What is the Intracranial Hemorrhage Diagnosis & Treatment Market Size?

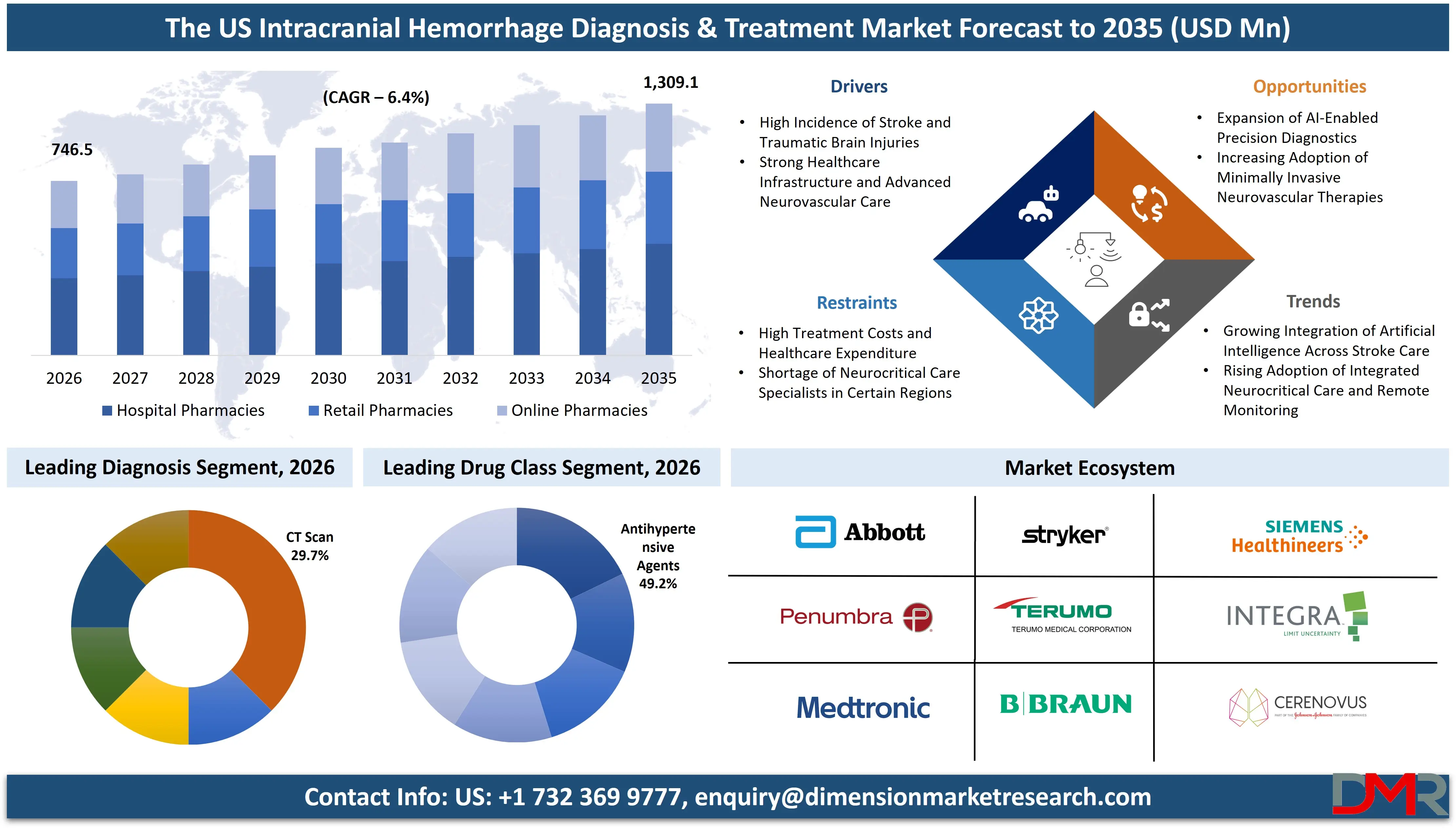

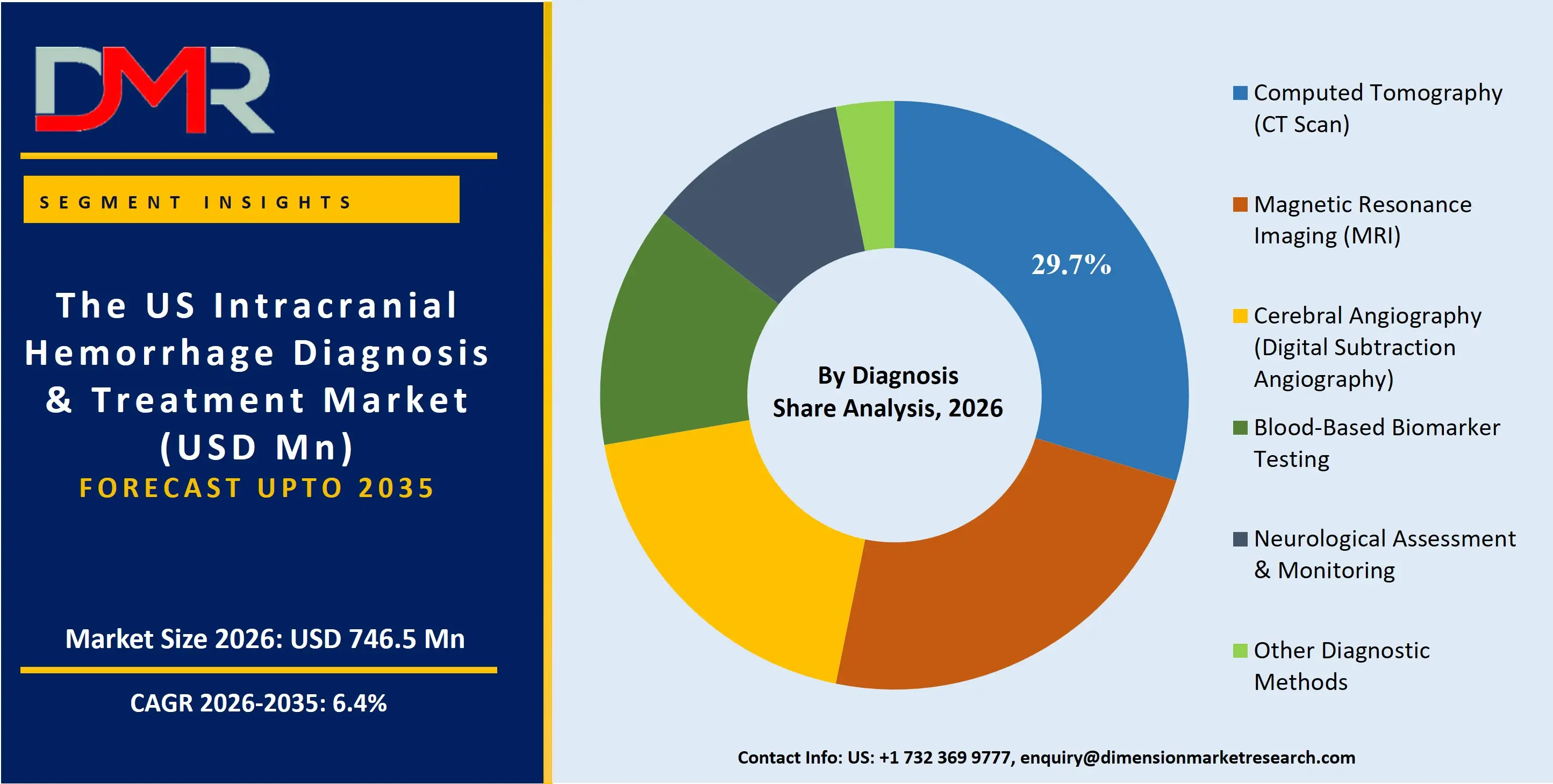

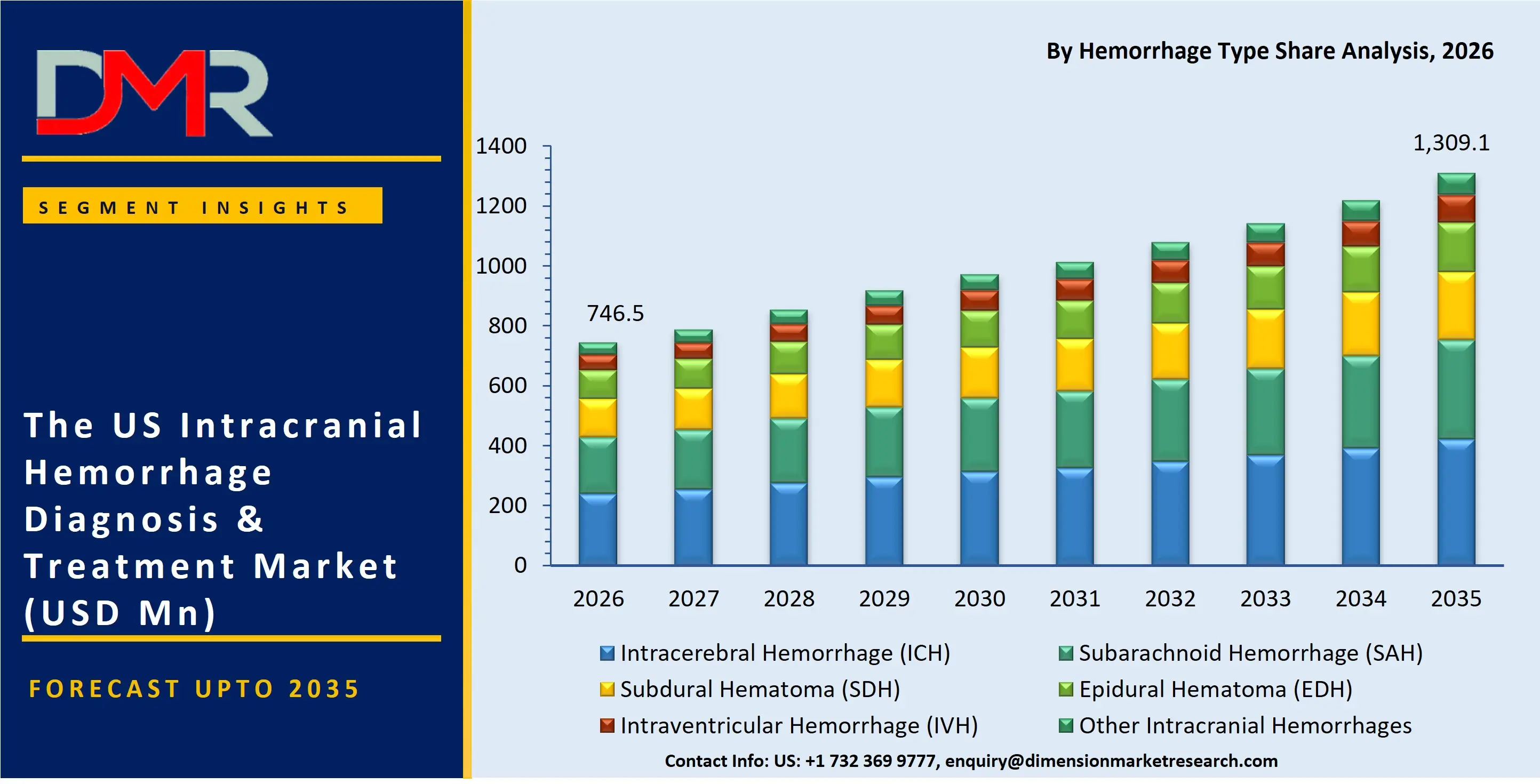

The US Intracranial Hemorrhage Diagnosis & Treatment Market is projected to be valued at USD 746.5 million in 2026 and is expected to reach USD 1,309.1 million by 2035, growing at a CAGR of 6.4% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The market for intracranial hemorrhage (ICH) management in the United States is experiencing robust growth, driven by an aging demographic susceptible to cerebrovascular events and the rapid adoption of technologically advanced diagnostic and minimally invasive surgical interventions. The market encompasses a comprehensive spectrum of care, from emergency neuroimaging and biomarker-based diagnostics to sophisticated pharmacological reversal agents and life-saving neurosurgical procedures like endovascular coiling and minimally invasive hematoma evacuation. The rising incidence of hypertension-related intracerebral hemorrhage and traumatic brain injuries, coupled with breakthroughs in neurocritical care, are primary catalysts. The clinical landscape is dominated by the integration of precision diagnostics with targeted therapeutic modalities to mitigate neuronal damage and improve functional outcomes.

