Market Overview

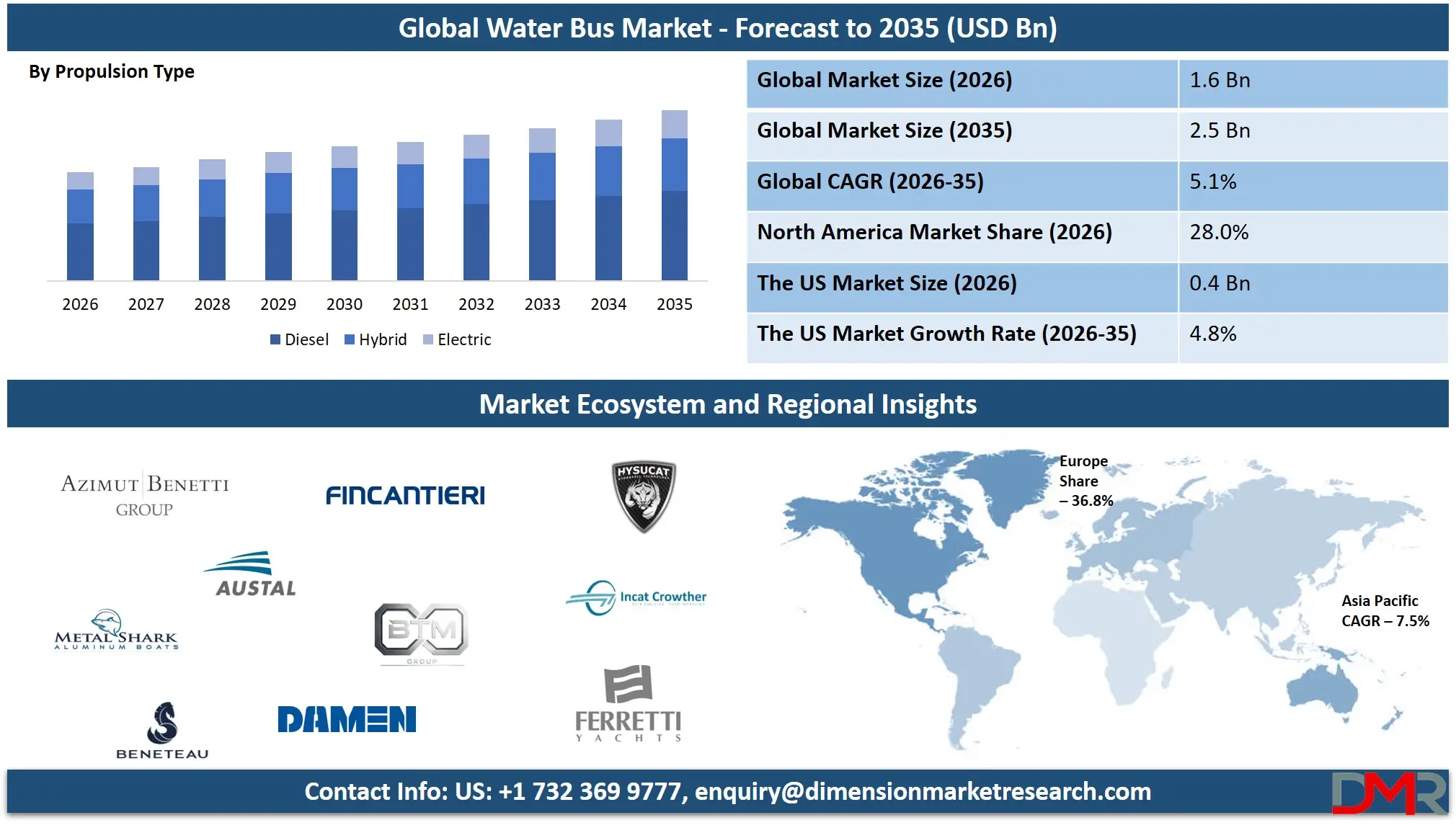

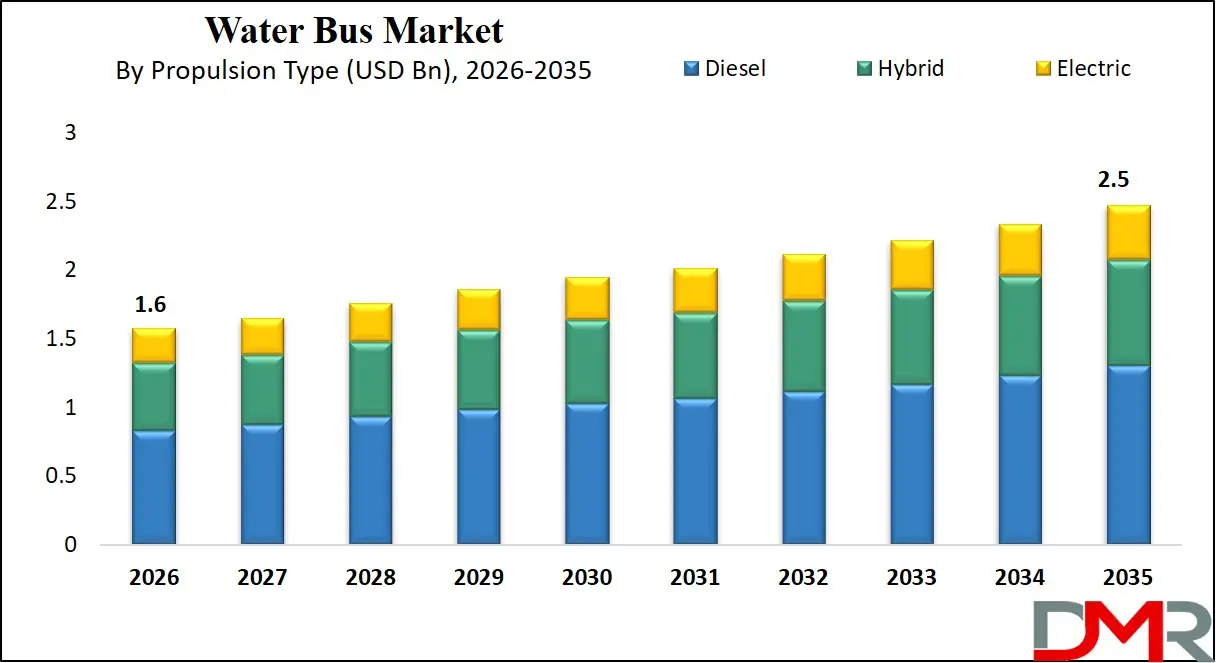

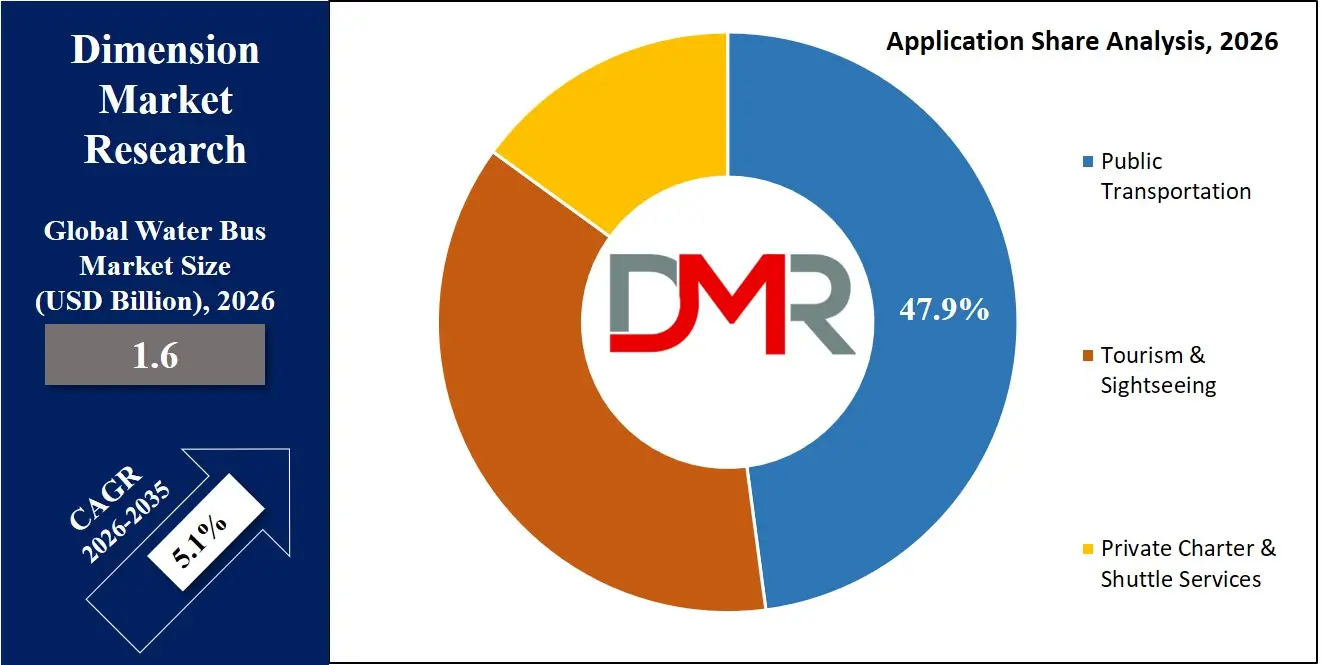

The Global Water Bus Market size is projected to reach USD 1.6 billion in 2026 and grow at a compound annual growth rate of 5.1% to reach a value of USD 2.5 billion in 2035.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

A water bus is a passenger transport vessel designed to operate on rivers, canals, lakes, and coastal waterways, providing scheduled urban or intercity mobility services. These vessels typically function as part of public transportation systems and are designed to carry multiple passengers efficiently across water routes. Water buses are equipped with features such as passenger seating, safety systems, navigation technology, and docking compatibility to ensure reliable operations. They may operate using diesel, hybrid, or fully electric propulsion systems, depending on environmental regulations and technological adoption. Water buses play an important role in cities with extensive waterways by providing an alternative mode of transport that reduces road congestion and enhances connectivity between waterfront districts.

The growing focus on sustainable urban mobility is encouraging cities to reconsider water-based transportation systems. Advancements in marine propulsion technologies, including hybrid and electric propulsion, are supporting environmentally friendly operations and reducing fuel consumption and emissions. Governments and urban planners are integrating water buses into multimodal transport networks alongside metro systems, buses, and railways. Smart navigation systems, automated ticketing, and improved port infrastructure are also improving passenger experience and operational efficiency. Increasing tourism activities in waterfront cities are further encouraging investments in modern water bus fleets.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Significant developments have been observed in the deployment of electric vessels, infrastructure upgrades, and public–private partnerships aimed at expanding water-based transit networks. Many cities are investing in new terminals, digital fleet management solutions, and environmentally compliant vessels to meet climate targets. Shipbuilders and technology providers are collaborating to design vessels with improved fuel efficiency, lightweight materials, and advanced safety features. These initiatives are transforming water buses into an increasingly reliable and sustainable transport solution, contributing to the modernization of urban mobility systems across global waterfront regions.

