Market Overview

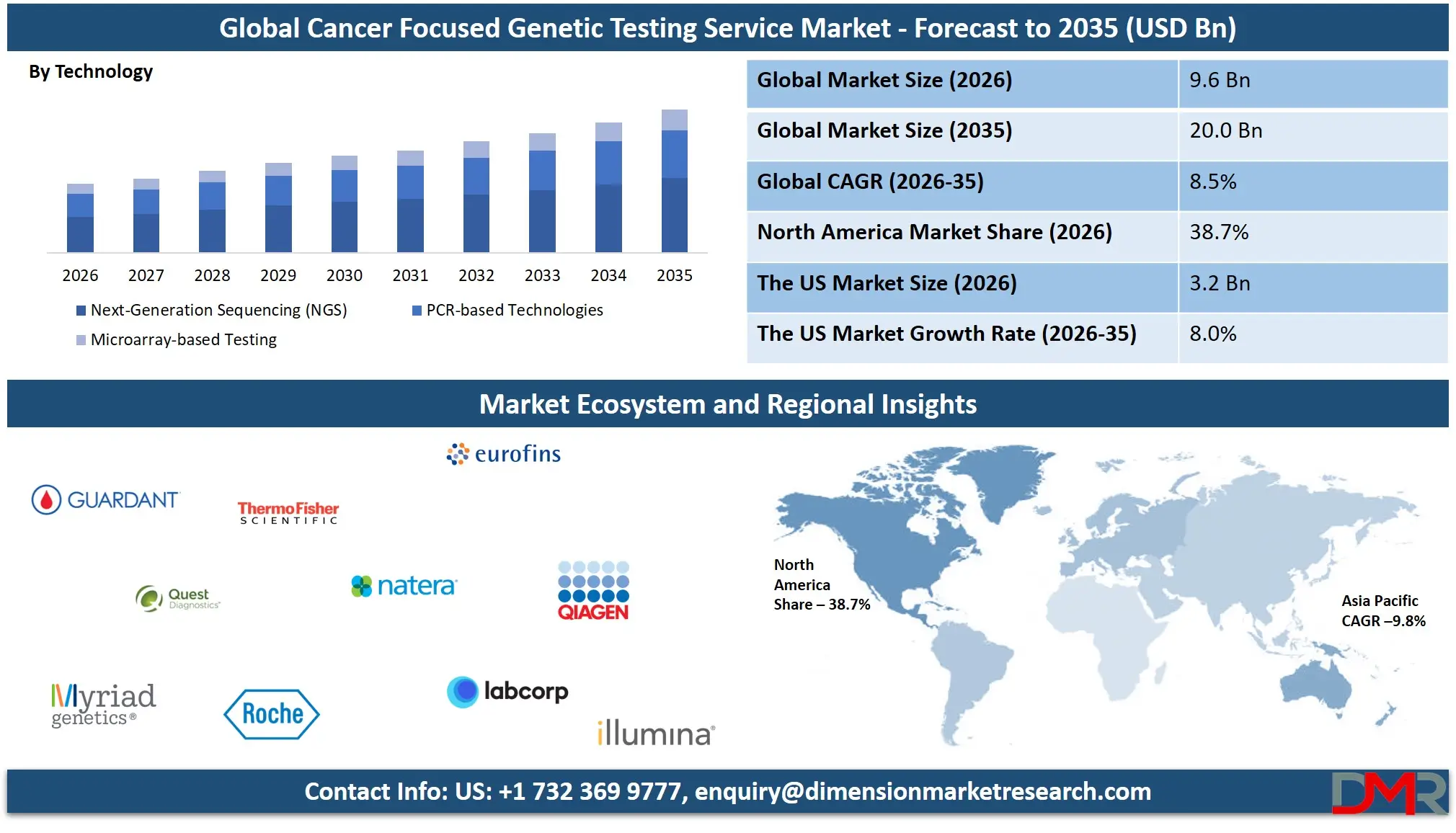

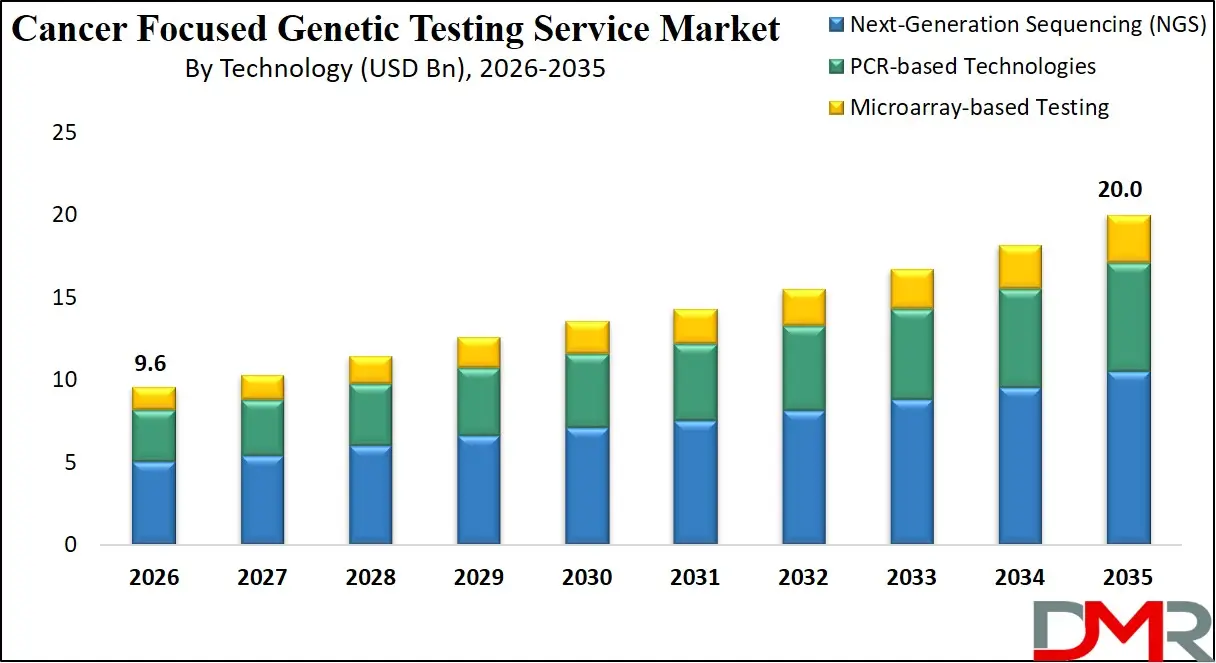

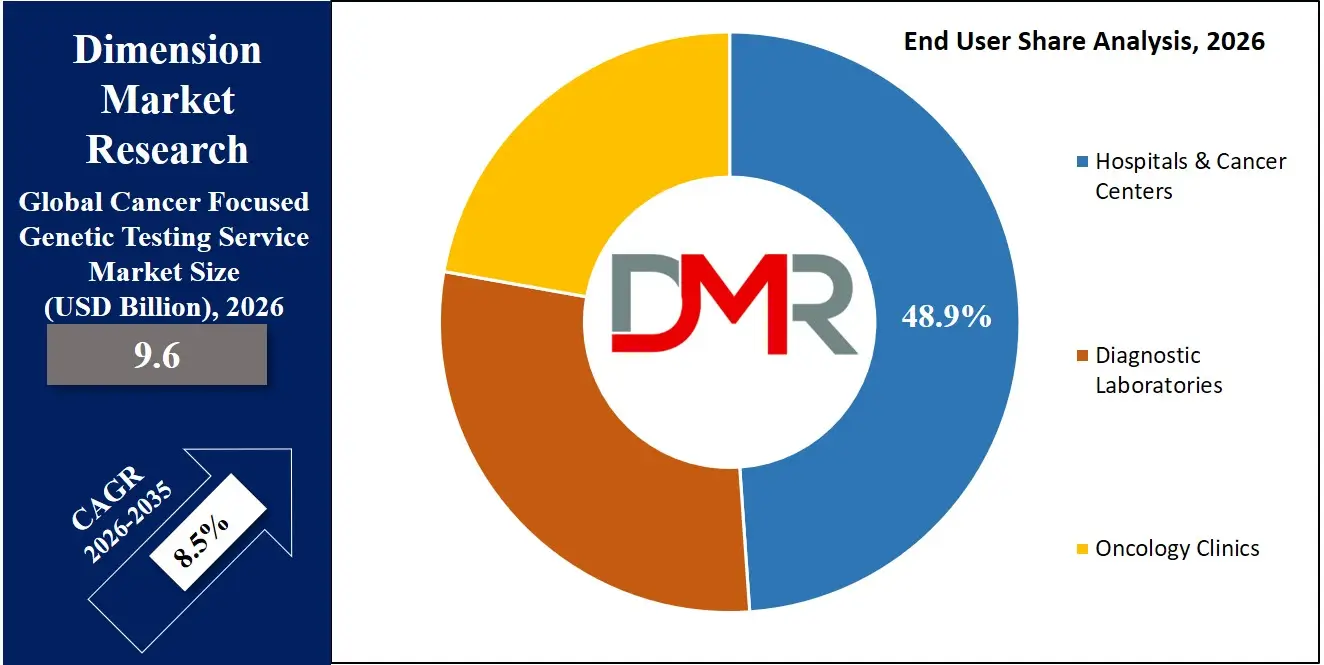

The Global Cancer Focused Genetic Testing Service Market size is projected to reach USD 9.6 billion in 2026 and grow at a compound annual growth rate of 8.5% to reach a value of USD 20.0 billion in 2035.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Cancer Focused Genetic Testing Service refers to specialized diagnostic and analytical services that examine an individual's DNA, RNA, or tumor-derived genetic material to identify mutations associated with cancer risk, progression, prognosis, and therapeutic response. These services include germline and somatic testing, companion diagnostics, gene expression profiling, minimal residual disease detection, and liquid biopsy analyses. Leveraging advanced technologies such as next-generation sequencing (NGS), PCR-based platforms, and microarrays, these services enable precision oncology by tailoring prevention and treatment strategies to a patient's molecular profile.

