What is the Vehicle to Grid Market Size?

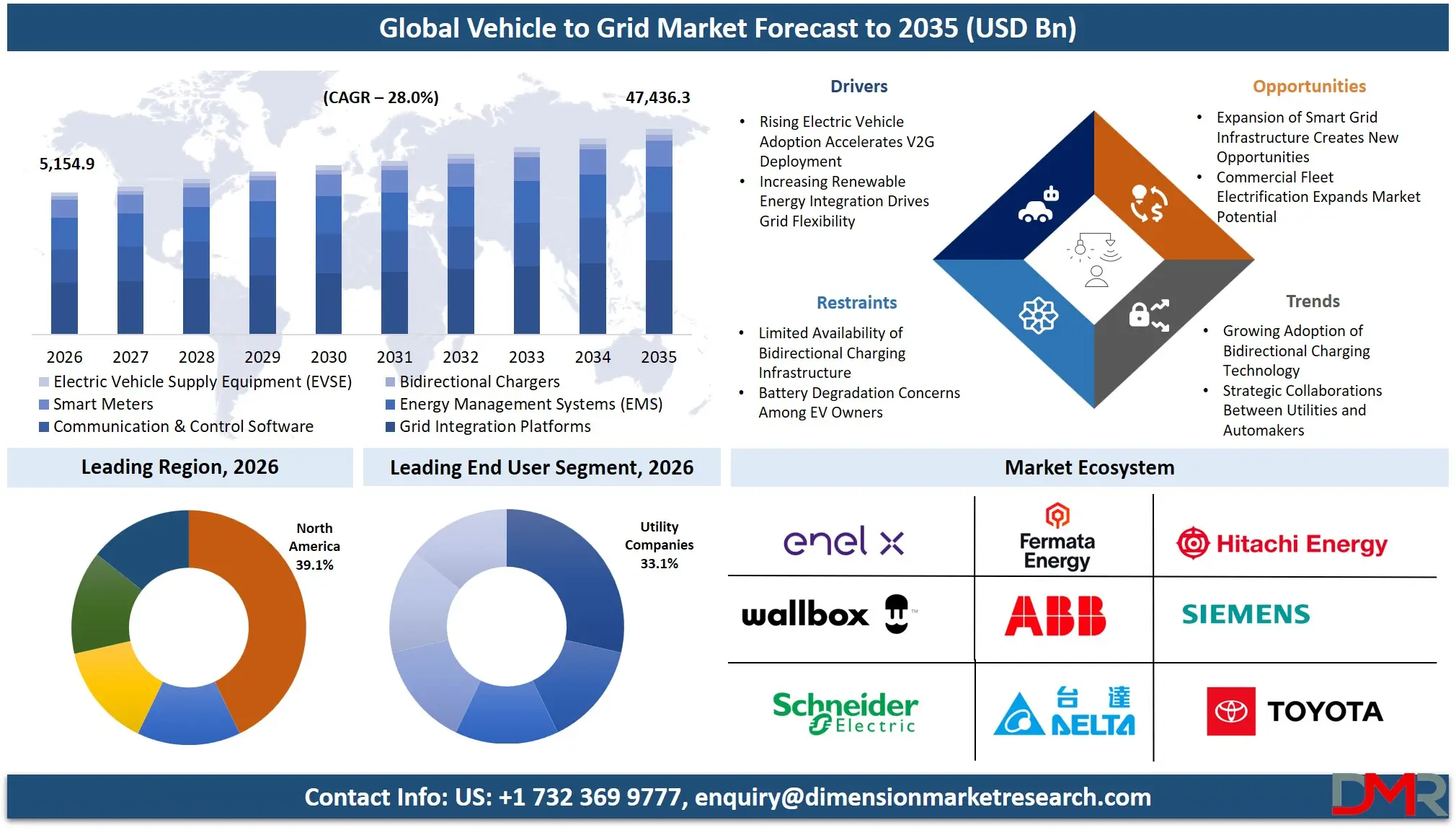

The Global Vehicle-to-Grid (V2G) Market is expected to reach a value of USD 5,154.9 million in 2026, and it is further anticipated to reach to USD 47,436.3 million by 2035, growing at a CAGR of 28.0% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

There are exponential opportunities for the V2G market as the merging of electric mobility and the emergence of smart grids has transformed the energy ecosystem. The market entails a dynamic energy ecosystem of energy flow, whereby electric vehicles act as distributed energy storage assets that can both take energy from and give energy back to the grid. The increased adoption of renewable energy sources in combination with the necessity of stabilizing and balancing the grid through the management of peak loads is leading to an increased demand for hardware, software, and services within the V2G domain.