Key Takeaways

- Market Size & Forecast: The US intracranial hemorrhage diagnosis and treatment market is forecast to expand from USD 746.5 million in 2026 to USD 1,309.1 million by 2035, fueled by a high prevalence of hypertension, widespread anticoagulant use, and the consolidation of advanced stroke care systems.

- Growth Rate & Outlook: A CAGR of 6.4% will be sustained by critical growth drivers, including a paradigm shift toward minimally invasive surgical evacuation, the development of novel hemostatic agents, and the integration of artificial intelligence in diagnostic imaging for faster triage.

- Primary Growth Drivers: The market is propelled by the increasing burden of hemorrhagic stroke in an aging population, regulatory approvals for reversal agents targeting direct oral anticoagulants (DOACs), and continuous advancements in neuroendovascular devices such as flow diverters and intrasaccular devices for aneurysm management.

- Key Market Trends: Dominant trends include the clinical validation of blood-based biomarkers (GFAP, UCH-L1) for rapid hemorrhage detection, the transition from open craniotomy to endoscopic and stereotactic aspiration techniques, and a growing focus on bundled neurocritical care protocols that integrate early rehabilitation.

- By Diagnosis Analysis: Non-contrast Computed Tomography (CT) remains the cornerstone diagnostic tool due to its speed and ubiquity in emergency settings. However, CT Angiography (CTA) and MRI with susceptibility-weighted imaging (SWI) are gaining traction for identifying underlying vascular malformations and microbleeds, crucial for secondary prevention.

- By Treatment Analysis: Surgical treatment is poised to dominate the surgical landscape, offering reduced operative morbidity compared to standard craniotomy. Concurrently, anticoagulation reversal therapy is the fastest-growing pharmacological segment, anchored by the clinical necessity to rapidly correct coagulopathy in warfarin- and DOAC-associated hemorrhages.

What is the Intracranial Hemorrhage Diagnosis & Treatment?

Intracranial hemorrhage refers to a critical, life-threatening condition characterized by spontaneous or traumatic bleeding within the cranial vault, encompassing intraparenchymal, subarachnoid, subdural, and epidural compartments. Unlike ischemic stroke management, the therapeutic window for ICH demands immediate diagnosis via non-contrast CT to differentiate hemorrhage from ischemia, followed by aggressive blood pressure control and coagulopathy correction to halt hematoma expansion. The treatment paradigm is bimodal: pharmacological strategies involve intensive antihypertensive therapy and hemostatic or reversal agents, while surgical interventions range from external ventricular drainage (EVD) for hydrocephalus to decompressive craniectomy for malignant cerebral edema. In the US, care is highly protocolized, transitioning from rapid emergency department triage to dedicated neurological intensive care units (Neuro-ICUs) that emphasize neuromonitoring and early mobilization.

Use Cases

- Hypertensive Intracerebral Hemorrhage Management: Tertiary care hospitals employ non-contrast CT for immediate diagnosis, followed by aggressive blood pressure management using intravenous antihypertensives and, in select cases, minimally invasive stereotactic aspiration to evacuate deep-seated hematomas.

- Aneurysmal Subarachnoid Hemorrhage Repair: Specialized neurovascular centers utilize CT angiography for initial detection, subsequently transitioning patients to cerebral angiography suites for endovascular coiling or flow diversion to secure the ruptured aneurysm and prevent rebleeding.

- Traumatic Subdural Hematoma Evacuation: Trauma centers diagnose acute subdural hematoma via CT, with surgical teams performing urgent decompressive craniectomy or craniotomy to relieve mass effect and manage intracranial pressure.

- Anticoagulation-Related Hemorrhage Reversal: Hospital pharmacies and emergency departments rapidly deploy specific reversal agents, such as idarucizumab for dabigatran or andexanet alfa for factor Xa inhibitors, to restore hemostatic integrity in patients presenting with life-threatening hemorrhages.

How AI is Transforming the Intracranial Hemorrhage Diagnosis & Treatment Market?

