Market Overview

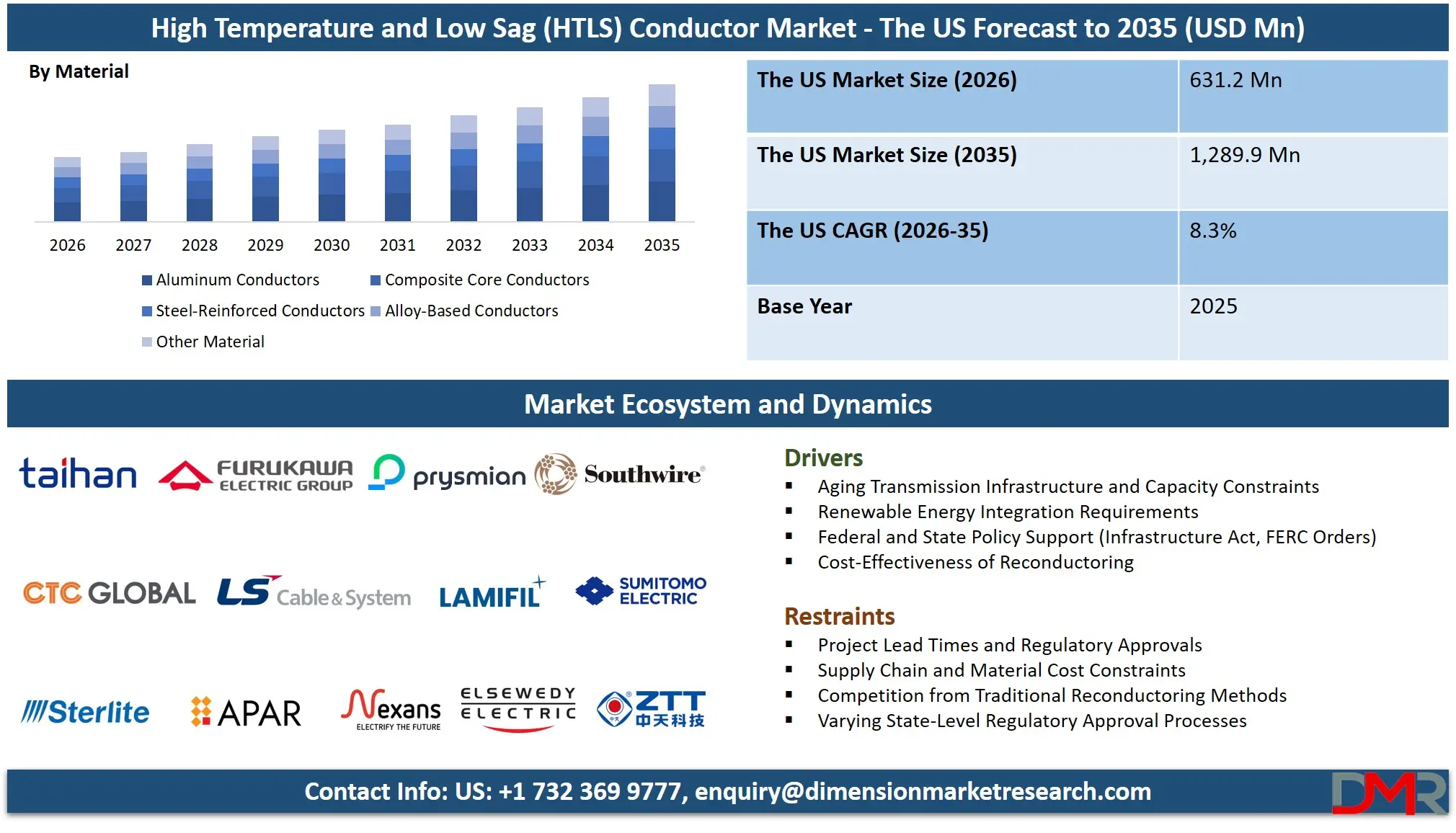

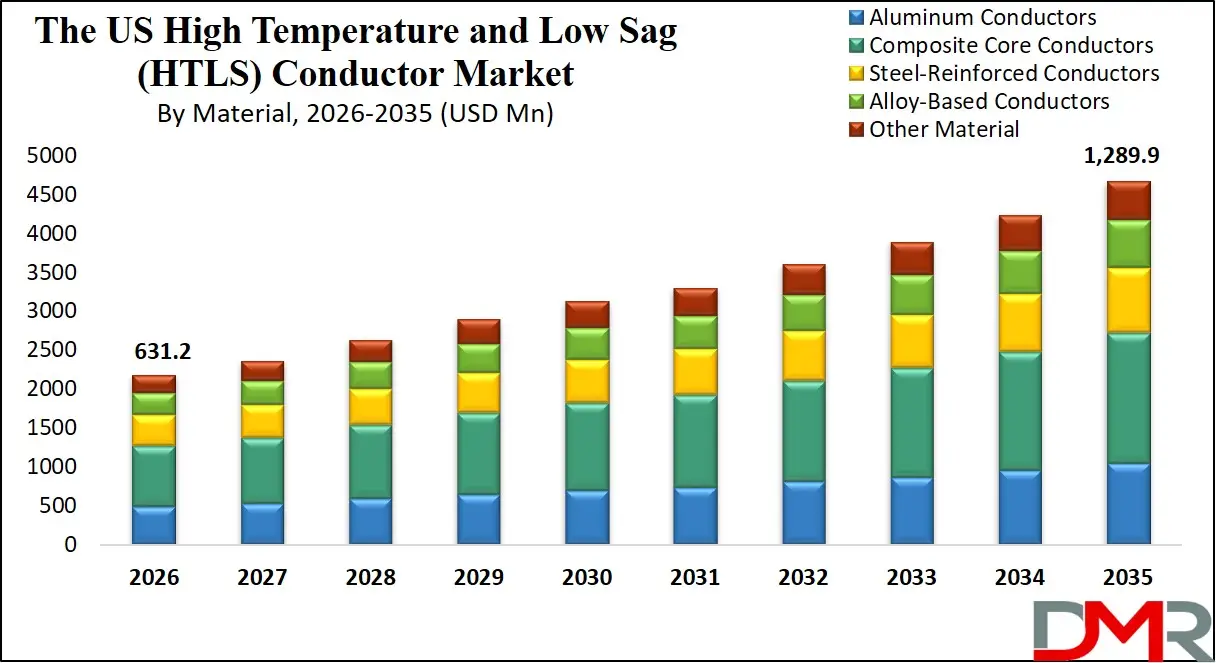

The United States High Temperature and Low Sag (HTLS) Conductor Market is projected to experience strong expansion, reaching an estimated USD 631.2 million in 2026 and forecasted to grow at a CAGR of 8.3% from 2026 to 2035, reaching approximately USD 1,289.9 million by 2035.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The growth of this market is largely driven by grid modernization initiatives, transmission capacity expansion, renewable energy integration, and increasing electricity demand across the U.S. power sector. The United States transmission grid is undergoing significant transformation due to the rapid deployment of utility-scale solar, onshore wind farms, offshore wind developments, battery storage facilities, and electric vehicle charging infrastructure.

A substantial portion of the U.S. Transmission network was constructed between the 1960s and 1980s, and many transmission lines are approaching the end of their design life. As a result, utilities are increasingly adopting HTLS conductors to upgrade transmission capacity without constructing new towers or transmission corridors, making reconductoring a cost-effective grid upgrade strategy.

In addition, regional transmission organizations (RTOs) and independent system operators (ISOs) such as PJM, MISO, ERCOT, and CAISO are facing increasing transmission congestion and interconnection backlogs. Advanced HTLS conductors provide utilities with a viable solution to increase line capacity and improve power transfer efficiency within existing infrastructure.

