What is the Global Antisense Oligonucleotide Therapy Market Size?

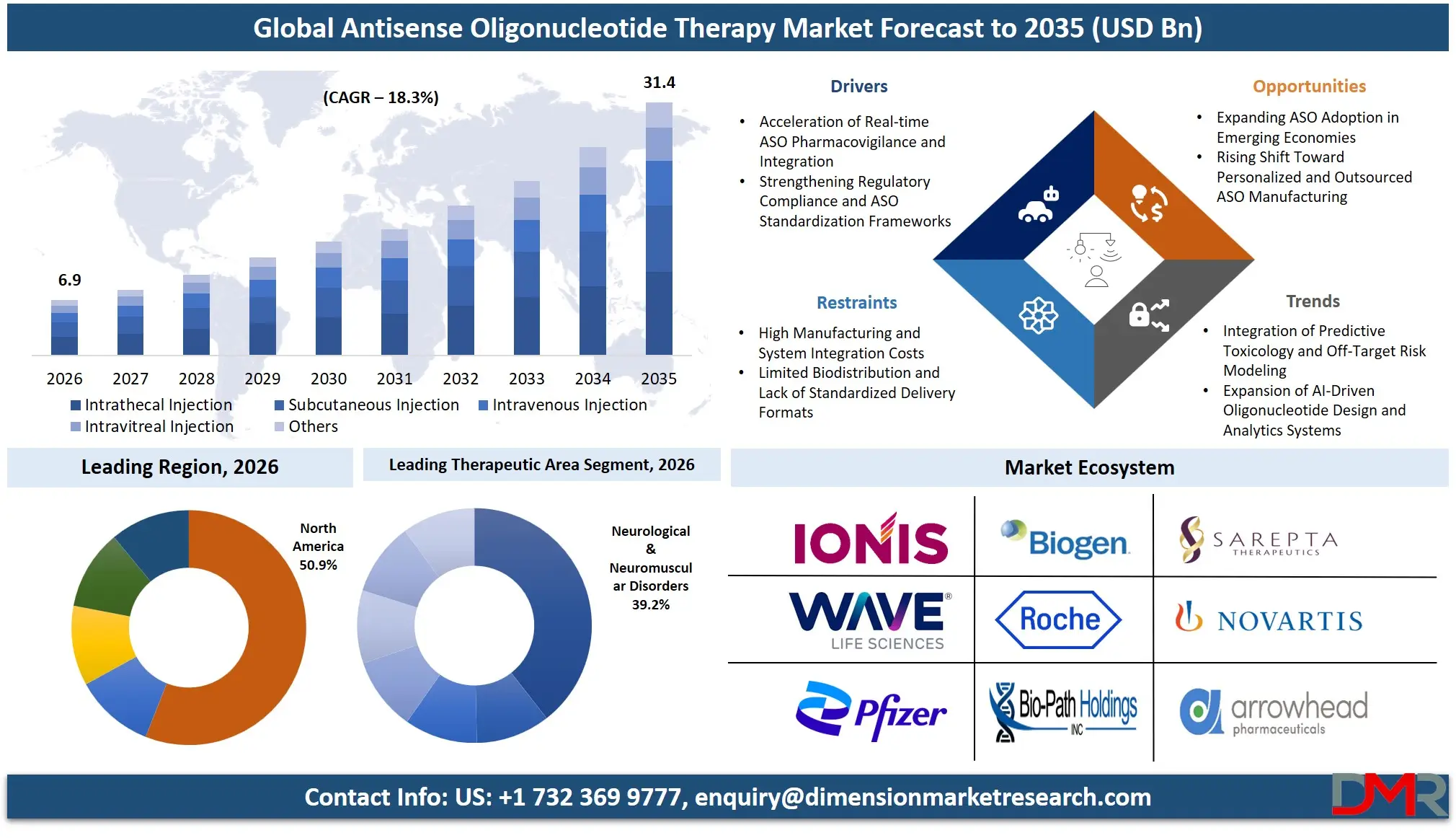

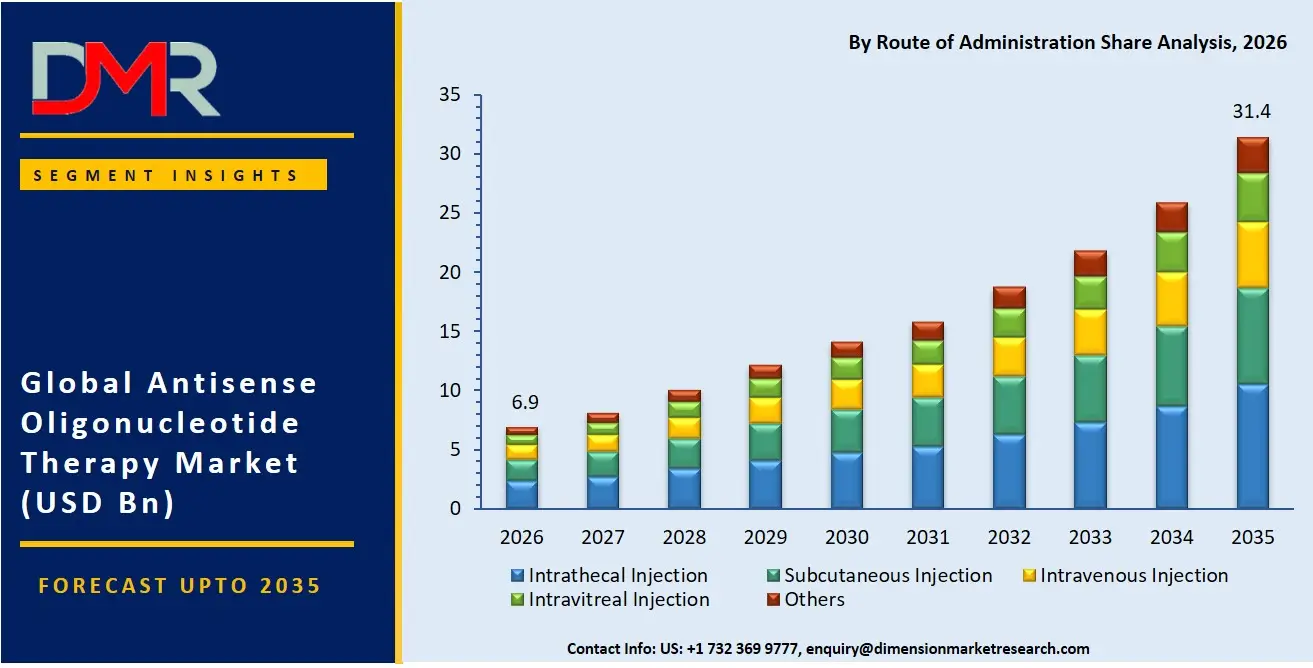

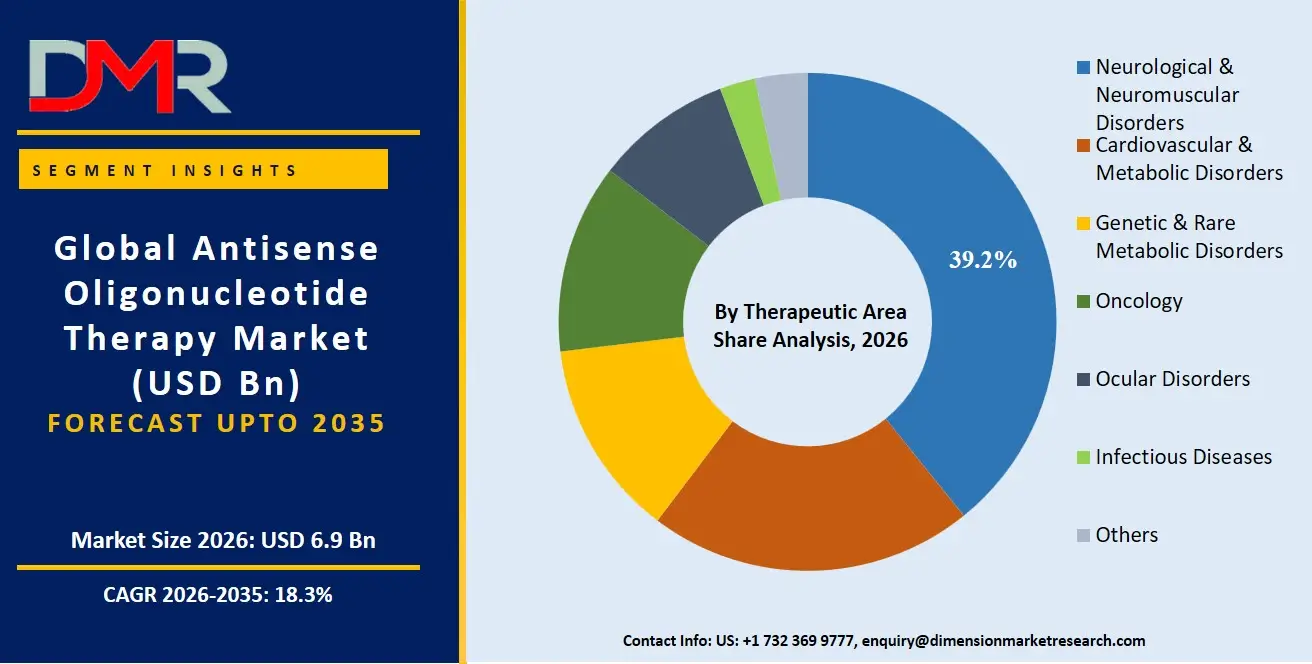

The Global Antisense Oligonucleotide Therapy Market size is estimated at USD 6.9 billion in 2026 and is projected to reach USD 31.4 billion by 2035, exhibiting a CAGR of 18.3% during the forecast period, driven by the rising use of targeted RNA modulation, accelerated regulatory designations for rare diseases, decentralized manufacturing models for personalized genetic medicines, and connected real-world evidence systems for ASO pharmacovigilance.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The global antisense oligonucleotide therapy market is expanding because of increasing application of chemically modified ASOs in treating neurological and neuromuscular disorders; increasing regulatory incentives, which reduce the risk of off-target effects during clinical development and speed up orphan drug designations for new genetic therapies; and more funding in automating ASO sequence design and toxicity prediction.

