Market Overview

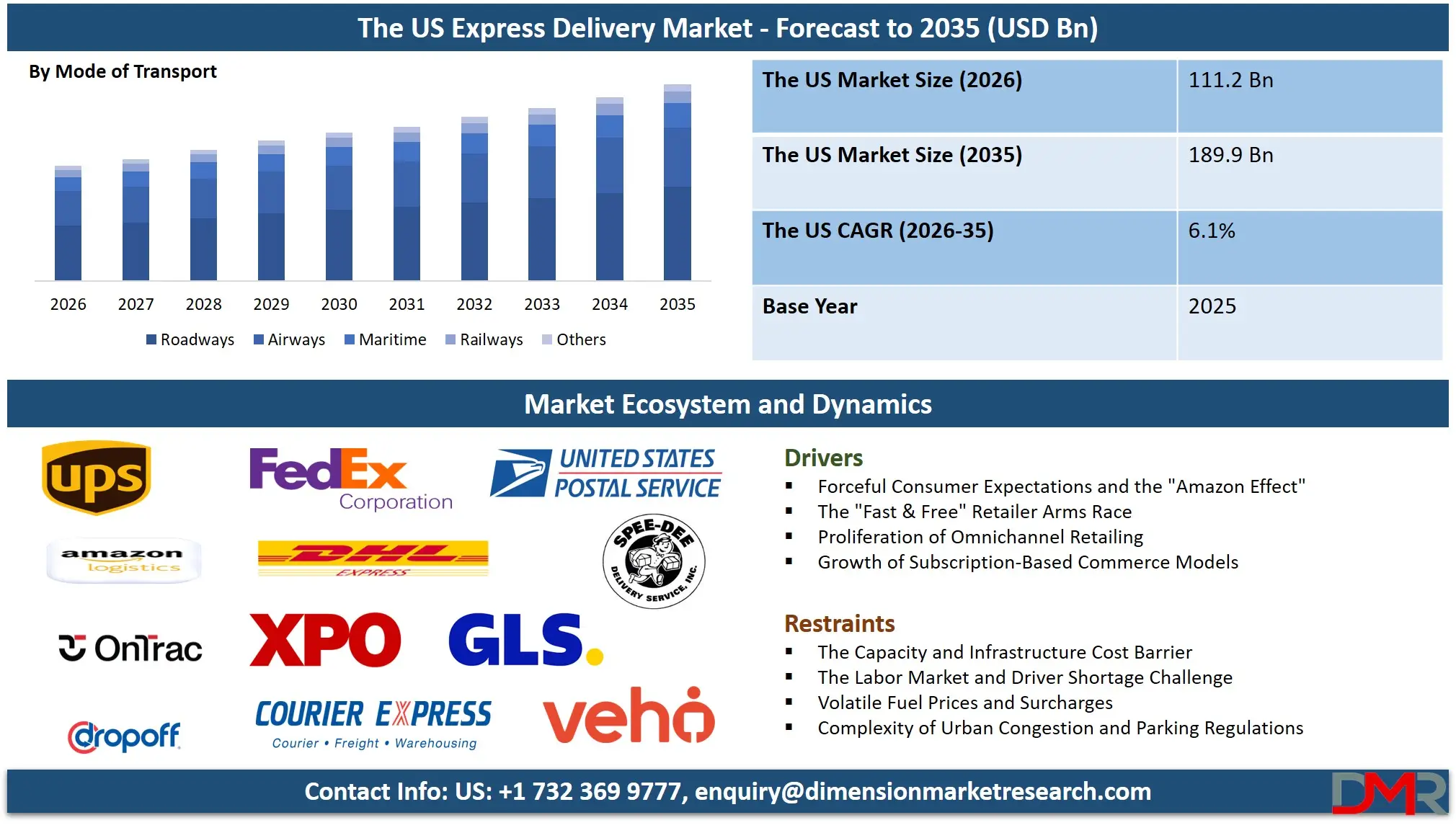

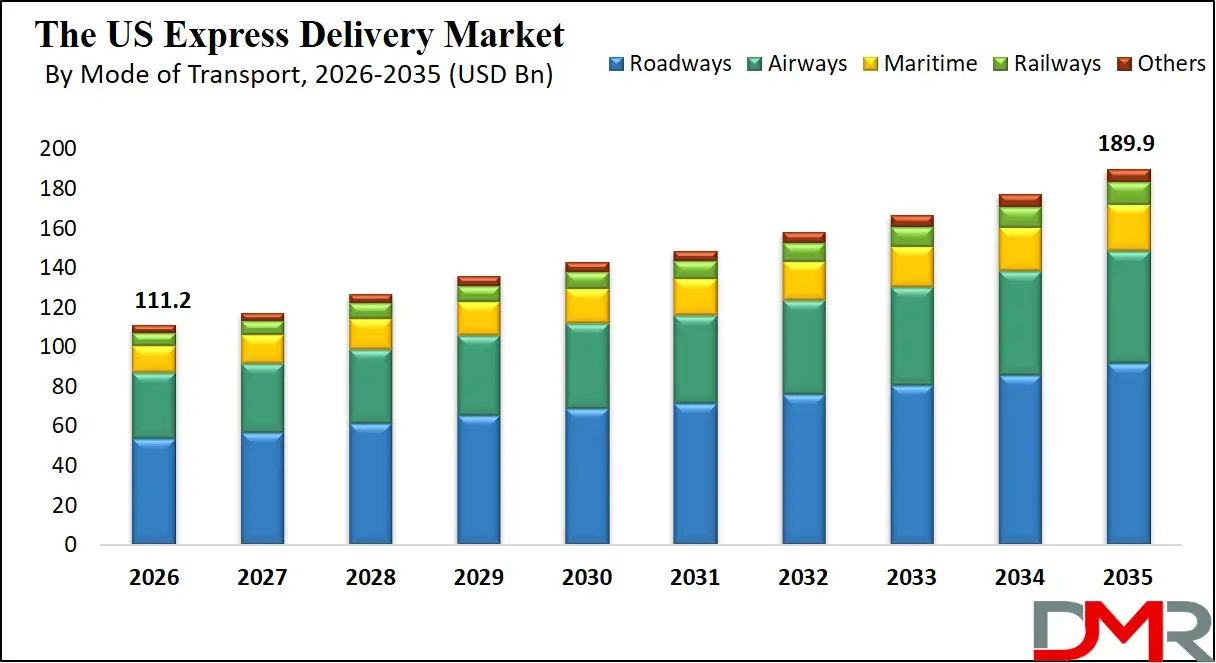

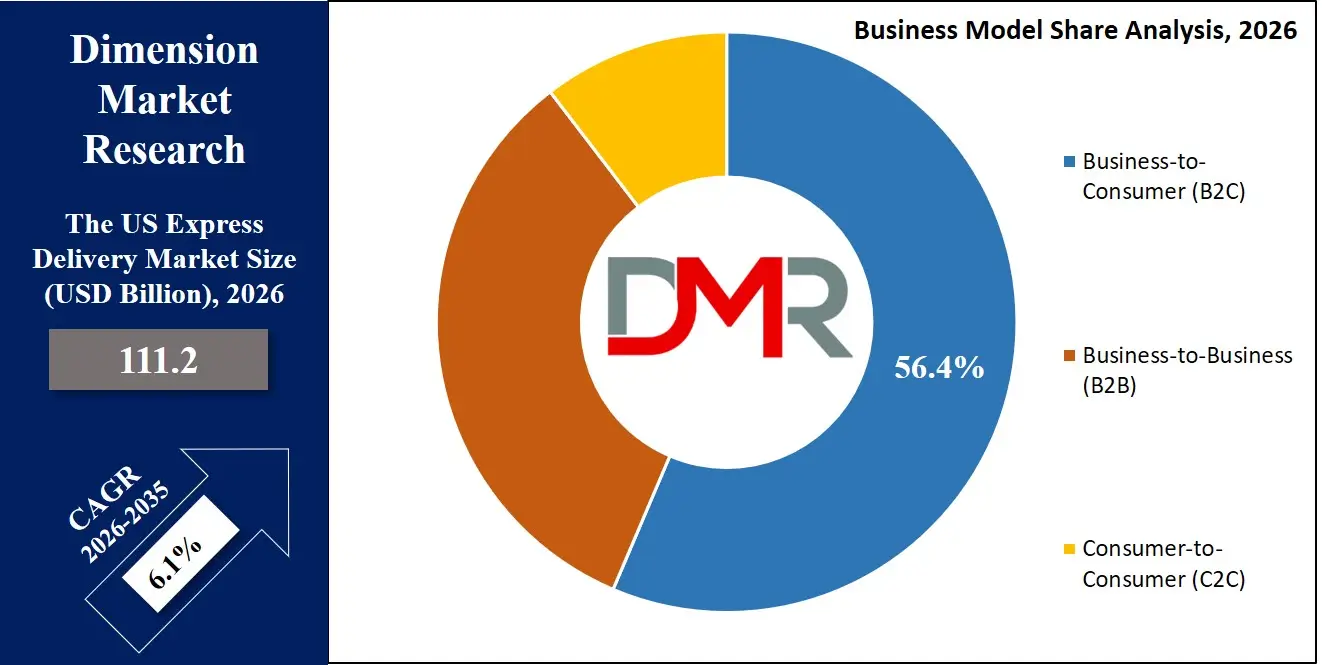

The US Express Delivery Market is projected to reach USD 111.2 billion in 2026 and is expected to grow at a CAGR of 6.1% from 2026 to 2035, reaching approximately USD 189.9 billion by 2035. The market growth is driven by the explosive growth of e-commerce, rising consumer expectations for faster shipping, and the expansion of time-definite delivery services across the United States. Additionally, advancements in route optimization software, real-time tracking technologies, drone delivery systems, and automated sorting hubs are accelerating the deployment of faster and more reliable delivery networks. These innovations are helping logistics providers enhance operational efficiency, reduce delivery times, and support the complex supply chains of modern omnichannel retail.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The American logistics landscape presents unique characteristics that amplify express delivery adoption. The world's largest consumer market with over 330 million people spanning a vast and geographically diverse territory; a consumer base that increasingly prioritizes delivery speed and reliability, influenced by giants like Amazon Prime; and a logistics industry undergoing its most significant transformation since the interstate highway system, with legacy carriers and innovative tech-enabled entrants competing fiercely on service level differentiation.

Regulatory momentum has reached an inflection point. The USPS's "Delivering for America" plan, ongoing reforms at the Federal Motor Carrier Safety Administration (FMCSA), and the implementation of the Infrastructure Investment and Jobs Act represent the most consequential logistics policy shifts in decades. The FMCSA's continued focus on Hours of Service (HOS) rules and electronic logging devices (ELDs) creates a compliance-driven demand for efficient, well-managed fleets. Simultaneously, the Infrastructure Investment and Jobs Act channels unprecedented federal funding into road, bridge, and port modernization, accelerating the deployment of freight corridors and intermodal connectors that will enable the next generation of high-speed, reliable express delivery networks.