Market Overview

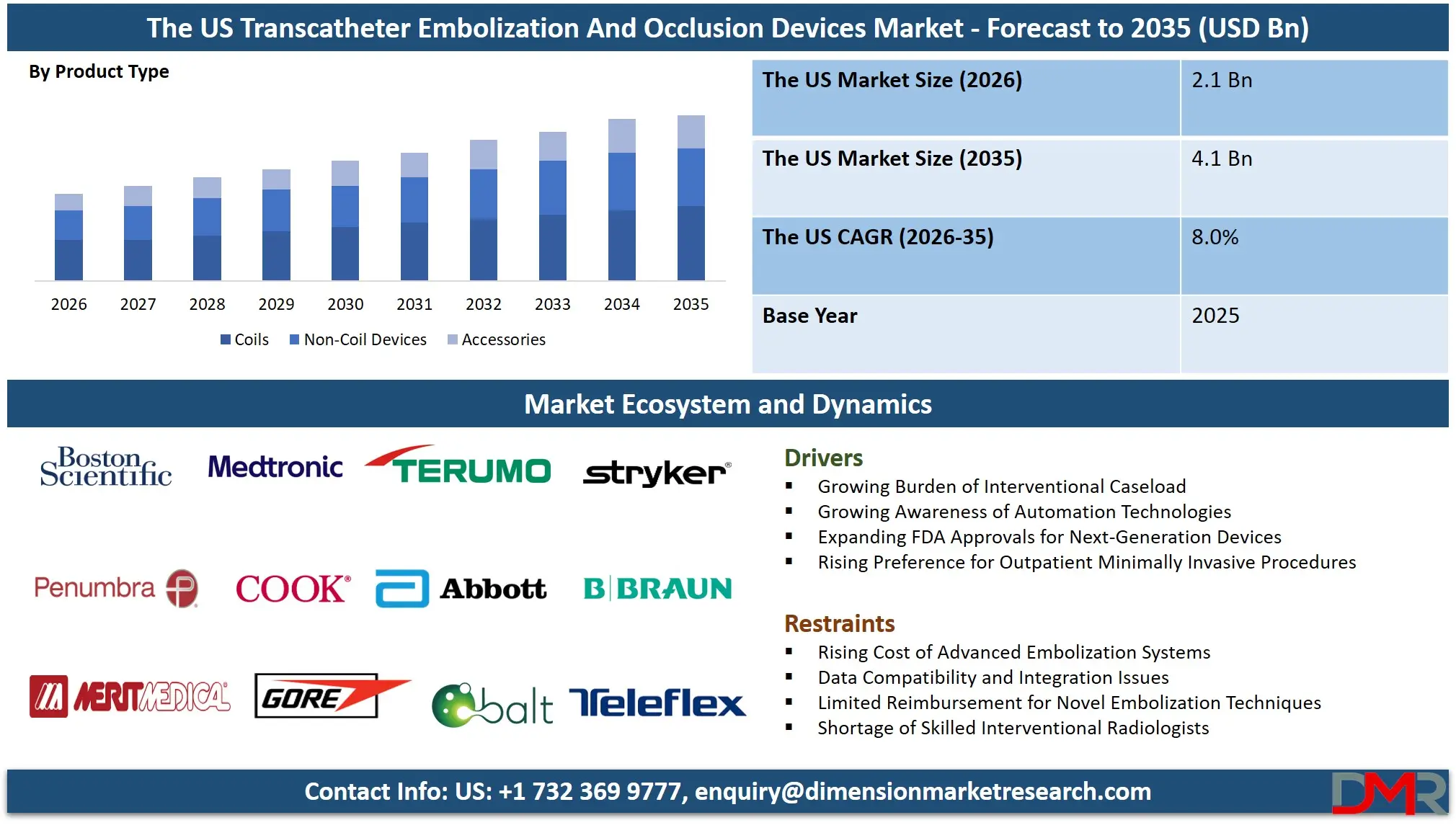

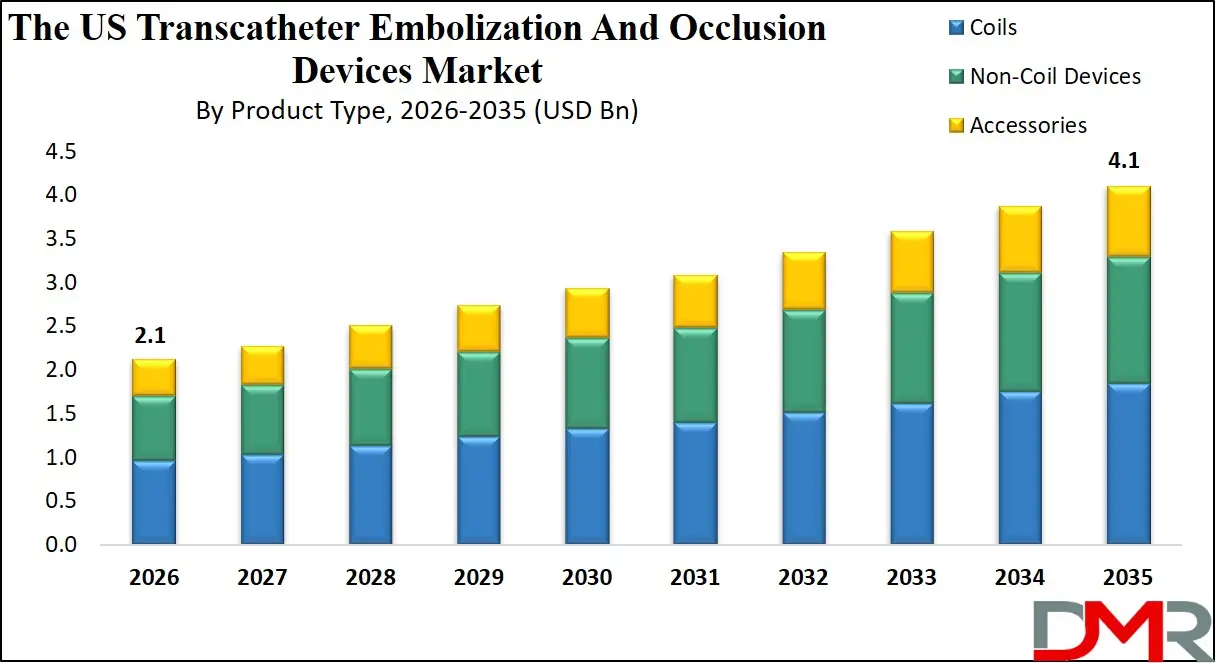

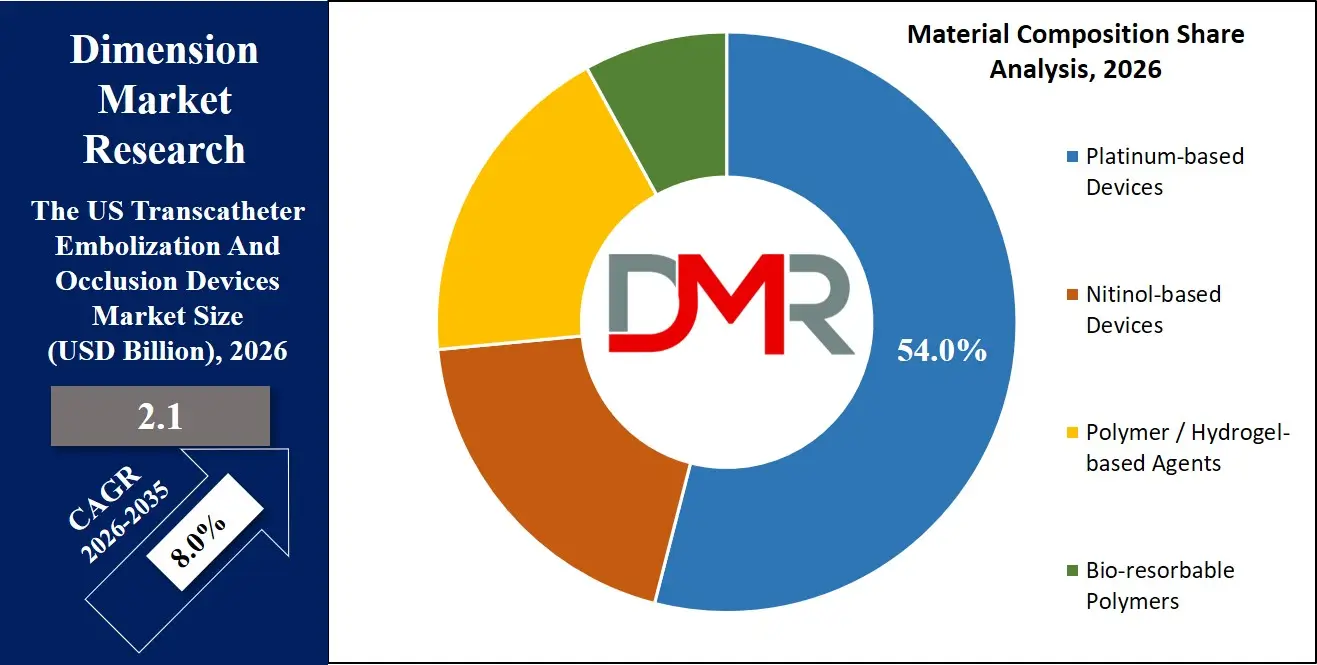

The US Transcatheter Embolization And Occlusion Devices Market size is expected to reach USD 2.1 billion in 2026 and grow at a compound annual growth rate of 8.0% to reach a value of USD 4.1 billion in 2035.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

A transcatheter embolization and occlusion device is a percutaneous device for occluding or reducing blood flow in designated vessels, useful for treating conditions like aneurysms, tumours, and vascular malformations. These include coils, flow diverters, embolization particles, and liquid embolics delivered via catheters to predetermined sites.

The US market dynamics are shifting to less visible offerings, and therefore, more biocompatible and bioresorbable options along with image-guided therapies as they respond to the growing incidence of hepatocellular carcinoma, cerebral aneurysms, and uterine fibroids on top of a trend towards same-day outpatient procedures combined with cutting-edge technologies such as nitinol or hydrogel for durable occlusions.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The US Transcatheter Embolization And Occlusion Devices Market: Key Takeaways and Other Influencing Factors

