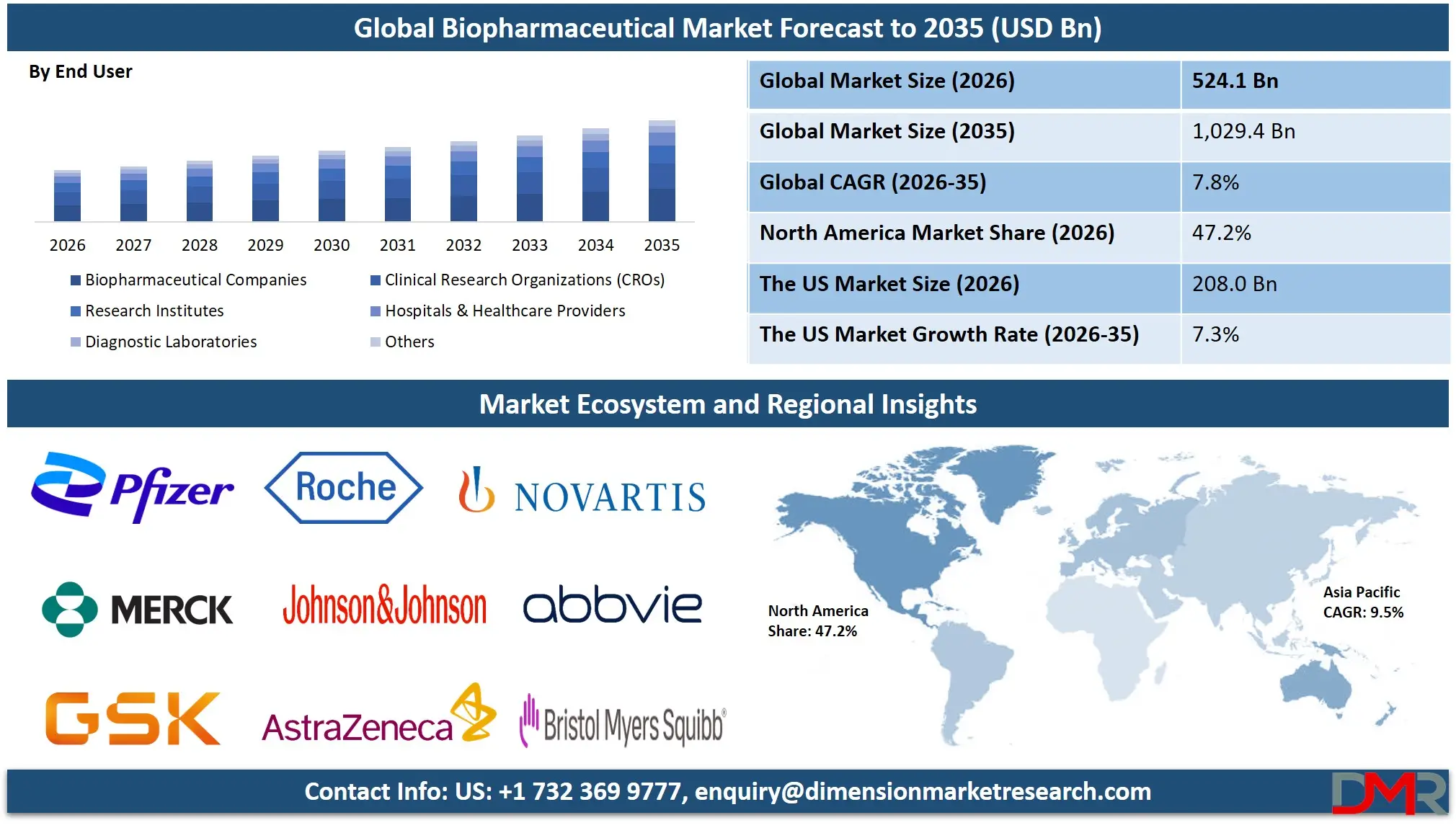

What is the Global Biopharmaceutical Market Size?

