Market Overview

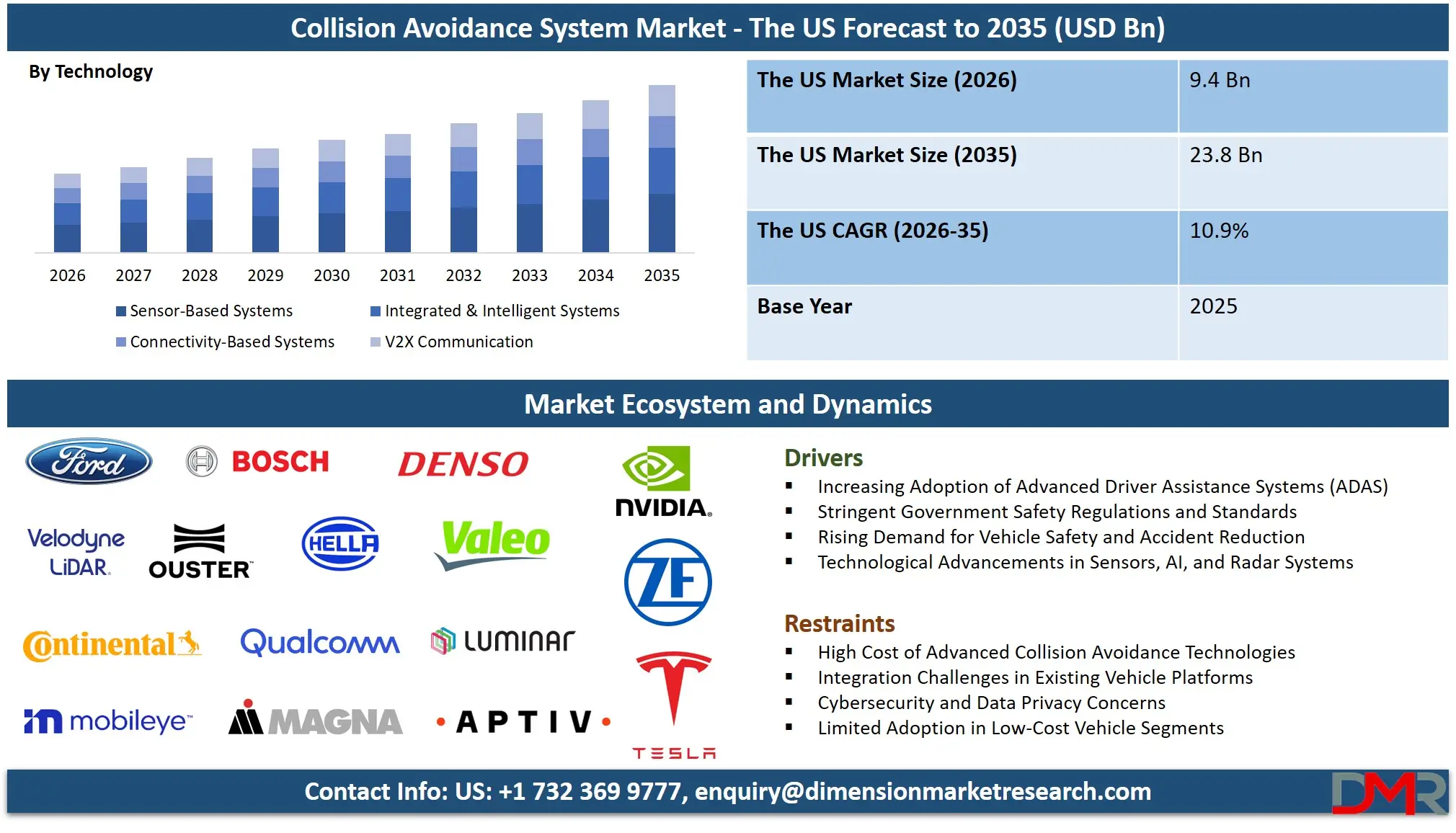

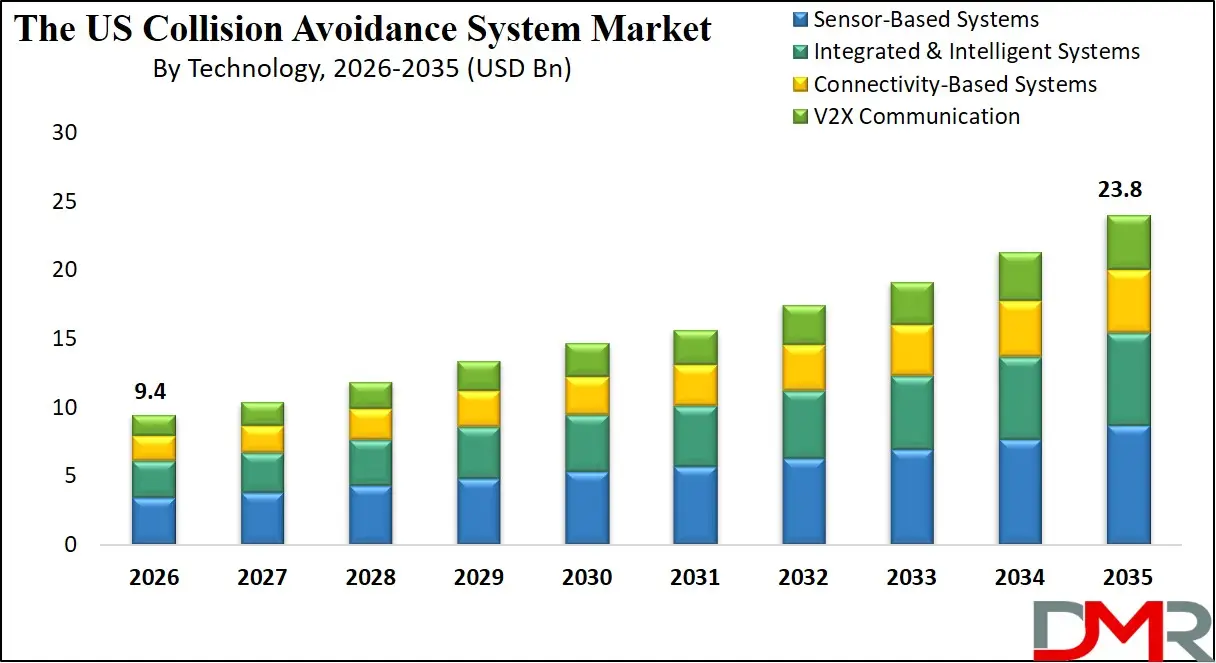

The U.S. Collision Avoidance System Market is projected to reach USD 9.4 billion in 2026 and is expected to grow at a CAGR of 10.9% from 2026 to 2035, reaching approximately USD 23.8 billion by 2035.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The market growth is driven by the increasing adoption of advanced driver assistance systems (ADAS), rising demand for vehicle safety technologies, and stringent automotive safety regulations across the United States. Additionally, advancements in radar sensors, LiDAR technology, artificial intelligence, and camera-based detection systems are accelerating the deployment of collision prevention and automated braking systems in both passenger and commercial vehicles. These innovations are helping automakers enhance road safety, reduce traffic accidents, and support the development of autonomous and semi-autonomous vehicles.

The American automotive landscape presents unique characteristics that amplify CAS adoption. The world's highest vehicle density with over 290 million registered vehicles spanning a vast and geographically diverse territory; a consumer base that increasingly researches and prioritizes safety ratings from the Insurance Institute for Highway Safety (IIHS) and NHTSA's 5-Star Safety Ratings; and an automotive industry undergoing its most significant transformation since the assembly line, with legacy manufacturers and innovative entrants competing fiercely on technological differentiation.

Regulatory momentum has reached an inflection point. The NHTSA's Automatic Emergency Braking (AEB) mandate, finalized in 2024, represents the most consequential safety regulation since seatbelts, requiring nearly all passenger vehicles and light trucks under 10,000 pounds to feature sophisticated AEB systems by 2029. This mandate establishes a non-negotiable market floor, compelling every manufacturer selling vehicles in America to integrate advanced forward collision warning and braking capabilities as standard equipment. Simultaneously, the Infrastructure Investment and Jobs Act channels unprecedented federal funding into connected vehicle infrastructure, accelerating the deployment of Vehicle-to-Everything (V2X) communication networks that will enable the next generation of cooperative collision prevention.