Market Overview

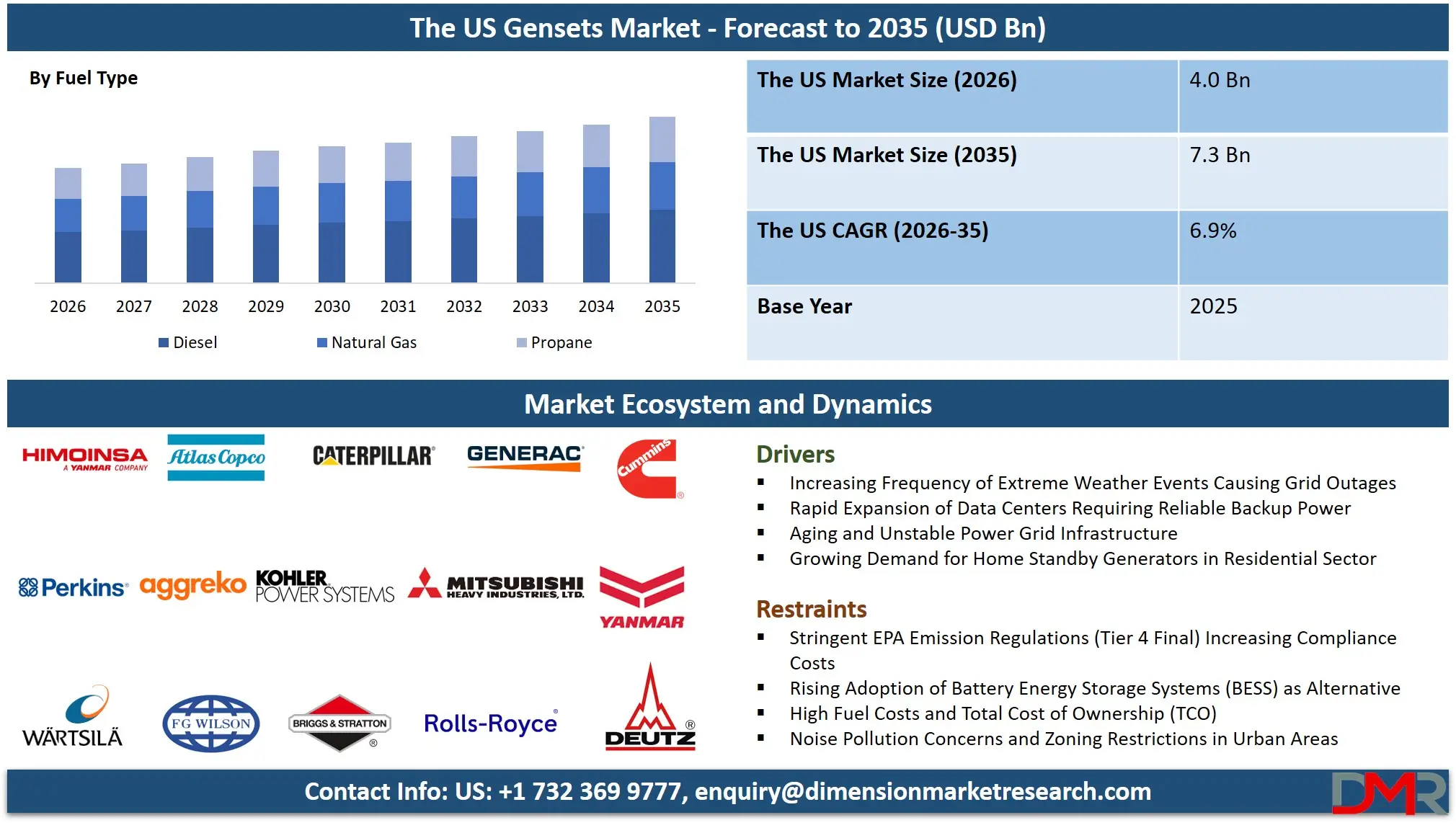

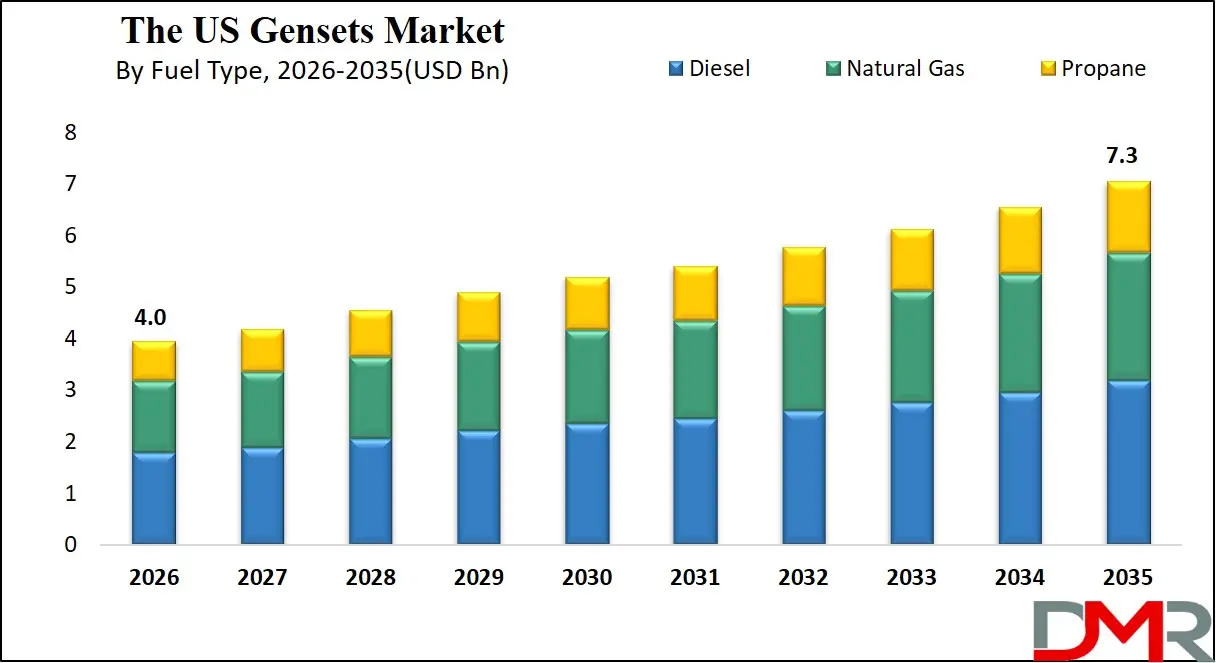

The US Gensets Market is projected to reach approximately USD 4.0 billion in 2026 and is anticipated to expand steadily, reaching around USD 7.3 billion by 2035, at a CAGR of 6.9% during the forecast period. The U.S. represents one of the most mature and technologically advanced markets for generator sets globally, characterized by high adoption across residential, commercial, and industrial sectors.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

A defining feature of the U.S. gensets market is the increasing frequency and severity of extreme weather events, including hurricanes, wildfires, winter storms, and heatwaves. These disruptions have exposed vulnerabilities in grid infrastructure, prompting businesses, households, and public institutions to invest heavily in backup power solutions. As a result, gensets are no longer considered optional assets but essential components of energy resilience strategies.

The country’s vast and diverse geography also plays a significant role in shaping demand. Rural and remote regions often face challenges related to grid connectivity and reliability, making gensets a critical source of both primary and standby power. In contrast, urban areas require high-capacity gensets to support dense infrastructure, including high-rise buildings, hospitals, and data centers.

The rapid expansion of the digital economy is another major driver. The United States is home to a large concentration of hyperscale data centers, which form the backbone of cloud computing, artificial intelligence, and digital services. These facilities require uninterrupted power supply, and gensets serve as the final line of defense against outages. High-capacity gensets, often above 750 kVA, are widely deployed in these environments, with multiple redundant systems ensuring reliability.

Industrial activity across sectors such as manufacturing, oil and gas, and construction further supports market growth. These industries rely on gensets for both standby and prime power applications, particularly in locations where grid power is insufficient or unreliable. The oil and gas sector, in particular, utilizes gensets extensively in upstream and midstream operations, where continuous power is essential for safety and efficiency.

Another notable aspect of the U.S. market is the strong presence of leading genset manufacturers and technology providers. Companies are continuously innovating to improve efficiency, reduce emissions, and integrate digital capabilities. The adoption of smart gensets equipped with advanced monitoring systems and IoT connectivity is becoming increasingly common, enabling real-time performance tracking and predictive maintenance.

Environmental regulations and sustainability goals are also influencing the market. While diesel gensets remain dominant due to their reliability and high power output, there is a growing shift toward cleaner alternatives such as natural gas and hybrid systems. The abundance of natural gas in the U.S. has made gas-powered gensets an attractive option, offering lower emissions and more stable fuel costs.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Additionally, the rise of distributed energy systems and microgrids is creating new opportunities for genset integration. These systems combine multiple energy sources, including renewables, battery storage, and gensets, to provide reliable and flexible power solutions. Gensets play a crucial role in ensuring stability and backup within these configurations.

