Market Overview

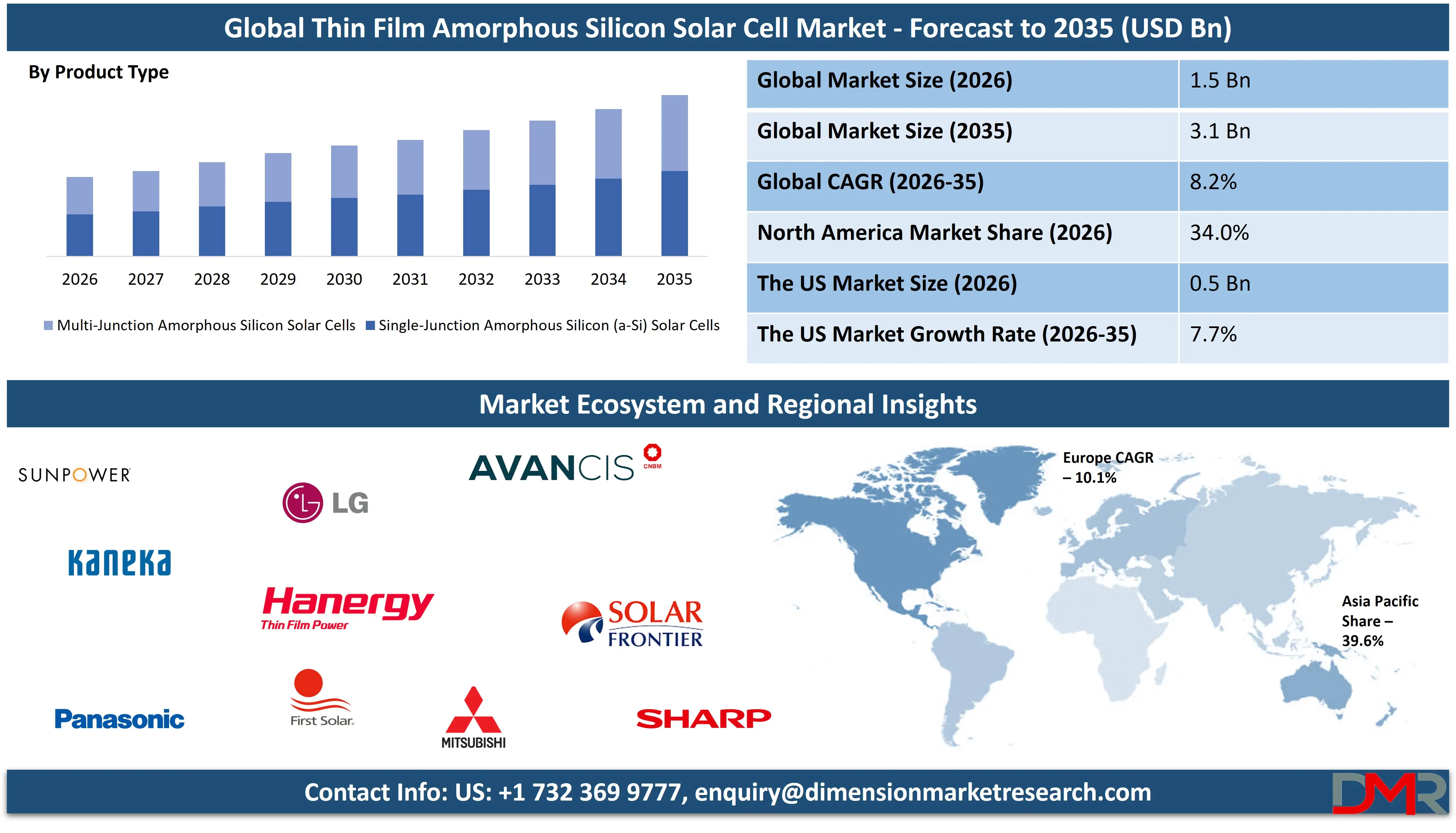

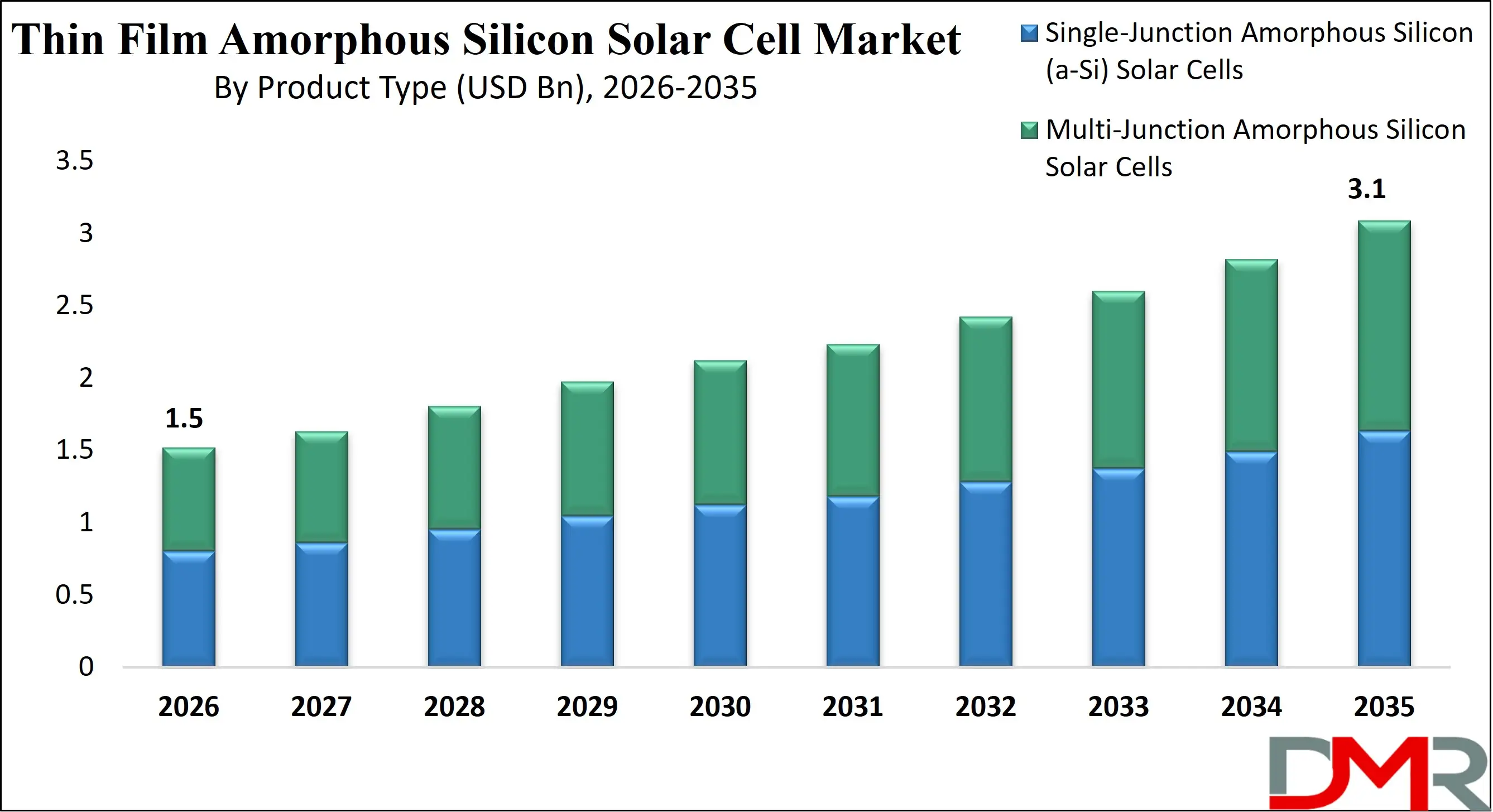

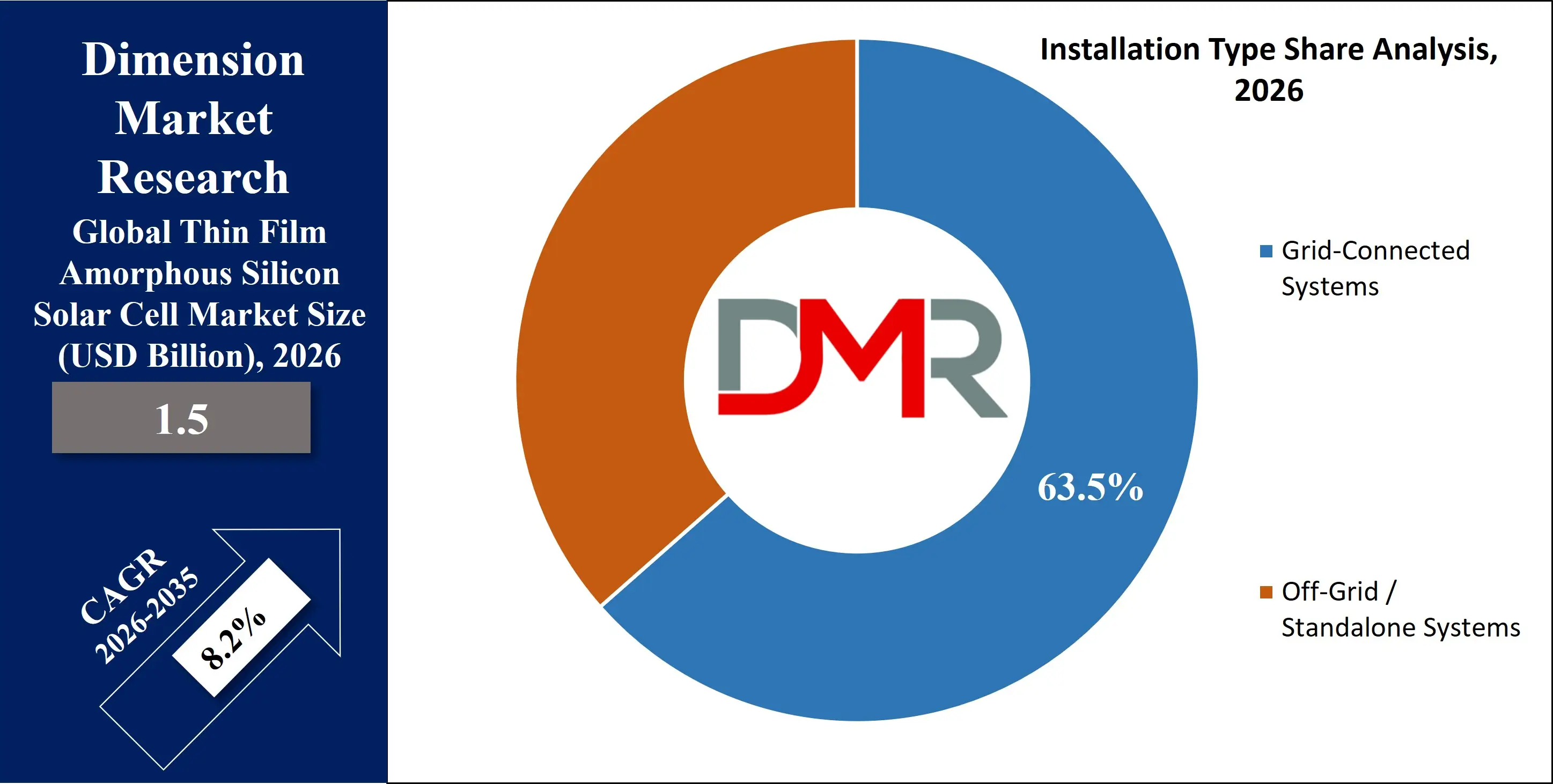

The Global Thin Film Amorphous Silicon Solar Cell Market size is projected to reach USD 1.5 billion in 2026 and grow at a compound annual growth rate of 8.2% to reach a value of USD 3.1 billion in 2035.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Thin Film Amorphous Silicon Solar Cell refers to a photovoltaic technology that uses non-crystalline silicon deposited in very thin layers onto substrates such as glass, metal, or plastic. Unlike conventional crystalline silicon cells, this technology leverages a disordered atomic structure, enabling flexibility, lightweight design, and reduced material consumption. It includes single-junction and multi-junction configurations such as tandem and micromorph structures, designed to enhance light absorption and improve conversion efficiency. These cells are widely used in building-integrated photovoltaics (BIPV), portable electronics, and utility-scale installations where cost, flexibility, and performance under low-light conditions are critical.

The technology holds strategic importance within the broader renewable energy industry due to its lower manufacturing temperatures, reduced silicon usage, and compatibility with large-area deposition techniques. Emerging trends such as flexible solar modules, semi-transparent facades, and integration into consumer electronics are accelerating adoption. Advancements in plasma-enhanced chemical vapor deposition (PECVD), efficiency improvements, and hybrid layering techniques are reshaping product capabilities and expanding applications across diverse sectors.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Continuous innovation in materials engineering, rising demand for lightweight photovoltaic solutions, and supportive renewable energy targets are transforming the competitive environment. Improvements in durability, better light-induced degradation management, and cost optimization are contributing to steady technological maturity and expanded commercial viability.