The integration of renewable energy resources, especially from remote wind and solar zones, further accelerates the adoption of HTLS technologies. Transmission operators are deploying Aluminum Conductor Composite Core (ACCC), Gap-type ACSR, Aluminum Conductor Steel Supported (ACSS), and advanced aluminum alloy conductors to enable higher power flows while maintaining safe clearance limits.

Furthermore, federal policies such as the Infrastructure Investment and Jobs Act (IIJA) and Inflation Reduction Act (IRA) are promoting large-scale investment in grid infrastructure and clean energy systems. These initiatives encourage utilities to modernize transmission networks, improve grid resilience, and expand renewable energy integration.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Despite strong growth prospects, the market faces several challenges, including high upfront installation costs, regulatory permitting delays, supply chain constraints for advanced composite materials, and competition from conventional reconductoring approaches.

Nevertheless, continuous innovation in advanced conductor materials, composite core technologies, dynamic line rating systems, and digital grid monitoring solutions is expected to strengthen the role of HTLS conductors in the modernization of the U.S. Transmission infrastructure.

Impact of Iran War on the U.S. High Temperature and Low Sag (HTLS) Conductor Market

- Volatility in Aluminum and Raw Material Prices: HTLS conductors primarily use aluminum and specialized alloy materials. Geopolitical tensions in the Middle East can disrupt global metal supply chains and create price volatility. Rising aluminum prices increase the manufacturing cost of HTLS conductors, which may raise project costs for utilities upgrading transmission lines.

