Market Overview

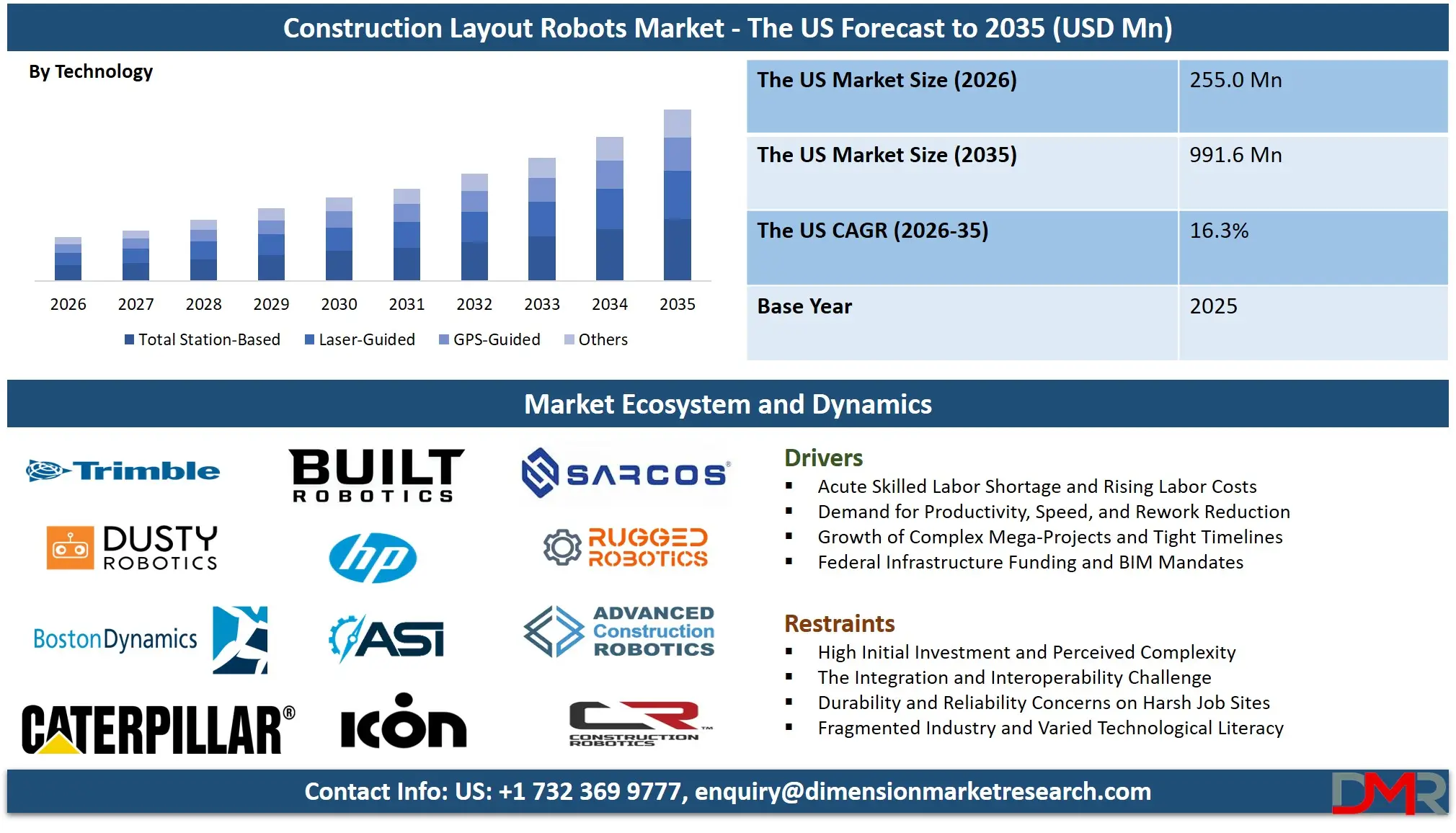

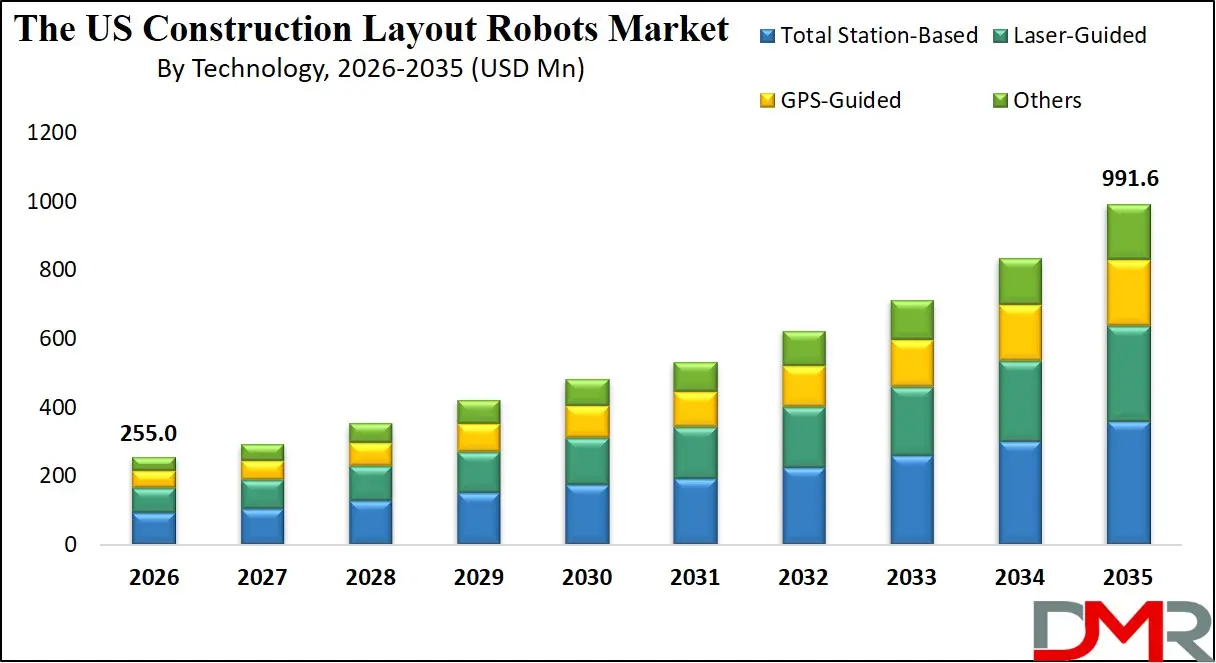

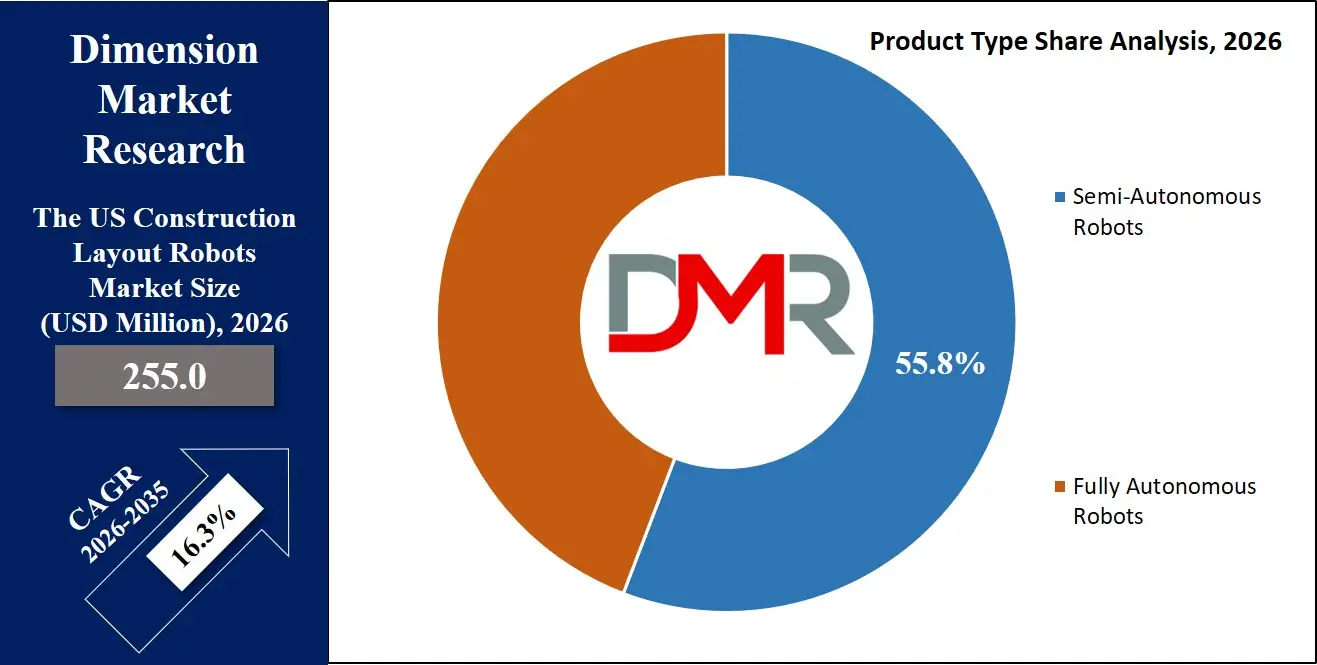

The US Construction Layout Robots Market is projected to reach USD 255.0 million in 2026 and is expected to grow at a CAGR of 16.3% from 2026 to 2035, reaching approximately USD 991.6 million by 2035.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The market growth is driven by the increasing adoption of automation to address skilled labor shortages, rising demand for precision and efficiency on job sites, and the need to accelerate project timelines across the United States. Additionally, advancements in robotic total stations (RTS), LiDAR technology, building information modeling (BIM) integration, and cloud-based data synchronization are accelerating the deployment of automated layout solutions in both commercial and infrastructure projects. These innovations are helping contractors reduce material waste, minimize costly rework, and improve overall project profitability.

