What is the Cruciate Ligament Diagnosis and Treatment Market Size?

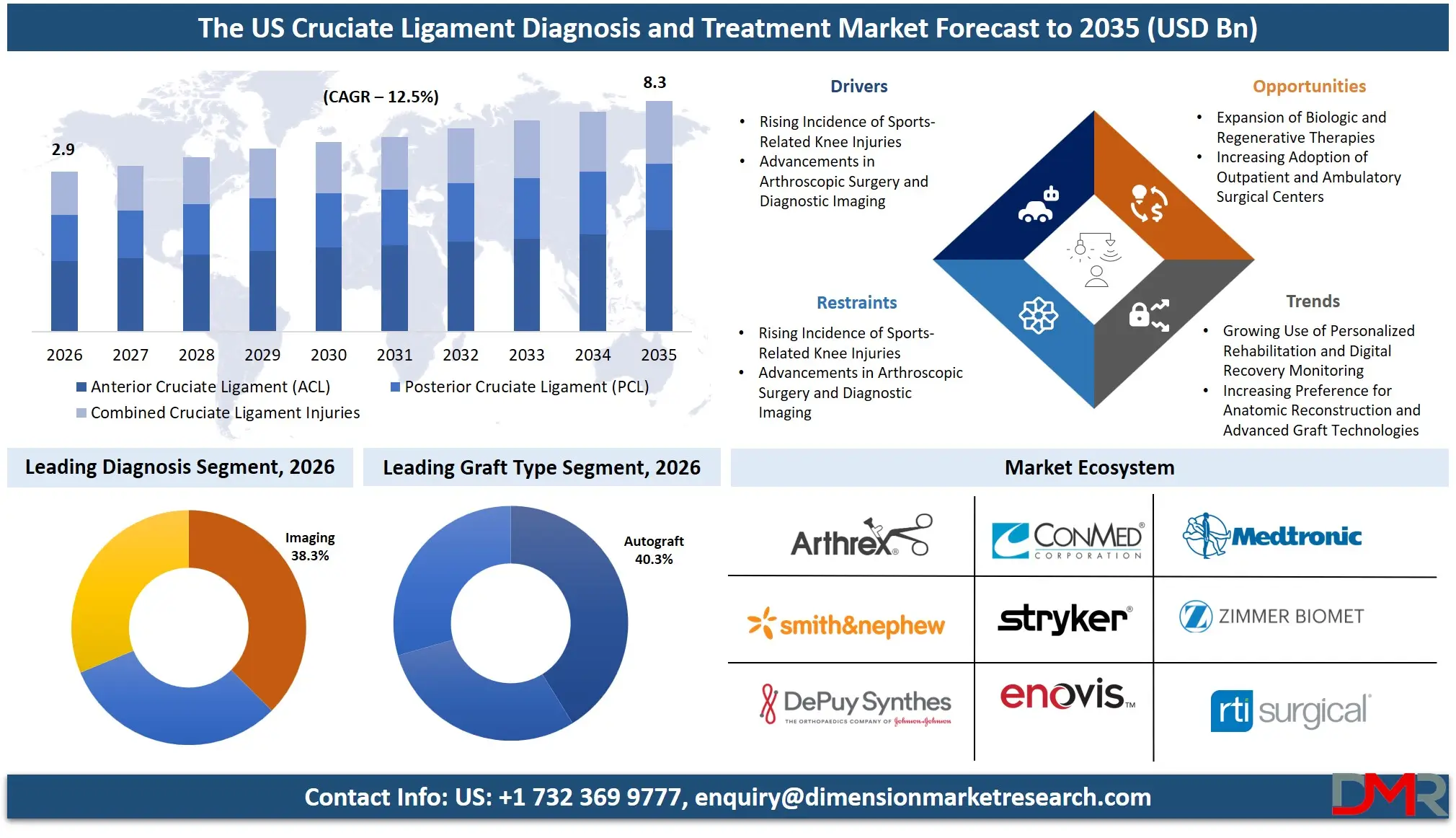

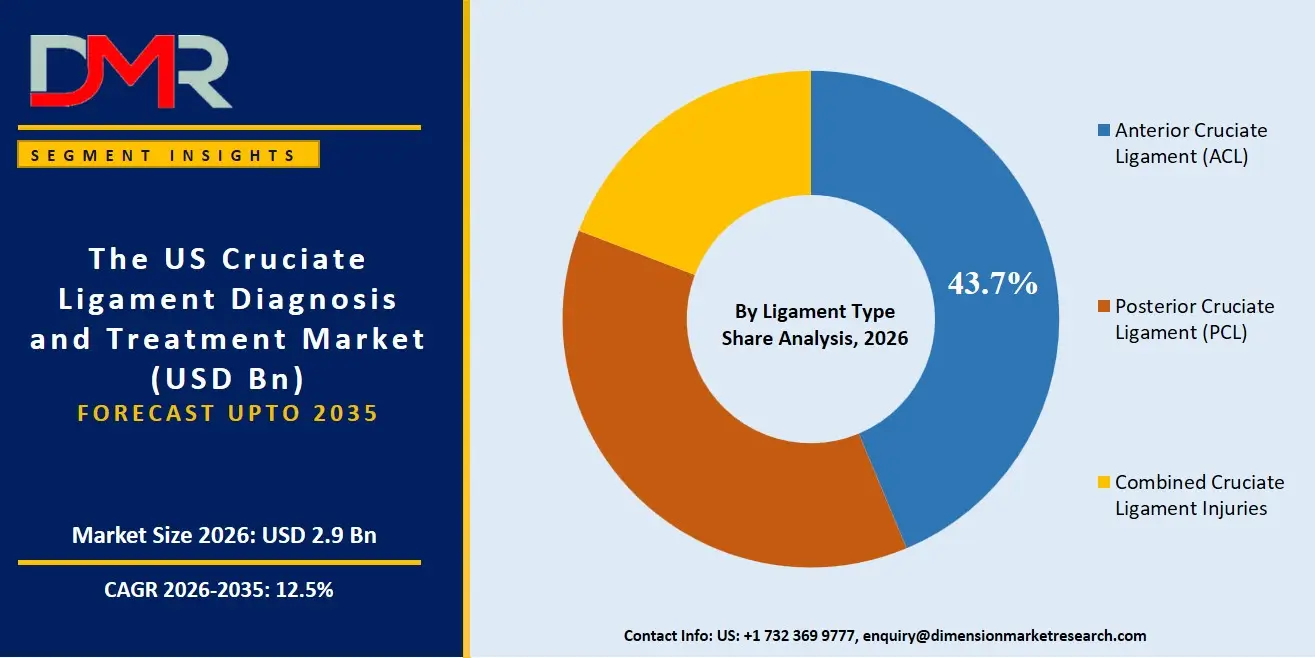

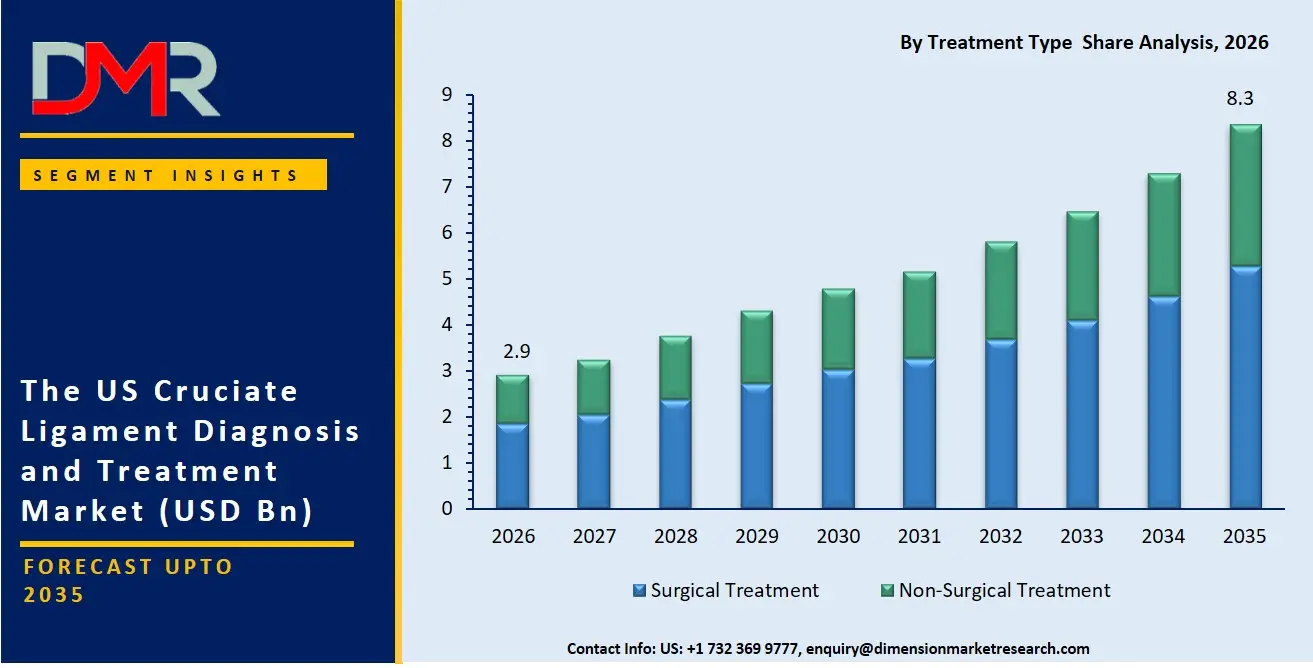

The US Cruciate Ligament Diagnosis and Treatment Market is expected to reach a value of USD 2.9 billion in 2026, and it is further anticipated to reach USD 8.3 billion by 2035, growing at a CAGR of 12.5% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The cruciate ligament diagnosis and treatment market in the US has experienced robust growth, underpinned by high sports participation rates and a strong focus on musculoskeletal health. The market encompasses the diagnosis and management of anterior, posterior, and combined ligament injuries through a range of surgical and non-surgical interventions. A rise in demand for prompt and effective care among recreational and professional athletes, coupled with an aging population keen to maintain an active lifestyle, has accelerated innovation in this space. Orthopedic surgeons, sports medicine centers, and device manufacturers are the key drivers, with arthroscopic reconstruction and biologic augmentation therapies continuing to gain prominence due to their ability to restore native knee kinematics.