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The competitive landscape reflects this dynamism. Traditional integrated carriers, including UPS, FedEx, and the USPS, compete alongside e-commerce behemoth Amazon Logistics, regional players like OnTrac and LaserShip, and technology-forward disruptors. New entrants leverage gig-economy platforms for last-mile delivery, while established players invest billions in automation, aircraft fleets, and facility expansions. Automakers and technology companies are also playing a larger role, with electric vehicle manufacturers like Rivian supplying custom delivery vans and software firms providing the routing intelligence that underpins operational efficiency.

The US Express Delivery Market: Key Takeaways

- Unparalleled Growth Trajectory: The US market is projected to surge from USD 111.2 billion in 2026 to USD 189.9 billion by 2035, driven by a potent mix of e-commerce penetration, demanding consumer expectations, and the rapid expansion of expedited service offerings like same-day and instant delivery.

- E-Commerce-Led Volume Explosion: The shift to online retail, accelerated by the pandemic, is the single most powerful force driving demand. The need for fast, reliable, and trackable delivery from doorstep to doorstep is the new baseline for customer satisfaction.

- The Last-Mile Frontier: Beyond long-haul trucking, the final leg of delivery to the consumer represents the most complex and high-growth opportunity. Carriers are rapidly adopting new business models (C2C, on-demand) and technologies (route optimization, crowd-shipping) not just for efficiency, but for a tangible competitive advantage through faster, more flexible delivery windows.

- AI-Powered Dynamic Routing: The market is shifting from static to dynamic logistics. US companies are leading the development of AI that predicts delivery windows, optimizes routes in real-time based on traffic and weather, and bundles shipments for maximum efficiency, enabling pre-emptive service adjustments.