The American construction landscape presents unique characteristics that amplify layout robot adoption. The nation faces a chronic shortage of skilled laborers, particularly experienced surveyors and carpenters, with over 400,000 job openings in construction monthly; a commercial construction sector racing to meet demand from mega-projects in data centers, healthcare, and renewable energy; and an industry undergoing digital transformation, with forward-thinking firms competing fiercely on technological differentiation to win bids.

Regulatory momentum has reached an inflection point. While not mandated directly, the increasing stringency of OSHA safety regulations and the growing prevalence of Davis-Bacon Act requirements for prevailing wage calculations create indirect pressure for efficiency. More significantly, the widespread adoption of BIM mandates by federal and state agencies, including the GSA's requirement for BIM on public buildings, makes digital layout tools essential. A robot can translate a BIM model directly to the jobsite floor with millimeter accuracy, a task impossible for manual methods alone. Simultaneously, the Infrastructure Investment and Jobs Act channels unprecedented federal funding into roads, bridges, and broadband, accelerating large-scale infrastructure projects that demand the speed and precision of automated layout technologies.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The competitive landscape reflects this dynamism. Specialized construction technology providers, including Topcon Corporation, Trimble Inc., Hexagon AB (Leica Geosystems), Hilti Corporation, and Dusty Robotics, compete alongside established surveying equipment manufacturers and innovative startups. The market is seeing increased participation from robotics-as-a-service (RaaS) providers, lowering the barrier to entry for smaller contractors. Furthermore, strategic partnerships between robot manufacturers and major software platforms (like Autodesk and Bentley Systems) are creating seamless BIM-to-field workflows, embedding layout robotics into the core construction process.

The US Construction Layout Robots Market: Key Takeaways

- Unparalleled Growth Trajectory: The US market is projected to surge from USD 255.0 million in 2026 to USD 991.6 million by 2035, driven by a potent mix of acute labor shortages, demand for productivity gains, and the rapid technological maturity of user-friendly robotic solutions.