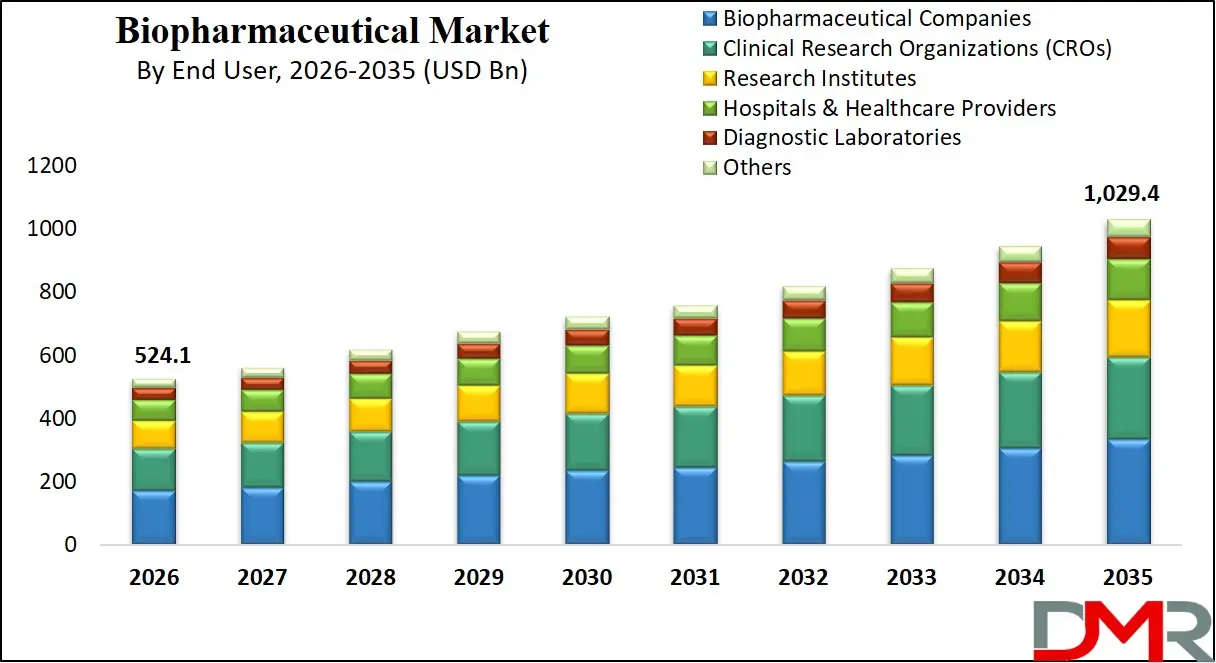

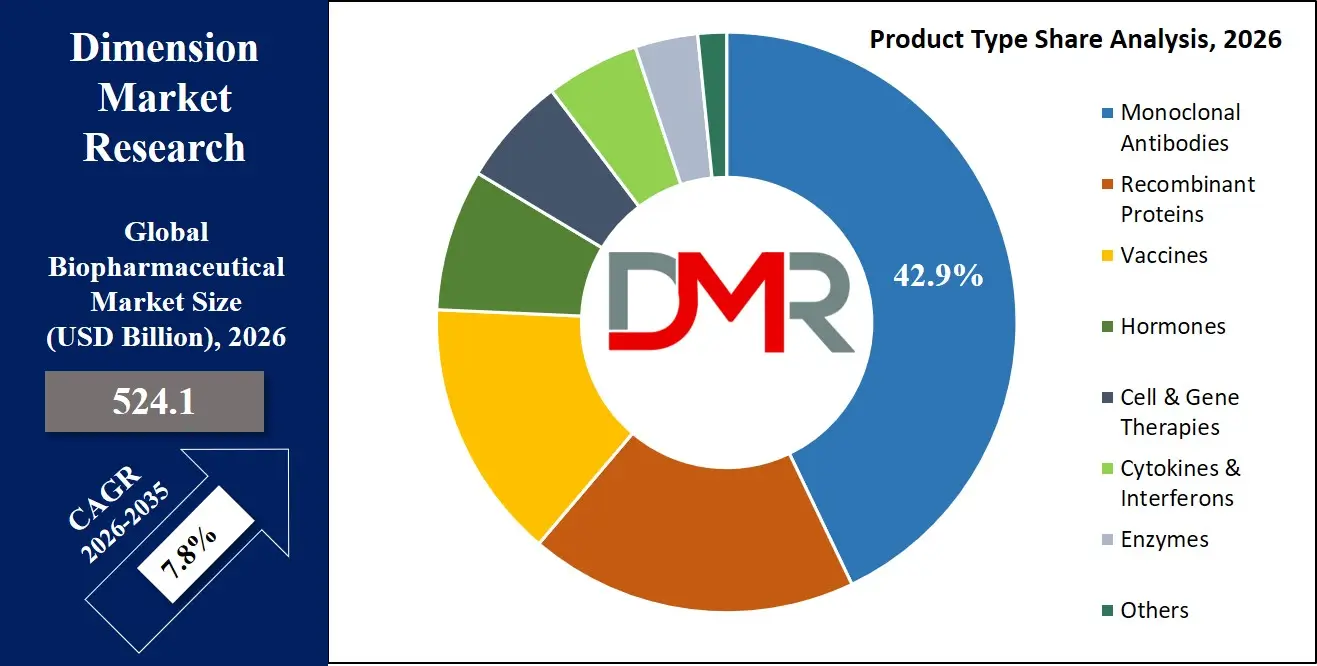

The Global Biopharmaceutical Market size is estimated at USD 524.1 billion in 2026 and is projected to reach USD 1,029.4 billion by 2035, exhibiting a CAGR of 7.8% during the forecast period, availability of advanced biologic pipelines, the use of biosimilars and integrated AI-based drug discovery platforms in precision medicine.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The biopharmaceutical market has grown exponentially due to the adoption of machine learning technologies for protein engineering and antibody design and optimization, regulatory requirements that reduce the attrition rates of clinical trials and accelerate the development of new biologics, and increased funding for automated drug discovery programs by private entities and governments. Other factors include the emergence of real-time bioreactor monitoring, predictive models of drug efficacy, cell line automation, high-throughput screening and other advances in data integration systems supporting biopharmaceutical R&D. Laboratory automation, predictive modeling and artificial intelligence-based drug discovery platforms have driven adoption and national strategies for bio economies have facilitated sustainable biologic production.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

