Market Overview

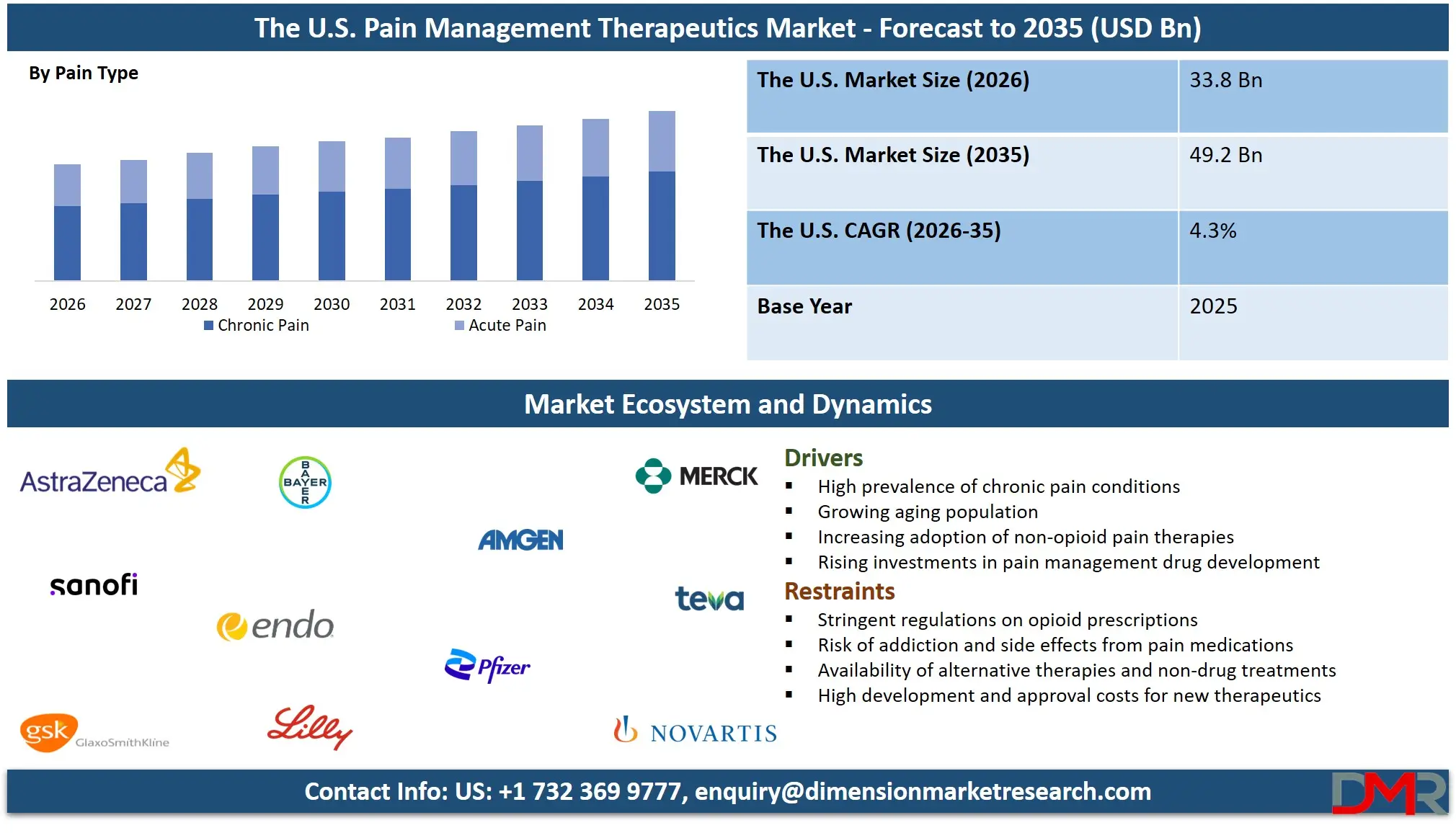

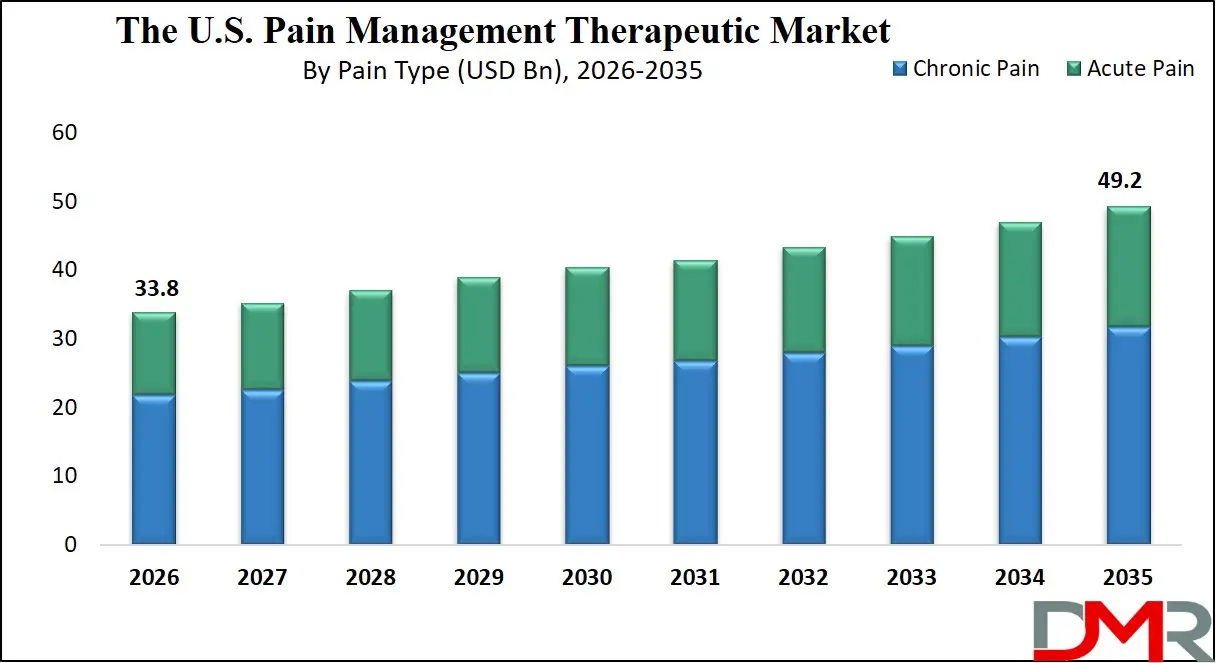

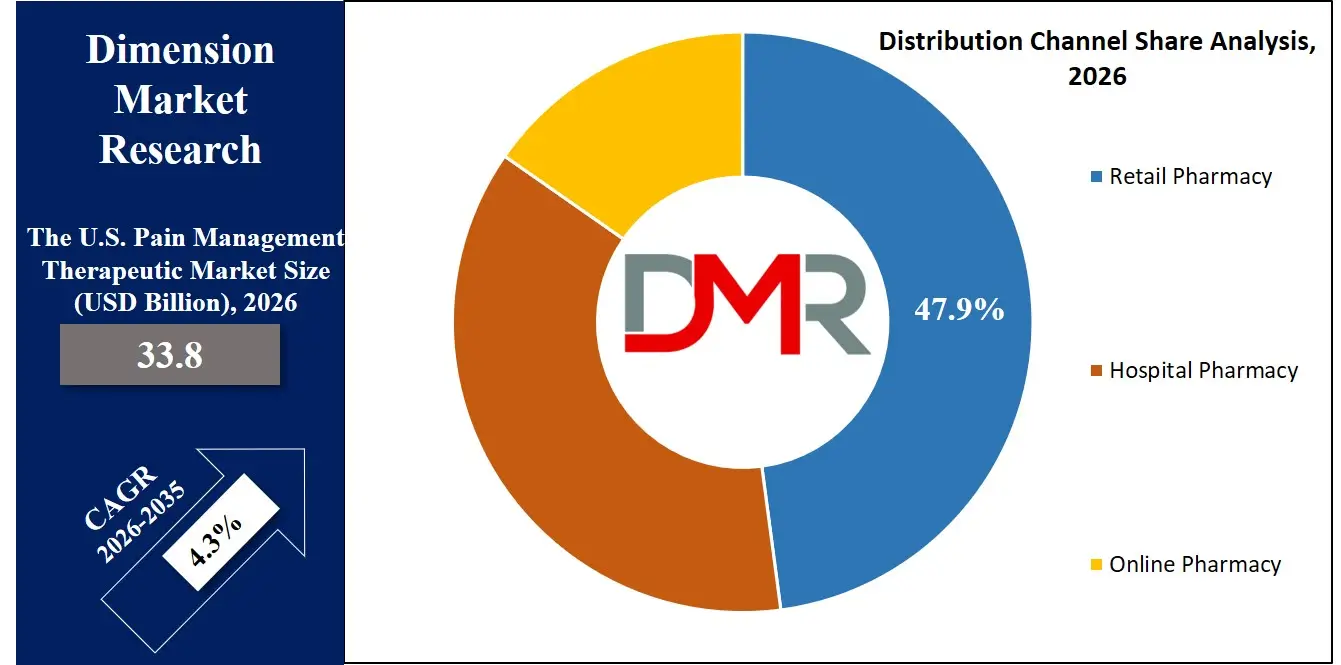

The U.S. Pain Management Therapeutics Market size is projected to reach USD 33.8 billion in 2026 and grow at a compound annual growth rate of 4.3% to reach a value of USD 49.2 billion in 2035.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Pain management therapeutics refers to the range of pharmaceutical products, medical formulations, and treatment approaches designed to alleviate or control acute and chronic pain conditions. These therapies include non-steroidal anti-inflammatory drugs, opioids, anesthetics, antidepressants, anticonvulsants, and anti-migraine medications delivered through oral or parenteral routes. They are widely used to treat conditions such as neuropathic pain, arthritis, cancer-related pain, postoperative pain, and musculoskeletal disorders. The field integrates pharmacological innovation, clinical pain management practices, and evolving healthcare protocols aimed at improving patient quality of life and functional outcomes.