Artificial intelligence is revolutionizing the US intracranial hemorrhage market by significantly compressing the "door-to-treatment" timeline through advanced image analysis. AI-driven triage software embedded in CT scanners can automatically detect acute intracranial hemorrhages, including subtle subdural and subarachnoid bleeds, and escalate these cases to the top of radiologists' worklists, drastically reducing diagnostic delays. Beyond detection, machine learning algorithms are being developed to predict hematoma expansion by analyzing non-contrast CT texture features, guiding early therapeutic decisions. Furthermore, AI-powered clinical decision support systems are assisting neurointensivists by integrating multimodal data imaging, intracranial pressure monitors, and vital signs to forecast secondary brain injury and optimize physiological management in the Neuro-ICU.

Market Dynamics

Key Drivers in the U.S. Intracranial Hemorrhage Diagnosis & Treatment Market

High Incidence of Stroke and Traumatic Brain Injuries

The United States continues to experience a high burden of intracranial hemorrhage due to the increasing incidence of hemorrhagic stroke, traumatic brain injuries (TBIs), cerebral aneurysms, and anticoagulant-related bleeding. An aging population, rising prevalence of hypertension, obesity, diabetes, and cardiovascular diseases further elevates the risk of spontaneous intracerebral hemorrhage. In addition, road traffic accidents, sports-related injuries, and falls among older adults contribute significantly to emergency neurological admissions. Growing public awareness regarding stroke symptoms and improved emergency medical response systems are driving earlier diagnosis and treatment, supporting sustained demand for advanced diagnostic imaging, neurosurgical procedures, and neurocritical care services.

Strong Healthcare Infrastructure and Advanced Neurovascular Care

The U.S. benefits from one of the world's most advanced healthcare systems, supported by comprehensive stroke centers, Level I trauma centers, and specialized neurological hospitals. Widespread availability of high-resolution CT scanners, MRI systems, cerebral angiography, and hybrid operating rooms enables rapid diagnosis and effective management of intracranial hemorrhage. Continuous investments in neurocritical care, robotic-assisted surgery, and minimally invasive neurointerventional technologies further improve clinical outcomes. The presence of experienced neurologists, neurosurgeons, and interventional neuroradiologists, along with favorable reimbursement for many advanced procedures, continues to strengthen market growth.

Restraints in the U.S. Intracranial Hemorrhage Diagnosis & Treatment Market

High Treatment Costs and Healthcare Expenditure

Despite advanced medical capabilities, intracranial hemorrhage treatment remains expensive in the United States. Costs associated with emergency imaging, neurosurgical interventions, intensive care unit admissions, prolonged hospitalization, and post-acute rehabilitation place a substantial financial burden on patients and healthcare providers. Although Medicare, Medicaid, and private insurance cover many treatment components, out-of-pocket expenses and coverage limitations for certain services may delay access to specialized care. Rising healthcare costs also increase financial pressure on hospitals investing in next-generation neuroimaging and surgical technologies.

Shortage of Neurocritical Care Specialists in Certain Regions

While major metropolitan areas offer highly specialized neurological care, several rural and underserved regions continue to experience shortages of neurologists, neurosurgeons, neurointensivists, and interventional neuroradiologists. Geographic disparities in access to comprehensive stroke centers can delay diagnosis and time-sensitive treatment for intracranial hemorrhage patients. Workforce shortages, increasing patient volumes, and uneven distribution of specialized facilities continue to challenge equitable access to advanced neurological services across the country.

Growth Opportunities in the U.S. Intracranial Hemorrhage Diagnosis & Treatment Market

Expansion of AI-Enabled Precision Diagnostics

The growing adoption of artificial intelligence and advanced imaging analytics presents significant opportunities for the U.S. intracranial hemorrhage diagnosis market. AI-assisted CT and MRI interpretation platforms enable faster hemorrhage detection, automated hematoma quantification, and rapid clinical prioritization in emergency departments. Integration of predictive analytics, cloud-based imaging platforms, and decision-support software is improving diagnostic efficiency while reducing treatment delays. Increasing investments in digital health and precision medicine are expected to accelerate commercialization of next-generation neurodiagnostic solutions.

Increasing Adoption of Minimally Invasive Neurovascular Therapies

Technological innovation in minimally invasive neurosurgery is creating new growth opportunities across the U.S. market. Image-guided hematoma evacuation, endovascular embolization, catheter-based interventions, robotic-assisted neurosurgery, and advanced neurovascular devices are improving patient outcomes while reducing surgical complications and hospital stays. Ongoing clinical research, FDA approvals of innovative medical devices, and increasing physician adoption of minimally invasive techniques are expected to drive sustained demand for advanced treatment solutions.