Key Takeaways

- Market Size & Forecast: Based on forecasts, the size of the market for the US cruciate ligament diagnosis and treatment will experience substantial growth, attaining a value of USD 2.9 billion by 2026 and expanding dramatically to USD 8.3 billion by 2035, driven by two crucial factors: the widespread adoption of advanced graft technologies and a growing preference for early surgical intervention in high-demand patients.

- Growth Rate & Outlook: It is predicted that the market will register a CAGR of 12.5%, which will be attributed to important growth factors such as a critical mass of clinical evidence supporting anatomic reconstruction techniques and an increased need to treat multi-ligament knee injuries resulting from high-velocity trauma.

- Primary Growth Drivers: Important growth factors will include the rising incidence of sports-related knee injuries, heightened awareness regarding long-term knee stability, and the integration of robotic-assisted platforms that enhance surgical precision and reproducibility.

- Key Market Trends: The market trends are mainly related to the expansion of outpatient arthroscopic procedures, the increased use of autografts augmented with orthobiologics like PRP to accelerate healing, and a strategic shift towards value-based care models that prioritize functional outcomes and lower revision rates.

- By Ligament Type Analysis: The cruciate ligament diagnosis and treatment market in the US is driven by anterior cruciate ligament (ACL) injuries, as they are the most frequently injured knee ligament, particularly among athletes in pivoting sports. However, posterior cruciate ligament (PCL) and combined injury segments are expanding with improved diagnostic accuracy for high-energy trauma.

- By Treatment Type Analysis: The US cruciate ligament diagnosis and treatment market is projected to be dominated by surgical treatment, specifically ACL reconstruction, as it offers the gold standard for restoring rotational stability and facilitating a return to pre-injury activity levels.

What is the Cruciate Ligament Diagnosis and Treatment?

