Market Overview

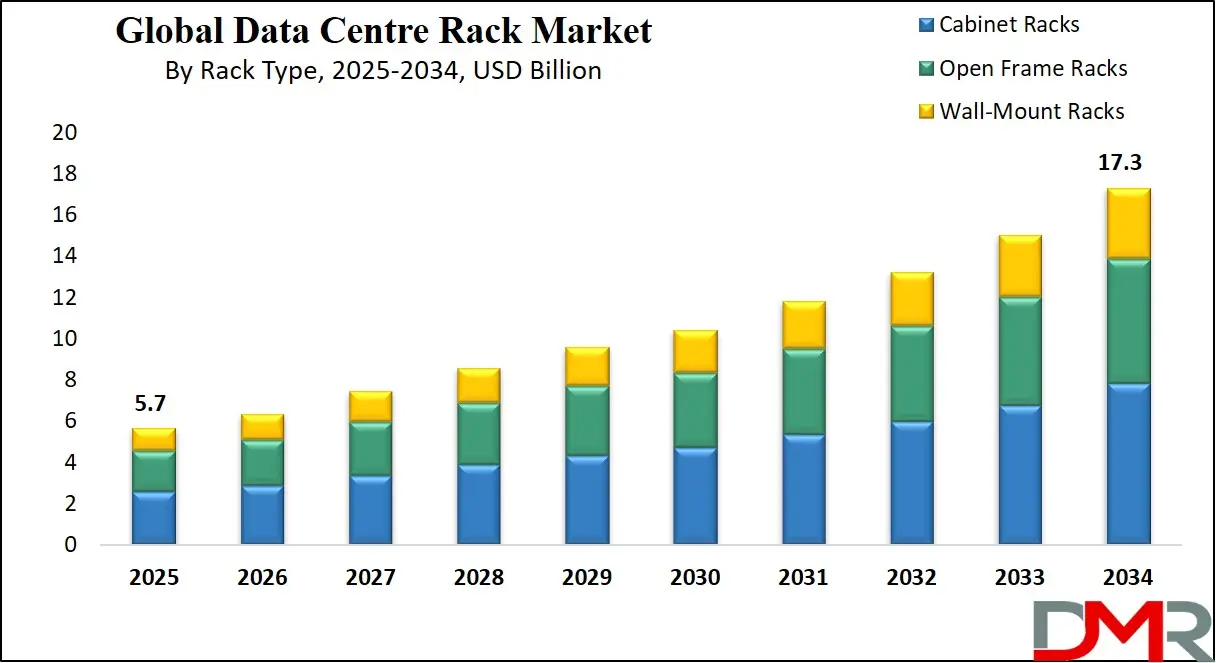

The Global Data Centre Rack Market is predicted to be valued at USD 5.7 billion in 2025 and is expected to grow to USD 17.3 billion by 2034, registering a compound annual growth rate (CAGR) of 13.2% from 2025 to 2034.

The global data center rack market encompasses the infrastructure equipment used to house servers, networking devices, and other computing hardware within data centers. These racks play a crucial role in optimizing space, improving airflow, and enabling efficient cable management and power distribution, making them essential in hyperscale, colocation, and enterprise data centers. The market includes a range of products such as open-frame racks, enclosed racks, and specialized rack accessories tailored to different workload environments and physical constraints.

As businesses worldwide embrace digital transformation and cloud computing, the demand for scalable and modular IT infrastructure has surged. This shift, coupled with the proliferation of IoT devices, 5G deployment, and edge computing, is intensifying the need for efficient server rack solutions that support high-density environments and thermal management. Sustainability concerns are also encouraging the adoption of energy-efficient racks that align with green data center initiatives.

Innovations such as intelligent rack systems, which integrate sensors for real-time monitoring of temperature, humidity, and power usage, are transforming operational efficiency. Additionally, the rise of AI and machine learning workloads is driving the need for specialized racks that support high-performance computing (HPC) environments.

The competitive landscape is characterized by both global and regional data center rack manufacturers striving for innovation and customization. Leading players such as Schneider Electric, Vertiv, Eaton, and Rittal are focusing on strategic partnerships, modular product lines, and smart infrastructure solutions to gain market traction. As data center infrastructure management (DCIM) tools become more integrated with rack systems, players that offer holistic, scalable solutions are poised to lead the market.

