Market Overview

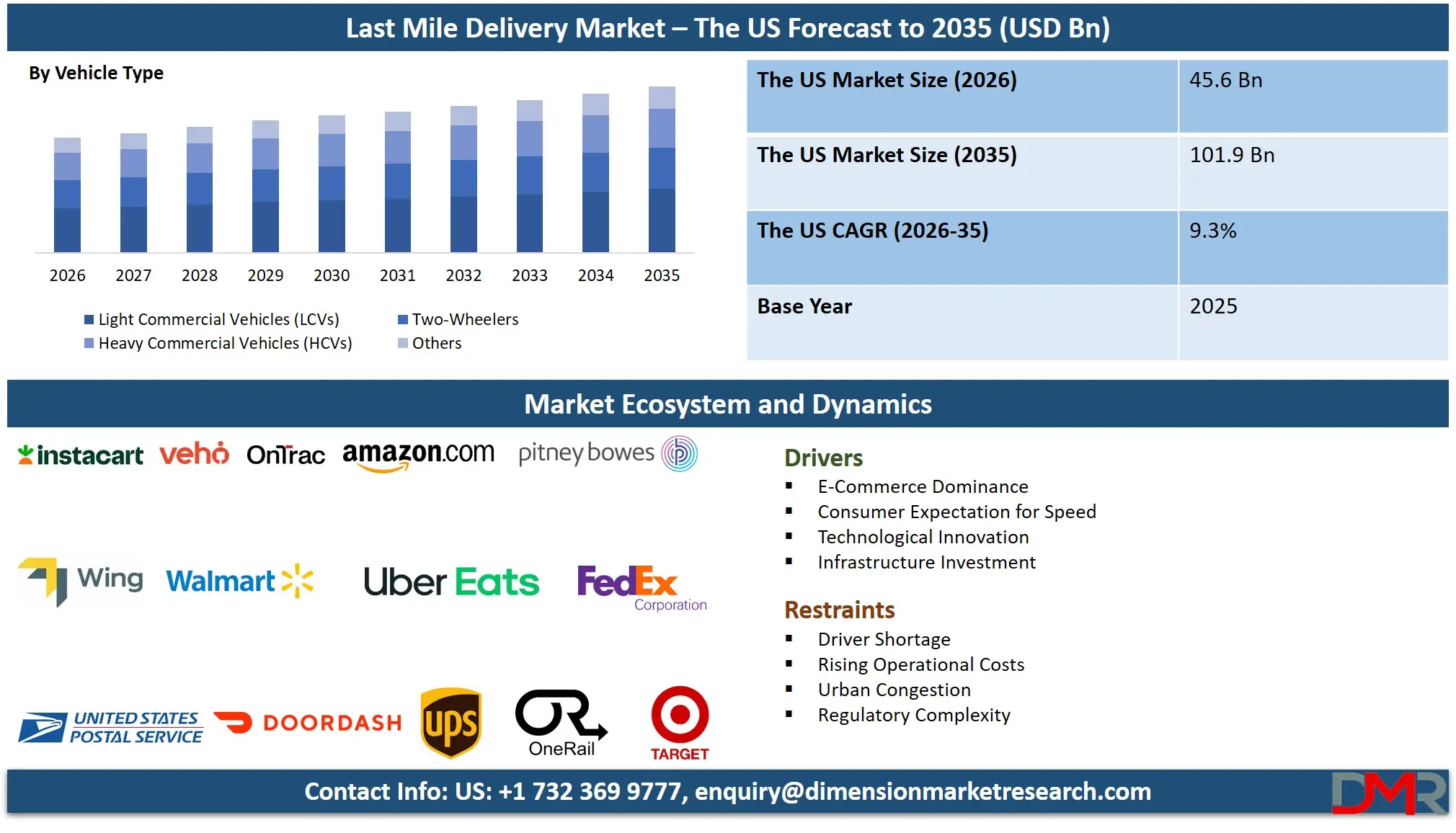

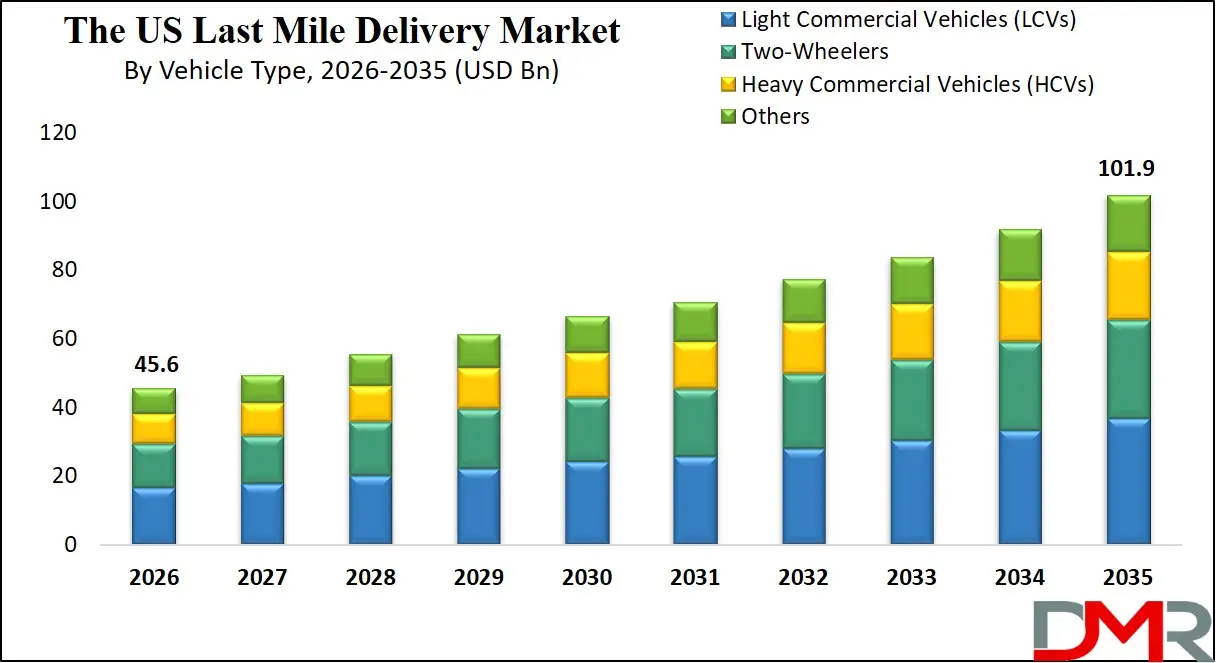

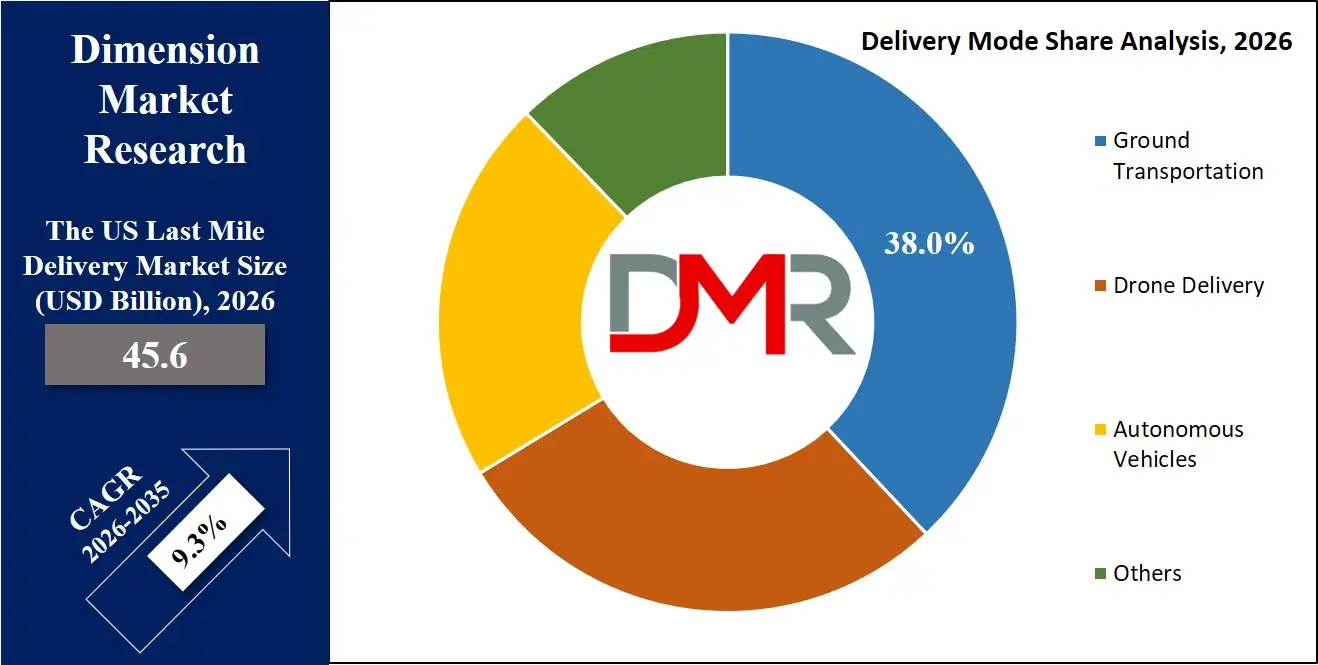

The US last mile delivery market size is expected to reach a value of USD 45.6 billion in 2026, and it is further anticipated to reach a market value of USD 101.9 billion by 2035 at a CAGR of 9.3%.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The last mile delivery market is a critical component of the United States' economic landscape, propelled by the exponential growth of e-commerce and shifting consumer expectations for speed and convenience. As the final and most visible stage of the supply chain, last mile delivery directly impacts customer satisfaction and brand loyalty. The sector encompasses a wide range of activities, from traditional ground transportation to cutting-edge autonomous vehicles and drone deliveries, all working to facilitate the movement of goods from distribution centers to end consumers. The ongoing transformation of retail, accelerated by the pandemic, has cemented last mile logistics as a central pillar of the US economy, driving significant investment in infrastructure, technology, and workforce development.