Some other reasons for expansion in this market include new technologies in stereopure ASO synthesis, splice-switching oligonucleotides through improved cellular uptake, automated large-scale solid-phase synthesis, high-throughput in vivo efficacy platforms, and improved cross-border data-sharing for rare disease registries. The digital shift in neurology clinics and metabolic care has been helpful in speeding up patient enrollment and making sensitive genetic data management easier. This includes encrypted clinical trial analytics research. In addition, government plans focusing on genomic medicine infrastructure and the secure ASO supply chain have ensured steady research in antisense oligonucleotide systems.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

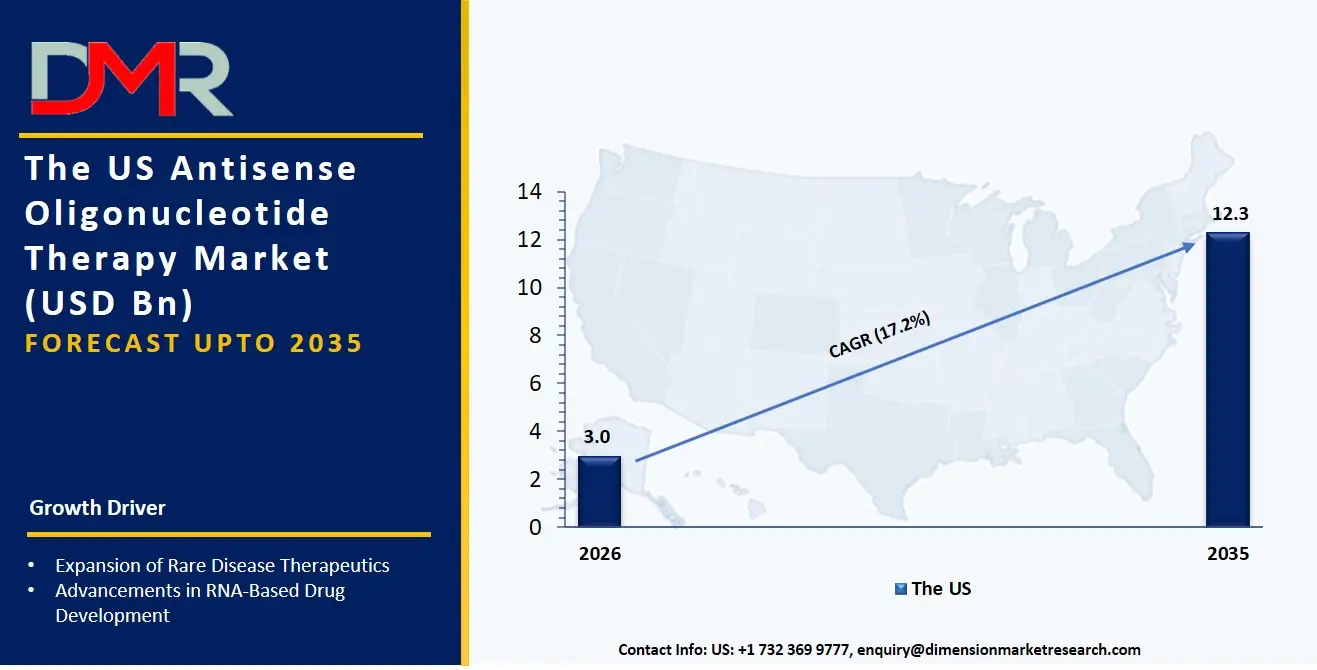

The US Antisense Oligonucleotide Therapy Market

The US Antisense Oligonucleotide Therapy Market is estimated to grow to USD 3.0 billion in 2026 with a compound annual growth rate of 17.2% during the forecast period.

The US market is shaped by major federal and state-level programs promoting personalized genomic therapies, secure ASO adoption supported by FDA's accelerated approval pathways and rare disease consortia, and NIH-led antisense modernization initiatives. These programs encourage the use of high-throughput ASO screening, real-time pharmacokinetic modeling, and predictive immunogenicity assessment software for ASO candidates. Automated antisense platform technologies are being rapidly adopted, and the US continues to invest in better data sharing between research labs, encrypted preclinical study systems, and reliable ASO toxicity prediction tools for ASO therapy platforms. Service providers are also influenced by laws like GLP, GCP, and national genomic data protection strategies to offer services that ensure ASO data safety, rule-following, and smooth integration across academic and commercial manufacturing environments.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Europe Antisense Oligonucleotide Therapy Market

The European Antisense Oligonucleotide Therapy Market is estimated to be valued at USD 1.7 billion in 2026, witnessing growth at a CAGR of 15.8%, during the forecast period.