- Infrastructure Integration with Smart Cities: Government funding from the Infrastructure Investment and Jobs Act is accelerating the deployment of smart infrastructure, from traffic signals that communicate with delivery vehicles to dedicated curb space for loading. This integration with urban planning allows carriers to "see" beyond their own data, addressing hidden inefficiencies like double-parking and congestion.

Impact of the Iran conflict on the US Express Delivery Market

- Exposed Critical Supply Chain Vulnerabilities: The conflict highlighted the US reliance on foreign sources (specifically China) for commercial vehicle components and telematics hardware used in delivery fleets. This will drive up vehicle maintenance costs and accelerate efforts to reshore manufacturing of critical logistics equipment.

- Accelerated Defense-to-Civilian Tech Transfer: Battlefield validation of autonomous supply convoys and drone-based resupply operations will directly accelerate the development of commercial applications, particularly for resilient and secure last-mile delivery networks in contested or remote environments.

- Increased Competition for Engineering Talent: A surge in US defense spending on AI, robotics, and autonomous systems will create a war for the same limited pool of highly skilled engineers needed to develop next-generation logistics technologies, from route optimization to drone fleet management.

- Shift in National R&D Priorities: While not halting logistics progress, increased federal focus and funding on defense technologies could represent an opportunity cost, potentially slowing public-private investment in complementary areas like smart city curb management and autonomous delivery infrastructure.

The US Express Delivery Market: Use Cases

- Peak Season Surge Management: With holiday volumes a major operational challenge, networks are now being engineered with flexible, AI-driven capacity models. This allows carriers to dynamically scale sortation capacity, hire temporary staff, and pre-position inventory to mitigate the severity of delivery delays during the peak holiday season.

