What is the Zero Liquid Discharge System Market Size?

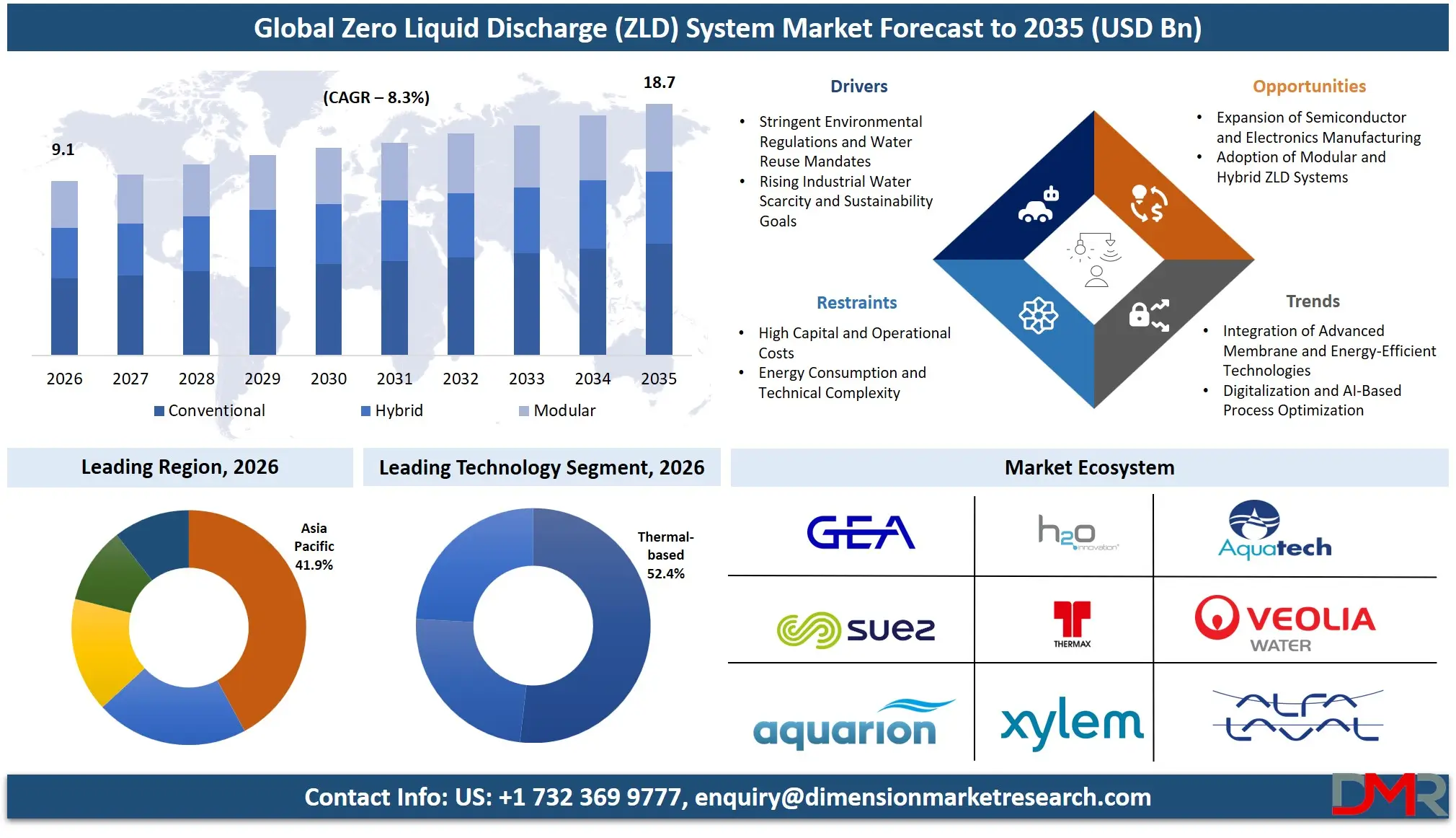

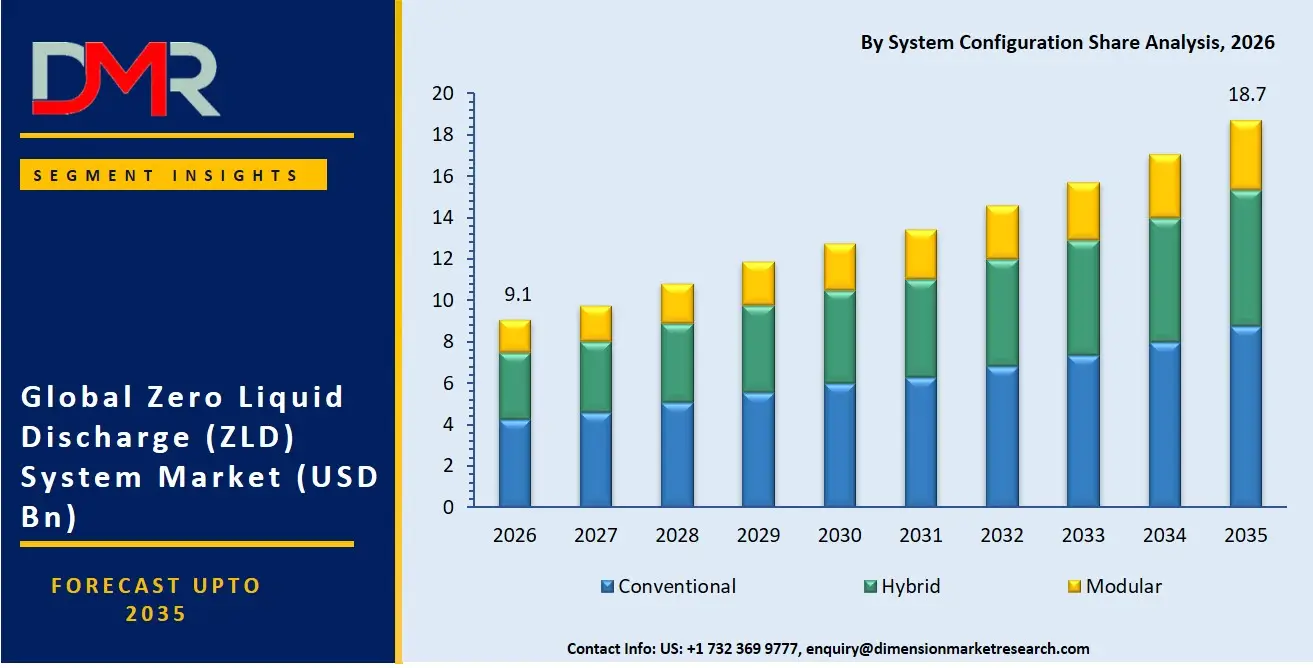

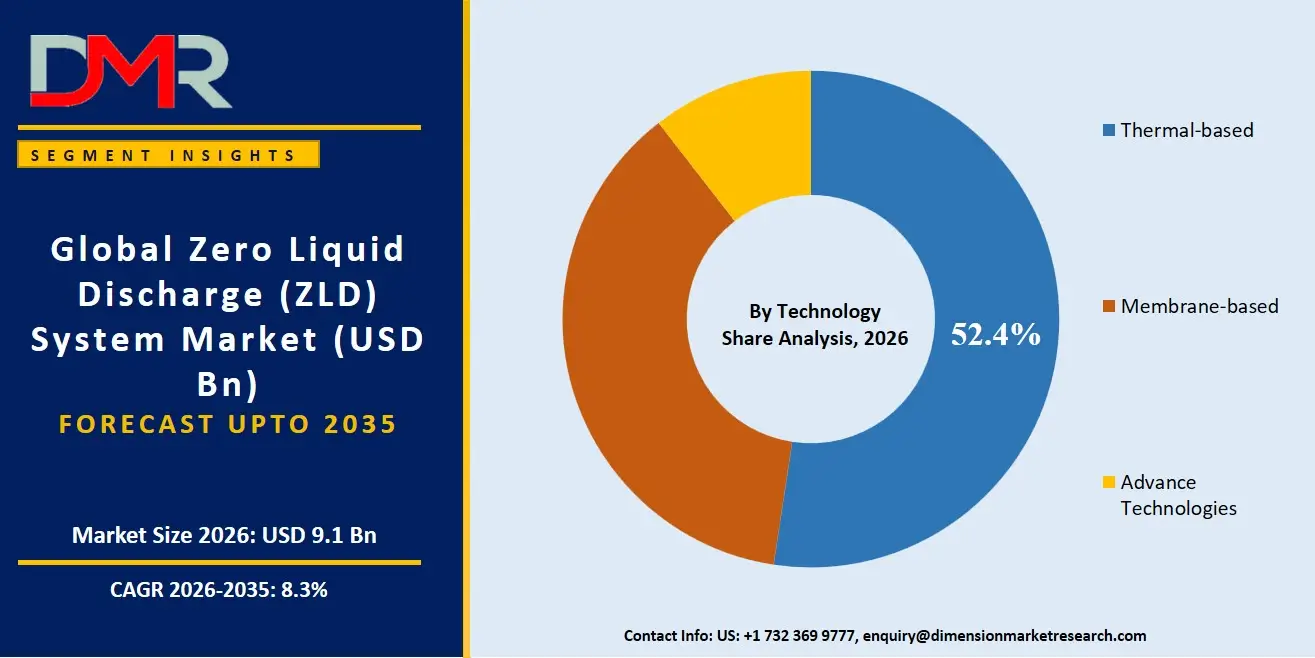

The Zero Liquid Discharge (ZLD) System Market size is expected to be USD 9.1 billion in 2026 and increase at a compound annual growth rate of 8.3% to USD 18.7 billion in 2035 due to need for environmental protection and preservation of freshwater.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The Zero Liquid Discharge (ZLD) System Market can be defined as advanced wastewater treatment technologies designed in such a way that wastewaters from industries can be treated properly without any liquid discharge, recovering a good part of the water used for discharge back into the system. These technologies include thermal process, membranes, evaporations, crystallizations, and filtration processes in order to avoid any contamination of the environment as well as achieve sustainable use of water resources. Usage of ZLD systems is increasing in power generation, oil and gas, chemicals, semiconductors, textile, and pharmaceutical sectors due to stringent regulations on environmental protection and awareness about water problems.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

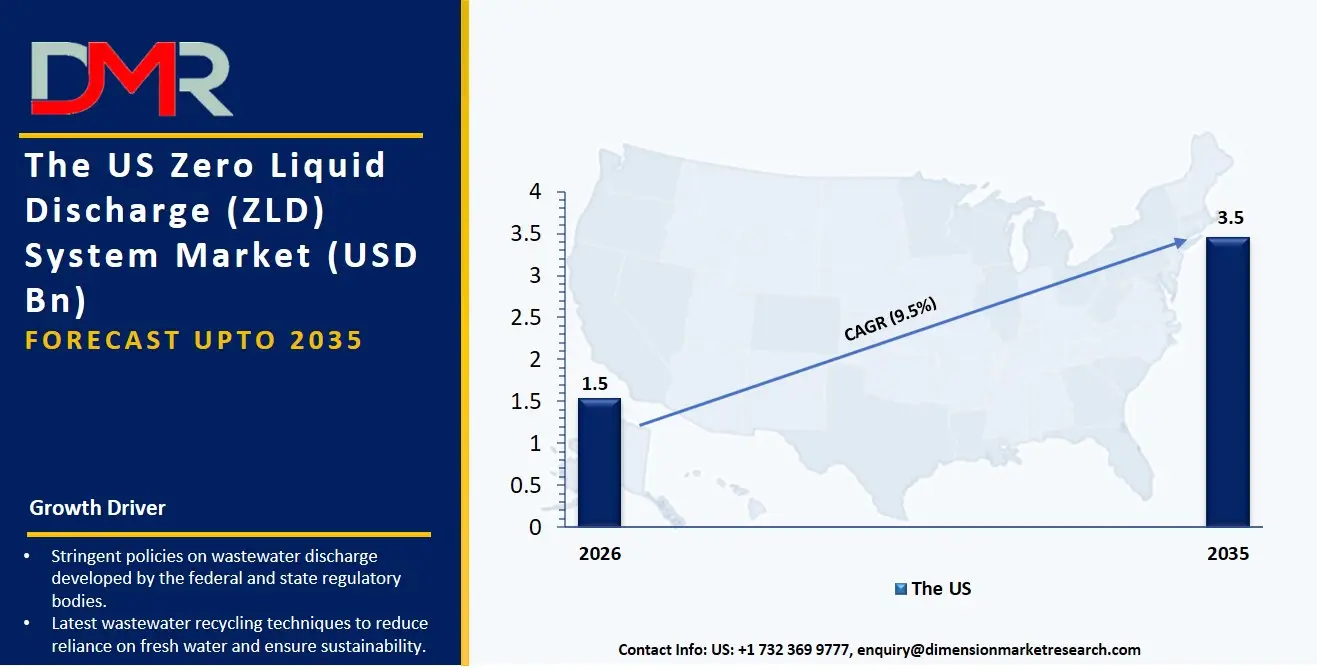

The US Zero Liquid Discharge System Market

The US Zero Liquid Discharge (ZLD) System Market size is estimated to be USD 1.5 billion in 2026 and is expected to increase at a CAGR of 9.5% over the forecast period.

