What is the US Automotive Adaptive Front Lighting System Market Size?

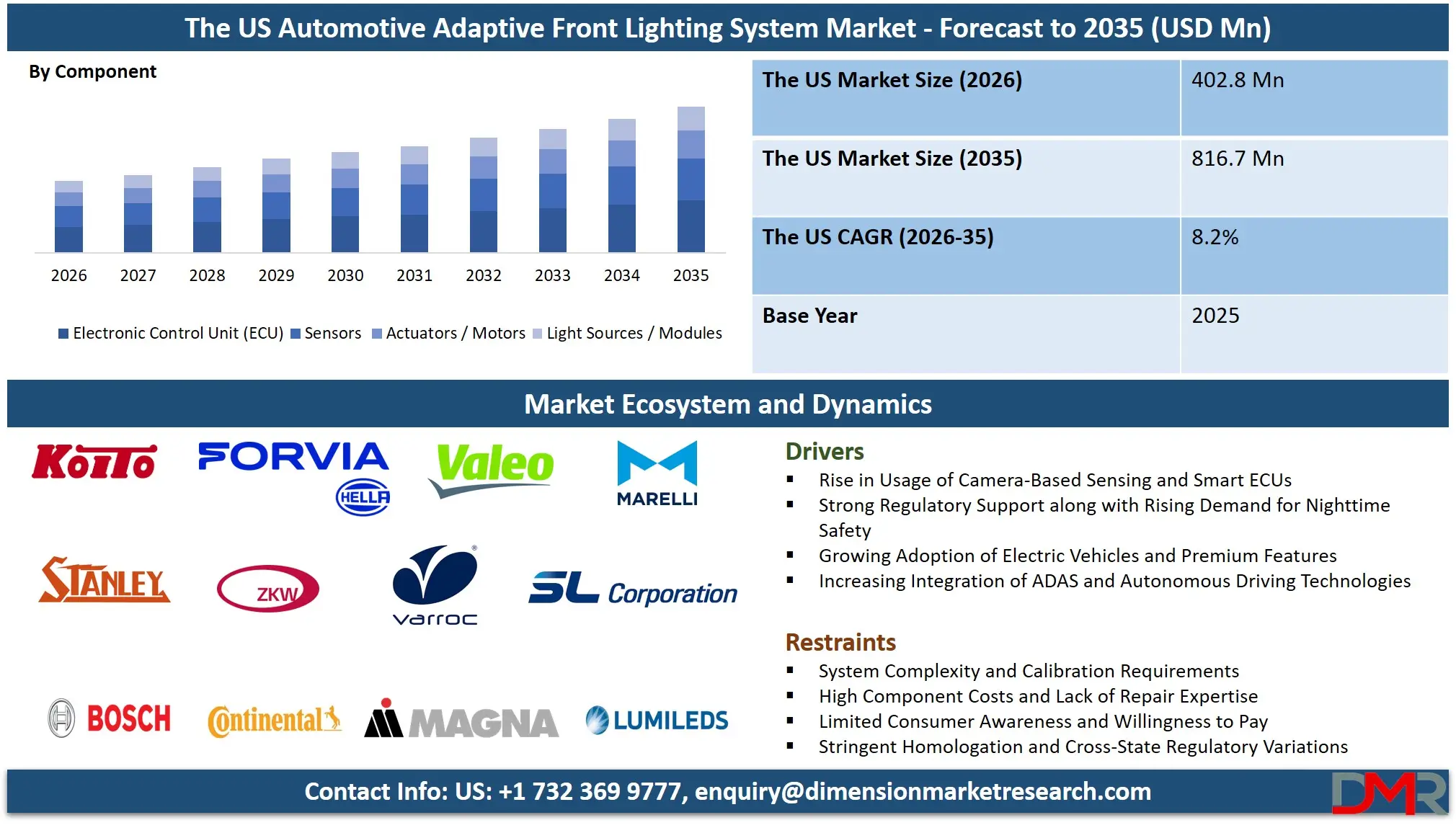

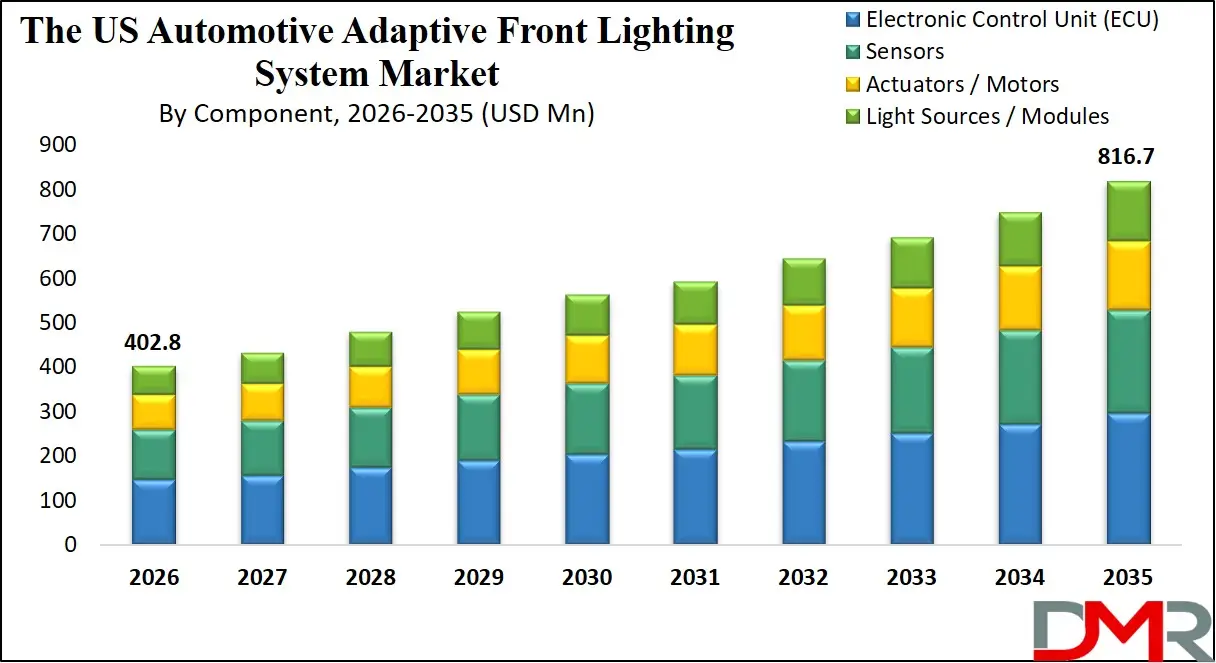

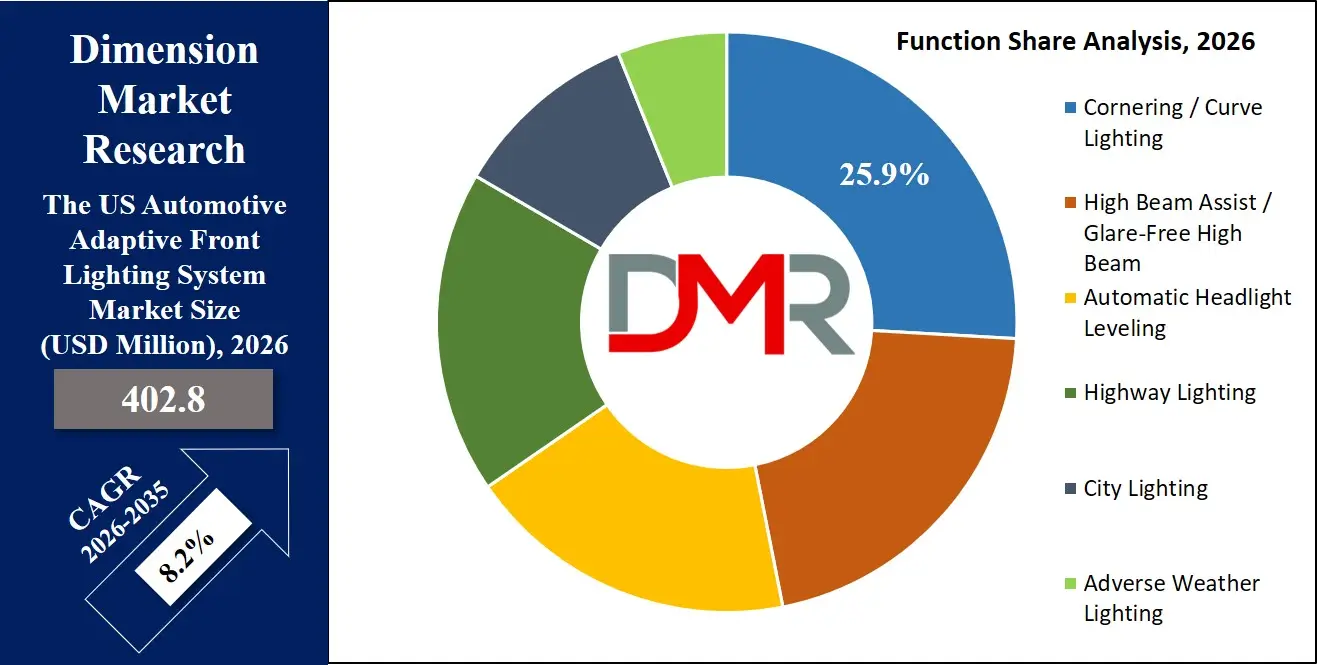

The US Automotive Adaptive Front Lighting System Market size is projected to be valued at USD 402.8 million in 2026 and is expected to grow at a CAGR of 8.2% from 2026 to 2035, reaching approximately USD 816.7 million by 2035.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The US adaptive front lighting system market of the automotive industry is recording high growth in both passenger and commercial vehicles due to the ever-changing consumer tastes and preferences, coupled with safety rules and regulations that are redefining the market. These changes are driven by the growing focus on vehicle safety, availability of strict federal lighting and road safety regulations, and the growing incorporation of state-of-the-art technologies like LED and matrix lighting, sensors, cameras, and real-time adaptive control systems.