Cruciate ligament diagnosis and treatment refers to the specialized field of orthopedic medicine focused on identifying and managing injuries to the anterior and posterior cruciate ligaments, the central stabilizing structures of the knee. Unlike conservative management alone, comprehensive treatment strategies are tailored to an individual's laxity grade, activity level, and functional demands. This is achieved through a multi-modal approach: diagnostic evaluation involves high-resolution imaging and precise manual tests, while treatment spans from structured rehabilitation protocols to advanced surgical interventions using biological or synthetic grafts. Considering the drive toward personalized medicine and faster recovery in the US, treatment plans increasingly incorporate prehabilitation, minimally invasive robotic-assisted surgery, and biologic augmentation.

Use Cases

- Primary ACL Reconstruction in Athletes: A sports medicine center uses an arthroscopically performed bone-patellar tendon-bone autograft to reconstruct the ACL of a collegiate football player, aiming to provide a durable, rigid fixation that allows for an aggressive rehabilitation timeline and a safe return to sport.

- Treatment of Multi-Ligament Knee Injuries: A Level I trauma center employs a combined arthroscopic and open approach for a patient with a knee dislocation involving both cruciate ligaments, using allograft tissue to reconstruct multiple ligaments in a single, complex surgery to restore limb viability and function.

- Pediatric ACL Management: A pediatric orthopedic hospital uses a physeal-sparing surgical technique with a hamstring autograft to treat a complete ACL tear in a 13-year-old athlete, focusing on stabilizing the knee while meticulously safeguarding the growth plates to prevent future angular deformities.

- Non-Surgical Augmentation for Partial Tears: An outpatient rehabilitation center applies a series of PRP injections under ultrasound guidance, followed by an intensive course of neuromuscular re-education, for a middle-aged recreational skier with a Grade II proximal ACL tear, promoting biologic healing without surgical intervention.

How AI is Transforming the Cruciate Ligament Diagnosis and Treatment Market?

The impact of AI on the US cruciate ligament diagnosis and treatment market covers accelerating the accuracy of image interpretation, predicting individual patient risk, and optimizing surgical planning. Speaking of diagnosis, AI-driven algorithms are helpful for parsing MRI sequences to automatically detect and grade ligament fiber disruption and concomitant meniscal or chondral pathology, reducing diagnostic oversights. AI-based preoperative analytics enable the prediction of graft failure risk and the customization of femoral and tibial tunnel placement based on patient-specific anatomy.

Furthermore, the role of AI in intraoperative and post-operative care is becoming significant. Robotic-assisted surgical systems use machine learning to provide real-time haptic feedback and execute precise bone cuts within a predefined virtual surgical field. AI-driven wearable sensors and smartphone applications analyze movement data during rehabilitation, providing surgeons and physical therapists with objective metrics on kinematic symmetry and warning of harmful deviations that could risk re-injury, thereby personalizing recovery protocols.

Market Dynamics

Key Drivers in The US Cruciate Ligament Diagnosis and Treatment Market

Rising Incidence of Sports-Related Knee Injuries

The increasing participation of Americans in organized sports, fitness programs, and recreational activities has significantly raised the incidence of anterior and posterior cruciate ligament injuries. High-impact sports such as football, basketball, soccer, skiing, and wrestling frequently result in ligament tears requiring prompt diagnosis and treatment. Growing awareness regarding early intervention, coupled with improved access to orthopedic specialists and sports medicine centers, has accelerated demand for advanced imaging, arthroscopic surgery, and rehabilitation services. Additionally, expanding youth and collegiate sports participation continues to generate a steady patient pool, strengthening demand for comprehensive cruciate ligament diagnosis and treatment across the United States.

Advancements in Arthroscopic Surgery and Diagnostic Imaging

Continuous technological innovations in magnetic resonance imaging (MRI), arthroscopic equipment, fixation devices, and biologic graft technologies are significantly improving treatment outcomes for cruciate ligament injuries. High-resolution imaging enables earlier and more accurate diagnosis, while minimally invasive arthroscopic procedures reduce complications, shorten hospital stays, and accelerate patient recovery. Enhanced surgical precision, customized rehabilitation protocols, and improved implant materials have increased physician confidence and patient acceptance of surgical interventions. The widespread availability of technologically advanced orthopedic centers and increasing investments in sports medicine infrastructure continue driving procedural volumes and supporting sustained market growth throughout the United States.