The therapeutic landscape in the United States is shaped by continuous pharmaceutical research, increasing demand for non-addictive pain therapies, and evolving clinical guidelines to address the complexities of pain treatment. Innovations in drug formulations, extended-release technologies, and targeted biologics have expanded treatment options for physicians. Healthcare systems are also emphasizing multimodal pain management approaches that combine different drug classes and delivery methods to enhance effectiveness while minimizing adverse effects.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Industry expansion is also influenced by regulatory initiatives addressing opioid misuse and encouraging the development of safer alternatives. Increased healthcare expenditure, rising incidence of chronic diseases, and a rapidly aging population are contributing to sustained demand for advanced pain treatment options. As a result, research institutions and pharmaceutical manufacturers are accelerating investments in novel analgesics, personalized treatment strategies, and improved drug delivery technologies.

The U.S. Pain Management Therapeutics Market: Key Takeaways

- Market Growth: The U.S. Pain Management Therapeutics Market size is expected to grow by USD 14.1 billion, at a CAGR of 4.3%, during the forecasted period of 2027 to 2035.

- By Pain Type: The chronic pain segment is anticipated to get the majority share of the U.S. Pain Management Therapeutics market in 2026.

- By Distribution Channel: The retail pharmacy segment is expected to get the largest revenue share in 2026 in the U.S. Pain Management Therapeutics market.

- Use Cases: Some of the use cases of athleisure include palliative care applications, cancer pain management, and more.

The U.S. Pain Management Therapeutics Market: Use Cases

- Post-Surgical Pain Control: Hospitals widely use analgesics, anesthetics, and opioids to manage postoperative pain following orthopedic, cardiac, and abdominal surgeries. Effective pain control helps patients recover faster, reduces hospital stays, and improves overall surgical outcomes.

- Chronic Musculoskeletal Disorders: Therapeutics such as NSAIDs, antidepressants, and anticonvulsants are frequently prescribed to treat long-term conditions including arthritis and chronic back pain. These treatments help reduce inflammation, improve mobility, and support long-term patient management.

- Cancer Pain Management: Oncology patients often experience severe and persistent pain related to tumors or treatment procedures. Opioids, adjuvant drugs, and targeted pain therapies are used to improve comfort and quality of life during treatment and palliative care.