Over the last few years, the US last mile delivery market has undergone a strategic transition towards hyper-efficiency and technological integration. Key technologies such as artificial intelligence, route optimization software, and real-time tracking platforms are now standard, enabling carriers to manage complex delivery networks with unprecedented precision. Furthermore, the rise of the on-demand economy has placed immense pressure on logistics providers to offer same-day and even instant delivery options. This confluence of technological advancement and market demand is fundamentally reshaping the industry, creating a highly competitive and dynamic environment.

Key trends currently evident within the US last mile delivery arena include the rapid adoption of micro-fulfillment centers located in urban areas to reduce delivery times and costs. Alongside this, the integration of AI and machine learning is enabling predictive delivery windows and dynamic rerouting based on real-time traffic and weather conditions. Additionally, there is a growing emphasis on sustainability, with major players investing in electric vehicle fleets, cargo bikes for dense urban cores, and carbon-neutral delivery programs to meet both regulatory pressures and consumer preferences for eco-friendly practices. The demand for contactless delivery options has also become a persistent feature, adding a new layer of operational complexity.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The market is consequently witnessing huge opportunities driven by sustained investment in logistics infrastructure and technology. Initiatives to expand and electrify delivery fleets, coupled with the Federal Aviation Administration's (FAA) evolving regulatory framework for drone delivery, are creating new avenues for growth. The expansion of suburban and exurban populations is also reshaping delivery zones, requiring logistics providers to optimize networks for longer distances and lower densities. The focus on smart logistics technologies, such as autonomous delivery vehicles and sidewalk robots, provides companies with opportunities to gain a competitive edge by reducing labor costs and improving delivery efficiency.

The US Last Mile Delivery Market: Key Takeaways

- Market Value: The United States Last Mile Delivery Market size is estimated to have a value of USD 45.6 billion in 2026 and is expected to reach USD 101.9 billion by the end of 2035.

- By Delivery Mode Segment Analysis: Ground Transportation is anticipated to dominate this segment in the market, as it will hold the largest market share in 2026.

- By Vehicle Type Segment Analysis: Light Commercial Vehicles (LCVs) are projected to dominate the vehicle type segment in the US Last Mile Delivery Market with the highest market share in 2026.

- By Service Type Segment Analysis: The B2C (Business-to-Consumer) segment is anticipated to dominate the service type segment of this market in 2026.

