What is the Whole Genome Sequencing Clinical Market Size?

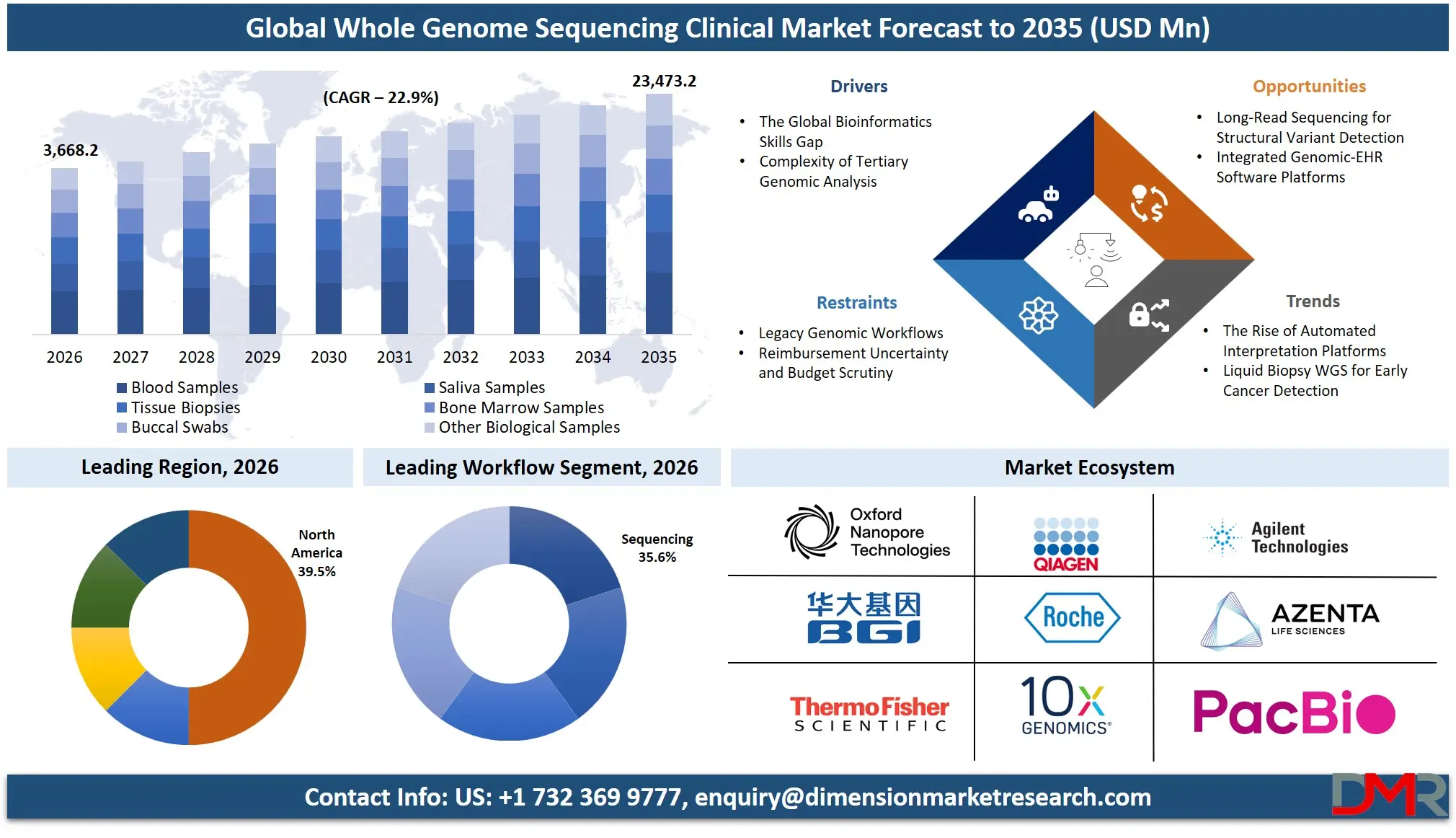

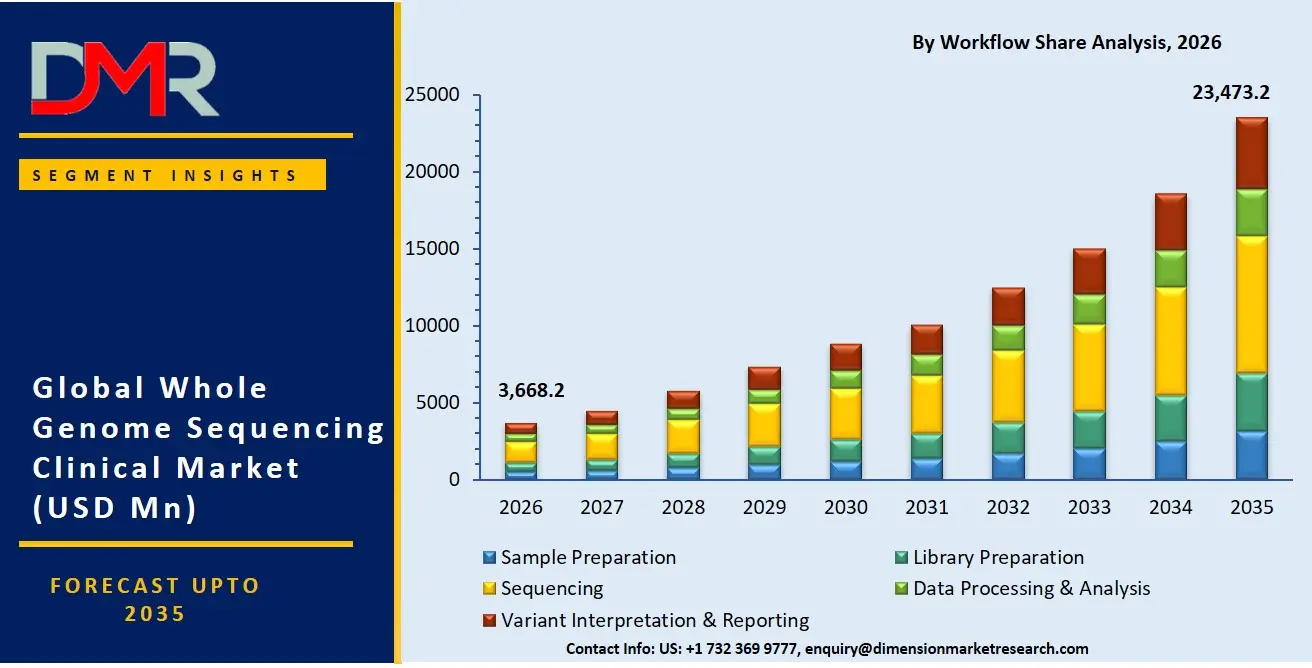

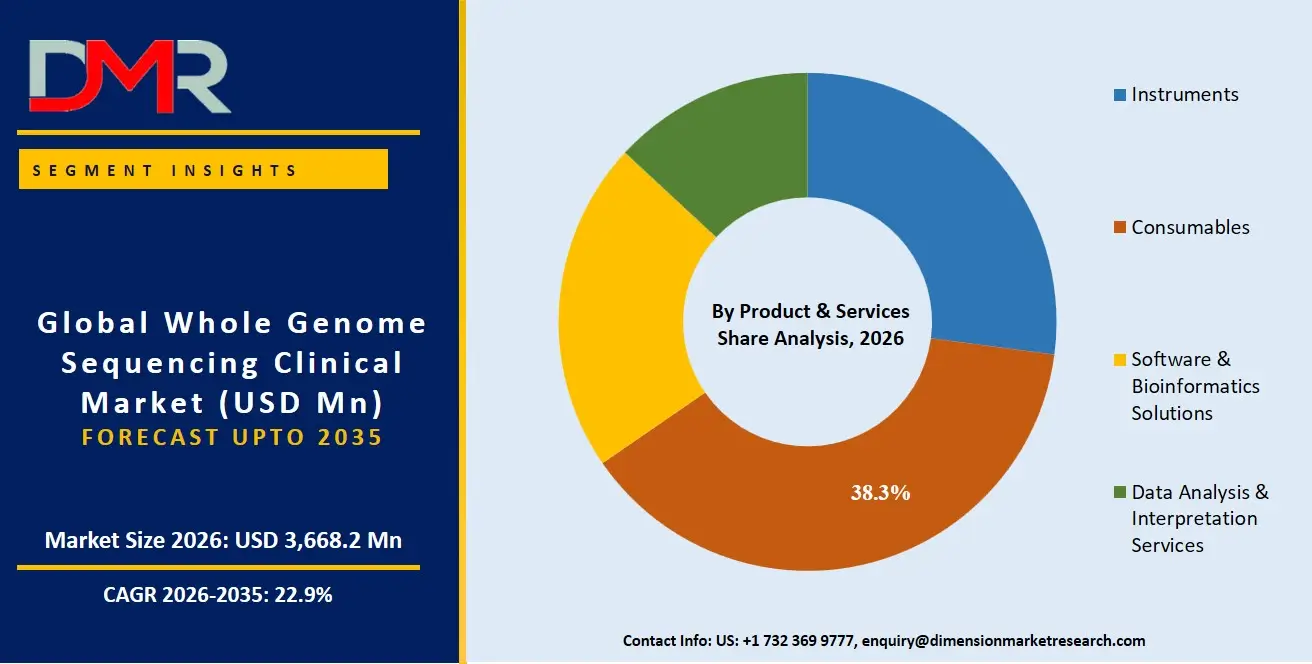

The Global Whole Genome Sequencing Clinical Market is expected to reach a value of USD 3,668.2 million in 2026, and it is further anticipated to reach USD 23,473.2 million by 2035, growing at a CAGR of 22.9% during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The whole genome sequencing clinical market has seen remarkable growth owing to the increase in speed by healthcare providers towards precision medicine through the move from legacy genomics technologies such as arrays and targeted panels into full genome sequencing. Clinical sequencing market is made up of four categories; instruments, reagents, software, and services. They help clinical labs and hospitals to sequence and analyze the complete human genomes. The increasing demand for adoption of sequencing for the purpose of oncology, rare diseases, and pharmacogenomics requires specific services on bioinformatics and interpretation. Hospitals and diagnostic laboratories are the most common adopters with the technology of SBS being the most popular due to its precision and capacity. Oncology, rare disease diagnostics, and reproductive health remain the most critical applications for the technology since they require accurate clinical sequencing data.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