Restraints in The US Cruciate Ligament Diagnosis and Treatment Market

High Treatment and Rehabilitation Costs

Cruciate ligament diagnosis and treatment involve substantial healthcare expenditures, including diagnostic imaging, orthopedic consultations, surgical reconstruction, implants, anesthesia, hospital services, postoperative rehabilitation, and follow-up care. Advanced arthroscopic procedures and biologic grafts further increase overall treatment costs. Although insurance covers many procedures, patients often face deductibles, copayments, and rehabilitation expenses that may delay treatment decisions. Long rehabilitation periods also contribute to indirect costs through lost productivity and extended recovery time. These financial burdens may limit treatment accessibility for uninsured or underinsured individuals, restricting overall market expansion despite increasing injury incidence.

Risk of Surgical Complications and Graft Failure

Despite significant improvements in surgical techniques, cruciate ligament reconstruction remains associated with potential complications including infection, graft failure, joint stiffness, persistent instability, thromboembolic events, and revision surgery. Younger athletes returning to sports prematurely may experience reinjury, while older patients often present with slower recovery and reduced functional outcomes. Variability in rehabilitation adherence also influences long-term success rates. Concerns regarding repeat surgeries, prolonged recovery, and uncertain clinical outcomes may encourage some patients and physicians to initially pursue conservative treatment options. These challenges continue to limit procedural growth within certain patient populations across the United States.

Growth Opportunities in The US Cruciate Ligament Diagnosis and Treatment Market

Expansion of Biologic and Regenerative Therapies

The growing adoption of regenerative medicine offers significant opportunities within the U.S. cruciate ligament treatment market. Platelet-rich plasma (PRP), stem cell therapies, biologic scaffolds, and tissue engineering technologies are increasingly being investigated to enhance ligament healing, reduce recovery time, and improve postoperative outcomes. Continuous clinical research and favorable technological advancements may expand the use of biologic therapies alongside conventional reconstruction procedures. As physicians seek personalized treatment approaches that improve functional recovery and reduce revision rates, regenerative solutions are expected to create new revenue opportunities for healthcare providers, orthopedic device manufacturers, and sports medicine specialists.

Increasing Adoption of Outpatient and Ambulatory Surgical Centers

Advancements in minimally invasive arthroscopic techniques have enabled more cruciate ligament procedures to be safely performed in ambulatory surgical centers (ASCs). These facilities offer reduced procedural costs, shorter patient stays, faster scheduling, and improved operational efficiency compared with traditional hospitals. Increasing payer preference for cost-effective outpatient care and growing patient demand for convenient treatment settings are accelerating ASC utilization. Investments in advanced orthopedic equipment and specialized surgical teams further strengthen their competitive position. This ongoing transition toward outpatient care presents substantial opportunities for providers delivering efficient, high-quality cruciate ligament diagnosis and treatment services.

Trends in The US Cruciate Ligament Diagnosis and Treatment Market

Growing Use of Personalized Rehabilitation and Digital Recovery Monitoring

Healthcare providers are increasingly adopting personalized rehabilitation programs supported by wearable sensors, mobile health applications, tele-rehabilitation platforms, and artificial intelligence-driven performance monitoring. These technologies enable clinicians to track patient progress remotely, optimize recovery protocols, and identify potential complications earlier. Customized rehabilitation based on patient age, activity level, and surgical outcomes improves functional recovery while reducing reinjury risks. Digital monitoring also enhances patient engagement and adherence to therapy programs. The integration of technology into postoperative care is becoming a defining trend that supports better long-term outcomes and greater healthcare efficiency.

Increasing Preference for Anatomic Reconstruction and Advanced Graft Technologies

Orthopedic surgeons are increasingly adopting anatomic ligament reconstruction techniques that more accurately restore native knee biomechanics and improve long-term joint stability. Simultaneously, advances in graft fixation devices, bioabsorbable implants, quadriceps tendon grafts, and biologic augmentation technologies continue improving surgical outcomes. Growing clinical evidence supporting individualized graft selection based on patient characteristics is influencing treatment strategies across sports medicine centers. Surgeons are also utilizing advanced navigation systems and precision-guided instrumentation to enhance procedural accuracy. These innovations continue shaping modern cruciate ligament reconstruction practices and strengthening overall treatment success in the United States.