The US Data Centre Rack Market

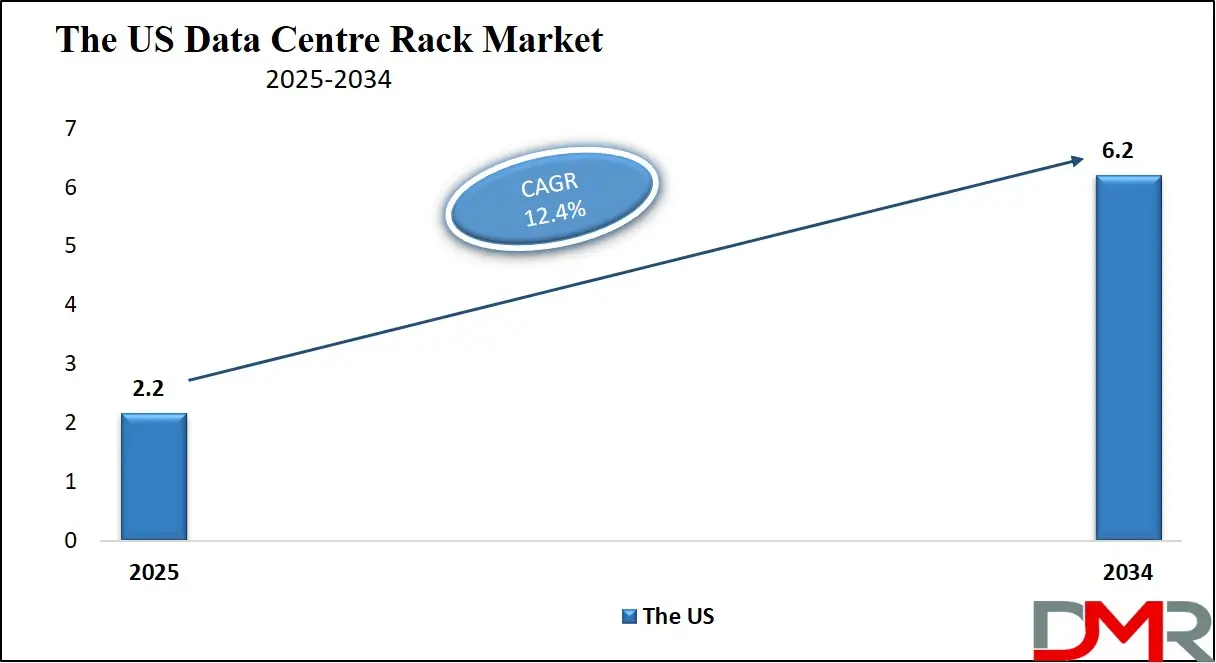

The US Data Centre Rack market is projected to be valued at USD 2.2 billion in 2025. It is expected to witness subsequent growth in the upcoming period as it holds USD 6.2 billion in 2034 at a CAGR of 12.4%.

The US data center rack market is primarily driven by the growing demand for cloud computing, digital transformation across industries, and the rapid adoption of AI and machine learning technologies. Enterprises are increasingly investing in scalable IT infrastructure to manage rising data volumes, spurring demand for high-performance rack solutions.

Additionally, the rise in hyperscale data centers and the need for efficient power and cooling management play significant roles. Government initiatives supporting digital infrastructure, combined with a growing number of internet users and connected devices, further boost market growth. Modular rack systems also gain traction due to their flexibility and deployment speed.

Emerging trends in the US data center rack market include a shift toward edge computing and micro data centers, which require compact and adaptable rack solutions. The market is seeing increased use of advanced thermal management systems integrated within racks to support high-density computing.

There's a notable push toward sustainability, driving the adoption of energy-efficient designs and materials. Smart racks with integrated sensors for real-time monitoring of temperature, humidity, and power usage are gaining popularity. The trend of colocation services continues to rise, fueling the demand for standardized and scalable rack infrastructure to accommodate varying client needs efficiently.

The Japan Data Centre Rack Market

The Japan Data Centre Rack market is projected to be valued at USD 150.7 million in 2025. It is expected to witness subsequent growth in the upcoming period as it holds USD 335.2 million in 2034 at a CAGR of 9.0%.

