms make them suitable for wound dressings, protective garments, and inflatable medical devices. In technical textiles, TPU films enhance waterproofness, breathability, and mechanical strength. Growing healthcare expenditures and increasing consumer demand for high-performance apparel continue to stimulate consumption. Furthermore, ongoing innovation in smart textiles and wearable technologies is creating additional demand for specialized TPU film grades. These expanding applications provide a strong and sustained impetus for market growth worldwide.

Restraints in the Global Thermoplastic Polyurethane Films Market

Volatility in Raw Material Prices

The production of TPU films relies heavily on petrochemical feedstocks whose prices are subject to fluctuations driven by crude oil markets and supply-chain disruptions. Such volatility can compress manufacturers' margins and create uncertainty in long-term planning. Frequent price changes may also be passed on to end users, potentially reducing competitiveness against alternative materials. Smaller producers are particularly vulnerable, as they often lack the purchasing power or hedging capabilities of larger firms. Consequently, unstable raw material costs remain a persistent challenge, affecting profitability and investment decisions throughout the TPU films value chain.

Competition from Substitute Materials

TPU films face competition from established materials such as PVC, polyolefins, and other specialty polymers that may offer lower costs or entrenched supply chains. In price-sensitive applications, end users may prioritize affordability over the superior performance characteristics of TPU. Additionally, some substitutes benefit from widespread processing infrastructure and familiarity among manufacturers, reducing barriers to adoption. This competitive environment can limit the penetration of TPU films in certain sectors despite their technical advantages. Overcoming this restraint requires continued innovation, cost optimization, and clear demonstration of the long-term value proposition of TPU film solutions.

Growth Opportunities in the Global Thermoplastic Polyurethane Films Market

Growth of Electric Vehicles and Advanced Mobility

The rapid expansion of electric vehicles presents a substantial opportunity for TPU film manufacturers. These vehicles increasingly incorporate lightweight, durable, and aesthetically refined materials to maximize efficiency and enhance passenger experience. TPU films are well suited for protective surfaces, battery-related components, and interior applications requiring flexibility and resistance to wear. As automakers invest in new mobility platforms and premium cabin designs, demand for advanced film solutions is expected to rise. Suppliers that develop tailored products meeting stringent automotive specifications can capture significant value from this evolving market landscape.

Development of Sustainable and Bio-Based TPU Films

Sustainability initiatives are encouraging the development of bio-based and recyclable TPU films. End users across industries are seeking environmentally responsible materials that align with regulatory requirements and corporate goals. Advances in renewable feedstocks and circular manufacturing processes enable producers to differentiate their offerings while reducing environmental impact. Companies that successfully commercialize high-performance sustainable TPU films can access new customer segments and strengthen brand value. This transition toward greener materials is likely to open attractive avenues for innovation, partnerships, and long-term market expansion.

Trends in the Global Thermoplastic Polyurethane Films Market

Increasing Adoption of Multifunctional Films

A notable market trend is the growing preference for TPU films that combine multiple functionalities within a single layer. Manufacturers are integrating features such as antimicrobial protection, UV resistance, and enhanced barrier performance to address evolving customer needs. Multifunctional films reduce component complexity and improve overall product performance, making them particularly attractive in medical, automotive, and consumer applications. The ability to tailor properties through advanced compounding and coating technologies is accelerating this shift. As end users seek greater value and efficiency, demand for sophisticated multifunctional TPU films is expected to continue rising.

Advancements in Processing and Customization Technologies

Continuous improvements in extrusion, lamination, and surface treatment technologies are enabling highly customized TPU film products. Producers can now achieve tighter tolerances, intricate textures, and application-specific performance characteristics with greater consistency. Digital manufacturing tools and automation further enhance production efficiency while reducing waste. These technological advances support rapid product development cycles and facilitate closer collaboration with end users. The resulting increase in customization capabilities is reshaping competitive dynamics within the market, with innovation and responsiveness becoming key differentiators for TPU film manufacturers worldwide.

Research Scope and Analysis

The global thermoplastic polyurethane films market is segmented by type into polyester-based, polyether-based, and polycaprolactone (PCL)-based films, by film form into transparent, opaque, and colored or decorative films, by processing technology into extrusion, calendered, and blown films, by thickness into up to 0.1 mm, 0.1–0.5 mm, and above 0.5 mm, and by application into automotive, medical and healthcare, textile and apparel, aerospace, building and construction, packaging, electronics, sports and leisure, and other uses.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Type Analysis

Polyester-based TPU films is poised to dominate the type segment owing to their excellent mechanical strength, abrasion resistance, and compatibility with demanding industrial applications. Their superior durability and resistance to oils, chemicals, and wear make them the preferred choice in automotive interiors, protective overlays, and high-performance laminates.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Manufacturers favor these films because they offer a balanced combination of toughness, processability, and cost efficiency, enabling large-scale production for diverse end uses. Continued growth in transportation, consumer goods, and technical textiles further reinforces their leadership. Their proven performance record and widespread availability ensure that polyester-based TPU films remain the largest and most established category within the global market.