- Neuropathic Pain Treatment: Conditions such as diabetic neuropathy and nerve injuries require specialized medications like anticonvulsants and certain antidepressants. These therapies target nerve signaling pathways to reduce chronic nerve pain symptoms.

- Migraine and Headache Disorders: Anti-migraine drugs such as triptans and CGRP inhibitors help manage recurring migraine episodes. These therapies aim to prevent attacks, reduce frequency, and minimize neurological symptoms.

- Emergency and Trauma Pain Relief: Emergency departments rely on rapid-acting analgesics and injectable anesthetics to manage acute pain resulting from injuries, fractures, or accidents, ensuring immediate patient stabilization.

- Palliative Care Applications: Pain therapeutics are essential in hospice and palliative settings to manage severe pain associated with terminal illnesses, ensuring patient comfort and dignity during advanced disease stages.

Stats & Facts

- U.S. Centers for Disease Control and Prevention (CDC) reported in 2024 that approximately 20.9% of U.S. adults live with chronic pain, representing over 51 million people.

- U.S. National Institutes of Health (NIH) estimates in 2024 that chronic pain costs the U.S. economy between $560 billion and $635 billion annually in healthcare expenses and lost productivity.

- U.S. Food and Drug Administration (FDA) stated in 2025 that more than 100 analgesic and pain-related drug products are currently approved for prescription use in the United States.

- U.S. Department of Health and Human Services (HHS) reported in 2024 that over 142 million opioid prescriptions were dispensed in the United States.

- National Institute of Neurological Disorders and Stroke (NINDS) reported in 2025 that migraine affects approximately 39 million Americans.

- U.S. Census Bureau estimated in 2024 that more than 58 million Americans aged 65 and above are more susceptible to chronic pain conditions.

- Agency for Healthcare Research and Quality (AHRQ) reported in 2024 that post-operative pain occurs in nearly 80% of surgical patients.

- Centers for Medicare & Medicaid Services (CMS) reported in 2025 that U.S. healthcare spending reached about USD 4.9 trillion, with pharmaceuticals accounting for a major share of treatment costs.

- U.S. Department of Veterans Affairs (VA) reported in 2024 that around 50% of veterans receiving care report chronic pain conditions.

- National Center for Health Statistics (NCHS) reported in 2024 that opioid overdose deaths exceeded 80,000 annually, prompting stricter prescribing regulations.

- U.S. Bureau of Labor Statistics (BLS) noted in 2025 that healthcare occupations are projected to grow by 13% from 2021–2031, increasing demand for pain management services.

- National Institute on Drug Abuse (NIDA) reported in 2025 that over 9 million Americans misused prescription opioids in the previous year, influencing regulatory changes in pain therapy.

Market Dynamic

Driving Factors in the U.S. Pain Management Therapeutics Market

Rising Prevalence of Chronic Diseases and Aging Population

The increasing prevalence of chronic diseases and the rapidly aging population in the United States are major contributors to the demand for pain management therapeutics. Conditions such as arthritis, cancer, diabetes, and musculoskeletal disorders frequently involve persistent pain that requires long-term treatment. Older adults are particularly vulnerable to degenerative conditions and neuropathic pain, leading to higher consumption of analgesics and adjuvant drugs. Additionally, improved diagnostic capabilities and increased awareness of pain as a treatable medical condition are encouraging patients to seek medical intervention. Healthcare providers are therefore prescribing diverse therapeutic options to address both acute and chronic pain conditions.

Expansion of Pharmaceutical Research and Drug Innovation

Pharmaceutical companies are heavily investing in research and development to create safer and more effective pain therapies. The development of non-opioid analgesics, biologic drugs, and targeted therapies is transforming treatment strategies. Extended-release formulations and combination therapies are improving patient compliance and treatment outcomes. Clinical trials exploring novel pain pathways and receptor targets are also expanding therapeutic possibilities. Regulatory agencies are encouraging innovation in pain management while emphasizing safety and abuse prevention. As a result, the industry is witnessing the introduction of advanced therapeutic options that reduce dependency risks and enhance long-term pain control.

