What is the Intracranial Hemorrhage Diagnosis & Treatment Market Size?

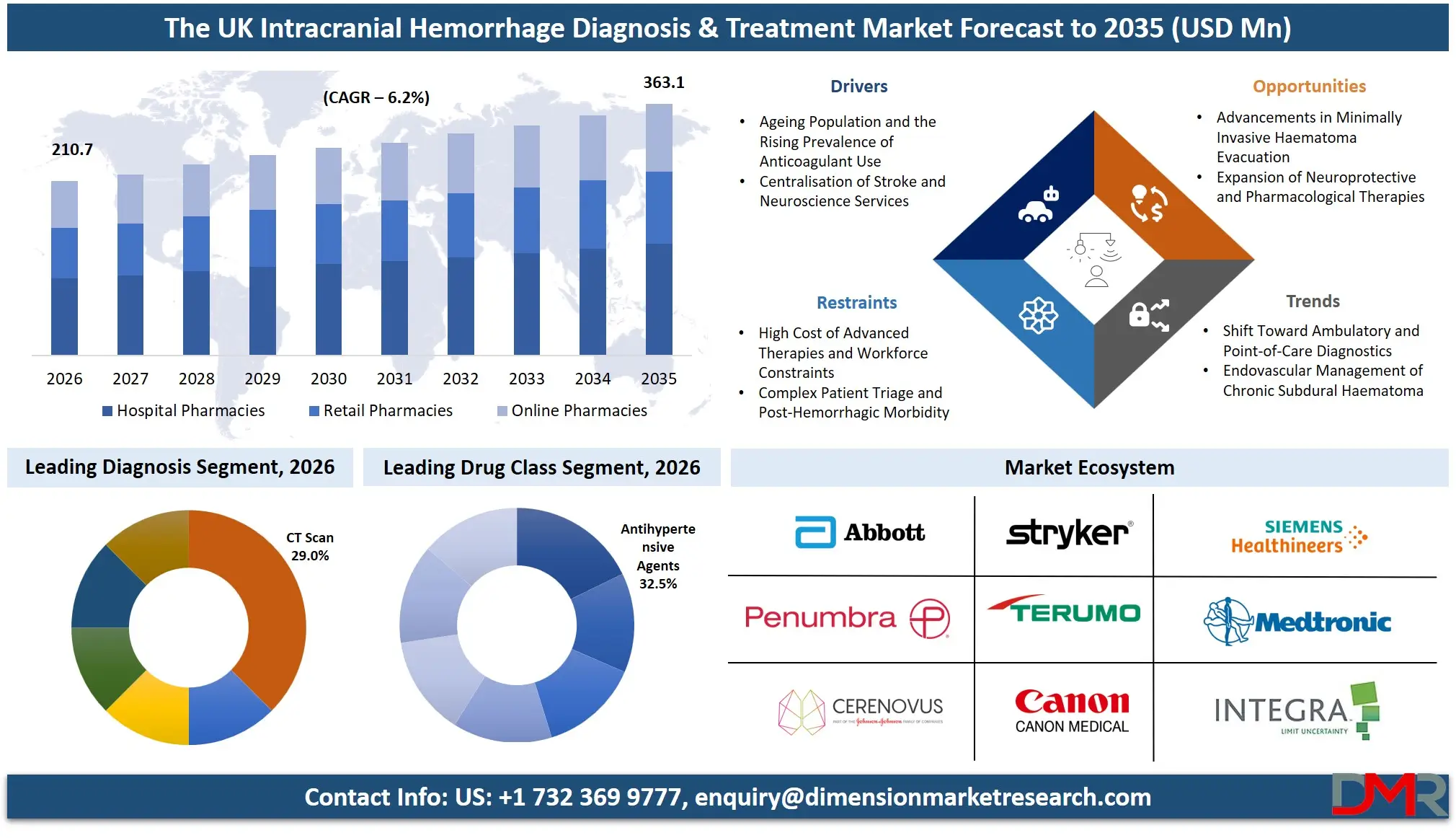

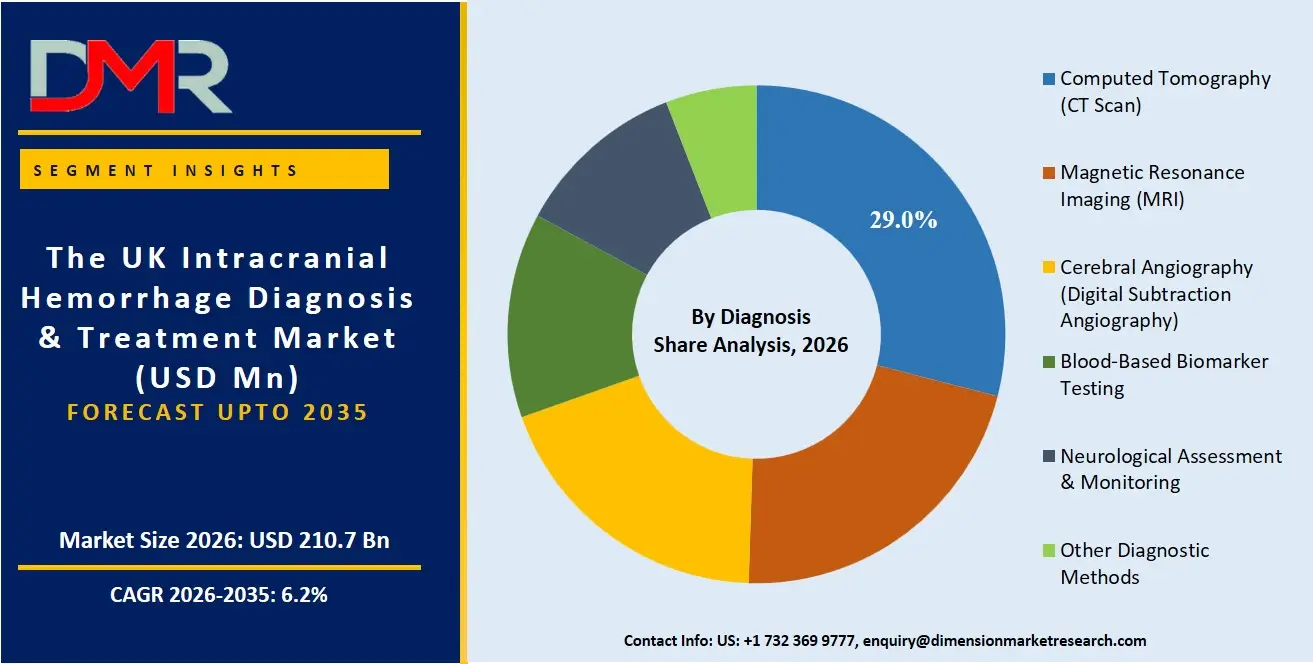

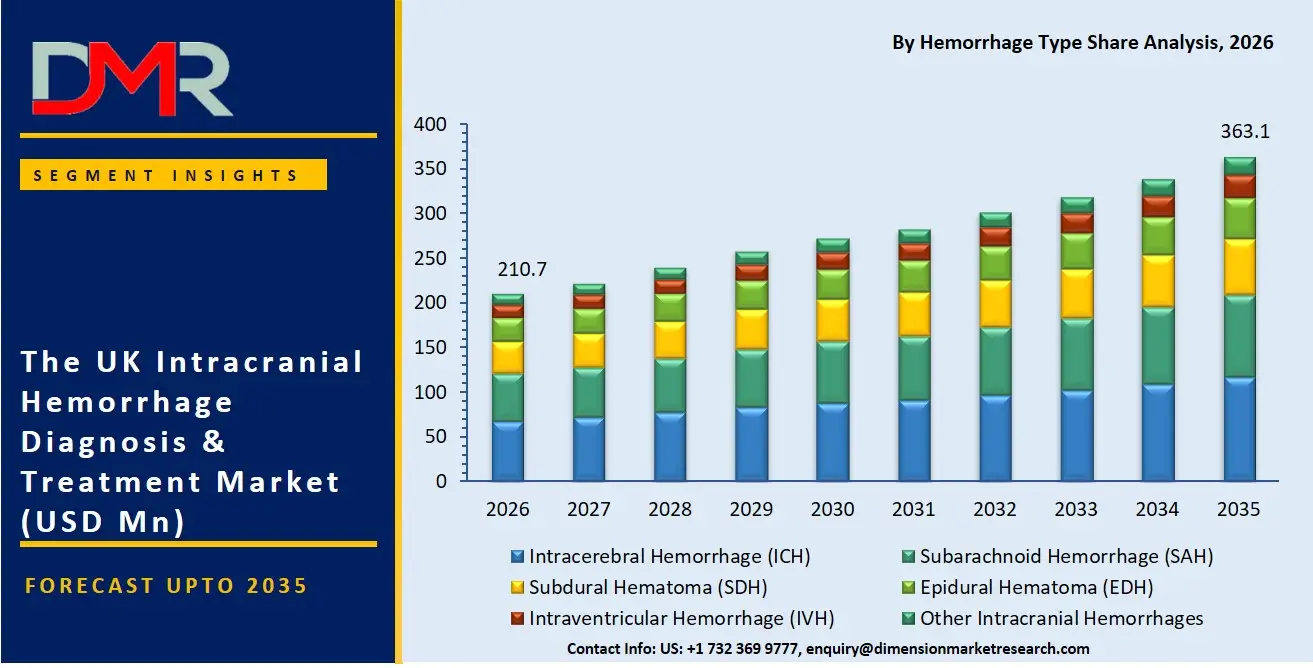

The UK Intracranial Hemorrhage Diagnosis & Treatment Market is projected to reach a value of USD 210.7 million in 2026, and it is further anticipated to reach USD 363.1 million by 2035, growing at a CAGR of 6.2% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The market for intracranial hemorrhage (ICH) management in the United Kingdom has witnessed steady growth, driven by an ageing population with a high prevalence of cerebrovascular risk factors and the rapid adoption of advanced neurosurgical and diagnostic technologies. The market encompasses the entire clinical pathway, from emergency neuroimaging for haemorrhagic stroke differentiation to acute