The US Thin Film Amorphous Silicon Solar Cell Market

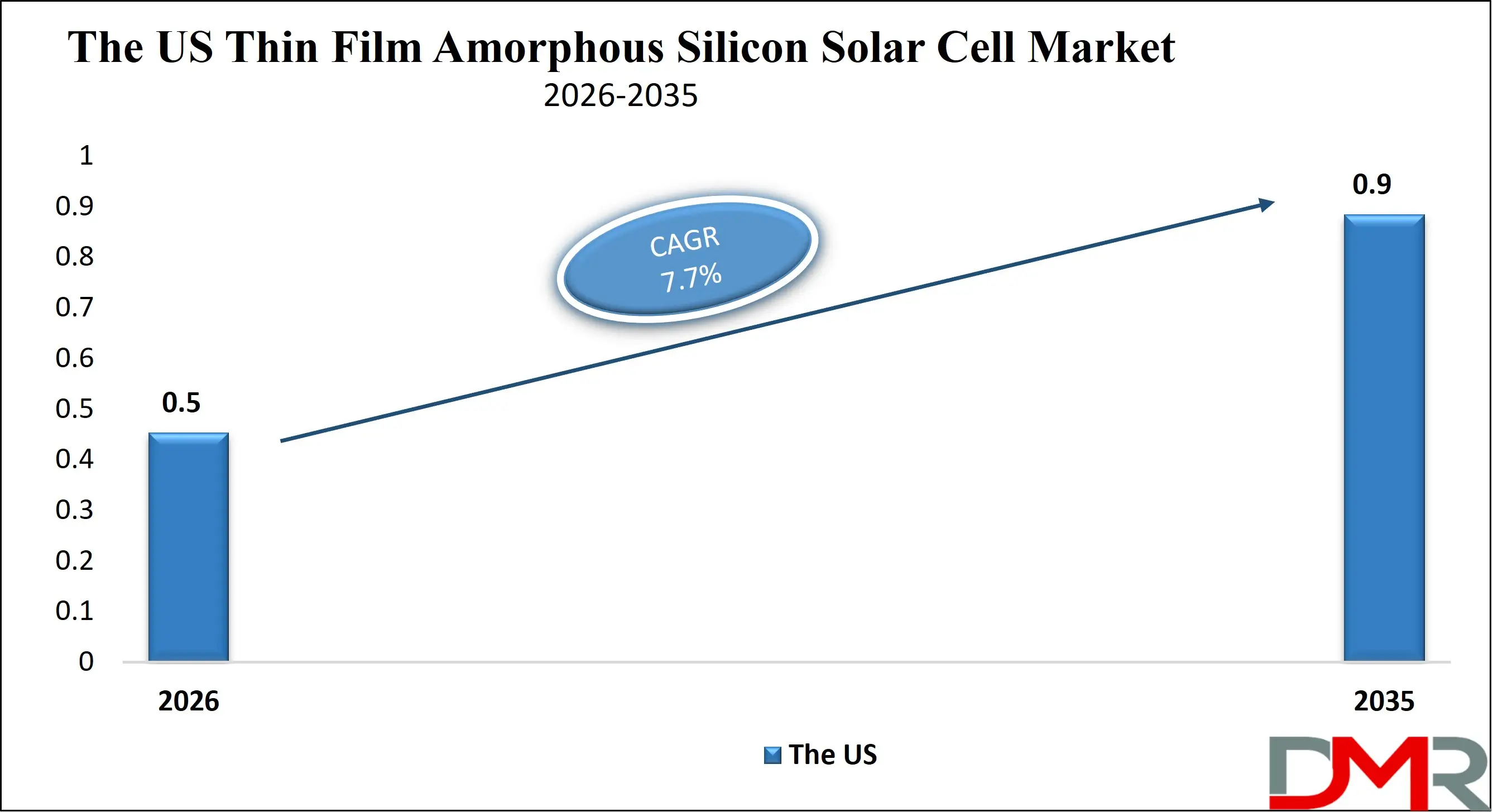

The US Thin Film Amorphous Silicon Solar Cell Market size is projected to reach USD 500 million in 2026 at a compound annual growth rate of 7.7% over its forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The US market is influenced by strong federal and state-level renewable energy incentives, tax credits, and net metering policies. Investment in distributed generation, particularly rooftop and BIPV applications, supports steady demand. The presence of advanced research institutions and clean energy funding programs fosters innovation in thin-film deposition and efficiency enhancement. Utility-scale solar expansion, especially in high-irradiance states such as California, Texas, and Arizona, creates opportunities for lightweight modules in commercial and industrial applications. Additionally, reshoring initiatives and domestic manufacturing incentives strengthen supply chain resilience and encourage localized production capacity expansion.

Europe Thin Film Amorphous Silicon Solar Cell Market

Europe Thin Film Amorphous Silicon Solar Cell Market size is projected to reach USD 270 million in 2026 at a compound annual growth rate of 10.1% over its forecast period.

Europe’s market growth is strongly linked to decarbonization policies and renewable integration targets aligned with regional climate frameworks. Countries such as Germany, France, Italy, and the Netherlands are advancing BIPV adoption, integrating thin-film modules into rooftops and facades. Energy efficiency standards for buildings and renovation wave initiatives accelerate demand for aesthetically adaptable photovoltaic materials. The region also emphasizes circular economy principles, promoting recyclable solar technologies. Innovation clusters and cross-border collaborations drive R&D in tandem and micromorph structures, enhancing competitiveness and supporting sustainable energy transitions across residential and commercial sectors.

Japan Thin Film Amorphous Silicon Solar Cell Market

Japan Thin Film Amorphous Silicon Solar Cell Market size is projected to reach USD 150 million in 2026 at a compound annual growth rate of 7.6% over its forecast period.

Japan’s market is characterized by advanced manufacturing capabilities, urban density, and strong emphasis on energy security. Limited land availability promotes rooftop and building-integrated solutions, favoring lightweight thin-film modules. Government-backed renewable incentives and feed-in tariff adjustments encourage distributed generation. The country’s expertise in electronics and semiconductor fabrication enhances innovation in deposition processes and module miniaturization. Integration into consumer electronics, smart infrastructure, and disaster-resilient off-grid systems supports expansion. However, high quality standards and competition from crystalline silicon modules present challenges that require ongoing efficiency and cost improvements.