- Labor-Shortage-Led Adoption: The chronic shortage of skilled labor, especially layout carpenters and surveyors, is the single most powerful force driving adoption. Robots allow a single worker to accomplish the work of a team, freeing up skilled labor for higher-value tasks.

- The Commercial Mega-Project Frontier: Beyond small-scale residential, the massive US commercial and industrial construction sectors represent a high-growth opportunity. General contractors are rapidly adopting layout robots not just for speed, but for a tangible return on investment through reduced rework, minimized material waste, and the ability to keep complex projects on tight schedules.

- BIM-to-Field Integration: The market is shifting towards seamless digital workflows. Leading US companies are perfecting the integration of robotic layout tools with BIM software, creating a "digital thread" that ensures the physical building matches the virtual model perfectly, enabling prefabrication and lean construction methodologies.

- Rise of Robotics-as-a-Service (RaaS): The high upfront cost of purchasing robotic equipment is being mitigated by the emergence of RaaS and leasing models. This allows contractors of all sizes to access the latest technology on a per-project basis, significantly accelerating market penetration.

The US Construction Layout Robots Market: Use Cases

- High-Rise Commercial Core & Shell: On large commercial projects, autonomous robots print complex layouts for core drilling, embeds, curtain wall anchors, and MEP (mechanical, electrical, plumbing) rough-ins directly onto concrete decks, saving days of manual measuring and preventing clashes.

- Data Center Precision Layout: The explosive growth of data center construction demands extreme precision for server rack cooling systems, cable trays, and raised flooring. Robots ensure millimeter accuracy across vast white space floors, critical for prefabricated component installation.

- MEP Trades Coordination: Mechanical, electrical, and plumbing contractors use robotic total stations guided by BIM models to mark thousands of hanger locations, penetrations, and equipment pads with perfect accuracy, ensuring that complex overhead MEP systems fit without field modifications.

- Complex Formwork and Rebar Placement: For intricate concrete structures like foundations, shear walls, and tilt-up panels, robots mark the exact positions for rebar, embeds, and formwork edges, drastically reducing errors that could compromise structural integrity.

- Infrastructure Staking: On highway and bridge projects, GPS-guided autonomous rovers replace manual surveying crews to stake out grading limits, pile locations, and alignment for drainage and utilities, improving safety by reducing worker exposure to traffic.

The US Construction Layout Robots Market: Stats & Facts

Bureau of Labor Statistics (BLS) – United States

- The construction industry routinely has over 400,000 job openings per month.

- The quit rate in construction remains high, indicating a mobile and unstable workforce.

- The average age of a skilled construction worker, including carpenters and surveyors, continues to rise, leading to a wave of retirements.

- Productivity growth in the construction sector has lagged behind the overall economy for decades, creating a pressing need for automation.

Associated General Contractors of America (AGC)

- Over 80% of construction firms report difficulty finding qualified hourly craft laborers.

- Many firms have increased base pay and benefits to attract workers, impacting project profitability.

- Contractors cite that adopting technology is a key strategy for doing more with less and winning new bids.

National Institute of Standards and Technology (NIST)

- Rework due to errors and omissions can account for up to 5% of total construction costs.

- Poor interoperability and data inaccuracy are leading causes of field errors.

- Improved layout accuracy directly contributes to reducing material waste, a significant cost and sustainability factor.

McKinsey Global Institute

- The construction industry has the potential for significant productivity gains through digitization and automation.

- Large, complex projects are 20% more likely to run over schedule, highlighting the need for precise planning and execution tools like layout robots.

- Automation in construction could help fill the labor gap created by retiring Baby Boomers.

US General Services Administration (GSA)

- GSA mandates the use of BIM for all major federal building projects.

- This requirement creates a need for digital tools on the jobsite that can interpret and execute the BIM model, a role perfectly suited for layout robots.

- Federal investment in infrastructure projects will require modern, efficient construction methods to stay within budget and on schedule.