- Supply Chain and Logistics Disruptions: Conflict in the Middle East can affect key shipping routes used for transporting metals and industrial materials. Delays in international shipping and higher freight costs can impact the availability of raw materials used in conductor manufacturing, potentially slowing transmission infrastructure projects.

- Increased Energy and Manufacturing Costs: Wars in major oil-producing regions often cause increases in global oil and energy prices. Since aluminum smelting and conductor production are energy-intensive processes, higher energy costs can increase production expenses for HTLS conductor manufacturers.

- Greater Focus on Grid Security and Infrastructure Investment: Geopolitical instability can encourage governments and utilities to strengthen domestic energy security. This may lead to increased investment in transmission infrastructure upgrades and grid modernization projects in the United States, which can support long-term demand for HTLS conductors.

The US High Temperature and Low Sag (HTLS) Conductor Market: Key Takeaways

- Strong U.S. Market Growth Outlook: the U.S. HTLS Conductor Market is expected to be valued at USD 631.2 million in 2026 and is projected to reach USD 1,289.9 million by 2035, showcasing rapid expansion supported by rising demand for grid modernization and transmission capacity upgrades.

- Steady CAGR Driven by Renewable Integration: the market is expected to grow at a steady CAGR of 8.3% from 2026 to 2035, fueled by accelerating renewable energy development, grid interconnection requirements, and increasing transmission congestion across the U.S.

- Aluminum Conductor Composite Core (ACCC) to Dominate Conductor Type Segment: ACCC is projected to hold the largest market share due to its superior strength-to-weight ratio, near-zero thermal expansion, and ability to increase transmission capacity by 30-100% without structural tower modifications, making it the preferred choice for constrained transmission corridors.

- Grid Reconductoring/Capacity Upgrade Leads Application Segment: This application dominates market revenue, driven by the need to maximize existing rights-of-way, avoid lengthy greenfield permitting, and accelerate capacity addition timelines for renewable integration and load growth requirements.

- Electric Utilities Dominate End-Use Industry Segment: Investor-owned utilities, public power authorities, and electric cooperatives account for the majority of HTLS procurement, driven by regulatory compliance, reliability mandates, and renewable portfolio standard obligations.

- Growing Grid Constraints Boost Adoption: Rising transmission congestion, delayed interconnection queues, and the need for cost-effective capacity expansion, coupled with limited new transmission corridor development, is driving sustained demand for HTLS reconductoring solutions.

The US High Temperature and Low Sag (HTLS) Conductor Market: Use Cases

- Renewable Energy Zone Interconnection: Transmission developers in wind-rich regions (e.g., MISO, SPP) and solar development areas (e.g., CAISO, ERCOT) utilize HTLS conductors to connect utility-scale renewable projects to constrained transmission networks.

- Urban Grid Capacity Upgrades: Metropolitan utilities reconductor existing transmission lines entering load centers with HTLS conductors to serve growing urban electricity demand without acquiring new right-of-way.

- Wildfire Mitigation Reconductoring: California utilities (e.g., PG&E, SCE) deploy HTLS conductors with enhanced thermal performance and reduced sag to increase clearance and reduce ignition risk in high fire-threat districts.

- Interregional Transmission Expansion: Regional transmission organizations reconductor critical interties with HTLS technology to increase power transfer capability between balancing authorities and enhance grid reliability.

- Industrial Load Serving: Oil & gas operations, mining facilities, and large industrial complexes utilize dedicated HTLS transmission feeds to support electrification and capacity expansion requirements.

The US High Temperature and Low Sag (HTLS) Conductor Market: Stats & Facts

U.S. Energy Information Administration (EIA)

- The United States experiences approximately 5% electricity losses during transmission and distribution annually.

- Total U.S. electricity generation exceeded 4,000 terawatt-hours (TWh) in 2023, increasing demand on transmission infrastructure.

- The U.S. electric power sector delivered electricity to over 160 million customers nationwide.

- Electricity demand in the United States increased by approximately 2% in 2023, placing additional pressure on the transmission grid.

- Renewable energy accounted for around 30% of total U.S. electricity generation in 2023.

U.S. Department of Energy (DOE)

- The United States has over 700,000 miles of high-voltage transmission lines connecting generation facilities to consumers.

- More than 70% of the U.S. Transmission infrastructure is over 25 years old and requires modernization.

- Transmission investment requirements in the United States are expected to reach hundreds of billions of dollars by 2035 to support grid expansion and renewable energy integration.

- Grid modernization initiatives are increasingly focusing on reconductoring existing lines instead of building new corridors.

- Electricity demand from data centers and artificial intelligence computing facilities is expected to grow significantly over the next decade.

Federal Energy Regulatory Commission (FERC)

- The United States transmission network includes hundreds of regional transmission operators and independent system operators managing interstate electricity flow.