medical interventions and complex surgical procedures. The rising incidence of traumatic brain injury (TBI) and spontaneous haemorrhagic stroke, coupled with the National Health Service's (NHS) focus on centralising acute stroke services into hyper-acute stroke units (HASUs) and comprehensive neuroscience centres, is a primary catalyst for this market's expansion.

Key Takeaways

- Market Size & Forecast: The UK market for intracranial hemorrhage diagnosis and treatment is forecast to attain a value of USD 210.7 million by 2026, expanding to USD 363.1 million by 2035, underpinned by the NHS Long Term Plan's emphasis on improving stroke and trauma care pathways and integrating cutting-edge neuro-interventional radiology.

- Growth Rate & Outlook: The market is predicted to register a CAGR of 6.2%, attributed to the rising geriatric demographic susceptible to cerebral amyloid angiopathy and anticoagulant-related bleeds, alongside the increasing adoption of minimally invasive neurosurgical techniques.

- Primary Growth Drivers: Critical growth factors include the integration of artificial intelligence (AI) in diagnostic imaging for rapid detection of large vessel occlusion and haemorrhage, the introduction of novel reversal agents for direct oral anticoagulants (DOACs), and a strong national research infrastructure conducting clinical trials in neurocritical care.

- Key Market Trends: Dominant trends involve the shift from open craniotomy to minimally invasive parafascicular surgery for intracerebral haemorrhage evacuation, the use of mobile stroke units equipped with CT scanners, and a growing focus on personalised rehabilitation protocols leveraging neuroplasticity and robotic-assisted therapy.