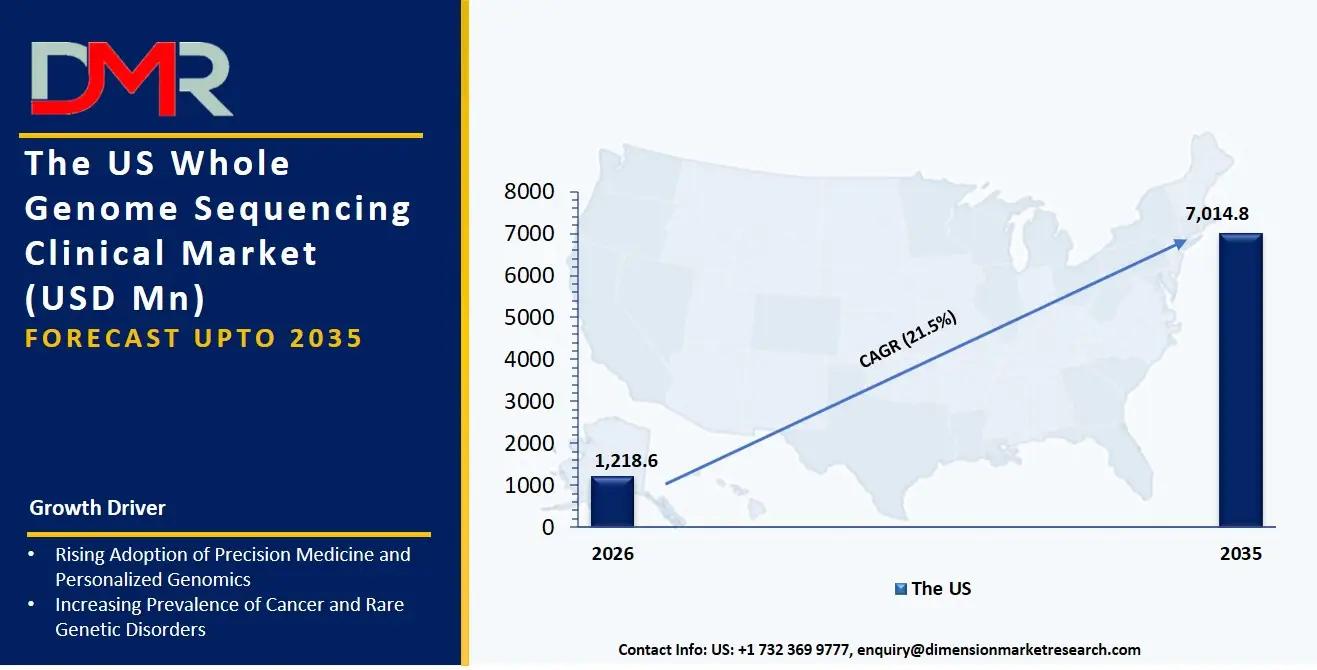

The US Whole Genome Sequencing Clinical Market

The US Whole Genome Sequencing Clinical Market is projected to reach USD 1,218.6 million in 2026 at a compound annual growth rate of 21.5% over its forecast period, culminating in a value of USD 7,014.8 million by 2035. This is attributed to the fact that the country still has leading clinical WGS markets on account of the vigorous precision medicine efforts carried out by leading hospital networks, as well as the distribution of CLIA-certified WGS laboratories. In this case, the market is characterized by very high demand for Data Analysis & Interpretation Services where the clinical facilities try to convert the generated data into meaningful information. Furthermore, the use of artificial intelligence for the interpretation of genomic data is creating an analogous need for software & bioinformatics solutions.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The Europe Whole Genome Sequencing Clinical Market

The Europe Whole Genome Sequencing Clinical Market is estimated to be valued at USD 1,136.7 million in 2026 (calculated based on 31% share of global) and is further anticipated to reach USD 7,281.5 million by 2035 at a CAGR of 22.9%. GDPR and EU AI Act regulations, among others, have a huge impact on the European market, thus increasing the demand for utilizing secure data analytics and genomic cloud solutions. Another factor responsible for rapid growth in Library Preparation Kits is accelerated growth in the region due to efforts from German and French laboratories that seek to find a compromise between sequencing accuracy and turnaround time in diagnosing rare diseases. Moreover, projects like the European '1+ Million Genomes' initiative pose the problem for service providers of developing consistent workflows in variant interpretation & reporting.