Thin Film Amorphous Silicon Solar Cell Market: Key Takeaways

- Market Growth: The Thin Film Amorphous Silicon Solar Cell Market size is expected to grow by USD 1.5 billion, at a CAGR of 8.2%, during the forecasted period of 2027 to 2035.

- By Product Type: The single junction amorphous silicon solar cells segment is anticipated to get the majority share of the thin film amorphous silicon solar cell market in 2026.

- By Installation Type: The grid-connected systems segment is expected to get the largest revenue share in 2026 in the thin film amorphous silicon solar cell market.

- Regional Insight: Asia Pacific is expected to hold a 39.6% share of revenue in the global thin film amorphous silicon solar cell market in 2026.

- Use Cases: some of the use cases of thin film amorphous silicon solar cell include agriculture system, transport integreration and more.

Thin Film Amorphous Silicon Solar Cell Market: Use Cases

- Building Integrated Photovoltaics (BIPV): Thin-film modules are embedded into roofing materials, facades, and skylights, offering aesthetic flexibility and lightweight integration for urban infrastructure.

- Utility-Scale Installations: Large-area thin-film arrays provide cost-effective power generation, particularly in regions with diffuse sunlight conditions.

- Consumer Electronics: Used in calculators, IoT devices, and wearables due to low-light efficiency and compact form factors.

- Telecommunications Infrastructure: Supports remote telecom towers with reliable off-grid solar power solutions.

- Agricultural Systems: Powers solar pumps and greenhouse systems, improving rural energy access and productivity.

- Transportation Integration: Applied in vehicle-integrated photovoltaics and EV charging support systems for auxiliary energy supply.

- Rural Electrification: Enables standalone energy systems in off-grid and remote communities.

Stats & Facts

- International Energy Agency reported that global renewable electricity capacity additions reached 507 GW in 2024.

- The US Energy Information Administration stated that solar power accounted for 7% of total the US electricity generation in 2024.

- European Commission confirmed that renewables contributed over 44% of EU electricity generation in 2024.

- International Renewable Energy Agency noted that solar PV represented the largest share of new renewable capacity additions in 2024.

- The US Department of Energy highlighted that solar module prices declined by more than 80% over the past decade as of 2024.