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The competitive landscape reflects this dynamism. Traditional Tier 1 suppliers, including Robert Bosch GmbH, Continental AG, Denso Corporation, ZF Friedrichshafen AG, and Aptiv PLC, compete alongside semiconductor architects NVIDIA Corporation, Intel (Mobileye), and Qualcomm Technologies, Inc., while domestic innovators like Luminar Technologies, Ouster, Inc., and Velodyne Lidar, Inc. push the boundaries of sensing technology. Automakers themselves are increasingly vertically integrating, with Tesla's Full Self-Driving computer, General Motors' Ultifi platform, and Ford's BlueCruise representing strategic investments in proprietary safety intelligence.

Impact of the Iran conflict on the U.S. Collision Avoidance System Market

- Exposed Critical Supply Chain Vulnerabilities: The conflict highlighted the U.S. reliance on foreign sources (specifically China) for gallium, a critical material used in radar and LiDAR sensors. This will drive up component costs and accelerate efforts to reshore semiconductor supply chains.

- Accelerated Defense-to-Civilian Tech Transfer: Battlefield validation of AI-powered object detection and counter-drone systems (C-UAS) will directly accelerate the development of commercial applications, particularly for detecting small, fast-moving threats like pedestrians and cyclists.

- Increased Competition for Engineering Talent: A surge in U.S. defense spending on AI, robotics, and sensor fusion will create a war for the same limited pool of highly skilled engineers needed to develop next-generation automotive safety systems.

- Shift in National R&D Priorities: While not halting automotive progress, increased federal focus and funding on defense technologies could represent an opportunity cost, potentially slowing investment in complementary areas like smart city infrastructure and V2X deployment.

The US Collision Avoidance System Market: Key Takeaways

- Unparalleled Growth Trajectory: The U.S. market is projected to surge from USD 9.4 billion in 2026 to USD 23.8 billion by 2035, driven by a potent mix of federal mandates, high consumer acceptance, and rapid technological obsolescence of older, non-equipped vehicles.

- Mandate-Led Mass Adoption: Federal regulations, most notably the NHTSA's AEB mandate and the influence of the IIHS Top Safety Pick ratings, are the single most powerful force driving standardization across all vehicle classes, from compact sedans to heavy-duty pickup trucks.