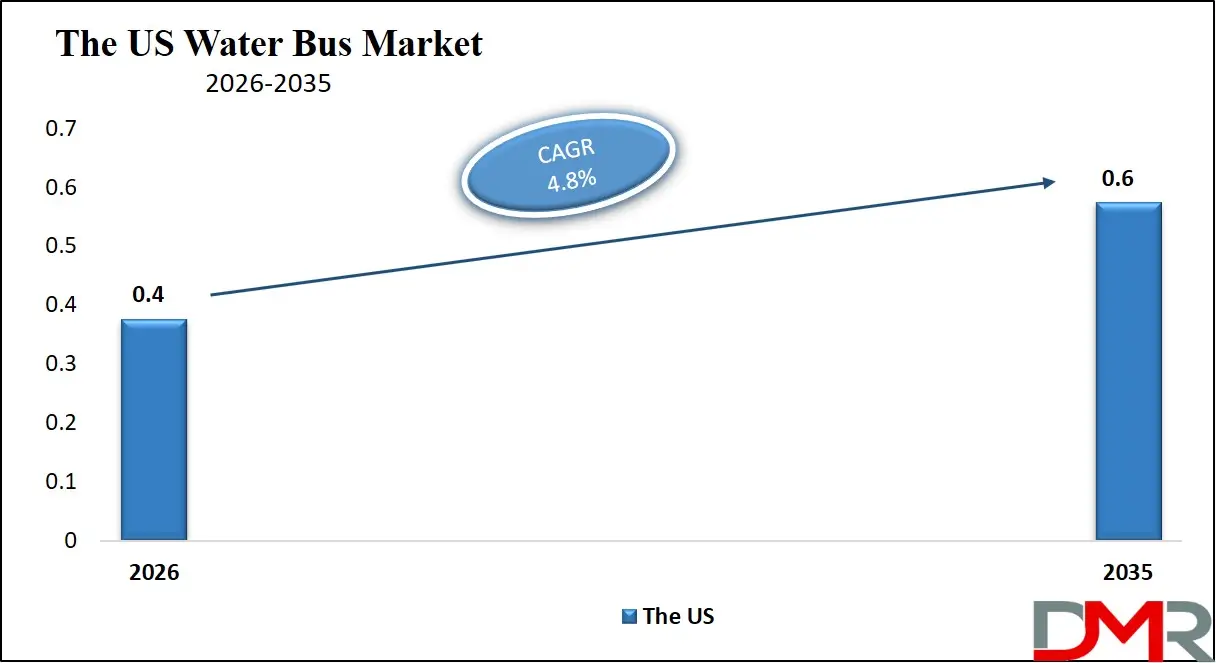

The US Water Bus Market

The US Water Bus Market size is projected to reach USD 400 million in 2026 at a compound annual growth rate of 4.8% over its forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The US water bus market is gradually expanding as cities explore alternative transport systems to reduce traffic congestion and improve urban mobility. Coastal cities and metropolitan regions with navigable waterways are increasingly evaluating water-based public transit solutions. Investments in sustainable marine transport, including electric and hybrid propulsion vessels, are gaining momentum due to strict environmental regulations and emission reduction targets. Local authorities are focusing on upgrading ferry terminals, integrating ticketing systems with urban transit networks, and improving last-mile connectivity. Public-private partnerships are also emerging as a key strategy to finance infrastructure development and fleet modernization. Tourism-driven routes in cities such as waterfront metropolitan areas are further supporting demand, while technological integration in navigation and vessel monitoring is improving operational efficiency and safety standards across water bus services.

Europe Water Bus Market

Europe Water Bus Market size is projected to reach USD 580 million in 2026 at a compound annual growth rate of 4.5% over its forecast period.

The Europe water bus market is strongly influenced by sustainability policies and environmental regulations across the region. European countries are actively promoting low-emission transport systems, which is encouraging the adoption of electric and hybrid water buses. Urban centers with extensive waterways are integrating water transport within public mobility networks to support congestion reduction and carbon neutrality goals. Infrastructure modernization, including advanced docking systems and smart ticketing platforms, is enabling seamless passenger travel. Maritime innovation hubs are also developing next-generation vessel designs with lightweight materials and improved energy efficiency. Tourism remains a major contributor to water bus demand across historic cities with canal networks and riverfront attractions. The region's emphasis on green mobility initiatives and investments in sustainable marine transport solutions is expected to sustain long-term market growth.

Japan Water Bus Market

Japan Water Bus Market size is projected to reach USD 80 million in 2026 at a compound annual growth rate of 5.0% over its forecast period.

Japan's water bus market is supported by strong maritime expertise, advanced shipbuilding capabilities, and government initiatives aimed at improving urban transport infrastructure. Cities with extensive coastal and river networks are exploring water buses as complementary transport options to alleviate congestion in densely populated urban areas. Technological innovation plays a central role in the market, with operators adopting efficient propulsion systems, improved safety mechanisms, and modern vessel designs. Japan's tourism industry also contributes significantly to demand, as water buses are widely used for sightseeing and harbor transportation. Government-backed initiatives encouraging environmentally friendly marine transportation are accelerating the adoption of hybrid and electric vessels. However, challenges such as high operational costs and infrastructure upgrades remain key considerations for large-scale deployment of water bus services.