- Grid congestion in the U.S. Transmission system costs electricity consumers billions of dollars annually.

- Interconnection queues in regional grid operators contain thousands of renewable energy projects awaiting connection to the grid.

- Large-scale transmission projects typically require several years of regulatory approval and planning.

- Transmission expansion projects in the U.S. increasingly prioritize capacity upgrades within existing corridors.

Electric Power Research Institute (EPRI)

- Advanced conductors such as HTLS can increase transmission capacity by up to 2.5 times compared with conventional conductors.

- HTLS conductors significantly reduce sag under high temperature conditions, improving safety clearances.

- Reconductoring using advanced conductors can increase transmission efficiency without replacing existing towers.

- HTLS conductors allow transmission lines to operate at temperatures above 150°C while maintaining structural integrity.

- Upgrading transmission lines with advanced conductors can reduce the need for new transmission corridor construction.

International Energy Agency (IEA)

- Around 1,500 GW of renewable energy projects in the United States are waiting for grid connection approvals.

- Electricity consumption globally is projected to grow by nearly 3% annually through the mid-2020s.

- Renewable energy capacity additions globally reached record levels in recent years, increasing transmission expansion needs.

- Wind and solar power projects are often located far from demand centers, requiring long-distance transmission infrastructure.

- Transmission upgrades are considered one of the most critical enablers for global energy transition.

U.S. Environmental Protection Agency (EPA)

- Approximately 5% of electricity generated in the United States is lost during transmission and distribution processes.

- Improving grid efficiency and reducing transmission losses can significantly reduce overall greenhouse gas emissions.

- Modern transmission technologies contribute to improved energy efficiency across the power system.

- Advanced transmission infrastructure helps support clean energy deployment and grid reliability.

- Transmission system improvements play an important role in achieving national climate and energy efficiency targets.

The US High Temperature and Low Sag (HTLS) Conductor Market: Market Dynamic

Driving Factors in the U.S. High Temperature and Low Sag (HTLS) Conductor Market

Aging Transmission Infrastructure and Capacity Constraints

The growing need to address aging grid infrastructure and transmission capacity limitations is a major driver for HTLS conductor adoption. Much of the U.S. high-voltage transmission system was constructed in the 1960s-1980s and requires significant upgrades to serve modern electricity demands. HTLS conductor systems that provide higher ampacity without requiring tower replacements or new right-of-way acquisition offer a cost-effective solution. This allows utilities to maximize existing infrastructure assets while improving reliability and serving load growth, especially in constrained urban and renewable-rich regions.

Renewable Energy Integration Requirements

HTLS conductor adoption benefits heavily from federal and state renewable energy targets and transmission planning policies like FERC Order No. 2023 and state RPS mandates. These policies legally require grid operators to accommodate increasing renewable generation, making transmission capacity expansion not just an operational improvement but a compliance necessity. The ability to reconductor existing lines with HTLS technology provides an accelerated path to increase transfer capability from renewable energy zones to load centers, avoiding lengthy greenfield transmission development timelines.

Restraints in the U.S. High Temperature and Low Sag (HTLS) Conductor Market

Project Lead Times and Regulatory Approvals

The significant challenge of navigating state-level siting and permitting processes creates friction for HTLS deployment. Achieving project approval requires coordination with multiple state public utility commissions, environmental agencies, and local stakeholders, which can be inconsistent across jurisdictions. In many regions, permitting timelines can extend project schedules, delaying capacity benefits and potentially impacting renewable integration deadlines.

Supply Chain and Material Cost Constraints

Supply chain limitations for specialized materials, particularly advanced composite cores and high-temperature alloys, create procurement challenges. Global demand for carbon fiber and specialized aluminum alloys can lead to extended lead times and price volatility. Domestic manufacturing capacity for certain HTLS conductor types remains limited, creating dependence on international suppliers and potentially delaying projects.

Opportunities in the U.S. High Temperature and Low Sag (HTLS) Conductor Market

Expansion into Transmission Interconnection Queues

The massive backlog of generation and storage projects in interconnection queues represents a major growth opportunity for HTLS conductors. Over 1,400 GW of capacity awaiting interconnection creates substantial demand for transmission capacity solutions. Targeted reconductoring of constrained transmission paths serving interconnection study areas can accelerate project timelines and reduce queue backlogs, creating value for both renewable developers and grid operators.

Grid-Enhancing Technologies (GETs) Integration

The integration of HTLS conductors with dynamic line rating (DLR) systems, advanced grid monitoring, and transmission operations software creates new value streams. Combined deployment enables real-time ampacity optimization, condition-based maintenance, and enhanced situational awareness. This transforms HTLS from a passive infrastructure component into an intelligent, adaptive grid asset that maximizes throughput and continuously improves operational efficiency.