Research Scope and Analysis

The US Cruciate Ligament Diagnosis and Treatment Market is segmented by Ligament Type, Diagnosis, Injury Severity, Treatment Type, Graft Type, Procedure Type, Patient Type, Payer Type, and End User. The market encompasses comprehensive diagnostic, surgical, and rehabilitation solutions, supporting effective management of cruciate ligament injuries through advanced imaging, minimally invasive procedures, specialized grafts, and multidisciplinary orthopedic care.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Ligament Type Analysis

Anterior Cruciate Ligament (ACL) injuries is projected to dominate the U.S. Cruciate Ligament Diagnosis and Treatment Market because they represent the most frequently injured cruciate ligament across sports and recreational activities. ACL tears are highly prevalent among athletes participating in football, soccer, basketball, skiing, and gymnastics, driving substantial demand for diagnostic imaging, surgical reconstruction, and rehabilitation services. Growing awareness of early intervention, expanding participation in competitive sports, and advances in minimally invasive surgical techniques further support market leadership. Additionally, high revision rates and long-term rehabilitation requirements generate recurring demand for diagnosis, treatment, follow-up care, and physical therapy, reinforcing ACL's dominant market position.

By Diagnosis Analysis

Imaging is expected to dominate the diagnosis segment because accurate visualization of ligament injuries is essential for confirming tear severity and planning appropriate treatment. Magnetic Resonance Imaging (MRI) serves as the clinical gold standard for evaluating ACL, PCL, meniscal injuries, cartilage damage, and associated soft tissue abnormalities. Physicians routinely utilize imaging before determining surgical or conservative treatment approaches. Continuous improvements in MRI resolution, faster scanning protocols, and wider accessibility have increased diagnostic accuracy and efficiency. Imaging also reduces unnecessary invasive procedures while supporting postoperative assessment and rehabilitation monitoring, making it the most utilized diagnostic approach across hospitals, orthopedic clinics, and sports medicine centers.

By Injury Severity Analysis

Grade III injuries is projected to account for the largest market share because complete ligament ruptures usually require comprehensive diagnostic evaluation, surgical reconstruction, prolonged rehabilitation, and continuous follow-up care. These severe injuries are particularly common among competitive athletes and active individuals experiencing high-impact trauma or twisting movements. Complete tears significantly impair knee stability, increasing the likelihood of surgery rather than conservative management. Higher healthcare expenditures associated with advanced imaging, graft implantation, arthroscopic procedures, postoperative rehabilitation, and return-to-sport assessments contribute substantially to market revenue. Consequently, Grade III injuries generate the greatest demand for cruciate ligament diagnosis and treatment services across the United States.

By Treatment Type Analysis

Surgical Treatment is anticipated to dominate the market because complete ACL and many complex PCL injuries generally require reconstruction to restore knee stability and functional performance. Arthroscopic ligament reconstruction has become the preferred standard of care due to favorable clinical outcomes, minimally invasive techniques, shorter hospital stays, and faster recovery.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Increasing sports participation, improved surgical technologies, advanced fixation devices, and enhanced rehabilitation protocols continue driving procedural volumes. Additionally, younger and physically active patients increasingly choose surgery to return to pre-injury activity levels. High procedural costs, implant utilization, and postoperative rehabilitation collectively position surgical treatment as the largest revenue-generating segment within the U.S. market.

By Graft Type Analysis

Autografts dominate graft selection is poised to dominate because they demonstrate superior biological incorporation, lower graft rejection risk, and excellent long-term clinical outcomes compared with alternative graft options. Hamstring tendon, patellar tendon, and quadriceps tendon autografts are widely used in ACL reconstruction, particularly among young, active, and competitive athletes. Orthopedic surgeons often prefer autografts because they provide greater graft durability, lower infection rates, and reduced failure risk. Clinical guidelines also support autograft use for primary ligament reconstruction in many patient populations. Strong physician preference, extensive clinical evidence, and favorable functional outcomes continue making autografts the leading graft choice throughout the United States.