- Prescription Drug Delivery in Urban Canyons: In dense US cities, advanced route optimization combines real-time traffic data with secure, temperature-controlled packaging to deliver critical medications via same-day or instant delivery services, providing chain-of-custody proof and time-definite windows in complex, high-rise environments.

- Cross-Border E-Commerce Fulfillment: Leveraging multi-modal transport, carriers combine long-haul air freight with final-mile ground delivery to streamline international shipments. They manage customs clearance and provide end-to-end tracking, addressing a logistics scenario that traditional freight forwarders cannot easily handle with speed and transparency.

- Returns Management on Multi-Channel Retail: Reverse logistics systems are evolving into more proactive offerings. Carriers use network analytics and mobile apps to assess returned item conditions, provide instant refund options, and guide items back to the optimal fulfillment center or restocking channel, minimizing loss and processing time.

- Geofenced Construction Site Logistics: Commercial construction firms and industrial suppliers are integrating delivery data with project management platforms. This allows for geofencing that automatically alerts drivers of site-specific safety rules, schedules deliveries precisely to crane availability, and documents proof of delivery at specific zones within large, complex job sites.

The US Express Delivery Market: Stats & Facts

Pitney Bowes Parcel Shipping Index

- Parcel volume in the US reached approximately 21 billion in 2022.

- The US handles more parcels than any other country globally.

- Revenue from parcel services in the US was over USD 190 billion in 2022.

- Carriers handle an average of nearly 60 million parcels per day.

- E-commerce is the primary driver of parcel volume growth.

United States Postal Service (USPS)

- The USPS delivers to over 163 million addresses in the US

- It processes and delivers an average of 425 million mail pieces daily.

- Package volume has grown significantly, offsetting declines in First-Class Mail.

- The "Delivering for America" 10-year plan aims to modernize the network.

- USPS Ground Advantage offers a competitive 2-5 day ground service.

Bureau of Transportation Statistics (BTS)

- Trucks moved 72.5% of the value of US-NAFTA trade in 2022.

- Air freight accounted for a significant portion of high-value, time-sensitive imports/exports.

- Over 12 million trucks cross the US-Canada border annually.

- Rail intermodal volume has seen steady growth, driven by e-commerce.

Statista & Industry Reports

- The US logistics market is the largest in the world.

- The same-day delivery market is projected to grow at over 20% annually.

- Consumer preference for "free" shipping often outweighs speed, but speed is a key differentiator for retailers.

- Returns can account for 15-30% of online purchases, driving growth in reverse logistics.

United Nations Conference on Trade and Development (UNCTAD)

- Global e-commerce sales reached nearly USD 27 trillion in 2022.

- The US remains one of the top three B2C e-commerce markets globally.

US Department of Transportation (USDOT)

- Vehicle-to-Infrastructure (V2I) technology can improve commercial fleet efficiency by up to 15%.

- The SMART Grants program funds projects demonstrating smart community technologies, including integrated logistics systems.

The US Express Delivery Market: Market Dynamic

Driving Factors in the US Express Delivery Market

Forceful Consumer Expectations and the "Amazon Effect"

The primary catalyst for the US market is the elevated consumer baseline set by e-commerce giants. The expectation for two-day, next-day, and even same-day delivery is no longer a premium feature but a standard requirement for many online purchases. This creates a guaranteed market floor for express services. Furthermore, transparent tracking and proactive communication, while not mandatory, exert immense influence on brand loyalty and repeat purchasing decisions. Retailers aggressively partner with carriers offering time-definite delivery and real-time visibility to achieve coveted customer satisfaction ratings.

The "Fast & Free" Retailer Arms Race

In the US market, delivery speed and cost have become a primary marketing battleground. Free shipping thresholds and expedited options once reserved for premium memberships are now heavily promoted by mass-market retailers. Consumer awareness, fueled by loyalty programs like Amazon Prime and Walmart+, is exceptionally high, leading to a willingness to subscribe for benefits that include instant delivery and freight express returns. This consumer pull accelerates carrier innovation and drives down per-unit costs through economies of scale.

Restraints in the US Express Delivery Market

The Capacity and Infrastructure Cost Barrier

While demand is growing, the physical infrastructure required for expanded sortation capacity, aircraft fleets, and last-mile delivery vans still requires significant capital expense. This creates an adoption barrier for smaller regional carriers and for expanding premium services into rural areas, potentially creating a two-tiered logistics landscape. The urban-rural divide in service levels is becoming a growing concern, as residents in sparsely populated areas often face longer delivery times and higher costs compared to their urban counterparts who benefit from dense carrier networks and instant delivery options.