Water Bus Market: Key Takeaways

- Market Growth: The Water Bus Market size is expected to grow by USD 800 million, at a CAGR of 5.1%, during the forecasted period of 2027 to 2035.

- By Propulsion Type: The diesel segment is anticipated to get the majority share of the Water Bus market in 2026.

- By Application: The public transportation segment is expected to get the largest revenue share in 2026 in the Water Bus market.

- Regional Insight: Europe is expected to hold a 36.8% share of revenue in the global Water Bus market in 2026.

- Use Cases: Some of the use cases of Water Bus include island connectivity, event transportation, and more.

Water Bus Market: Use Cases:

- Urban Public Transportation: Water buses serve as scheduled public transport systems across rivers, lakes, and canals in major cities. They help reduce traffic congestion while providing efficient commuting options between waterfront districts.

- Tourism & Sightseeing Services: Tour operators widely use water buses for sightseeing tours in cities with iconic waterways, offering scenic travel experiences for tourists while connecting major attractions.

- Island Connectivity: Water buses provide reliable transport links between mainland cities and nearby islands, supporting both daily commuting and economic activities.

- Event Transportation: During festivals, large public events, and waterfront celebrations, water buses help manage increased passenger traffic by offering temporary or additional routes.

- Corporate Shuttle Services: Some metropolitan regions utilize water buses as corporate transport solutions, enabling employees to travel efficiently between business districts located along waterways.

- Emergency & Disaster Mobility: Water buses can function as emergency transport during floods or infrastructure disruptions, ensuring mobility when road networks are compromised.

- Eco-Friendly Urban Mobility: Electric or hybrid water buses are increasingly used as sustainable mobility options to support low-emission transport initiatives in environmentally conscious cities.

Stats & Facts

- International Energy Agency (IEA) reported in 2024 that global transport accounts for nearly 23% of energy-related CO₂ emissions, encouraging governments to expand low-carbon transport alternatives including water transport systems.

- European Commission stated in 2024 that the maritime sector must reduce greenhouse gas emissions by at least 55% by 2030, driving investments in electric and hybrid vessels used in urban waterways.

- U.S. Department of Transportation reported in 2024 that ferry and water transit systems in the United States carried over 80 million passengers annually, highlighting the importance of water-based transport networks.

- International Maritime Organization (IMO) announced in 2025 that shipping emissions must reach net-zero around 2050, accelerating the development of cleaner propulsion systems for passenger vessels.

- Eurostat reported in 2024 that inland waterways in the European Union extend over 41,000 kilometers, providing substantial potential for passenger and commuter water transport services.

- Japan Ministry of Land, Infrastructure, Transport and Tourism (MLIT) recorded in 2024 that Japan operates over 700 passenger vessels for domestic water transport, including ferries and sightseeing boats.

- World Bank reported in 2024 that urban congestion costs cities up to 3–4% of GDP, encouraging governments to diversify transportation infrastructure including waterways.

- International Transport Forum (ITF) reported in 2025 that sustainable urban mobility initiatives could reduce transport emissions by up to 70% by 2050 through multimodal transport integration.

- United Nations Conference on Trade and Development (UNCTAD) noted in 2024 that maritime transport handles around 80% of global trade by volume, reinforcing the strategic importance of marine transport infrastructure.

- Asian Development Bank (ADB) stated in 2024 that investments in sustainable urban transport infrastructure across Asia exceeded USD 40 billion annually, supporting expansion of water-based mobility systems.

- U.S. Environmental Protection Agency (EPA) reported in 2025 that switching to electric marine propulsion can reduce vessel emissions by up to 90% in urban waterways.

- Organisation for Economic Co-operation and Development (OECD) reported in 2024 that urban populations living near coastlines and rivers are expected to reach over 1.8 billion people globally by 2050, creating strong demand for alternative water-based transport systems.

Market Dynamic

Driving Factors in the Water Bus Market

Growing Demand for Sustainable Urban Transportation

Urbanization and rising environmental concerns are encouraging governments to adopt sustainable transport alternatives, significantly driving the water bus market. Cities facing heavy traffic congestion are exploring water-based mobility as a complementary transport option that can efficiently move passengers without adding pressure to road infrastructure. Water buses help reduce carbon emissions, fuel consumption, and travel time in densely populated metropolitan regions. Furthermore, environmental policies promoting low-emission transport are accelerating the adoption of electric and hybrid water buses. Investments in eco-friendly vessels and green port infrastructure are strengthening the role of waterways in urban transit networks. As cities focus on climate goals and carbon neutrality targets, water buses are emerging as a practical and environmentally responsible transportation solution for future urban mobility systems.

Expansion of Waterfront Infrastructure and Tourism Activities

The growing development of waterfront areas and tourism destinations is another major factor driving the water bus market. Many cities with rivers, lakes, and coastal regions are investing in modern terminals, docking facilities, and navigation systems to support water-based transportation services. Tourism sectors are also integrating water buses into sightseeing and recreational travel routes, attracting visitors seeking scenic urban travel experiences. Governments and private operators are collaborating to introduce new water bus fleets designed for passenger comfort, safety, and energy efficiency. These developments are encouraging wider adoption of water transport systems while creating new revenue streams for municipal authorities and transport operators. The expansion of tourism infrastructure and urban waterfront redevelopment projects is therefore strengthening the demand for modern water bus services around the world.