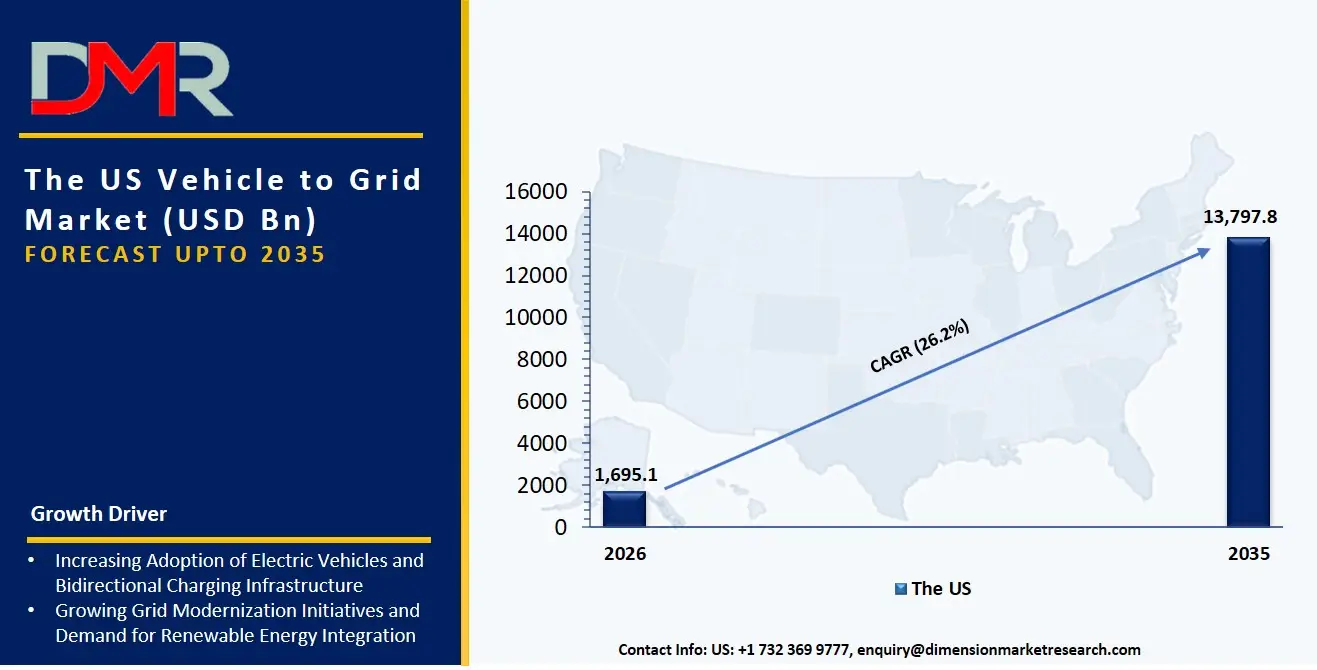

The US Vehicle to Grid Market

The US V2G Market is projected to reach USD 1,695.1 million in 2026 at a compound annual growth rate of 26.2% over its forecast period, culminating in a value of USD 13,797.8 million by 2035. The US is the market leader when it comes to the development of V2G technologies due to stringent state-wide Renewable Portfolio Standards and the adoption of electric school buses and commercial fleets across the country.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

It is notable that there is a significant demand for frequency regulation and demand response services, where the batteries of the electric vehicles are able to provide essential ancillary services to balance transmission grids. Additionally, there is an urgent need for cybersecurity protocols and grid integration platforms owing to the emergence of advanced communication and control software.

The Europe Vehicle to Grid Market

The Europe V2G Market is estimated to be valued at USD 1,491.6 million in 2026 and is further anticipated to reach USD 13,018.6 million by 2035 at a CAGR of 27.2%. The European market is strongly influenced by decarbonization directives including "Fit for 55" packages and quick deployment of offshore wind farms, making it a necessity to have distributed energy storage. Quick rollout of AC/DC Bidirectional Chargers is observed in the region, especially in the UK and the Netherlands, as pilots get transformed into a commercially feasible Virtual Power Plants (VPP). Furthermore, smart charging obligations for the supply of EVs have been posing challenges to technology vendors to come up with Energy Management Systems that enable data interoperability and grid balancing throughout the entire European network.

The Japan Vehicle to Grid Market

The Japan V2G Market is projected to be valued at USD 567.0 million in 2026. It is further expected to witness robust growth, holding USD 4,698.8 million in 2035 at a CAGR of 26.5%. This market is highly specific because of the national strategy that prioritizes the development of an energy secure nation after the Fukushima event and establishment of a hydrogen and electricity-based society. The segment of Emergency Backup and Distribution Services accounts for a large share of the market value as the country strives to design a disaster-resistant energy system through the use of its growing stock of Battery Electric Vehicles (BEVs) and Fuel Cell Electric Vehicles (FCEVs). Another important challenge to meet is that of integrating deeply into the local environment in order to make up for the deficiencies of the legacy grid and Smart Meters systems.

Key Takeaways

- Market Size & Forecast: The Global V2G market is projected to reach USD 5,154.9 million in 2026, expanding meteorically to USD 47,436.3 million by 2035, fueled by the dual catalysts of mass EV adoption and the critical need to buffer a renewables-heavy electrical grid.

- Growth Rate & Outlook: Global market growth is expected at a CAGR of 28.0%, driven by a critical shortage of integrated hardware-software solutions and the escalating complexity of managing bidirectional power flows and real-time energy arbitrage.