Trends in the U.S. Intracranial Hemorrhage Diagnosis & Treatment Market

Growing Integration of Artificial Intelligence Across Stroke Care

Artificial intelligence is becoming an integral component of stroke and intracranial hemorrhage management across U.S. healthcare systems. AI-powered software is increasingly used for automated hemorrhage detection, imaging workflow optimization, clinical decision support, and patient triage in emergency settings. Integration with hospital information systems and tele-stroke networks enables faster diagnosis and treatment coordination, improving clinical efficiency and reducing time to intervention for critically ill patients.

Rising Adoption of Integrated Neurocritical Care and Remote Monitoring

Healthcare providers are increasingly implementing comprehensive neurocritical care pathways that combine emergency diagnosis, surgical intervention, intensive care management, rehabilitation, and long-term neurological follow-up. Remote patient monitoring, wearable technologies, tele-neurology consultations, and digital rehabilitation platforms are expanding continuity of care beyond hospital settings. These integrated care models improve functional recovery, reduce readmission rates, and support the broader adoption of advanced intracranial hemorrhage diagnosis and treatment solutions throughout the United States.

Research Scope and Analysis

The U.S. Intracranial Hemorrhage Diagnosis & Treatment Market is segmented by hemorrhage type, diagnosis, treatment, drug class, distribution channel, and end user. These segments provide a comprehensive assessment of disease burden, diagnostic imaging utilization, therapeutic strategies, pharmaceutical adoption, healthcare delivery channels, and treatment settings across the United States. The analysis reflects the country's advanced healthcare infrastructure, widespread availability of neuroimaging technologies, established stroke care networks, favorable reimbursement landscape, and continuous innovation in neurocritical care and minimally invasive neurosurgical interventions.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Hemorrhage Type Analysis

Intracerebral Hemorrhage (ICH) is expected to dominate the U.S. Intracranial Hemorrhage Diagnosis & Treatment Market owing to its high prevalence among the country's aging population and individuals with hypertension, diabetes, and cardiovascular diseases. Hypertension remains the leading cause of spontaneous ICH, while increasing use of anticoagulant therapies among elderly patients further contributes to disease incidence.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The condition requires rapid diagnosis, intensive neurocritical care, and often complex neurosurgical intervention, resulting in significant healthcare utilization. The widespread presence of Comprehensive Stroke Centers, improved emergency medical services (EMS), and established stroke management protocols continue to strengthen the dominance of the ICH segment across the United States.

By Diagnosis Analysis

Computed Tomography (CT Scan), particularly Non-Contrast CT (NCCT), is projected to dominate the diagnosis segment as it remains the gold standard for the rapid evaluation of suspected intracranial hemorrhage. CT scanners are extensively available across emergency departments, trauma centers, academic medical centers, and community hospitals throughout the United States. The modality enables accurate hemorrhage detection within minutes, facilitating timely treatment decisions and reducing delays in acute stroke management. Continuous investments in advanced multidetector CT systems, AI-assisted imaging software, and nationwide stroke care networks further reinforce CT's leading position. Although MRI provides superior soft tissue characterization, CT remains the preferred first-line imaging modality due to its speed, accessibility, and cost-effectiveness in emergency settings.

By Treatment Analysis

Medical Management is anticipated to dominate the treatment segment because initial stabilization represents the cornerstone of intracranial hemorrhage care before surgical intervention is considered. Blood pressure optimization, anticoagulant reversal, intracranial pressure control, seizure management, and intensive neurological monitoring are standard components of evidence-based treatment. A substantial proportion of patients are successfully managed conservatively without surgery, particularly those with smaller hemorrhages or high surgical risk. The extensive network of certified stroke centers, neurocritical care units, and adherence to American Heart Association/American Stroke Association (AHA/ASA) clinical guidelines continue to support the widespread adoption of medical management across U.S. healthcare institutions.