Japan's data center rack market is propelled by the country’s rapid digitalization, increasing reliance on cloud-based services, and the rising adoption of smart technologies across sectors. As businesses shift toward digital platforms and remote operations, the need for high-performance, space-efficient, and scalable IT infrastructure becomes critical. Strong government support for digital transformation and disaster-resilient infrastructure also enhances market development.

Moreover, Japan's emphasis on energy efficiency and sustainability influences the demand for advanced rack systems with integrated cooling and power management solutions. The rise in data traffic from technologies like 5G, IoT, and AI further intensifies the need for robust data center infrastructure.

In Japan, data center rack trends focus on compact, earthquake-resistant designs tailored for high-density urban environments. There's a growing adoption of intelligent racks with real-time monitoring capabilities for temperature, humidity, and energy usage to optimize performance and reduce downtime. Edge computing is gaining ground, leading to increased demand for portable and modular rack solutions. Integration with advanced cooling technologies, including liquid cooling, is becoming more prevalent.

Additionally, Japanese companies are increasingly opting for sustainable, energy-efficient infrastructure aligned with national green policies. Innovations in cable management and rack security are also influencing procurement decisions, especially in highly regulated and tech-intensive sectors.

The Europe Data Centre Rack Market

The Europe Data Centre Rack market is projected to be valued at USD 1.5 billion in 2025. It is expected to witness subsequent growth in the upcoming period as it holds USD 3.0 billion in 2034 at a CAGR of 8.0%.

Europe’s data center rack market is driven by the region's expanding digital economy, growing emphasis on data sovereignty, and increasing investments in cloud and colocation facilities. The need for high-speed connectivity, real-time data processing, and efficient storage systems accelerates demand for sophisticated rack solutions.

The rise of Industry 4.0 and adoption of automation technologies also contribute to the need for robust and scalable data center infrastructure. Environmental regulations and energy-efficiency mandates in European countries are encouraging enterprises to adopt racks that support advanced cooling and power management systems, aligning with the region’s push toward sustainable IT operations.

Key trends shaping the European data center rack market include a strong focus on green data center initiatives and eco-friendly rack designs that align with strict environmental standards. There is increasing interest in modular and pre-configured racks to accelerate deployment and improve space utilization. Integration of advanced cable management and airflow optimization features is becoming standard.

The market also sees growing demand for racks compatible with liquid cooling systems, particularly in high-performance computing environments. Cross-border data flow regulations are driving investments in regional data centers, further encouraging the use of flexible and secure rack solutions tailored to local operational requirements.

Data Centre Rack Market: Key Takeaways

- Global Overview: The global data centre rack market is forecast to reach a value of USD 5.7 billion in 2025 and is projected to expand to USD 17.3 billion by 2034, reflecting a compound annual growth rate (CAGR) of 13.2% over this period.

- US Market: The US market is expected to be worth USD 2.2 billion in 2025, growing to USD 6.2 billion by 2034 with a CAGR of 12.4%.

- Japan Market: In Japan, the market is anticipated to reach USD 150.7 million in 2025 and USD 335.2 million by 2034, translating to a CAGR of 9.0%.

- Europe Market: The European market is set to be valued at USD 1.5 billion in 2025 and is projected to double to USD 3.0 billion by 2034, with an 8.0% CAGR.

- By Rack Type: Cabinet racks are expected to lead the market, comprising over 55% of the total share by the end of 2025.

- By Rack Height: The 37U–48U segment is anticipated to account for around 45% of the market by 2025.

- By Rack Width: Racks with a 19-inch width are projected to dominate, capturing about 65% of the market share by 2025.

- By Service: Installation services are set to represent approximately 50% of the market by the end of 2025.

- By Data Center Size: Large data centers are expected to command nearly 60% of the market share by 2025.

- By Data Center Type: Hyperscale data centers are forecast to hold about 52% of the market share by the end of 2025.