Restraints in the U.S. Pain Management Therapeutics Market

Stringent Regulations on Opioid Prescriptions

Strict regulatory frameworks surrounding opioid medications present a major constraint for the market. Due to concerns about addiction and overdose risks, federal and state authorities have implemented stringent prescribing guidelines and monitoring systems. Healthcare providers must follow strict documentation and patient evaluation protocols before prescribing opioid analgesics. While these regulations are crucial for public health, they also limit the availability of certain high-efficacy drugs for legitimate pain patients. Pharmaceutical manufacturers face additional compliance requirements and scrutiny during drug approval processes, which can delay product launches and reduce overall prescription volumes.

Adverse Effects and Risk of Drug Dependency

Many pain management therapeutics, particularly opioids and certain antidepressants, are associated with side effects such as nausea, dizziness, tolerance development, and dependency risks. These safety concerns often discourage physicians from prescribing long-term pharmacological treatments. Patients may also hesitate to continue therapy due to fear of addiction or adverse reactions. Healthcare providers increasingly emphasize alternative therapies such as physical rehabilitation or interventional procedures, which can reduce reliance on medications. The need to balance effective pain relief with patient safety creates a challenge for pharmaceutical developers seeking to produce widely accepted analgesic drugs.

Opportunities in the U.S. Pain Management Therapeutics Market

Development of Non-Opioid and Biologic Pain Therapies

The shift toward non-opioid pain management solutions presents a significant opportunity for pharmaceutical companies. Researchers are developing novel drug classes targeting inflammatory pathways, nerve signaling mechanisms, and immune responses involved in pain perception. Biologic therapies and monoclonal antibodies designed to block pain-related proteins are gaining attention in clinical trials. These treatments aim to deliver effective pain relief while minimizing addiction risks and side effects. As regulatory bodies encourage safer alternatives, companies investing in innovative non-opioid analgesics are expected to gain competitive advantages and capture emerging patient demand.

Expansion of Digital Health and Personalized Medicine

Digital health technologies and personalized treatment approaches are opening new possibilities in pain management. Wearable devices, remote monitoring tools, and data analytics platforms enable physicians to track patient symptoms and treatment responses in real time. Personalized medicine strategies use genetic and clinical data to tailor therapeutic regimens according to individual patient profiles. These advancements help optimize treatment effectiveness while minimizing adverse reactions. As healthcare systems increasingly adopt digital health infrastructure, pharmaceutical companies and care providers can integrate advanced technologies with pain therapeutics to improve patient outcomes.

Trends in the U.S. Pain Management Therapeutics Market

Increasing Adoption of Multimodal Pain Management

Healthcare providers are increasingly adopting multimodal pain management approaches that combine different drug classes and treatment methods. Instead of relying on a single medication, physicians use a combination of NSAIDs, antidepressants, anticonvulsants, and anesthetics to target multiple pain pathways simultaneously. This strategy enhances therapeutic effectiveness while reducing reliance on high-dose opioid medications. Multimodal therapy is particularly common in postoperative care, cancer treatment, and chronic pain management programs. Hospitals and pain clinics are integrating pharmacological treatments with physical therapy, psychological support, and interventional procedures to deliver comprehensive pain relief.

Growth of Targeted and Long-Acting Drug Formulations

Another important trend is the development of targeted and long-acting drug formulations designed to improve treatment efficiency and patient adherence. Extended-release tablets, transdermal patches, and injectable formulations provide sustained pain relief with fewer doses throughout the day. These formulations help maintain consistent therapeutic levels in the body, reducing breakthrough pain episodes. Pharmaceutical companies are also focusing on receptor-specific drugs that precisely target pain signaling mechanisms. Such innovations enhance treatment outcomes while reducing side effects, making them increasingly attractive options for long-term pain management.

Impact of Artificial Intelligence in the U.S. Pain Management Therapeutics Market

- AI-Driven Drug Discovery: Artificial intelligence accelerates the identification of new analgesic compounds by analyzing molecular interactions and predicting therapeutic effectiveness.

- Predictive Pain Assessment: AI algorithms analyze patient data, medical histories, and symptom patterns to predict pain severity and guide personalized treatment plans.

- Clinical Trial Optimization: AI tools streamline patient recruitment, trial design, and data analysis, reducing the time required to develop new pain therapeutics.