- Outlook of Market Growth Expansion: The US Transcatheter Embolization And Occlusion Devices Market is expected to grow to USD 2.1 billion in 2026 and reach up to USD 4.1 billion by 2035, due to growing adoption for minimally invasive treatment as well as outpatient-based interventional radiology procedures.

- High Growth Rate Momentum: The market has the potential to grow at a rate of 8.0% CAGR in the period ranging from 2026 to 2035, owing to the increasing prevalence of neurovascular disorders, liver cancer, and a shift towards bioresorbable embolization agents.

- Segment Leadership Structure: The product type segment is led by non-coil devices, accounting for approximately 56.2% share in 2026. By application, the market is led by oncology, contributing approximately 45.8% share, driven by widespread adoption of transarterial chemoembolization (TACE), tumor embolization, and radioembolization procedures.

- Technology Driven Operational Shift: The market is moving to bioresorbable polymers, hydrogel-coated coils, and liquid embolics with better radiopacity, which enhance occlusion precision and decrease the need for repeat interventions.

- Labor Shortage Burden Impact: As the U.S. Bureau of Labor Statistics reveals, there are over 5,000-6,000 vacancies in technologists and nurses in the interventional radiology and vascular surgery departments each year, with vacancies accounting for more than 8-10% of the staffing in specialized imaging units, thereby validating the necessity of easily used and ready-to-go embolic devices.

- Operational Downtime Insight: Industry statistics show that cases of catheter re-cannulation or coil relocation arise roughly every 25-30 minutes in busy angiography rooms, resulting in a 12-18% increment in procedures' duration, thereby validating the requirement for advanced detachable coil technology.

- Reduction of Errors in Large-Volume Lines: As evidenced by the clinical studies conducted, the likelihood of non-target embolization and extended fluoroscopy time is almost three to four times greater in centers using old-fashioned pushable coils, with fluoroscopy exposure rising by 20-35%, thus confirming the importance of detachable and flow-directed coils.

Impact of the Iran conflict on the US Transcatheter Embolization And Occlusion Devices Market

The escalation of the Iranian conflict is disrupting global supply chains which influence the output of embolization devices in the US in terms of availability of platinum, nitinol, and polymer raw materials; rising energy prices are raising the cost of sterilization and cleanroom manufacturing, which in turn raises the cost of the device; scarcity of precision microcatheters and delivery wires may affect volumes of production; cybersecurity and operational risks are making differences to the US hospital inventory management and medical device logistics companies.