- By Hemorrhage Type Analysis: The spontaneous intracerebral haemorrhage (ICH) segment holds a significant share, driven by the high burden of hypertension and anticoagulant use in the UK's ageing population. Chronic subdural hematoma (CSDH) is a rapidly growing subsegment due to its strong correlation with age-related brain atrophy and the increasing use of antiplatelet agents.

- By Diagnosis Analysis: Computed Tomography (CT) imaging, particularly non-contrast CT and CT angiography, dominates the diagnostic market as the first-line, gold-standard modality for the emergency triage of suspected intracranial bleeds in Accident & Emergency (A&E) departments across the NHS.

What is the Intracranial Hemorrhage Diagnosis & Treatment?

Intracranial hemorrhage diagnosis and treatment refers to the comprehensive clinical approach for managing bleeding within the skull, a life-threatening medical emergency. This involves rapid neuroradiological assessment to distinguish between different haemorrhagic stroke subtypes such as intracerebral, subarachnoid, subdural, and epidural haematomas from ischaemic stroke, as the therapeutic pathways are diametrically opposed. Treatment is a multidisciplinary effort encompassing emergency medical stabilization, neurosurgical intervention to evacuate space-occupying haematomas and decompress the brain, endovascular procedures to secure ruptured aneurysms, and long-term neurorehabilitation to address post-stroke sequelae. In the UK, this care is delivered through a tiered system of trauma units, HASUs, and specialist neuroscience centres, with a strong emphasis on adherence to National Institute for Health and Care Excellence (NICE) guidelines for head injury and stroke management.

Use Cases

- Hyperacute Stroke Triage: Paramedics and emergency physicians use clinical assessment tools and immediate non-contrast CT scanning in a HASU to rapidly differentiate a haemorrhagic stroke from an ischaemic event, a critical decision that contraindicates thrombolysis and directs the patient toward blood pressure management or neurosurgery.

- Aneurysmal Subarachnoid Hemorrhage Management: A neurosurgical team at a tertiary care centre performs a CT angiogram followed by digital subtraction angiography to identify a ruptured cerebral aneurysm, then proceeds with endovascular coiling or microsurgical clipping to prevent a catastrophic re-bleed.

- Traumatic Brain Injury Pathway: A trauma centre manages a patient with an acute subdural haematoma following a fall, performing an emergency decompressive craniectomy to evacuate the clot and manage life-threatening intracranial pressure (ICP) elevations.

- Anticoagulation Reversal in ICH: A specialist pharmacist in an acute medical unit immediately administers a specific reversal agent, such as idarucizumab or andexanet alfa, to a patient on direct oral anticoagulants presenting with a spontaneous intracerebral haemorrhage.

How AI is Transforming the Intracranial Hemorrhage Diagnosis & Treatment Market?

The impact of AI on the UK intracranial hemorrhage market is centred on accelerating time-to-diagnosis and improving prognostic accuracy within the NHS's resource-constrained environment. AI-driven triage and computer-aided detection (CAD) software are being deployed to analyse CT scans in real-time, flagging critical findings like hyperdense haematomas, midline shift, and hydrocephalus to the radiology worklist within seconds, thereby slashing door-to-treatment times. Beyond detection, machine learning algorithms are being used to provide quantitative volumetric analysis of haematoma expansion and predict functional outcomes by integrating imaging biomarkers with clinical parameters, such as the Glasgow Coma Scale and INR levels. This supports clinicians in making nuanced decisions about surgical evacuation versus conservative neurocritical care. Furthermore, AI-powered tools are streamlining the often-complex pathway of transferring critical images between district general hospitals and tertiary neuroscience centres for specialist neurosurgical opinions, enhancing the hub-and-spoke model of care.