Europe's ASO therapy market is well-established, shaped by EU-wide policies such as the European Reference Networks for rare diseases, EMA's PRIME scheme, and national policies to support oligonucleotide innovation hubs (e.g., Germany's RNA medicine initiatives and France's national genomic medicine plans). Countries are also making ASO post-authorization safety monitoring more flexible to align payer and provider demands and enable the sharing of real-world ASO outcomes across borders. The market grows due to new tools like software for in silico ASO off-target prediction and risk stratification systems for ASO manufacturing. Use is made easier by teamwork between public and private consortia and shared ASO safety protocols. Manufacturers have access to technologies such as LNA-based high-affinity binding, Gapmer-mediated gene silencing, and secure ASO audit logging, and Europe is at the forefront of the digitisation of safe and efficient ASO therapy operations.

Japan Antisense Oligonucleotide Therapy Market

The Japan Antisense Oligonucleotide Therapy Market is projected to be valued at USD 486.0 million in 2026, progressing at a CAGR of 20.4%, during the period spanning from 2026 to 2035.

Japan's ASO therapy market is well developed, with high-quality oligonucleotide data platforms, connected secure ASO manufacturing management systems, and a wide array of ASO analytics software tools. National focus on automation, efficiency, and process integrity is delivered via encrypted ASO data models and smart genomic asset protection. Growth opportunities are helped by government measures under the Japan Agency for Medical Research and Development (AMED)'s secure RNA strategy, METI's biomanufacturing initiatives, and continued investment in ASO cloud R&D. AI-driven ASO design research, multi-party analytics for condition-specific genomic data sharing, and virtualized ASO manufacturing environments all need effective ASO software to keep pace with modified oligonucleotide synthesis. Higher costs for validating new ASO platform technologies and connecting them with older infrastructure are significant, but there are opportunities for the export of Japanese ASO technologies to the Asian and Pacific markets.

Key Takeaways

- Market Size & Forecast: The Global Antisense Oligonucleotide Therapy Market is estimated to be valued at USD 6.9 billion in 2026 and is expected to grow to USD 31.4 billion by 2035.

- Growth Rate & Outlook: The market is expected to witness growth at a compound annual growth rate of 18.3% in the forecast period.

- Primary Growth Drivers: The availability of new ASO chemical modification technologies that use stereopure synthesis, the need to speed up regulatory outcomes for rare diseases and improve success rates of targeted gene modulation, and more government investment in national genomic medicine infrastructure are key growth drivers.

- Key Market Trends: The real-time profiling of ASO immunogenicity risks, modified oligonucleotide payload handling, and the shift to AI-driven ASO design platforms and automated oligo manufacturing management are key market trends.

- By Therapeutic Area: The neurological & neuromuscular disorders segment is expected to take the largest revenue share in 2026.

- By Route of Administration: Intrathecal injection is expected to take the largest revenue share in 2026 in the ASO therapy market.

- By End User: Hospitals & specialized clinics are estimated to take the lead in 2026 with the largest share in the ASO therapy market.

- Regional Leadership: North America is estimated to take the lead in 2026 with 50.9% share in the ASO therapy market, owing to significant investment in genomic data privacy modernization and sovereign oligonucleotide manufacturing technologies.

What is Antisense Oligonucleotide Therapy?

Antisense Oligonucleotide Therapy refers to a class of synthetic, chemically modified short nucleic acid sequences that bind to complementary RNA targets via Watson-Crick base pairing, providing enhanced capabilities beyond traditional small molecules, including the ability to modulate gene expression pre-translationally, prevent synthesis of toxic proteins via RNase H-mediated degradation, and enable splice-switching for exon skipping or inclusion. These therapies include phosphorothioate ASOs, PMO-based drugs, 2'-MOE gapmers, and LNA-modified ASOs. These platforms use modern systems such as in silico target prediction, high-throughput solid-phase synthesizers, and remote pharmacovigilance to manage, verify, and track patient genetic responses and outcomes. To improve ASO therapeutic outcomes, manage dosing variability and condition-specific treatment programs, and expand coverage into personalized genomic medicine to support individual patient care and promote the development of targeted genetic products.

Use Cases

- Market Stability for Recurrent Dosing: ASO therapy platforms can provide market-balancing benefits through software (real-world analytics, adherence monitoring) and control systems to reduce dose omission risk and support settlement of ASO reimbursement claims in days, compared to weeks that it would take with only manual paperwork.

- Long-Term Genetic Asset Management: Long-term data on ongoing ASO safety issues, including immunogenicity intermittency, supply chain price spikes, or manufacturing degradation, are studied to better understand market performance and to help plan long-term software-based patient care.