Within the broader healthcare and life sciences ecosystem, Cancer Focused Genetic Testing Service plays a critical role in personalized medicine, early detection, and targeted therapy selection. The field is evolving alongside breakthroughs in genomics, bioinformatics, and biomarker discovery. Growing integration of multi-omics approaches and AI-driven interpretation tools is transforming laboratory workflows and enabling faster, more accurate results.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Strong demand for precision oncology, rising cancer prevalence, and increasing awareness of hereditary cancer syndromes are accelerating transformation. Regulatory approvals for companion diagnostics, expanded reimbursement frameworks, and the shift toward minimally invasive liquid biopsies mark significant maturation milestones, positioning these services as central pillars of modern oncology care.

The US Cancer Focused Genetic Testing Service Market

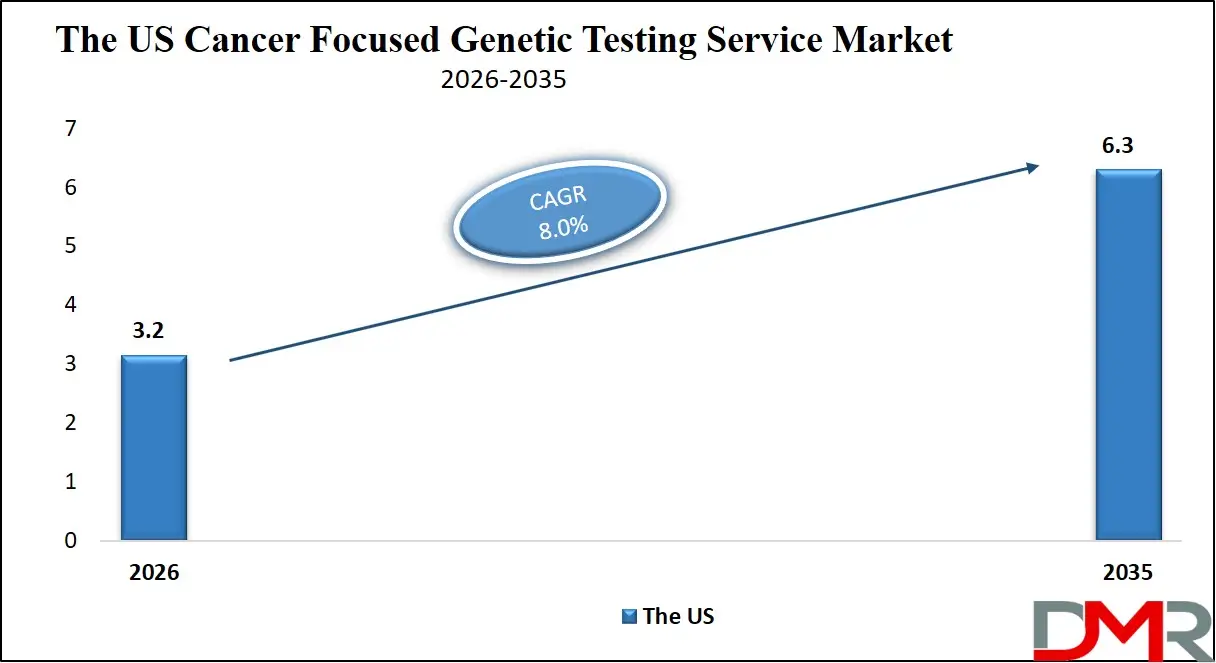

The US Cancer Focused Genetic Testing Service Market size is projected to reach USD 3.2 billion in 2026 at a compound annual growth rate of 8.0% over its forecast period.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

The US represents a highly advanced and innovation-driven landscape for Cancer Focused Genetic Testing Service. Growth is influenced by strong R&D investments, widespread adoption of NGS platforms, and integration of testing into clinical oncology pathways. Federal initiatives such as those led by the National Cancer Institute and precision medicine programs encourage genomic data utilization in cancer care. Favorable reimbursement policies for companion diagnostics and liquid biopsy testing further promote adoption. Additionally, collaboration between academic cancer centers, biotechnology firms, and diagnostic laboratories enhances market penetration, while regulatory oversight by the US Food and Drug Administration ensures quality and clinical validity standards.

Europe Cancer Focused Genetic Testing Service Market

Europe Cancer Focused Genetic Testing Service Market size is projected to reach USD 2.4 billion in 2026 at a compound annual growth rate of 8.1% over its forecast period.