Trends in the U.S. High Temperature and Low Sag (HTLS) Conductor Market

Composite Core Conductor Adoption

The rise of Aluminum Conductor Composite Core (ACCC) and similar composite core technologies is gaining significant traction. These conductors utilize lightweight, high-strength carbon/glass fiber cores that enable higher operating temperatures with minimal sag. This trend leverages advanced materials science to provide superior thermal performance and lower line losses compared to conventional steel-reinforced conductors, becoming increasingly specified for high-capacity reconductoring projects.

Gap-Type Conductor Deployment

Gap-type ACSR (G(Z)ACSR) conductors are experiencing increased deployment for applications requiring high-temperature operation with existing tower structures. The design features a gap between the steel core and aluminum layers filled with high-temperature grease, allowing the conductor to expand independently and maintain sag characteristics at elevated temperatures. This trend supports utilities seeking proven, cost-effective HTLS solutions with established manufacturing bases and utility acceptance.

The US High Temperature and Low Sag (HTLS) Conductor Market: Research Scope and Analysis

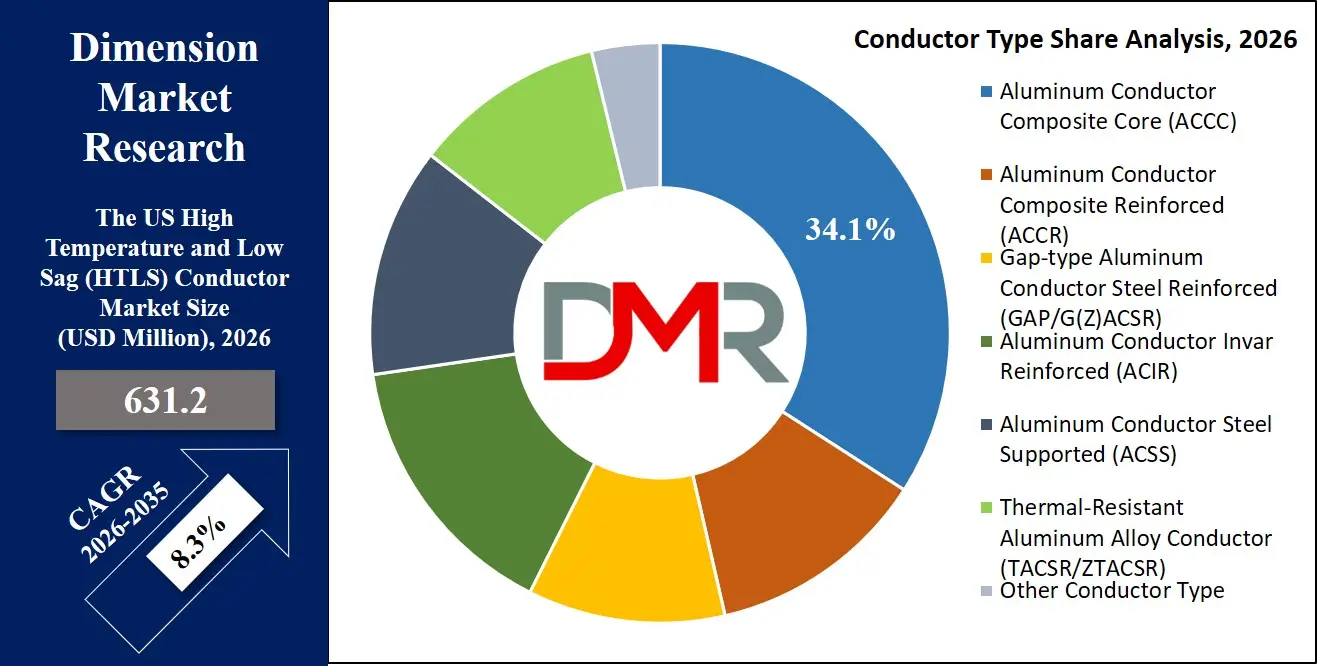

By Conductor Type Analysis

The Aluminum Conductor Composite Core (ACCC) segment is projected to dominate the U.S. HTLS Conductor Market, accounting for 34.1% of share in 2026 highest compared to other conductor types. This dominance is primarily driven by the growing need for high-capacity, low-sag conductors that maximize transmission capacity without structural modifications to existing towers. Utilities across renewable-rich regions, urban load centers, and constrained transmission corridors require advanced composite core conductors capable of operating at elevated temperatures while maintaining critical ground clearance.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Modern ACCC conductors provide advanced capabilities such as high-temperature operation (up to 180°C), a coefficient of thermal expansion approximately 1/10th of steel, and reduced line losses compared to conventional conductors. These features significantly increase power transfer capability by 30-100% on existing rights-of-way while improving grid efficiency. Transmission planners prefer composite core solutions that offer lightweight construction, corrosion resistance, and long-term reliability for capacity-constrained applications.