- Japan Ministry of Economy, Trade and Industry reported continued expansion of rooftop solar installations in 2024.

- International Energy Agency projected solar PV to remain the fastest-growing renewable source through 2025.

- The US Environmental Protection Agency emphasized increased federal funding for clean energy manufacturing in 2024.

- European Environment Agency reported steady growth in distributed solar capacity across member states in 2024.

- International Renewable Energy Agency confirmed that global solar PV capacity exceeded 1,400 GW in 2024.

- Department of Agriculture supported rural solar electrification initiatives in 2024.

- World Bank indicated increased renewable energy investments in emerging economies in 2025.

Market Dynamic

Driving Factors in the Thin Film Amorphous Silicon Solar Cell Market

Rising Demand for Lightweight and Flexible Solar Solutions

The growing need for lightweight, adaptable, and flexible photovoltaic modules significantly drives adoption. Thin film amorphous silicon technology offers reduced weight compared to crystalline silicon, making it suitable for rooftops with load constraints and portable applications. Urban infrastructure modernization, green building certifications, and distributed generation initiatives support deployment. Additionally, improved performance in low-light and high-temperature conditions enhances suitability for varied climates, strengthening its position in commercial and residential installations.

Technological Advancements in Deposition and Multi-Junction Designs

Continuous advancements in deposition processes such as PECVD and the development of tandem and micromorph structures are improving efficiency levels and durability. Multi-junction architectures enhance spectral absorption, addressing historical efficiency limitations. Improved encapsulation and degradation mitigation technologies extend operational lifespan, making the technology more competitive. Manufacturing scale optimization and automation further reduce production costs, encouraging broader commercial acceptance across diverse end-use sectors.

Restraints in the Thin Film Amorphous Silicon Solar Cell Market

Lower Efficiency Compared to Crystalline Silicon

Despite improvements, conversion efficiency remains lower than monocrystalline and polycrystalline silicon cells. This limitation restricts adoption in space-constrained utility-scale projects where higher efficiency modules are preferred. The need for larger surface areas to generate equivalent power can increase installation costs and land use requirements, potentially discouraging investors seeking maximum energy yield per square meter.

Market Competition and Price Pressure

Intense competition from established crystalline silicon technologies exerts downward price pressure. Rapid innovation cycles and economies of scale in traditional PV manufacturing create cost challenges for thin-film producers. Additionally, supply chain volatility and raw material availability influence production stability, impacting profitability margins and long-term investment planning.

Opportunities in the Thin Film Amorphous Silicon Solar Cell Market

Expansion of Building-Integrated Photovoltaics

The rising adoption of energy-efficient building codes and smart city initiatives creates strong opportunities in BIPV. Thin film modules offer aesthetic integration, semi-transparency, and design flexibility, enabling architects to incorporate solar solutions seamlessly. Growing urbanization and commercial real estate development further enhance long-term growth potential in this segment.

Growth in Off-Grid and Emerging Markets

Expanding rural electrification programs and increasing energy demand in developing economies present substantial growth potential. Thin film modules’ lightweight and low-light performance characteristics make them suitable for remote and decentralized systems. International funding programs and sustainability commitments are likely to accelerate deployment in underserved regions.

Trends in the Thin Film Amorphous Silicon Solar Cell Market

Integration with Smart Infrastructure

Integration with smart grids, IoT-enabled monitoring systems, and energy storage solutions is reshaping deployment strategies. Real-time performance analytics and predictive maintenance improve operational efficiency and system reliability. Smart building integration further enhances distributed generation capabilities and energy optimization.

Hybrid and Multi-Layer Configurations

Hybrid designs combining amorphous silicon with microcrystalline layers are gaining traction. These configurations improve energy yield and stability while maintaining flexibility. Research in advanced materials and nanostructuring continues to enhance efficiency and reduce degradation effects, influencing next-generation product development.

Impact of Artificial Intelligence in Thin Film Amorphous Silicon Solar Cell Market

- Predictive Maintenance: AI algorithms analyze performance data to detect faults early and reduce downtime.

- Manufacturing Optimization: Machine learning enhances deposition uniformity and reduces material waste.

- Energy Yield Forecasting: AI models predict output based on weather and environmental data.

- Quality Control Automation: Computer vision systems identify micro-defects during production.

- Design Simulation: Advanced modeling accelerates multi-junction structure development.

- Smart Grid Integration: AI optimizes energy distribution and load balancing.

- Supply Chain Optimization: AI tools forecast demand and streamline logistics.

- Customer Energy Management: Intelligent platforms optimize self-consumption and storage integration.

Research Scope and Analysis

By Product Type Analysis

Single-junction amorphous silicon (a-Si) solar cells remain the dominant product segment and are projected to hold approximately 52.8% market share in 2026. Their leadership comes from lower production complexity, reduced silicon material consumption, and compatibility with large-area thin-film deposition techniques such as PECVD. These cells are widely used in consumer electronics, calculators, small IoT devices, and low-power building applications due to their excellent low-light and indoor performance. Their ability to be fabricated on flexible substrates further broadens their application scope. Continuous advancements in light-induced degradation mitigation and encapsulation technologies enhance durability and lifecycle performance, reinforcing their strong position in cost-sensitive and high-volume markets.