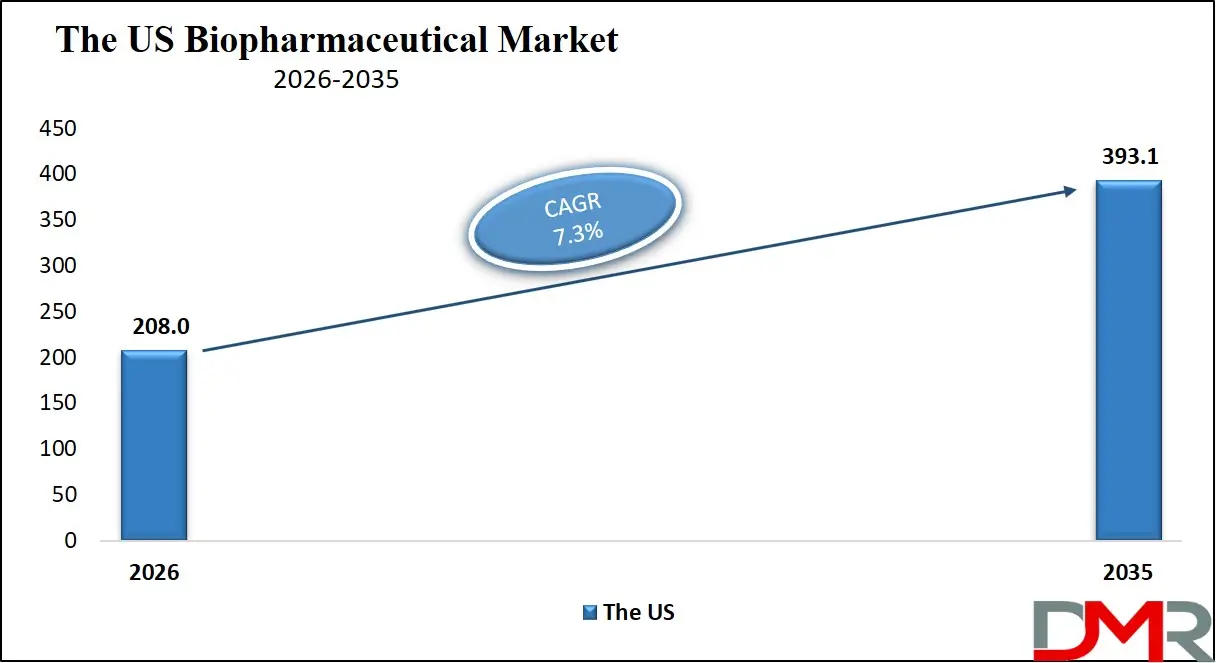

The US Biopharmaceutical Market

The US Biopharmaceutical Market is estimated to grow to USD 208.0 billion in 2026 with a compound annual growth rate of 7.3% during the forecast period.

The US market is defined by the existence of significant federal funding schemes like the Advanced Research Projects Agency for Health (ARPA-H), the National Institute for Innovation in Manufacturing Biopharmaceuticals (NIIMBL) centers, and the FDA's AI/ML-enabled drug development pathway for gene therapies and vaccines, all of which will help the necessity of AI-driven protein engineering, real-time bioprocess monitoring of automated bioreactors, and predictive drug development software. Automated biopharmaceutical manufacturing systems continue to be rapidly adopted in the region, and the US needs highly developed interoperability frameworks, integration of real-world evidence using electronic health records, and verifiable AI assurance for drug development. Also, service providers are being pressured by initiatives like the 21st Century Cures Act and national AI in biomanufacturing strategies to create dedicated integration and deployment services to guarantee data interoperability, security, and compliance across pharma R&D departments and academic research centers.