The Labor Market and Driver Shortage Challenge

The labor-intensive nature of package delivery introduces new challenges for the logistics industry. Even minor fluctuations in driver availability can necessitate expensive overtime and temporary hiring, impacting margins. A shortage of qualified Commercial Driver's License (CDL) holders for heavy trucking and a high turnover rate for last-mile delivery drivers can lead to service delays, longer delivery windows, and higher labor costs, potentially affecting long-term service reliability and consumer trust. This complexity is compounded by the fact that labor demands are not consistent; peak season volumes can require a surge workforce that is difficult to source and train quickly. Carriers are still grappling with how to properly balance a flexible gig-economy workforce with the need for reliable, background-checked employees, leading to operational challenges and potential service inconsistencies.

Opportunities in the US Express Delivery Market

The Massive Healthcare and Pharmaceutical Frontier

The healthcare logistics sector, a critical and growing part of the US economy, presents a massive growth opportunity. Pharmacies, hospitals, and specialty pharmacies are under immense pressure to manage temperature-sensitive inventories and ensure patient adherence. Partnering with express carriers for time-definite and next-day delivery of prescriptions and medical devices offers a clear value proposition through improved patient outcomes and reduced hospital readmissions. The opportunity is staggering: an aging US population and the rise of expensive biologic drugs, which require strict cold-chain management, create high-margin, recurring revenue streams. A single lost or delayed temperature-sensitive shipment can cost a pharmaceutical company millions in product and compliance penalties.

AI-Powered Predictive Logistics and Dynamic ETA Accuracy

The next frontier is moving from reactive tracking to predictive ETAs. US software and AI companies are developing platforms that use cloud data, real-time traffic analysis, and historical delivery patterns to predict and communicate precise delivery windows to consumers minutes before arrival. This includes personalizing communication channels and re-delivery options based on individual customer preferences, monitored through interaction data. Startups and established carriers are moving beyond simple GPS tracking to create a "predictive logistics cocoon" that understands context. For example, an AI system might analyze that a specific residential street typically has heavy delivery volume on Tuesday afternoons. If a new shipment enters the area, the system can predict a more accurate window, bundling it with nearby stops for efficiency, and provide a personalized, real-time alert to the customer.

Trends in the US Express Delivery Market

Network Fusion and System Redundancy

The industry is rapidly moving away from relying on a single mode of transport or a single carrier network. The dominant trend is network fusion, where data from road, air, and rail are synthesized by a central logistics AI platform to create a robust, redundant, and resilient operational model. This is critical for enabling higher service levels and ensuring performance during peak seasons or disruptive weather events. This trend is best exemplified by the shift in logistics architecture. Older models operated in silos: a ground network for standard parcels, an air network for express. Today, carriers are adopting "integrated networks" where the optimal mode is chosen dynamically. This allows for "multi-modal fusion," where the speed of air compensates for the capacity of ground, and the resilience of rail offers a backup when highways are congested.

The Rise of Alternative Delivery Methods and Digital Infrastructure

Drone delivery, autonomous ground vehicles (AGVs), and crowd-shipping are gaining undeniable momentum. With FAA certification pathways and active pilot programs in states like Texas, North Carolina, and California, the integration of non-traditional delivery methods into the logistics ecosystem is accelerating. This allows for "hyper-local" capabilities, bypassing road traffic to deliver small parcels, meals, or medical supplies directly to consumers in minutes. The momentum is shifting decisively from traditional hub-and-spoke models to distributed, micro-fulfillment strategies leveraging the scalability of gig-economy platforms. The USDOT's focus on integration and safety aims for nationwide adoption frameworks, with significant milestones by 2028. In California, companies are using autonomous bots for last-mile grocery delivery, dramatically reducing per-stop costs and carbon emissions. In North Carolina, drone delivery pilots are being used to study how to transport lab samples between hospitals, bypassing ground traffic and providing near-instantaneous service.

The US Express Delivery Market: Research Scope and Analysis

By Destination Analysis

In the United States express delivery market, domestic shipments are currently projected to dominate adoption. Among these, intra-city and inter-state express delivery is the most significant service due to the sheer size of the US economy and the high volume of e-commerce transactions originating and ending within the country. As retailers and consumers push for faster delivery times, domestic express services are rapidly becoming the standard for online orders.

However, the fastest-growing segment is international express deliveries. These shipments use a combination of air freight and last-mile ground networks to connect US consumers and businesses with global markets. E-commerce platforms are integrating international shipping as a key feature, enabling cross-border trade. Beyond standard documents and parcels, international express services are evolving to manage complex customs clearance and regulatory compliance for specialized industries like healthcare & pharmaceuticals and technology & electronics. These capabilities may eventually offer fully managed, door-to-door global logistics with predictive delay alerts.

Domestic delivery, including both B2B and B2C, is also widely adopted and is the foundation of the express market. These services help businesses reach customers and manage supply chains efficiently.

Another important destination category is domestic shipments facilitated by regional carriers. These regional specialists focus on specific geographic areas, offering cost-effective and fast ground delivery for lightweight e-commerce parcels. Their focus on density within a region allows them to compete effectively with national carriers on both price and speed for next-day and two-day delivery zones.