The residential segment is also experiencing significant growth, driven by increasing awareness of power reliability and the availability of affordable backup solutions. Homeowners are investing in standby generators to protect against outages, particularly in regions prone to severe weather.

In conclusion, the United States Gensets Market is driven by a combination of environmental challenges, technological advancements, and evolving energy needs. The market is expected to continue its growth trajectory, supported by strong demand across multiple sectors and ongoing innovation in genset technologies.

The US Gensets Market: Key Takeaways

- Steady The US Market Growth Outlook: The US Gensets Market is expected to be valued at USD 4.0 billion in 2026 and is projected to reach USD 7.3 billion by 2035, showcasing steady expansion supported by rising power demand and grid unreliability.

- Moderate CAGR Driven by Industrialization: The market is expected to grow at a CAGR of 6.9% from 2026 to 2035, fueled by increasing infrastructure projects, urbanization, and a growing focus on energy security across industries.

- Diesel Segment Dominance with Transition Trends: Diesel gensets continue to dominate the U.S. market due to reliability, high power density, and widespread fuel availability. However, stricter emission regulations are accelerating innovation in cleaner diesel technologies, bi-fuel systems, and renewable diesel compatibility.

- High-Capacity Segment Driven by Data Centers: Gensets above 750 kVA are the fastest-growing segment, fueled by hyperscale data centers and large industrial facilities. Increasing digitalization, AI infrastructure, and manufacturing expansion are driving demand for high-capacity, multi-megawatt backup power solutions.

- Standby Power as Primary Application: Standby power remains the dominant application due to rising grid instability and extreme weather events. Regulatory mandates across healthcare, telecom, and infrastructure sectors further ensure consistent demand for reliable emergency backup power systems nationwide.

- Data Centers and Healthcare Lead End-User Demand: Data centers and healthcare sectors are the most critical end-users, requiring uninterrupted power and high reliability. Rapid digital growth, 5G expansion, and stringent healthcare regulations continue to drive strong demand for advanced genset solutions.

Impact of Iran Conflict on the US Gensets Market

- Volatility in Global Fuel Prices: Geopolitical tensions arising from the Iran conflict contribute to fluctuations in global oil and gas prices, directly impacting operating costs of gensets in the United States, especially diesel-based systems that rely on stable fuel pricing.

- Increased Focus on Domestic Energy Security: The United States is emphasizing domestic energy production to reduce reliance on imports amid geopolitical tensions, encouraging the adoption of natural gas-based gensets, which offer cost efficiency, fuel stability, and alignment with national energy security strategies.

- Rising Demand for Backup Power Solutions: Uncertainty in global energy markets due to geopolitical conflicts increases the importance of reliable backup power systems, driving demand for gensets across residential, commercial, and industrial sectors to ensure operational continuity during supply disruptions and outages.

The US Gensets Market: Use Cases

- Emergency Backup for Residential and Commercial Buildings: Gensets play a crucial role in providing backup power during outages caused by extreme weather events, ensuring uninterrupted electricity supply for homes, offices, retail spaces, and essential services across urban and suburban areas in the United States.

- Data Center Power Reliability: High-capacity gensets are essential for ensuring uninterrupted operations in data centers, supporting critical digital infrastructure by providing instant backup power during grid failures, maintaining uptime, protecting sensitive equipment, and preventing costly data loss or service disruptions.

- Industrial and Oil & Gas Applications: In industrial and oil and gas sectors, gensets are widely used for standby and prime power applications, supporting continuous operations in remote locations, ensuring energy reliability, and maintaining productivity in energy-intensive and mission-critical industrial environments.

- Construction and Temporary Power Needs: Rental gensets are extensively used in construction and infrastructure projects to provide temporary power supply, supporting equipment operation, site lighting, and project continuity in locations where grid access is limited or unavailable during development phases.

- Microgrid and Distributed Energy Systems: Gensets are increasingly integrated into microgrid and distributed energy systems, providing backup and load balancing support alongside renewable sources, enhancing grid resilience, improving energy efficiency, and ensuring stable power supply in both urban and remote environments.

The US Gensets Market: Stats & Facts

U.S. Energy Information Administration (EIA) / U.S. Government

- U.S. electricity consumption is projected to reach 4,165 billion kWh in 2025, a record high.

- Electricity consumption was 4,086 billion kWh in 2024.