- The Commercial Fleet Frontier: Beyond personal vehicles, the massive U.S. trucking and logistics sector represents a high-growth opportunity. Fleet operators are rapidly adopting collision avoidance systems not just for safety, but for a tangible return on investment through reduced insurance premiums, fewer accidents, and improved operational efficiency.

- AI-Powered Predictive Safety: The market is shifting from reactive to proactive safety. U.S. companies are leading the development of AI that predicts potential collisions by analyzing driver behavior, real-time traffic data, and historical accident patterns, enabling pre-emptive warnings and interventions.

- Infrastructure Integration with C-V2X: Government funding from the Infrastructure Investment and Jobs Act is accelerating the deployment of Cellular Vehicle-to-Everything (C-V2X) technology. This integration with smart city infrastructure allows vehicles to "see" beyond line-of-sight, addressing hidden threats like red-light runners or obstacles around corners.

The US Collision Avoidance System Market: Use Cases

- Highway Speed AEB: With highway fatalities a major concern, systems are now being engineered to operate effectively at high speeds, detecting stationary or slow-moving vehicles and autonomously applying brakes to mitigate the severity of high-speed rear-end collisions.

- Vulnerable Road User (VRU) Protection in Urban Canyons: In dense U.S. cities, advanced sensor fusion combines camera data with radar to detect pedestrians, cyclists, and scooter riders, providing forward collision warnings and initiating autonomous emergency braking in complex, obstacle-rich environments.

- Intersection Safety via V2X: Leveraging C-V2X technology, vehicles can communicate with traffic signals and infrastructure to alert drivers of potential red-light violators or hidden pedestrians, addressing a crash scenario that onboard sensors alone cannot easily detect.

- Lane Change Decision Aids on Multi-Lane Highways: Blind-spot monitoring and lane-keeping assist systems are evolving into more proactive lane change assistants that use surround-view cameras and radar to assess adjacent lane conditions and provide gentle steering torque to guide the vehicle away from a potential side-impact collision.

- Fleet Telematics and Geofenced Safety: Commercial fleets and logistics operators are integrating collision avoidance data with telematics platforms. This allows for geofencing automatically tightening safety parameters (e.g., lowering AEB activation speeds, increasing following distance warnings) in high-risk zones like school zones or construction areas.

The US Collision Avoidance System Market: Stats & Facts

National Highway Traffic Safety Administration (NHTSA) – United States

- 42,795 people were killed in U.S. motor vehicle crashes in 2022.

- Over 2.38 million people were injured in motor vehicle crashes in 2022.

- Approximately 94% of serious crashes are attributed to human error.

- Rear-end crashes account for nearly 29% of all crashes in the U.S.

- In 2023, NHTSA proposed making Automatic Emergency Braking (AEB) mandatory on all light vehicles.

- By 2029, all new passenger vehicles in the U.S. must include AEB under a finalized federal rule.

- Heavy vehicles (>10,000 lbs) are involved in over 400,000 police-reported crashes annually.

- Around 5,000 fatalities annually involve large trucks.

Insurance Institute for Highway Safety (IIHS) – United States

- Front crash prevention systems reduce rear-end crashes by approximately 50%.

- Vehicles equipped with AEB show a 13% reduction in pedestrian crashes.

- Lane Departure Warning reduces single-vehicle, sideswipe, and head-on crashes by 11%.

- Blind Spot Monitoring reduces lane-change crashes by 14%.

- Rear Automatic Braking reduces backing crashes by up to 78%.

- By 2023, over 90% of new passenger vehicles sold in the U.S. were equipped with standard AEB.

United Nations (UN) – Decade of Action for Road Safety

- The UN targets a 50% reduction in the US road traffic deaths and injuries by 2030.

- The first Decade of Action for Road Safety aimed to save 5 million lives.

U.S. Department of Transportation (USDOT)

- Vehicle-to-Everything (V2X) technology could address up to 80% of unimpaired crash scenarios.

- The Connected Vehicle Pilot Deployment Program includes over 10,000 equipped vehicles across test sites.

The US Collision Avoidance System Market: Market Dynamic

Driving Factors in the US Collision Avoidance System Market

Forceful Federal Mandates and NCAP Influence

The primary catalyst for the U.S. market is the NHTSA's regulatory authority. The AEB mandate for light vehicles is a game-changer, creating a guaranteed market floor. Furthermore, the New Car Assessment Program (NCAP), while not mandatory, exerts immense influence by assigning safety star ratings that directly impact consumer purchasing decisions. Automakers aggressively equip vehicles with features like lane keeping assist and collision imminent braking to achieve coveted 5-star ratings.

The "Safety Tech" Consumer Arms Race

In the U.S. market, advanced driver-assistance systems (ADAS) have become a primary marketing battleground. Features once reserved for luxury marques are now heavily promoted in mass-market vehicles. Consumer awareness, fueled by organizations like the IIHS and automotive media, is exceptionally high, leading to a willingness to pay for packages that include adaptive cruise control, surround-view cameras, and cross-traffic alerts. This consumer pull accelerates innovation and cost reduction.