- Primary Growth Drivers: Key forces include the widespread shift from unidirectional to bidirectional charging infrastructure, the need for Frequency Response & Reserve services to mitigate grid instability, and the integration of AI-driven predictive analytics within Energy Management Systems to optimize charge/discharge cycles against wholesale electricity prices.

- Key Market Trends: Major trends include the rise of turnkey V2G platforms for commercial fleets, the use of blockchain-based settlement layers within Communication & Control Software to ensure transparent financial transactions, and the shift toward standardized plug-and-charge protocols as regulators prioritize interoperability and consumer safety.

- By Charger Type Analysis: DC Bidirectional Chargers are expected to dominate high-power commercial and fleet applications due to their inherent grid-forming capabilities and faster response times. Professional services are increasingly required to engineer the complex thermal management and power conversion systems that connect high-voltage vehicle batteries directly to distribution transformers.

- By Application Analysis: Frequency Regulation and Demand Response are the most lucrative applications due to the instantaneous response capability of EV batteries. Energy Arbitrage is the fastest-growing segment as volatile electricity markets create strong financial incentives for storing low-cost renewable energy and discharging it during peak price periods.

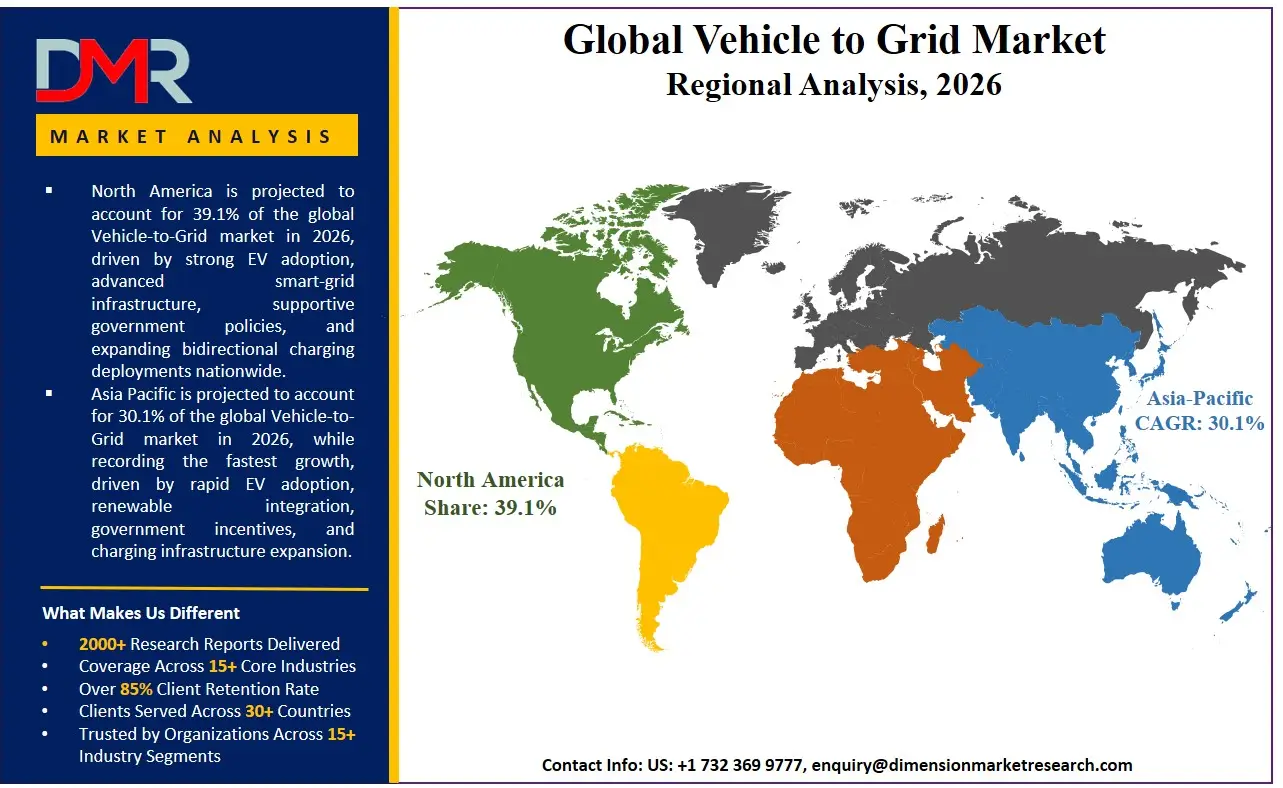

- Regional Leadership: North America is poised to dominate this market with 39.1% of the market share in 2026 due to its advanced electricity market structures that monetize fast-responding frequency regulation services, making it a leader in this market.

What is the Vehicle-to-Grid (V2G)?

Vehicle-to-Grid (V2G) Professional Services are the specialized consulting, system integration, and technical implementation services offered by third-party experts, engineering firms, and digital solution providers to assist stakeholders across the e-mobility and energy value chain. These services, unlike the physical hardware (the bidirectional charger or vehicle itself), are related to the how of V2G deployment. This involves designing grid integration studies, establishing cybersecurity frameworks for communication protocols, customizing Energy Management Systems for fleet aggregation, and deploying Grid Integration Platforms that allow utilities to orchestrate thousands of distributed energy resources. With global EV penetration accelerating rapidly, professional services are required to achieve seamless interoperability between diverse vehicle OEMs, charging hardware, and utility backends, ensuring that V2G investments translate into tangible grid resilience and new revenue streams, rather than technical incompatibility.