- Total electricity consumption was 4,012 billion kWh in 2023.

- Natural gas accounts for about 43%–44% of total electricity generation.

- Coal contributes around 15%–17% of electricity generation.

- Nuclear energy provides about 19% of electricity generation.

- Renewable energy share is expected to reach around 25% of electricity generation by 2025.

- Renewable energy generated about 24.2% of U.S. electricity in 2024.

- Wind power contributes around 10.3% of total electricity generation.

- Solar energy contributes about 6.9% of total electricity generation.

Federal Energy Regulatory Commission (FERC)

- Over 90% of new electricity generation capacity additions in 2024 came from renewable sources.

- Renewable energy accounts for over 30% of total installed U.S. generating capacity.

North American Electric Reliability Corporation (NERC)

- The Generating Availability Data System tracks over 5,800 generating units across North America.

- These units represent about 71% of installed generating capacity in the U.S. and Canada.

- Reporting is mandatory for generating units 20 MW and above.

U.S. Power Reliability & Outage Data (Government / Academic-backed Studies)

- Around 179 million outage records were recorded across U.S. counties from 2014–2023.

- Approximately 318 counties across 45 states are identified as high power vulnerability zones.

- Counties experienced about 999 outages on average over a decade.

- Each county experienced outages affecting over 540,000 customers on average.

- Power outages occur approximately weekly in many regions.

- Over 25% of U.S. households experienced power outages in 2023.

- Power outages cost the U.S. economy around USD 150 billion annually.

- About 87% of outages are caused by natural hazards such as storms and wildfires.

American Public Power Association (APPA)

- Public power utilities serve around 15% of U.S. electricity customers.

- These utilities generate approximately 9% of total electricity output.

U.S. Energy Transition & Infrastructure Insights (Government / Institutional Data)

- Fossil fuels contributed less than 50% of U.S. electricity generation for the first time in 2025.

- Wind and solar together generated over 17% of electricity in 2024.

- Renewable electricity generation grew by around 9.6% in 2024.

- Solar generation increased by over 26% year-on-year in 2024.

- Wind generation increased by about 7.7% in 2024.

The US Gensets Market: Market Dynamic

Driving Factors in the United States Gensets Market

Increasing Frequency of Power Outages

The United States has experienced a marked increase in weather-related power outages over the past decade, with hurricanes, wildfires, winter storms, and heatwaves placing unprecedented strain on aging grid infrastructure. Events such as Hurricane Ida, Texas winter storms, and California wildfire-related shutoffs have demonstrated the vulnerability of centralized power systems, driving both commercial entities and residential homeowners to invest in backup power solutions. This trend has elevated gensets from optional equipment to essential infrastructure across regions previously considered grid-reliable, fundamentally expanding the addressable market.

Expansion of Digital and Industrial Infrastructure

The rapid growth of hyperscale data centers, semiconductor fabrication facilities, e-commerce fulfillment centers, and advanced manufacturing operations across the United States has created substantial demand for high-reliability backup power systems. Data center construction in markets such as Northern Virginia, Silicon Valley, Dallas, Phoenix, and Atlanta requires multi-megawatt genset installations with extended runtime capabilities and redundant configurations. Similarly, industrial reshoring initiatives and manufacturing expansion under federal infrastructure programs are driving increased adoption across industrial sectors.

Restraints in the United States Gensets Market

Environmental Regulations

Stringent emissions standards enforced by the Environmental Protection Agency, particularly Tier 4 final requirements for non-road diesel engines, impose significant compliance costs on manufacturers and end-users. These regulations limit diesel genset applications in urban areas with strict air quality management districts, particularly in California where the California Air Resources Board enforces additional requirements. Compliance necessitates advanced after-treatment systems including diesel particulate filters and selective catalytic reduction, increasing upfront capital costs and operational complexity for fleet operators.

Fuel Price Volatility

Diesel and natural gas price fluctuations expose genset operators to operational cost uncertainty, particularly for prime power applications and facilities requiring extended runtime during prolonged outages. Geopolitical tensions, supply chain disruptions, and domestic energy policy shifts contribute to price instability that affects total cost of ownership calculations. This volatility encourages end-users to explore alternative fuel options and hybrid configurations that reduce dependence on single fuel sources while maintaining reliability standards.

Opportunities in the United States Gensets Market

Growth of Natural Gas-Based Gensets

Abundant domestic natural gas reserves and extensive pipeline infrastructure across the United States create favorable conditions for natural gas genset adoption. These systems offer lower emissions profiles compared to diesel, quieter operation suitable for urban and residential applications, and generally more stable fuel pricing. Applications including combined heat and power for commercial buildings, industrial cogeneration, and utility-scale peak shaving are experiencing accelerated growth, supported by federal and state incentives for high-efficiency distributed generation.

