Market Overview

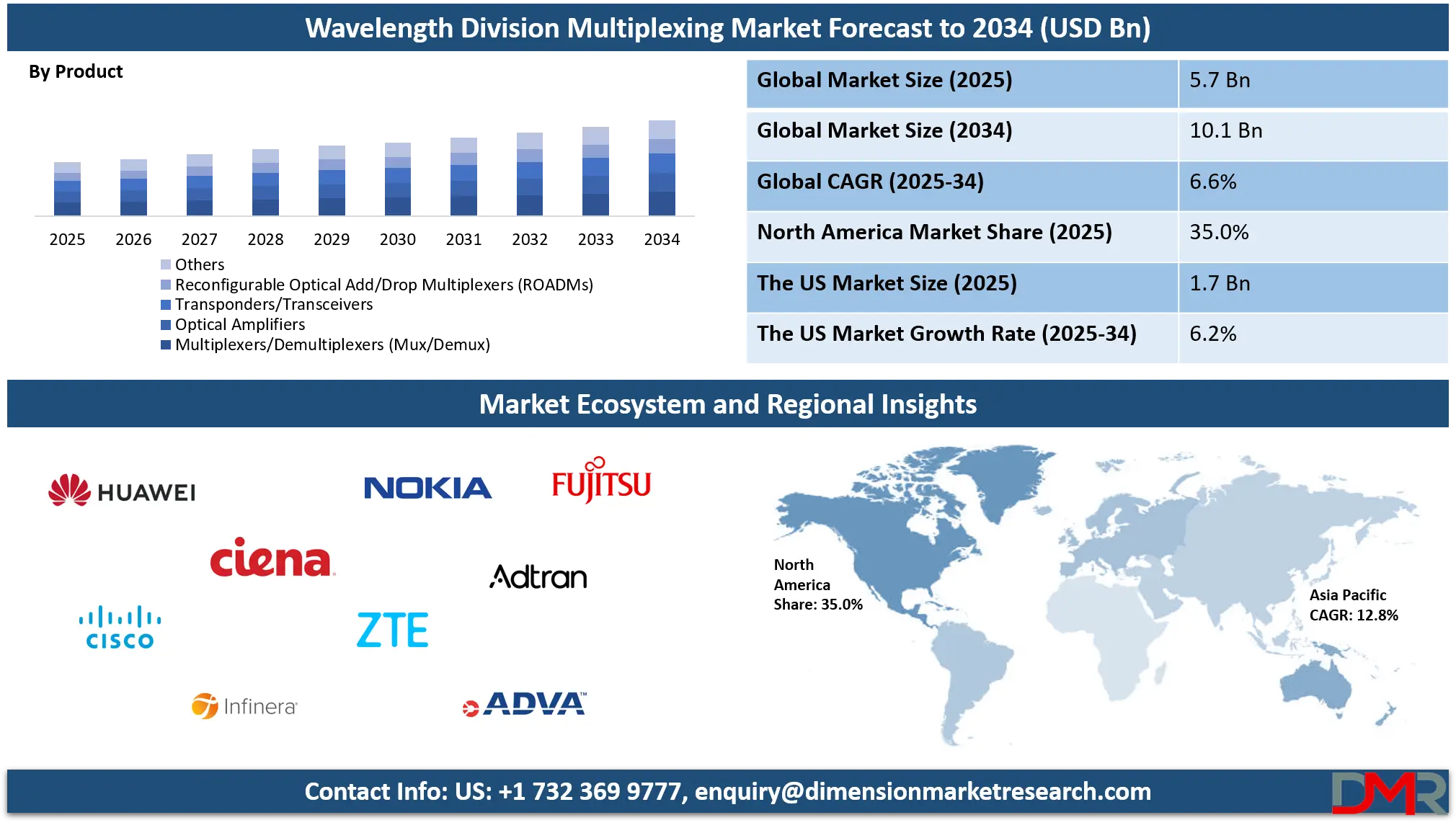

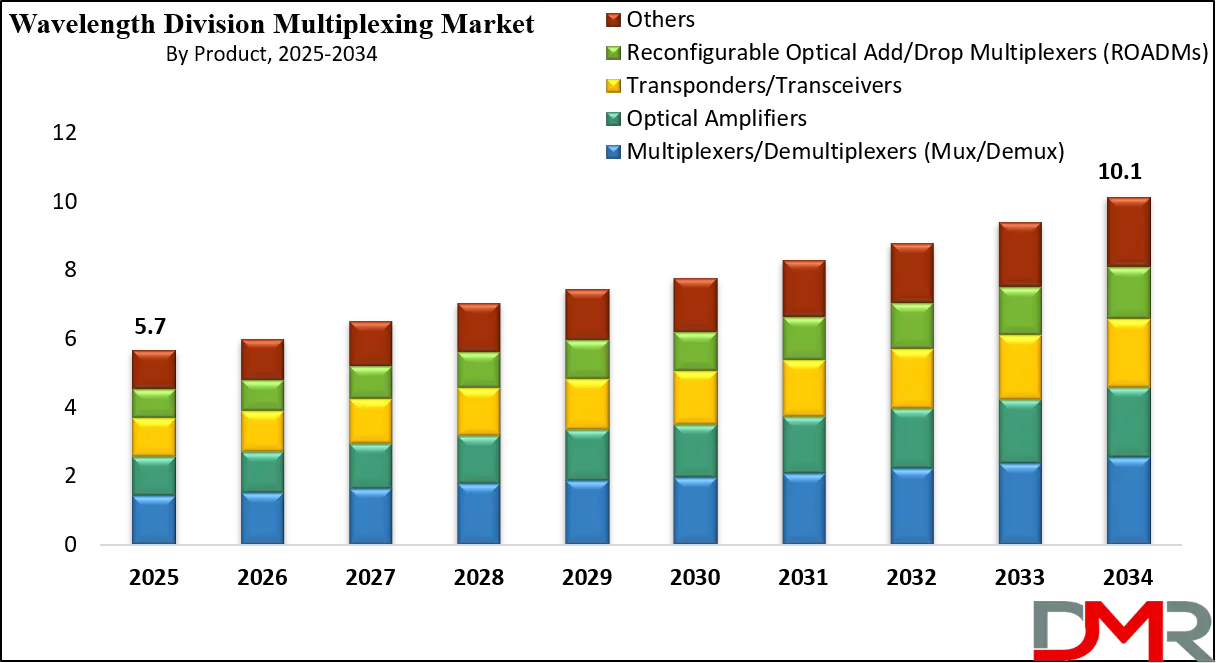

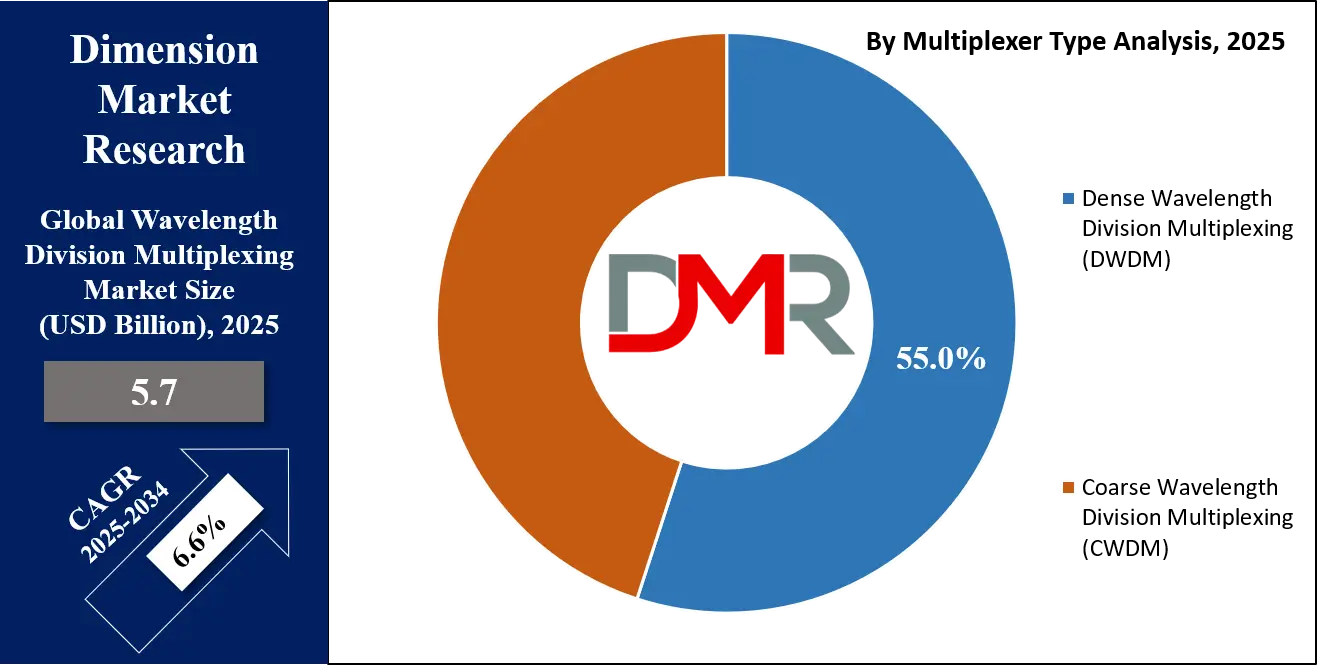

The global wavelength division multiplexing market is projected to reach USD 5.7 billion in 2025 and is expected to grow to USD 10.1 billion by 2034, registering a CAGR of 6.6% during the forecast period, driven by rising demand for high bandwidth, optical networking solutions, and expanding telecom and data center applications.

Wavelength Division Multiplexing (WDM) is an advanced optical networking technology that enables the transmission of multiple data streams simultaneously over a single optical fiber by assigning each stream to a distinct wavelength of light. This method maximizes the use of available fiber bandwidth, allowing telecom providers, data centers, and enterprise networks to scale their capacity without the need for additional physical infrastructure. By separating and combining light signals through multiplexers and demultiplexers, WDM provides a cost-effective solution for high-capacity data transfer, offering enhanced efficiency, improved spectral utilization, and reduced latency across long-haul, metro, and access networks.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The global Wavelength Division Multiplexing market is expanding as industries increasingly depend on high-speed connectivity and efficient bandwidth management to support applications such as 5G backhaul, cloud services, video streaming, and enterprise communication. Telecommunications providers remain the largest adopters of WDM systems as they address the exponential growth in internet traffic and mobile data usage. Meanwhile, hyperscale data centers and cloud service operators are accelerating deployment of DWDM and CWDM solutions to improve storage, retrieval, and workload distribution across geographically dispersed facilities.