Market Dynamics

Key Drivers in the UK Intracranial Hemorrhage Diagnosis & Treatment Market

Ageing Population and the Rising Prevalence of Anticoagulant Use

A primary driver is the UK's demographic shift towards an older population, which exhibits a higher incidence of both falls-related traumatic haematomas and spontaneous ICH linked to conditions like hypertension and cerebral amyloid angiopathy. Concomitantly, the widespread prescription of anticoagulants and antiplatelet agents for atrial fibrillation and other cardiovascular conditions in this demographic has significantly increased the risk of major bleeding events. This dual trend directly fuels demand for specialist diagnostic services, rapid-access neuroimaging, and the effective management of haemorrhagic complications with specific pharmacological reversal strategies.

Centralisation of Stroke and Neuroscience Services

NHS England's strategic reconfiguration of services into hyper-acute stroke units and specialist neuroscience centres is a powerful market driver. This centralisation concentrates clinical expertise, advanced imaging modalities like catheter angiography labs, and neurosurgical resources, creating high-volume hubs that are more efficient at procuring and adopting advanced technologies. It ensures that patients with complex intracranial bleeds, such as aneurysmal SAH, have timely access to 24/7 endovascular coiling or microsurgical clipping, thereby standardising treatment protocols across the country and improving outcomes which, in turn, validates investment in these technologies.

Restraints in the UK Intracranial Hemorrhage Diagnosis & Treatment Market

High Cost of Advanced Therapies and Workforce Constraints

The capital and operational expenditure associated with equipping comprehensive stroke and neuroscience centres is substantial. The cost of biplane angiography systems, advanced 3-Tesla MRI scanners, and the highly skilled interventional neuroradiology and neurosurgery workforce required to operate them limits their availability to major urban hubs. This creates capacity pressure and workforce burnout, particularly as out-of-hours interventional services are resource-intensive. The specialised training pipeline for neurosurgeons and interventional neuroradiologists is lengthy, creating a bottleneck that can slow the adoption of cutting-edge minimally invasive surgical techniques on a national scale.

Complex Patient Triage and Post-Haemorrhagic Morbidity

Despite advancements in acute care, intracranial hemorrhage carries high rates of mortality and long-term neurological disability. Prognostic uncertainty makes clinical decision-making at the extremes—whether to offer aggressive surgical intervention for a devastating ICH—extremely challenging. Furthermore, the downstream social care and rehabilitation costs associated with survivors are immense, placing a burden on a healthcare system increasingly focused on outcome-based value. This complexity can make health economic evaluations for new, high-cost technologies difficult to prove, potentially acting as a barrier to market access and commissioning.

Growth Opportunities in the UK Intracranial Hemorrhage Diagnosis & Treatment Market

Advancements in Minimally Invasive Haematoma Evacuation

A significant commercial and clinical opportunity lies in the shift towards minimally invasive surgery (MIS) for intracerebral haemorrhage and chronic subdural haematoma. Technologies such as the BrainPath parafascicular approach, Artemis Neuro Evacuation Device, and middle meningeal artery (MMA) embolisation represent a paradigm shift from the open craniotomy, which involves significant collateral tissue damage. In the UK context, where reducing ICU length of stay and improving functional neurological outcomes are paramount for the NHS, there is a strong growth runway for devices and trials that can demonstrate superior patient recovery profiles with these less invasive techniques.

Expansion of Neuroprotective and Pharmacological Therapies

Beyond acute reversal and blood pressure control, the current absence of a specific neuroprotective agent approved for ICH represents a multi-billion-dollar gap in the pharmacological market. The UK's strong academic clinical trial networks offer a fertile environment for pharmaceutical companies to investigate novel therapies targeting the secondary injury cascade, such as iron chelators, stem cell therapies, and anti-inflammatory agents. The successful development and commercialisation of a drug that limits peri-haematomal oedema and neuronal death would be a transformative growth opportunity, dramatically reshaping the current standard of care.