Use Cases

- School Bus Fleet Electrification in North America: School districts hire system integrators to deploy Bidirectional DC Chargers and specialized Energy Management Systems (EMS). These services orchestrate aggregated bus batteries to provide Demand Response during peak summer afternoons, generating revenue while ensuring the buses are fully charged for morning routes.

- Commercial Fleet-as-a-Storage in Logistics: Logistics companies utilize Communication & Control Software platforms to perform Energy Arbitrage, automatically charging depot-based BEV fleets during negative-pricing solar hours and discharging back to the grid during evening peak demand, turning a cost center into a profit center.

- Residential Virtual Power Plant (VPP) Integration: Homeowners are equipped with Smart Meters and AC Bidirectional Chargers integrated into a utility-run VPP. Professional services provide the firmware updates and grid integration protocols, allowing the utility to draw power for Emergency Backup during storm-induced outages.

- Island Microgrid Stabilization: On islands with high solar penetration, Grid Integration Platforms manage a mixed fleet of BEVs and stationary batteries, using V2G services for Time Shifting. This displaces diesel generators by absorbing excess midday solar and providing frequency stabilization during the evening ramp.

How AI is Transforming the Vehicle to Grid Market?

AI is fundamentally transforming V2G professional services by enabling predictive optimization and autonomous grid interaction. In Energy Management Systems, AI-driven forecasting tools are moving beyond simple schedules to predict individual vehicle availability, driver behavior, and real-time locational marginal pricing, dynamically optimizing bidding strategies into wholesale energy markets to maximize Energy Arbitrage profits. Meanwhile, AI-powered modules within Communication & Control Software are essential for real-time anomaly detection, using pattern recognition to differentiate between normal battery degradation and a cybersecurity intrusion vector on a bidirectional charger, thereby maintaining grid security. Governance and strategic planning projects are also revolving around AI. In the realm of grid planning, intelligent digital twin platforms simulate the impact of millions of EVs on distribution transformers, allowing utilities to defer costly infrastructure upgrades. Moreover, generative AI assistants are streamlining Distribution Services by automatically dispatching and adjusting reactive power from EV inverters to maintain voltage levels autonomously across low-voltage feeder lines.

Market Dynamics

Key Drivers in the Global Vehicle-to-Grid Market

Rising Electric Vehicle Adoption Accelerates V2G Deployment

The rapid adoption of battery electric vehicles worldwide is a primary driver of the Vehicle-to-Grid (V2G) market. Governments are promoting EV ownership through purchase incentives, stricter emission regulations, and investments in charging infrastructure. As the number of electric vehicles increases, their combined battery capacity creates a significant distributed energy resource that can support electricity grids. Utilities increasingly recognize EVs as mobile energy storage systems capable of supplying electricity during peak demand while charging during off-peak hours. This improves grid stability, lowers operating costs, and creates additional income opportunities for EV owners, encouraging wider deployment of V2G technologies across residential, commercial, and utility applications.

Increasing Renewable Energy Integration Drives Grid Flexibility

The growing deployment of renewable energy sources such as solar and wind is increasing demand for flexible energy storage solutions. Since renewable power generation is intermittent, utilities require fast-response resources to balance electricity supply and demand. Vehicle-to-Grid technology enables connected electric vehicles to store excess renewable electricity and return it to the grid whenever generation declines. This capability reduces renewable energy curtailment while improving overall grid reliability. Governments and grid operators increasingly support V2G pilot projects because they strengthen energy resilience without requiring large investments in stationary battery storage. The transition toward cleaner electricity systems continues to accelerate demand for V2G-enabled infrastructure.

Restraints in the Global Vehicle-to-Grid Market

Limited Availability of Bidirectional Charging Infrastructure

Despite growing interest in Vehicle-to-Grid technology, the availability of bidirectional charging infrastructure remains limited across many countries. Most existing EV charging stations support only one-way charging, requiring costly hardware upgrades for V2G compatibility. Utilities and charging operators must also invest in communication systems, cybersecurity, and grid integration technologies before commercial deployment becomes viable. High installation costs discourage smaller businesses and residential users from adopting bidirectional chargers. Furthermore, inconsistent charging standards across manufacturers create interoperability challenges that delay implementation. These infrastructure limitations continue to slow widespread commercialization despite increasing demand for grid-connected electric vehicle solutions.

Battery Degradation Concerns Among EV Owners

Many electric vehicle owners remain concerned that frequent charging and discharging through Vehicle-to-Grid applications could accelerate battery degradation and reduce vehicle lifespan. Although several studies suggest controlled V2G operation has limited long-term impact, consumer uncertainty continues to affect adoption. Vehicle owners often prioritize battery health because battery replacement represents one of the most expensive ownership costs. Automakers also vary in their warranty policies regarding bidirectional charging, creating additional hesitation. Until manufacturers provide standardized warranties, improved battery management systems, and stronger evidence supporting minimal degradation, consumer confidence may remain a significant barrier to large-scale V2G participation.