In addition to telecom and data center growth, advancements in photonics, optical amplifiers, and reconfigurable optical add drop multiplexers are reshaping the WDM ecosystem. Governments and enterprises are also investing in optical infrastructure to meet digitalization goals, strengthen national broadband programs, and enhance critical communication networks. These trends, integrated with technological innovation and rising demand for seamless connectivity, continue to position WDM as a foundational element in the evolution of global optical networking solutions.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The US Wavelength Division Multiplexing Market

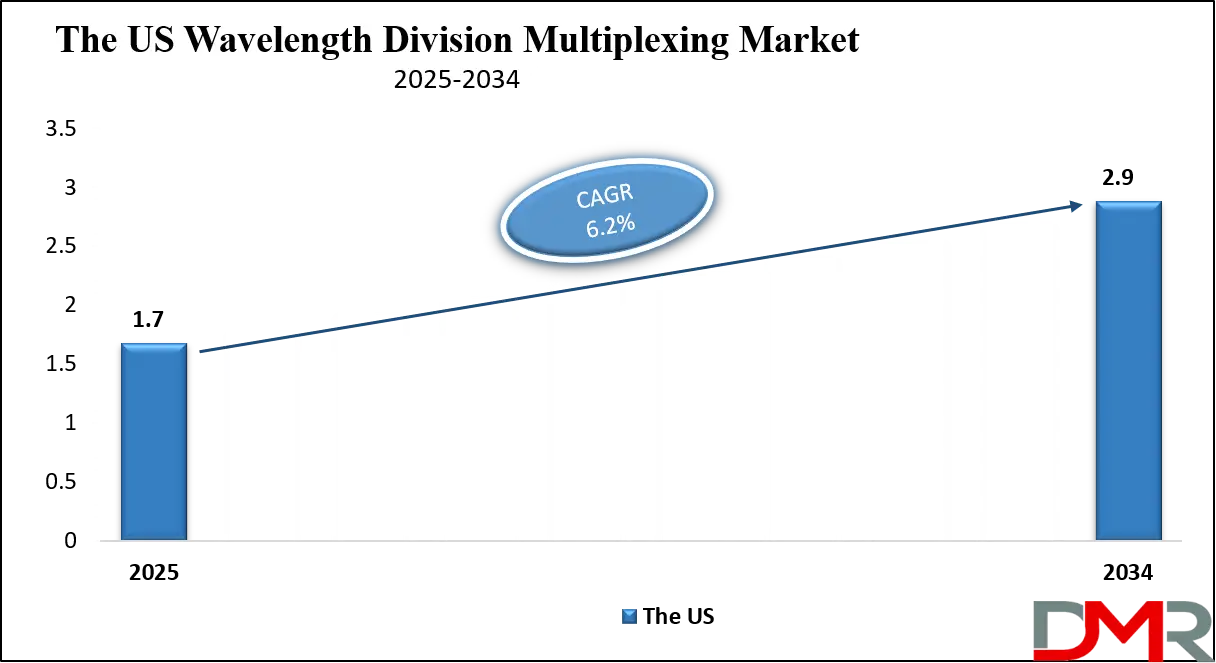

The U.S. Wavelength Division Multiplexing market size is projected to be valued at USD 1.7 billion by 2025. It is further expected to witness subsequent growth in the upcoming period, holding USD 2.9 billion in 2034 at a CAGR of 6.2%.

The US wavelength division multiplexing market is experiencing steady growth fueled by the growing demand for high-capacity optical networks across telecommunications, cloud computing, and enterprise connectivity. Telecom service providers in the country are rapidly upgrading their backbone infrastructure with dense wavelength division multiplexing (DWDM) and coarse wavelength division multiplexing (CWDM) technologies to manage surging mobile data traffic, 5G deployment, and fiber-to-the-home services.

The presence of hyperscale data centers and cloud operators in the US has also accelerated adoption of WDM solutions, as these facilities require high-speed interconnects, improved spectral efficiency, and low-latency optical communication systems. Government initiatives aimed at strengthening digital infrastructure and expanding rural broadband access are further creating opportunities for the deployment of optical transport networks supported by WDM technology.

In addition to telecom and data centers, enterprises across sectors such as finance, healthcare, and media are increasingly leveraging wavelength division multiplexing to support secure, high-volume data transfer and real-time applications. Continuous advancements in reconfigurable optical add drop multiplexers, optical amplifiers, and transponders are enhancing network flexibility and scalability, making WDM a critical enabler of digital transformation. With strong investment from technology providers, favorable regulatory support, and the growing need for next-generation broadband services, the US WDM market is positioned as one of the most advanced and competitive landscapes globally, driving innovation in optical networking solutions.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Europe Wavelength Division Multiplexing Market

The Europe wavelength division multiplexing market is projected to reach a valuation of USD 1.1 billion in 2025, accounting for a significant share of the global landscape. The region’s strong adoption of advanced optical networking technologies is driven by the rapid expansion of high-speed broadband infrastructure, 5G rollout initiatives, and the modernization of legacy telecom networks.