Trends in the UK Intracranial Hemorrhage Diagnosis & Treatment Market

Shift Toward Ambulatory and Point-of-Care Diagnostics

A notable trend is the investigation into mobile stroke units (MSUs) with onboard CT scanners and point-of-care blood-based biomarker testing. In the UK, pilot schemes are exploring the feasibility of MSUs to expedite the diagnosis of intracranial hemorrhage at the patient's location, thereby facilitating direct transport to the most appropriate specialist centre (bypassing general A&Es) and enabling the pre-hospital initiation of blood pressure-lowering therapy. Parallel research into a diagnostic 'triage test' using GFAP and UCH-L1 biomarkers to rapidly rule out hemorrhage would revolutionise pre-hospital stroke pathways.

Endovascular Management of Chronic Subdural Haematoma

A practice-changing trend is the emergence of middle meningeal artery (MMA) embolisation as a standalone or adjunctive treatment for chronic subdural haematoma, particularly in recurrent cases or patients with high surgical risk. By endovascularly devascularising the pathological neomembranes that cause CSF leakage, this procedure addresses the underlying pathophysiology rather than simply draining the fluid. Interventional neuroradiologists in leading UK neuroscience centres are increasingly adopting this technique, which reduces recurrence rates and is a less invasive alternative to a burr hole craniostomy for elderly patients, marking a significant evolution in therapeutic options.

Research Scope and Analysis

The UK Intracranial Hemorrhage Diagnosis & Treatment Market is segmented by hemorrhage type, diagnosis, treatment, drug class, distribution channel, and end user, including tertiary care hospitals, neurology centres, and trauma centres.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Hemorrhage Type Analysis

The intracerebral hemorrhage (ICH) segment is projected to dominate the UK market due to its high incidence, significant mortality and morbidity burden, and the direct link to prevalent risk factors like hypertension and anticoagulant-related coagulopathy.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

ICH represents a critical focus area for clinical research into both neuroprotective therapeutics and MIS evacuation techniques. The chronic subdural hematoma (CSDH) subsegment is experiencing accelerated growth, fuelled by the UK's demographic shift toward an ageing population prone to brain atrophy, low-impact head trauma, and increased usage of antiplatelet and anticoagulant medications, making its management a core activity in regional neurosurgical units.

By Diagnosis Analysis

Computed Tomography (CT Scan) is the cornerstone diagnostic modality in the UK market, with non-contrast CT serving as the unrivalled gold-standard first-line emergency investigation due to its speed, widespread availability in NHS A&E departments, and superb sensitivity for acute haemorrhage. CT Angiography (CTA) is heavily utilised to diagnose vascular pathologies like aneurysms and arteriovenous malformations (AVMs). While MRI with susceptibility-weighted imaging is gaining traction for detecting microbleeds and underlying pathology in the non-acute phase, CT's utility in time-critical treatment decisions, from triaging for thrombolysis to emergency surgical evacuation, ensures its dominant market share.

By Treatment Analysis

Medical management represents the foundational therapeutic pillar, encompassing the spectrum of care from aggressive blood pressure control and ICP management in an ICU to anticoagulation reversal and seizure prophylaxis. This segment holds a substantial market volume as it is the standard approach for most non-surgical ICHs and is a critical adjunct to all surgical cases. However, the surgical treatment segment is the high-value growth engine, driven by the evolution from classical craniotomy towards MIS techniques such as endoscopic haematoma evacuation and stereotactic aspiration, which aim to reduce operative morbidity. Endovascular coiling is the dominant modality for securing ruptured aneurysms, underscoring the pivotal role of interventional neuroradiology in modern hemorrhage management.

By Drug Class Analysis

The segment for reversal agents for anticoagulants is experiencing the most dynamic growth in the UK pharmaceutical market. The FDA and EMA-approved specific reversal agents for Factor Xa inhibitors (andexanet alfa) and direct thrombin inhibitors (idarucizumab) have revolutionised acute management, enabling rapid cessation of bleeding and facilitating safe surgical intervention. Antihypertensive agents, particularly intravenous nicardipine and clevidipine, form a massive volume market for the intensive control mandated in hyperacute ICH care. Concurrently, the market for hemostatic agents is also significant in managing perioperative and coagulopathic bleeds.