Moreover, the United States is experiencing growth through the following factors: an increase in high-end cars sales, a higher number of vehicles using ADAS and connected car technology, a growing number of individuals aware of why night-time driving is not safe, significant investments, direct involvement of the major automotive OEMs and lighting producers, ongoing development of vehicle electronics, and the integration of intelligent lighting systems with next-generation mobility solutions.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Key Takeaways

- Market Size & Forecast: The US automotive adaptive front lighting system market is projected to reach USD 402.8 million in 2026 and expand to USD 816.7 million by 2035, driven by rising vehicle safety standards and federal lighting technology approvals.

- Growth Rate & Outlook: The market is estimated to experience a compound annual growth rate of 8.2% during the forecast period of 2026 to 2035.

- Primary Growth Drivers: Key growth drivers include rising nighttime accident rates, expansion of advanced driver assistance systems (ADAS), and increasing demand for enhanced visibility among commercial fleet operators.

- Key Market Trends: The major market trends that have shown a high potential of this market include more people using matrix LED modules, integration of camera-based predictive lighting, and glare-free high beam analytics development.

- By Component Analysis: The Electronic Control Unit (ECU) segment is expected to get the largest revenue share in 2026 since it is the fundamental intelligence-gathering and decision-making element of any adaptive front lighting system.

- By Technology / Light Source Analysis: The LED segment is going to acquire the largest share of the US automotive adaptive front lighting system market in 2026.