- By Delivery Time Frame Segment Analysis: Standard (2-5 days) delivery is projected to hold the leading position in the delivery time frame segment of this market in 2026, though same-day is the fastest-growing.

- By Application Segment Analysis: E-commerce/Retail is projected to dominate the application segment in the US last-mile delivery market in 2026.

- By End-User Segment Analysis: Large Enterprises are projected to dominate the end-user segment in the US last-mile delivery market in 2026.

- Key Players: Some of the major key players in the United States Last Mile Delivery Market are Amazon Logistics, UPS, FedEx, USPS, DHL eCommerce, XPO Logistics, and many others.

- Market Growth Rate: The market is growing at a CAGR of 9.3 percent over the forecasted period.

Impact of Iran Conflict on Japan Last Mile Delivery Market

- Rising Transportation and Fuel Expenses: Iran-related tensions drive global oil price increases, raising fuel costs in the US and pressuring last mile delivery firms to adopt efficient routing systems and electrified vehicle fleets to reduce dependency on fuel.

- Global Supply Chain Delays: Disruptions in international shipping affect the availability of imported goods, leading US logistics providers to rely more on domestic distribution networks and regional fulfillment centers for faster last mile delivery.

- Port and Cargo Handling Bottlenecks: Enhanced security measures at ports and airports slow cargo processing, increasing lead times and forcing US delivery companies to improve logistics coordination and adopt automation for faster throughput.

- Trade Policy and Tariff Uncertainty: Geopolitical instability influences trade negotiations and tariffs, impacting product flows and forcing US companies to adjust sourcing strategies and forecast demand more accurately for last mile operations.

The US Last Mile Delivery Market: Use Cases

- E-commerce Parcel Delivery: Last-mile delivery enables fast shipment of online purchases from platforms like Amazon and Walmart, ensuring efficient doorstep fulfillment, improved customer satisfaction, reduced delivery timelines, and seamless order tracking across urban and suburban regions.

- Food & Grocery Delivery: On-demand last-mile services support rapid delivery of meals and groceries via platforms such as DoorDash and Instacart, meeting rising consumer expectations for convenience, freshness, speed, flexible scheduling, and real-time tracking capabilities.

- Healthcare & Pharmaceutical Delivery: Last-mile logistics facilitate timely distribution of medicines, diagnostic kits, and medical devices, enhancing patient care, supporting telehealth services, reducing hospital visits, ensuring temperature-controlled transport, and improving accessibility across remote and underserved U.S. locations.

- Same-Day & Express Logistics: Last-mile delivery enables urgent shipments of documents, electronics, and essentials through providers like FedEx and UPS, ensuring speed, reliability, optimized routing, real-time updates, and efficient handling of time-sensitive deliveries.

The US Last Mile Delivery Market: Stats & Facts

United States Postal Service (USPS)

- Delivers to 170+ million addresses across the U.S. six days a week.

- Handled ~16 billion mail items and packages during the 2025 holiday season.

- Average delivery time improved to 2.5 days, down from 2.8 days year-over-year.

- Delivered 6.9 billion parcels in 2024, one of the largest last-mile volumes in the U.S.

- Operates 18,000+ delivery units and processing centers nationwide.

- Has 3.5–4 billion units of annual last-mile delivery capacity.

- Generates USD 5.5–6 billion annually from last-mile delivery services.

- Mail volume declined from 220 billion to 110 billion pieces over 15 years, shifting focus toward parcels.

United States Census Bureau

- The U.S. processes ~21–22 billion parcels annually, largely driven by e-commerce demand.

- Equivalent to ~1.75 billion parcels per month.

- Around 404 million parcels are delivered weekly across the country.

National Retail Federation

- 66% of U.S. consumers expect same-day delivery for online purchases.

- 84% of consumers abandon a brand after a poor delivery experience.

United States Department of Transportation

- Last-mile delivery accounts for over 50% of total shipping costs.

- Cost per failed delivery attempt is approximately USD 18.

- Urban delivery costs average ~USD 10 per package, while rural deliveries reach ~USD 50 per package.

- U.S. delivery costs increased by ~12% from 2024 to 2025.