- Personalized Treatment Recommendations: Machine learning models help physicians choose optimal drug combinations based on individual patient characteristics and response history.

- Real-Time Patient Monitoring: AI-enabled wearable devices track patient pain levels, medication adherence, and physiological indicators for continuous care management.

- Adverse Effect Prediction: AI systems analyze large datasets to identify potential side effects and drug interactions before medications reach the market.

- Healthcare Workflow Automation: AI tools assist healthcare professionals in managing prescriptions, patient records, and clinical decision-making.

- Patient Engagement Platforms: AI-powered mobile health applications provide guidance on medication usage, symptom tracking, and treatment adherence.

Research Scope and Analysis

By Pain Type Analysis

Chronic pain represents the largest segment in the U.S. pain management therapeutics market due to the growing number of individuals suffering from long-term conditions such as arthritis, neuropathic disorders, fibromyalgia, and chronic back pain. These conditions require ongoing pharmacological treatment, creating consistent demand for analgesics and supportive therapies. Healthcare providers frequently prescribe combinations of NSAIDs, antidepressants, and anticonvulsants to manage persistent pain symptoms. Increasing life expectancy and the rising incidence of lifestyle-related disorders have further expanded the patient population requiring chronic pain management. In addition, medical awareness campaigns and improved diagnostic methods are encouraging more patients to seek professional treatment for long-standing pain conditions. As healthcare systems emphasize long-term disease management and improved quality of life, chronic pain therapies continue to dominate treatment demand. This segment is projected to account for approximately 64.3% of the market share in 2026, reflecting its significant contribution to overall therapeutic consumption and clinical treatment needs.

Acute pain represents the fastest-growing segment due to increasing surgical procedures, emergency care treatments, and trauma cases in the United States. Acute pain typically arises from injuries, surgeries, or short-term medical conditions requiring immediate treatment. Hospitals and outpatient facilities commonly use fast-acting analgesics, anesthetics, and injectable medications to manage such conditions. The growing number of minimally invasive surgeries and outpatient procedures has increased the demand for effective short-term pain relief therapies. Additionally, improved emergency medical services and rapid response systems are supporting higher adoption of acute pain medications. As healthcare facilities prioritize patient comfort and faster recovery, demand for efficient acute pain treatment options is expected to expand steadily.

By Drug Class Analysis

NSAIDs remain the leading drug class in the U.S. pain management therapeutics market due to their broad application in treating mild to moderate pain conditions. These drugs are widely prescribed for arthritis, musculoskeletal injuries, headaches, and postoperative pain due to their anti-inflammatory and analgesic properties. NSAIDs are available in both prescription and over-the-counter formulations, making them easily accessible to patients across healthcare settings. Physicians often prefer these medications as first-line treatment options because they carry a lower risk of dependency compared to opioids. Pharmaceutical companies continue to introduce improved formulations with reduced gastrointestinal side effects and enhanced effectiveness. Additionally, the growing prevalence of chronic inflammatory conditions among aging populations is increasing the demand for NSAID-based treatments. NSAIDs are expected to account for around 36.8% of the market share in 2026, reflecting their widespread usage and strong clinical acceptance.

Anti-migraine drugs represent the fastest-growing segment due to the increasing prevalence of migraine and headache disorders in the United States. Medications such as triptans, ergot alkaloids, and CGRP inhibitors are increasingly prescribed to prevent and treat migraine attacks. Advances in neurological research have enabled the development of targeted therapies that block migraine-related biological pathways. CGRP inhibitors, in particular, have gained significant attention for their effectiveness in reducing migraine frequency and severity. Growing awareness about migraine management and improved access to specialized neurological care are also contributing to segment growth. As pharmaceutical companies continue to invest in migraine-specific drug development, this segment is expected to witness strong expansion.

By Route of Administration Analysis

Oral administration dominates the market due to its convenience, patient preference, and ease of long-term treatment. Tablets, capsules, and liquid medications are widely prescribed for chronic pain, migraine, and inflammatory conditions. Oral drugs are generally easier to store, transport, and administer compared to injectable therapies, making them highly suitable for outpatient and home-based treatment. Pharmaceutical companies are also introducing extended-release oral formulations that provide prolonged pain relief while reducing dosing frequency. These advantages contribute to strong patient adherence and widespread clinical acceptance. Oral therapies are expected to hold approximately 68.5% of the market share in 2026, making them the most common route for pain management treatment in the United States.