By Film Form Analysis

Transparent TPU films are expected to hold the leading position among film forms due to their exceptional optical clarity and versatility. They are extensively employed in protective applications, decorative laminates, medical devices, and consumer products where visibility and aesthetics are essential. Their ability to combine transparency with flexibility, impact resistance, and weatherability makes them highly attractive to manufacturers seeking premium performance. In addition, transparent films support advanced printing and coating technologies, broadening their use across industries. Rising demand for high-quality surface protection and visually appealing products continues to strengthen their market share, establishing transparent TPU films as the dominant form segment worldwide.

By Processing Technology Analysis

Extrusion films is projected to dominate processing technologies because extrusion offers superior productivity, consistent quality, and cost-effective scalability. The process accommodates a wide range of thicknesses and formulations while ensuring uniform film properties, making it ideal for mass production. Extrusion lines are widely adopted across automotive, medical, textile, and packaging applications, enabling manufacturers to meet growing demand efficiently. The technology also allows integration with multilayer structures and advanced finishing techniques, enhancing product functionality. Its operational flexibility, relatively low production costs, and compatibility with continuous manufacturing have firmly established extrusion as the preferred processing route in the global TPU films industry.

By Thickness Analysis

Films with thicknesses between 0.1 and 0.5 mm are poised to represent the dominant thickness category because they provide an optimal balance between strength, flexibility, and material efficiency. This range satisfies the requirements of major applications such as automotive components, apparel laminates, and medical products, where durability is essential without sacrificing ease of handling. Manufacturers benefit from reduced raw material consumption compared with thicker films while still achieving excellent performance characteristics. The versatility of this thickness range allows it to address a broad spectrum of end-use needs, supporting high production volumes and sustaining its leading position within the global thermoplastic polyurethane films market.

By Application Analysis

The automotive sector is anticipated to be the largest application segment for TPU films, driven by increasing demand for lightweight, durable, and aesthetically appealing materials. TPU films are widely used for interior surfaces, paint protection, seating components, and functional laminates due to their abrasion resistance and design flexibility. Automakers also value their contribution to vehicle weight reduction and enhanced passenger comfort. Expanding production of electric vehicles and premium automobiles further boosts consumption, as these vehicles frequently incorporate advanced film technologies. Continuous innovation in automotive design and the need for long-lasting, high-performance materials ensure that the automotive industry remains the foremost consumer of TPU films globally.

The Global Thermoplastic Polyurethane Films Market Report is segmented on the basis of the following:

By Type

- Polyester-Based TPU Films

- Polyether-Based TPU Films

- Polycaprolactone (PCL)-Based TPU Films

By Film Form

- Transparent Films

- Opaque Films

- Colored/Decorative Films

By Processing Technology

- Extrusion Films

- Calendered Films

- Blown Films

By Thickness

- 0.1–0.5 mm

- Up to 0.1 mm

- Above 0.5 mm

By Application

- Automotive

- Medical & Healthcare

- Textile & Apparel

- Aerospace

- Building & Construction

- Packaging

- Electronics

- Sports & Leisure

- Others

Regional Analysis

Leading Region by Market Share

ℹ

To learn more about this report –

Download Your Free Sample Report Here

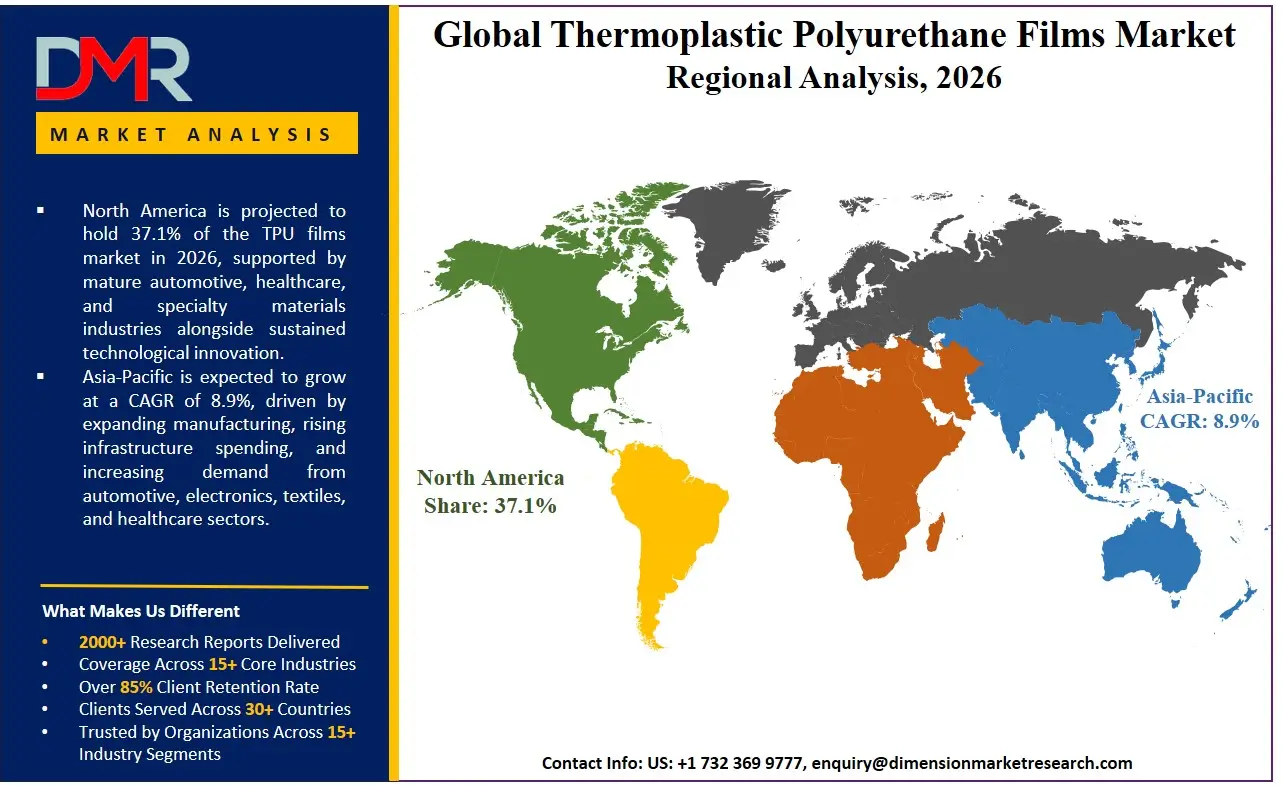

North America is poised to dominate the global thermoplastic polyurethane films market, holding 37.1% of the market share in 2026. The United States, which anchors the North American market, commands the leading position in TPU films due to the unmatched concentration of advanced medical device manufacturers, the robust automotive manufacturing and aftermarket sectors, and the presence of globally leading TPU resin and film producers with extensive research and development capabilities. The region benefits from a sophisticated healthcare system that drives demand for high-quality medical-grade films, stringent automotive quality standards that favor premium material solutions, and a regulatory environment that has actively restricted phthalate-containing PVC films in consumer and medical applications. Enterprise investment in advanced film processing technologies, bio-based TPU development, and multi-layer film engineering continues to reinforce North America's technological leadership position. Furthermore, the strong intellectual property framework and the presence of major consumer brands in footwear, apparel, and outdoor equipment headquartered in the region provide a robust demand environment for innovative, sustainably positioned TPU film products.

Fastest-Growing Regional Market

Asia-Pacific is expected to be the most rapidly expanding regional market for thermoplastic polyurethane films, driven by the rapid industrialization, expanding healthcare infrastructure, and the dynamic growth of automotive production and textile manufacturing across China, India, Japan, and Southeast Asian nations. The region's emergence as the global manufacturing hub for footwear, apparel, and consumer electronics creates enormous demand for TPU films as functional and decorative material components. Rising living standards and growing consumer spending on premium vehicles are driving increased adoption of automotive paint protection films and high-quality interior materials. Medical device manufacturing is expanding rapidly in the region, supported by government healthcare investment programs and the growth of domestic medical device industries, creating new demand for medical-grade TPU films. While domestic TPU film production capacity in the region is expanding significantly, technology gaps in high-end medical and optical-grade film manufacturing persist, creating opportunities for international technology leaders to serve these premium market segments through local production partnerships or direct export.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The competitive environment of the global thermoplastic polyurethane films market is characterized by the presence of diversified specialty chemical and material science corporations, focused film manufacturing specialists, and integrated TPU resin producers with forward integration into film production. Success in the market depends on a combination of raw material access and formulation expertise, advanced film processing capabilities, application engineering support, and the ability to meet the demanding quality and regulatory requirements of medical, automotive, and other high-value end-use markets. Strategic relationships with TPU resin producers provide competitive advantages in formulation development, raw material supply security, and cost management. The trend toward market specialization is evident, with leading competitors developing focused expertise in specific application segments, film types, or processing technologies rather than pursuing undifferentiated broad-market strategies. Product differentiation through proprietary formulations, advanced processing capabilities for ultra-thin or multi-layer films, bio-based content offerings, and application-specific performance characteristics represents the primary competitive strategy rather than price-based competition in commodity film categories.