Multi-junction amorphous silicon solar cells, including tandem, triple-junction, and micromorph configurations, represent the fastest-growing product category. These structures stack multiple semiconductor layers with varying bandgaps to capture a broader portion of the solar spectrum, significantly improving conversion efficiency compared to single-junction variants. Their enhanced energy yield makes them suitable for performance-driven applications such as commercial rooftops and building-integrated photovoltaics (BIPV). As R&D investments accelerate and manufacturing processes become more optimized, production costs are expected to decline. Growing demand for higher-efficiency thin-film modules in urban and infrastructure projects is likely to further accelerate adoption across developed and emerging markets.

By Form Factor Analysis

Rigid modules are anticipated to account for 52.3% of the market share in 2026, maintaining their position as the leading form factor. Their structural robustness, long operational lifespan, and compatibility with conventional mounting systems make them highly suitable for commercial rooftops and utility-scale installations. These modules offer reliable performance in diverse weather conditions and benefit from established installation practices, reducing deployment risks. Improved encapsulation materials and protective coatings further enhance resistance to moisture and UV degradation. Their scalability and standardized integration into grid-connected systems support sustained dominance in large-scale solar infrastructure projects worldwide.

Flexible and lightweight modules are witnessing rapid expansion due to increasing demand for adaptable solar solutions across transportation, portable electronics, and curved architectural surfaces. Their reduced weight allows installation on structures with limited load-bearing capacity, such as lightweight rooftops or temporary constructions. These modules are also gaining traction in vehicle-integrated photovoltaics and mobile energy systems. Technological improvements in substrate materials and encapsulation enhance durability without compromising flexibility. As urbanization intensifies and innovative building designs emerge, demand for aesthetically adaptable and structurally versatile thin-film modules is expected to accelerate significantly.

By Installation Type Analysis

Grid-connected systems are projected to hold a 63.5% share in 2026, driven by supportive renewable energy policies, net metering frameworks, and long-term power purchase agreements. Integration with smart grids and energy storage technologies enhances energy reliability and financial returns for commercial and industrial users. These systems benefit from predictable revenue streams and strong government incentives in multiple regions. Improved inverter technologies and digital monitoring platforms further optimize performance and reduce maintenance costs. As countries continue expanding renewable capacity targets, grid-connected thin-film installations are expected to remain the primary deployment model.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Off-grid and standalone systems are expanding steadily, particularly in rural, remote, and disaster-prone regions. Thin film amorphous silicon modules perform efficiently in low-light and high-temperature conditions, making them suitable for decentralized electrification projects. Government-supported rural electrification initiatives and humanitarian infrastructure programs are key growth drivers. These systems are commonly used in telecommunications towers, agricultural pumps, and small community microgrids. Their lightweight structure simplifies transportation and installation in remote areas. As global efforts to improve energy access intensify, off-grid applications are anticipated to contribute significantly to market expansion.

By Application Analysis

Building Integrated Photovoltaics (BIPV) is expected to command 38.7% share in 2026, emerging as a leading application segment. Thin film amorphous silicon modules are particularly suited for BIPV due to their lightweight design, semi-transparency, and aesthetic flexibility. They can be seamlessly integrated into roofing systems, facades, skylights, and canopies without compromising architectural design. Growing adoption of green building certifications and stringent energy efficiency standards supports this segment’s growth. Urban redevelopment projects and smart city initiatives further accelerate demand. As construction industries increasingly prioritize sustainability and on-site energy generation, BIPV applications are likely to witness sustained momentum.

Utility-scale power generation applications are growing steadily, leveraging the cost advantages and large-area deposition capabilities of thin-film technologies. Although efficiency is lower compared to crystalline modules, performance in diffuse light and high-temperature environments makes them viable in certain climatic conditions. These installations benefit from economies of scale and long-term energy contracts. Advances in module stability and degradation resistance enhance reliability for large solar farms. Increasing grid expansion and renewable portfolio standards worldwide are expected to support continued adoption of thin film modules in selected utility-scale projects.

By End User Analysis

The commercial segment is forecast to capture 41.2% share in 2026, driven by corporate sustainability commitments and the pursuit of long-term energy cost savings. Businesses are increasingly installing rooftop solar systems to meet ESG targets and reduce reliance on conventional grid power. Thin film amorphous silicon modules are attractive for commercial buildings due to their lightweight nature and compatibility with large roof surfaces. Integration with energy management systems and storage solutions enhances financial returns. Growing regulatory pressure for carbon disclosure and energy efficiency compliance further supports adoption in offices, retail complexes, and industrial facilities.

Residential adoption is expanding steadily, supported by distributed generation trends and improved affordability of thin-film modules. Homeowners are increasingly seeking rooftop solar solutions that are lightweight and visually adaptable. Thin film modules provide effective performance under partial shading and low-light conditions common in urban neighborhoods. Government subsidies, tax credits, and net metering schemes enhance return on investment. Additionally, the rise of smart homes and battery storage integration strengthens the residential value proposition. As awareness of energy independence and sustainability grows, residential installations are expected to contribute meaningfully to overall market development.