Restraints in the US Collision Avoidance System Market

Affordability and the Vehicle Cost Barrier

While costs are decreasing, the sophisticated hardware required for imaging radar, high-resolution optical cameras, and powerful systems-on-a-chip (SoCs) still adds significant expense. This creates an adoption barrier for the lower-priced segments of the used car market and for entry-level new vehicles, potentially creating a two-tiered safety landscape. The economic divide in safety is becoming a growing concern for advocacy groups, as vehicles priced below USD 25,000 often feature less sophisticated, single-sensor systems (e.g., camera-only AEB) that may underperform in low-light or adverse weather conditions compared to their radar-equipped premium counterparts.

The Calibration and Repair Complexity Challenge

The high precision required for these systems introduces new challenges for the automotive service industry. Even minor fender benders can necessitate expensive recalibration of cameras and radar sensors. A shortage of trained technicians and specialized equipment for ADAS calibration can lead to improper repairs, longer downtimes, and higher insurance costs, potentially affecting long-term system reliability and consumer trust. This complexity is compounded by the fact that calibration requirements are not standardized; procedures vary wildly between a Ford, a Tesla, and a Toyota, requiring repair shops to invest in multiple, expensive OEM-specific scan tools and software subscriptions. Insurers are still grappling with how to properly account for these costs in claims adjustments, leading to disputes and delayed repairs.

Opportunities in the US Collision Avoidance System Market

The Massive Commercial Trucking Frontier

The over-the-road trucking industry, a backbone of the U.S. economy, presents a massive growth opportunity. Fleet operators are under immense pressure from insurance costs and safety regulations. Retrofitting existing fleets with aftermarket collision-avoidance systems, including side-object detection and forward-collision warning, offers a clear return on investment through accident prevention and fuel-efficiency gains from predictive cruise control. The opportunity is staggering: the American Trucking Associations estimates the industry is short 78,000 drivers, a number that could rise to 160,000 by 2031. With an acute driver shortage, protecting existing drivers and assets becomes paramount. Insurance premiums for long-haul trucks have skyrocketed, with a single at-fault accident potentially costing a fleet millions in liability and increased premiums.

AI-Powered Predictive Safety and Personalization

The next frontier is moving from reactive to predictive safety. U.S. software and AI companies are developing platforms that use cloud data, driver behavior monitoring, and real-time traffic analysis to predict and warn drivers of potential hazards seconds before they become apparent. This includes personalizing warning thresholds based on individual driver fatigue or distraction levels, monitored by in-cabin driver monitoring systems (DMS). Startups and Tier-1 suppliers are moving beyond simple object detection to create a "safety cocoon" that understands context. For example, an AI system might analyze that a driver typically brakes later at a specific off-ramp. If the driver's usual behavior deviates due to distraction, the system can provide an earlier, personalized alert. Companies like Cipia and Smart Eye are advancing DMS technology to not just detect drowsiness but to assess cognitive load, determining if a driver is overwhelmed by complex traffic and can safely engage a semi-autonomous feature.

Trends in the US Collision Avoidance System Market

Sensor Fusion and System Redundancy

The industry is rapidly moving away from relying on a single sensor type. The dominant trend is sensor fusion, where data from cameras, radar, and LiDAR are synthesized by a central AI processing unit to create a robust, redundant, and fail-safe operational model. This is critical for enabling higher levels of automation and ensuring system performance in diverse weather conditions like heavy rain or snow. This trend is best exemplified by the shift in system architecture. Older ADAS systems operated in silos: a camera module for lane keeping, a radar module for AEB. Today, automakers are adopting "centralized computing" architectures (like ZF's ProAI or NVIDIA DRIVE) where raw data from all sensors is streamed to a powerful central computer. This allows for "deep fusion," where the strengths of one sensor compensate for the weaknesses of another. For instance, if a camera is blinded by direct sunlight, the system can rely on radar for object detection and ranging.

The Rise of C-V2X and Digital Infrastructure

Cellular Vehicle-to-Everything (C-V2X) technology is gaining undeniable momentum. With USDOT funding and active pilot programs in states like Utah, Virginia, and Arizona, the integration of vehicles with smart city infrastructure is accelerating. This allows for "see-through" capabilities, alerting drivers to hazards beyond their line of sight, such as a car running a red light around a sharp curve. The momentum is shifting decisively from the older DSRC standard to C-V2X, leveraging the economies of scale of 5G cellular networks. The USDOT's Save Lives with Connectivity: V2X Deployment Plan aims for nationwide V2X adoption, with significant milestones by 2028. In Utah, UDOT's connected vehicle corridor uses C-V2X to alert drivers to snowplows, work zones, and stopped vehicles, dramatically reducing secondary accidents. In Virginia, the Virginia Tech Transportation Institute (VTTI) is using C-V2X to study how to protect pedestrians and cyclists at complex intersections by broadcasting their positions to approaching vehicles.