The market demonstrates moderate barriers to entry in standard industrial-grade film segments but significantly higher barriers in regulated medical and demanding automotive applications where customer qualification processes, regulatory certifications, and long-term supply relationships create substantial competitive moats for established suppliers. Intellectual property protection for proprietary film formulations, processing methods, and application technologies further reinforces competitive positions in premium market segments.

Some of the prominent players in the Global Thermoplastic Polyurethane Films Market are:

- Covestro AG

- Huntsman Corporation

- Lubrizol Corporation

- BASF SE

- Wanhua Chemical Group Co., Ltd.

- Avery Dennison Corporation

- Schweitzer-Mauduit International, Inc. (SWM)

- DingZing Advanced Materials Inc.

- American Polyfilm, Inc.

- RTP Company

- Permali Gloucester Limited

- Novotex Italiana S.p.A.

- Taiwan PU Corporation

- Epurex Films GmbH & Co. KG

- Fatra, a.s.

- Argotec LLC

- Hexis S.A.S.

- MH&W International Corporation

- Plastics Group of America

- 3M Company

- Other Key Players

Recent Developments

- April 2026: Lubrizol Corporation expanded its ESTANE® TPU film portfolio with new grades tailored for protective apparel and industrial laminates, offering enhanced flexibility, durability, and processing efficiency to address growing demand for high-performance, lightweight film solutions worldwide.

- January 2026: Wanhua Chemical Group Co., Ltd. commissioned additional TPU production capacity in Asia, strengthening supply for specialty film applications in automotive and consumer goods while supporting regional market growth and improved customer responsiveness across key industries.

- September 2025: BASF SE launched sustainable TPU solutions incorporating renewable feedstocks for film and sheet applications, enabling customers to reduce carbon footprints while maintaining the durability, mechanical strength, and performance required in demanding end-use environments globally.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 481.8 Mn |

| Forecast Value (2035) |

USD 875.0 Mn |

| CAGR (2026–2035) |

6.9% |

| The US Market Size (2026) |

USD 150.3 Mn |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Type, By Film Form, By Processing Technology, By Thickness, and By Application |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Global Thermoplastic Polyurethane Films Market?

▾ The Global Thermoplastic Polyurethane Films market is poised to be valued at USD 481.8 million in 2026 and is projected to reach USD 875.0 million by 2035, driven by the universal shift toward high-performance, sustainable polymer films across automotive, medical, textile, and industrial applications.

What is the CAGR of the Global Thermoplastic Polyurethane Films Market from 2026 to 2035?

▾ The market is expected to grow at a CAGR of 6.9% from 2026 to 2035, reflecting the sustained demand for durable, lightweight film materials and the expanding application scope enabled by advanced processing technologies and innovative TPU formulations.

What factors are driving the growth of the Global Thermoplastic Polyurethane Films Market?

▾ Key drivers include the regulatory phase-out of PVC and phthalate plasticizers across major markets, the growing demand for automotive lightweighting and surface protection solutions, the expansion of breathable membrane applications in performance textiles, and the increasing adoption of TPU films in medical devices requiring biocompatibility and durability.

Which region held the largest share of the Thermoplastic Polyurethane Films Market in 2026?

▾ North America is poised to hold 37.1% of the market share in 2026, driven by advanced medical device manufacturing, robust automotive paint protection demand, and strong research and development infrastructure supporting continuous TPU film innovation.

Which region is expected to grow the fastest in the Thermoplastic Polyurethane Films Market?

▾ The Asia-Pacific region is expected to grow the fastest, fueled by rapid expansion of manufacturing capacity for footwear, apparel, and electronics, growing automotive production and ownership, and expanding healthcare infrastructure across China, India, and Southeast Asian economies.

What are the major trends in the Global Thermoplastic Polyurethane Films Market?

▾ Major trends include the development of bio-based and renewable content TPU film formulations, advancements in multi-layer co-extrusion film structures, the rise of ultra-thin films for electronics and textile applications, and the growing emphasis on recyclable and circular-economy-aligned TPU film systems.

Who are the key players in the Global Thermoplastic Polyurethane Films Market?

▾ Key players include diversified material science companies like Covestro, BASF, Huntsman, and Lubrizol, along with specialized film manufacturers such as American Polyfilm, Avery Dennison, DingZing Advanced Materials, and SWM, who together drive innovation and competition across the global TPU films landscape.

How is the Global Thermoplastic Polyurethane Films Market segmented?

▾ The market is segmented by Type, by Film Form, by Processing Technology, by Thickness, and by Application.