Parenteral administration is the fastest-growing route of administration, particularly in hospital and emergency care settings. Injectable pain medications provide rapid therapeutic action, making them suitable for acute pain, trauma cases, and postoperative treatment. Hospitals frequently use intravenous or intramuscular analgesics for immediate pain control and patient stabilization. Advances in injectable drug formulations and hospital care infrastructure are further supporting segment growth. Additionally, certain biologic pain therapies require parenteral administration to ensure effective delivery and faster response times. As healthcare facilities continue to prioritize efficient and rapid pain management solutions, demand for parenteral treatments is expected to grow steadily.

By Indication Analysis

Arthritic pain accounts for the largest share of pain management therapeutics usage in the United States. Arthritis, including osteoarthritis and rheumatoid arthritis, is a major cause of disability and chronic pain among adults and elderly populations. Patients often require long-term pharmacological treatment involving NSAIDs, corticosteroids, and adjunct medications to manage inflammation and joint discomfort. Growing awareness about early arthritis diagnosis and treatment is increasing the number of patients receiving therapeutic care. The rising prevalence of obesity and aging populations further contributes to the increasing burden of joint-related disorders. Healthcare providers are also adopting combination therapy approaches to improve patient mobility and quality of life. Arthritic pain treatments are projected to account for approximately 31.6% of the market share in 2026, reflecting their high demand and long-term treatment requirements.

Neuropathic pain represents one of the fastest-growing indications due to the increasing prevalence of diabetes, nerve injuries, and neurological disorders. Patients with diabetic neuropathy or nerve damage often require specialized medications such as anticonvulsants and antidepressants to control nerve-related pain signals. Advancements in neuroscience research have improved understanding of neuropathic pain mechanisms, leading to the development of targeted therapies. Healthcare providers are increasingly diagnosing neuropathic conditions earlier, which contributes to greater treatment adoption. As the number of patients with metabolic and neurological disorders continues to rise, the demand for neuropathic pain therapies is expected to grow rapidly.

By Distribution Channel Analysis

Retail pharmacies dominate the distribution channel due to their accessibility and convenience for patients requiring prescription refills or over-the-counter pain medications. Many chronic pain patients rely on local pharmacies for long-term medication management and consultation with pharmacists. Retail chains also provide patient counseling, medication guidance, and insurance support services that enhance treatment adherence. The widespread presence of retail pharmacies across urban and rural areas ensures consistent availability of pain therapeutics. Additionally, partnerships between pharmaceutical companies and pharmacy chains support efficient drug distribution networks. Retail pharmacies are projected to hold approximately 47.9% of the market share in 2026, making them the leading distribution channel.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Online pharmacies represent the fastest-growing distribution channel due to the increasing adoption of digital healthcare services and home delivery options. Patients increasingly prefer online platforms for purchasing prescription refills and over-the-counter medications due to convenience and competitive pricing. Digital pharmacy services also offer subscription models, automated refill reminders, and telehealth integration. These features improve medication adherence and accessibility, particularly for patients managing chronic conditions. As e-commerce infrastructure continues to expand in healthcare, online pharmacy services are expected to gain a larger share of the pain management therapeutics market.

The U.S. Pain Management Therapeutics Market Report is segmented on the basis of the following:

By Pain Type

By Drug Class

- Non-steroidal Anti-inflammatory Drugs (NSAIDs)