Additionally, the shift toward accelerated reconductoring to address interconnection queue backlogs has increased reliance on high-performance conductor technologies. Utility procurement programs and transmission expansion budgets further strengthen the ACCC segment's dominance, as companies can deploy solutions with established field performance and manufacturer technical support.

While Gap-type ACSR (GAP/G(Z)ACSR) and Aluminum Conductor Steel Supported (ACSS) conductors maintain significant market positions for specific applications, ACCC continues to lead due to superior sag performance and capacity enhancement capabilities. As renewable integration accelerates and transmission constraints intensify across the U.S., the ACCC segment is expected to maintain its leadership position due to continuous material innovation and proven reconductoring applications.

By Material Analysis

Composite core materials are expected to dominate the material segment with 36.1% of market share in 2026, due to their superior strength-to-weight ratio, thermal stability, and sag reduction characteristics. Utilities increasingly prefer composite core conductors for high-capacity applications because they enable significant ampacity increases while minimizing structural loading on existing towers. As transmission owners expand capacity across multiple regions, composite materials enable reliable high-temperature operation without tower reinforcement or replacement.

Composite core-based solutions allow maximum thermal ratings with minimal thermal sag, supporting high transfer capability across constrained transmission paths. They support high-temperature continuous operation, reduced line losses, and compatibility with existing hardware. This is particularly beneficial for renewable energy zones, urban load centers, and interregional transmission paths handling high utilization rates.

Another major advantage of composite core materials is their ability to resist corrosion, reduce ice loading concerns, and provide long-term durability in diverse environmental conditions. These features enhance transmission reliability while minimizing maintenance requirements. The favorable economics of capacity gain per dollar invested further supports adoption among utilities and transmission developers, accelerating overall market penetration.

Although steel-reinforced and alloy-based conductors remain relevant for specific voltage levels and applications, their adoption for high-performance HTLS applications is comparatively limited due to higher sag at elevated temperatures. As capacity requirements increase and utilities prioritize infrastructure optimization, composite core materials continue to lead the market and are projected to maintain dominance over the forecast period.

By Voltage Level Analysis

High Voltage (HV) transmission applications are anticipated to dominate the voltage level segment due to their prevalence in the bulk transmission network and critical role in renewable energy delivery. These voltage levels (typically 115 kV to 230 kV) represent the backbone of the regional transmission system, connecting generation resources to load centers and interconnecting balancing authorities.

HTLS deployment at HV levels remains popular because it delivers substantial capacity increases on existing rights-of-way with well-understood engineering practices. It is extensively used by investor-owned utilities, transmission companies, and regional transmission organizations for reconductoring aging lines and increasing transfer capability between renewable zones and load centers. Extra High Voltage (EHV) applications strengthen transmission capacity by adding capacity on major interties and bulk power export paths, significantly reducing congestion and enabling interregional power transfers.

Regulatory requirements in transmission planning processes and cost allocation methodologies across various regions further drive adoption of HTLS at HV and EHV levels. As renewable development accelerates and interregional transfers increase, utilities are prioritizing high-capacity conductor technologies at these voltage levels to combat transmission constraints and interconnection delays.

Although medium voltage distribution applications are growing with distributed generation integration, HV and EHV applications continue to dominate because of their direct impact on bulk transmission capacity and regional congestion relief. Their widespread deployment across interconnection-wide transmission expansion ensures continued leadership in this segment.

By Application Analysis

Grid reconductoring and capacity upgrade applications are forecasted to dominate the application segment, driven by the growing need to enhance existing transmission infrastructure without greenfield development. With limited new transmission corridor availability, right-of-way acquisition challenges, and lengthy permitting processes, utilities rely heavily on HTLS reconductoring to increase capacity on existing rights-of-way.

Transmission owners utilize HTLS reconductoring to upgrade constrained lines, replace aging conductors, and interconnect renewable generation without building new transmission lines. Regional transmission organizations leverage reconductoring programs to increase transfer capability between balancing authorities and relieve transmission congestion. Similarly, renewable generators utilize reconductoring to accelerate interconnection timelines for queued projects.

Capacity upgrades have become increasingly important as interconnection queues swell with renewable and storage projects seeking grid access. HTLS reconductoring provides a critical pathway to increase throughput on transmission paths serving interconnection study areas without initiating new greenfield transmission proceedings.

Although renewable energy grid integration and new power transmission applications are growing, reconductoring and capacity upgrades remain the primary revenue drivers. As the U.S. pursues ambitious renewable deployment targets, this segment will continue to dominate due to its direct role in enabling cost-effective, timely transmission capacity expansion.