Growth Opportunities in the Global Vehicle-to-Grid Market

Expansion of Smart Grid Infrastructure Creates New Opportunities

Rapid investments in smart grid modernization are creating significant opportunities for the Vehicle-to-Grid market. Utilities worldwide are deploying advanced metering infrastructure, digital grid management platforms, and intelligent energy management systems capable of integrating distributed energy resources. Vehicle-to-Grid technology complements these developments by enabling electric vehicles to participate in automated demand response, frequency regulation, and peak load management programs. Governments are also supporting digital grid transformation through funding initiatives and energy transition policies. As smart grid deployment expands across developed and emerging economies, demand for V2G-compatible charging infrastructure and software platforms is expected to increase substantially.

Commercial Fleet Electrification Expands Market Potential

The growing electrification of commercial fleets presents a major growth opportunity for Vehicle-to-Grid technology. Delivery companies, public transportation operators, municipal fleets, and corporate vehicle owners typically maintain predictable charging schedules and centralized parking facilities, making them ideal participants in V2G programs. Large fleet batteries collectively provide substantial energy storage capacity that utilities can utilize for grid balancing services. Fleet operators also benefit from additional revenue generated through electricity trading and ancillary grid services. As governments promote zero-emission transportation and businesses pursue sustainability targets, commercial fleet electrification will significantly expand demand for scalable Vehicle-to-Grid solutions.

Trends in the Global Vehicle-to-Grid Market

Growing Adoption of Bidirectional Charging Technology

One of the most significant trends in the Vehicle-to-Grid market is the rapid advancement of bidirectional charging technology. Leading automotive manufacturers and charging equipment providers are introducing chargers capable of safely transferring electricity between vehicles and the power grid. Improvements in power electronics, communication protocols, and battery management systems have enhanced charging efficiency and interoperability. Increasing commercialization of bidirectional chargers supports wider participation in energy markets by residential users, businesses, and fleet operators. As hardware costs decline and charging standards mature, bidirectional charging is expected to become a standard feature within next-generation electric mobility infrastructure.

Strategic Collaborations Between Utilities and Automakers

Partnerships among utilities, electric vehicle manufacturers, charging infrastructure providers, and technology companies are becoming increasingly common across the Vehicle-to-Grid market. These collaborations accelerate pilot projects, establish interoperability standards, and develop commercially viable business models for bidirectional energy services. Automakers benefit by expanding vehicle functionality, while utilities gain access to flexible distributed energy resources that improve grid stability. Joint initiatives also encourage regulatory support and consumer awareness through real-world demonstrations of V2G capabilities. As public and private organizations continue collaborating, these strategic partnerships are expected to accelerate commercialization and large-scale deployment of Vehicle-to-Grid ecosystems worldwide.

Research Scope and Analysis

The Global Vehicle-to-Grid Market is segmented by Component, Service, Vehicle Type, Charger Type, Application, and End User. Components include EVSE, bidirectional chargers, smart meters, EMS, software, and grid platforms. Services cover frequency response, time shifting, distribution, backup, and arbitrage. Applications span grid optimization, while end users include residential, commercial, industrial, utilities, fleets, and public charging providers.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