Europe demonstrates steady expansion, supported by robust healthcare infrastructure and coordinated genomic initiatives. Regional strategies aligned with the European Commission and Europe's Beating Cancer Plan emphasize early detection and personalized treatment. Countries such as Germany, France, and the UK are integrating genomic profiling into public oncology programs. Data protection frameworks under GDPR influence laboratory operations, ensuring secure handling of genetic information. Cross-border collaborations and publicly funded genomic sequencing projects are strengthening capabilities. Adoption is particularly strong in breast and colorectal cancer testing, while reimbursement harmonization across member states remains a gradual but progressing effort.

Japan Cancer Focused Genetic Testing Service Market

Japan Cancer Focused Genetic Testing Service Market size is projected to reach USD 432 million in 2026 at a compound annual growth rate of 8.4% over its forecast period.

Japan's market is expanding through national precision medicine strategies and technological innovation. Government-backed genomic medicine initiatives led by the Ministry of Health, Labour and Welfare promote tumor profiling and hereditary cancer screening. Urbanization and advanced hospital networks enable integration of genomic diagnostics into routine oncology care. Japan's emphasis on early detection and aging population demographics contribute to growing demand. However, regulatory stringency and cost-containment measures pose challenges. Strategic partnerships between domestic diagnostic companies and global sequencing technology providers are accelerating adoption of NGS-based cancer panels across major metropolitan healthcare centers.

Cancer Focused Genetic Testing Service Market: Key Takeaways

- Market Growth: The Cancer Focused Genetic Testing Service Market size is expected to grow by USD 9.7 billion, at a CAGR of 8.5%, during the forecasted period of 2027 to 2035.

- By Technology: The NGS segment is anticipated to get the majority share of the Cancer Focused Genetic Testing Service market in 2026.

- By End User: The hospital & cancer centers segment is expected to get the largest revenue share in 2026 in the Cancer Focused Genetic Testing Service market.

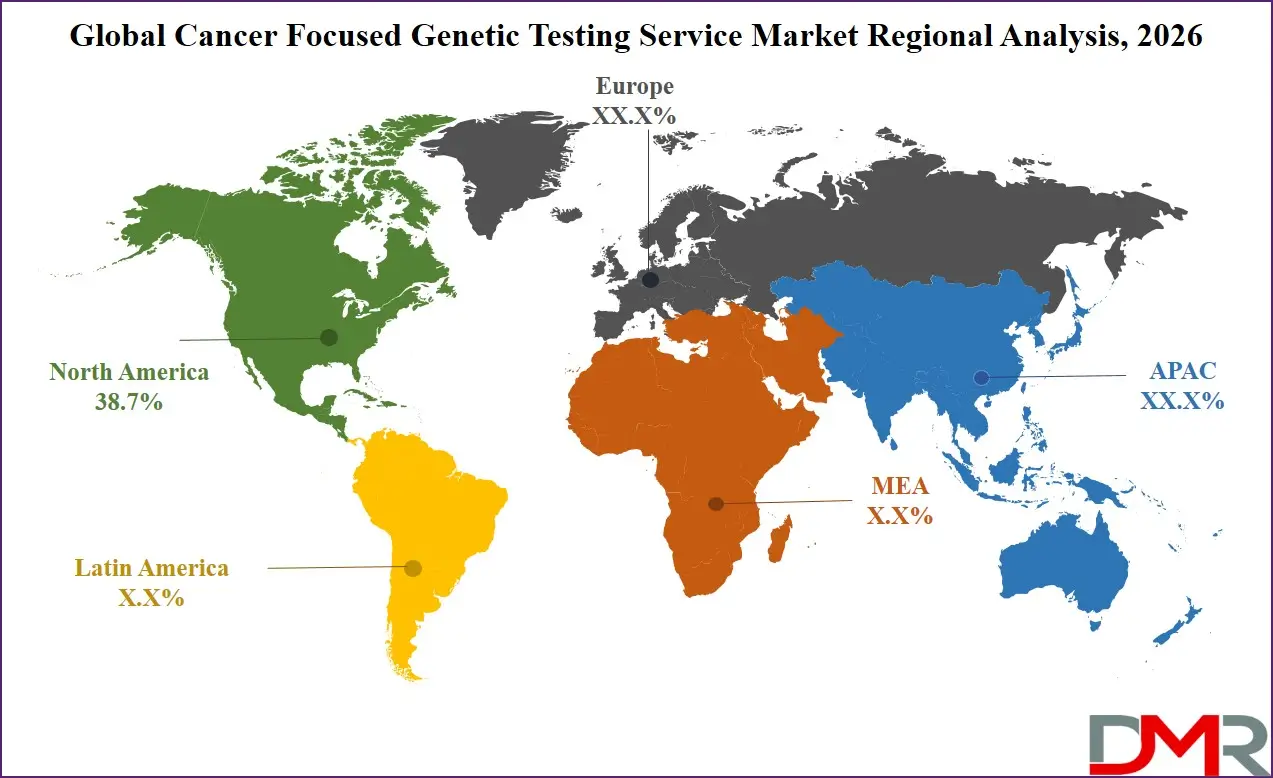

- Regional Insight: North America is expected to hold a 38.7% share of revenue in the global Cancer Focused Genetic Testing Service market in 2026.