Europe Biopharmaceutical Market

The Europe Biopharmaceutical Market is estimated to be valued at USD 131.6 billion in 2026, witnessing growth at a CAGR of 6.6%, during the forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The biopharmaceutical market is mature in Europe, with strong influence from regulatory specifications and regional policies including the EU Pharmaceutical Strategy, the European Biomanufacturing Pilot Lines, and national digital health programs (e.g., France's Genomic Medicine Plan and Germany's Bioökonomie 2030 strategy). Another area that countries are working towards is smart biopharmaceutical modularization to align research and production workload demands and interoperability of cross-border clinical trial data supply chains. The market is driven by advanced technologies, such as real-time protein design engines and high-reliability efficacy prediction algorithms with embedded predictive models for novel drug candidates. Adoption is facilitated by the use of public-private partnerships and harmonization of biopharmaceutical manufacturing standards. Technologies like real-time computational workload balancing and secure data sharing are commonly practiced in research-centric programs, and Europe is a frontrunner in the digital transformation of safe and efficient biologic drug development.

Japan Biopharmaceutical Market

The Japan Biopharmaceutical Market is projected to be valued at USD 33.5 billion in 2026, progressing at a CAGR of 7.1%, during the period spanning from 2026 to 2035.

Japan boasts a mature biopharmaceutical market supported by high-performance automated cell culture systems, diagnostic fermentation integration technology, and a wide network of robotic drug discovery innovations. Automation, precision, and process integrity are priorities in the country, achieved by predictive pharmacokinetic models and intelligent process management systems for biologic manufacturing. Growth is stimulated by government actions under the Society 5.0 initiative and constant investment in digital biomanufacturing infrastructure. The high level of biopharmaceutical research and development activities, industrial protein production for enzymes and monoclonal antibodies, and automation processes demand efficient artificial intelligence for instantaneous decision-making based on data analysis. Challenges such as expensive validation for novel biopharmaceutical automation frameworks and legacy manufacturing processes are present; however, there is great potential in exporting the advanced technology in the biopharmaceutical industry to Asian and Pacific markets.

Key Takeaways

- Market Size & Forecast: The Global Biopharmaceutical Market is estimated to be valued at USD 524.1 billion in 2026 and is expected to grow to USD 1,029.4 billion by 2035.

- Growth Rate & Outlook: The market is expected to witness growth at a compound annual growth rate of 7.8% in the forecast period.

- Primary Growth Drivers: Some of the major factors driving growth are advances in machine-learning based protein engineering for drugs, regulatory requirements for faster clinical development and reduced failure rates, and clinical/industrial deployment of intelligent drug discovery platforms.

- Key Market Trends: The use of predictive clinical outcome monitoring, real-time manufacturing optimization, and the transition to cloud-based drug development data management systems are some of the primary market trends.

- By Product Type: The Monoclonal Antibodies segment is anticipated to hold the majority share of the biopharmaceutical market in 2026.

- By Therapeutic Application: The Oncology segment is expected to occupy the largest revenue share in 2026.

- By Drug Type: Proprietary Biologics are expected to capture the largest revenue share in 2026.