- Manufacturing Load Balancing: Oligonucleotide production and quality control are handled through ASO platform software in CDMO and corporate settings to support market capacity balance for modified ASO workloads.

- Government & Regulated Programs: Faster ASO candidate development helps genomic innovation and targeted rare disease programs; government programs, through smart monitoring of national real-world ASO outcomes, advance national genomic protection strategies and help the adoption of operational standards.

How AI Is Transforming the Global Antisense Oligonucleotide Therapy Market?

Artificial intelligence (AI) is being used progressively more often in ASO therapy platforms to improve ASO sequence efficacy forecasting, find safety quality trends in clinical trial data, and automatically spot unusual patterns in patient immunogenicity responses. It also allows faster ASO lead optimization because it can handle in silico sequence submissions on a large scale. Encrypted clinical trial logs are easier to study and help registries find integration issues, reduce mistakes, and improve the overall accuracy of ASO regulatory submissions. This has resulted in R&D being cost-effective, quicker, and more efficient than the old manual screening method.

AI is also strengthening research and development by improving ASO off-target risk assessment and enabling more accurate capacity planning for ASO synthesizers. It helps manufacturers predict how many modified oligonucleotide batches will be needed, find possible synthesis delays, and monitor the performance of ASO supply networks more effectively. In addition, automation of routine pharmacovigilance checks and performance tracking is reducing operational workload, lowering administrative costs, and improving overall efficiency. This is leading to better financial results and more stable operations across the ASO therapy production chain.

Market Dynamics

Key Drivers of the Global Antisense Oligonucleotide Therapy Market

Acceleration of Real-time ASO Pharmacovigilance and Integration

The market is growing with the rise of real-world evidence tools to check and process ASO safety integration, better management of sensitive patient genomic workloads, and a closer connection of patient registries and secure ASO distribution channels. ASO therapy platforms provide real-world data that allows monitoring of long-term efficacy, helping to spot safety signals early, and checking dosing protocols much faster. This has improved efficiency in clinical operations and reduced human mistakes as well as administrative costs. At the same time, demand for more automated R&D is being helped by more activity in predictive analytics for the assessment of individual patient responses, as genetic medicine further digitizes basic RNA data processing tasks.

Strengthening Regulatory Compliance and ASO Standardization Frameworks

There is increasing emphasis on openness, genomic data accuracy, and rule-following within the ASO therapy system. Rules and frameworks such as FDA accelerated approval, EMA PRIME, and orphan drug designations in key markets are encouraging better ASO handling practices and more structured clinical development processes. These advances are supporting the need for systems that can offer steady monitoring of sensitive genetic assets and standardized safety reporting. At the same time, active work to improve the sharing of real-world ASO outcomes and reduce verification issues is strengthening the need for more effective management systems in both government and private market participants.

Restraints in the Global Antisense Oligonucleotide Therapy Market

High Manufacturing and System Integration Costs

The rollout of ASO therapy manufacturing remains costly, requiring significant investment in solid-phase synthesizers, purification systems (e.g., HPLC), analytical characterization, and alignment with existing GMP workflows. In addition, following data privacy rules such as GDPR and other regional genetic data laws adds to trial complexity. These factors increase upfront costs and can limit adoption, especially among smaller biotechs and emerging gene therapy companies.

Limited Biodistribution and Lack of Standardized Delivery Formats

There is still fragmentation in the market in terms of ASO tissue distribution and cellular uptake mechanisms. Although some areas have put in place organized ASO delivery systems (e.g., conjugates), many programs continue to work with both unmodified and advanced chemical modifications. Lack of standardized extrahepatic delivery protocols limits the ability to achieve therapeutic concentrations in target tissues and results in inefficiencies in clinical development and patient outcomes.

Growth Opportunities in the Global Antisense Oligonucleotide Therapy Market

Expanding ASO Adoption in Emerging Economies

Newly developing economies such as Brazil, Indonesia, Nigeria, the UAE, and Vietnam are slowly building their genomic medicine and ASO therapy systems. These regions have long-term growth possibilities, with more people gaining access to rare disease diagnosis, and with more people becoming aware of genetic treatment programs and slowly digitizing patient data care. These markets have few older ASO registry systems and can be used with new, technology-driven ASO platforms that can grow over time.

Rising Shift Toward Personalized and Outsourced ASO Manufacturing

The move to decentralized oligonucleotide production, modular ASO synthesis networks, and real-time quality control is creating the adoption of flexible manufacturing platforms. These systems allow centralized patient data access, better coordination between diagnostic registries and therapy providers, and faster ASO batch release. Outsourced manufacturing is increasingly becoming a trend among modern ASO drug developers as operational efficiency becomes one of the competitive factors.

Global Antisense Oligonucleotide Therapy Market Trends

Integration of Predictive Toxicology and Off-Target Risk Modeling

ASO therapy platforms are gradually adding data-driven technology to find off-target risks and improve accuracy in patient stratification. These systems allow clinicians and researchers to study patient genotypic behavior better, simplify the management of their ASO therapeutic portfolios, and improve overall treatment outcomes. This move is slowly turning the industry more proactive and data-driven in genetic medicine instead of being purely reactive in clinical practice.