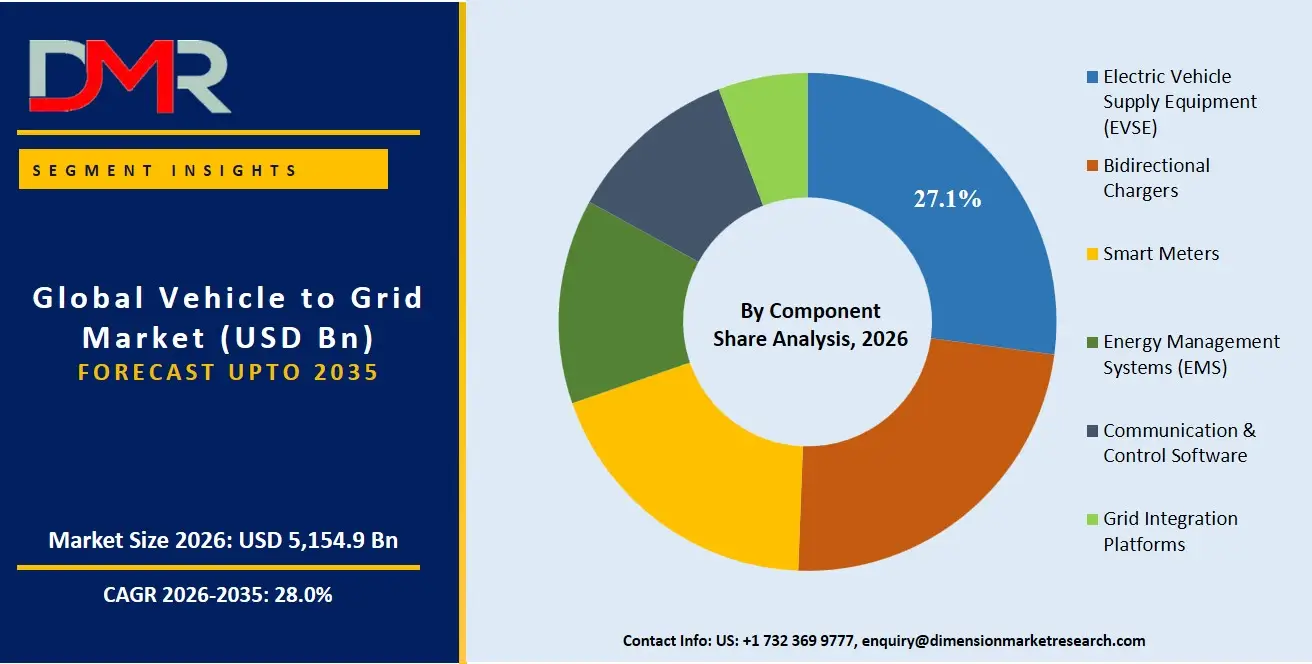

By Component Analysis

Electric Vehicle Supply Equipment (EVSE) is projected to dominate the component segment because it forms the physical foundation of every Vehicle-to-Grid (V2G) ecosystem. Utilities, businesses, and homeowners require compatible charging stations to enable bidirectional electricity flow between electric vehicles and power grids. Continuous investments in public and private charging infrastructure, government incentives supporting EV adoption, and increasing installation of smart chargers have accelerated EVSE deployment worldwide. Modern EVSE also integrates communication protocols, load balancing, remote monitoring, and energy management capabilities, making it essential for V2G operations. As EV ownership expands globally, demand for advanced charging equipment continues to outpace other supporting components, reinforcing EVSE's dominant market position.

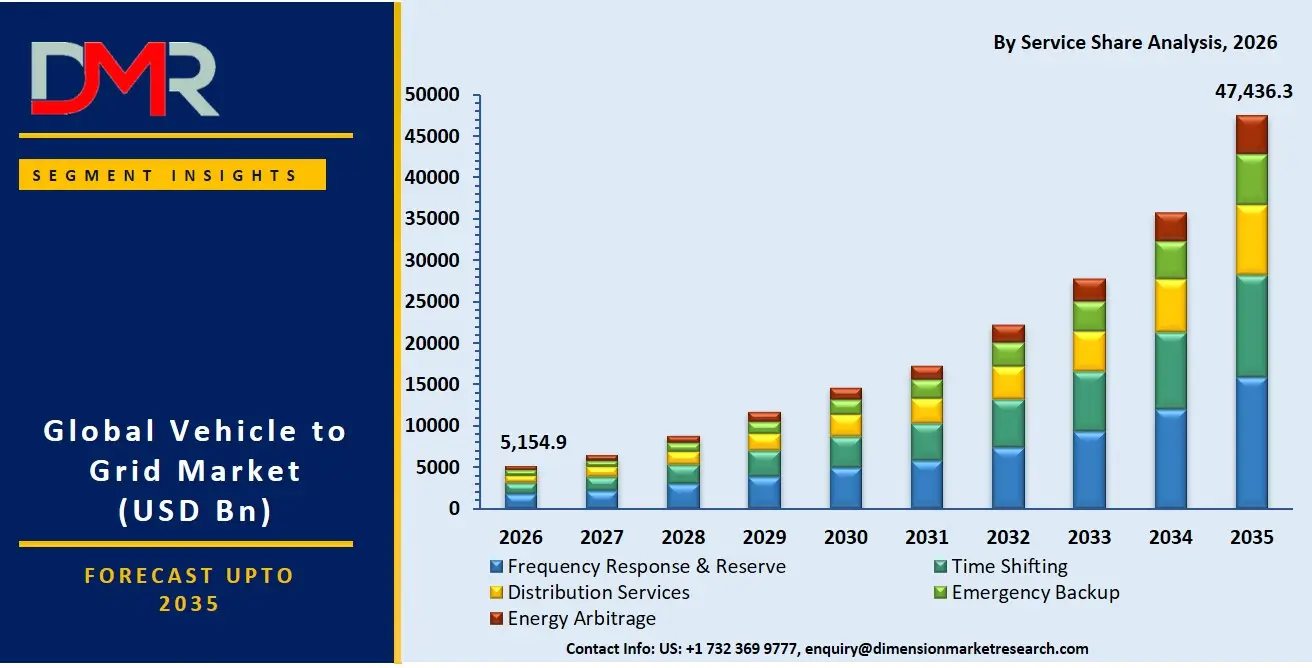

By Service Analysis

Frequency Response & Reserve is expected to lead the service segment because electrical grids require rapid balancing to maintain stable frequency amid fluctuating electricity demand and renewable energy generation. Vehicle-to-Grid technology enables connected electric vehicles to instantly inject or absorb electricity, providing highly responsive ancillary services.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Utilities value these services because they reduce dependence on expensive peaking plants while improving grid reliability. Since frequency regulation commands attractive financial returns for utilities and EV owners, many commercial V2G pilot programs prioritize this application. Growing renewable energy penetration further increases the need for flexible balancing resources, making Frequency Response & Reserve the most commercially established V2G service worldwide.