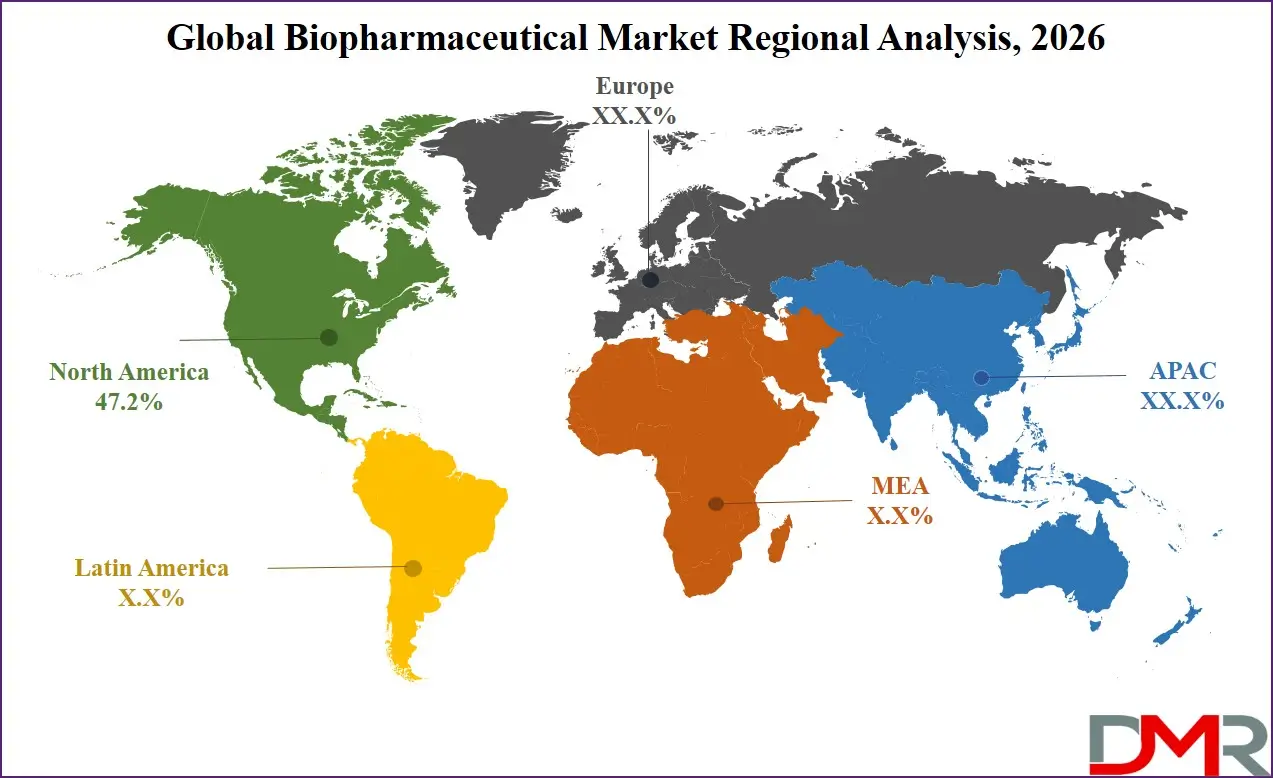

- Regional Leadership: North America is predicted to dominate the market with an estimated 47.2% share in 2026, driven by high biotech R&D spend and biopharmaceutical technology investment.

What are Biopharmaceuticals?

Biopharmaceuticals (or biologics) are biomedical products derived out of living organisms or cells by the use of biotechnological techniques. They are monoclonal antibodies, recombinant proteins (insulin and erythropoietin), vaccines, cell and gene therapies, hormones, cytokines and other multifaceted biologic molecules. Biopharmaceuticals are not chemically synthesized as traditional small-molecule drugs are, but are produced biologically, such as by genetic engineering, cell culture, and fermentation. Their application is in the treatment of a broad spectrum of diseases such as cancer, autoimmune, infectious, and rare genetic diseases. The high molecular complexity, target selectivity and the requirement of rigorous manufacturing and regulatory controls to guarantee safety and efficacy characterize biopharmaceuticals.

Use Cases

- Monoclonal Antibodies for Oncology: Biopharmaceutical firms are developing high-throughput screening strategies to identify the best antibody candidates in cancer immunotherapies, which require months rather than years to develop and would save a lot of money over conventional hybridoma screening.

- Recombinant Protein Development: Long-term cell culture and yield data, including cumulative productivity and impurity accumulation, are modeled to provide process adjustment recommendations to provide safe and continuous manufacturing operations of drugs, like insulin and erythropoietin.

- Bioreactor Monitoring & Control: Industrial manufacturing deployments employ machine learning and bioreactor analytics to perform real-time yield prediction, process anomaly detection, and automated feed adjustment with quantifiable accuracy.

- Population Health & Government Programs: More effective biopharmaceutical R&D assists in pandemic preparedness, developing therapeutics in rare disease models, and smart drug monitoring, enabling national bioeconomy adoption and aiding in the implementation of policies, including drug pricing reforms and biomanufacturing standards.

How AI Is Transforming the Global Biopharmaceutical Market?

Artificial intelligence is revolutionizing the biopharmaceutical field, allowing predictive modeling of drug candidate success likelihood, automatic detection of anomalies in cell culture data patterns, and optimization of protein design parameters in a disease-specific scenario. Bioreactor-generated telemetry and omics data can be processed using AI algorithms to identify any degradation or performance drift and optimize production outcomes at scale. This saves time, improves verifiability, and reduces costs compared to manual data analysis.

Moreover, AI enhances drug development assurance through adaptive computational event-based scheduling, anticipating workflow threats to design accuracy, and intelligent prioritization of manufacturing equipment health monitoring. It is also involved in reducing the cost of baseline testing and ongoing performance tracking, allowing biopharmaceutical IT operators to reduce the physical footprint of on-prem test campaigns and improve the reliability of drug development workloads and their financial returns.

Market Dynamics

Key Drivers of the Global Biopharmaceutical Market

Rapid developments in Machine Learning and Real-Time Bioprocess Inference

Fast adoption of AI-driven protein and process optimization, high-efficiency bio-processing data analysis, API-based interoperability with electronic lab notebooks (ELNs) and laboratory information management systems (LIMS), and real-time telemetry analytics of bioreactors are pushing the market. These technologies allow real-time monitoring of the performance of biopharmaceutical manufacturing, early detection of anomalies in the process, prediction of cell culture productivity rates, and ease of experimental validation. As a result, there is a high level of operational uptime and R&D efficiency and reduced costs of manual data analysis. The advancement in machine learning-based protein design, especially, is hastening the demand of intelligent automation of biopharmaceutical workflows, with more and more manufacturers turning to data-driven workflows optimization.