By Distribution Channel Analysis

Hospital pharmacies overwhelmingly dominate the distribution landscape for intracranial hemorrhage management. The entire clinical pathway from the administration of intravenous antihypertensives, hyperosmolar therapy, and complex reversal agents in the emergency department and neurocritical care unit, to the specialised consumables used in angiography suites and operating theatres is inseparable from the hospital infrastructure. Retail and online pharmacies hold a negligible share in the acute phase, though they play a role in the chronic distribution of secondary prevention medications and post-rehabilitation pharmacotherapies.

By End User Analysis

Tertiary care hospitals and comprehensive neuroscience centres are the primary end users, functioning as the apex of the hub-and-spoke model for ICH care in the UK. These sites house the neurosurgical theatres, interventional neuroradiology suites, and specialised neurocritical care units (NICUs) essential for managing complex cases like aneurysmal SAH and massive space-occupying hematomas. This is closely followed by the expanding network of hyper-acute stroke units (HASUs), which are the crucial entry points for the majority of spontaneous ICH cases, providing the immediate diagnostic and acute medical management before onward referral for surgery if required.

The UK Intracranial Hemorrhage Diagnosis & Treatment Market Report is segmented on the basis of the following:

By Hemorrhage Type

- Intracerebral Hemorrhage (ICH)

- Subarachnoid Hemorrhage (SAH)

- Subdural Hematoma (SDH)

- Acute Subdural Hematoma

- Chronic Subdural Hematoma

- Epidural Hematoma (EDH)

- Intraventricular Hemorrhage (IVH)

- Other Intracranial Hemorrhages

By Diagnosis

- Computed Tomography (CT Scan)

- Non-Contrast CT

- CT Angiography (CTA)

- CT Perfusion

- Magnetic Resonance Imaging (MRI)

- Conventional MRI

- MR Angiography (MRA)

- Cerebral Angiography (Digital Subtraction Angiography)

- Blood-Based Biomarker Testing

- Neurological Assessment & Monitoring

- Other Diagnostic Methods

By Treatment

- Medical Management

- Blood Pressure Management

- Anticoagulation Reversal Therapy

- Osmotherapy

- Anticonvulsants

- Other Pharmacological Therapies

- Surgical Treatment

- Craniotomy

- Minimally Invasive Hematoma Evacuation

- Decompressive Craniectomy

- Endoscopic Surgery

- Ventricular Drainage (EVD)

- Aneurysm Clipping

- Endovascular Coiling

- Rehabilitation Therapy

By Drug Class

- Antihypertensive Agents

- Hemostatic Agents

- Reversal Agents for Anticoagulants

- Antiepileptic Drugs

- Osmotic Diuretics

- Neuroprotective Agents

- Other Drug Classes

By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

By End User

- Tertiary Care Hospitals

- Multispecialty Hospitals

- Neurology & Neurosurgery Centers

- Trauma Centers

- Diagnostic Imaging Centers

- Rehabilitation Centers

- Other End Users

Competitive Landscape

The competitive landscape of the UK intracranial hemorrhage diagnosis and treatment market is shaped by a blend of global medical device giants, specialised pharmaceutical firms, and pioneering interventional technology companies. These entities compete intensely on the pillars of technological innovation, clinical evidence demonstrating superior patient outcomes, and alignment with the NHS's value-based procurement agenda. The market for neurosurgical tools is seeing a vibrant race toward validating minimally invasive evacuation systems, while the pharmaceutical space is dominated by the competition among proprietary anticoagulation reversal agents. Strategic collaborations with leading UK neuroscience centres and academic institutions like the Queen Elizabeth Hospital Birmingham and Salford Royal Hospital are not merely beneficial but essential for conducting pivotal clinical trials, gaining clinician acceptance, and ultimately securing formulary inclusion and commissioning support from NICE and NHS England.