The US Last Mile Delivery Market: Market Dynamic

Driving Factors in the US Last Mile Delivery Market

Proliferation of E-commerce and On-Demand Culture

The sustained growth of e-commerce is the primary growth driver for the US last-mile delivery market. The shift in consumer behavior towards online shopping for a vast array of goods, from apparel to electronics, has created an unrelenting demand for delivery services. Furthermore, the on-demand culture, where consumers expect delivery within hours, is pushing retailers and logistics providers to innovate and invest heavily in their last-mile capabilities to remain competitive.

Advancements in Logistics Technology

Technological advancements are enabling new levels of efficiency and service that were previously unattainable. The development of sophisticated Transportation Management Systems (TMS), the proliferation of mobile apps for drivers, and the integration of APIs for seamless carrier connectivity are all growth drivers. These technologies allow for better capacity utilization, lower operational costs, and the ability to offer customers more choice and transparency regarding their deliveries.

Restraints in the US Last Mile Delivery Market

Escalating Operational Costs

Last mile delivery is the most expensive part of the supply chain, and costs are rising. These costs are driven by high fuel prices, increasing labor wages and benefits, vehicle maintenance, and the capital expenditure required for technology and new vehicle fleets. For many companies, balancing the consumer demand for fast, free shipping with profitability remains a critical challenge.

Workforce Challenges and Labor Shortages

The industry faces persistent challenges related to recruiting and retaining a sufficient workforce. High turnover rates, the physical demands of the job, and competition for labor among various sectors create chronic shortages of drivers and warehouse staff. This constraint limits operational capacity and can lead to service disruptions, particularly during peak demand seasons.

Opportunities in the US Last Mile Delivery Market

Expansion of Autonomous Delivery Fleets

The commercialization of autonomous delivery vehicles and drones presents a significant growth opportunity. As regulatory frameworks mature and technology costs decrease, companies can leverage autonomy to reduce the high costs associated with driver labor, address driver shortages, and enable 24/7 delivery capabilities. This offers a major opportunity for technology developers and early-adopting logistics firms to capture market share.

Green and Sustainable Delivery Services

With growing consumer and regulatory pressure to reduce carbon emissions, there is a substantial opportunity to build sustainable last mile delivery networks. This includes large-scale fleet electrification, the use of alternative fuels, and the deployment of micro-hubs to consolidate deliveries in urban areas. Companies that successfully develop and market carbon-neutral or carbon-negative delivery options can differentiate themselves and appeal to environmentally conscious consumers.

Trends in the US Last Mile Delivery Market

Digital Transformation of Last Mile Operations

The US last mile delivery sector is undergoing a massive digital transformation, driven by the need for efficiency and transparency. Companies are leveraging technologies such as AI-powered route optimization, real-time tracking with geofencing, and dynamic scheduling platforms. For example, machine learning algorithms can predict delivery windows with high accuracy and automatically reroute drivers based on real-time traffic data. This trend significantly improves operational efficiencies, reduces fuel consumption, and enhances the customer experience, aligning with the broader shift towards a data-driven logistics landscape.

Rise of Alternative Delivery Modes

Beyond traditional ground transportation, the market is seeing a surge in alternative delivery modes. Drone delivery is moving from pilot programs to commercial reality in select markets, offering ultra-fast delivery for urgent items. Autonomous vehicles, including sidewalk robots and self-driving vans, are being deployed to handle the "final 50 feet" and short-haul deliveries, promising to reduce labor dependency. The adoption of micromobility solutions like e-cargo bikes for dense urban areas is also accelerating, driven by sustainability goals and the need to navigate congestion.

The US Last Mile Delivery Market: Research Scope and Analysis

By Delivery Mode Analysis

Ground Transportation is projected to dominate the delivery mode segment in the U.S. Last Mile Delivery Market in 2026, maintaining the largest market share due to its mature infrastructure, operational scalability, and cost-efficiency. The United States has a highly developed road network that supports extensive last-mile connectivity across urban, suburban, and rural regions, enabling consistent and reliable delivery services. Major logistics providers such as United States Postal Service, Amazon Logistics, and FedEx rely heavily on fleets of trucks, vans, and passenger vehicles to execute daily deliveries at scale.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Ground transportation supports a wide range of delivery types, including B2C and B2B shipments, and offers flexibility in routing, scheduling, and capacity management. Its ability to handle high parcel volumes while maintaining relatively lower operational costs compared to air or emerging delivery modes further reinforces its dominance. Additionally, advancements in route optimization software, telematics, and fleet electrification are enhancing the efficiency and sustainability of ground operations. Although innovations such as drone delivery and autonomous vehicles are gaining attention, their adoption remains limited due to regulatory, technological, and infrastructure challenges. As a result, ground transportation continues to serve as the backbone of the last-mile ecosystem, ensuring dependable and scalable delivery solutions across the country.