The US Collision Avoidance System Market: Research Scope and Analysis

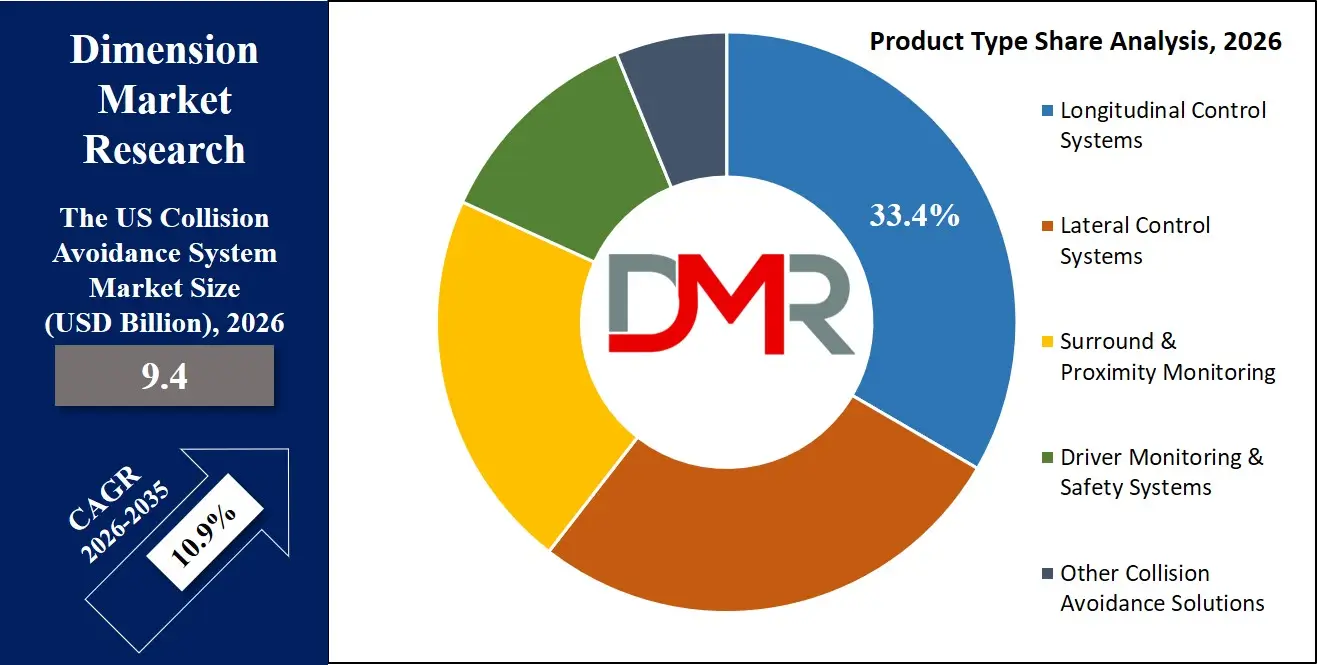

By Product Type Analysis

In the United States collision avoidance systems market, longitudinal control systems are currently projected to dominate adoption. Among these, Automatic Emergency Braking (AEB) is the most significant technology due to regulatory support from the National Highway Traffic Safety Administration (NHTSA) and its proven effectiveness in preventing the most common accident type, rear-end collisions. As regulators and safety organizations push for wider deployment, AEB is rapidly becoming standard across new vehicles.

However, the fastest-growing segment is Driver Monitoring Systems (DMS). These systems use in-cabin cameras and sensors to monitor driver attention and ensure that drivers remain alert while using semi-autonomous features. Automakers are integrating DMS as a requirement for hands-free driving technologies such as Super Cruise and BlueCruise. Beyond detecting driver distraction, next-generation DMS systems are evolving to measure physiological indicators using technologies such as remote photoplethysmography (rPPG), which can monitor heart rate and respiratory rate. These capabilities may eventually detect medical emergencies like heart attacks before they lead to accidents.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Lateral control systems, including lane keeping assist and lane centering, are also widely adopted and are increasingly standard in modern vehicles. These systems help prevent lane departure incidents and improve highway safety.

Another important product category is surround and proximity monitoring systems, which include 360-degree cameras and parking sensors. These technologies are particularly valuable for large vehicles such as SUVs and pickup trucks, where blind spots can pose risks to pedestrians, children, and pets. Advanced camera-based features such as transparent trailer views and hitch-assist technologies are gaining popularity in truck and recreational vehicle segments, improving maneuverability and towing safety.

Overall, product innovation in collision avoidance systems is increasingly focused on combining safety, driver monitoring, and convenience features.

By Technology Analysis

The technological landscape of collision avoidance systems in the United States is built primarily on sensor-based technologies, with cameras and radar forming the core sensing architecture in most modern vehicles. Cameras provide detailed visual information such as lane markings, traffic signs, and object classification, while radar offers reliable distance measurement and object detection under challenging weather conditions. Together, they form the foundation of advanced driver assistance systems (ADAS).

A key emerging trend is the development of imaging radar, an advanced radar technology capable of detecting both distance and elevation. Unlike traditional radar systems, imaging radar can distinguish between different types of obstacles, for example, identifying whether an object is a low-hanging bridge, an overhead sign, or a pedestrian. This additional spatial awareness improves the reliability of collision avoidance decisions.

The next major technological layer is integrated and intelligent systems, particularly sensor fusion platforms. Sensor fusion combines data from cameras, radar, lidar, and other sensors to produce a more accurate representation of the vehicle's environment. Leading automakers such as Tesla, General Motors, and Ford Motor Company are investing heavily in proprietary artificial intelligence and machine learning platforms to process this data in real time. The industry's competitive focus is increasingly shifting from hardware to software capabilities.

One controversial approach is Tesla's camera-only "Tesla Vision" system, which removes radar sensors and relies entirely on deep neural networks to interpret camera data. In contrast, most automakers prefer a multi-modal sensor fusion strategy, using multiple sensor types to improve redundancy and safety.