Growing Focus on Bioprocess Regulation and Sustainable Manufacturing

Governments and regulatory agencies are becoming more concerned about drug safety and quality, and have instituted biomanufacturing efficiency frameworks, including the EU Pharmaceutical Strategy and the Advanced Manufacturing Technologies framework to biologics and cell therapies at the FDA. These structures are driving demand for efficient biopharmaceutical automation capable of supporting real-time process monitoring and continuous learning. In parallel, global initiatives promoting manufacturing standardization and workforce development are encouraging the adoption of evidence-based drug development architecture. The increasing focus on transparency in biologic design and reduction in production failure rates is also enhancing the necessity of reliable and scalable biopharmaceutical automation in both public and private manufacturing systems.

Restraints in the Global Biopharmaceutical Market

High Expenses of Integration and Process Validation

Manufacturing platforms of bio-pharmaceuticals are costly and time consuming to adopt, involving intensive testing in the manufacturing environment, assertion of process logic credibility, and performance testing over a protracted time of new components. Regulatory restrictions and data privacy regulations (e.g., GDPR on patient data, trade secret restrictions) also increase the cost and complexity of deployment. These factors are entry barriers, increase deployment time, and increase the cost of capital outlay.

Limited Standardization Across Drug Development Data and Workflows

The industry still makes use of various automation systems, such as high-throughput screening based on robotics, process optimization based on AI, and quality control based on computer vision. However, the lack of standardized data interfaces beyond platforms like SiLA for lab automation and Allotrope for analytical data remains a key challenge. Biopharmaceutical R&D lacks universal plug-and-play standards compared to traditional manufacturing modules, making integration complex and limiting interoperability of data models across different R&D and production systems.

Growth Opportunities in the Global Biopharmaceutical Market

Expansion of Emerging Biopharmaceutical Programs

Developing biopharmaceutical markets such as Brazil, Indonesia, Nigeria, the UAE, and Vietnam are investing in digital bioeconomy infrastructure and advanced biologic manufacturing capabilities. These regions present strong growth potential due to increasing demand for automated protein development, bioreactor monitoring, and remote drug development consultation applications. With limited legacy manufacturing infrastructure, they provide opportunities for the deployment of modern biopharmaceutical automation optimized for R&D and manufacturing environments.

Rising Demand for Cloud-Based Drug Development Platforms

The increased requirement for advanced biopharmaceutical automation is being generated by the growth of remote R&D collaboration, distributed manufacturing, and real-time process control applications. These technologies play a vital role in virtual drug development platforms, remote production facilities, and biotech innovation hubs. With the rising importance of real-time process monitoring as a major production concern, cloud-based analytics capabilities are likely to be fundamental to future biopharmaceutical and biotech IT infrastructure.

Global Biopharmaceutical Market Trends

Predictive Clinical Outcome Monitoring and Computational Analytics

Biopharmaceutical manufacturing platforms are being monitored for process logic anomalies in real-time, with predictive algorithms identifying potential deviations. The use of digital twin models of cell culture performance and machine learning algorithms is enhancing production workflow scheduling, system lifespan, and deployment reliability. This shift is transforming drug development management from manual data review to fully automated, continuously optimized system monitoring.

Cloud-Based Data Management and Fleet Management Systems

Cloud computing and digital twin technologies are taking centre stage in the operations of biopharmaceutical manufacturing networks. These platforms enable real-time storage and analysis of drug development data, centralized fleet management of automated work cells, and remote monitoring of manufacturing equipment health. Cloud-based systems enhance transparency, lower on-prem infrastructure expenses, and provide quicker responses to workflow changes across R&D sites, as experienced by operators of large biopharmaceutical networks.

Research Scope and Analysis

The biopharmaceutical market is led by monoclonal antibodies and proprietary biologics, with oncology as the primary application. Strong growth is driven by cell and gene therapies, outsourcing trends, digital distribution channels, and increasing adoption across hospitals and advanced healthcare providers.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

By Product Type Analysis

The Monoclonal Antibodies segment is expected to remain the largest in 2026, accounting for about 42.9% of the global biopharmaceutical market, driven by its dominant use in oncology, immunology, and personalized medicine, as well as seamless integration into R&D workflows where real-time efficacy data and manufacturing maturity are essential. Meanwhile, the Cell & Gene Therapies segment is witnessing strong growth, driven by rising demand for personalized cancer treatments, rare disease therapies, and ex-vivo gene editing in R&D and clinical settings where real-time patient data capture and treatment reproducibility are critical. Adoption is further supported by workflow optimization, real-time efficiency improvements, and modular configurations for improved treatment flexibility.

By Therapeutic Application Analysis

The Oncology segment is expected to account for 38.5% share in 2026, as biopharmaceuticals heavily rely on checkpoint inhibitors, antibody-drug conjugates, and CAR-T cell therapies. The segment is further supported by increasing deployment of targeted therapies, combination regimens, and integrated biomarker platforms that enhance treatment outcomes and operational efficiency across drug development applications. It is also among the fastest-growing segments, driven by rapid adoption of precision oncology and scalable immunotherapy infrastructure.