Countries such as Germany, the United Kingdom, and France are investing heavily in digital transformation programs, which include large-scale deployment of dense WDM and coarse WDM systems to support rising data consumption and bandwidth-intensive applications. Additionally, Europe’s focus on developing cross-border fiber connectivity to strengthen digital integration across the EU is fueling the adoption of scalable optical transport solutions.

The market is further supported by Europe’s growing emphasis on cloud computing, data center interconnectivity, and enterprise digitalization initiatives. As cloud service providers and hyperscale data centers expand across major hubs like Amsterdam, Frankfurt, and London, the demand for high-capacity and low-latency transmission solutions continues to accelerate. With a projected CAGR of 6.0% during the forecast period, the region is expected to maintain steady growth, supported by government-backed digital infrastructure programs and growing investments in research and development of next-generation photonics and optical networking solutions. Europe’s commitment to sustainability and energy-efficient network solutions also positions it as a key innovator in the wavelength division multiplexing market.

Japan Wavelength Division Multiplexing Market

The Japan wavelength division multiplexing market is projected to reach approximately USD 250 million in 2025, reflecting steady growth in line with the country’s advanced telecommunications infrastructure. Japan’s strong focus on next-generation network technologies, including 5G deployment and high-speed optical fiber expansion, is driving the demand for dense and coarse WDM solutions.

Telecom operators are increasingly adopting DWDM systems to handle growing mobile data traffic, support cloud-based services, and ensure reliable broadband connectivity across urban and regional areas. The country’s emphasis on digital transformation in both private and public sectors further fuels the deployment of WDM technology in metro and long-haul networks.

The market is expected to grow at a CAGR of 6.5%, supported by the proliferation of hyperscale data centers and enterprise network upgrades that require high-capacity, low-latency optical interconnects. Advancements in optical amplifiers, transponders, and reconfigurable optical add drop multiplexers are enhancing network scalability and efficiency, enabling telecom operators and cloud providers to meet rising data demands.

Additionally, government initiatives aimed at smart city projects, IoT integration, and rural broadband expansion are providing further opportunities for WDM adoption. With continuous innovation in photonics and optical networking, Japan is positioned as a strategic growth region within the global wavelength division multiplexing market.

Global Wavelength Division Multiplexing Market: Key Takeaways

- Market Value: The global Wavelength Division Multiplexing market size is expected to reach a value of USD 10.1 billion by 2034 from a base value of USD 5.7 billion in 2025 at a CAGR of 6.6%.

- By Component Analysis: Multiplexers/Demultiplexers (Mux/Demux) are anticipated to dominate the component segment, capturing 25.0% of the total market share in 2025.

- By Multiplexer Type Segment Analysis: Dense Wavelength Division Multiplexing (DWDM) is expected to maintain its dominance in the multiplexer type segment, capturing 55.0% of the total market share in 2025.

- By Application Segment Analysis: Telecommunication applications capture the maximum share in the application segment, capturing 40.0% of the market share in 2025.

- By End-Use Industry Segment Analysis: Telecommunications Service Providers will dominate the end-use industry segment, capturing 60.0% of the market share in 2025.