The Japan Whole Genome Sequencing Clinical Market

The Japan Whole Genome Sequencing Clinical Market is projected to be valued at USD 440.2 million in 2026 (approx. 12% of global). It is further expected to witness robust growth, holding USD 2,816.8 million in 2035 at a CAGR of 22.9%. Japan's healthcare market is distinctive, where both corporations and governments are keen on incorporating genomics medicine as part of their regular care due to demographic changes and the presence of more advanced cases of cancer. In terms of expenditures, the areas of Data Processing & Analysis and Sample Preparation account for a considerable portion since the large-scale hospital networks are moving away from the old-generation genetic analyzers to whole-genome sequencing processes. It should be noted that there is a demand for integrating the market locally through bridging the gap between their current EMRs and genomic reporting systems.

Key Takeaways

- Market Size & Forecast: The Global Whole Genome Sequencing Clinical market is projected to reach USD 3,668.2 million in 2026, expanding dramatically to USD 23,473.2 million by 2035, due to the impact of the two factors, i.e., clinical AI usage and a mandatory transition from targeted panels to full-genomic tests.

- Growth Rate & Outlook: Global market growth is expected at a CAGR of 22.9%, due to the lack of in-house bioinformaticians and the growing complexity of the tertiary data analysis and clinical variant interpretations.

- Primary Growth Drivers: The most important growth drivers are a global shift from targeted genotyping to WGS, data analysis & interpretation services that prevent diagnostic odysseys and are needed for incorporation of the genomic data into electronic health records through the software & bioinformatics solutions.

- Key Market Trends: The key trends include the emergence of long-read sequencing technologies (Nanopore, SMRT), AI-powered instruments within Variant Interpretation & Reporting (auto-classification of the variants), population-wide approach to genomics in order to promote preventive medicine at the national healthcare level.

- By Product & Service Analysis: Consumables (including Reagents & Kits and Library Preparation Kits) is projected to hold dominance as they are repeatedly consumed per sample. On the other hand, Data Analysis & Interpretation Services will experience significant growth as clinical laboratories prefer outsourcing their bioinformatics needs.

- By Application Analysis: Oncology & Cancer Genomics and Rare Disease Diagnosis is poised to be account for the most profitable applications owing to their clinical significance and reimbursement routes. Meanwhile, pharmacogenomics and personalized medicine will be the fastest-growing applications since payers have started recognizing the cost avoidance potential of genomics.

- Regional Leadership: North America is projected to command the largest share in the global genomics market, contributing 39.5% to the total market value in 2026, owing to its advanced reimbursement infrastructure and adoption of clinical genomics.

What is the Whole Genome Sequencing Clinical?

Whole Genome Sequencing Clinical Services refer to specialized sequencing technology, reagents, and analysis provided by third-party labs, equipment vendors, and information technology suppliers to help clinical facilities throughout the sequencing workflow process. In contrast to laboratory-scale sequencing, these services have everything to do with the "how" of clinical utility. This encompasses Sample Prep & Library Prep to guarantee the quality of the sample, Sequencing on a platform such as SBS or Nanopore, and Data Processing & Analysis for detecting SNVs, indels, and other structural variations. As whole genome sequencing becomes more about same-day delivery in clinical genomics, professional services are necessary for regulatory compliance, clinical precision, and economical interpretation, thus transforming genomics investments into actionable results.

Use Cases

- Fast Diagnosis in the Neonatal Intensive Care Unit (NICU): The NICU employs Data Analysis & Interpretation Services to analyze whole genomes in less than 48 hours, resulting in a molecular diagnosis for critically ill newborns with rare genetic disorders.

- Tumor and Normal Whole Genomes in Oncology: Cancer research institutes apply Consumables (Library Preparation Kits) and Software & Bioinformatics Services to compare the whole genome of tumors with the patient's germline DNA to determine somatic driver mutations and inherited risk factors for the development of cancers.

- Replacement of Pharmacogenomic Panels in Pharmacies: Hospitals replace genotyping for targeted drug alleles by using Instruments and Reagents & Kits to conduct whole-genome sequencing, thus prospectively prescribing warfarin, clopidogrel, and statins based on patients' profiles of CYP450 and HLA alleles.

- Public Health and Population Genomics: Agencies use Data Processing & Analysis workflows to compile anonymized WGS data stored in biobanks, allowing them to monitor outbreaks of infections (e.g., tuberculosis, SARS-CoV-2 strains) and founder mutations in certain ethnic groups.

How AI is Transforming the Whole Genome Sequencing Clinical Market

Artificial intelligence is disrupting the clinical whole-genome sequencing industry by speeding up the process of variant interpretation and increasing diagnostic success rates. Under the heading of Variant Interpretation & Reporting, artificial intelligence algorithms can automatically prioritize pathogenic variants from millions of variants, eliminating most of the need for ACMG classification and shaving the time from weeks to days. Meanwhile, artificial intelligence tools in Data Processing & Analysis enable clinical labs to improve tertiary analysis through false positive detection, functional prediction, and gene-disease association suggestions.