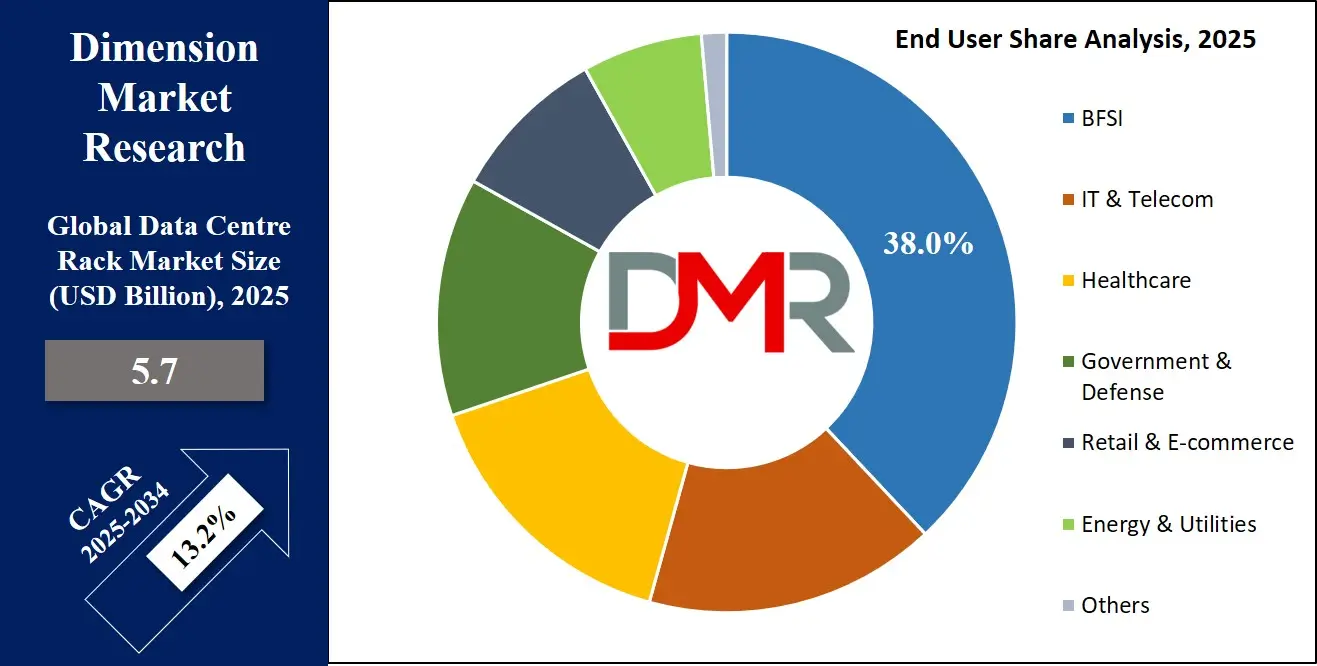

- By End-Use Industry: The IT & Telecom sector is projected to be the leading end-user, accounting for roughly 38% of the total market share by 2025.