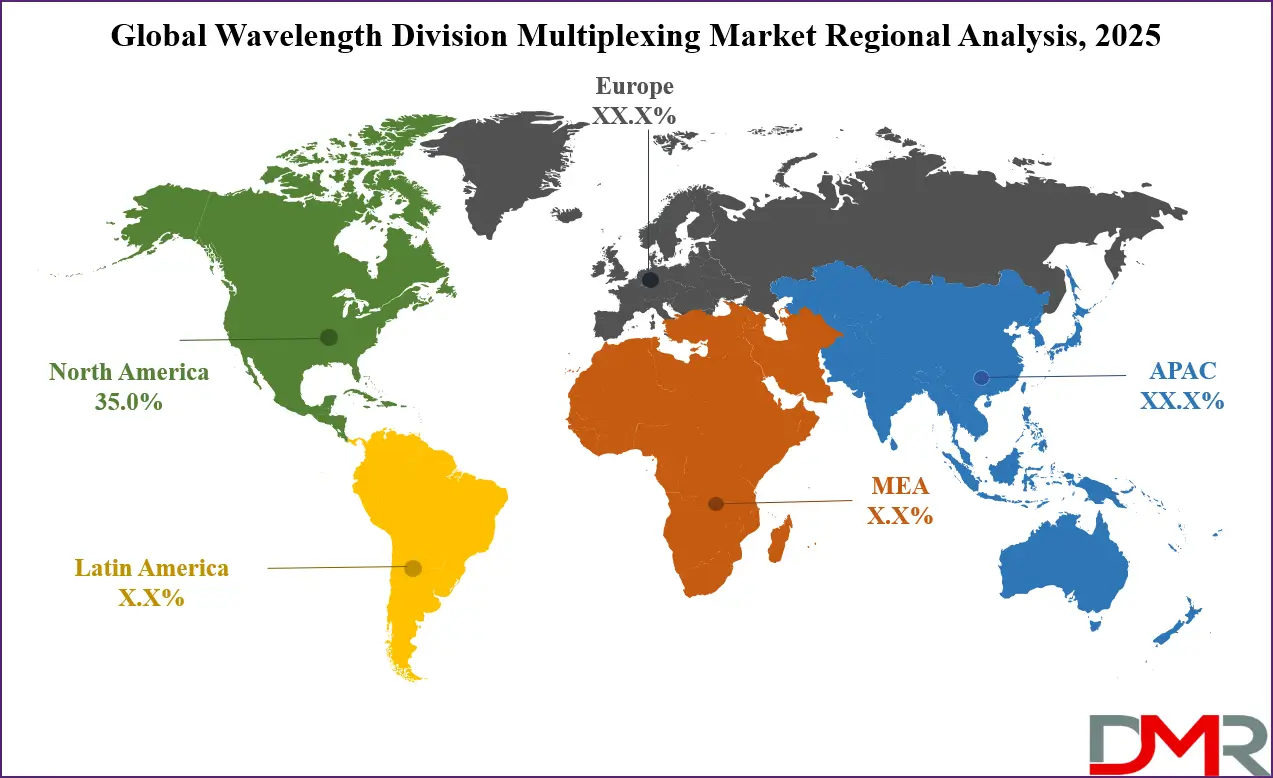

- Regional Analysis: North America is anticipated to lead the global Wavelength Division Multiplexing market landscape with 35.0% of total global market revenue in 2025.

- Key Players: Some key players in the global Wavelength Division Multiplexing market include Huawei, Ciena Corporation, Cisco Systems Inc., Infinera Corporation, Nokia Corporation, ZTE Corporation, and Others.

Global Wavelength Division Multiplexing Market: Use Cases

- High-Capacity Telecom Networks: Telecommunication service providers leverage wavelength division multiplexing to increase the capacity of existing optical fiber infrastructure without laying new cables. Dense WDM systems allow simultaneous transmission of multiple wavelengths across long-haul and metro networks, supporting 5G backhaul, fiber-to-the-home services, and seamless voice and data connectivity. This use case helps operators meet the exponential growth in internet traffic and ensures efficient spectral utilization for nationwide broadband expansion.

- Hyperscale Data Center Interconnects: Cloud service providers and hyperscale data centers rely on WDM technology for high-speed interconnection between facilities. With growing demand for video streaming, cloud storage, and artificial intelligence workloads, WDM solutions provide low-latency optical communication, secure bandwidth allocation, and scalable performance. By deploying reconfigurable optical add drop multiplexers and optical amplifiers, data centers ensure optimal workload distribution and business continuity across multiple geographic locations.

- Enterprise and Financial Services Networks: Large enterprises, including financial institutions and healthcare providers, use wavelength division multiplexing to manage mission-critical applications that require high reliability and security. WDM enables dedicated optical channels for data transfer, disaster recovery, and real-time analytics. In sectors like banking and trading, DWDM ensures uninterrupted connectivity with minimal latency, supporting high-frequency transactions and safeguarding sensitive information through private optical networking infrastructure.

- Government and Defense Communication Systems: Government agencies and defense organizations adopt WDM solutions to build secure, resilient, and high-capacity communication networks. The technology supports real-time intelligence sharing, remote operations, and command-and-control systems that demand reliable optical connectivity. With advancements in CWDM and DWDM, military and public safety networks can integrate high bandwidth applications, satellite links, and surveillance systems, ensuring robust communication infrastructure even under critical conditions.

Impact of Artificial Intelligence on the global Wavelength Division Multiplexing market

Artificial intelligence is reshaping the global wavelength division multiplexing market by enabling smarter, more adaptive, and automated optical networks. AI-driven analytics are being integrated into WDM systems to optimize traffic management, predict network congestion, and dynamically allocate wavelengths, thereby improving spectral efficiency and reducing operational costs.

Machine learning algorithms enhance fault detection, predictive maintenance, and energy efficiency in optical amplifiers, transponders, and reconfigurable optical add drop multiplexers, ensuring higher reliability and lower downtime. As telecom operators, data centers, and enterprises increasingly adopt AI-powered WDM solutions, the market is witnessing faster scalability, improved quality of service, and greater support for next-generation applications such as 5G, edge computing, and cloud-based services.

Global Wavelength Division Multiplexing Market: Stats & Facts

Economic Survey 2024-25

- India's colocation data center capacity reached 977 MW in 2023.

- An additional 258 MW was added in 2023.

- The total capacity under construction for 2024-2028 is 1.03 GW, with an additional 1.29 GW planned.

Comprehensive Modular Survey: Telecom, 2025

- Percentage of households with internet facility within household premises: 80% urban, 60% rural.

- Percentage of households with optical fiber connectivity: 15% urban, 5% rural.

- Percentage of households possessing landline or mobile phone: 95% urban, 85% rural.

- Percentage of persons able to use internet: 90% urban, 70% rural.

- Percentage of persons performing online banking transactions: 65% urban, 45% rural.