By Drug Type Analysis

The Proprietary Biologics segment is expected to dominate with around 76.8% market share in 2026, driven by the critical need for novel, patent-protected therapies for cancer, autoimmune diseases, and rare disorders. Biopharmaceutical companies prioritize proprietary drug development due to higher pricing power and longer market exclusivity. The Biosimilars segment, while smaller, is witnessing strong growth, driven by healthcare cost containment pressures and expiry of biologic patents, particularly in Europe and Asia-Pacific.

By Drug Development Type Analysis

The In-house segment represents the largest development model in 2026, accounting for 62.4% share, driven by large pharma companies maintaining internal R&D capabilities for biologics discovery and process development. Outsourced development is the fastest-growing area, as smaller biotech firms and virtual drug developers increasingly rely on contract development and manufacturing organizations (CDMOs) for cell line development, process scale-up, and clinical manufacturing.

By Distribution Channel Analysis

Hospital Pharmacies represent the largest distribution channel in 2026, accounting for 54.3% share, driven by the specialized storage and administration requirements of biologic drugs, particularly for oncology and autoimmune therapies administered in clinical settings. Retail Pharmacies form the second-largest channel, while Online Pharmacies are the fastest-growing, supported by increasing adoption of digital health platforms and home delivery for chronic disease biologics such as insulin and self-administered monoclonal antibodies.

By End User Analysis

Biopharmaceutical Companies represent the largest end-user in 2026, accounting for 67.2% share, driven by complex R&D environments requiring real-time protein design and process optimization for biologics, vaccines, and gene therapies. Research Institutes form the second-largest segment, utilizing biopharmaceutical tools for fundamental drug discovery research. The fastest-growing area is Hospitals & Healthcare Providers, adopting advanced biologics for patient care and personalized treatment protocols. CROs and Diagnostic Laboratories are emerging segments supporting clinical trials and companion diagnostic development.

The Global Biopharmaceutical Market Report is segmented based on the following:

By Product Type

- Monoclonal Antibodies

- Recombinant Proteins

- Insulin

- Erythropoietin

- Growth & Coagulation Factors

- Others

- Vaccines

- Hormones

- Cytokines & Interferons

- Enzymes

- Cell & Gene Therapies

- Others

By Therapeutic Application

- Oncology

- Immunology & Autoimmune Diseases

- Infectious Diseases

- Metabolic Disorders

- Cardiovascular Diseases

- Neurological Disorders

- Blood Disorders

- Hormonal Disorders

- Others

By Drug Type

- Proprietary Biologics

- Biosimilars

By Drug Development Type

By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

By End User

- Biopharmaceutical Companies

- Clinical Research Organizations (CROs)

- Research Institutes

- Hospitals & Healthcare Providers

- Diagnostic Laboratories

- Others

Regional Analysis

Leading Region in the Biopharmaceutical Market

It is projected that North America will take the lead in the global biopharmaceutical market, covering a market share of about 47.2% in the year 2026. The region's dominance is driven by strong biotech R&D spending (US-based ARPA-H and NIIMBL programs), high drug prices relative to other regions, a mature healthcare IT supply chain for advanced interoperability and high-speed data exchange, and the presence of key biopharmaceutical companies and research labs. The widespread adoption of advanced machine learning and robotics-based drug discovery for oncology, immunology, and rare diseases further strengthens North America's leading position. Additionally, continuous investments in AI-enabled process monitoring and interoperability capabilities further reinforce regional technological leadership.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Fastest-Growing Region in the Biopharmaceutical Market

Asia-Pacific is the fastest-growing region, supported by strong biopharmaceutical deployment targets (China, India, Japan), increasing drug self-sufficiency initiatives, rising investments in domestic biologic manufacturing capabilities, and growing adoption of automated protein development systems. The region benefits from well-established generic drug manufacturing capacity, increasing commercial participation, and alignment with national bioeconomy roadmaps. Countries across the region are actively deploying biopharmaceutical infrastructure to enhance R&D productivity-per-dollar and strengthen drug manufacturing capabilities. Growing emphasis on biopharmaceutical R&D and structured process development further accelerates market expansion. Moreover, increasing government support and commercial biotech commitments are expected to sustain high growth momentum.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The biopharmaceutical market is highly competitive, with innovation and strategic alliances shaping the competitive environment. In order to achieve a competitive advantage, companies are focused on the development of advanced biologic platforms (e.g., AI-based protein design, robotics for high-throughput screening, and machine learning for manufacturing optimization), AI-powered process monitoring, and digital twin-enabled drug development platforms. There are high barriers to entry due to capital-intensive validation infrastructure, specialized biologics expertise, and the need for mature software ecosystems and regulatory compliance.