The clinical workflow and interpretation segment of the business is also gravitating towards artificial intelligence. Under the heading of Software & Bioinformatics Solutions, machine learning models are employed to continuously re-examine unsolved genomes when new gene-disease relationships come out in the open, finding new pathogenic variants that were not seen before. In addition, generative artificial intelligence assistants under Variant Interpretation & Reporting are automating clinical report writing, literature summary, and incidental findings for genetic counselors, leading to a quicker diagnosis for clinicians.

Market Dynamics

Key Drivers in the Global Whole Genome Sequencing Clinical Market

The Global Bioinformatics Skills Gap

Clinical research facilities around the world are struggling to recruit competent individuals who can perform analyses using secondary analysis tools (like BWA, GATK), variant calling, and clinical data interpretation (ClinVar, HGMD). The recruitment and training of bioinformaticians has not kept up with the increasing demand for these capabilities, creating a structural shortage in the field. The consequence of this has been a shift towards outsourcing Data Analysis & Interpretation Services by clinical labs. Clinical laboratories that outsource Data Analysis & Interpretation Services help perform activities such as read alignment, variant calling, annotations, and reporting.

Complexity of Tertiary Genomic Analysis

Additionally, large-sized enterprises (large diagnostic chains) usually employ several types of sequencing platforms (such as Illumina SBS, PacBio SMRT, and Oxford Nanopore) in order to guarantee comprehensive variant identification. Nevertheless, combining information from various technologies is rather challenging. The companies should combine read alignment, variant normalization, structural variant detection, and pharmacogenomic star allele calling on several platforms using different formats of information (FASTQ, BAM, VCF, BED). Such difficulties could provoke diagnostic odysseys and unneeded repeat biopsies in case there is no expert help. In this regard, there is an increasing demand for software & bioinformatics solutions.

Restraints in the Global Whole Genome Sequencing Clinical Market

Legacy Genomic Workflows

The vast majority of clinical laboratories remain on a panel-based and microarray workflow that has evolved over decades and is very customized for individual diseases. The legacy workflows are one of the main barriers to innovation, despite WGS having the potential to offer better results. Transitioning from the existing workflows involves high costs and risks associated with transferring large amounts of historical data, validating lab processes, and educating employees on whole-genome analysis. Large-scale migration involving petabytes of raw sequencing data requires extensive storage and cybersecurity measures. Hospitals fear disruptions in their operations, loss of accreditation from CLIA/CAP, and unexpected costs related to validation.

Reimbursement Uncertainty and Budget Scrutiny

The unstable economic conditions in healthcare and the uncertain payment models make clinical labs more cautious when investing in new instruments and consumables. Despite its importance for precision medicine, whole-genome sequencing faces growing pressure to show its tangible benefits for patients. Capital investments in the purchase of new Instruments (such as the NovaSeq X and PromethION) and consumable agreements will probably be under greater scrutiny. More and more institutions are focusing on small sequencing projects aimed at achieving rapid wins in diagnosis rather than undertaking large population-based sequencing studies or tumor/normal whole-genome sequencing efforts.

Growth Opportunities in the Global Whole Genome Sequencing Clinical Market

Long-Read Sequencing for Structural Variant Detection

The other opportunity for growth in the clinical WGS space is the help provided to institutions in adopting SMRT and nanopore sequencing technologies. While many clinical labs may have worked with SBS short-read sequencing, there is now an interest in adopting technologies that can sequence long fragments to allow for the identification of structural variants, repeat expansions, and homologous sequences that cannot be detected using short-read sequencing. This technology implementation needs specific know-how related to library preparation (high molecular weight DNA), flow cell loading, and long-read sequencing algorithms that tolerate errors. Service providers can assist clinical laboratories to develop workflows to identify conditions such as fragile X, Huntington's disease, and cancer chromothripsis; thus, generating huge demand for specialized consumables and interpretations.

Integrated Genomic-EHR Software Platforms

In addition, the necessity of having genomic information alongside clinical workflow information will promote the adoption of Software & Bioinformatics Solutions that are built in-house within the hospital's EMR infrastructure. The clinicians would need the assistance of making clinical decisions based on the actionable variant information generated automatically. For the professional service providers, it would be beneficial to develop WGS interpretation solutions along with the current EMR infrastructure, using HL7/FHIR guidelines, and developing clinical alerts.

Trends in the Global Whole Genome Sequencing Clinical Market

The Rise of Automated Interpretation Platforms

The trend towards automation in clinical genomics is growing as a solution to manual variant classification. Companies are developing AI-based interpretation tools that produce sign-off ready reports that go to geneticists without having to employ other staff for read mapping, annotations, and classification. Such systems allow for the fast identification of pathogenic variants, automatic scoring based on the ACMG guidelines, and automatic literature curation. To combat this development, suppliers of consumables and instrument manufacturers are joining forces with software companies.

Liquid Biopsy WGS for Early Cancer Detection

Environmental sustainability does not represent the key factor here, but the use of Blood Samples for circulating tumor DNA (ctDNA) whole-genome sequencing appears to be becoming an essential application. The companies are obliged to identify the presence of minimal residual disease and track the treatment response through non-invasive means. This is what has led to the necessity to develop highly deep Reagents & Kits suitable for handling low-input degraded cfDNA. The professional service providers help the clinical laboratories with the validation of ctDNA WGS processes and library preparations for fragmented DNA samples.