By Vehicle Type Analysis

Light Commercial Vehicles (LCVs), including cargo vans and step vans, are expected to dominate the vehicle type segment in the U.S. Last Mile Delivery Market in 2026. Their widespread adoption is driven by their versatility, optimal payload capacity, and ability to efficiently navigate diverse delivery environments. LCVs strike a critical balance between cargo volume and maneuverability, making them well-suited for operations in congested urban centers as well as suburban neighborhoods. Leading logistics and e-commerce companies such as Amazon, UPS, and FedEx have built extensive fleets of LCVs to support their last-mile operations. These vehicles provide greater cargo protection and operational efficiency compared to two-wheelers, while also offering easier access and lower operational costs than heavy commercial vehicles in last-mile scenarios. Moreover, the growing emphasis on sustainability is accelerating the adoption of electric LCVs, with companies investing in zero-emission delivery fleets to meet environmental targets and regulatory requirements. While two-wheelers are effective for quick deliveries in dense urban zones and heavy commercial vehicles are used for bulk transportation to distribution hubs, LCVs remain the primary vehicle for final doorstep delivery. Their adaptability, efficiency, and alignment with evolving logistics needs ensure their continued dominance in the market.

By Service Type Analysis

The B2C (Business-to-Consumer) segment is anticipated to dominate the service type segment in the U.S. Last Mile Delivery Market in 2026, driven primarily by the rapid expansion of e-commerce and direct-to-consumer retail models. The shift in consumer behavior toward online shopping has significantly increased the volume of parcels delivered directly to residential addresses. Major platforms such as Amazon, Walmart, and Target are central to this growth, generating millions of daily deliveries across the country. B2C logistics is characterized by high shipment volumes, smaller package sizes, and complex delivery requirements, including scheduled time slots, contactless delivery, and secure drop-off solutions. These operational complexities require advanced routing technologies, real-time tracking systems, and efficient last-mile networks to meet rising consumer expectations. Additionally, the increasing demand for faster delivery options, such as same-day and next-day shipping, further strengthens the importance of B2C services. While B2B deliveries continue to play a significant role in supporting commercial supply chains, they typically involve fewer shipments with larger volumes per order. In contrast, the frequency, scale, and growth trajectory of B2C deliveries firmly position this segment as the dominant force in the last-mile delivery market.

By Delivery Time Frame Analysis

Standard delivery, typically ranging from two to five days, is projected to dominate the delivery time frame segment in the U.S. Last Mile Delivery Market in 2026. This segment's leadership is primarily attributed to its cost-effectiveness and widespread adoption among both consumers and retailers. For a large portion of non-urgent purchases, customers prefer economical shipping options, often provided free or at minimal cost by major retailers and platforms such as Amazon and Walmart. Standard delivery allows logistics providers to optimize routes, consolidate shipments, and improve overall operational efficiency, making it a sustainable option for handling large volumes of parcels. While same-day and next-day delivery services are gaining popularity due to increasing consumer demand for speed, they are typically offered as premium services with higher costs. Consequently, they represent a smaller share of total deliveries despite their rapid growth. Standard delivery also provides greater flexibility in capacity planning and reduces pressure on logistics infrastructure, enabling providers to maintain service quality at scale. As e-commerce volumes continue to rise, the balance between cost and delivery speed will remain a key factor, ensuring that standard delivery retains its dominant position in the market.

By Application Analysis

The E-commerce and Retail segment is expected to dominate the application segment of the U.S. Last Mile Delivery Market in 2026, driven by the sector's role as the primary generator of delivery demand. The exponential growth of online shopping has led to a surge in parcel volumes, with products ranging from electronics and apparel to household goods being delivered directly to consumers. Companies such as Amazon, Walmart, and Target are key contributors to this trend, continuously expanding their logistics networks to meet rising demand. The influence of the "Amazon effect" has reshaped consumer expectations, making fast, reliable, and transparent delivery a standard requirement across the retail industry. As a result, businesses are heavily investing in last-mile infrastructure, including fulfillment centers, delivery fleets, and advanced technologies such as AI-driven route optimization and real-time tracking. While other applications such as food delivery and healthcare logistics are growing, their overall contribution to parcel volume remains smaller in comparison. The scale, frequency, and diversity of shipments within the e-commerce sector firmly establish it as the dominant application driving the evolution of last-mile delivery.