- By Product Type Analysis: The Adaptive Driving Beam (ADB) segment is expected to get the largest revenue share in 2026, as it provides the highest level of glare-free high beam functionality for nighttime driving safety.

What is Automotive Adaptive Front Lighting System?

Automotive Adaptive Front Lighting System (AFS) is a high-tech vehicle lighting technology that is mounted on the front side of vehicles, unlike fixed-beam headlights, which are expected to vary the patterns of the light beams according to the conditions of driving, the speed of the vehicle, the angle of the steering wheel, and the presence of other vehicles. This can be accompanied by simple systems, which can be compared to matrix LED systems, but are very effective, as opposed to traditional halogen headlights. They are able to operate in standalone mode or integrated with vehicle ADAS sensors. Some of the technologies that may improve the functionality of the adaptive front lighting system are the use of camera-based beam control, dynamic bending modules, and glare-free high beam.

Use Cases

- Rural Curving Roads: Adaptive headlights adjust beam direction to illuminate blind corners, delivering safer nighttime driving for families and commuters traveling on unlit country roads.

- Commercial Fleet Night Operations: Delivery vans and logistics trucks powered by adaptive lighting examples offering objectives to fleet operators to decrease nighttime accident rates across the United States, along with minimizing insurance claims.

- Highway High-Speed Driving: Speed-responsive beam patterns that extend range at higher speeds, serving long-haul drivers who are driving on interstates and reducing reliance on manual high beam switching.

- Adverse Weather Conditions: Rain and fog-optimized beam patterns that reduce back-glare, improve visibility, and provide significant safety improvements during storms.

- Residential Urban Driving: Glare-free ADB systems in city vehicles that keep high beams active while masking light from reaching oncoming cars, windshields, or rearview mirrors of preceding vehicles.

How AI Is Transforming the US Automotive Adaptive Front Lighting System Market?

Artificial intelligence is transforming the US Automotive Adaptive Front Lighting System Market by improving beam pattern prediction through predictive analytics and real-time camera sensor insights. It enables faster diagnosis with AI-driven object detection, automated light masking classification, and dynamic glare elimination for oncoming traffic. Remote system calibration is enhanced through continuous tracking and early anomaly detection for stepper motors, actuators, and leveling sensors. AI also facilitates predictive maintenance by analyzing historical failure patterns and alerting drivers before component malfunction occurs.

Lighting performance analysis benefits from natural language processing and automated reporting, enabling fleet operators to monitor headlight health remotely. AI also supports personalized beam scheduling and over-the-air updates for lighting algorithms, continuously learning from real-world driving scenarios to optimize beam throw distance and weather-specific lighting modes, ultimately enhancing nighttime driving safety and driver confidence.

Market Dynamics

Key Drivers of the US Automotive Adaptive Front Lighting System Market

Rise in Usage of Camera-Based Sensing and Smart ECUs

The rising usage of forward-facing cameras, radar sensors, and cloud-connected calibration solutions is providing enhanced insights into the operational performance of these adaptive lighting systems. This helps the OEMs identify areas where they can optimize beam throw and cut-off lines. Along with this, the rise in smart ECUs is helping in improving overall vehicle integration, thermal management, and system reliability, which is leading to more widespread use of adaptive front lighting systems. The capability of real-time beam shaping and managing pixel-level light distribution makes them crucial for modern vehicle installations.

Strong Regulatory Support along with Rising Demand for Nighttime Safety

The NHTSA final rule on Adaptive Driving Beam (ADB) is significantly boosting system adoption via regulatory approval and safety ratings, thereby enhancing the installation of adaptive lighting systems. Concurrently, increasing nighttime accident statistics and a move towards zero-fatality road safety have spurred commercial fleet operators and individual consumers to demand better visibility and self-adaptive headlights.