By Procedure Type Analysis

Arthroscopic Surgery is projected to represents the dominant procedure because it offers minimally invasive treatment with reduced postoperative pain, smaller incisions, lower infection risk, and quicker functional recovery than conventional open surgery. Most ACL and PCL reconstructions in the United States are performed arthroscopically using advanced visualization systems and specialized surgical instruments. Continuous technological innovations, including improved fixation devices and navigation systems, have enhanced procedural precision and patient outcomes. Arthroscopy also shortens hospitalization and accelerates rehabilitation, enabling patients to return to daily activities and sports more rapidly. These clinical advantages have established arthroscopic surgery as the preferred treatment approach nationwide.

By Patient Type Analysis

Recreational Athletes is poised to constitute the largest patient segment because millions of Americans participate regularly in organized sports, fitness activities, running, cycling, skiing, and recreational competitions. These individuals experience frequent knee injuries involving twisting, pivoting, and sudden directional changes that commonly result in ACL tears. Compared with professional athletes, recreational participants represent a substantially larger population requiring diagnosis, imaging, surgery, and rehabilitation. Growing health awareness and increasing participation in amateur sports continue expanding this patient pool. Their consistent demand for effective treatment, rehabilitation, and return-to-activity programs positions recreational athletes as the dominant patient category in the U.S. market.

By Payer Type Analysis

Private Insurance is expected to dominate reimbursement because most cruciate ligament injuries occur among working-age adults and younger individuals covered through employer-sponsored or commercial health insurance plans. These policies generally provide comprehensive coverage for diagnostic imaging, orthopedic consultations, arthroscopic reconstruction, hospital services, rehabilitation, and postoperative physical therapy. Broad insurance coverage improves patient access to timely diagnosis and advanced surgical interventions while supporting higher procedural volumes. Compared with public healthcare programs, commercially insured patients are more likely to undergo elective ligament reconstruction following sports-related injuries. Consequently, private insurance accounts for the largest share of healthcare expenditures within this market.

By End User Analysis

Hospitals are poised to dominate the end-user segment because they possess comprehensive orthopedic departments, advanced diagnostic imaging capabilities, specialized surgical infrastructure, and multidisciplinary rehabilitation services required for cruciate ligament management. Most complex ligament reconstructions and emergency trauma cases are treated within hospital settings where orthopedic surgeons, radiologists, anesthesiologists, and rehabilitation specialists collaborate to deliver integrated care. Hospitals also maintain access to advanced arthroscopic equipment, inpatient facilities, and postoperative monitoring capabilities unavailable in many smaller centers. Strong referral networks, higher patient volumes, and the ability to manage complex or revision surgeries continue reinforcing hospitals as the leading providers of cruciate ligament diagnosis and treatment services

The US Cruciate Ligament Diagnosis and Treatment Market Report is segmented on the basis of the following:

By Ligament Type

- Anterior Cruciate Ligament (ACL)

- Posterior Cruciate Ligament (PCL)

- Combined Cruciate Ligament Injuries

By Diagnosis

- Imaging

- Magnetic Resonance Imaging (MRI)

- X-ray

- Computed Tomography (CT)

- Ultrasound

- Physical Examination

- Arthroscopy

By Injury Severity

- Grade I (Mild Sprain)

- Grade II (Partial Tear)

- Grade III (Complete Tear)

By Treatment Type

- Surgical Treatment

- ACL Reconstruction

- PCL Reconstruction

- Multi-Ligament Reconstruction

- Revision Ligament Surgery

- Non-Surgical Treatment

- Physical Therapy & Rehabilitation

- Bracing

- Pain Management & Medication

- Platelet-Rich Plasma (PRP) Therapy

By Graft Type

- Autograft

- Patellar Tendon

- Hamstring Tendon

- Quadriceps Tendon

- Allograft

- Synthetic Graft

By Procedure Type

- Arthroscopic Surgery

- Open Surgery

- Robotic-Assisted Surgery

By Patient Type

- Recreational Athletes

- Professional Athletes

- General Population

- Pediatric Patients

- Geriatric Patients

By Payer Type

- Private Insurance

- Medicare

- Medicaid

- Self-Pay

By End User

- Hospitals

- Orthopedic Clinics

- Ambulatory Surgical Centers (ASCs)

- Sports Medicine Centers

- Rehabilitation Centers

Competitive Landscape

The nature of competition in the US cruciate ligament diagnosis and treatment market has become very dynamic, given the diverse range of multinational orthopedic conglomerates, specialized sports medicine device firms, and a vast network of orthopedic practices and therapy providers. Strategic alliances with professional sports leagues and major academic medical centers would be crucial for the company, as they help gain clinical validation for novel implants and act as key opinion leader hubs for surgical education. The trend of vertical consolidation is growing at a rapid pace, as device manufacturers are acquiring digital health platforms to offer integrated care pathways that bundle implant sales with rehabilitation monitoring tools. In this environment, differentiation is based less on the basic interference screw and more on comprehensive procedural solutions, including robotic interfaces, personalized 3D-printed instrumentation, and smart bracing.