Another important technological trend is connectivity-based systems, including cellular vehicle-to-everything (C-V2X) communication. As digital road infrastructure expands, vehicles will increasingly exchange information with other vehicles and traffic systems. Additionally, over-the-air (OTA) updates allow automakers to continuously improve safety algorithms and introduce new features after vehicles are already on the road.

By Vehicle Type Analysis

In the U.S. collision avoidance systems market, passenger vehicles, including cars, SUVs, and light trucks, represent the largest segment by volume. This dominance is largely driven by regulatory mandates and consumer demand for advanced safety features. The widespread adoption of Automatic Emergency Braking and lane-keeping systems in passenger vehicles has accelerated the integration of advanced driver assistance systems across mainstream vehicle models.

However, light and heavy commercial vehicles are emerging as the fastest-growing segment for collision avoidance technology. Commercial fleets face significant financial and legal risks from accidents, including liability costs, insurance premiums, and operational downtime. As a result, fleet operators are increasingly investing in advanced safety systems to protect drivers and improve operational efficiency. Compliance with federal safety standards and improved fleet safety ratings are also key drivers of adoption.

The rapid growth of e-commerce has significantly increased the number of last-mile delivery vehicles operating in dense urban environments. Delivery vans frequently operate in congested streets and residential neighborhoods where visibility challenges and pedestrian traffic are high. To address these risks, fleets are deploying technologies such as 360-degree camera systems, cross-traffic alerts, and blind-spot monitoring systems.

Another important segment driving technological innovation is the electric vehicle (EV) market. Leading EV manufacturers such as Tesla, Rivian, and Lucid Motors are integrating advanced safety technologies directly into centralized vehicle computing architectures. Electric vehicles often feature simplified electrical systems and centralized software platforms, making them ideal platforms for sophisticated sensor suites and AI-based safety features.

Consequently, EVs are increasingly serving as innovation testbeds for next-generation collision avoidance technologies such as automated lane changes, advanced navigation assistance, and city-street autonomous driving capabilities.

By Autonomy Level Analysis

Vehicle automation levels play a crucial role in shaping the adoption of collision avoidance technologies in the United States. Most vehicles currently on the road operate at Level 1 or Level 2 automation, where driver assistance systems support the driver but do not replace human control. Level 1 systems typically include features such as adaptive cruise control or lane departure warnings, while Level 2 systems combine multiple functions such as steering and acceleration assistance.

Premium Level 2 systems are evolving into Level 2+ capabilities, where vehicles can provide hands-free highway driving under certain conditions. Examples include Super Cruise from General Motors and BlueCruise from Ford Motor Company. These systems allow drivers to remove their hands from the steering wheel on mapped highways while the vehicle maintains speed, lane position, and safe following distance. Consumers are increasingly willing to pay premium prices for these technologies because they reduce fatigue during long highway trips.

Level 3 automation, also known as conditional automation, is beginning to appear in limited vehicle models. A notable example is DRIVE PILOT, which allows the vehicle to handle certain driving tasks under specific conditions. However, widespread adoption in the U.S. remains limited due to complex regulatory frameworks and unresolved liability questions regarding responsibility in case of accidents.

Meanwhile, Level 4 automation is currently confined to experimental and pilot programs in select cities. Companies such as Waymo and Cruise are testing robo-taxi services in controlled environments like San Francisco and Phoenix. Despite ongoing development, Level 4 technology remains a long-term objective rather than a near-term mass-market reality.

By Sales Channel Analysis

In the United States collision avoidance systems market, the original equipment manufacturer (OEM) channel overwhelmingly dominates distribution. Most modern safety systems require deep integration with vehicle hardware, including electronic control units (ECUs), braking systems, steering mechanisms, and central computing platforms. Because of this complexity, these systems must typically be installed during vehicle manufacturing rather than added later.

Automakers integrate collision avoidance technologies directly into their vehicle architectures to ensure seamless functionality, safety compliance, and reliability. Additionally, liability considerations and warranty requirements make factory installation the preferred option for both manufacturers and consumers. As vehicles evolve into software-defined platforms, many safety features are embedded within the vehicle's core software and firmware. This deep integration makes it extremely difficult to replicate the same functionality through aftermarket installations.

Nevertheless, the aftermarket segment still plays an important role, particularly within the commercial vehicle sector. Fleet operators often retrofit existing trucks with advanced safety technologies to improve driver protection and reduce accident risks. Major suppliers such as Bendix Commercial Vehicle Systems and WABCO provide aftermarket safety solutions for medium- and heavy-duty vehicles.

The aftermarket also serves owners of older vehicles and classic cars who want basic safety enhancements. However, these solutions are generally simpler and less integrated compared to OEM systems. For example, systems such as Mobileye 8 Connect offer features like forward collision warnings and lane departure alerts, but typically cannot intervene in braking or steering.

For passenger vehicles, the aftermarket is largely limited to independent safety tools such as dashcams and alert-based driver assistance systems.

By End User Analysis

In the U.S. collision avoidance systems market, automotive original equipment manufacturers (OEMs) represent the primary end users of advanced safety technologies. Major vehicle manufacturers define system specifications and collaborate closely with Tier 1 technology suppliers to integrate advanced driver assistance systems into their vehicles. Suppliers such as Bosch, Continental AG, and Aptiv play a critical role in developing sensors, software platforms, and integrated safety modules.