By End-User Analysis

Large enterprises are projected to dominate the end-user segment in the U.S. Last Mile Delivery Market in 2026, owing to their substantial financial resources, technological capabilities, and extensive operational scale. Major corporations such as Amazon, Walmart, and Target have built sophisticated last-mile delivery networks that enable them to serve millions of customers efficiently. These organizations invest heavily in infrastructure, including automated warehouses, advanced sortation centers, and large delivery fleets, allowing them to manage high volumes of shipments with precision and speed. Their scale also provides significant bargaining power when partnering with third-party logistics providers, enabling cost optimization and service enhancements. Furthermore, large enterprises are at the forefront of adopting innovative technologies such as electric delivery vehicles, AI-powered logistics platforms, and autonomous delivery solutions. While small and medium-sized enterprises (SMEs) contribute to overall demand, they often rely on larger platforms or logistics providers to fulfill deliveries, limiting their direct control over last-mile operations. As a result, the concentration of delivery volume, strategic decision-making, and technological investment within large enterprises ensures their continued dominance in the market.

The US Last Mile Delivery Market Report is segmented on the basis of the following:

By Delivery Mode

- Ground Transportation

- Drone Delivery

- Autonomous Vehicles

- Others

By Vehicle Type

- Light Commercial Vehicles (LCVs)

- Two-Wheelers

- Heavy Commercial Vehicles (HCVs)

- Others

By Service Type

By Delivery Time Frame

- Next-day Delivery

- Same-day Delivery

- Standard (2-5 days)

By Application

- E-commerce/Retail

- Grocery & Food Delivery

- Healthcare & Pharmaceuticals

- Documents & Parcels

- Others

By End-User

- Retail Customers

- SMEs

- Large Enterprises

Impact of Artificial Intelligence in the US Last Mile Delivery Market

- Route Optimization and Efficiency: AI-powered algorithms used by companies like FedEx and UPS analyze traffic patterns, weather, and delivery density to optimize routes in real time, reducing fuel consumption, delivery time, and operational costs.

- Demand Forecasting and Capacity Planning: Platforms such as Amazon leverage AI to predict order volumes, seasonal spikes, and regional demand patterns, enabling better workforce allocation, inventory positioning, and fleet utilization across last-mile networks.

- Autonomous and Smart Delivery Systems: AI is enabling innovations like delivery robots and drones developed by Alphabet's Wing, improving delivery speed, reducing human dependency, and supporting contactless delivery models in select U.S. regions.

- Real-Time Tracking and Customer Experience: AI-driven systems enhance visibility by providing accurate delivery ETAs, dynamic updates, and predictive alerts, as seen in services offered by Amazon and DoorDash, significantly improving customer satisfaction and transparency.

- Warehouse Automation and Order Processing: AI-powered robotics and sorting systems streamline fulfillment operations, enabling faster order processing and dispatch, which strengthens last-mile efficiency and supports high-volume e-commerce deliveries across the U.S. market.

The US Last Mile Delivery Market: Competitive Landscape

The competitive landscape in the United States Last Mile Delivery Market is characterized by intense rivalry among a mix of national carriers, specialized logistics firms, and technology-enabled startups. Major companies are aggressively deploying advanced technologies such as AI, route optimization, and real-time tracking to enhance operational efficiency and the customer experience. The leading players are a blend of integrated carriers like UPS, FedEx, and the USPS, alongside the rapidly growing Amazon Logistics, which has built a vast, vertically integrated network. Technology-focused players like Uber Eats, DoorDash, and Instacart dominate the on-demand food and grocery segment, while specialized 3PLs (Third-Party Logistics providers) offer flexible, tech-driven solutions for a variety of shippers. These companies leverage data and network scale to align their offerings with the high demands of modern consumers.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Mergers, acquisitions, and strategic partnerships are common strategies allowing companies to expand service portfolios, enter new markets, and acquire technological capabilities. For instance, traditional carriers are acquiring or partnering with last-mile technology platforms to improve their e-commerce offerings. While the market is dominated by a few very large players, a competitive niche exists for innovative startups focused on autonomous vehicles, drone delivery, and micro-fulfillment. The intense competitive environment, coupled with strong investment in infrastructure and technology, continues to drive rapid evolution within the sector.