Restraints in the US Automotive Adaptive Front Lighting System Market

System Complexity and Calibration Requirements

Zoning restrictions on light intensity, environmental considerations like moisture ingress, and sensor alignment issues remain obstacles that hinder the deployment of projects. These issues contribute to extended calibration durations, thus increasing the difficulty of aftermarket replacements, especially for mid-sized vehicles equipped with camera-based adaptive systems.

High Component Costs and Lack of Repair Expertise

The utilization of sophisticated matrix LED modules, laser light sources, and smart actuators involves huge capital expenditure. This makes it difficult for smaller OEMs and aftermarket shops to engage in such systems, thereby depending heavily on specialized diagnostic tools. Further, the lack of qualified personnel in calibrating and integrating such lighting technology poses challenges in rapid deployment, especially for independent repair facilities.

Growth Opportunities in the US Automotive Adaptive Front Lighting System Market

Development of AI-Enabled Predictive Lighting Solutions

Forecasting road curvature, detecting oncoming vehicles, and predictive beam adaptation with the help of artificial intelligence are being applied with the aim of enhancing the performance of the system and minimizing driver distraction. These technologies are facilitating a wider base of data-driven decision-making and enhancing the long-term performance of lighting assets. In the long run, AI optimization will help to achieve more effective energy management and performance-based service contracts.

Expansion of Over-the-Air (OTA) Calibration and Cloud-Based Diagnostics

The growing requirement of remote system management is encouraging the use of cloud-based solutions to facilitate centralized calibration and troubleshooting, thereby optimizing the performance of the system. It helps save on workshop costs while also enhancing the reliability of the system. Cloud technology also facilitates the remote management of multiple vehicle fleets through a single window solution.

The US Automotive Adaptive Front Lighting System Market Trends

AI-Enabled Performance Monitoring Systems

Artificial intelligence-based tools are being integrated into lighting control modules for the study of beam throw, glare zones, and thermal variability analysis. This will help in improved early detection of actuator faults and improve preventive maintenance scheduling. With the improvement in data quality, the future beam pattern forecast accuracy is bound to increase.

Growing Adoption of Cloud Analytics and Early Digital Twin

The use of cloud analytics solutions for performance monitoring and reporting is becoming common practice. Cloud analytics solutions provide capabilities such as real-time dashboards, automatic alerts, and benchmarking of historical lighting performance. In more sophisticated cases, digital twin simulations are starting to be developed at an early stage, which will help model system behavior for better adaptive algorithm predictions.

Research Scope and Analysis

By Component Analysis

The Electronic Control Unit (ECU) is expected to take over the component segment with approximately 28.4% share in 2026, owing to increased processing power, cost optimization, and increased use of the systems in commercial and electric vehicle projects. These types of systems enable real-time beam adaptation and increased safety, fueling increased application. Conversely, sensors (camera, radar, steering angle, speed) continue to be a vital element in every installation, especially in higher-end installations and projects with variable driving characteristics, since they permit high-accuracy beam control and interaction with ADAS as well as reliability of the system, though the cost sensitivity and calibration may affect the choice of technology.

By Technology / Light Source Analysis

The segment is projected to be dominated by LED with approximately 58.7% share in 2026 because of the growing need for energy-efficient and long-lasting lighting solutions in commercial and passenger vehicle environments. This growth is also supported by a focus on cost-effective illumination and lower thermal complexity. The increasing adoption of premium vehicle production is driving demand for laser lights, with automotive systems equipped with phosphor converters and lenses allowing extremely long beam range. OLEDs are gaining traction in high-end luxury vehicles where styling and homogeneous light distribution justify higher investment.

By Product Type Analysis

The product type segment is poised to be dominated by Adaptive Driving Beam (ADB) with approximately 44.2% share in 2026 as a result of the rising demand for glare-free high-beam functionality and improved nighttime safety in passenger car applications. This growth is also supported by the emphasis on driver convenience, improved visibility, and durability. Static adaptive front lighting and dynamic/bending light solutions are still being implemented in selected entry-level and mid-range applications based on vehicle-specific requirements and cost considerations.