By End-Use Industry Analysis

The electric utilities sector is expected to dominate the end-use segment due to its ownership and operation of the majority of U.S. Transmission infrastructure. Investor-owned utilities, public power authorities, and electric cooperatives require substantial transmission capacity upgrades to serve load growth, integrate renewable resources, and maintain reliability.

State renewable portfolio standards, regional transmission planning requirements, and federal transmission incentive policies require electric utilities to implement comprehensive grid modernization programs. The rise of utility-scale renewable procurement and utility commitments to decarbonization targets has further accelerated demand for HTLS conductor deployment on utility-owned transmission assets.

Independent transmission companies and project developers also rely on HTLS technologies to develop merchant transmission projects and generator interconnection facilities. Given the high capital intensity and reliability requirements associated with transmission infrastructure, electric utilities allocate significant budgets toward conductor technologies that maximize asset utilization and regulatory compliance.

While renewable energy developers, oil & gas operators, and transportation authorities also contribute to market demand, electric utilities remain the largest revenue contributor due to their extensive transmission asset base and mandatory service obligations.

The US High Temperature and Low Sag (HTLS) Conductor Market Report is segmented on the basis of the following:

By Conductor Type

- Aluminum Conductor Composite Core (ACCC)

- Aluminum Conductor Composite Reinforced (ACCR)

- Gap-type Aluminum Conductor Steel Reinforced (GAP/G(Z)ACSR)

- Aluminum Conductor Invar Reinforced (ACIR)

- Aluminum Conductor Steel Supported (ACSS)

- Thermal-Resistant Aluminum Alloy Conductor (TACSR/ZTACSR)

- Other Conductor Type

By Material

- Aluminum Conductors

- Composite Core Conductors

- Steel-Reinforced Conductors

- Alloy-Based Conductors

- Other Material

By Voltage Level

- Low Voltage (LV)

- Medium Voltage (MV)

- High Voltage (HV)

- Extra High Voltage (EHV)

By Application

- Power Transmission

- Power Distribution

- Renewable Energy Grid Integration

- Grid Reconductoring / Capacity Upgrade

- Other Application

By End-Use Industry

- Electric Utilities

- Renewable Energy Integration

- Oil & Gas

- Mining & Metal Processing

- Railways & Transportation

- Other End-Use Industry

Impact of Artificial Intelligence in the US High Temperature and Low Sag (HTLS) Conductor Market

- Advanced Composites for Core Materials: Carbon fiber and glass fiber composite cores provide exceptional strength-to-weight ratios and near-zero thermal expansion, enabling significantly higher operating temperatures with minimal sag compared to traditional steel cores.

- High-Temperature Aluminum Alloys: Heat-resistant aluminum-zirconium alloys maintain mechanical strength at continuous operating temperatures up to 210°C, allowing substantial ampacity increases without conductor degradation.

- Gap-Type Conductor Engineering: Innovative gap designs between steel core and aluminum strands filled with high-temperature grease allow independent thermal expansion, maintaining sag performance at elevated temperatures.

- Corrosion-Resistant Coating Technologies: Advanced coating systems and core materials provide enhanced resistance to corrosion in coastal, industrial, and high-pollution environments, extending service life and reducing maintenance requirements.

- Computational Modeling for Conductor Design: Finite element analysis and thermal modeling optimize conductor stranding geometry, core configuration, and material selection for specific application requirements and operating conditions.

The US High Temperature and Low Sag (HTLS) Conductor Market: Competitive Landscape

The U.S. HTLS Conductor Market is moderately consolidated, featuring a mix of global cable manufacturers, specialized conductor technology providers, and materials science companies. Leading players like Southwire Company, LS Cable & System, and Nexans leverage their extensive manufacturing capabilities and utility relationships to offer HTLS conductors as core transmission products. Pure-play HTLS innovators such as CTC Global (ACCC conductor) and 3M (ACCR conductor, now discontinued new sales) have driven market dynamics with specialized, high-performance composite core technologies.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Traditional cable manufacturers like General Cable (acquired by Prysmian), Midal Cables, and ZTT International Limited play a crucial role as tier-1 suppliers, while materials science companies such as Toray Industries (carbon fiber) provide critical raw materials for composite core production. Regional players and domestic manufacturers are also active, serving specific utility procurement requirements and project specifications.

Some of the prominent players in the US High Temperature and Low Sag (HTLS) Conductor Market are:

- Southwire Company, LLC

- CTC Global Corporation

- LS Cable & System Ltd.

- Nexans S.A.

- Prysmian S.p.A.

- Midal Cables Ltd.

- ZTT International Limited

- Lamifil N.V.

- Hengtong Group

- Sumitomo Electric Industries, Ltd.