By Drug Class Analysis

Antihypertensive Agents are expected to dominate the drug class segment because elevated blood pressure is the primary modifiable risk factor associated with spontaneous intracerebral hemorrhage. Rapid blood pressure reduction during the acute phase is recommended to minimize hematoma expansion and improve neurological outcomes. Consequently, intravenous and oral antihypertensive medications are routinely administered in emergency departments, stroke units, and intensive care settings across the United States. The country's high prevalence of hypertension, established clinical treatment protocols, broad availability of branded and generic medications, and increasing emphasis on secondary stroke prevention continue to drive strong utilization of antihypertensive therapies.

By Distribution Channel Analysis

Hospital Pharmacies are projected to dominate the distribution channel segment as intracranial hemorrhage requires immediate access to emergency medications, reversal agents, neurocritical care drugs, anesthetics, and perioperative pharmaceutical support. Most patients receive diagnosis and treatment within hospitals, where medications are dispensed through institutional pharmacy systems to ensure rapid availability and adherence to standardized treatment protocols. Large academic medical centers and comprehensive stroke hospitals maintain specialized pharmacy services that support multidisciplinary neurological care. Retail and specialty pharmacies primarily contribute to long-term medication management and rehabilitation following hospital discharge.

By End User Analysis

Tertiary Care Hospitals are expected to dominate the end-user segment due to their comprehensive capabilities in managing complex intracranial hemorrhage cases. These facilities offer 24/7 emergency services, advanced CT and MRI imaging, neurocritical care units, neurosurgical operating rooms, endovascular intervention suites, and multidisciplinary stroke teams. Most severe hemorrhagic stroke and traumatic brain injury patients are referred to tertiary hospitals for specialized treatment unavailable at smaller healthcare facilities. Continuous investments in Comprehensive Stroke Centers, robotic-assisted neurosurgery, AI-enabled imaging, and advanced neurovascular technologies further reinforce the leadership of tertiary care hospitals within the U.S. Intracranial Hemorrhage Diagnosis & Treatment Market.

The US Intracranial Hemorrhage Diagnosis & Treatment Market Report is segmented on the basis of the following:

By Hemorrhage Type

- Intracerebral Hemorrhage (ICH)

- Subarachnoid Hemorrhage (SAH)

- Subdural Hematoma (SDH)

- Acute Subdural Hematoma

- Chronic Subdural Hematoma

- Epidural Hematoma (EDH)

- Intraventricular Hemorrhage (IVH)

- Other Intracranial Hemorrhages

By Diagnosis

- Computed Tomography (CT Scan)

- Non-Contrast CT

- CT Angiography (CTA)

- CT Perfusion

- Magnetic Resonance Imaging (MRI)

- Conventional MRI

- MR Angiography (MRA)

- Cerebral Angiography (Digital Subtraction Angiography)

- Blood-Based Biomarker Testing

- Neurological Assessment & Monitoring

- Other Diagnostic Methods

By Treatment

- Medical Management

- Blood Pressure Management

- Anticoagulation Reversal Therapy

- Osmotherapy

- Anticonvulsants

- Other Pharmacological Therapies

- Surgical Treatment

- Craniotomy

- Minimally Invasive Hematoma Evacuation

- Decompressive Craniectomy

- Endoscopic Surgery

- Ventricular Drainage (EVD)

- Aneurysm Clipping

- Endovascular Coiling

- Rehabilitation Therapy

By Drug Class

- Antihypertensive Agents

- Hemostatic Agents

- Reversal Agents for Anticoagulants

- Antiepileptic Drugs

- Osmotic Diuretics

- Neuroprotective Agents

- Other Drug Classes

By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

By End User

- Tertiary Care Hospitals

- Multispecialty Hospitals

- Neurology & Neurosurgery Centers

- Trauma Centers

- Diagnostic Imaging Centers

- Rehabilitation Centers

- Other End Users

Competitive Landscape

The US intracranial hemorrhage diagnosis and treatment market is highly consolidated among tier-1 medical device manufacturers, major pharmaceutical firms specializing in hemostasis and reversal agents, and integrated healthcare systems. Competitive advantage hinges on clinical evidence demonstrating efficacy in pivotal trials like INTERACT3 and ENRICH, which validate physiological and surgical interventions. The landscape is characterized by aggressive R&D investment in neurovascular implant technology specifically flow diversion stents and intrasaccular aneurysm occlusion devices and the launch of AI-enhanced diagnostic algorithms for hemorrhage detection. Strategic alliances between pharmaceutical companies and hospital pharmacy benefit managers are critical for securing formulary access for high-cost, novel reversal agents. Innovation pipelines focus keenly on neuroprotective drug classes and robotic-assisted stereotactic systems designed to refine minimally invasive surgical evacuation.