Strategic approaches to increase market presence include partnerships with pharma companies and manufacturing centers, mergers between automation solution providers and system integrators, and long-term supply contracts with R&D labs and academic institutions. Moreover, research and development in interoperability frameworks and scalable manufacturing architectures are important factors in maintaining competitiveness and addressing the evolving needs of the biopharmaceutical community.

Some of the prominent players in the Global Biopharmaceutical Market are:

- Pfizer Inc.

- F. Hoffmann-La Roche Ltd

- Johnson & Johnson

- Novartis AG

- Merck & Co., Inc.

- AbbVie Inc.

- Sanofi S.A.

- GSK plc

- AstraZeneca PLC

- Bristol-Myers Squibb Company

- Eli Lilly and Company

- Amgen Inc.

- Gilead Sciences, Inc.

- Biogen Inc.

- Novo Nordisk A/S

- Takeda Pharmaceutical Company Limited

- Regeneron Pharmaceuticals, Inc.

- Vertex Pharmaceuticals Incorporated

- Alnylam Pharmaceuticals, Inc.

- UCB S.A.

- Other Key Players

Recent Developments

- March 2026: GSK plc announced the completion of its acquisition of RAPT Therapeutics, a clinical-stage biopharmaceutical company, strengthening its immunology and inflammation pipeline with the addition of ozureprubart, a long-acting anti-IgE monoclonal antibody for food allergies.

- January 2026: AstraZeneca PLC announced the acquisition of Modella AI, a Boston-based artificial intelligence company, to enhance oncology R&D through AI-driven biomarker discovery and clinical development.

- December 2025: Eli Lilly and Company received the U.S. regulatory approval for its oral weight-loss drug (orforglipron), marking a major advancement in the obesity therapeutics market and intensifying competition with Novo Nordisk.

- November 2025: Pfizer Inc. announced that shareholders approved its acquisition of Metsera, valued up to USD 10.0 billion, to strengthen its position in the rapidly growing obesity drug market, expanding its GLP-1 and metabolic disease pipeline.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 524.1 Bn |

| Forecast Value (2035) |

USD 1,029.4 Bn |

| CAGR (2026–2035) |

7.8% |

| The US Market Size (2026) |

USD 208.0 Bn |

| Historical Period |

2021 – 2025 |

| Forecast Period |

2027 – 2035 |

| Base Year |

2025 |

| Estimated Year |

2026 |

| Segments Covered |

By Product Type (Monoclonal Antibodies, Recombinant Proteins, Vaccines, Hormones, Cytokines & Interferons, Enzymes, Cell & Gene Therapies, Others), By Therapeutic Application (Oncology, Immunology & Autoimmune Diseases, Infectious Diseases, Metabolic Disorders, Cardiovascular Diseases, Neurological Disorders, Blood Disorders, Hormonal Disorders, Others), By Drug Type (Proprietary Biologics, Biosimilars), By Drug Development Type (In-house, Outsourced), By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies), and By End User (Biopharmaceutical Companies, Clinical Research Organizations (CROs), Research Institutes, Hospitals & Healthcare Providers, Diagnostic Laboratories, Others) |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

Frequently Asked Questions

How big is the Global Biopharmaceutical Market?

▾ The Global Biopharmaceutical Market size is estimated to have a value of USD 524.1 billion in 2026 and is expected to reach USD 1,029.4 billion by the end of 2035.

Which region held the largest share of the Global Biopharmaceutical Market in 2026?

▾ North America is expected to account for the largest market share in 2026, with a share of about 47.2%.

Who are the key players in the Global Biopharmaceutical Market?

▾ Some of the major key players in the Global Biopharmaceutical Market are F. Hoffmann-La Roche Ltd., AbbVie Inc., Johnson & Johnson, Merck & Co., Pfizer Inc., Novartis AG, Sanofi S.A., AstraZeneca PLC, and many others.

What is the CAGR of the Global Biopharmaceutical Market from 2026 to 2035?

▾ The market is growing at a CAGR of 7.8% over the forecasted period.

What factors are driving the growth of the Global Biopharmaceutical Market?

▾ The market is driven by advances in machine learning-based protein engineering, regulatory pressure to accelerate drug development and reduce production failure rates, and increasing government investment in national bioeconomy infrastructure.

What are the major trends in the Global Biopharmaceutical Market?

▾ The key market trends include the adoption of predictive clinical outcome monitoring and real-time manufacturing control, along with a growing shift toward cloud-based drug development platforms and data-enabled workflow management systems.

Which region is expected to grow the fastest in the Global Biopharmaceutical Market?

▾ Asia Pacific is the fastest-growing region in the market during the forecast period.

How is the Global Biopharmaceutical Market segmented?

▾ The market is segmented by product type, therapeutic application, drug type, drug development type, distribution channel, and end user.