- Use Cases: Some of the use cases of Cancer Focused Genetic Testing Service include targeted therapy selection, clinical trial enrollment, and more.

Cancer Focused Genetic Testing Service Market: Use Cases

- Hereditary Cancer Risk Assessment: Identification of BRCA1/2 and other inherited mutations to guide preventive interventions and family screening strategies.

- Targeted Therapy Selection: Tumor genomic profiling to match patients with specific targeted therapies or immunotherapies.

- Companion Diagnostics Development: Validation of biomarkers that determine patient eligibility for specific oncology drugs.

- Minimal Residual Disease Monitoring: Detection of trace cancer DNA post-treatment to assess recurrence risk.

- Liquid Biopsy Applications: Non-invasive blood-based tests for mutation detection and therapy monitoring.

- Clinical Trial Enrollment: Genomic stratification of patients for precision oncology research studies.

- Prognostic Evaluation: Gene expression profiling to predict disease progression and survival outcomes.

Stats & Facts

- National Cancer Institute reported in 2024 that approximately 2 million new cancer cases are projected in the United States.

- World Health Organization stated in 2024 that cancer accounts for nearly 10 million deaths annually worldwide.

- Centers for Disease Control and Prevention indicated in 2024 that cancer remains the second leading cause of death in the United States.

- European Commission noted in 2025 that cancer causes over 1.3 million deaths annually across the EU.

- National Institutes of Health confirmed in 2024 that BRCA1 and BRCA2 mutations account for about 5–10% of breast cancers.

- International Agency for Research on Cancer estimated in 2024 that global cancer incidence will rise by over 60% by 2040.

- U.S. Food and Drug Administration reported in 2025 that over 50 oncology drugs require companion diagnostic testing.

- Ministry of Health, Labour and Welfare Japan stated in 2024 that cancer represents the leading cause of mortality in Japan.

- OECD reported in 2024 that healthcare spending accounts for approximately 9% of GDP across member countries.

- National Health Service England highlighted in 2025 that genomic testing capacity has doubled since 2020 under national programs.

Market Dynamic

Driving Factors in the Cancer Focused Genetic Testing Service Market

Expansion of Precision Oncology

The rapid advancement of precision oncology is a primary force accelerating the Cancer Focused Genetic Testing Service landscape. Increasing understanding of tumor genomics and biomarker-driven therapies has transformed cancer treatment from a one-size-fits-all model to highly personalized care. Regulatory bodies such as the U.S. Food and Drug Administration continue approving targeted therapies that require companion diagnostics, directly increasing testing demand. Additionally, clinical guidelines from oncology associations now recommend genomic profiling for multiple cancer types. Growing physician awareness, improved sequencing accuracy, and decreasing per-sample testing costs further reinforce the integration of comprehensive genetic testing into standard oncology protocols globally.

Rising Adoption of Liquid Biopsy and MRD Testing

The emergence of liquid biopsy and minimal residual disease (MRD) testing is reshaping oncology diagnostics. Unlike traditional tissue biopsies, these minimally invasive approaches allow continuous disease monitoring using circulating tumor DNA. Advancements in digital PCR and high-sensitivity NGS platforms enhance early detection of relapse. Healthcare systems are investing in laboratory infrastructure to support routine MRD testing, particularly in hematologic malignancies and solid tumors. As patients and clinicians prioritize less invasive and faster diagnostic solutions, liquid biopsy adoption is accelerating, strengthening the role of advanced genetic testing services in both initial diagnosis and long-term surveillance.

Restraints in the Cancer Focused Genetic Testing Service Market

High Testing Costs and Reimbursement Variability

Despite technological progress, comprehensive genomic profiling remains costly, particularly multi-gene panels and whole genome sequencing. Pricing variability across regions and inconsistent reimbursement policies create barriers to widespread adoption. In emerging economies, limited insurance coverage and constrained healthcare budgets restrict patient access. Laboratories must also invest heavily in bioinformatics infrastructure, skilled personnel, and quality compliance systems. These financial and operational challenges can delay testing integration into routine oncology practice, particularly in community hospitals and smaller diagnostic centers with limited capital resources.

Data Privacy and Regulatory Complexity

Handling sensitive genetic data requires strict compliance with national and international regulations. Frameworks such as GDPR in Europe impose stringent data protection standards, influencing data storage and cross-border sharing. Regulatory pathways for new diagnostic approvals can be lengthy and complex, slowing innovation commercialization. Furthermore, ethical concerns regarding incidental findings and hereditary risk disclosure add complexity to clinical workflows. Variability in regulatory harmonization across countries creates operational uncertainty for multinational diagnostic providers, potentially slowing global expansion strategies.

Opportunities in the Cancer Focused Genetic Testing Service Market

Expansion in Emerging Markets

Emerging economies in Asia-Pacific, Latin America, and the Middle East present significant untapped potential. Rapid healthcare infrastructure development, rising cancer awareness, and government-led screening initiatives are driving demand for advanced diagnostics. As sequencing costs decline and local laboratory capacity increases, accessibility improves. Partnerships between global genomics firms and regional healthcare providers can accelerate technology transfer and training. The growing middle-class population and increasing health insurance penetration in these regions further enhance long-term growth prospects for genetic testing services.