The US Construction Layout Robots Market: Market Dynamic

Driving Factors in the US Construction Layout Robots Market

Acute Skilled Labor Shortage and Rising Labor Costs

The primary catalyst for the US market is the chronic and worsening shortage of skilled tradespeople. Layout is traditionally performed by experienced carpenters or surveyors, a workforce that is retiring faster than it can be replaced. This labor gap creates a powerful economic incentive for general contractors and subcontractors to adopt robotic solutions that can perform the work of 2-3 people with higher speed and 24/7 availability, directly addressing project delays and escalating labor costs.

Demand for Productivity, Speed, and Rework Reduction

In an environment of thin profit margins, the ability to reduce rework is a game-changer. Manual layout is prone to human error, leading to costly mistakes like misplaced embeds or incorrectly located MEP rough-ins. Robots, guided directly from the BIM model, ensure millimeter accuracy, eliminating these errors. This "measure twice, cut once" philosophy, executed perfectly, translates directly into faster project close-out, reduced material waste, and higher profitability, making the business case for robots compelling for forward-thinking firms.

Restraints in the US Construction Layout Robots Market

High Initial Investment and Perceived Complexity

The upfront capital expenditure for purchasing advanced robotic total stations or autonomous layout robots can be a significant barrier, especially for small to medium-sized contractors. While the ROI is clear, the initial outlay of $50,000 to $100,000+ can be daunting. Furthermore, there is a perceived complexity and a learning curve associated with adopting new digital workflows, which can create resistance among field personnel accustomed to traditional tape measure and chalk line methods. This is being mitigated by RaaS models and increasing user-friendliness.

The Integration and Interoperability Challenge

While improving, seamless integration between robotic hardware and various construction software platforms (BIM authoring tools, project management software, etc.) is not always plug-and-play. Project data often needs to be cleaned, simplified, or exported in specific formats to be usable by the robot's control system. This creates a potential bottleneck and requires a "digital champion" on site who understands both the software and the hardware. The lack of a fully standardized data exchange protocol across the industry remains a hurdle to frictionless adoption.

Opportunities in the US Construction Layout Robots Market

The Massive MEP and Prefabrication Frontier

The growth of prefabrication and modular construction presents a massive opportunity. Prefabricated components, whether for MEP racks, bathroom pods, or entire wall panels, require absolute precision to fit together on site. Layout robots are essential tools for creating the jigs and templates in the factory and for marking the exact locations for these modules on the construction site. The opportunity is staggering: as the construction industry shifts towards off-site manufacturing to solve the labor crisis, the need for precise digital layout becomes paramount, creating a symbiotic relationship with robotic automation.

AI-Powered Quality Control and Progress Tracking

The next frontier for layout robots is moving from simply marking points to becoming integrated quality control and progress tracking platforms. US software and robotics companies are developing AI that uses data from the robot's sensors to compare as-built conditions against the BIM model in real-time. For example, after a concrete pour, the robot could scan the surface and automatically flag areas that are out of tolerance before they cause problems for subsequent trades. This "scan-vs-BIM" capability transforms the robot from a simple marking tool into a comprehensive jobsite quality assurance system, offering a new value proposition beyond initial layout.

Trends in the US Construction Layout Robots Market

Sensor Fusion and Multi-Functionality

The industry is moving beyond single-purpose robots. The dominant trend is the integration of multiple technologies into a single platform. A robot might use a robotic total station for primary positioning, but also incorporate laser scanners for quality control, 360-degree cameras for documentation, and advanced sensors for autonomous navigation around a dynamic jobsite. This sensor fusion allows a single robot to perform layout, as-built verification, and progress tracking in one pass, dramatically increasing its utility and ROI.

The Rise of Cloud-Connected Workflows and Digital Twins

The integration of robotic layout tools with cloud-based construction platforms is gaining undeniable momentum. Instead of transferring files via USB stick, layout data from the BIM model is pushed directly to the robot via the cloud. The robot, in turn, uploads as-built data and progress information back to the cloud, updating the project's digital twin in near real-time. This creates a continuous feedback loop between the office and the field. This seamless connectivity, enabled by advancements in cellular and on-site mesh networks, is the foundation for the "smart jobsite," where all stakeholders have access to a single source of truth.