By Function Analysis

The cornering/curve lighting segment is estimated to be the leading function segment with about 25.9% share in 2026 due to the unique visibility needs of rural, mountainous, and suburban driving conditions, which require tailored beam swivel angles, sensor integration, and service calibration.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Lighting suppliers are finding more major OEMs and commercial fleet clients to get custom solutions and multi-year performance warranties. The remainder of the market is satisfied by highway lighting, adverse weather lighting, and other functions, especially entry-level vehicles, which prefer standardized and economical beam patterns.

By Vehicle Type Analysis

The passenger cars segment is estimated to be the leading vehicle type segment with about 67.3% share in 2026 due to the unique lighting needs of sedans, SUVs, and luxury vehicles, which require tailored system integration, sensor fusion, and service maintenance. Lighting providers are finding more major automotive OEMs and EV manufacturers to get custom solutions and multi-year supply contracts. The remainder of the market is satisfied by light commercial vehicles, heavy commercial vehicles, and electric vehicles, especially fleet installations, which prefer standardized and durable systems.

By Sales Channel Analysis

The OEM segment is estimated to be the leading sales channel segment with about 78.5% share in 2026 due to factory-integrated calibration, warranty coverage, and seamless ADAS integration. Automotive manufacturers prefer direct supply contracts for adaptive lighting systems to ensure quality and compliance. The aftermarket segment serves replacement needs, vehicle upgrades, and retrofits for older vehicles, though calibration complexity and diagnostic requirements remain key challenges.

The US Automotive Adaptive Front Lighting System Market Report is segmented based on the following:

By Component

- Electronic Control Unit (ECU)

- Sensors

- Camera

- Radar

- Steering Angle Sensor

- Speed Sensor

- Actuators / Motors

- Light Sources / Modules

By Technology / Light Source

- Halogen

- Xenon / HID (High-Intensity Discharge)

- LED (Light-Emitting Diode)

- OLED (Organic LED)

- Laser

By Product Type

- Static Adaptive Front Lighting

- Dynamic / Bending Light

- Matrix / Pixel Lighting

- Adaptive Driving Beam (ADB)

By Function

- Cornering / Curve Lighting

- High Beam Assist / Glare-Free High Beam

- Automatic Headlight Leveling

- Highway Lighting

- City Lighting

- Adverse Weather Lighting

By Vehicle Type

- Passenger Cars

- Hatchback

- Sedan

- SUV

- Luxury Vehicles

- Light Commercial Vehicles (LCV)

- Heavy Commercial Vehicles (HCV)

- Electric Vehicles (EVs)

By Sales Channel

- OEM (Original Equipment Manufacturer)

- Aftermarket

Competitive Landscape

The US automotive adaptive front lighting system industry is quite competitive, with the presence of leading manufacturers of ECUs, sensors, actuators, and light modules who vie for dominance in the market. Critical areas of differentiation include beam pattern accuracy, durability, warranty coverage, as well as ADAS integration and advanced sensor fusion capabilities. Additionally, regional tier-1 suppliers and calibration service players play an essential role in the deployment of systems.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Leading market participants are seeking to adopt a vertically integrated approach as well as forming partnerships to bolster their competitive edge. Some of the recent initiatives undertaken by industry leaders have been focused on buying up software providers for AI lighting applications and developing domestic manufacturing capacity via policy incentives such as the Bipartisan Infrastructure Law. The market is characterized by tough price competition, especially in the passenger car and entry-level segments.

Some of the prominent players in the US Automotive Adaptive Front Lighting System Market are:

- Koito Manufacturing Co., Ltd.

- Forvia SE (Hella GmbH & Co. KGaA)

- Valeo SE

- Marelli Holdings Co., Ltd.