Integration with Multi-Omics and AI Platforms

The convergence of genomics with proteomics, transcriptomics, and AI-powered analytics offers new avenues for differentiation. Advanced algorithms enable rapid interpretation of complex datasets, reducing turnaround times and improving diagnostic accuracy. Integration with electronic health records supports predictive modeling and treatment optimization. As healthcare systems embrace digital transformation, combining genetic testing with AI-driven decision-support platforms creates value-added service models that extend beyond basic mutation detection into comprehensive oncology intelligence solutions.

Trends in the Cancer Focused Genetic Testing Service Market

Shift Toward Comprehensive Genomic Profiling

There is a growing preference for broad-panel testing over single-gene assays. Comprehensive genomic profiling enables simultaneous analysis of multiple actionable mutations, supporting personalized therapy decisions. This shift is particularly evident in lung and colorectal cancers, where multiple biomarkers influence treatment selection. Laboratories are increasingly adopting high-throughput NGS platforms to meet rising demand, improving scalability and efficiency while reducing per-test costs.

Decentralization of Testing Infrastructure

Healthcare systems are moving from centralized reference laboratories to distributed genomic testing networks. Regional cancer centers are building in-house sequencing capabilities to reduce turnaround times. Cloud-based bioinformatics platforms facilitate remote data analysis and collaboration among clinicians. This decentralization enhances accessibility, especially in rural areas, while maintaining quality standards through standardized protocols and accreditation frameworks.

Impact of Artificial Intelligence in Cancer Focused Genetic Testing Service Market

- Variant Interpretation Automation: AI algorithms classify genetic variants faster, reducing manual review workload and improving diagnostic accuracy.

- Predictive Treatment Matching: Machine learning models correlate mutation profiles with therapy outcomes, guiding personalized drug selection.

- Workflow Optimization: AI-driven laboratory management systems streamline sequencing, reporting, and quality control processes.

- Early Recurrence Detection: Predictive analytics enhance sensitivity in MRD testing by identifying subtle ctDNA patterns.

- Drug Discovery Support: AI assists pharmaceutical companies in identifying novel genomic targets for oncology therapies.

- Population Risk Stratification: Advanced models analyze large genomic datasets to identify high-risk patient groups.

- Clinical Decision Support Integration: AI platforms integrate genomic results with patient records for real-time physician guidance.

- Cost Reduction: Automation and intelligent data processing lower operational expenses and turnaround times.

Research Scope and Analysis

By Test Type Analysis

Diagnostic Testing is projected to dominate the Cancer Focused Genetic Testing Service market, accounting for 46.8% share in 2026. This segment includes germline testing, somatic (tumor) testing, and companion diagnostics, which are widely integrated into oncology care pathways. The increasing number of targeted therapies approved by regulatory authorities and the expansion of biomarker-driven treatment protocols are reinforcing demand. Hospitals and cancer centers are routinely adopting multi-gene panels to guide therapeutic decisions, particularly in lung, breast, and colorectal cancers. The growing emphasis on precision oncology, combined with physician awareness and reimbursement support in developed markets, strengthens the segment's leadership. Companion diagnostics are especially influential, as many oncology drugs now require validated genetic tests prior to prescription, making diagnostic testing indispensable in modern cancer management.

Monitoring & Recurrence Testing is the fastest-growing segment, driven by rising adoption of minimal residual disease (MRD) testing and liquid biopsy solutions. Advances in circulating tumor DNA detection and digital PCR technologies have enabled earlier relapse identification with improved sensitivity. Oncology care models increasingly incorporate longitudinal monitoring to optimize treatment adjustments and improve survival outcomes. As healthcare systems prioritize non-invasive surveillance methods and personalized follow-up strategies, this segment is witnessing accelerated uptake across both solid tumors and hematologic malignancies.

By Technology Analysis

Next-Generation Sequencing (NGS) is expected to hold 52.4% market share in 2026, making it the leading technology segment. NGS supports targeted gene panels, whole exome sequencing (WES), and whole genome sequencing (WGS), offering comprehensive mutation profiling in a single workflow. Its scalability, declining sequencing costs, and high throughput capabilities position it as the preferred platform for comprehensive genomic profiling. The increasing complexity of cancer biomarkers and demand for multiplex testing further reinforce NGS adoption. Continuous improvements in bioinformatics pipelines and automation are also enhancing turnaround times and data accuracy, solidifying its dominance.

PCR-based technologies represent the fastest-growing technology segment due to advancements in real-time PCR and digital PCR. These methods offer high sensitivity, rapid processing, and cost efficiency, particularly in MRD testing and targeted mutation analysis. Their utility in smaller laboratories and resource-constrained settings contributes to broader accessibility. As digital PCR platforms evolve with enhanced precision, their application in liquid biopsy and early detection continues expanding.