The increase in the use of ZLD systems in the US can be credited to the stringent policies on wastewater discharge developed by the federal and state regulatory bodies, particularly when it comes to power generation plants, chemical production processes, and semiconductor production facilities. Several sectors are using the latest wastewater recycling techniques to reduce reliance on fresh water and ensure sustainability. The rising tendency to exploit shale gas and water used in extracting shale gas is yet another driving factor behind the growing popularity of ZLD systems.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Europe Zero Liquid Discharge System Market

The Europe Zero Liquid Discharge (ZLD) System Market size is estimated to be USD 2.3 billion in 2026 and is expected to increase at a CAGR of 8.1% over the forecast period.

There is an increase in the Europe Zero Liquid Discharge (ZLD) System market because of the stringent environmental compliance frameworks in place and the adoption of sustainable measures that go well with the European Green Deal and circular economy approaches. Companies operating in Germany, France, Italy, and Nordic countries are focusing on water reuse as well as minimizing the production of wastewater in order to mitigate their environmental footprint. As investments in sustainable manufacturing processes, chemical process industries, and pharmaceutical manufacturing increase, there will be more interest in the application of the ZLD technology.

Japan Zero Liquid Discharge System Market

The market size of Japan Zero Liquid Discharge (ZLD) System will be USD 637 million in 2026 and at a CAGR of 7.8% in the forecast period.

The growth of the ZLD System market in Japan has been facilitated by the development of advanced industrial infrastructure, strict environmental regulations, and increasing focus on technologies that conserve water. Semiconductor fabrication, electronics manufacturing, chemicals, and power generation are some important end-use sectors contributing towards market growth. Japan is currently focusing on the installation of energy-efficient and automated wastewater treatment technologies owing to limitations on the availability of fresh water. Growing government initiatives towards improving resource efficiency and de-carbonizing industries will support the adoption of ZLD systems. Membrane technology improvements and process optimization through the use of AI-powered solutions in automated industries requiring ultra-pure water recycling present lucrative opportunities in Japan.

Key Takeaways

- Market Size & Forecast: The Zero Liquid Discharge (ZLD) System Market size is projected to reach USD 9.1 billion in 2026 and is anticipated to have a value of USD 18.7 billion in 2035.

- Growth Rate & Outlook: The Zero Liquid Discharge (ZLD) System Market size is set to grow at a compound annual growth rate of 8.3% during the forecast period of 2026 to 2035.

- Primary Growth Drivers: Some of the major growth drivers in the market Strict Environmental Regulations and Water Recycle Laws, and more.

- Key Market Trends: Some of the major trends in the market are Combining Advanced Membrane Filtration with Energy Efficiency, and more.

- By System Configuration: Conventional segment is anticipated to get the majority share of the Zero Liquid Discharge (ZLD) System Market in 2026.

- By Technology: Thermal-based is expected to get the largest revenue share in 2026 in the Zero Liquid Discharge (ZLD) System Market.

- By End User Industry: Power Generation segment is expected to get the largest revenue share in 2026 in the Zero Liquid Discharge (ZLD) System Market.

- Regional Leadership: Asia Pacific is set to lead the Zero Liquid Discharge (ZLD) System Market with an estimated 41.9% share in 2026.

What is the Zero Liquid Discharge System?

Zero Liquid Discharge (ZLD) Treatment Technology refers to highly sophisticated industrial wastewater treatment that aims at reclaiming almost all water from liquid waste and turning dissolved waste components into solids through various processes. The main processes involved in ZLD technology include membranes, evaporation, crystallization, and thermal separation. The technology is employed in industries that consume huge volumes of water and operate under stringent environmental regulations. These industries include power plants, chemicals, mining, textile, semiconductors, and petroleum and gas industries among others. With rapid industrialization, increasing demand for fresh water, and stringent environmental regulations, there have been increasing efforts in promoting ZLD technology.

Use Cases

- Wastewater recycling in industrial sectors: ZLD technology is extensively adopted in industries to recycle wastewater in order to be reused repeatedly. Chemical industries, pharmaceutical industries, and textile industries make use of this technology in order to save water usage, minimize waste disposal expenses, and adhere to environmental norms for wastewater discharges.