By Vehicle Type Analysis

Battery Electric Vehicles (BEVs) is poised to dominate the vehicle type segment because they possess larger battery capacities and are fully dependent on electricity, making them ideal participants in Vehicle-to-Grid programs. Unlike Plug-in Hybrid Electric Vehicles, BEVs can dedicate greater energy storage for bidirectional charging without relying on internal combustion engines. Rapid global adoption of BEVs, declining battery prices, expanding charging infrastructure, and government incentives continue to strengthen their market leadership. Major automotive manufacturers increasingly develop V2G-compatible BEVs equipped with intelligent charging systems. Their longer parking durations also provide utilities with greater energy flexibility, maximizing revenue opportunities and improving grid stability.

By Charger Type Analysis

AC Chargers is projected to dominate the charger type segment due to their affordability, widespread availability, and compatibility with residential and workplace charging environments where vehicles remain parked for extended periods. Vehicle-to-Grid applications generally require longer charging durations rather than ultra-fast charging, making AC systems highly suitable for bidirectional energy exchange. Utilities and homeowners also prefer AC chargers because installation costs are lower than DC charging infrastructure. Technological improvements in bidirectional AC charging further enhance market adoption. As residential smart charging expands globally and overnight charging remains the preferred charging behavior, AC chargers continue to represent the largest share of V2G installations.

By Application Analysis

Peak Load Management expected to dominate the application segment because utilities increasingly rely on Vehicle-to-Grid technology to reduce electricity demand during high-consumption periods. Electric vehicles function as distributed energy storage assets that discharge electricity back to the grid when demand spikes, reducing stress on transmission networks and minimizing the need for costly backup generation. This approach improves grid efficiency while lowering operational expenses and reducing carbon emissions. Utilities benefit from deferred investments in new infrastructure, while EV owners receive financial incentives for participating. Growing electricity consumption and renewable energy integration continue to strengthen Peak Load Management as the leading V2G application.

By End User Analysis

Utility Companies anticipated to dominate the end-user segment because they are the primary operators responsible for maintaining grid reliability, balancing electricity supply, and integrating renewable energy resources. Utilities actively invest in Vehicle-to-Grid infrastructure to improve demand response capabilities, stabilize frequency, reduce peak loads, and optimize energy distribution. Numerous commercial V2G projects worldwide are utility-led, often in collaboration with automakers, charging equipment manufacturers, and technology providers. Government policies supporting smart grids further encourage utility participation. Since utilities directly monetize grid services while improving operational efficiency, they remain the largest investors and adopters of Vehicle-to-Grid technologies globally.

The Global Vehicle to Grid Market Report is segmented on the basis of the following:

By Component

- Electric Vehicle Supply Equipment (EVSE)

- Bidirectional Chargers

- Smart Meters

- Energy Management Systems (EMS)

- Communication & Control Software

- Grid Integration Platforms

By Service

- Frequency Response & Reserve

- Time Shifting

- Distribution Services

- Emergency Backup

- Energy Arbitrage

By Vehicle Type

- Battery Electric Vehicles (BEVs)

- Plug-in Hybrid Electric Vehicles (PHEVs)

- Fuel Cell Electric Vehicles (FCEVs)

By Charger Type

By Application

- Peak Load Management

- Frequency Regulation

- Demand Response

- Renewable Energy Integration

- Backup Power Supply

- Energy Arbitrage

By End User

- Residential

- Commercial

- Industrial

- Utility Companies

- Fleet Operators

- Public Charging Infrastructure Providers

Regional Analysis

Leading Region by Market Share

ℹ

To learn more about this report –

Download Your Free Sample Report Here

North America is poised to dominate the global V2G market as it is projected to hold 39.1% of the market share by the end of 2026. The United States, which dominates North America, has the highest share in the V2G market because of its unparalleled structure of deregulated wholesale energy markets, notably in regions managed by PJM Interconnection and ERCOT, which offer clear market-based compensation for fast-responding frequency regulation. The area has an established ecosystem of pioneering EV manufacturers, specialized power electronics firms, and a rich pool of electrical and software engineering talent. Utility investment in distribution-level smart grid modernization, rapid electrification of school bus and delivery fleets, and the overall retirement of fossil fuel peaker plants contribute to the continued demand for bidirectional hardware deployment, EMS platform customization, and ongoing managed services. Moreover, a favorable policy environment, including state-level mandates and federal infrastructure funding, persistently finances nascent V2X pilots that need expert professional services to achieve scalable and cybersecure deployment.