OEM purchasing decisions are heavily influenced by regulatory requirements and industry safety benchmarks. Achieving top safety ratings from organizations such as the Insurance Institute for Highway Safety is an important competitive factor for automakers, encouraging them to adopt increasingly advanced collision avoidance technologies.

The second major end-user group consists of fleet operators, including trucking companies, delivery services, and government transportation agencies. Unlike individual consumers, fleet operators approach safety technology from a financial and operational perspective. They evaluate technologies based on total cost of ownership (TCO), accident reduction potential, insurance benefits, and long-term operational efficiency. As a result, fleets often actively invest in advanced safety packages when purchasing new vehicles or retrofit existing vehicles with safety systems.

Although the aviation and railway sectors also utilize collision avoidance technologies, their markets are significantly smaller compared with automotive applications. Aviation systems such as the Traffic Collision Avoidance System and rail technologies like Positive Train Control operate under strict regulatory frameworks and mature safety standards.

Despite their smaller market size, these industries influence automotive safety development by introducing advanced concepts such as redundancy and safety-critical software engineering practices, which are increasingly being adopted in modern automotive systems.

The US Collision Avoidance System Market Report is segmented on the basis of the following:

By Product Type

- Longitudinal Control Systems

- Adaptive Cruise Control (ACC)

- Autonomous Emergency Braking (AEB)

- Forward Collision Warning (FCW)

- Pedestrian & Cyclist Detection Systems

- Lateral Control Systems

- Lane Departure Warning System (LDWS)

- Lane Keeping Assist (LKA)

- Lane Centering Assist

- Surround & Proximity Monitoring

- Blind Spot Detection (BSD)

- Rear Cross Traffic Alert (RCTA)

- Front & Rear Parking Sensors

- 360° Surround View Camera Systems

- Automated Parking Assistance

- Driver Monitoring & Safety Systems

- Driver Monitoring Systems (DMS)

- Driver Drowsiness Detection

- Attention & Distraction Monitoring

- Other Collision Avoidance Solutions

By Technology

- Sensor-Based Systems

- Radar

- LiDAR

- Camera

- Ultrasonic

- Fusion (Multi-Sensor)

- Infrared/Thermal Imaging

- Integrated & Intelligent Systems

- Sensor Fusion (Multi-Sensor Integration)

- Artificial Intelligence & Machine Learning-Based Processing

- Connectivity-Based Systems

- V2X Communication

By Vehicle Type

- Passenger Vehicles

- Light Commercial Vehicles (LCVs)

- Heavy Commercial Vehicles (HCVs)

- Electric Vehicles

- Two-Wheelers

- Autonomous Vehicles

By Autonomy Level

- Level 0 (No Automation)

- Level 1 (Driver Assistance)

- Level 2 (Partial Automation)

- Level 3 (Conditional Automation)

- Level 4 (High Automation)

- Level 5 (Full Automation)

By Sales Channel

By End User Industry

- Automotive

- Aviation

- Marine & Shipping

- Railways

- Industrial / Warehousing & Logistics

- Other End-Use Areas

Impact of Artificial Intelligence in the US Collision Avoidance System Market

- Deep Learning for Object Classification: AI, particularly convolutional neural networks (CNNs), is used to classify thousands of objects, distinguishing between a pedestrian, a cyclist, a deer, and a piece of road debris with ever-increasing accuracy.

- Predictive Path Planning: AI algorithms analyze motion vectors and contextual cues (e.g., a child's ball rolling into the street) to predict the future trajectory of objects, enabling pre-emptive action.

- Robust Sensor Fusion: AI is the "brain" that fuses disparate data from cameras, radar, and LiDAR into a single, coherent, and reliable model of the vehicle's environment.

- Edge AI for Instantaneous Decision-Making: High-performance systems-on-chips (SoCs) from NVIDIA, Qualcomm, and Tesla perform trillions of operations per second, allowing the vehicle to make split-second braking or steering decisions without relying on the cloud.

- Fleet Learning (The "NVIDIA DRIVE" Model): Automakers use anonymized data from their entire fleet to continuously train and improve their central AI models. When one vehicle encounters a novel edge case, the learning can be uploaded and, after validation, downloaded to the entire fleet via an OTA update.

- In-Cabin Sensing & Personalization: AI analyzes driver head pose, eye gaze, and blink rate to detect drowsiness or distraction. It can then customize alert timing or intervene more aggressively, tailoring the safety response to the driver's real-time state.

The US Collision Avoidance System Market: Competitive Landscape

The U.S. collision avoidance systems market is a highly dynamic and moderately consolidated competitive landscape characterized by the presence of global Tier 1 automotive suppliers, major semiconductor and AI technology companies, specialized sensor manufacturers, and vertically integrated automakers. Leading Tier 1 suppliers such as Robert Bosch GmbH, Continental AG, Denso Corporation, ZF Friedrichshafen AG, and Aptiv PLC maintain strong market positions by supplying integrated, production-ready collision avoidance systems to major automakers, including the Detroit Big Three and other international brands operating in the United States. Alongside these suppliers, semiconductor and artificial intelligence leaders are becoming increasingly influential in shaping system capabilities. Companies such as NVIDIA Corporation with its DRIVE platform, Intel through its autonomous driving subsidiary Mobileye, and Qualcomm Technologies with its Snapdragon Ride platform provide the high-performance computing hardware and AI software frameworks that power advanced driver assistance systems and automated driving features.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

In addition, sensor specialists such as Valeo, Magna International, and Hella play a key role in developing advanced camera and radar technologies. The United States also hosts leading LiDAR innovators including Luminar Technologies, Ouster, and Velodyne Lidar, which are focused on improving sensor performance while reducing costs. At the same time, automakers like Tesla and General Motors are pursuing vertical integration strategies, developing proprietary hardware and AI platforms such as Tesla's Full Self-Driving computer and GM's Ultra Cruise system to strengthen their competitive advantage in advanced vehicle safety technologies.