- Water management in power plants: Power plants use ZLD technology to treat flue gas desulfurization wastewater, blowdown from cooling towers, and boiler wastewater in order to recover water effectively without any environmental pollution, meeting environmental norms of wastewater discharges.

- Recycling in semiconductors and electronics: Semiconductors manufacture requires pure water, which results in high contamination wastewater. The ZLD technology can assist the electronics manufacturer to recover valuable water resource and maintain strict quality standards in manufacturing process.

- Produced water treatment in oil & gas industry: ZLD technology is employed by the oil and gas producers to treat produced water, and to reuse this water again in hydrofracturing process.

How AI Is Transforming the Zero Liquid Discharge System Market

Artificial Intelligence is optimizing the efficiency of Zero Liquid Discharge technologies via predictive analytics, automated monitoring, and intelligent process optimization. The AI-driven sensors and monitoring systems can assess the state of water quality, pressure changes, scaling risks, and membrane operation in real-time to help cut down on downtime while increasing efficiency of water purification processes. Artificial Intelligence is also optimizing evaporative and crystallization performance through machine learning algorithms.

In addition to that, AI technologies are increasingly utilized for the purpose of preventing equipment failures, minimizing energy usage, and increasing the accuracy of chemical dosing at wastewater treatment facilities. The use of digital twins and AI-driven simulations helps companies test their wastewater treatment procedures prior to implementing them to minimize risks and save money in the long run.

Market Dynamic

Driving Factors in the Zero Liquid Discharge System Market

Strict Environmental Regulations and Water Recycle Laws

There has been an imposition of strict regulations on the discharge of water from industries due to the need for environmental protection and preservation of freshwater. There have been increased requirements for industries to have efficient waste water treatments that limit the amount of liquid discharged. Compliance penalties and sustainability policies have been motivating organizations to install ZLD technology. There has also been increasing pressure from the ESG and other sustainability policies motivating installation of water recycle facilities.

Restraints in the Zero Liquid Discharge System Market

Higher Capital and Operating Costs

Incorporating and operating Zero Liquid Discharge treatment technologies entails high capital expenditures because of the use of complicated machinery like evaporators, crystallizers, and membranes for water purification processes. Operating costs such as energy costs, maintenance, and chemicals may affect the feasibility of implementation of such projects, particularly in small-scale operations. The high cost of operations is usually the reason behind the delayed implementation of these technologies.

Opportunities in the Zero Liquid Discharge System Market

Expanding Semiconductor and Electronic Manufacturing Plants

The fast expansion in the construction of semiconductor production plants and electronic manufacturing plants offers immense prospects for ZLD technology. Such plants are known to require pure water and produce wastewater with great complexity that requires effective methods of treatment. Growing spending on setting up chip-manufacturing plants in the US, Japan, South Korea, and Europe is likely to boost the need for high-performance membrane and crystallization techniques.

Trends in the Zero Liquid Discharge System Market

Combining Advanced Membrane Filtration with Energy Efficiency

Industries are adopting new membrane filtration technologies such as reverse osmosis, nanofiltration, and forward osmosis in ZLD systems to optimize the recovery process and minimize the operating cost. The use of energy-efficient evaporators and mechanical vapor compression systems is becoming popular since these systems require less energy than other systems. Technological innovations that address the challenges of scaling and fouling in the process of water treatment have made ZLD systems more commercially viable.

Research Scope and Analysis

The scope of research is responsible for determining the limits and goals of the research, and it indicates what needs to be studied and what should be left out. On the other hand, analysis entails the evaluation of gathered information and the identification of trends within the data in order to make sense out of it.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By System Configuration Analysis

Conventional ZLD Systems are estimated to capture around 46.8% of the total market share in 2026 due to their extensive application at industrial sites that have existing wastewater treatment infrastructures. This can be attributed to the reliability of these systems in terms of functioning and suitability for the combination of membrane filtration techniques along with thermal evaporation, which is widely prevalent in both power plants and chemical plants. On the contrary, Hybrid ZLD Systems are anticipated to become the most lucrative category owing to the increasing emphasis on energy efficiency and low operating expenses through hybridization of membrane technology with thermal technologies. There has also been rising popularity for modular and portable ZLD systems in order to cater to decentralized industrial operations and small-scale manufacturing units.