By Cancer Type Analysis

Breast Cancer testing is anticipated to account for 24.6% market share in 2026, maintaining its leading position within the Cancer Focused Genetic Testing Service market. Strong awareness of hereditary mutations such as BRCA1 and BRCA2, along with established national screening initiatives, continues to drive consistent demand. Genetic profiling plays a vital role in both preventive risk assessment and therapeutic decision-making, particularly for HER2-positive and triple-negative subtypes. Clinical guidelines increasingly recommend germline and somatic testing at diagnosis, supporting broader adoption across hospitals and specialized oncology centers in both developed and emerging healthcare systems.

Lung Cancer testing represents the fastest-growing cancer type segment, supported by the rising identification of actionable mutations including EGFR, ALK, KRAS, and BRAF. The increasing prevalence of non-small cell lung cancer has intensified the need for comprehensive genomic profiling. Liquid biopsy adoption significantly enhances accessibility, particularly for patients unable to undergo invasive tissue sampling. The rapid expansion of targeted therapies and immunotherapy regimens requires routine biomarker testing prior to treatment initiation. As precision oncology protocols become standardized in clinical practice, genomic testing for lung cancer continues to expand at a robust pace globally.

By End User Analysis

Hospitals & Cancer Centers are projected to hold 48.9% share in 2026, dominating the end-user segment. These institutions integrate genetic testing directly into oncology workflows, enabling timely diagnosis, treatment selection, and monitoring. The presence of multidisciplinary tumor boards ensures collaborative interpretation of genomic results, improving patient outcomes. Many large academic and tertiary care centers operate in-house sequencing laboratories, reducing turnaround time and enhancing control over quality standards. Ongoing participation in precision medicine initiatives and oncology clinical trials further strengthens their leadership position within the overall service ecosystem.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Diagnostic Laboratories represent the fastest-growing end-user segment, driven by increasing outsourcing of complex genomic analyses by hospitals and oncology clinics. The expansion of centralized and regional genomic laboratories improves access to advanced testing technologies, particularly in semi-urban and emerging markets. Investments in automation, high-throughput sequencing systems, and cloud-based bioinformatics platforms are enhancing operational scalability and cost efficiency. Additionally, partnerships with pharmaceutical companies for companion diagnostic development provide recurring revenue streams. As demand for comprehensive genomic profiling grows, specialized diagnostic laboratories are rapidly strengthening their competitive position.

The Cancer Focused Genetic Testing Service Market Report is segmented on the basis of the following:

By Test Type

- Diagnostic Testing

- Germline Testing

- Somatic (Tumor) Testing

- Companion Diagnostics

- Predictive & Risk Assessment Testing

- Prognostic Testing

- Gene Expression Profiling

- Monitoring & Recurrence Testing

- Minimal Residual Disease (MRD) Testing

- Liquid Biopsy

By Technology

- Next-Generation Sequencing (NGS)

- Targeted Gene Panels

- Whole Exome Sequencing (WES)

- Whole Genome Sequencing (WGS)

- PCR-based Technologies

- Real-Time PCR

- Digital PCR

- Microarray-based Testing

By Cancer Type

- Breast Cancer

- Lung Cancer

- Colorectal Cancer

- Prostate Cancer

- Ovarian Cancer

- Hematologic Malignancies

- Other Solid Tumors

By End User

- Hospitals & Cancer Centers

- Diagnostic Laboratories

- Oncology Clinics

Regional Analysis

Leading Region in the Cancer Focused Genetic Testing Service Market

North America is anticipated to lead the global market with 38.7% share in 2026. The region benefits from advanced healthcare infrastructure, high adoption of next-generation sequencing technologies, and strong integration of precision oncology into routine clinical practice. Government-supported cancer research programs and favorable reimbursement policies encourage widespread genomic testing utilization. The concentration of biotechnology innovators, pharmaceutical companies, and academic cancer centers fosters rapid technological advancements. Clear regulatory pathways for companion diagnostics and targeted therapies further reinforce regional dominance, positioning North America as the primary revenue-generating hub.

ℹ

To learn more about this report –

Download Your Free Sample Report Here

Fastest Growing Region in the Cancer Focused Genetic Testing Service Market

Asia-Pacific is the fastest-growing region, fueled by expanding healthcare infrastructure, increasing cancer incidence, and rising public awareness of genetic screening. Governments across China, Japan, South Korea, and India are investing in national genomic medicine initiatives and expanding sequencing capabilities. Growing middle-class populations and broader health insurance coverage are improving patient access to advanced diagnostics. Local manufacturing of sequencing instruments and reagents is also reducing costs. Strategic collaborations between international genomics providers and regional healthcare systems are accelerating technology transfer and strengthening long-term market expansion.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The Cancer Focused Genetic Testing Service market is characterized by strong technological competition, continuous innovation, and strategic collaborations. Companies focus on expanding NGS capabilities, improving bioinformatics platforms, and developing proprietary biomarker panels to differentiate offerings. High entry barriers exist due to regulatory requirements, capital-intensive sequencing infrastructure, and the need for clinical validation studies. Market participants pursue partnerships with pharmaceutical firms to develop companion diagnostics, enhancing long-term revenue streams. Investments in AI-driven interpretation tools and automation are strengthening competitive positioning, while geographic expansion into emerging markets supports revenue diversification and sustained growth.