Some of the prominent players in the US Collision Avoidance System Market are:

- Robert Bosch GmbH

- Continental AG

- Denso Corporation

- ZF Friedrichshafen AG

- Aptiv PLC

- NVIDIA Corporation

- Intel (Mobileye)

- Qualcomm Technologies, Inc.

- Valeo

- Magna International

- Hella

- Luminar Technologies

- Ouster, Inc.

- Velodyne Lidar, Inc.

- Tesla, Inc.

- General Motors

- Ford Motor Company

- Waymo

- Cruise

- Argo AI

- Other Key Players

Recent Developments in the US Collision Avoidance System Market

- November 2025: At the Los Angeles Auto Show, a leading U.S. EV manufacturer unveiled its new "AI Safety Engine," a generative AI model designed to simulate and learn from millions of rare crash scenarios in a virtual environment, pushing the boundaries of predictive threat modeling.

- October 2025: Aptiv PLC announced a multi-year contract with a major U.S.-based trucking fleet to equip over 10,000 Class 8 trucks with its integrated radar and camera system, specifically designed to mitigate blind-spot accidents common in port and logistics hub environments.

- September 2025: NHTSA opened a public comment period on a proposed rule to mandate automatic emergency braking (AEB) on all heavy-duty trucks over 10,000 pounds, signaling the next major wave of regulatory impact on the market.

- August 2025: The State of Utah Department of Transportation (UDOT) expanded its C-V2X corridor, now covering over 300 miles of highway, enabling real-time alerts for work zones, disabled vehicles, and approaching emergency responders to equipped vehicles.

- July 2025: Qualcomm announced its next-generation Snapdragon Ride Flex SoC will be used by a Detroit automaker to centralize processing for both ADAS (including collision avoidance) and in-vehicle infotainment on a single chip, a major step toward software-defined vehicles.

- June 2025: Luminar Technologies finalized a deal to supply its Iris+ LiDAR units to a leading global automaker for its new U.S.-built electric SUV, aiming to enable a highway autonomous driving feature that will be activated via OTA update in late 2026.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 9.4 Bn |

| Forecast Value (2035) |

USD 23.8 Bn |

| CAGR (2026–2035) |

10.9% |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors and etc. |

| Segments Covered |

By Product Type (Longitudinal Control Systems, Lateral Control Systems, Surround & Proximity Monitoring, Driver Monitoring & Safety Systems, and Other Collision Avoidance Solutions), By Technology (Sensor-Based Systems, Integrated & Intelligent Systems, Connectivity-Based Systems, and V2X Communication), By Vehicle Type (Passenger Vehicles, Light Commercial Vehicles (LCVs), Heavy Commercial Vehicles (HCVs), Electric Vehicles, Two-Wheelers, and Autonomous Vehicles), By Autonomy Level (Level 0 (No Automation), Level 1 (Driver Assistance), Level 2 (Partial Automation), Level 3 (Conditional Automation), Level 4 (High Automation), and Level 5 (Full Automation)), By Sales Channel (OEM, and Aftermarket), By End User Industry (Automotive, Aviation, Marine & Shipping, Railways, Industrial / Warehousing & Logistics, Other end-use areas) |

| Country Coverage |

The US |

| Prominent Players |

Robert Bosch GmbH, Continental AG, Denso Corporation, ZF Friedrichshafen AG, Aptiv PLC, NVIDIA Corporation, Intel (Mobileye), Qualcomm Technologies, Inc., Valeo, Magna International, Hella, Luminar Technologies, Ouster, Inc., Velodyne Lidar, Inc., Tesla, Inc., General Motors, Ford Motor Company, Waymo, Cruise, Argo AI., and Other Key Players |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users) and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days and 5 analysts working days respectively. |

Frequently Asked Questions

How big is the US Collision Avoidance System Market?

▾ The US Collision Avoidance System Market is valued at USD 9.4 billion in 2026 and is projected to reach USD 23.8 billion by the end of 2035.

What is the growth rate for the US Collision Avoidance System Market?

▾ The market is growing at a robust compound annual growth rate (CAGR) of 10.9% over the forecast period of 2026 to 2035.

What factors are driving growth in the US market?

▾ The primary drivers are stringent federal safety mandates (like the NHTSA AEB rule), high consumer demand for safety technology, intense competition among automakers, and growing investment in V2X infrastructure.

Who are the key players in the US Collision Avoidance System Market?

▾ Key players include global Tier 1 suppliers like Robert Bosch GmbH, Continental AG, Denso Corporation, ZF Friedrichshafen AG, and Aptiv PLC; tech giants and semiconductor firms like NVIDIA Corporation, Intel (Mobileye), and Qualcomm Technologies, Inc. ; and sensor innovators like Luminar Technologies and Ouster, Inc.