By Technology Analysis

Thermal-Based Technologies are projected to account for about 52.4% market share by 2026 due to their highly efficient capacity for treating highly saline industrial wastewater. Technologies like Multi-Effect Evaporation and Mechanical Vapor Recompression continue to be extensively employed in power plants, chemical industries, and mining operations where zero discharge of wastewater is imperative. On the other hand, Membrane-Based Technologies are forecasted to exhibit the fastest growth attributed to the fact that they consume less energy compared to other systems. They are currently being incorporated in advanced ZLD systems to decrease costs and mitigate environmental impacts associated with operations. Other emerging technologies that include Forward Osmosis and Membrane Distillation are also gaining ground due to their efficiency in treating wastewater from industrial sources.

By Treatment Capacity Analysis

Large Scale systems with capacities between 1,000 and 10,000 m³/day are forecast to capture about 39.7% of market share by 2026 owing to their widespread application at power stations, petrochemical sites, and industrial plants. Such large scale industrial applications demand substantial wastewater treatment plants to meet regulatory requirements as well as facilitate uninterrupted industrial operations. Nevertheless, Very Large Scale systems above 10,000 m³/day are expected to experience the highest growth rate in the coming years as clusters of industrial activity and mega manufacturing plants start to invest in water recycling systems. With growing industrialization and increasing pressure on freshwater resources in emerging economies, investments in such water recycling systems are likely to increase rapidly.

By Feed Water Type Analysis

Industrial Wastewater is set to lead the industry with a projected market share of 44.3% by 2026 due to high amounts of wastewater generated by industries including chemicals, pharmaceuticals, textile and manufacturing processes. Environmental compliance and growing need for industrial water reuse are encouraging the installation of ZLD technologies in order to treat industrial wastewater. The Produced Water treatment is anticipated to be the most attractive sector for the industry due to rising exploration activities of oil and gas and concern towards the environment regarding produced water disposal. Furthermore, treatment of Flue Gas Desulfurization (FGD) wastewater has become significant for thermal power generation due to growing environmental regulation pressures.

By End Use Industry Analysis

Power Generation is anticipated to hold almost 28.6% market share by 2026 owing to huge amounts of wastewater generation and stringent environmental discharge policies enforced on thermal and nuclear power plants. Zero Liquid Discharge systems find widespread application in treatment of blowdown from cooling towers and flue gas desulfurization wastewaters. Nonetheless, it is predicted that Semiconductor & Electronics industry would emerge as the fastest-growing market segment owing to rising requirement for highly pure water and efficient wastewater recovery systems in semiconductor chip fabrication plants. There continues to be strong investment by Chemical & Petrochemical industries towards sustainable water treatment processes.

The Zero Liquid Discharge System Market Report is segmented on the basis of the following:

By System Configuration

- Conventional ZLD Systems

- Hybrid ZLD Systems

- Modular/Containerized ZLD Systems

By Technology

- Thermal-Based Technologies

- Multi-Effect Evaporation (MEE)

- Mechanical Vapor Recompression (MVR)

- Brine Concentrators

- Crystallizers

- Membrane-Based Technologies

- Reverse Osmosis (RO)

- Ultrafiltration (UF)

- Nanofiltration (NF)

- Electrodialysis / Electrodialysis Reversal (ED/EDR)

- Advanced Technologies

- Forward Osmosis (FO)

- Membrane Distillation

- Freeze Crystallization

- Electrochemical Treatment

By Treatment Capacity

- Small Scale (<100 m³/day)

- Medium Scale (100–1,000 m³/day)

- Large Scale (1,000–10,000 m³/day)

- Very Large Scale (>10,000 m³/day)