Global Wavelength Division Multiplexing Market: Market Dynamics

Global Wavelength Division Multiplexing Market: Driving Factors

Rising Bandwidth Demand across Telecom and Data Centers

The exponential surge in internet usage, 5G rollouts, cloud services, and video streaming is pushing telecom providers and hyperscale data centers to adopt dense wavelength division multiplexing solutions. By enhancing fiber capacity and supporting high-speed optical transmission, WDM helps meet the growing need for seamless connectivity, low-latency communication, and large-scale data transfer.

Expansion of Fiber Optic Infrastructure

Governments and private operators are heavily investing in fiber optic deployments to improve broadband penetration, rural connectivity, and enterprise networking. WDM technology maximizes the utilization of these networks by allowing multiple data channels over a single fiber, making it an essential enabler for cost-efficient and scalable optical transport systems.

Global Wavelength Division Multiplexing Market: Restraints

High Initial Deployment Costs

The adoption of wavelength division multiplexing systems involves significant capital expenditure on components such as multiplexers, demultiplexers, transponders, and optical amplifiers. Smaller enterprises and regional operators often face financial constraints in deploying DWDM and CWDM infrastructure, slowing down adoption in certain markets.

Complex Network Management and Maintenance

Operating WDM-based networks requires advanced expertise to manage wavelength allocation, optical amplifiers, and reconfigurable add drop multiplexers. The complexity of integrating these systems with legacy infrastructure increases operational challenges and may limit faster deployment for organizations lacking technical resources.

Global Wavelength Division Multiplexing Market: Opportunities

Growing Role of Cloud and Edge Computing

The rapid adoption of cloud platforms, artificial intelligence, and edge computing is driving the need for robust optical connectivity with high bandwidth and minimal latency. WDM solutions present a lucrative opportunity by enabling faster interconnection between data centers and supporting distributed workloads across global enterprise networks.

Government Investments in Digital Infrastructure

National broadband programs and smart city initiatives are creating favorable opportunities for large-scale WDM deployments. By supporting secure and high-capacity communication channels, wavelength division multiplexing becomes integral to public sector projects, defense communication, and rural internet expansion, further boosting market penetration.

Global Wavelength Division Multiplexing Market: Trends

Integration of Artificial Intelligence in Optical Networks

AI and machine learning are transforming WDM systems by enabling predictive maintenance, real-time traffic optimization, and automated wavelength allocation. This trend enhances efficiency, reduces downtime, and allows network operators to provide scalable and adaptive optical networking solutions.

Shift Toward Reconfigurable Optical Add Drop Multiplexers (ROADMs)

The growing demand for network flexibility and dynamic bandwidth allocation has accelerated the adoption of ROADMs in DWDM networks. These solutions allow operators to remotely add, drop, or reroute wavelengths, making WDM infrastructure more agile and cost-effective for telecom providers and cloud service operators.

Global Wavelength Division Multiplexing Market: Research Scope and Analysis

By Component Analysis

Multiplexers and demultiplexers are anticipated to dominate the component segment of the wavelength division multiplexing market, capturing 25.0% of the total share in 2025. These devices are indispensable in optical networking as they enable multiple wavelengths to be combined and transmitted through a single optical fiber, significantly enhancing spectral efficiency. By efficiently separating and routing signals at the receiving end, Mux/Demux units allow telecom providers and data centers to scale their capacity without laying additional fiber infrastructure, thereby lowering capital expenditure while boosting network performance.

Their strong market presence is also driven by the surge in 5G deployments, cloud service adoption, and the need for reliable metro and long-haul network connections. In addition, advancements in photonic integration and compact form factors are making multiplexers and demultiplexers more cost-effective, energy-efficient, and easier to deploy, which further strengthens their role as a cornerstone of modern optical communication systems.

Optical amplifiers account for around 20.0% of the wavelength division multiplexing market share and remain a crucial component for enabling long-distance, high-capacity communication. Unlike traditional electronic regeneration methods, optical amplifiers boost light signals directly without requiring optical-to-electrical conversion, reducing both latency and power consumption. Their importance is growing as global data traffic expands, with hyperscale data centers, submarine cable systems, and cross-border telecom networks increasingly relying on optical amplification to maintain signal integrity over thousands of kilometers.

Amplifiers such as erbium-doped fiber amplifiers (EDFAs) and Raman amplifiers are particularly valuable in dense wavelength division multiplexing systems, ensuring consistent signal strength across multiple channels. With the ongoing expansion of international bandwidth demand, rising investments in fiber optic infrastructure, and the push for faster broadband services, optical amplifiers are expected to remain a critical driver of network scalability, reliability, and cost efficiency in the WDM market.

By Multiplexer Type Analysis

Dense wavelength division multiplexing is projected to remain the dominant technology within the multiplexer type segment, accounting for 55.0% of the total market share in 2025. DWDM systems are preferred for their ability to support a very high number of closely spaced wavelengths, allowing service providers to maximize fiber utilization and achieve superior data transmission rates across long-haul and metro networks. This capability makes DWDM especially suitable for telecommunications backbones, international cable systems, and hyperscale data centers that require robust bandwidth to handle soaring demand from 5G services, cloud computing, and video streaming.

The technology also provides higher scalability and flexibility, enabling operators to expand capacity without significant physical upgrades. Continuous advancements in transponders, optical amplifiers, and reconfigurable add drop multiplexers further strengthen the adoption of DWDM, making it the backbone of global high-capacity communication infrastructure.