Restraints in the Water Bus Market

High Infrastructure and Vessel Investment Costs

One of the major challenges in the water bus market is the high capital investment required for vessel procurement and infrastructure development. Water buses require specialized docking terminals, maintenance facilities, navigation systems, and safety equipment to operate efficiently. Establishing these facilities can involve substantial financial investment, particularly in cities where water transport infrastructure is limited or outdated. Additionally, advanced vessels powered by hybrid or electric propulsion technologies often involve higher upfront costs compared with conventional marine transport systems. These financial barriers may discourage small operators or municipal authorities from launching new water bus services. As a result, funding constraints and lengthy infrastructure development timelines can slow down the expansion of water-based passenger transport networks in several regions.

Operational Limitations and Weather Dependency

Water bus operations are highly dependent on environmental conditions and navigational constraints, which can limit service reliability. Weather conditions such as storms, heavy rainfall, fog, or strong currents may disrupt scheduled routes and impact passenger safety. Seasonal variations in water levels, especially in rivers and canals, can also affect navigation and vessel capacity. Additionally, waterways in some cities may face congestion from commercial shipping or recreational boating, creating operational challenges for passenger services. These limitations can make water buses less predictable compared with road or rail transport systems. Consequently, operators must invest in advanced navigation systems, weather monitoring technologies, and contingency planning to ensure safe and reliable service delivery.

Opportunities in the Water Bus Market

Adoption of Electric and Hybrid Propulsion Technologies

The transition toward electric and hybrid marine propulsion systems is creating significant growth opportunities for the water bus market. Governments worldwide are implementing strict emission regulations for marine transport, encouraging operators to replace conventional diesel vessels with environmentally friendly alternatives. Electric water buses offer advantages such as lower operating costs, reduced noise pollution, and minimal environmental impact. Advances in battery technology, charging infrastructure, and energy-efficient vessel design are further supporting the feasibility of electric water transport systems. As sustainability becomes a key priority in urban planning, the adoption of zero-emission vessels is expected to accelerate, creating new opportunities for shipbuilders, technology providers, and transport operators in the water bus sector.

Integration with Smart and Multimodal Transportation Systems

The integration of water buses with modern multimodal transport systems presents another promising opportunity for market growth. Cities are increasingly adopting integrated mobility platforms that connect buses, railways, metro systems, and water transport through unified ticketing and digital scheduling systems. Smart mobility technologies such as mobile ticketing, GPS-based vessel tracking, and automated passenger information systems are improving convenience and accessibility for commuters. This integration enables passengers to seamlessly switch between different transport modes during their daily journeys. By becoming part of comprehensive urban mobility networks, water buses can expand their role in public transportation and attract a broader user base, strengthening their position in sustainable urban transit ecosystems.

Trends in the Water Bus Market

Increasing Adoption of Smart Marine Technologies

The adoption of smart technologies is transforming the operational efficiency of water bus services. Modern vessels are being equipped with advanced navigation systems, real-time monitoring solutions, and automated fleet management platforms that improve route optimization and passenger safety. Digital ticketing systems and mobile applications are simplifying the travel experience for commuters by enabling seamless booking and payment processes. Additionally, predictive maintenance technologies powered by sensors and data analytics help operators monitor vessel performance and reduce downtime. These technological advancements are enabling operators to manage fleets more efficiently while ensuring higher reliability and improved passenger satisfaction in water bus transport systems.

Growing Focus on Eco-Friendly Vessel Design

Environmental sustainability is becoming a central trend shaping the water bus market. Shipbuilders are increasingly designing vessels with lightweight materials, energy-efficient hull structures, and advanced propulsion systems that minimize fuel consumption and emissions. Electric and hybrid propulsion technologies are gaining widespread adoption as cities aim to reduce air pollution and meet climate targets. Additionally, the use of renewable energy sources such as solar-assisted charging systems is being explored to further enhance vessel sustainability. These eco-friendly innovations are not only helping operators comply with environmental regulations but also improving operational efficiency and long-term cost savings in water bus transportation systems.

Impact of Artificial Intelligence in Water Bus Market

- Predictive Maintenance Systems: AI-powered analytics monitor vessel components and engine performance in real time, helping operators identify maintenance needs early and reduce unexpected downtime.

- Route Optimization: AI algorithms analyze passenger demand, waterway traffic, and weather patterns to optimize routes and schedules, improving operational efficiency and travel time.

- Smart Navigation Assistance: AI-based navigation tools enhance vessel safety by identifying obstacles, monitoring water conditions, and supporting real-time decision-making for captains.

- Passenger Demand Forecasting: AI models analyze historical travel data and seasonal tourism patterns to forecast passenger volumes and adjust fleet deployment accordingly.

- Autonomous Vessel Development: AI technologies are being explored for semi-autonomous or fully autonomous water buses, potentially improving safety and reducing operational costs.

- Energy Management Optimization: AI helps manage battery usage and power distribution in electric water buses, increasing operational range and efficiency.

- Enhanced Passenger Experience: AI-driven mobile applications provide personalized travel information, route updates, and ticketing services for passengers.

- Security and Surveillance: AI-enabled video monitoring systems enhance onboard safety by detecting suspicious activities and alerting operators in real time.

- Operational Analytics: AI platforms analyze operational data from multiple vessels to improve fleet performance, reduce fuel consumption, and support strategic planning.