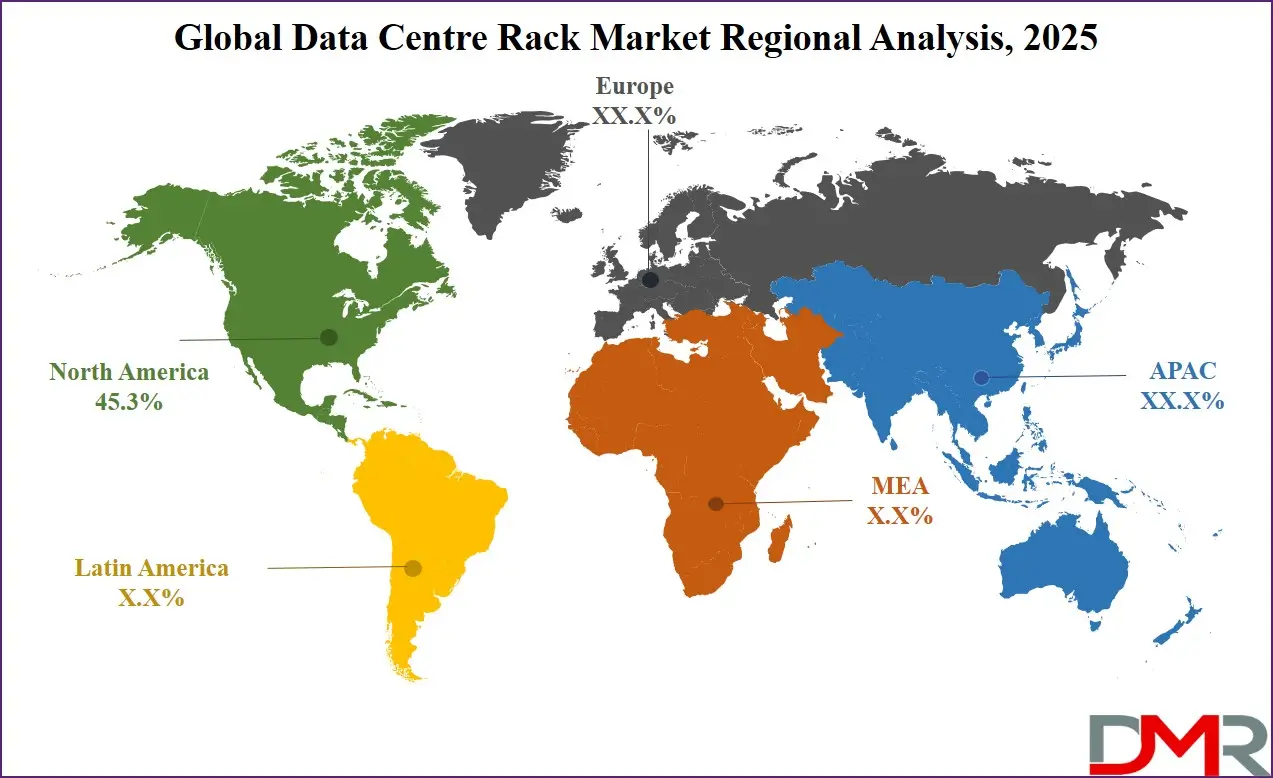

- Regional Leadership: North America is expected to maintain its position as the largest regional market, contributing around 45.3% of global revenue in 2025.

Data Centre Rack Market: Use Cases

- Centralized IT Equipment Organization: Data center racks provide a standardized framework for neatly organizing servers, networking devices, and storage systems. This structured setup maximizes space utilization, simplifies equipment access, and enables efficient maintenance, ensuring that all IT hardware is logically arranged for streamlined operations and troubleshooting.

- Enhanced Cooling and Airflow Management: Racks are engineered to optimize airflow around densely packed hardware, using features like perforated doors, side panels, and cable management. Proper airflow management prevents overheating, reduces reliance on artificial cooling systems, and extends the lifespan of critical IT infrastructure by maintaining optimal operating temperatures.

- Physical Security and Equipment Protection: Data center racks often incorporate lockable doors, side panels, and access controls, safeguarding sensitive IT equipment from unauthorized access, theft, or tampering. This enhanced physical security is crucial for protecting valuable hardware and the sensitive data stored within, especially in shared or colocation environments.

- Scalability and Future-Proofing: Modern racks are designed for scalability, allowing organizations to add or remove servers and other hardware as needs evolve. This modularity supports seamless expansion, accommodates new technologies like high-density AI workloads, and ensures that infrastructure can adapt to growing business demands without major overhauls.

Data Centre Rack Market: Stats & Facts

- Data Center Knowledge: In 2024, average rack density reached 12 kW, double from 6.1 kW eight years earlier, leading 60.0 % of respondents to invest in airflow improvements, containment, and liquid cooling.

- Data Center Frontier: By 2020, 17 % of surveyed racks exceeded 20 kW, with 5 % surpassing 40 kW. Air-cooling alone supports up to 25–40 kW; liquid cooling is already used for racks generating 40–100 kW, and future GPU-centered setups may hit 250–300 kW per rack.

- McKinsey: Air-based cooling effectively handles up to ~50 kW/rack, but for AI training workloads with higher densities, liquid cooling solutions (rear-door exchangers, direct-to-chip) support between 40 and 150 kW per rack.

- IEEE-standard (19-inch rack): Established by AT&T circa 1922, the 19-inch rack remains the industry norm, with a typical height of 42 U (rack units), each U equaling 1.75 in (44.45 mm).

- Emerson DCUG (EMC report): In 2009, average rack power density was ~7.4 kW, anticipated to grow to 12 kW in 2011 and 16.5 kW by 2019. High-density setups (>15 kW/rack) often include blade chassis or denser equipment.