By Feed Water Type

- Industrial Wastewater

- Produced Water

- Brine Concentrate

- Flue Gas Desulfurization (FGD) Wastewater

- Municipal Wastewater

By End-use Industry

- Oil & Gas

- Chemical & Process Industries

- Chemicals & Petrochemicals

- Pharmaceuticals

- Fertilizers

- Water-Intensive Manufacturing

- Textile & Dyeing

- Pulp & Paper

- Food & Beverage

- Heavy & Advanced Manufacturing

- Mining & Metallurgy

- Semiconductor & Electronics

- Automotive Manufacturing

- Other Industrial Applications

- Leather Processing

- Municipal Utilities

- Agrochemicals

- Power Generation

Regional Analysis

Leading Region in the Zero Liquid Discharge System Market

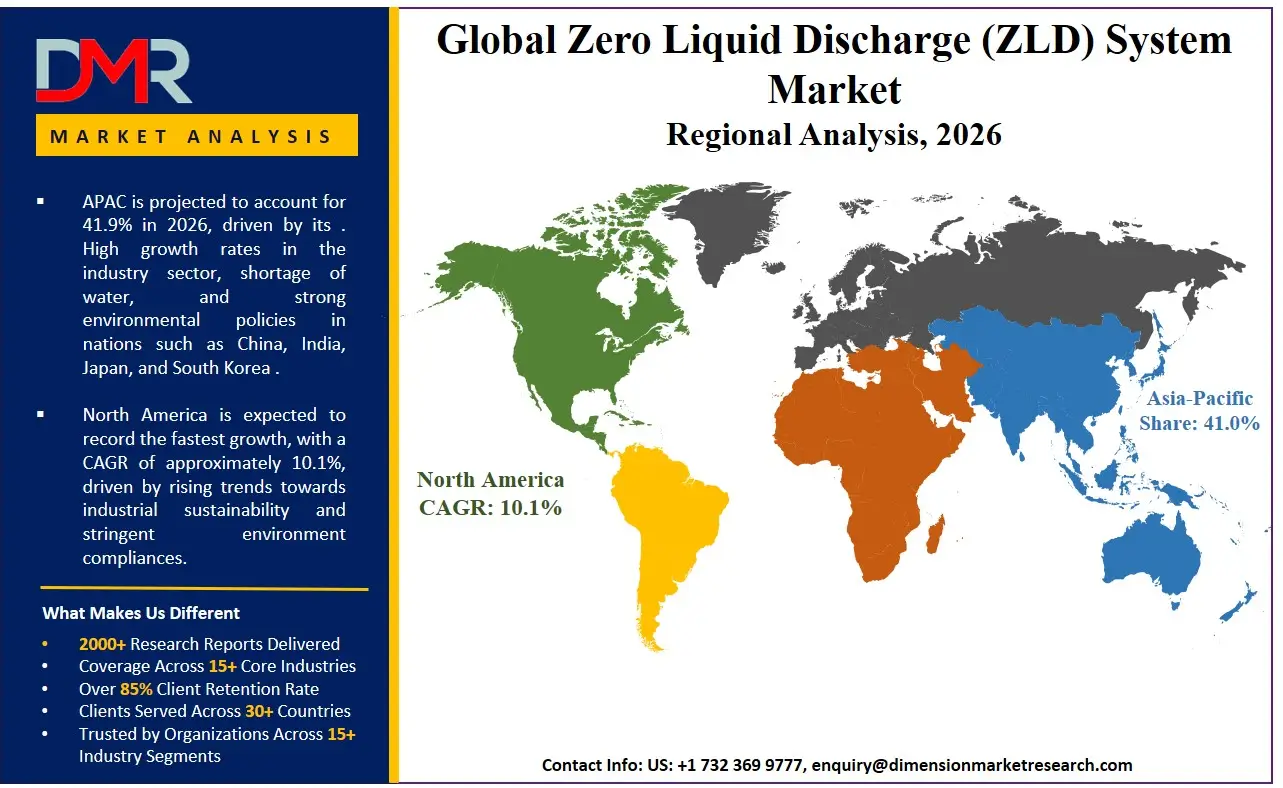

Asia-Pacific is expected to hold a market share of 41.9% by 2026 due to its dominance in the ZLD system market. High growth rates in the industry sector, shortage of water, and strong environmental policies in nations such as China, India, Japan, and South Korea are responsible for making the region a dominant one. Increased demand from the chemical, power, semiconductor, and textile industry sectors is driving growth in the market. Awareness regarding sustainability practices on the part of government officials in the region is helping boost the trend.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Fastest Growing Region in the Zero Liquid Discharge System Market

The North American region is expected to emerge as the fastest-growing regional market for the Zero Liquid Discharge (ZLD) System market owing to the rising trends towards industrial sustainability and stringent environment compliances. The proliferation of semiconductor manufacturing plants, shale gas plants, and advanced manufacturing plants has led to an increased demand for water recycling and waste-water reduction solutions. Industrial sectors from the USA and Canada have started adopting ZLD systems which operate efficiently in saving energy and conserving water. With government support towards sustainable industrial developments along with technological developments such as automation and membrane filtration processes, the growth of the regional market has gained pace.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The ZLD System market is noted for high levels of technological competition, heavy reliance on capital investment, and an ever-growing trend towards innovation-based differentiation. The primary focus within the ZLD market revolves around efforts to boost membrane efficiency, cut down on energy requirements, and develop hybridized systems. Partnerships with manufacturers, engineers, and utilities have been seen increasingly as a means of enhancing project implementation skills. Investments in R&D as well as in digital monitoring and AI technologies have also become important for gaining competitive edge in industrial wastewater treatment efficiency, scalability, and regulatory compliance.