Research Scope and Analysis

The Global Whole Genome Sequencing Clinical Market Report is segmented by Product & Service, Technology, Sample Type, Workflow, Application, End User, and Region. It covers consumable sub-segments like Reagents & Kits, Flow Cells, and Library Preparation Kits, providing a comprehensive view of the clinical genomics landscape.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Product & Service Analysis

Consumables is poised to hold the highest proportion in the product & services section of the global whole genome sequencing clinical market due to the need to keep using the consumables on an ongoing basis during the sequencing procedures in every sequence analysis that takes place. There is always a regular demand for consumables in clinical labs where there are thousands of samples analyzed daily rather than buying sequencing equipment once in clinical facilities. With the growing use of precision medicine, oncology tests, and rare diseases, more reagent usage can be expected in hospital settings and laboratories. Moreover, innovations in next-generation sequencing technology have helped analyze more samples within the same period.

By Technology Analysis

The Sequencing by Synthesis (SBS) technology segment is poised to holds the dominance over other segments owing to its superior sequencing accuracy, scalability, cost-effectiveness, and clinical adoption rate. In particular, the SBS technology, which relies mainly on the Illumina platform, is prevalent in clinical applications related to cancer genomics, genetic diseases, reproductive genomics, and population genomics. This is because SBS technology produces highly accurate short-read sequences appropriate for clinical applications. SBS technology can produce highly accurate sequences at higher speeds, thus making it perfect for high-throughput sequencing labs. The wide adoption of SBS-based instruments across the globe, coupled with bioinformatics compatibility and regulatory compliance, enhances its market share.

By Sample Type Analysis

The dominant sample type in terms of usage is blood, thanks to its minimal invasiveness, ease of collection, and compatibility with many applications. Whole-genome sequencing on blood is popular in oncological liquid biopsy studies, genetic diagnosis, pre-natal diagnostics, and pharmacogenomics. Health care professionals are inclined to use blood samples for sequencing, because they simplify the collection process, increase patients' compliance, and facilitate integration into the hospital's workflow. Moreover, blood samples contain high-quality DNA for sequencing purposes and are relatively simple to transport and preserve when compared with tissue biopsies. Increased popularity of ctDNA analysis and non-invasive prenatal screening drives even greater interest in the use of blood samples for genomic tests.

By Workflow Analysis

Sequencing is the leading element of the workflow sector, considering that it forms the backbone of the whole genome sequencing process and is the most technically complex part of the workflow. The sequencing process relies on sophisticated sequencing devices, unique reagents, computing, and other operations, representing the most expensive part of the workflow in terms of expenses. Modern clinical laboratories continue to invest in high-throughput sequencing technologies to enhance their efficiency and increase precision for oncology, orphan diseases, and infectious disease diagnoses. In addition, constant improvements in technology that facilitate faster read lengths, enhanced throughput, and low sequencing costs have led to widespread adoption of sequencing techniques in clinical practices.

By Application Analysis

Oncology and Cancer Genomics are expected to be the leading segments of the application domain because of the high prevalence of cancer across the world and the use of precision oncology techniques. Whole genome sequencing technology allows for the detection of all kinds of mutations, genomic abnormalities, biomarkers, and mechanisms of drug resistance in tumors. The technology has helped healthcare professionals design personalized treatment plans for their patients. Leading pharmaceutical firms and health organizations are using genomic testing to provide targeted drugs and immunotherapy treatments to cancer patients. Other factors such as support from governments through funding of cancer genomics research and increased insurance coverage for molecular diagnostics have fueled market growth.

By End User Analysis

The diagnostic laboratories is anticipated to account for the dominant market share in the end-user industry segment due to their high volumes of genomic testing and the presence of specific infrastructure that is needed for clinical sequencing services. The diagnostic laboratories provide sequencing facilities, certified testing conditions, bioinformatics knowledge, and efficient throughput systems for effective analysis of genomes. Complex sequencing tests are often outsourced by hospitals and other health organizations to diagnostic laboratories because of cost-effectiveness and scale advantages. In addition, an increase in the testing of oncology, prenatal care, and rare diseases has increased the number of sequences in commercial and reference laboratories.