Some of the prominent players in The US Cruciate Ligament Diagnosis and Treatment Market are:

- Arthrex, Inc.

- Smith+Nephew plc

- Stryker Corporation

- Johnson & Johnson MedTech (DePuy Synthes)

- Zimmer Biomet Holdings, Inc.

- CONMED Corporation

- Medtronic plc

- Enovis Corporation

- RTI Surgical Holdings, Inc.

- Parcus Medical, LLC

- LifeNet Health

- AlloSource

- Organogenesis Holdings Inc.

- Vericel Corporation

- Breg, Inc.

- Össur

- DJO, LLC (now part of Enovis)

- Xiros Ltd.

- Acumed LLC

- Corin Group

- Other Key Players

Recent Developments

- February 2026: Arthrex expanded its sports medicine portfolio in the U.S. with next-generation ACL and PCL reconstruction instrumentation designed to improve graft fixation, surgical precision, and procedural efficiency during arthroscopic ligament repair.

- November 2025: Smith+Nephew introduced enhanced digital planning and arthroscopic visualization technologies for knee ligament reconstruction, enabling orthopedic surgeons to improve intraoperative accuracy and patient-specific treatment planning.

- August 2025: Zimmer Biomet strengthened its knee preservation and sports medicine offerings by expanding solutions for ACL reconstruction, including advanced fixation devices and soft-tissue repair technologies aimed at improving clinical outcomes and recovery.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 2.9 Bn |

| Forecast Value (2035) |

USD 8.3 Bn |

| CAGR (2026–2035) |

12.5% |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Ligament Type, By Diagnosis, By Injury Severity, By Treatment Type, By Graft Type, By Procedure Type, By Patient Type, By Payer Type, By End User |

| Country Coverage |

The US |

Frequently Asked Questions

How big is the US Cruciate Ligament Diagnosis and Treatment Market?

▾ The US Cruciate Ligament Diagnosis and Treatment market is poised to be valued at USD 2.9 billion in 2026 and is projected to reach USD 8.3 billion by 2035, driven by the universal need for mechanical knee stability in a highly active, sports-focused society.

What is the CAGR of the US Cruciate Ligament Diagnosis and Treatment Market from 2026 to 2035?

▾ The market is expected to grow at a CAGR of 12.5% from 2026 to 2035, reflecting the accelerating adoption of minimally invasive surgical techniques, biologic augmentation, and the migration of procedures to high-efficiency Ambulatory Surgical Centers.

What factors are driving the growth of the US Cruciate Ligament Diagnosis and Treatment Market?

▾ Key drivers include the persistently high incidence of ACL tears in youth sports, the expanding demographic of active older adults with complex knee injuries, and the integration of enabling technologies like robotic surgery that attract patients seeking superior outcomes.

What are the major trends in the US Cruciate Ligament Diagnosis and Treatment Market?

▾ Major trends include the development of next-generation autografts like the quadriceps tendon, the shift toward all-arthroscopic, outpatient “all-inside” reconstruction, and a strong focus on value-based care models driven by validated patient-reported functional outcome measures.

Who are the key players in the US Cruciate Ligament Diagnosis and Treatment Market?

▾ Key players in the US Cruciate Ligament Diagnosis and Treatment Market include Arthrex, Stryker, Smith+Nephew, DePuy Synthes, and Zimmer Biomet, driving innovation through implant design, robotic platforms, surgeon training programs, and commercialization activities.

How is the US Cruciate Ligament Diagnosis and Treatment Market segmented?

▾ The market is segmented by Ligament Type, Diagnosis, Injury Severity, Treatment Type, Graft Type, Procedure Type, Patient Type, Payer Type, and End User.