Integration with Renewable Energy Systems

The rapid expansion of solar and wind generation across the United States creates significant opportunities for hybrid systems combining gensets with renewable energy sources and battery storage. These configurations enable facility operators to optimize energy costs, reduce carbon footprints, and maintain resilience during grid events. Microgrid deployments across commercial campuses, critical infrastructure facilities, and community resilience hubs increasingly incorporate gensets as dispatchable backup assets within sophisticated energy management architectures.

Trends in the United States Gensets Market

Adoption of Smart and Connected Gensets

IoT-enabled gensets with cloud-based monitoring platforms, predictive maintenance algorithms, and remote diagnostics capabilities are becoming standard across commercial and industrial applications. These smart systems provide facility managers with real-time visibility into equipment status, automated alerts for maintenance needs, and performance analytics that optimize fuel efficiency and extend equipment life. The integration of artificial intelligence for fault detection and operational optimization represents the next frontier in connected genset technology.

Rise of Residential Backup Power Solutions

Homeowner investment in standby generators has accelerated dramatically following recent extreme weather events that exposed grid vulnerabilities across all regions. Residential adoption, once concentrated in hurricane-prone coastal areas and regions with unreliable grid infrastructure, has expanded nationwide. Manufacturers are responding with quieter, more aesthetically integrated systems featuring automatic transfer switches, remote monitoring capabilities, and options for natural gas or propane fuel sources that appeal to suburban and even urban homeowners prioritizing energy independence.

The US Gensets Market: Research Scope and Analysis

By Fuel Type Analysis

Diesel gensets is projected to dominate the United States gensets market, maintaining their position as the preferred choice for critical backup power applications across commercial, industrial, and infrastructure sectors. This dominance is rooted in diesel's proven reliability, high power density, and ability to deliver instantaneous response during grid failures. Critical facilities including hospitals, data centers, telecommunications networks, and emergency services overwhelmingly specify diesel gensets for their ability to handle large load blocks and provide extended runtime capabilities essential during prolonged outages caused by hurricanes, winter storms, or grid failures. The extensive diesel fuel distribution infrastructure across all fifty states, including remote rural areas and regions prone to natural disasters, further reinforces this segment's market leadership. The existing installed base of diesel units across the United States represents a substantial replacement and maintenance-driven market, with many units reaching end-of-life after decades of service. However, the diesel segment faces increasing regulatory pressure from Environmental Protection Agency Tier 4 emissions standards, particularly in states with additional air quality requirements such as California under California Air Resources Board jurisdiction. Manufacturers are responding with advanced after-treatment systems including diesel particulate filters and selective catalytic reduction, alongside improved combustion efficiency technologies that maintain performance while reducing environmental impact. The segment is also seeing innovation in bi-fuel capabilities and renewable diesel compatibility, providing transitional pathways for users seeking to reduce carbon footprints without sacrificing the reliability characteristics that make diesel the industry standard.