Some of the prominent players in The UK Intracranial Hemorrhage Diagnosis & Treatment Market are:

- Medtronic plc

- Stryker Corporation

- Johnson & Johnson MedTech (Cerenovus)

- Penumbra, Inc.

- MicroVention, Inc.

- Terumo Corporation

- Integra LifeSciences Holdings Corporation

- B. Braun SE

- Brainlab AG

- Siemens Healthineers AG

- GE HealthCare Technologies Inc.

- Canon Medical Systems Corporation

- Philips Healthcare

- Fujifilm Healthcare

- Abbott Laboratories

- Bristol Myers Squibb

- Bayer AG

- AstraZeneca plc

- Boehringer Ingelheim International GmbH

- Sosei Heptares plc

- Other Key Players

Recent Developments

- February 2026: EMBOLISE-2 results presented at ISC 2026 showed upfront Onyx embolization roughly halved the primary endpoint in mildly symptomatic, non-surgical subdural haematoma patients across 60 US centers.

- December 2025: FDA approved Medtronic's Onyx liquid embolic system for MMA embolization as a surgical adjunct in subacute/chronic subdural haematoma, based on EMBOLISE trial results.

- December 2025: FDA-mandated US withdrawal of andexanet alfa (Andexxa) announced, effective 22 December 2025, disrupting the Factor Xa reversal-agent market as clinicians shift toward PCC-based protocols and await alternatives like ciraparantag.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 210.7 Mn |

| Forecast Value (2035) |

USD 363.1 Mn |

| CAGR (2026–2035) |

6.2% |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Hemorrhage Type, By Diagnosis, By Treatment, By Drug Class, By Distribution Channel, and By End User |

| Country Coverage |

The UK |

Frequently Asked Questions

How big is the UK Intracranial Hemorrhage Diagnosis & Treatment Market?

▾ The UK Intracranial Hemorrhage Diagnosis & Treatment market is poised to be valued at USD 210.7 million in 2026 and is projected to reach USD 363.1 million by 2035, driven by the demographic pressures of an ageing population and the increasing complexity of haemorrhagic stroke management.

What is the CAGR of the UK Intracranial Hemorrhage Diagnosis & Treatment Market from 2026 to 2035?

▾ The market is expected to grow at a CAGR of 6.2% from 2026 to 2035, reflecting the steady translation of technological innovations in neuro-intervention and MIS into standard NHS clinical practice, alongside growing pharmaceutical expenditure on novel reversal agents.

What factors are driving the growth of the UK Intracranial Hemorrhage Diagnosis & Treatment Market?

▾ Key drivers include the high prevalence of cerebrovascular disease and falls in the geriatric population, the widespread use of long-term anticoagulation, the centralisation of specialist neuroscience services, and the rapid integration of AI-augmented diagnostics for faster treatment decisions.

What are the major trends in the UK Intracranial Hemorrhage Diagnosis & Treatment Market?

▾ Major trends include a paradigm shift from open craniotomy to MIS parafascicular surgery for haematoma evacuation, the rise of endovascular MMA embolisation for chronic subdural haematoma, and the exploration of mobile stroke units and blood-based biomarkers to expedite pre-hospital diagnosis.

Who are the key players in the UK Intracranial Hemorrhage Diagnosis & Treatment Market?

▾ The market includes leading global medical device and pharmaceutical companies active in neurosurgery, interventional neuroradiology, and neurocritical care, who are engaged in a competitive race to establish their technologies as the new standard of care through robust health-economic data tailored for the NHS.

How is the UK Intracranial Hemorrhage Diagnosis & Treatment Market segmented?

▾ The market is segmented by Hemorrhage Type, Diagnosis, Treatment, Drug Class, Distribution Channel, and End User.