The US Construction Layout Robots Market: Research Scope and Analysis

By Product Type Analysis

In the United States construction layout robots market, semi-autonomous robots are currently projected to dominate adoption. Among these, robotic total stations (RTS) operated by a single surveyor or layout technician are the most significant technology due to their proven reliability, familiarity to professionals, and suitability for a wide range of tasks from foundation stakes to MEP anchor points. As project complexity and accuracy demands increase, these semi-autonomous tools are rapidly becoming standard on large commercial and industrial sites.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

However, the fastest-growing segment is fully autonomous robots. These self-driving rovers, such as those developed by Dusty Robotics, can print complex layouts directly onto floor decks without continuous human operation. They navigate the jobsite independently, allowing a single worker to oversee multiple robots or focus on other tasks while the robot works. Beyond simple marking, next-generation autonomous systems are evolving to perform integrated scan-vs-BIM functions as they move, automatically detecting and reporting deviations from the plan. These capabilities may eventually allow for automated progress payments based on verified as-built data.

Other product categories, while smaller, are also evolving. Specialized systems for specific tasks, such as robotic arms for precise placement of survey markers, represent niche but important applications. Overall, product innovation in construction layout robots is increasingly focused on combining positioning accuracy, autonomous mobility, and real-time data capture.

By Technology Analysis

The technological landscape of construction layout robots in the United States is built primarily on sensor-based positioning technologies. Total station-based systems, which use a robotic theodolite and reflector to achieve millimeter-accurate 3D positions, form the core of most high-precision layout work. They provide the reliability and accuracy required for complex commercial and industrial construction.

A key emerging trend is the advancement of laser-guided systems. While traditional laser levels are common, newer systems use rotating lasers and robotic receivers for automated grade checking and layout. More sophisticated systems, sometimes called "laser templating," can project full-scale 2D templates directly onto floors or walls, showing the exact location of every stud, outlet, and pipe in a room, vastly speeding up layout for trades.

The next major technological layer is GPS-guided systems. These are particularly dominant in infrastructure and large-site civil works. Using Real-Time Kinematic (RTK) corrections, GPS-guided robots and rovers can stake out points over vast areas quickly and accurately without needing a line of sight to a fixed instrument, making them ideal for roads, pipelines, and site grading. The industry's competitive focus is increasingly shifting from the positioning hardware alone to the software that enables seamless BIM-to-field workflows. The "others" category includes emerging technologies like indoor GPS (iGPS) and ultra-wideband (UWB) for tracking assets and personnel, which are beginning to find applications in layout verification.

By Application Analysis

In the US construction layout robots market, commercial construction represents the largest segment by value. This dominance is largely driven by the complexity and scale of projects like office towers, hospitals, and data centers. The demand for speed, precision, and clash-free MEP installation in these buildings makes robotic layout an indispensable tool for top-tier general contractors and MEP subcontractors.

However, industrial construction is emerging as the fastest-growing segment. The construction of factories, power plants (including renewable energy), and refineries involves highly complex mechanical and process piping installations that demand extreme precision. Layout robots are essential for positioning equipment foundations and pipe supports accurately. The rapid growth of on-shoring and the construction of massive battery and semiconductor "giga-factories" in the US is a key driver.

Infrastructure construction is also a significant and growing application. Road building, bridge construction, and utility projects benefit from the speed and accuracy of GPS-guided robotic layout for grading, staking, and alignment. The influx of federal funding from the Infrastructure Investment and Jobs Act is fueling this segment. Residential construction, while a large market by unit volume, currently sees lower adoption due to cost sensitivity and smaller project scales, though high-end custom home builders and large residential developers are beginning to explore the technology for foundation and framing layout to improve efficiency.