Some of the prominent players in the global Cancer Focused Genetic Testing Service are:

- Illumina, Inc.

- Thermo Fisher Scientific Inc.

- F. Hoffmann-La Roche Ltd.

- QIAGEN N.V.

- Myriad Genetics, Inc.

- Natera, Inc.

- Guardant Health, Inc.

- Laboratory Corporation of America Holdings

- Quest Diagnostics Incorporated

- Foundation Medicine, Inc.

- Eurofins Scientific SE

- Agilent Technologies, Inc.

- Exact Sciences Corporation

- Caris Life Sciences

- NeoGenomics Laboratories, Inc.

- Ambry Genetics Corporation

- Invitae Corporation

- BGI Genomics Co., Ltd.

- Genetron Health

- Tempus AI, Inc.

- Other Key Players

Recent Developments

- In February 2026, MiraDx has announced the U.S. commercial launch of PROSTOX™ Standard, a clinically validated genetic test designed to personalize radiation therapy for patients with localized prostate cancer. The test identifies individuals at higher risk of long-term urinary side effects following conventionally fractionated or moderately hypofractionated radiation therapy and complements the company's PROSTOX Ultra for stereotactic body radiation therapy, expanding access to toxicity risk assessment in external beam radiation therapy.

- In May 2025, Metropolis Healthcare Limited has introduced TruHealth Cancer Screen 360, an integrated cancer screening panel designed to tackle India's growing cancer burden. The program features scientifically curated male and female profiles to support early detection and improve access to specialized diagnostics. The launch addresses low screening rates, as highlighted by Global Cancer Observatory 2022 data, which underscores India's high incidence and mortality rates and screening coverage below global targets set by World Health Organization.

Report Details

| Report Characteristics |

| Market Size (2026) |

USD 9.6 Bn |

| Forecast Value (2035) |

USD 20.0 Bn |

| CAGR (2026–2035) |

8.5% |

| The US Market Size (2026) |

USD 3.2 Bn |

| Historical Data |

2021 – 2025 |

| Forecast Data |

2027 – 2035 |

| Base Year |

2025 |

| Estimate Year |

2026 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors and etc. |

| Segments Covered |

By Test Type (Diagnostic Testing, Predictive & Risk Assessment Testing, Prognostic Testing, Monitoring & Recurrence Testing), By Technology (Next-Generation Sequencing (NGS), PCR-based Technologies, Microarray-based Testing), By Cancer Type (Breast Cancer, Lung Cancer, Colorectal Cancer, Prostate Cancer, Ovarian Cancer, Hematologic Malignancies, Other Solid Tumors), By End User (Hospitals & Cancer Centers, Diagnostic Laboratories, Oncology Clinics) |

| Regional Coverage |

North America – The US and Canada; Europe – Germany, The UK, France, Russia, Spain, Italy, Benelux, Nordic, & Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, & Rest of MEA |

| Prominent Players |

Illumina, Inc., Thermo Fisher Scientific Inc., F. Hoffmann-La Roche Ltd., QIAGEN N.V., Myriad Genetics, Inc., Natera, Inc., Guardant Health, Inc., Laboratory Corporation of America Holdings, Quest Diagnostics Incorporated, Foundation Medicine, Inc., Eurofins Scientific SE, Agilent Technologies, Inc., Exact Sciences Corporation, Caris Life Sciences, NeoGenomics Laboratories, Inc., Ambry Genetics Corporation, Invitae Corporation, BGI Genomics Co., Ltd., Genetron Health, Tempus AI, Inc., and Other Key Players |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users) and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days and 5 analysts working days respectively. |

Frequently Asked Questions

How big is the Global Cancer Focused Genetic Testing Service Market?

▾ The Global Cancer Focused Genetic Testing Service Market size is expected to reach USD 9.6 billion by 2026 and is projected to reach USD 20.0 billion by the end of 2035.

Which region accounted for the largest Global Cancer Focused Genetic Testing Service Market?

▾ North America is expected to have the largest market share in the Global Cancer Focused Genetic Testing Service Market, with a share of about 38.7% in 2026.

How big is the Cancer Focused Genetic Testing Service Market in the US?

▾ The US Cancer Focused Genetic Testing Service market is expected to reach USD 3.2 billion by 2026.

Who are the key players in the Cancer Focused Genetic Testing Service Market?

▾ Some of the major key players in the Global Cancer Focused Genetic Testing Service Market include Illumina, Thermofisher, Roche, and others.

What is the growth rate in the Global Cancer Focused Genetic Testing Service Market?

▾ The market is growing at a CAGR of 8.5 percent over the forecasted period.