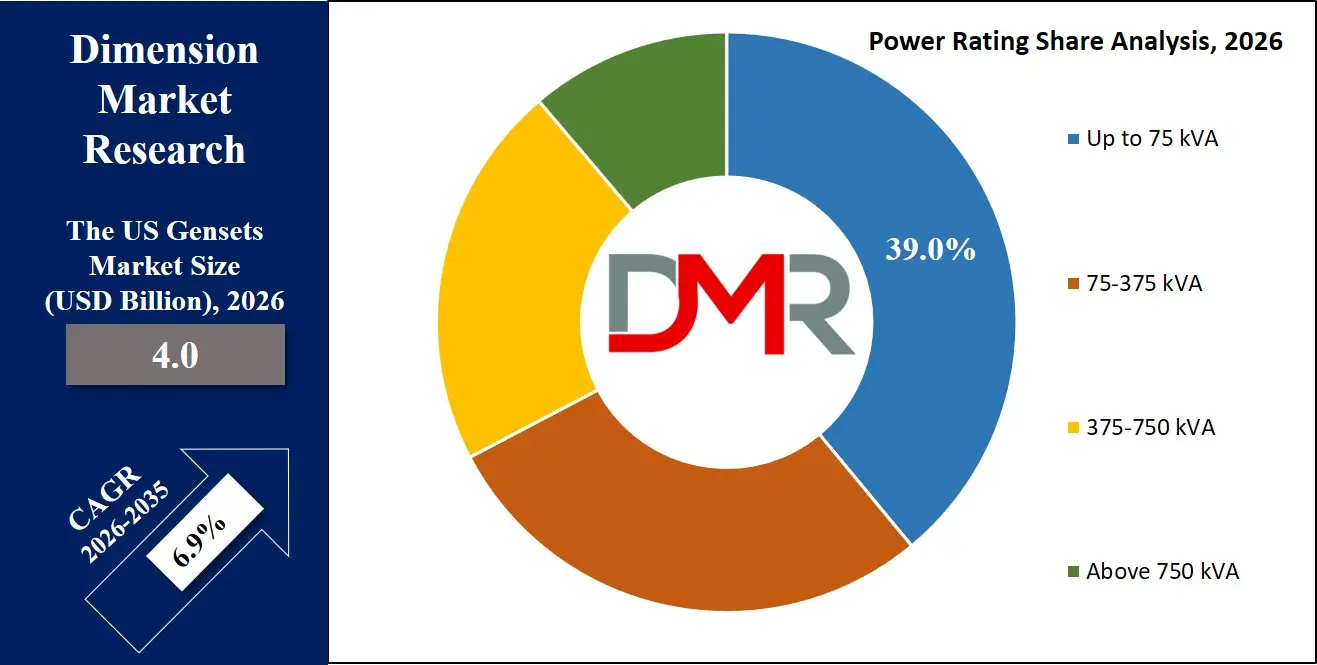

By Power Rating Analysis

High-capacity gensets above 750 kVA represent the most dynamic segment of the United States gensets market, driven by the explosive growth of hyperscale data centers, large-scale industrial facilities, and critical infrastructure protection requirements. The United States is home to the world's largest concentration of data centers, with major markets including Northern Virginia, Dallas-Fort Worth, Silicon Valley, Phoenix, Chicago, and Atlanta experiencing continuous expansion. These facilities require multi-megawatt genset installations, often featuring multiple units operating in parallel with redundant configurations to ensure the highest levels of availability. The above 750 kVA segment also serves large healthcare campuses, semiconductor fabrication plants, advanced manufacturing facilities, and major commercial complexes where power continuity is essential to operations and safety. These high-capacity installations increasingly incorporate sophisticated emissions control systems, parallel switching gear, and integration with building management platforms to meet both regulatory requirements and operational efficiency goals. The segment benefits from the broader trend of industrial reshoring and domestic manufacturing expansion supported by federal infrastructure initiatives and supply chain diversification efforts.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Mid-range gensets spanning the 75 kVA to 750 kVA power band serve as the backbone of commercial backup power infrastructure across the United States, supporting office buildings, retail centers, educational institutions, small to medium manufacturing facilities, and municipal government operations. This versatile segment benefits from consistent replacement cycles driven by building code requirements, insurance mandates, and facility management best practices across commercial real estate. The 75-375 kVA range is particularly prevalent in suburban and urban commercial applications where space constraints and noise considerations demand compact, low-sound enclosures suitable for outdoor installation or rooftop deployment. The 375-750 kVA segment addresses larger commercial buildings, community hospitals, regional data centers, and industrial facilities requiring substantial backup capacity without reaching the scale of hyperscale deployments. Smaller units up to 75 kVA serve residential applications, small businesses, agricultural operations, and telecommunications infrastructure, with growing adoption driven by increasing homeowner awareness of grid vulnerability following extreme weather events.

By Application Analysis

Standby power is expected to constitute as the primary application segment in the United States gensets market, reflecting the critical need for emergency backup across commercial, industrial, and residential sectors facing increasing grid reliability challenges. The United States has experienced a marked increase in weather-related power outages over the past two decades, with hurricanes along the Gulf and Atlantic coasts, wildfires across Western states, winter storms in Texas and the Northeast, and heatwaves placing unprecedented strain on aging grid infrastructure. This trend has elevated standby gensets from optional equipment to essential infrastructure investments across regions previously considered grid-reliable. Regulatory frameworks at federal, state, and local levels mandate standby power for critical facilities including hospitals, emergency services, telecommunications infrastructure, and certain commercial occupancies, creating a stable foundation of demand. The healthcare sector faces the most stringent requirements, with regulations specifying minimum runtime capabilities, automatic transfer switching, regular testing protocols, and fuel supply arrangements to ensure operational readiness during disasters. Financial institutions, data centers, transportation infrastructure including airports and rail systems, and water treatment facilities similarly maintain sophisticated standby power systems.