The Global Whole Genome Sequencing Clinical Market Report is segmented on the basis of the following:

By Product & Service

- Instruments

- Consumables

- Reagents & Kits

- Flow Cells

- Library Preparation Kits

- Software & Bioinformatics Solutions

- Data Analysis & Interpretation Services

By Technology

- Sequencing by Synthesis (SBS)

- Single Molecule Real-Time Sequencing (SMRT)

- Nanopore Sequencing

- Ion Semiconductor Sequencing

- Pyrosequencing

- Other Next-Generation Sequencing Technologies

By Sample Type

- Blood Samples

- Saliva Samples

- Tissue Biopsies

- Bone Marrow Samples

- Buccal Swabs

- Other Biological Samples

By Workflow

- Sample Preparation

- Library Preparation

- Sequencing

- Data Processing & Analysis

- Variant Interpretation & Reporting

By Application

- Oncology & Cancer Genomics

- Rare Disease Diagnosis

- Reproductive Health & Prenatal Testing

- Infectious Disease Diagnostics

- Pharmacogenomics

- Personalized Medicine

- Neurological Disorder Testing

- Cardiovascular Genetic Testing

- Population Genomics

By End User

- Hospitals & Clinics

- Diagnostic Laboratories

- Academic & Research Institutes

- Pharmaceutical & Biotechnology Companies

- Contract Research Organizations (CROs)

- Government & Public Health Agencies

Regional Analysis

Leading Region by Market Share

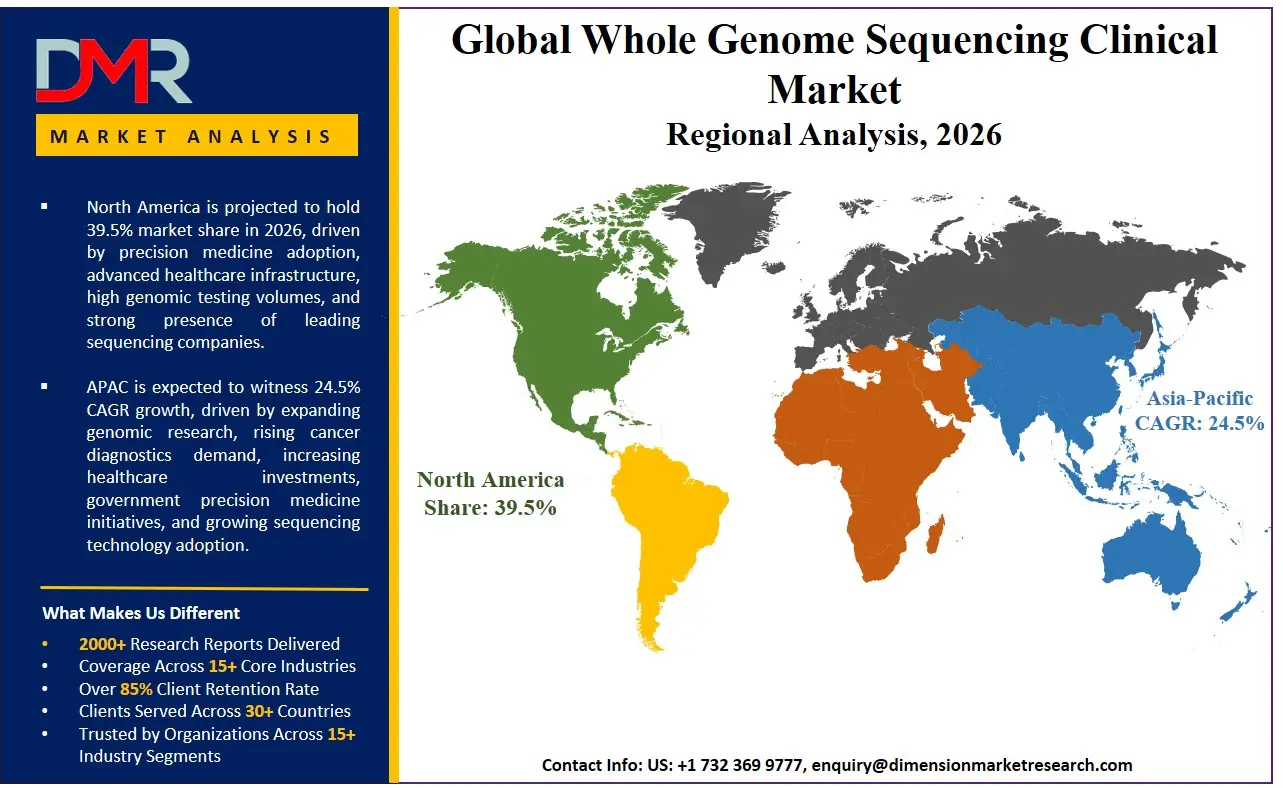

North America is poised to dominate the global clinical whole genome sequencing market as it is projected to hold 39.5% of the market share by the end of 2026. North America, led by the United States, leads with the largest market share, owing to the unparalleled presence of CLIA-certified high-throughput sequencing laboratories and precision medicine initiatives among top cancer institutes and pediatric institutions. The region already possesses a well-developed ecosystem of instrumentation manufacturers such as Illumina and PacBio, bioinformatics solutions providers, and a highly skilled clinical geneticist community. Additionally, investment by enterprises in population genomics studies (All of Us initiative, Million Veteran Program), as well as the phasing out of older genotyping platforms, drives the demand for Data Processing & Analysis and long-read sequencing validation workflows.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Fastest-Growing Regional Market