The US Transcatheter Embolization And Occlusion Devices Market: Use Cases

- Oncologic Embolization (Chemoembolization): It can be used in administering drug eluting beads and liquid embolics to hyper vascular tumors of the liver through microcatheters which are able to access difficult to reach tortuous vessels with less reflux at the point of target.

- Neurovascular Embolization: It involves treatment of aneurysm, arteriovenous malformation (AVMs) and cerebrovascular lesions through application of coils, flow diverter and liquid embolic materials that can help in blocking blood vessels.

- Peripheral Vascular Embolization: Used in the control of internal bleeding, uterine fibroids embolization, gastrointestinal hemorrhages and trauma related hemorrhages by occluding peripheral blood vessels.

- Pre-Surgical Tumor Embolization: Blood supply to highly vascular tumors is controlled before surgery in order to minimize bleeding during surgery. This procedure is most frequently used in renal cell carcinomas, meningiomas and hepatocellular carcinoma.

The US Transcatheter Embolization And Occlusion Devices Market: Market Dynamics

Driving Factors in the US Transcatheter Embolization And Occlusion Devices Market

Growing Burden of Interventional Caseload

The increasing number of minimally invasive procedures for hepatocellular carcinoma, cerebral aneurysms, and symptomatic uterine fibroids in the US is adding to the push to deploy advanced, reliable embolization solutions. Modern detachable coils and liquid embolics can be used to achieve operational efficiency by enabling precise, permanent occlusion to increase throughput and eliminate reliance on surgical resection.

Growing Awareness of Automation Technologies

Image-guided automation and smart delivery systems are being adopted at an accelerated pace because of the growth of robotic-assisted interventional suites and AI-based fluoroscopy analytics. Live transmission of device positioning data, analytics based on cloud platforms, and linkage of hospital PACS ecosystems are enhancing procedure management and reducing the dependency of the facility on manual microcatheter manipulation.

Restraints in the US Transcatheter Embolization And Occlusion Devices Market

Rising Cost of Advanced Embolization Systems

The prohibitive nature of bioactive coils, flow-diverting stents, and pressure-enabling liquid embolics makes these systems inaccessible, and the application of these solutions by small regional hospitals or independent interventionalists may not be welcome. The use of advanced device technology on a large-scale basis may not be adopted by cost-sensitive outpatient clinics.

Data Compatibility and Integration Issues

System interoperability and equipment validation have compliance requirements (e.g., FDA, ISO 13485) that are strict and hamper market expansion. Some of the problems that affect the implementation of next-generation embolization devices include cybersecurity, data integration, and compatibility with existing angiography systems or legacy microcatheters.

Opportunities in the US Transcatheter Embolization And Occlusion Devices Market

Development of Bio-Resorbable and Smart Embolization Solutions

Adoption of bio-resorbable polymer technology in embolization devices will enable temporary occlusion, reduced chronic inflammation, and controlled degradation. Bio-resorbable-based devices will increase safety, decrease the number of long-term follow-up visits required, and improve the value of post-procedural patient outcomes.

Expansion of Neurology and Stroke Care

The growing demand for endovascular treatment of cerebral aneurysms, arteriovenous malformations (AVMs), and acute ischemic stroke is creating the need for precise, trackable, and rapid-detachment embolization devices. Neurovascular coils and liquid embolics assist with the procedure of continuous occlusion in highly tortuous cerebral vasculature, enabling the control of high-acuity interventional cases as well as offering just-in-time thrombectomy backup.

Trends in the US Transcatheter Embolization And Occlusion Devices Market

Transition to Detachable Coils and Flow Diverters

The transition to detachable coils and flow-diverting devices with controlled deployment and decreased operator fatigue is self-evident, as pushable coils are on the decline. The trend assists in maintaining precise occlusion with a minimum amount of interference with normal procedural timelines.

Advancements in Wireless and Cloud-Linked Procedure Logging

The embolization device data management is changing with the growing application of wireless connectivity, mobile dashboards, and cloud platforms. The automation of interventional radiology in the US will be in the form of smooth information sharing, remote post-op diagnostics, and connectivity to hospital inventory management systems.