Some of the prominent players in the US Last Mile Delivery Market are:

- Amazon

- United Parcel Service (UPS)

- FedEx

- XPO Inc.

- J.B. Hunt Transport Services

- OnTrac

- USPS

- Pitney Bowes

- CEVA Logistics

- SEKO Logistics

- ShipBob

- OneRail

- Veho

- DoorDash

- Uber Eats

- Instacart

- Walmart

- Target

- Serve Robotics

- Alphabet Wing

- Other Key Players

Recent Developments in the US Last Mile Delivery Market

- October 2025: Amazon announced the expansion of its drone delivery program to a third major US metropolitan area, utilizing its latest MK-30 drone model designed for better performance in light rain and higher temperatures.

- September 2025: UPS unveiled a strategic partnership with a leading electric vehicle (EV) manufacturer to purchase 10,000 custom-built electric delivery vans, scheduled for deployment over the next two years, significantly advancing its fleet electrification goals.

- August 2025: FedEx launched a new, fully automated micro-fulfillment center in Manhattan, designed to consolidate deliveries and utilize cargo bikes for the final leg, aiming to reduce congestion and emissions in the city center.

- November 2024: The FAA issued a final rule for powered-lift aircraft (drones), creating a new category of airworthiness and operational rules that is expected to pave the way for scaled commercial drone delivery services in the US.

- July 2024: Walmart completed the acquisition of a robotics startup specializing in automated warehouse systems for its "dark stores," designed to process online grocery orders for same-day delivery with minimal human intervention.

- April 2024: XPO Logistics launched a new AI-powered platform for its last mile network, providing shippers with real-time visibility, predictive arrival windows, and automated exception management for heavy-goods deliveries.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 45.6 Bn |

| Forecast Value (2035) |

USD 101.9 Bn |

| CAGR (2026–2035) |

9.3% |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors and etc. |

| Segments Covered |

By Component (Solutions and Services), By Size (Small & Medium-sized Enterprises and Large Enterprises), By Industry Vertical (Public Sector, Pharmaceuticals, Media & Entertainment, IT & Telecommunication, BFSI, and Others Industry Verticals), By Delivery Mode (Ground Transportation, Drone Delivery, Autonomous Vehicles, and Others), By Vehicle Type (Light Commercial Vehicles, Two-Wheelers, Heavy Commercial Vehicles, and Others), By Service Type (B2C, B2B, and C2C), By Delivery Time Frame (Next-day Delivery, Same-day Delivery, and Standard [2–5 days]), By Application (E-commerce/Retail, Grocery & Food Delivery, Healthcare & Pharmaceuticals, Documents & Parcels, and Others), and By End-User (Retail Customers, SMEs, and Large Enterprises) |

| Country Coverage |

The US |

| Prominent Players |

Amazon, United Parcel Service (UPS), FedEx, XPO Inc., J.B. Hunt Transport Services, OnTrac, USPS, Pitney Bowes, CEVA Logistics, SEKO Logistics, ShipBob, OneRail, Veho, DoorDash, Uber Eats, Instacart, Walmart, Target, Serve Robotics, Alphabet Wing, and Other Key Players |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users) and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days and 5 analysts working days respectively. |

Frequently Asked Questions

How big is the United States Last Mile Delivery Market?

▾ The United States Last Mile Delivery Market size is estimated to have a value of USD 45.6 billion in 2026 and is expected to reach USD 101.9 billion by the end of 2035.

Who are the key players in the United States Last Mile Delivery Market?

▾ Some of the major key players in the United States Last Mile Delivery Market are Amazon Logistics, UPS, FedEx, USPS, DHL eCommerce, XPO Logistics, and many others.

What is the growth rate in the United States Last Mile Delivery Market?

▾ The market is growing at a CAGR of 9.3 percent over the forecasted period.