- Opioids

- Oxycodone

- Hydrocodones

- Tramadol

- Morphine

- Fentanyl

- Others

- Anesthetics

- Anti-Migraine Drugs

- Triptans

- Ergot Alkaloids

- CGRP Inhibitors

- Antidepressants

- Anticonvulsants

- Other Drug Class

By Route of Administration

By Indication

- Arthritic Pain

- Neuropathic Pain

- Chronic Back Pain

- Post-Operative Pain

- Cancer Pain

- Fibromyalgia

- Other Indication

By Distribution Channel

- Online Pharmacy

- Retail Pharmacy

- Hospital Pharmacy

Competitive Landscape

The U.S. pain management therapeutics market is characterized by intense competition driven by continuous pharmaceutical innovation, strict regulatory oversight, and evolving clinical guidelines. Companies operating in this space focus heavily on research and development to create safer, non-addictive pain therapies while improving the effectiveness of existing drug classes.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Strategic collaborations with research institutions, biotechnology firms, and healthcare providers play a crucial role in accelerating drug development and expanding clinical applications. Market participants are also investing in advanced drug delivery technologies and extended-release formulations to enhance patient compliance. High regulatory requirements and extensive clinical trial processes create significant entry barriers for new participants, while established companies maintain competitive advantages through strong distribution networks, intellectual property portfolios, and diversified product pipelines.

Some of the prominent players in the U.S. Pain Management Therapeutics are:

- Pfizer

- Johnson & Johnson

- Merck & Co.

- Abbott Laboratories

- Eli Lilly and Company

- Amgen

- Endo International

- Teva Pharmaceutical Industries

- Novartis

- GlaxoSmithKline

- Bayer

- Sanofi

- AstraZeneca

- Bausch Health Companies

- Purdue Pharma

- Mallinckrodt Pharmaceuticals

- Grünenthal

- Hikma Pharmaceuticals

- Hisamitsu Pharmaceutical

- Viatris

- Other Key Players

Recent Developments

- In September 2025, Eli Lilly and Company announced a strategic investment to expand its neurological and pain therapy research division. The company allocated significant funding toward the development of biologic treatments designed to target migraine and chronic neuropathic pain pathways. The initiative includes the establishment of new research laboratories and partnerships with biotechnology firms specializing in monoclonal antibody technologies. Eli Lilly stated that the investment aims to accelerate the commercialization of innovative therapies that offer improved safety profiles and longer-lasting pain relief for patients suffering from severe chronic pain conditions.

- In February 2025, Pfizer Inc. announced the expansion of its pain management research program focused on developing next-generation non-opioid analgesics. The company revealed that it had initiated advanced clinical trials for a novel oral therapy targeting specific pain receptors associated with neuropathic and inflammatory pain. The program involves collaborations with several academic medical centers across the United States to evaluate long-term safety and effectiveness.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 33.8 Bn |

| Forecast Value (2035) |

USD 49.2 Bn |

| CAGR (2026–2035) |

4.3% |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors and etc. |

| Segments Covered |

By Pain Type (Chronic Pain, Acute Pain), By Drug Class (Non-steroidal Anti-inflammatory Drugs (NSAIDs), Opioids, Anesthetics, Anti-Migraine Drugs, Antidepressants, Anticonvulsants, Other Drug Class), By Route of Administration (Oral, Parenteral), By Indication (Arthritic Pain, Neuropathic Pain, Chronic Back Pain, Post-Operative Pain, Cancer Pain, Fibromyalgia, Other Indication), By Distribution Channel (Online Pharmacy, Retail Pharmacy, Hospital Pharmacy) |

| Country Coverage |

The US |

| Prominent Players |

Pfizer, Johnson & Johnson, Merck & Co., Abbott Laboratories, Eli Lilly and Company, Amgen, Endo International, Teva Pharmaceutical Industries, Novartis, GlaxoSmithKline, Bayer, Sanofi, AstraZeneca, Bausch Health Companies, Purdue Pharma, Mallinckrodt Pharmaceuticals, Grünenthal, Hikma Pharmaceuticals, Hisamitsu Pharmaceutical, Viatris, and Other Key Players |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users) and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days and 5 analysts working days respectively. |

Frequently Asked Questions

How big is the U.S. Pain Management Therapeutics Market?

▾ The U.S. Pain Management Therapeutics Market size is expected to reach USD 33.8 billion by 2026 and is projected to reach USD 49.2 billion by the end of 2035.

Who are the key players in the U.S. Pain Management Therapeutics Market?

▾ Some of the major key players in the U.S. Pain Management Therapeutics Market include Pfizer, Merck, Amgen and others.

What is the growth rate in the U.S. Pain Management Therapeutics Market?

▾ The market is growing at a CAGR of 4.3 percent over the forecasted period.