Overall, service innovation in express delivery is increasingly focused on combining speed, international capability, and seamless customer experience.

By Business Model Analysis

The business model landscape of express delivery in the United States is built primarily on Business-to-Consumer (B2C) shipments, with e-commerce orders forming the core volume for most major carriers. B2C deliveries are characterized by high volumes, individual residential addresses, and the need for features like evening or weekend delivery windows and real-time tracking. Together with returns processing, they form the foundation of modern express delivery networks.

A key emerging trend is the growth of the Consumer-to-Consumer (C2C) model, enabled by online marketplaces and peer-to-peer platforms. Unlike traditional retail, C2C shipments often involve unique items, irregular shapes, and the need for affordable, reliable shipping options between individuals. Platforms like eBay, Poshmark, and Facebook Marketplace generate significant volume for carriers offering simple, trackable services.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The next major business model layer is Business-to-Business (B2B) express delivery, particularly for time-critical restocking of retail stores, just-in-time manufacturing parts, and document delivery. Leading carriers such as FedEx, UPS, and regional LTL (Less-Than-Truckload) providers are investing heavily in proprietary networks and technology platforms to handle the specific needs of B2B shipments, including rigid delivery windows, palletized freight, and proof of delivery.

One controversial approach is some retailers' use of gig-economy drivers for instant delivery, which prioritizes speed and flexibility but can raise questions about worker classification and consistent service quality. In contrast, most major carriers prefer a mixed-model strategy, using employee drivers for core network reliability and supplementing with gig workers during peak demand.

Another important business model trend is the rise of fulfillment-as-a-service providers, where carriers not only deliver but also store, pick, and pack inventory for merchants. As e-commerce complexity increases, businesses will increasingly seek partners offering end-to-end logistics solutions. Additionally, reverse logistics networks are becoming a critical service, allowing carriers to manage returns efficiently and cost-effectively.

By Mode of Transport Analysis

In the US express delivery market, roadways, including a vast network of trucks and vans, represent the largest segment by volume. This dominance is largely driven by the flexibility and reach of ground transportation for last-mile delivery. The widespread adoption of linehaul trucks and delivery vans for both long-haul and final-mile segments has accelerated the integration of express delivery services across all geographies.

However, airways are emerging as the fastest-growing segment for time-critical express delivery. Express carriers face significant competitive pressure to reduce transit times for long-distance and cross-border shipments. As a result, companies are increasingly investing in their own air fleets and partnering with commercial airlines to move packages overnight, ensuring next-day and time-definite delivery commitments are met. The rapid growth of e-commerce has significantly increased the number of air cargo shipments, particularly for high-value or time-sensitive goods.

The integration of railways into express networks is also an important development. Intermodal containers moving on rail provide a cost-effective and fuel-efficient alternative to long-haul trucking for the middle mile of a shipment's journey. Carriers use rail to move large volumes of parcels between regional hubs, where they are then transferred to trucks for final delivery.

Another important segment supporting network efficiency is maritime for international express. While slower than air, ocean freight is essential for high-volume, less time-sensitive imports, feeding inventory into distribution centers that then fulfill express orders via ground or air. Leading carriers are integrating maritime services into their end-to-end express offerings, providing a complete logistics solution for international e-commerce.

By Shipment Weight Analysis

Shipment weight plays a crucial role in shaping the economics and operations of express delivery in the United States. Most parcels currently moving through express networks fall into the lightweight category, typically under 5 lbs. These include small e-commerce items, documents, and pharmaceuticals. Lightweight shipments are ideal for air transport and last-mile delivery vans due to their high density and ease of handling.

Medium weight shipments, ranging from 5 to 70 lbs, represent a significant and growing segment. This category includes larger e-commerce items like small appliances, boxes of books, and auto parts. Medium weight shipments require more robust handling and often move via a mix of air and ground, with carriers optimizing the mode based on speed requirements and cost. Consumers are increasingly willing to purchase these heavier items online, driving growth in this segment.

Heavyweight shipments, typically palletized freight over 70 lbs or shipments requiring a truck for a single item, are the domain of freight express services. These shipments are critical for B2B supply chains, construction, and industrial manufacturing. The demand for faster, more reliable freight service is growing, with carriers offering time-definite and even next-day options for heavyweight LTL (Less-Than-Truckload) shipments.

The service type used is highly dependent on weight. Lightweight parcels are well-suited for same-day courier services and instant delivery platforms. Medium weight items are the bread and butter of next-day and two-day express networks. Heavyweight freight is primarily served by dedicated freight express and LTL networks that are separate from the small parcel sortation systems.

By Service Type Analysis

Service type is the defining characteristic of the express delivery market, driven by varying customer expectations and willingness to pay. Time-definite delivery (Express) services, guaranteeing delivery by a specific time (e.g., 10:30 AM next day), represent the premium tier and are widely adopted for critical business documents and urgent shipments. Deferred delivery (Standard) , with a longer, less specific window (e.g., 2-5 days), is the workhorse for most e-commerce and routine B2B shipments.