Coarse wavelength division multiplexing, on the other hand, contributes significantly to the market by offering a cost-effective solution for metro and access networks. CWDM uses fewer and more widely spaced channels compared to DWDM, which reduces equipment cost and power consumption, making it attractive for short to medium-distance applications.

Enterprises, cable television providers, and regional telecom operators often deploy CWDM solutions to expand network capacity for services like enterprise connectivity, broadband access, and disaster recovery links. While CWDM does not offer the same scalability as DWDM, its affordability, simplified design, and suitability for less demanding network environments ensure its continued relevance in the overall WDM ecosystem, particularly for organizations looking for economical bandwidth expansion options.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Application Analysis

Telecommunication applications are set to capture the largest portion of the wavelength division multiplexing market, accounting for 40.0% of the total share in 2025. The dominance of this segment is driven by the rising demand for high-speed internet, the global expansion of 5G networks, and the growing reliance on fiber optic backhaul to support growing mobile and broadband traffic. WDM technology allows telecom operators to maximize the capacity of existing fiber infrastructure by transmitting multiple signals simultaneously, ensuring efficient use of bandwidth and reducing the need for additional cable installations.

Dense WDM, in particular, has become the backbone of telecom networks, enabling long-haul and metro transmission with minimal latency and high reliability. Investments in national broadband programs, cross-border connectivity, and next-generation network upgrades further strengthen the role of telecommunication applications as the leading contributor to WDM adoption globally.

Data centers also play a vital role in driving demand for wavelength division multiplexing, as they increasingly depend on high-capacity optical interconnects to manage cloud computing, artificial intelligence, and big data workloads. The rapid growth of hyperscale facilities and multi-cloud ecosystems requires scalable, low-latency communication between geographically dispersed data centers, where WDM ensures secure and efficient transfer of massive data volumes. By supporting seamless workload distribution and disaster recovery, WDM enhances operational resilience and business continuity for cloud service providers and enterprises.

Furthermore, the integration of reconfigurable add drop multiplexers and optical amplifiers in data center networks allows for greater flexibility, energy efficiency, and bandwidth optimization, making WDM a cornerstone technology for digital infrastructure expansion.

By End-Use Industry Analysis

Telecommunications service providers are expected to dominate the end-use industry segment of the wavelength division multiplexing market, capturing 60.0% of the share in 2025. This leadership stems from their pivotal role in delivering high-speed connectivity, supporting mobile networks, and expanding fiber optic infrastructure to meet surging demand for internet services.

With the rollout of 5G and the growing adoption of fiber-to-the-home solutions, service providers are heavily investing in dense wavelength division multiplexing to enhance long-haul, metro, and access networks. WDM allows these operators to scale bandwidth, reduce latency, and improve spectral efficiency, ensuring seamless delivery of voice, video, and data services. National broadband initiatives, cross-border submarine cable systems, and the need for reliable backhaul connections further reinforce the reliance of telecom providers on WDM technology, solidifying their position as the largest market contributors.

Cloud service providers represent another critical segment in the WDM market as they depend on high-capacity optical networking to support the rapid growth of cloud computing, artificial intelligence, and edge applications. These providers utilize wavelength division multiplexing to interconnect hyperscale data centers, ensuring low-latency communication, secure bandwidth allocation, and efficient handling of large-scale workloads.

As enterprises continue to migrate operations to multi-cloud environments, the demand for flexible and scalable WDM solutions has accelerated. Reconfigurable optical add drop multiplexers and optical amplifiers are increasingly integrated into cloud infrastructure to optimize performance, enable seamless workload distribution, and strengthen disaster recovery capabilities. With digital transformation expanding globally, cloud service providers are becoming a key growth driver for WDM adoption, complementing the dominance of traditional telecom operators.

The Wavelength Division Multiplexing Market Report is segmented on the basis of the following:

By Component

- Multiplexers/Demultiplexers (Mux/Demux)

- Optical Amplifiers

- Transponders/Transceivers

- Reconfigurable Optical Add/Drop Multiplexers (ROADMs)

- Others (Optical Switches, Filters, etc.)

By Multiplexer Type

- Dense Wavelength Division Multiplexing (DWDM)

- Coarse Wavelength Division Multiplexing (CWDM)

By Application

- Telecommunications

- Data Centers

- Broadcasting & Cable TV

- Others

By End-User Industry

- Telecommunications Service Providers

- Cloud Service Providers

- Enterprises

Global Wavelength Division Multiplexing Market: Regional Analysis

Region with the Largest Revenue Share

North America is projected to lead the global wavelength division multiplexing market, accounting for 35.0% of total revenue in 2025, supported by advanced digital infrastructure, high adoption of 5G, and the presence of hyperscale data centers. The region benefits from strong investments by telecom operators and cloud service providers in dense wavelength division multiplexing systems to manage growing mobile data traffic, cloud computing, and video streaming demands.