The Asia-Pacific region is anticipated to see the fastest growth rate in the clinical WGS market, backed by national-level genome medicine efforts such as those in China, India, Japan, and South Korea. Due to rapid economic development, huge patient populations, and the growing number of precision medicine projects, the existing health care facilities and governmental authorities are compelled to replace their old-school genetic analysis systems. The service of Variant Interpretation & Reporting is highly sought after for these organizations to cope with the challenges of ACMG criteria and population-specific variant databases. There is also a shortage of skilled clinical bioinformaticians in the region, which compels them to rely on outsourcing Data Analysis & Interpretation Services.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The competitive landscape in global whole genome sequencing has evolved into one that is very dynamic, with an eclectic mix of international equipment suppliers such as Illumina, PacBio, Oxford Nanopore, and Thermo Fisher, along with suppliers of consumables like Agilent, Qiagen, and Roche, and boutique bioinformatics consultancies. The crucial factor is the formation of strategic partnerships with hospital networks and reference laboratories, which will provide the vital opportunity for validation and co-marketing. Consolidation trends are gaining momentum as the traditional genetic diagnostics companies are merging with AI-driven interpretation firms in order to survive. The role of proprietary IP, in terms of automated variant classifiers and disease interpretation engines, is assuming greater importance in competitive advantage than equipment efficiency and sample cost alone.

Some of the prominent players in the Global Whole Genome Sequencing Clinical Market are:

- Illumina

- Thermo Fisher Scientific

- Oxford Nanopore Technologies

- Pacific Biosciences

- BGI

- QIAGEN

- Agilent Technologies

- Roche

- 10x Genomics

- Azenta Life Sciences

- Eurofins Scientific

- Macrogen

- Novogene

- PerkinElmer

- Bio-Rad Laboratories

- GeneDx

- Nebula Genomics

- Psomagen

- Complete Genomics

- Ultima Genomics

- Other Key Players

Recent Developments

- January 2026: Illumina announced a substantial extension of its clinical bioinformatics partner program, an offering that will enable clients in the field of oncology and rare diseases to adopt automated variant interpretation & reporting processes, leveraging DRAGEN and artificial intelligence-based tertiary analysis capabilities.

- November 2025: PacBio expanded its partnership with one of the largest hospital groups and launched a dedicated workflow for long-read library construction and structural variants analysis for solving rare disease patients who remained undiagnosed despite negative sequencing by synthesis.

- October 2025: Sophia Genetics completed the acquisition of a European clinical decision support system to support its Data analysis & interpretation services for sovereign genomics data centers, catering to the complex needs of governmental and public health organizations in relation to data residency.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 3,668.2 Mn |

| Forecast Value (2035) |

USD 23,473.2 Mn |

| CAGR (2026–2035) |

22.9% |

| The US Market Size (2026) |

USD 1,218.6 Mn |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By Product & Service, By Technology, By Sample Type, By Workflow, By Application, and By End User |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Global Whole Genome Sequencing Clinical Market?

▾ The Global Whole Genome Sequencing Clinical market is poised to be valued at USD 3,668.2 million in 2026 and is projected to reach USD 23,473.2 million by 2035, driven by the universal need for comprehensive genomic testing in oncology, rare diseases, and pharmacogenomics.

What is the CAGR of the Global Whole Genome Sequencing Clinical Market from 2026 to 2035?

▾ The market is expected to grow at a CAGR of 22.9% from 2026 to 2035, reflecting the accelerating complexity of clinical genomic interpretation and the persistent shortage of in-house bioinformatics talent.

What factors are driving the growth of the Global Whole Genome Sequencing Clinical Market?

▾ Key drivers include the global bioinformatics skills gap, the imperative to replace targeted panels with whole genome coverage, the management complexity of tertiary data analysis, and the surge in demand for Variant Interpretation & Reporting amid evolving reimbursement for comprehensive genomic testing.

Which region held the largest share of the Whole Genome Sequencing Clinical Market in 2026?

▾ North America, specifically the United States, is poised to dominate this market as they hold 39.5% of the market share in 2026, driven by a mature reimbursement ecosystem and aggressive hospital investment in population genomics and AI-driven interpretation capabilities.

Which region is expected to grow the fastest in the Whole Genome Sequencing Clinical Market?

▾ The Asia-Pacific region is expected to grow the fastest, fueled by rapid precision medicine initiatives in China, India, and Japan, where Data Analysis & Interpretation Services are critical for transitioning large hospital networks to genomic medicine.

What are the major trends in the Global Whole Genome Sequencing Clinical Market?

▾ Major trends include the integration of AI into Variant Interpretation & Reporting, the rise of long-read sequencing for structural variants, the demand for automated bioinformatics pipelines, and the focus on liquid biopsy WGS for early cancer detection.

Who are the key players in the Global Whole Genome Sequencing Clinical Market?

▾ Key players include instrument manufacturers (Illumina, PacBio, Oxford Nanopore, Thermo Fisher), consumables providers (Agilent, Qiagen, Roche), and clinical bioinformatics platforms (Sophia Genetics, Fabric Genomics, Congenica, DNAnexus).

How is the Global Whole Genome Sequencing Clinical Market segmented?

▾ The market is segmented by Product & Service, Technology, Sample Type, Workflow, Application, and End User.