Premium express services are evolving into same-day delivery and instant delivery (on-demand) capabilities. Examples include courier services that pick up and deliver within hours, or platform-based delivery of restaurant meals and retail goods. Consumers and businesses are increasingly willing to pay premium prices for these hyper-convenient services because they solve immediate needs.

Next-day delivery, a more accessible premium service, has become a competitive necessity for many online retailers. It represents a key battleground where carriers differentiate themselves through network speed and reliability.

Meanwhile, freight express is currently focused on the B2B and industrial sectors, offering accelerated handling and delivery for palletized and heavyweight shipments. Despite ongoing development of faster freight options, time-definite and next-day for freight remain a key differentiator rather than a universal offering, as the operational complexity is significantly higher than for small parcels.

By End-User Industry Analysis

In the United States express delivery market, the Retail & E-commerce industry overwhelmingly dominates as the end-user. Most modern express delivery volume is driven by online orders requiring fast, reliable transportation from fulfillment centers to consumers' doorsteps. Because of the scale and velocity of this segment, carriers have built their networks primarily around the needs of e-commerce and omnichannel retail.

Retailers integrate express delivery options directly into their online checkout flows to ensure seamless customer experience, competitive shipping rates, and service reliability. Additionally, the high rate of online returns makes efficient reverse logistics a critical requirement for both merchants and carriers. As retail evolves into an omnichannel model, many inventory movements are embedded within the carrier's core network, serving both store replenishment and direct-to-consumer orders. This deep integration makes it extremely difficult to replicate the same level of service without a sophisticated carrier partnership.

Nevertheless, the Healthcare & Pharmaceuticals segment plays an important and rapidly growing role, particularly within the temperature-controlled and time-critical delivery sectors. Hospitals, pharmacies, and labs often require express delivery for blood samples, organs for transplant, or specialty prescription drugs. Major carriers such as FedEx Custom Critical and UPS Healthcare provide specialized express solutions for medical shipments.

The healthcare sector also relies on express delivery for direct-to-patient medication dispensing. However, these solutions are generally more complex and regulated compared to standard retail shipments. For example, services may offer same-day or next-day delivery of temperature-sensitive biologics, but typically require special packaging and chain-of-custody protocols.

For other sectors like Automotive & Industrial and Technology & Electronics, express delivery is largely limited to mission-critical parts and prototype shipments where downtime or delay is costly.

The US Express Delivery Market Report is segmented on the basis of the following:

By Destination

By Business Model

- Business-to-Business (B2B)

- Business-to-Consumer (B2C)

- Consumer-to-Consumer (C2C)

By Mode of Transport

- Roadways

- Airways

- Railways

- Maritime

- Others

By Shipment Weight

- Lightweight

- Medium Weight

- Heavyweight

By Service Type

- Time-Definite Delivery (Express)

- Deferred Delivery (Standard)

- Same-Day Delivery

- Next-Day Delivery

- Instant Delivery (On-Demand)

- Freight Express

By End-User Industry

- Retail & E-commerce

- Healthcare & Pharmaceuticals

- Automotive & Industrial

- Banking, Financial Services & Insurance (BFSI)

- Technology & Electronics

- Manufacturing

- Construction

- Others

Impact of Artificial Intelligence in the US Express Delivery Market

- Deep Learning for Package Sorting & Handling: AI, particularly computer vision, is used to classify millions of packages per hour, reading labels and determining optimal sortation paths with ever-increasing accuracy, reducing missorts and damage.

- Predictive Route Planning: AI algorithms analyze historical traffic patterns, weather data, and delivery density to predict the most efficient routes for drivers, enabling pre-emptive re-routing to avoid delays.

- Robust Network Optimization: AI is the "brain" that fuses disparate data from sortation centers, vehicle telematics, and customer apps into a single, coherent, and dynamic model of the carrier's entire logistics network.

- Edge AI for Instantaneous Delivery Matching: High-performance computing in delivery vehicles and driver apps allows for split-second decisions on dynamic dispatch, bundling a new on-demand pickup with an existing route without relying on the cloud.

- Fleet Learning (The "Continuous Improvement" Model): Carriers use anonymized data from their entire delivery fleet to continuously train and improve their central AI models. When one driver encounters a novel obstacle or finds a faster way to navigate a neighborhood, the learning can be uploaded and, after validation, disseminated to the entire fleet via an OTA update.

- Customer Interaction & Personalization: AI analyzes customer communication preferences and historical delivery choices to personalize delivery windows, notification methods (SMS, email, app), and even offer specific value-added services like evening delivery or secure drop-off locations.