- Stanley Electric Co., Ltd.

- ZKW Group GmbH

- Varroc Engineering Limited

- SL Corporation

- Ichikoh Industries, Ltd.

- Robert Bosch GmbH

- Continental AG

- Denso Corporation

- Texas Instruments Incorporated

- ams-OSRAM AG

- Lumileds Holding B.V.

- Aptiv PLC

- Magna International Inc.

- Hyundai Mobis Co., Ltd.

- Johnson Electric Holdings Limited

- Koninklijke Philips N.V.

- Other Key Players

Recent Developments

- March 2026: Koito Manufacturing Co., Ltd. expanded production capacity for advanced adaptive lighting modules to address rising demand from global OEMs, particularly for next-generation and electric vehicles.

- April 2025: Valeo SE announced a strategic partnership with Appotronics to develop next-generation front lighting systems integrating laser projection technology, aimed at enhancing adaptive driving beam (ADB) functionality and in-vehicle experience.

- January 2025: HELLA GmbH & Co. KGaA introduced advanced LED matrix headlamp systems featuring adaptive driving beam (ADB) and dynamic bending light technologies, enabling real-time adjustment of light distribution for improved night-time safety and driving comfort.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 402.8 Mn |

| Forecast Value (2035) |

USD 816.7 Mn |

| CAGR (2026–2035) |

8.2% |

| Historical Period |

2021 – 2025 |

| Forecast Period |

2027 – 2035 |

| Base Year |

2025 |

| Estimated Year |

2026 |

| Segments Covered |

By Component (Electronic Control Unit (ECU), Sensors, Actuators / Motors, Light Sources / Modules), By Technology / Light Source (Halogen, Xenon / HID (High-Intensity Discharge), LED (Light-Emitting Diode), OLED (Organic LED), Laser), By Product Type (Static Adaptive Front Lighting, Dynamic / Bending Light, Matrix / Pixel Lighting, Adaptive Driving Beam (ADB)), By Function (Cornering / Curve Lighting, High Beam Assist / Glare-Free High Beam, Automatic Headlight Leveling, Highway Lighting, City Lighting, Adverse Weather Lighting), By Vehicle Type (Passenger Cars, Light Commercial Vehicles (LCV), Heavy Commercial Vehicles (HCV), Electric Vehicles (EVs)), By Sales Channel (OEM (Original Equipment Manufacturer), Aftermarket) |

| Country Coverage |

The US |

Frequently Asked Questions

How big is the US Automotive Adaptive Front Lighting System Market?

▾ The US Automotive Adaptive Front Lighting System Market is valued at USD 402.8 million in 2026 and is projected to reach USD 816.7 million by the end of 2035.

What is the CAGR of the US Automotive Adaptive Front Lighting System Market from 2026 to 2035?

▾ The market is growing at a robust compound annual growth rate (CAGR) of 8.2% over the forecast period of 2026 to 2035.

What factors are driving the growth of the US Automotive Adaptive Front Lighting System Market?

▾ The rising nighttime accident rates and the NHTSA final rule on Adaptive Driving Beam (ADB) are the key factors driving the market growth.

What are the major trends in the US Automotive Adaptive Front Lighting System Market?

▾ Major trends in the market include the increasing shift toward matrix LED headlights, camera-based predictive lighting, glare-free high beam technology, and AI-driven adaptive beam control algorithms.

Who are the key players in the US Automotive Adaptive Front Lighting System Market?

▾ Some of the major key players in the US Automotive Adaptive Front Lighting System Market are Koito Manufacturing, Marelli Holdings Co., Ltd., Valeo SE, Forvia SE (Hella GmbH & Co. KGaA), Stanley Electric, Hyundai Mobis, and many others.

How is the US Automotive Adaptive Front Lighting System Market segmented?

▾ The market is segmented by Component, Technology / Light Source, Product Type, Function, Vehicle Type, and Sales Channel.