Some of the prominent players in the global Zero Liquid Discharge (ZLD) System are:

- Veolia Water Technologies

- Aquatech International

- GEA Group

- Alfa Laval

- Xylem

- SUEZ Water Technologies & Solutions

- IDE Technologies

- Thermax Limited

- Kurita Water Industries

- Saltworks Technologies

- Praj Industries

- H2O GmbH

- Mitsubishi Heavy Industries

- SafBon Water Technology

- Aquarion AG

- Evoqua Water Technologies

- Doosan Hydro Technology

- Condorchem Envitech

- Oasys Water

- ANDRITZ

- Other Key Players

Recent Developments

- In May 2026, Aquatech has announced the acquisition of FTS H2O for bolstering its competencies in lithium processing, Zero Liquid Discharge (ZLD), and industrial brine treatment systems. It further improves the knowledge base around energy efficient evaporation and crystallization systems which enable enhanced lithium recovery, wastewater recycling, and brine concentration technologies. The need for such sustainable water treatment services is ever increasing due to changing environmental laws and pressure from the industry to reduce reliance on fresh water sources.

- In April 2026, DuPont launched two new reverse osmosis membrane elements, which include FilmTec™ Fortilife™ XC-Max UHP and FilmTec™ Fortilife™ XC220, that will further improve ZLD and MLD processes. These solutions offer better efficiency for water recovery and brine management that enable industries to achieve greater efficiency and lower costs while addressing water recycling needs and other concerns in a highly regulated industry.

- In March 2026, The Enviro Control Company announced that their project for a 250 MLD Water Treatment Plant with zero liquid discharge will be started at Variav, Surat. The plant has a complete recycling system of the backwash and sludge filtrate flows, thus making an additional contribution of 10 MLD within the premises. With cascade aeration, lamella clarification, rapid gravity filtration, and disinfection, the plant produces high-quality water regardless of fluctuations in the quality of raw water.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 9.1 Bn |

| Forecast Value (2035) |

USD 18.7 Bn |

| CAGR (2026-2035) |

8.3% |

| Historical Period |

2021 – 2025 |

| Forecast Period |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Segments Covered |

By System Configuration, By Technology, By Treatment Capacity, By Feed Water Type, By End-use Industry |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Zero Liquid Discharge (ZLD) System Market?

▾ The Zero Liquid Discharge (ZLD) System Market size is expected to reach USD 9.1 billion by 2026 and is projected to reach USD 18.7 billion by the end of 2035.

What is the CAGR of the Zero Liquid Discharge (ZLD) System Market from 2026 to 2035?

▾ The market is growing at a CAGR of 8.3 percent over the forecasted period.

What factors are driving the growth of the Zero Liquid Discharge (ZLD) System Market?

▾ Digital Transformation through Cloud Technology, and more are the factors driving the growth of the Zero Liquid Discharge (ZLD) System Market.

What are the major trends in the Zero Liquid Discharge (ZLD) System Market?

▾ Combining Advanced Membrane Filtration with Energy Efficiency, and more are some of the major trends in the market.

Who are the key players in the Zero Liquid Discharge (ZLD) System Market?

▾ Some of the key players in the Zero Liquid Discharge (ZLD) System Market include GEA, Xylem, Thermax, and more.

How is the Zero Liquid Discharge (ZLD) System Market segmented?

▾ The Zero Liquid Discharge (ZLD) System Market is segmented by system configuration, technology, treatment capacity, feed water type, end-use industry.

Which region held the largest share of the Zero Liquid Discharge (ZLD) System Market in 2026?

▾ Asia Pacific is set to lead the Zero Liquid Discharge (ZLD) System Market with an estimated 41.9% share in 2026.

Which region is expected to grow the fastest in the Zero Liquid Discharge (ZLD) System Market?

▾ North America is the fastest-growing region in the Zero Liquid Discharge (ZLD) System Market during the forecast period.