Research Scope and Analysis

By Propulsion Type Analysis

Diesel-powered water buses currently represent the most widely deployed propulsion type due to their established technology, reliability, and extensive fueling infrastructure. In 2026, the diesel segment is expected to account for 52.6% of the global water bus market share. Many municipal and private operators continue to rely on diesel-powered vessels because they offer strong performance for medium and long-distance routes and require lower initial investment compared with hybrid or electric alternatives. Additionally, diesel engines remain suitable for large-capacity vessels operating in high-demand commuter routes. Despite growing environmental regulations, diesel-powered water buses remain dominant in regions where electric charging infrastructure for marine transport is still developing. However, operators are increasingly integrating fuel-efficient engines and emission-reduction technologies to comply with regulatory standards. While diesel propulsion continues to support large-scale fleet operations due to operational reliability and cost-effectiveness, its market share may gradually decline as sustainability policies accelerate the adoption of hybrid and electric propulsion systems across urban water transport networks.

Electric propulsion is emerging as the fastest-growing segment within the water bus market as governments and transport authorities intensify efforts to reduce emissions from marine transportation. Electric water buses operate using battery-powered propulsion systems, which significantly reduce greenhouse gas emissions and noise pollution in urban waterways. Cities aiming to achieve carbon neutrality are increasingly adopting electric vessels for short-distance commuter routes and tourism activities. Improvements in battery technology, energy storage capacity, and fast-charging infrastructure are further enabling the deployment of electric water buses. Additionally, electric vessels typically require lower maintenance and operational costs compared with diesel-powered vessels over their lifecycle. As environmental regulations become stricter and public demand for sustainable mobility increases, electric propulsion systems are expected to experience rapid adoption across urban waterfront transportation networks worldwide.

By Passenger Capacity Analysis

The medium capacity segment is projected to dominate the water bus market with an estimated 44.8% market share in 2026. Water buses with seating capacity between 50 and 150 passengers provide a balanced solution between operational efficiency and passenger demand. These vessels are widely used in urban commuter routes where consistent passenger volumes require reliable and moderately sized transport systems. Medium capacity water buses offer advantages such as lower operational costs, efficient fuel consumption, and flexibility in navigating narrow waterways and urban canals. Municipal transport authorities frequently deploy these vessels for scheduled daily commuter services because they are capable of handling peak passenger demand without requiring large docking infrastructure. Additionally, medium-sized vessels provide optimal maneuverability and operational flexibility, making them suitable for both public transport routes and tourism-based services. As urban mobility systems increasingly integrate water-based transport, medium-capacity water buses are expected to remain the preferred choice for operators seeking efficient passenger transportation across city waterways.

Large-capacity water buses represent the fastest-growing passenger capacity segment as urban populations and tourism activities continue to increase in waterfront cities. These vessels are capable of carrying over 150 passengers, making them suitable for high-demand routes and heavily populated metropolitan regions. The adoption of large-capacity water buses is particularly rising in cities with extensive river or coastal transportation systems where large commuter volumes require efficient transit solutions. These vessels are also commonly used in tourism hotspots where operators aim to transport large groups of travelers simultaneously. Improvements in vessel design, hull stability, and propulsion efficiency have enhanced the performance of large-capacity water buses. As cities seek to move large passenger volumes while reducing road congestion, the demand for high-capacity water transport vessels is expected to expand significantly.

By Application Analysis

Public transportation is the leading application segment in the water bus market and is expected to account for 47.9% of market share in 2026. Many governments are integrating water buses into urban transport systems to address road congestion and improve commuting options in cities located near rivers, lakes, and coastal areas. Water buses operating under public transport systems provide scheduled services similar to traditional bus networks, offering affordable and efficient transportation for daily commuters. These systems often integrate digital ticketing and multimodal connectivity with metro, rail, and road transport networks. Public transport water buses are particularly beneficial in cities where waterways provide natural transport corridors that can reduce travel time significantly. With growing urban populations and increasing focus on sustainable mobility, water buses are being considered an important component of urban public transportation infrastructure.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Tourism and sightseeing represent the fastest-growing application segment in the water bus market. Many waterfront cities attract millions of visitors each year who seek scenic travel experiences through rivers, canals, and harbors. Water buses are increasingly used for organized sightseeing tours, offering passengers a unique perspective of urban landscapes and cultural landmarks. Tourism operators are investing in modern vessels equipped with improved seating arrangements, large viewing decks, and onboard amenities to enhance the travel experience. Additionally, tourism-focused water buses often operate on flexible routes connecting major attractions, entertainment districts, and waterfront developments. The growth of global tourism, combined with rising interest in eco-friendly travel options, is expected to accelerate the adoption of water buses in tourism and recreational activities.

By Hull Type Analysis

Monohull vessels dominate the water bus market and are expected to hold 51.7% market share in 2026. Monohull water buses feature a single-hull design, which makes them suitable for a wide range of waterways including rivers, lakes, and coastal areas. These vessels are commonly used because they are relatively simple to design, cost-effective to manufacture, and easier to maintain compared with multi-hull alternatives. Monohull water buses also provide strong structural stability and are capable of carrying moderate to large passenger capacities depending on vessel size. Transport operators often prefer monohull vessels for traditional commuter routes due to their reliability and adaptability across different water conditions. In addition, the well-established shipbuilding expertise for monohull vessels ensures easier maintenance and spare parts availability. As a result, monohull vessels continue to represent the primary hull configuration for water bus fleets across most global regions.

Catamaran water buses are the fastest-growing hull type in the market due to their superior stability, speed, and passenger comfort. These vessels feature two parallel hulls connected by a platform, which improves balance and reduces wave resistance during operation. Catamarans are particularly beneficial for high-speed passenger transport and routes with rough water conditions. They also offer larger deck space and improved passenger seating arrangements, making them ideal for tourism and high-capacity commuter services. Many modern shipbuilders are designing electric and hybrid catamaran vessels that combine sustainability with improved performance. As demand grows for efficient and comfortable passenger water transport, catamaran water buses are expected to experience increasing adoption across major urban waterways.