Some of the prominent players in the The US Intracranial Hemorrhage Diagnosis & Treatment Market are:

- Medtronic plc

- Johnson & Johnson (Cerenovus)

- Stryker Corporation

- Penumbra, Inc.

- Integra LifeSciences Holdings Corporation

- B. Braun SE

- Terumo Corporation

- MicroVention, Inc.

- Philips Healthcare

- GE HealthCare Technologies Inc.

- Siemens Healthineers AG

- Canon Medical Systems Corporation

- Fujifilm Healthcare Corporation

- Merck & Co., Inc.

- Pfizer Inc.

- Novo Nordisk A/S

- Baxter International Inc.

- Natus Medical Incorporated

- Zimmer Biomet Holdings, Inc.

- Abbott Laboratories

- Other Key Players

Recent Developments

- June 2026: GE HealthCare received expanded adoption across leading U.S. stroke centers for its AI-enabled CT imaging solutions, enhancing rapid detection and triage of intracranial hemorrhage patients in emergency departments.

- March 2026: Penumbra, Inc. expanded physician training and clinical education programs across the United States to support broader adoption of minimally invasive neurovascular technologies for the treatment of hemorrhagic stroke and intracranial bleeding.

- October 2025: Siemens Healthineers introduced advanced AI-powered neuroimaging workflow enhancements for U.S. hospitals, improving emergency CT scan interpretation and accelerating clinical decision-making for suspected intracranial hemorrhage cases.

- May 2025: Medtronic plc expanded its neurovascular portfolio and physician training initiatives in the United States, supporting greater use of minimally invasive endovascular procedures for the management of intracranial hemorrhage and complex neurovascular disorders.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 746.5 Mn |

| Forecast Value (2035) |

USD 1,309.1 Mn |

| CAGR (2026–2035) |

6.4% |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Hemorrhage Type, By Diagnosis, By Treatment, By Drug Class, By Distribution Channel, and By End User |

| Country Coverage |

The US |

Frequently Asked Questions

How big is the US Intracranial Hemorrhage Diagnosis & Treatment Market?

▾ The US Intracranial Hemorrhage Diagnosis & Treatment market is poised to be valued at USD 746.5 million in 2026 and is projected to reach USD 1,309.1 million by 2035, driven by the demographic tailwinds of an aging population and the technological shift toward minimally invasive neurosurgery.

What is the CAGR of the US Intracranial Hemorrhage Diagnosis & Treatment Market from 2026 to 2035?

▾ The market is expected to grow at a CAGR of 6.4% from 2026 to 2035, reflecting the robust clinical pipeline for neuroprotective agents and the increasing standard-of-care utilization of endovascular and endoscopic surgical techniques.

What factors are driving the growth of the US Intracranial Hemorrhage Diagnosis & Treatment Market?

▾ Key drivers include the high prevalence of hypertension-induced spontaneous ICH, the therapeutic necessity created by widespread anticoagulant use, and the clinical shift toward proven minimally invasive evacuation technologies that reduce mortality and improve functional recovery.

What are the major trends in the US Intracranial Hemorrhage Diagnosis & Treatment Market?

▾ Major trends include the adoption of AI-driven triage for non-contrast CT brain scans, the expanding indication for decompressive craniectomy, the pivot from standard craniotomy to endoscopic hematoma evacuation, and the growth of tele-neurosurgery networks to standardize acute management in underserved regions.

Who are the key players in the US Intracranial Hemorrhage Diagnosis & Treatment Market?

▾ Key players include Medtronic, Stryker, Penumbra, Johnson & Johnson (Cerenovus), Siemens Healthineers, and Pfizer, driving innovation through clinical trials, next-generation neurovascular implant development, AI diagnostic software, and the commercialization of targeted anticoagulant reversal agents.

How is the US Intracranial Hemorrhage Diagnosis & Treatment Market segmented?

▾ The market is segmented by Hemorrhage Type, Diagnosis, Treatment, Drug Class, Distribution Channel, and End User.