By End-User Analysis

End-users in the US construction layout robots market are diverse. Construction companies, particularly large general contractors, represent the primary end-users. They utilize robots for self-perform work, such as core and shell layout, and often mandate their use by subcontractors to ensure overall project accuracy and coordination. Their purchasing decisions are driven by the need to mitigate risk, stay on schedule, and protect profit margins.

Contractors, specifically specialty trade contractors in MEP, concrete, and drywall, are a crucial and growing end-user group. For these firms, layout robots are a direct tool for their core work. An MEP contractor, for example, can use a robot to layout thousands of hanger and equipment locations, dramatically reducing errors and the costly field modifications that eat into their profits. For them, the ROI is clear and immediate. Surveyors are established users of robotic total stations, and they are key adopters of more advanced robotic technologies for site surveying, staking, and as-built verification, serving both construction companies and civil engineering firms.

Architects are emerging as an indirect but influential end-user. While they typically don't operate the robots, their creation of the digital BIM model is the foundation for robotic workflows. The ability to see their designs translated with perfect fidelity to the physical site strengthens the architect's role and reduces the risk of misinterpretation. Other end-users include specialized concrete formwork companies and precast concrete manufacturers, who use robots to create precise forms and templates.

The US Construction Layout Robots Market Report is segmented on the basis of the following:

By Product Type

- Semi-Autonomous Robots

- Fully Autonomous Robots

By Technology

- Total Station-Based

- Laser-Guided

- GPS-Guided

- Others

By Application

- Commercial Construction

- Residential Construction

- Industrial Construction

- Infrastructure Construction

By End-User

- Construction Companies

- Contractors

- Surveyors

- Architects

- Others

Impact of Artificial Intelligence in the US Construction Layout Robots Market

- Autonomous Navigation & Obstacle Avoidance: AI enables fully autonomous robots to navigate complex, dynamic jobsites. They use sensor data to identify and avoid obstacles like workers, equipment, and debris, allowing them to work safely and efficiently without human intervention.

- Intelligent Scan-vs-BIM Analysis: AI algorithms, particularly computer vision, are used to automatically compare 3D scans of as-built conditions (captured by the robot) with the original BIM model. The AI can instantly flag deviations, potential clashes, or quality issues, providing real-time quality control.

- Predictive Path Planning for Layout: AI can analyze the project schedule and BIM model to optimize the robot's path across a floor plate, ensuring it marks all necessary points in the most efficient sequence, minimizing travel time and battery usage.

- Edge AI for On-Device Processing: High-performance computing on the robot itself (edge AI) allows for real-time sensor fusion and decision-making. The robot can adjust its positioning based on changing site conditions or re-plan its route instantly without needing a cloud connection.

- Fleet Learning for Continuous Improvement: Manufacturers can use anonymized data from their entire fleet of robots operating across the country to continuously train and improve their central AI models. If one robot encounters a challenging navigation scenario or a new type of obstacle, the learning can be uploaded and, after validation, downloaded to the entire fleet via an OTA update.

- Generative Design for Layout Optimization: In the future, AI could move beyond executing a layout to suggesting optimal layouts. For instance, based on the BIM model, an AI could propose the most efficient arrangement of MEP anchor points to minimize material use or suggest the best locations for construction joints to reduce waste.

The US Construction Layout Robots Market: Competitive Landscape

The US construction layout robots market is a dynamic and moderately consolidated competitive landscape characterized by the presence of established surveying and construction equipment giants, specialized construction robotics companies, and innovative technology startups. Leading players such as Trimble Inc., Topcon Corporation, and Hexagon AB (through its Leica Geosystems brand) maintain strong market positions by supplying high-precision robotic total stations and GPS systems, leveraging their extensive distribution networks and brand trust with surveyors and contractors. Alongside these established suppliers, specialized robotics companies are becoming increasingly influential. Firms such as Dusty Robotics, with its autonomous layout printing solution, and Hilti Corporation, with its integrated layout and measurement tools, are pioneering new, user-friendly approaches that are accelerating adoption among general contractors and trades.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

In addition, technology integration specialists play a key role in connecting robotic hardware with construction software platforms. The United States also hosts a growing ecosystem of startups focusing on niche applications, such as robotic marking for specific trades or AI-powered progress tracking software that integrates with robotic data. At the same time, major software providers like Autodesk are deepening their integration with robotic hardware providers, ensuring seamless data flow from design to field, which is critical for widespread adoption.