Fastest-Growing Regional Market

Asia-Pacific is expected to be the most rapidly expanding V2G market, driven by the government-led sweeping grid modernization and EV adoption targets in China, Japan, South Korea, and India. The fast-paced urbanization, the explosive growth in renewable energy capacity, and the dynamic expansion of the electric two-wheeler and three-wheeler market is compelling established state-owned utilities and private conglomerates to build digitally native, resilient grid architectures. Business transformation consulting is in high demand to help these large organizations pivot towards distributed energy resource management models. There is also a severe lack of qualified power systems and software integration talent in the region, making it necessary to outsource professional services for the deployment of Grid Integration Platforms, advanced metering infrastructure, and managed security operations to fill the skills gap and enable faster, safer investments in large-scale V2G aggregation projects.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The competitive environment of the global V2G market has become highly dynamic, with a heterogeneous array of multinational power equipment conglomerates, dedicated automotive OEM energy divisions, and niche AI-driven software startups. The key to success is proving deep strategic alliances with automotive giants like Ford, GM, or Hyundai to ensure vehicle-side integration, as well as with utilities like Enel or E.ON to open the necessary co-selling opportunities for grid-side orchestration. The movement towards market consolidation is rapidly progressing, with traditional electrical infrastructure companies acquiring specialized IoT communication and AI-based trading platform specialists to remain competitive. Proprietary intellectual property, including automated trading algorithms, battery-safe cycling protocols, and V2G-specific vehicle telematics interfaces, is becoming a more important basis of competitive differentiation than just charging hardware commoditization or generic installation services.

Some of the prominent players in the Global Vehicle to Grid Market are:

- Nuvve Holding Corp.

- Fermata Energy

- Enel X

- ABB Ltd.

- Siemens AG

- Schneider Electric

- Hitachi Energy

- Wallbox N.V.

- Delta Electronics, Inc.

- Toyota Motor Corporation

- Nissan Motor Co., Ltd.

- Mitsubishi Motors Corporation

- Honda Motor Co., Ltd.

- Ford Motor Company

- General Motors Company

- Volkswagen AG

- Hyundai Motor Company

- BMW AG

- DENSO Corporation

- The Mobility House

- Other Key Players

Recent Developments

- March 2026: Nuvve Holding Corp. announced a major expansion of its GIVe™ (Grid Integrated Vehicle) platform, launching a specialized professional services initiative to assist utility companies in California and Texas with aggregating electric school bus fleets for Frequency Regulation and Demand Response.

- December 2025: Siemens strengthened its collaboration with a leading European automotive OEM, introducing a dedicated practice for Grid Integration Platforms and cybersecurity-hardened Bidirectional Chargers. This practice is specifically designed to support Fleet Operators and Public Charging Infrastructure Providers in deploying ISO 15118-20 compliant DC charging hubs that can perform Energy Arbitrage and Peak Load Management.

- October 2025: The Mobility House acquired a specialized AI-driven battery analytics firm to enhance its Energy Arbitrage and Time Shifting service offerings. The acquisition aims to integrate deep battery state-of-health predictive algorithms into its Energy Management Systems, creating a warranty-safe cycling protocol that directly addresses OEM and consumer battery degradation anxiety.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 5.6 Bn |

| Forecast Value (2035) |

USD 35.3 Bn |

| CAGR (2026–2035) |

22.8% |

| The US Market Size (2026) |

USD 1.8 Bn |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Component, By Service, By Vehicle Type, By Charger Type, By Application, and By End User |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Global Vehicle-to-Grid Market?

▾ The Global Vehicle-to-Grid market is poised to be valued at USD 5,154.9 million in 2026 and is projected to reach USD 47,436.3 million by 2035, driven by the universal need for grid stability amidst the renewable energy transition and mass EV deployment.

What is the CAGR of the Global Vehicle-to-Grid Market from 2026 to 2035?

▾ The market is expected to grow at a CAGR of 28.0% from 2026 to 2035, reflecting the accelerating complexity of decentralized energy systems and the persistent monetization of dormant EV battery storage capacity.

What factors are driving the growth of the Global Vehicle-to-Grid Market?

▾ Key drivers include the unbundling of ancillary services markets, the imperative to integrate intermittent renewable generation, the management complexity of bi-directional power flows, and the surge in demand for Energy Arbitrage amid volatile electricity pricing.

Which region held the largest share of the Vehicle-to-Grid Market in 2026?

▾ North America, specifically the United States, held 39.1% of the market share in 2026, driven by mature competitive wholesale electricity markets and aggressive investment in electric school bus and fleet electrification as mobile storage assets.

Which region is expected to grow the fastest in the Vehicle-to-Grid Market?

▾ The Asia-Pacific region is expected to grow the fastest, fueled by rapid EV adoption and grid infrastructure investment in China and India, where Energy Management Systems are critical for managing densely populated urban grid loads.

What are the major trends in the Global Vehicle-to-Grid Market?

▾ Major trends include the integration of AI into energy trading platforms, the convergence of V2G into a broader Vehicle-to-Everything (V2X) platform, the standardization of ISO 15118-20 protocols, and the focus on battery-safe cycling algorithms within complex fleet management software.

Who are the key players in the Global Vehicle-to-Grid Market?

▾ Key players include global power technology firms like ABB and Siemens, automotive OEMs like Tesla and Nissan, dedicated V2G platform providers like Nuvve and The Mobility House, alongside large energy utilities establishing new decentralized energy service divisions.

How is the Global Vehicle-to-Grid Market segmented?

▾ The market is segmented by Component, Service, Vehicle Type, Charger Type, Application, and End User.