The Thin Film Amorphous Silicon Solar Cell Market Report is segmented on the basis of the following

By Product Type

- Single-Junction Amorphous Silicon (a-Si) Solar Cells

- Multi-Junction Amorphous Silicon Solar Cells

- Tandem a-Si

- Triple-Junction a-Si

- a-Si/µ-Si (Micromorph)

By Form Factor

- Rigid Modules

- Flexible / Lightweight Modules

- Integrated Thin-Film Strips

By Installation Type

- Grid-Connected Systems

- Off-Grid / Standalone Systems

By Application

- Building Integrated Photovoltaics (BIPV)

- Roofing

- Facades

- Skylights / Canopies

- Utility-Scale Power Generation

- Consumer Electronics

- Calculators & Small Devices

- Wearables / IoT Devices

- Telecommunications Infrastructure

- Agricultural Applications

- Solar Pumps

- Greenhouse Systems

- Transportation

- Automotive Integration

- EV Charging Support Systems

By End-User

- Residential

- Commercial

- Industrial

- Government & Public Sector

- Rural Electrification / Off-Grid Projects

Regional Analysis

Leading Region in the Thin Film Amorphous Silicon Solar Cell Market

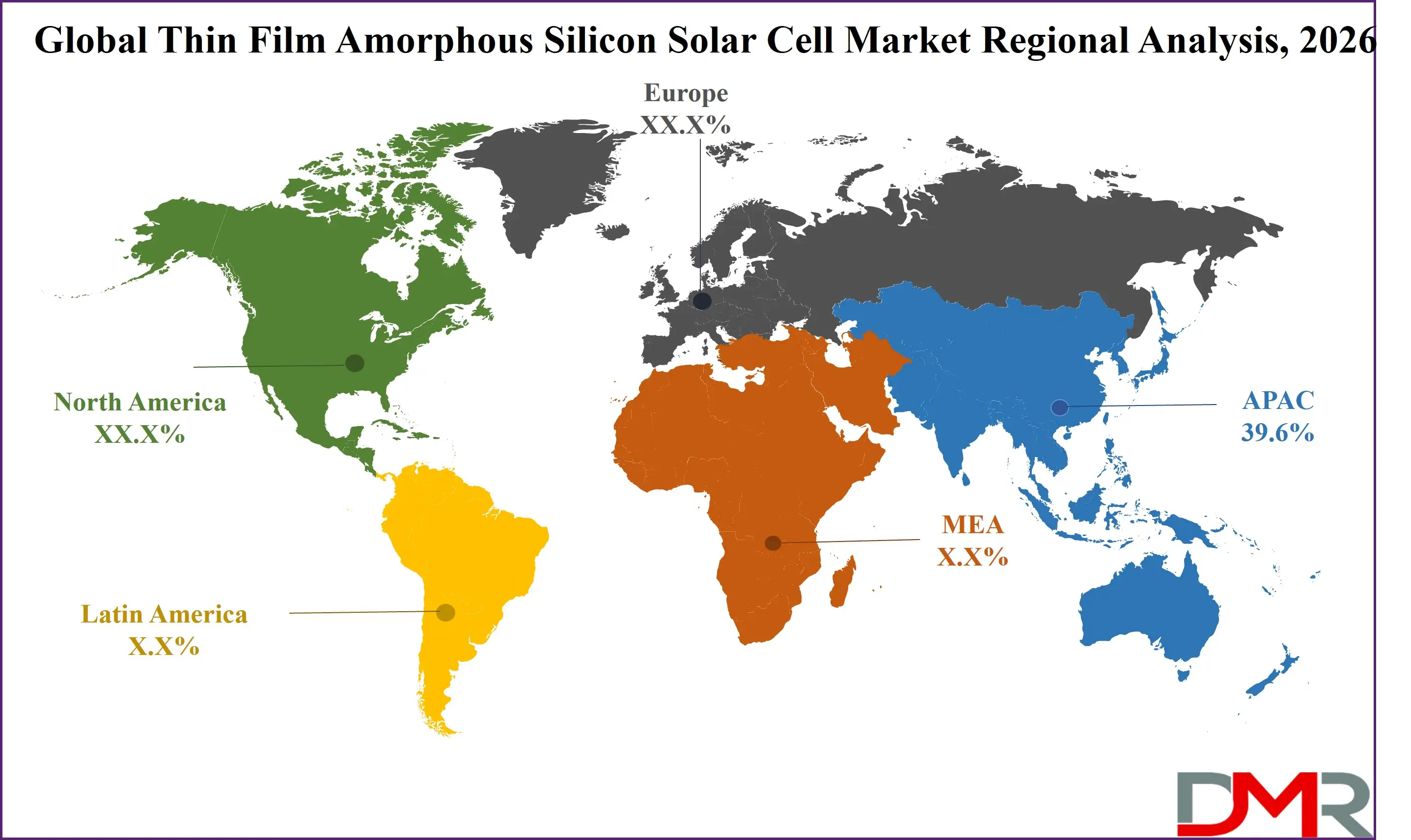

Asia-Pacific is projected to dominate the market with an estimated 39.6% share in 2026. The region benefits from strong manufacturing ecosystems, established semiconductor supply chains, and large-scale solar deployment programs. Countries such as China, Japan, South Korea, and India are investing heavily in renewable capacity expansion and domestic production facilities. Rapid urbanization, infrastructure development, and supportive government policies drive consistent demand. Cost-efficient labor and raw material accessibility further enhance regional competitiveness. Additionally, rising electricity demand and energy security concerns strengthen long-term growth prospects, reinforcing Asia-Pacific’s leadership position.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Fastest Growing Region in the Thin Film Amorphous Silicon Solar Cell Market