- Fujikura Ltd.

- Furukawa Electric Co., Ltd.

- AFL

- Walsin Lihwa Corporation

- Eland Cables

- APAR Industries Limited

- Sterlite Power

- Taihan Electric Wire Co., Ltd.

- KEC International Limited

- Kalpataru Power Transmission Limited

- Other Key Players

Recent Developments in the US High Temperature and Low Sag (HTLS) Conductor Market

- April 2025: Prysmian Group announced the acquisition of Encore Wire Corporation for approximately USD 4.15 billion, strengthening Prysmian's manufacturing and distribution capabilities in the United States and expanding its portfolio of power transmission conductors supporting grid modernization and renewable energy integration projects.

- March 2025: Southwire Company, LLC presented its advanced transmission conductor technologies at major U.S. power grid modernization conferences, highlighting the use of HTLS conductors to increase transmission capacity and reduce congestion in aging transmission infrastructure.

- January 2025: CTC Global Corporation, developer of ACCC® composite-core conductors, expanded collaboration with U.S. utilities and transmission planners to promote ACCC HTLS conductor deployment for reconductoring projects aimed at increasing transmission capacity without constructing new towers.

- September 2024: Nexans S.A. supplied advanced overhead conductors for transmission network upgrade projects supporting renewable energy integration and higher-capacity transmission infrastructure across North America.

- July 2024: Sumitomo Electric Industries Ltd. supported utilities with high-temperature conductor solutions designed to improve ampacity and reduce sag on existing transmission lines as part of grid reliability improvement programs.

- May 2024: LS Cable & System Ltd. partnered with regional electric utilities and transmission developers to demonstrate high-capacity overhead conductors for renewable energy transmission corridors.

- March 2024: Sterlite Power promoted HTLS conductor technologies for high-capacity transmission lines during infrastructure development programs and industry forums focusing on renewable energy grid integration.

- January 2024: Lamifil NV collaborated with engineering research institutions and transmission utilities to evaluate high-temperature conductor materials and performance characteristics for next-generation power transmission networks.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 631.2 Mn |

| Forecast Value (2035) |

USD 1,289.9 Mn |

| CAGR (2026–2035) |

8.3% |

| Historical Data |

2020 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors and etc. |

| Segments Covered |

By Conductor Type (Aluminum Conductor Composite Core (ACCC), Aluminum Conductor Composite Reinforced (ACCR), Gap-type Aluminum Conductor Steel Reinforced (GAP/G(Z)ACSR), Aluminum Conductor Invar Reinforced (ACIR), Aluminum Conductor Steel Supported (ACSS), Thermal-Resistant Aluminum Alloy Conductor (TACSR/ZTACSR), Other Conductor Type), By Material (Aluminum Conductors, Composite Core Conductors, Steel-Reinforced Conductors, Alloy-Based Conductors, Other Material), By Voltage Level (Low Voltage (LV), Medium Voltage (MV), High Voltage (HV), Extra High Voltage (EHV)), By Application (Power Transmission, Power Distribution, Renewable Energy Grid Integration, Grid Reconductoring / Capacity Upgrade, Other Application), and By End-Use Industry (Electric Utilities, Renewable Energy Integration, Oil & Gas, Mining & Metal Processing, Railways & Transportation, Other End-Use Industry). |

| Country Coverage |

The US |

| Prominent Players |

Southwire Company, LLC, CTC Global Corporation, LS Cable & System Ltd., Nexans S.A., Prysmian S.p.A., Midal Cables Ltd., ZTT International Limited, Lamifil N.V., Hengtong Group, Sumitomo Electric Industries, Ltd., Fujikura Ltd., Furukawa Electric Co., Ltd., AFL, Walsin Lihwa Corporation, Eland Cables, APAR Industries Limited, Sterlite Power, Taihan Electric Wire Co., Ltd., KEC International Limited, Kalpataru Power Transmission Limited, and Other Key Players. |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users) and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days and 5 analysts working days respectively. |

Frequently Asked Questions

How big is the U.S. High Temperature and Low Sag (HTLS) Conductor Market?

▾ The U.S. HTLS Conductor Market size is estimated to have a value of USD 631.2 million in 2026 and is expected to reach USD 1,289.9 million by the end of 2035.

What is the growth rate in the U.S. High Temperature and Low Sag (HTLS) Conductor Market?

▾ The market is growing at a CAGR of 8.3 percent over the forecasted period of 2026-2035.

Who are the key players in the U.S. High Temperature and Low Sag (HTLS) Conductor Market?

▾ Some of the major key players in the U.S. HTLS Conductor Market are Southwire Company, CTC Global Corporation, LS Cable & System, Nexans, Prysmian, Midal Cables, and many others.