The US Transcatheter Embolization And Occlusion Devices Market: Research Scope and Analysis

By Product Type Analysis

The Non-Coil Devices are expected to capture the largest market share of around 56.2% in the product type segment in 2026. The compatibility with minimally invasive surgery using embolic beads and liquid embolics, avoidance of complications such as catheter entrapment and inaccurate deployment, and increased adoption in complex vascular and oncological cases that require more precise care all contribute to this result. These types of devices allow for better navigation through challenging anatomy and controlled embolization while increasing efficiency, thus contributing to growth. On the other hand, the Coil Devices (detachable and pushable coils) are considered effective in treating aneurysms and arteriovenous malformations because of their proven occlusion capabilities and clinical familiarity, although the higher procedural dependency and slower adoption pace hinder their development compared to non-coil technology. Accessories continue to facilitate the placement and deployment.

By Material Composition Analysis

The material composition segment is projected to be dominated by Platinum-based Devices with approximately 54.0% share in 2026 because of the proven radiopacity, biocompatibility, and track record in coil and flow-diverter manufacturing. Within platinum-based devices, neurovascular coils and peripheral microcoils are the primary sub-applications. A focus on compatibility with standard microcatheters also helps this growth.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The Nitinol-based Devices segment, covering self-expanding flow diverters and occlusion systems, remains relevant for its super elasticity and kink resistance. Polymer / Hydrogel-based Agents, including hydrogel-coated coils and embolization beads, are becoming more popular in hyper vascular tumor embolization requiring volumetric occlusion. Bio-resorbable Polymers are emerging in temporary vessel occlusion applications.

By Application Analysis

The application segment is projected to be dominated by Oncology with approximately 45.8% share in 2026 as a result of the rising need for precise, super selective embolization of hepatocellular carcinoma, colorectal liver metastases, and renal tumors. This growth is also supported by the emphasis on reducing non-target embolization, preserving healthy parenchyma, and complying with NCCN guidelines. Peripheral Vascular Disease applications, including uterine fibroid embolization and peripheral aneurysm treatment, are still being implemented alongside other applications (Neurology, Urology) at different rates based on disease prevalence and referral patterns.

By End-User Analysis

In 2026, Hospitals & Clinics is projected to take up a larger market share of approximately 71.3% in the end-user segment as a result of high procedure volumes, well-developed interventional radiology infrastructure, and the high preference for premium-priced detachable coils and liquid embolics to ensure precise and durable occlusion. Transcatheter embolization devices are also commonplace in these settings, both in elective oncology embolization and in emergency neurovascular procedures. Ambulatory Surgical Centers and other end-users are also increasing their use of embolization devices, as minimally invasive procedures are increasingly affordable and accessible for outpatient varicocele and fibroid treatment.

The US Transcatheter Embolization And Occlusion Devices Market Report is segmented on the basis of the following:

By Product Type

- Coils

- Pushable Coils

- Detachable Coils

- Non-Coil Devices

- Flow Diverting Devices

- Embolization Particles

- Liquid Embolics

- Other Non-Coil Devices

- Accessories

By Material Composition

- Platinum-based Devices

- Nitinol-based Devices

- Polymer / Hydrogel-based Agents

- Bio-resorbable Polymers

By Application

- Oncology

- Peripheral Vascular Disease

- Neurology

- Urology

- Others

By End User

- Hospitals & Clinics

- Ambulatory Surgical Centers

- Others

Impact of Artificial Intelligence in the US Transcatheter Embolization And Occlusion Devices Market

The US transcatheter embolization and occlusion devices market is being improved with the help of artificial intelligence that allows automatic vessel segmentation and makes embolic agent selection decisions more accurate and faster. AI-powered procedural planning facilitates real-time adjustments and detects incomplete occlusion or abnormal flow patterns early on.

AI can be integrated with angiography systems to enhance predictive knowledge and minimize the workload of interventionalists. Machine learning is also used to process large amounts of procedural outcome data. In general, AI is enhancing efficiency, precision, and the use of modern image-guided embolization systems.

The US Transcatheter Embolization And Occlusion Devices Market: Competitive Landscape

The US transcatheter embolization and occlusion devices market is very competitive with great interest in innovation in detachable coils and bioresorbable embolic agents. Oncology, neurology, and peripheral vascular disease applications are also witnessing improvement in device deliverability, occlusion durability, and material flexibility in systems that can be developed by companies in advanced interventional devices.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The competition is growing with the increase in the adoption of AI-based procedural planning and bioresorbable polymer efficiency. The important growth strategies are product innovation and strategic partnerships with hospital interventional radiology departments.