Europe is expected to experience the fastest growth due to stringent decarbonization targets and strong policy frameworks promoting renewable integration. Building renovation programs and energy efficiency directives encourage the adoption of BIPV solutions across residential and commercial sectors. Financial incentives, innovation grants, and regional climate commitments accelerate technology deployment. Increased focus on reducing energy imports and enhancing grid resilience further stimulates investment in distributed solar systems. Collaborative research initiatives and sustainability-driven urban planning are likely to sustain Europe’s rapid expansion trajectory in the coming years.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The thin film amorphous silicon solar cell market is moderately consolidated, with companies concentrating on technological differentiation, cost optimization, and strategic collaborations to strengthen their competitive positions. Market participants prioritize sustained R&D investments to enhance conversion efficiency, minimize light-induced degradation, and improve module durability. Vertical integration strategies are increasingly adopted to secure raw material supply, streamline production, and reduce dependency on external vendors. Partnerships with construction firms, infrastructure developers, and electronics manufacturers are expanding application scope, particularly in bipv and portable device segments. High capital requirements for deposition equipment, cleanroom facilities, and advanced manufacturing technologies create significant entry barriers. Continuous innovation, patent portfolio expansion, and geographic capacity diversification remain essential strategies for maintaining long-term competitive advantage in the thin film amorphous silicon solar cell market.

Some of the prominent players in the global Thin Film Amorphous Silicon Solar Cell are

- First Solar, Inc.

- Hanergy Thin Film Power Group

- Sharp Corporation

- Kaneka Corporation

- Mitsubishi Electric Corporation

- Panasonic Corporation

- Solar Frontier K.K.

- Trina Solar Co., Ltd.

- Canadian Solar Inc.

- GCL System Integration Technology Co., Ltd.

- Wuxi Suntech Power Co., Ltd.

- Yingli Solar

- SunPower Corporation

- LG Electronics Inc.

- United Solar Ovonic LLC

- Ascent Solar Technologies, Inc.

- Global Solar Energy, Inc.

- NexPower Technology Corporation

- AVANCIS GmbH

- Heliatek GmbH

- Other Key Players

Recent Developments

- In August 2025, Japanese firms PXP Inc. and Tokyo Gas Co. announced a partnership for the development of an advanced lightweight solar cell designed for industrial rooftops with limited load-bearing strength. The system combines PXP’s ultra-light chalcopyrite solar cells, weighing under 0.2 pounds per square foot, with Tokyo Gas’s specialized installation method, enabling deployment on roofing materials such as slate without structural concerns. The companies estimate that such roofs in Japan could support up to 169 gigawatts of capacity by 2050.

- In January 2025, Poland-based CIGS thin-film solar manufacturer Roltec announced the establishment of a new production facility in Jerzmanów, Wrocław. The plant marked as the country’s first manufacturing project utilizing copper indium gallium diselenide (CIGS) technology and is designed with an annual production capacity of 50 MW. According to the company, the site will allow large-scale manufacturing of CIGS modules that have been developed and validated through its laboratory research and pilot production line.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 1.5 Bn |

| Forecast Value (2035) |

USD 3.1 Bn |

| CAGR (2026–2035) |

8.2% |

| The US Market Size (2026) |

USD 0.5 Bn |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors, etc. |

| Segments Covered |

Segments Covered By Product Type (Single-Junction Amorphous Silicon (a-Si) Solar Cells, Multi-Junction Amorphous Silicon Solar Cells), By Form Factor (Rigid Modules, Flexible / Lightweight Modules, Integrated Thin-Film Strips), By Installation Type (Grid-Connected Systems, Off-Grid / Standalone Systems), By Application (Building Integrated Photovoltaics (BIPV), Utility-Scale Power Generation, Consumer Electronics, Telecommunications Infrastructure, Agricultural Applications, Transportation), By End-User (Residential, Commercial, Industrial, Government & Public Sector, Rural Electrification / Off-Grid Projects) |

| Regional Coverage |

North America – US, Canada; Europe – Germany, UK, France, Russia, Spain, Italy, Benelux, Nordic, Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, Rest of MEA |

| Prominent Players |

First Solar, Inc., Hanergy Thin Film Power Group, Sharp Corporation, Kaneka Corporation, Mitsubishi Electric Corporation, Panasonic Corporation, Solar Frontier K.K., Trina Solar Co., Ltd., Canadian Solar Inc., GCL System Integration Technology Co., Ltd., Wuxi Suntech Power Co., Ltd., Yingli Solar, SunPower Corporation, LG Electronics Inc., United Solar Ovonic LLC, Ascent Solar Technologies, Inc., Global Solar Energy, Inc., NexPower Technology Corporation, AVANCIS GmbH, Heliatek GmbH, and Other Key Players |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users), and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days, and 5 analysts working days respectively. |

Frequently Asked Questions

How big is the Global Thin Film Amorphous Silicon Solar Cell Market?

▾ The Global Thin Film Amorphous Silicon Solar Cell Market size is expected to reach USD 1.5 billion by 2026 and is projected to reach USD 3.1 billion by the end of 2035.

Which region accounted for the largest Global Thin Film Amorphous Silicon Solar Cell Market?

▾ Asia Pacific is expected to have the largest market share in the Global Thin Film Amorphous Silicon Solar Cell Market, with a share of about 39.6% in 2026.

How big is the Thin Film Amorphous Silicon Solar Cell Market in the US?

▾ The US Thin Film Amorphous Silicon Solar Cell market is expected to reach USD 0.5 billion by 2026.

Who are the key players in the Thin Film Amorphous Silicon Solar Cell Market?

▾ Some of the major key players in the Global Thin Film Amorphous Silicon Solar Cell Market include First Solar, Panasonic, Sharp, and others

What is the growth rate in the Global Thin Film Amorphous Silicon Solar Cell Market?

▾ The market is growing at a CAGR of 8.2 percent over the forecasted period.