Government-backed broadband initiatives and the expansion of fiber optic networks across the United States and Canada further strengthen market growth, while continuous innovation from leading players headquartered in the region positions North America as a hub for optical networking advancements.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Region with significant growth

Asia Pacific is expected to witness the most significant growth in the wavelength division multiplexing market over the forecast period, driven by rapid digitalization, expanding telecom infrastructure, and the rising penetration of high-speed internet across countries such as China, India, Japan, and South Korea. Massive investments in 5G rollout, fiber-to-the-home services, and hyperscale data centers are fueling demand for dense and coarse WDM solutions in the region. Additionally, government initiatives promoting broadband expansion and smart city projects, along with the booming e-commerce and cloud services sector, are accelerating adoption. The growing need for scalable, low-latency networks positions Asia Pacific as a key growth engine in the global WDM market.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Global Wavelength Division Multiplexing Market: Competitive Landscape

The global wavelength division multiplexing market features a highly competitive landscape, characterized by the presence of leading technology providers, telecom equipment manufacturers, and optical component suppliers striving to strengthen their market position through innovation and strategic partnerships. Key players such as Huawei Technologies, Ciena, Cisco Systems, Infinera, Nokia, ZTE, and Fujitsu dominate with extensive product portfolios in dense and coarse WDM systems, while companies like ADVA Optical Networking, Lumentum, Corning, and CommScope contribute with specialized optical components and solutions.

Intense competition is driving continuous advancements in reconfigurable add drop multiplexers, optical amplifiers, and transponders to meet rising demand for scalable, high-capacity networks. Mergers, acquisitions, and collaborations are also shaping the market as vendors aim to expand global reach, enhance R&D capabilities, and cater to the growing requirements of telecom operators, cloud service providers, and enterprises globally.

Some of the prominent players in the global Wavelength Division Multiplexing market are:

- Huawei Technologies Co., Ltd.

- Ciena Corporation

- Cisco Systems, Inc.

- Infinera Corporation

- Nokia Corporation

- ZTE Corporation

- Fujitsu Ltd.

- ADTRAN, Inc.

- ADVA Optical Networking SE

- Aliathon Technology Ltd.

- Alcatel-Lucent

- Juniper Networks

- IBM Corporation

- Coriant

- Ericsson AB

- Timbercon, Inc.

- CommScope Holding Company, Inc.

- Optiwave Systems Inc.

- Lumentum Operations LLC

- Corning Incorporated

- Other Key Players

Global Wavelength Division Multiplexing Market: Recent Developments

- March 2025: BizLink rolled out a high-density WDM cassette with 216 LC ports in a 1RU format, designed for space-efficient deployments in data centers and telecom networks.

- March 2025: Pilot Photonics introduced its first 16-channel O-band laser arrays aligned to WDM standards, aimed at boosting scalable optical connectivity in AI and cloud data center systems.

- March 2024: Pilot Photonics received €2.5 million in funding from the European Innovation Council to advance coherent co-packaged optics and wavelength multiplexing technologies.

Report Details

| Report Characteristics |

| Market Size (2025) |

USD 5.7 Bn |

| Forecast Value (2034) |

USD 10.1 Bn |

| CAGR (2025–2034) |

6.6% |

| The US Market Size (2025) |

USD 1.7 Bn |

| Historical Data |

2019 – 2024 |

| Forecast Data |

2026 – 2034 |

| Base Year |

2024 |

| Estimate Year |

2025 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors, etc. |

| Segments Covered |

By Component (Multiplexers/Demultiplexers, Optical Amplifiers, Transponders/Transceivers, Reconfigurable Optical Add/Drop Multiplexers, Others), By Multiplexer Type (Dense Wavelength Division Multiplexing, Coarse Wavelength Division Multiplexing), By Application (Telecommunications, Data Centers, Broadcasting & Cable TV, Others), and By End-User Industry (Telecommunications Service Providers, Cloud Service Providers, Enterprises) |

| Regional Coverage |

North America – US, Canada; Europe – Germany, UK, France, Russia, Spain, Italy, Benelux, Nordic, Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, Rest of MEA |

| Prominent Players |

Huawei, Ciena Corporation, Cisco Systems Inc., Infinera Corporation, Nokia Corporation, ZTE Corporation, and Others. |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users), and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days, and 5 analysts working days respectively. |

Frequently Asked Questions

How big is the global Wavelength Division Multiplexing market?

▾ The global Wavelength Division Multiplexing market size is estimated to have a value of USD 5.7 billion in 2025 and is expected to reach USD 10.1 billion by the end of 2034.

What is the size of the US Wavelength Division Multiplexing market?

▾ The US Wavelength Division Multiplexing market is projected to be valued at USD 1.7 billion in 2025. It is expected to witness subsequent growth in the upcoming period as it holds USD 2.9 billion in 2034 at a CAGR of 6.2%.

Which region accounted for the largest global Wavelength Division Multiplexing market?

▾ North America is expected to have the largest market share in the global Wavelength Division Multiplexing market, with a share of about 35.0% in 2025.

Who are the key players in the global Wavelength Division Multiplexing market?

▾ Some of the major key players in the global Wavelength Division Multiplexing market are Huawei, Ciena Corporation, Cisco Systems Inc., Infinera Corporation, Nokia Corporation, ZTE Corporation, and Others.

What is the growth rate of the global Wavelength Division Multiplexing market?

▾ The market is growing at a CAGR of 6.6 percent over the forecasted period.