The US Express Delivery Market: Competitive Landscape

The US express delivery market is a highly dynamic and concentrated competitive landscape characterized by the presence of global integrated carriers, national postal operators, regional ground specialists, and technology-driven platform players. Leading integrated carriers such as UPS, FedEx, and the United States Postal Service (USPS) maintain strong market positions by operating vast, vertically integrated air and ground networks capable of handling everything from documents to heavyweight freight. Alongside these giants, e-commerce-driven logistics providers are becoming increasingly influential in shaping market dynamics. Companies such as Amazon Logistics are building massive in-house delivery capabilities, fundamentally altering the competitive balance and raising service expectations for all.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

In addition, regional carriers such as OnTrac (now part of LSO) and LaserShip (now operating as Veho in some markets) play a key role in providing cost-effective, high-speed ground delivery for e-commerce in dense geographic corridors. The United States also hosts a growing ecosystem of on-demand delivery platforms including Uber Direct, DoorDash Drive, and Roadie, which are focused on enabling instant delivery and same-day delivery for retailers without their own fleets. At the same time, technology giants like Google and Microsoft are partnering with carriers to provide the cloud computing and AI platforms that power modern logistics optimization.

Some of the prominent players in the US Express Delivery Market are:

- United Parcel Service (UPS)

- FedEx Corporation

- United States Postal Service (USPS)

- Amazon Logistics

- DHL Express

- OnTrac

- LaserShip

- Spee-Dee Delivery Service

- Courier Express

- Dropoff Inc.

- Roadie

- Veho Technologies

- Onfleet

- XPO, Inc.

- TFI International

- GLS US (General Logistics Systems)

- Lone Star Overnight (LSO)

- Need It Now Delivers

- MedSpeed

- Priority One Courier

- Other Key Players

Recent Developments in the US Express Delivery Market

- January 2026: United Parcel Service announced a major USD 3 billion restructuring plan, including workforce reductions and facility closures, as it shifts focus away from low-margin volumes (especially from Amazon) toward higher-profit segments like healthcare logistics and SMB customers.

- December 2025: Amazon continued expanding its logistics dominance, delivering over 6.3 billion parcels in 2024 and rapidly increasing its market share, with projections to surpass United States Postal Service in total parcel volumes by 2028.

- December 2025: General Logistics Systems announced a strategic partnership with ePost Global to expand its cross-border e-commerce capabilities, enhancing delivery solutions across key trade lanes between the US, Europe, Canada, and Australia.

- September 2025: OnTrac announced the launch of new services including “OnTrac Express” and “Ground Essentials,” aimed at providing cost-effective and flexible delivery options, with full rollout planned for early 2026.

- August 2025: United States Postal Service implemented rate adjustments across services (approximately, 3–9%), reflecting rising operational costs and network modernization efforts.

- May 2025: Amazon signed a multi-year delivery partnership with FedEx Corporation, allowing FedEx to handle select large-package residential deliveries. This marks a strategic shift in Amazon’s logistics network and intensifies competition with UPS.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 111.2 Bn |

| Forecast Value (2035) |

USD 189.9 Bn |

| CAGR (2026–2035) |

6.1% |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors and etc. |

| Segments Covered |

By Destination (Domestic and International), By Business Model (Business-to-Business (B2B), Business-to-Consumer (B2C) and Consumer-to-Consumer (C2C)), By Mode of Transport (Roadways, Airways, Railways, Maritime and Others), By Shipment Weight (Lightweight, Medium Weight and Heavyweight), By Service Type (Time-Definite Delivery (Express), Deferred Delivery (Standard), Same-Day Delivery, Next-Day Delivery, Instant Delivery (On-Demand) and Freight Express), By End-User Industry (Retail & E-commerce, Healthcare & Pharmaceuticals, Automotive & Industrial, Banking, Financial Services & Insurance (BFSI), Technology & Electronics, Manufacturing, Construction and Others) |

| Country Coverage |

The US |

| Prominent Players |

United Parcel Service, FedEx Corporation, United States Postal Service, Amazon Logistics, DHL Express, OnTrac, LaserShip, Spee-Dee Delivery Service, Courier Express, Dropoff Inc., Roadie, Veho Technologies, Onfleet, XPO Inc., TFI International, General Logistics Systems (GLS US), Lone Star Overnight, Need It Now Delivers, MedSpeed, Priority One Courier, and Other Key Players |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users) and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days and 5 analysts working days respectively. |

Frequently Asked Questions

How big is the US Express Delivery Market?

▾ The US Express Delivery Market is valued at USD 111.2 billion in 2026 and is projected to reach USD 189.9 billion by the end of 2035.

What is the growth rate for the US Express Delivery Market?

▾ The market is growing at a robust compound annual growth rate (CAGR) of 6.1% over the forecast period of 2026 to 2035.

Who are the key players in the US Express Delivery Market?

▾ Some of the major key players in the US Express Delivery Market are United Parcel Service (UPS), FedEx Corporation, United States Postal Service (USPS), Amazon Logistics, DHL Express, OnTrac, LaserShip, Spee-Dee Delivery Service, and many others.