Some of the prominent players in the US Transcatheter Embolization And Occlusion Devices Market are:

- Boston Scientific Corporation

- Medtronic plc

- Terumo Corporation (MicroVention, Inc.)

- Stryker Corporation

- Johnson & Johnson (Cerenovus)

- Penumbra, Inc.

- Cook Group Incorporated (Cook Medical LLC)

- Merit Medical Systems, Inc.

- W. L. Gore & Associates, Inc.

- Abbott Laboratories

- AngioDynamics, Inc.

- B. Braun Melsungen AG

- Becton, Dickinson and Company (Bard Peripheral Vascular)

- CDWT Holding LLC (Sirtex Medical)

- Balt Group (Balt International)

- Teleflex Incorporated

- Kaneka Corporation

- Siemens Healthineers AG (Varian Medical Systems, Inc.)

- Asahi Intecc Co., Ltd.

- MicroPort Scientific Corporation

- Other Key Players

Recent Developments in the US Transcatheter Embolization And Occlusion Devices Market

- January 2026: Boston Scientific Corporation announced a definitive agreement to acquire Penumbra, Inc., strengthening its position in neurovascular and embolization technologies, including thrombectomy and embolization solutions.

- March 2025: Medtronic plc had its Pipeline Vantage embolization devices classified by the U.S. FDA as a Class I recall (most serious) due to risks of stroke and death linked to improper vessel wall attachment.

- November 2024: Boston Scientific Corporation announced the acquisition of Intera Oncology, Inc. to expand its interventional oncology portfolio, particularly therapies related to liver-directed embolization procedures.

- March 2024: Boston Scientific Corporation received U.S. FDA approval for the AGENT drug-coated balloon, a first-in-class device for treating coronary in-stent restenosis, supporting minimally invasive vascular interventions.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 2.1 Bn |

| Forecast Value (2035) |

USD 4.1 Bn |

| CAGR (2026–2035) |

8.0% |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors, etc. |

| Segments Covered |

By Product Type (Coils, Non-Coil Devices, Accessories), By Material Composition (Platinum-based Devices, Nitinol-based Devices, Polymer / Hydrogel-based Agents, Bio-resorbable Polymers), By Application (Oncology, Peripheral Vascular Disease, Neurology, Urology, Others), By End User (Hospitals & Clinics, Ambulatory Surgical Centers, Others) |

| Country Coverage |

The US |

| Prominent Players |

Boston Scientific Corporation, Medtronic plc, Terumo Corporation (MicroVention, Inc.), Stryker Corporation, Johnson & Johnson (Cerenovus), Penumbra, Inc., Cook Group Incorporated (Cook Medical LLC), Merit Medical Systems, Inc., W. L. Gore & Associates, Inc., Abbott Laboratories, AngioDynamics, Inc., B. Braun Melsungen AG, Becton, Dickinson and Company (Bard Peripheral Vascular), CDWT Holding LLC (Sirtex Medical), Balt Group (Balt International), Teleflex Incorporated, Kaneka Corporation, Siemens Healthineers AG (Varian Medical Systems, Inc.), Asahi Intecc Co., Ltd., MicroPort Scientific Corporation and Other Key Players |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users) and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days and 5 analysts working days respectively. |

Frequently Asked Questions

How big is the US Transcatheter Embolization And Occlusion Devices Market?

▾ The US Transcatheter Embolization And Occlusion Devices Market is valued at USD 2.1 billion in 2026 and is projected to reach USD 4.1 billion by the end of 2035.

What is the growth rate for the US Transcatheter Embolization And Occlusion Devices Market?

▾ The market is growing at a robust compound annual growth rate (CAGR) of 8.0% over the forecast period of 2026 to 2035.

Who are the key players in the US Transcatheter Embolization And Occlusion Devices Market?

▾ Some of the major key players in the US Transcatheter Embolization And Occlusion Devices Market are Boston Scientific Corporation, Medtronic plc, Stryker Corporation, Terumo Corporation, Johnson & Johnson (Cerenovus), Penumbra, Inc., and many others.