Prime power applications represent a significant segment serving off-grid industrial operations, remote construction projects, and facilities in regions with inadequate grid infrastructure. The United States energy sector, including oil and gas extraction operations across Texas, North Dakota, and the Gulf of Mexico, relies on prime power gensets for drilling operations, pipeline facilities, and production sites. Large-scale infrastructure projects, including highway construction, renewable energy installations, and industrial facility development, utilize rental gensets for temporary prime power before permanent grid connections are established. Peak shaving applications are gaining traction among industrial and commercial facilities facing complex electricity tariff structures, with operators deploying gensets during periods of peak demand to reduce utility charges and optimize overall energy costs. This application is particularly prevalent among manufacturing facilities in states with demand-based electricity pricing.

By End-User Analysis

Key end-users across the United States gensets market include data centers, healthcare, manufacturing, telecommunications, and residential sectors, each presenting distinct requirements and purchasing drivers that shape market dynamics. The data center segment has emerged as the most demanding and fastest-growing end-user category, driven by the United States' position as the global center of digital infrastructure. Major hyperscale facilities concentrated in Northern Virginia, Dallas-Fort Worth, Silicon Valley, Phoenix, Chicago, Atlanta, and the Pacific Northwest require multi-megawatt genset installations with redundant configurations, extended fuel storage, and sophisticated integration with uninterruptible power supplies and switchgear. These facilities demand the highest levels of reliability, with contractual uptime guarantees requiring fail-safe backup power architectures. The healthcare sector represents an indispensable end-user with stringent regulatory requirements, encompassing hospitals, surgical centers, long-term care facilities, and outpatient clinics across all fifty states. The healthcare segment's backup power requirements have intensified following recent extreme weather events that demonstrated the life-safety implications of grid failures at medical facilities.

The manufacturing sector stands as a foundational end-user, reflecting the United States' diverse industrial base spanning automotive, aerospace, chemical, pharmaceutical, food processing, and semiconductor manufacturing. The semiconductor industry, with fabrication facilities requiring continuous cleanroom operation, demands the highest power reliability standards. The telecommunications sector, undergoing 5G infrastructure expansion and network modernization, represents a growing market for distributed backup solutions across cell towers, data switching centers, and network nodes.

The US Gensets Market Report is segmented on the basis of the following:

By Fuel Type

- Diesel

- Natural Gas

- Propane

By Power Rating

- Up to 75 kVA

- 75-375 kVA

- 375-750 kVA

- Above 750 kVA

By Application

- Standby Power

- Peak Shaving

- Prime/Continuous Power

By End-User

- Construction

- Manufacturing

- Telecom

- Healthcare

- Retail

- Data Centers

- Others

Impact of Artificial Intelligence in the US Gensets Market

- Predictive Maintenance Using AI: AI analyzes operational data, vibration patterns, and thermal signatures to detect potential component failures before they occur, significantly reducing unplanned downtime and extending equipment service life across critical facilities.

- Advanced Energy Optimization: AI-driven platforms optimize fuel consumption and power distribution by analyzing load patterns and grid conditions, automatically adjusting parameters to maximize efficiency and minimize operational costs for diverse applications.

- Integration with Smart Grids: AI enables seamless coordination between gensets, renewable energy systems, and utility grids, creating intelligent microgrids that automatically balance power sources based on real-time demand and availability.

- Remote Monitoring Capabilities: Real-time data analytics platforms leverage AI to continuously assess genset performance across distributed installations, providing operators with actionable insights, automated alerts, and diagnostic recommendations that enhance fleet management.

- Automated Fault Detection: Machine learning algorithms identify subtle anomalies in engine performance, electrical output, and system behavior that human operators might miss, enabling rapid intervention before minor issues escalate into major failures.

The US Gensets Market: Competitive Landscape

The United States gensets market features a highly competitive landscape shaped by the presence of established global manufacturers, specialized domestic players, and a robust rental sector serving diverse end-user requirements. Caterpillar Inc., Cummins Inc., Generac Power Systems, Kohler Energy (rebranded as Rehlko), and Atlas Copco AB represent the dominant forces, collectively accounting for a substantial share of installed capacity across commercial, industrial, and residential applications. Generac holds a particularly strong position in the residential backup segment, leveraging its extensive distribution network and brand recognition to capture significant market share following increased homeowner demand for standby power solutions.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Global multinational corporations including Rolls-Royce Power Systems (MTU), Volvo Penta AB, Deutz AG, and Mitsubishi Heavy Industries compete effectively in high-capacity segments serving data centers, healthcare facilities, and industrial applications where advanced engineering capabilities and global service standards carry significant weight. Aggreko PLC leads the rental segment, providing temporary power solutions for construction projects, large-scale events, and emergency response scenarios across all regions.