Some of the prominent players in the US Construction Layout Robots Market are:

- Trimble Inc.

- Dusty Robotics

- HP Inc.

- Built Robotics

- Advanced Construction Robotics

- Rugged Robotics

- Caterpillar Inc.

- Boston Dynamics

- Autonomous Solutions Inc.

- Construction Robotics

- Canvas

- ICON Technology, Inc.

- Sarcos Technology and Robotics Corporation

- Ekso Bionics Holdings, Inc.

- Iron Ox

- ROBOT‑Rx

- Asylon Robotics

- Smartvid.io

- Field AI

- Vicarious AI

- Other Key Players

Recent Developments in the US Construction Layout Robots Market

- March 2026: ICON Technology, Inc. announced the commercial rollout of its Titan robotic 3D-printing construction system, enabling builders and developers to purchase and deploy large-scale robotic printers for multi-story construction projects, aimed at reducing costs and addressing housing shortages through automated building technologies.

- January 2026: Caterpillar Inc. unveiled its next generation of autonomous construction technologies, introducing intelligent machines and automation capabilities designed to improve productivity, safety, and operational efficiency across large-scale construction projects.

- November 2025: Trimble Inc. announced several digital construction workflow innovations during the Trimble Dimensions 2025 conference, including enhanced data-sharing and AI-enabled collaboration tools aimed at improving jobsite coordination and layout accuracy.

- September 2025: Dusty Robotics continued expanding industry adoption of its FieldPrinter robotic layout system, which transfers BIM design models directly onto jobsite floors, enabling contractors to automate layout tasks and reduce manual measurement errors.

- August 2025: HP Inc. expanded industry adoption of its SitePrint robotic layout solution, which prints digital building layouts directly onto construction floors, helping contractors automate layout processes and reduce rework and delays in large projects.

- June 2025: Boston Dynamics continued advancing industrial robotics deployment, highlighting its mobile robot Spot, which is capable of navigating complex environments such as construction sites to collect site data and perform inspection tasks autonomously.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 255.0 Mn |

| Forecast Value (2035) |

USD 991.6 Mn |

| CAGR (2026–2035) |

16.3% |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors and etc. |

| Segments Covered |

By Product Type (Semi-Autonomous Robots and Fully Autonomous Robots), By Technology (Total Station-Based, Laser-Guided, GPS-Guided and Others), By Application (Commercial Construction, Residential Construction, Industrial Construction and Infrastructure Construction), By End-User (Construction Companies, Contractors, Surveyors, Architects and Others) |

| Country Coverage |

The US |

| Prominent Players |

Trimble Inc., Dusty Robotics, HP Inc., Built Robotics, Advanced Construction Robotics, Rugged Robotics, Caterpillar Inc., Boston Dynamics, Autonomous Solutions Inc., Construction Robotics, Canvas, ICON Technology, Inc., Sarcos Technology and Robotics Corporation, Ekso Bionics Holdings, Inc., Iron Ox, ROBOT‑Rx, Asylon Robotics, Smartvid.io, Field AI, and Vicarious AI, and Other Key Players |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users) and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days and 5 analysts working days respectively. |

Frequently Asked Questions

How big is the US Construction Layout Robots Market?

▾ The US Construction Layout Robots Market is valued at USD 255.0 million in 2026 and is projected to reach USD 991.6 million by the end of 2035.

What is the growth rate for the US Construction Layout Robots Market?

▾ The market is growing at a robust compound annual growth rate (CAGR) of 16.3% over the forecast period of 2026 to 2035.

Who are the key players in the US Construction Layout Robots Market?

▾ Some of the major key players in the US Construction Layout Robots Market are Dusty Robotics, HP Inc., Built Robotics, Advanced Construction Robotics and Rugged Robotics and many others.