By End User Analysis

Municipal and government authorities represent the dominant end-user segment and are expected to hold 55.3% of the water bus market share in 2026. Public authorities typically operate water bus services as part of integrated urban transportation networks. These authorities invest in fleet procurement, terminal infrastructure, and route development to improve public mobility. Government-operated water buses often provide affordable and scheduled commuter services, particularly in cities where waterways offer efficient travel routes. Additionally, governments frequently implement environmental policies encouraging the transition toward electric or hybrid marine vessels. Funding programs, infrastructure investments, and urban mobility initiatives have strengthened the role of municipal authorities in expanding water bus services. As governments continue to address urban congestion and environmental challenges, public sector participation will remain a major driver for water bus market expansion.

Tourism and hospitality companies represent the fastest-growing end-user segment in the water bus market. Hotels, resorts, and tour operators increasingly use water buses to provide transportation services for guests and visitors. These services often connect hotels, tourist attractions, entertainment districts, and waterfront destinations. Tourism-focused water buses emphasize passenger comfort, sightseeing opportunities, and premium travel experiences. Many operators are investing in modern vessels equipped with advanced amenities and eco-friendly propulsion systems to attract environmentally conscious travelers. As global tourism continues to expand and waterfront tourism developments increase, tourism and hospitality companies are expected to play a larger role in the adoption of water bus transportation services.

The Water Bus Market Report is segmented on the basis of the following:

By Propulsion Type

By Passenger Capacity

- Small Capacity (Up to 50 Passengers)

- Medium Capacity (50–150 Passengers)

- Large Capacity (Above 150 Passengers)

By Application

- Public Transportation

- Tourism & Sightseeing

- Private Charter & Shuttle Services

By Hull Type

- Monohull

- Catamaran

- Trimaran

By End User

- Municipal & Government Authorities

- Private Transport Operators

- Tobrief & Hospitality Companies

Regional Analysis

Leading Region in the Water Bus Market

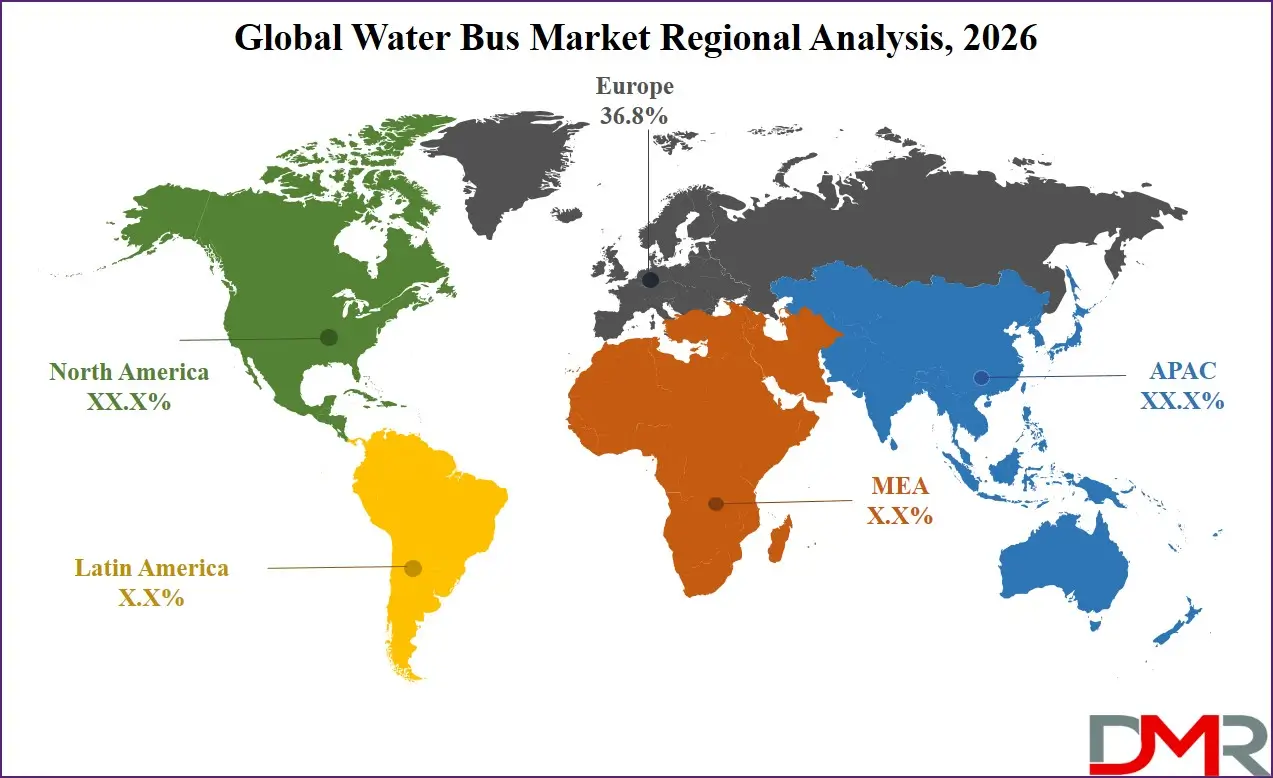

Europe is expected to dominate the global water bus market, accounting for 36.8% market share in 2026. The region's leadership is largely driven by its extensive network of navigable waterways, strong maritime infrastructure, and progressive environmental regulations promoting sustainable transportation. Many European cities are integrating water buses into their urban mobility systems to reduce traffic congestion and support environmentally friendly commuting alternatives. Governments across the region are investing heavily in electric and hybrid marine vessels to meet strict emission reduction targets. In addition, Europe's tourism sector strongly supports water bus services in canal cities and riverfront destinations where water transport is a major attraction for visitors. The presence of advanced shipbuilding industries and continuous technological innovation in marine engineering also contributes to the region's dominance. These factors collectively position Europe as the leading region in the global water bus market, supported by strong policy frameworks and sustainable transport initiatives.