Expansion of AI-Driven Oligonucleotide Design and Analytics Systems

The use of AI-based ASO design platforms is currently becoming a basic part of today's oligonucleotide development. These systems allow real-time sequence optimization, centralized target administration, and better collaboration among research participants. AI-based ASO design platforms are improving the efficiency and success rates of developers that operate across multiple therapeutic areas by removing the need to rely solely on empirical screening and allowing operations to scale more easily.

Research Scope and Analysis

The Global Antisense Oligonucleotide Therapy Market is witnessing strong growth driven by rising approvals of ASO drugs, expansion into new therapeutic areas, and increasing demand for targeted genetic therapies. The market is segmented based on therapeutic area, route of administration, drug type, technology platform, and end user.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Therapeutic Area Analysis

The Neurological & Neuromuscular Disorders segment is likely to continue dominating the market in 2026, accounting for approximately 39.2% of the global ASO therapy market share. This is due to its key role in enabling treatment for SMA (Spinraza), Duchenne muscular dystrophy (Exondys 51), and other CNS disorders, and its usefulness in indications with high unmet need where targeted RNA modulation is required. Within this segment, Spinraza holds the largest share, driven by established commercial presence, long-term real-world evidence, and continued international access programs. The Genetic & Rare Metabolic Disorders segment is driven by novel ASO candidates for transthyretin amyloidosis (Tegsedi) and familial chylomicronemia syndrome (Waylivra). These therapies support ongoing clinical activity and standardized safety management across rare disease populations.

By Route of Administration Analysis

The Intrathecal injection segment is likely to continue holding the lead in 2026, accounting for approximately 41.5% of the global ASO therapy market share, driven by strong clinical validation for spinal muscular atrophy and other CNS disorders where direct CNS delivery is required. This segment reflects the continued need for targeted delivery to the central nervous system despite procedural complexity. The Subcutaneous injection segment is the second-largest, supported by patient preference for home self-administration and growing use in metabolic disorders (Waylivra, Tegsedi). The Intravenous injection segment is also growing, driven by hospital-based dosing for certain neuromuscular and oncology indications.

By Drug Type Analysis

The Spinraza segment is expected to dominate with around 38.5% market share in 2026, driven by broad global reimbursement, established neurologist familiarity, and continued expansion into newborn screening programs. Spinraza supports long-term patient management plans because of its well-characterized intrathecal dosing regimen and real-world durability data. The Emerging ASO Therapies segment is the fastest-growing, driven by pipeline candidates in Huntington's disease, Angelman syndrome, ALS, and cardiovascular indications. This segment is seeing strong growth with increasing venture capital investment and orphan drug designations.

By Technology Platform Analysis

The Phosphorothioate ASOs segment is the largest technology platform in 2026, accounting for 35.8% share, driven by their widespread use in approved drugs (Spinraza, Tegsedi, Waylivra) and favorable nuclease resistance. These modifications provide backbone stability and support systemic and CNS delivery. The 2'-MOE ASOs segment is the second-largest, supported by enhanced binding affinity and reduced immunogenicity, while LNA ASOs are the fastest-growing, driven by ultra-high affinity for difficult targets and gapmer designs for gene silencing.

By End User Analysis

The Hospitals & Specialized Clinics segment is the largest end user in 2026, accounting for 48.5% share, driven by the need for specialized administration (e.g., intrathecal infusion), patient monitoring for immunogenicity, and multidisciplinary rare disease care. Neuromuscular centers and specialized metabolic clinics are adopting ASO therapies for direct patient management. Pharmaceutical & Biotechnology Companies is the second-largest and fastest-growing segment, supported by robust ASO pipeline development, in-house and CDMO manufacturing, and preclinical to clinical translation of novel chemical modalities.

The Global Antisense Oligonucleotide Therapy Market Report is segmented on the basis of the following:

By Therapeutic Area

- Neurological & Neuromuscular Disorders

- Cardiovascular & Metabolic Disorders

- Oncology

- Ocular Disorders

- Genetic & Rare Metabolic Disorders

- Infectious Diseases

- Others

By Route of Administration

- Subcutaneous Injection

- Intrathecal Injection

- Intravenous Injection

- Intravitreal Injection

- Others

By Drug Type

- Spinraza

- Exondys 51

- Tegsedi

- Waylivra

- Emerging ASO Therapies

By Technology Platform

- Phosphorothioate ASOs

- PMO ASOs

- 2'-MOE ASOs

- LNA ASOs

- Gapmers

- Others

By End User

- Hospitals & Specialized Clinics

- Pharmaceutical & Biotechnology Companies

- Academic & Research Institutes

- Others

Regional Analysis

Leading Region in the Antisense Oligonucleotide Therapy Market

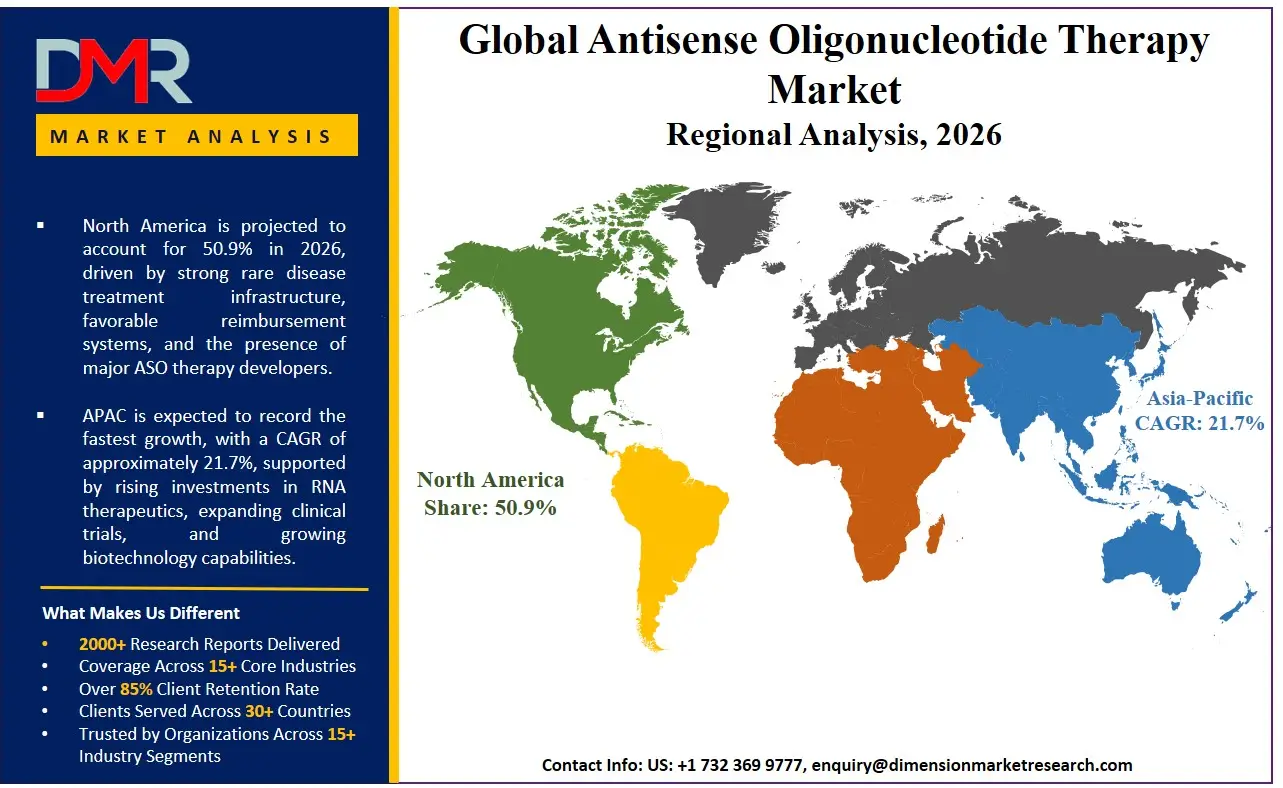

It is projected that North America will take the lead in the global ASO therapy market, covering a market share of about 50.9% in the year 2026. The region's dominance is driven by the presence of the world's largest biopharmaceutical R&D clusters (Boston, San Francisco), rapid clinical adoption of intrathecally administered ASOs and subcutaneous metabolic ASOs, strong genomic medicine modernization spending funded by private and public sources, higher average treatment volumes compared to other regions, a mature supply chain for advanced oligonucleotide manufacturing, and the presence of major ASO drug developers. The widespread adoption of advanced ASO screening and automation for rare disease treatment, neuromuscular care, and long-term patient management further strengthens North America's leading position. Additionally, ongoing investments in newborn screening programs and cross-system interoperability under the FDA's real-world evidence frameworks further reinforce the region's technology leadership.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Fastest-Growing Region in the Antisense Oligonucleotide Therapy Market

Asia-Pacific is the fastest-growing region, supported by strong genomic medicine infrastructure goals in China, Japan, and India, increasing rare disease diagnosis awareness efforts, rising investments in local ASO manufacturing capabilities, and growing adoption of cost-effective generic ASO alternatives. The region benefits from well-established hospital systems for rare disease management, increasing business activity in CROs/CDMOs, and alignment with national genomic protection roadmaps. Countries across the region are actively setting up specialized neuromuscular centers and ASO therapy access programs to improve treatment efficiency and strengthen genetic privacy infrastructure. Growing focus on ASO research and structured rare disease registries further speeds up market expansion. Moreover, increasing government support and corporate rare disease commitments are expected to keep growth momentum high.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The ASO therapy market is highly competitive, with new ideas and strategic partnerships shaping the competitive environment. To gain an advantage, companies and developers are focused on developing better ASO chemical modification platforms (such as stereopure ASOs, peptide-conjugated ASOs, and ligand-conjugated delivery systems), smart clinical analytics, and centralized pharmacovigilance monitoring. There are high barriers to entering the market due to the large amount of investment needed for regulatory approval, specialized oligonucleotide chemistry expertise, and the need for mature GMP manufacturing systems and rule-following.