Competitive differentiation increasingly centers on emissions compliance with EPA Tier 4 standards, integration capabilities with renewable energy systems and smart grid infrastructure, and advanced digital monitoring platforms. The residential segment has attracted new entrants and expanded product lines as home backup power transitions from regional to nationwide market. Service network strength and parts availability remain critical differentiators, with customers prioritizing rapid response times and long-term maintenance support across geographically dispersed operations.

Some of the prominent players in the US Gensets Market are:

- Caterpillar Inc. (Cat)

- Cummins Inc.

- Generac Power Systems

- Kohler Co. (Rehlko)

- Briggs & Stratton LLC

- Atlas Copco AB

- Rolls-Royce Power Systems (MTU)

- Mitsubishi Heavy Industries

- Yanmar Holdings Co., Ltd.

- Wärtsilä Corporation

- Aggreko PLC

- FG Wilson

- HIMOINSA S.L.

- DEUTZ AG

- ABB Ltd

- AKSA Power Generation

- Perkins Engines Company

- Honda Motor Co., Ltd.

- JCB Power Products

- HITEC Power Protection

- Other Key Players

Recent Developments in the US Gensets Market

- March 2026: Atlas Energy Solutions signed an $840 million agreement with Caterpillar Inc. to procure natural gas generator sets, securing approximately 1.4 GW capacity for data center and energy projects.

- December 2025: Caterpillar Inc. reported strong growth in generator demand driven by AI data centers, with large-scale deployments of gensets for on-site power generation.

- December 2025: Cummins Inc. expanded its genset portfolio by launching high-efficiency models compatible with low-carbon fuels such as HVO, supporting emissions reduction initiatives.

- November 2025: Rising AI-driven electricity demand prompted companies like Caterpillar Inc. and Cummins Inc. to scale up production of modular and gas-powered gensets.

- October 2025: Expansion of data center infrastructure across the U.S. significantly increased procurement of high-capacity gensets, with manufacturers strengthening production and supply chain capabilities.

- August 2025: Caterpillar Inc. launched the Cat D1500 diesel generator set (1.5 MW capacity), targeting large-scale industrial and data center applications with improved efficiency.

- July 2025: Cummins Inc. introduced the Centum Series S17 genset, featuring advanced engine technology and compatibility with renewable fuels.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 4.0 Bn |

| Forecast Value (2035) |

USD 7.3 Bn |

| CAGR (2026–2035) |

6.9% |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors and etc. |

| Segments Covered |

By Fuel Type (Diesel, Natural Gas, Propane), By Power Rating (Up to 75 kVA, 75-375 kVA, 375-750 kVA, Above 750 kVA), By Application (Standby Power, Peak Shaving, Prime/Continuous Power), By End-User (Construction, Manufacturing, Telecom, Healthcare, Retail, Data Centers, Others) |

| Country Coverage |

The US |

| Prominent Players |

Caterpillar Inc. (Cat), Cummins Inc., Generac Power Systems, Kohler Co. (Rehlko), Briggs & Stratton LLC, Atlas Copco AB, Rolls-Royce Power Systems (MTU), Mitsubishi Heavy Industries, Yanmar Holdings Co., Ltd., Wärtsilä Corporation, Aggreko PLC, FG Wilson, HIMOINSA S.L., DEUTZ AG, ABB Ltd, AKSA Power Generation, Perkins Engines Company, Honda Motor Co., Ltd., JCB Power Products, HITEC Power Protection, and Other Key Players |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users), and Corporate Use License (Unlimited User), along with free report customization equivalent to 0 analyst working days, 3 analyst working days, and 5 analyst working days respectively. |

Frequently Asked Questions

How big is the US Gensets Market?

▾ The US Gensets Market size is estimated to have a value of USD 4.0 billion in 2026 and is expected to reach USD 7.3 billion by the end of 2035.

What is the growth rate in the US Gensets Market?

▾ The market is growing at a CAGR of 6.9 percent over the forecasted period of 2026-2035.

Who are the key players in the US Gensets Market?

▾ Some of the major key players in the US Gensets Market are Caterpillar Inc., Cummins Inc., Generac Holdings Inc., Kohler Co., Mitsubishi Heavy Industries, Ltd., Yanmar, Rolls-Royce plc, and many others.