Fastest Growing Region in the Water Bus Market

Asia Pacific is expected to emerge as the fastest-growing region in the water bus market due to rapid urbanization, expanding coastal cities, and growing investments in transportation infrastructure. Many cities in the region are located near rivers, lakes, and coastal zones, making water-based transport a practical mobility solution. Governments across several countries are exploring water bus systems to reduce traffic congestion and improve public transportation capacity in densely populated metropolitan areas. Increasing tourism activities and waterfront development projects are also contributing to market expansion. In addition, shipbuilding industries in the region are advancing in vessel design and manufacturing technologies, enabling cost-effective water bus production. With rising investments in sustainable transport and urban mobility solutions, Asia Pacific is expected to experience strong growth in water bus adoption.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The water bus market is characterized by a combination of established marine vessel manufacturers, shipbuilders, transport operators, and technology providers. Market competition is primarily driven by innovation in vessel design, propulsion technology, and operational efficiency. Companies are focusing on developing electric and hybrid water buses that comply with environmental regulations while reducing operational costs. Strategic partnerships between shipbuilders, technology developers, and municipal transport authorities are becoming increasingly common to accelerate fleet modernization projects.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Investments in research and development are enabling companies to introduce lightweight vessel structures, smart navigation technologies, and advanced energy management systems. Additionally, market entry barriers include high capital investment requirements, specialized shipbuilding capabilities, and strict maritime safety regulations. Operators are also emphasizing digital fleet management systems and passenger experience improvements to strengthen their competitive positioning within the evolving water bus transportation sector.

Some of the prominent players in the global Water Bus are:

- Damen Shipyards Group

- Austal Limited

- Incat Crowther

- Fincantieri S.p.A.

- Beneteau Group

- Azimut Benetti S.p.A.

- Ferretti S.p.A.

- Sunseeker International

- Bavaria Yachtbau

- Wight Shipyard Company

- BMT Group

- Artemis Technologies Ltd

- Candela Technology AB

- Baltic Workboats

- Hysucat

- Metal Shark Boats

- Willard Marine Inc.

- Munson Boats

- Nichols Brothers Boat Builders

- Gladding-Hearn Shipbuilding

- Other Key Players

Recent Developments

- In June 2025, ABB Marine & Ports entered into a strategic partnership with a major ferry transport operator to deploy hybrid propulsion systems for next-generation water bus vessels. The project focuses on integrating battery-electric technology with conventional propulsion to reduce fuel consumption and emissions during urban water transport operations. The hybrid systems also include intelligent power management solutions that optimize energy usage across different operating conditions.

- In February 2025, Damen Shipyards announced the launch of a new fully electric water bus fleet designed for urban passenger transportation in European waterways. The vessels were developed with advanced battery propulsion systems capable of operating with zero emissions, aligning with regional sustainability goals. Each vessel is equipped with fast-charging capabilities, enabling rapid turnaround times between routes.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 1.6 Bn |

| Forecast Value (2035) |

USD 2.5 Bn |

| CAGR (2026–2035) |

5.1% |

| The US Market Size (2026) |

USD 0.4 Bn |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors and etc. |

| Segments Covered |

By Propulsion Type (Diesel, Hybrid, Electric),

By Passenger Capacity (Small Capacity, Medium Capacity, Large Capacity),

By Application (Public Transportation, Tourism & Sightseeing, Private Charter & Shuttle Services),

By Hull Type (Monohull, Catamaran, Trimaran),

By End User (Municipal & Government Authorities, Private Transport Operators, Tourism & Hospitality Companies) |

| Regional Coverage |

North America – The US and Canada;

Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe;

Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC;

Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America;

Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

| Prominent Players |

Damen Shipyards Group, Austal Limited, Incat Crowther, Fincantieri S.p.A., Beneteau Group, Azimut Benetti S.p.A., Ferretti S.p.A., Sunseeker International, Bavaria Yachtbau, Wight Shipyard Company, BMT Group, Artemis Technologies Ltd, Candela Technology AB, Baltic Workboats, Hysucat, Metal Shark Boats, Willard Marine Inc., Munson Boats, Nichols Brothers Boat Builders, Gladding-Hearn Shipbuilding, and Other Key Players |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users) and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days and 5 analysts working days respectively. |

Frequently Asked Questions

How big is the Global Water Bus Market?

▾ The Global Water Bus Market size is expected to reach USD 1.6 billion by 2026 and is projected to reach USD 2.5 billion by the end of 2035.

Which region accounted for the largest Global Water Bus Market?

▾ Europe is expected to have the largest market share in the Global Water Bus Market, with a share of about 36.8% in 2026.

How big is the Water Bus Market in the US?

▾ The US Water Bus market is expected to reach USD 0.4 billion by 2026.

Who are the key players in the Water Bus Market?

▾ Some of the major key players in the Global Water Bus Market include Damen, Incat, Ferretti, and others.

What is the growth rate in the Global Water Bus Market?

▾ The market is growing at a CAGR of 5.1 percent over the forecasted period.