Strategic approaches to increase market presence include partnerships with rare disease patient registries and academic medical centers, mergers between ASO platform providers and CDMOs, and long-term supply contracts with hospital systems and government institutions. Additionally, research and development in ASO delivery technologies (e.g., GalNAc conjugates) and flexible solid-phase synthesis designs are important for staying competitive and meeting the changing needs of the ASO therapy community.

Some of the prominent players in the Global Antisense Oligonucleotide Therapy Market are:

- Ionis Pharmaceuticals, Inc.

- Biogen Inc.

- Sarepta Therapeutics, Inc.

- Alnylam Pharmaceuticals, Inc.

- Wave Life Sciences Ltd.

- F. Hoffmann-La Roche Ltd

- Novartis AG

- Pfizer Inc.

- Arrowhead Pharmaceuticals, Inc.

- Avidity Biosciences, Inc.

- Stoke Therapeutics, Inc.

- ProQR Therapeutics N.V.

- Regulus Therapeutics Inc.

- Silence Therapeutics plc

- Bio-Path Holdings, Inc.

- Dyne Therapeutics, Inc.

- Astellas Pharma Inc.

- Jazz Pharmaceuticals plc

- Nippon Shinyaku Co., Ltd.

- Nitto Denko Corporation

- Other Key Players

Recent Developments

- March 2026: Biogen Inc. received U.S. FDA approval for the higher-dose regimen of Spinraza for spinal muscular atrophy (SMA), strengthening its position in the antisense oligonucleotide therapy market.

- March 2026: Ionis Pharmaceuticals, Inc. announced that the FDA accepted the New Drug Application (NDA) for zilganersen for Alexander disease under Priority Review, with a PDUFA date set for September 22, 2026.

- January 2026: Ionis Pharmaceuticals, Inc. and partner GlaxoSmithKline plc reported positive Phase 3 results for bepirovirsen, an investigational antisense oligonucleotide therapy for chronic hepatitis B, with global regulatory filings planned in 2026.

- June 2025: Biogen Inc. presented new clinical data from the DEVOTE and NURTURE studies demonstrating improved motor outcomes and long-term efficacy of Spinraza in spinal muscular atrophy patients.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 6.9 Bn |

| Forecast Value (2035) |

USD 31.4 Bn |

| CAGR (2026–2035) |

18.3% |

| The US Market Size (2026) |

USD 3.0 Bn |

| Historical Period |

2021 – 2025 |

| Forecast Period |

2027 – 2035 |

| Base Year |

2025 |

| Estimated Year |

2026 |

| Segments Covered |

By Therapeutic Area, By Route of Administration, By Drug Type, By Technology Platform, By End User |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Global Antisense Oligonucleotide Therapy Market?

▾ The Global Antisense Oligonucleotide Therapy Market size is estimated to have a value of USD 6.9 billion in 2026 and is expected to reach USD 31.4 billion by the end of 2035.

What is the CAGR of the Global Antisense Oligonucleotide Therapy Market from 2026 to 2035?

▾ The market is growing at a CAGR of 18.3% over the forecasted period.

What factors are driving the growth of the Global Antisense Oligonucleotide Therapy Market?

▾ The market is driven by advances in stereopure ASO synthesis and targeted RNA modulation, regulatory pressure to speed up orphan drug designation and reduce off-target toxicity mistakes, and increased government investment in national genomic medicine infrastructure.

What are the major trends in the Global Antisense Oligonucleotide Therapy Market?

▾ The key market trends include the adoption of real-time ASO immunogenicity tracking and AI-driven sequence design, along with a growing shift toward personalized ASO manufacturing and real-world evidence management systems.

Which region held the largest share of the Global Antisense Oligonucleotide Therapy Market in 2026?

▾ North America is expected to account for the largest market share in 2026, with a share of about 50.9%.

Which region is expected to grow the fastest in the Global Antisense Oligonucleotide Therapy Market?

▾ Asia Pacific is the fastest-growing region in the market during the forecast period.

Who are the key players in the Global Antisense Oligonucleotide Therapy Market?

▾ Some of the major key players in the Global Antisense Oligonucleotide Therapy Market are Biogen Inc., Sarepta Therapeutics, Inc., Ionis Pharmaceuticals, F. Hoffmann-La Roche Ltd, Novartis AG, and many others.

How is the Global Antisense Oligonucleotide Therapy Market segmented?

▾ The market is segmented by therapeutic area, route of administration, drug type, technology platform, and end user.