Data Centre Rack Market: Market Dynamics

Driving Factors in the Data Centre Rack Market

Expansion of Cloud and Hyperscale Data Centers

The rapid growth of cloud computing services and hyperscale data centers is a primary driver of the data center rack market. Cloud service providers like AWS, Microsoft Azure, and Google Cloud continue to build large-scale data centers globally, requiring scalable, high-density server rack systems to support enormous computing loads. These facilities prioritize efficient space utilization, advanced cable management, and robust airflow, all of which are enabled by modular rack solutions.

Furthermore, the increasing demand for colocation services and hybrid cloud environments has intensified the need for standardized and customizable rack enclosures, fostering steady growth in the data center infrastructure ecosystem and supporting the evolution of next-generation server rack designs.

Proliferation of IoT and Edge Computing Applications

With the increasing adoption of IoT devices and the expansion of edge computing, there is a surge in demand for decentralized data centers that process data closer to the source. These edge data centers require compact, ruggedized rack solutions optimized for remote locations and minimal footprints. This trend boosts the need for adaptable rack systems with integrated cooling and power management.

The deployment of edge nodes in smart cities, autonomous vehicles, and industrial automation underscores the importance of scalable rack infrastructure, contributing significantly to the data center rack market. The combination of latency-sensitive applications and distributed workloads fuels the demand for intelligent rack designs and edge-optimized rack enclosures.

Restraints in the Data Centre Rack Market

High Initial Investment and Infrastructure Costs

Despite the long-term efficiency gains, the initial cost of deploying advanced data center racks—especially those with integrated cooling, intelligent power distribution units (PDUs), and remote monitoring systems—can be prohibitive. This is particularly challenging for small and medium-sized enterprises (SMEs) that lack the capital to invest in high-end rack infrastructure.

In addition to rack costs, associated expenses such as floor reinforcement, structured cabling, and airflow management systems further strain budgets. This cost barrier may delay modernization in traditional server rooms and limit adoption in emerging markets, thereby restraining overall data center rack market expansion despite rising data demands.

Thermal Management Challenges in High-Density Environments

As servers and networking devices become more compact and powerful, data center racks are increasingly required to handle high-density configurations. However, effective heat dissipation remains a significant challenge. Inadequate cooling and airflow management within tightly packed server racks can lead to overheating, reduced equipment lifespan, and increased downtime.

These challenges make it difficult for operators to fully utilize rack capacity, ultimately hindering data center efficiency. While technologies like hot/cold aisle containment and liquid cooling exist, their implementation can be complex and costly. Such operational limitations serve as critical restraints in the adoption of dense rack systems in modern data centers.

Opportunities in the Data Centre Rack Market

Rising Demand for Modular and Customizable Rack Solutions

The shift toward modular data center designs presents a major opportunity for rack vendors to offer customizable and scalable solutions. Modular racks allow for easier deployment, faster scalability, and tailored configurations suited for specific workloads or environmental conditions. Enterprises and colocation providers increasingly seek flexibility in rack dimensions, cable routing, and cooling integration to meet unique performance requirements.

This trend opens the door for manufacturers to innovate in terms of design, functionality, and materials used in server enclosures. As data centers continue to evolve toward software-defined infrastructure, modular racks will become integral components of agile and future-proof facilities.

Integration with Data Center Infrastructure Management (DCIM) Systems

The growing need for real-time monitoring and automation in data centers is creating significant opportunities for smart rack systems integrated with DCIM platforms. Intelligent racks equipped with environmental sensors, smart PDUs, and asset tracking technologies provide administrators with granular visibility into rack-level performance metrics.

This integration enhances energy efficiency, predictive maintenance, and resource optimization across data center operations. As AI and machine learning become embedded in infrastructure management, racks that support advanced telemetry and automation will see increased adoption. Vendors investing in smart infrastructure that aligns with DCIM trends are poised to gain a competitive edge in the evolving market landscape.

Trends in the Data Centre Rack Market

Emergence of Liquid Cooling-Compatible Rack Systems

With the growing demand for high-performance computing (HPC) and AI workloads, traditional air cooling methods are reaching their limits. This has led to a significant trend toward liquid cooling-compatible rack solutions. These racks are designed to support direct-to-chip and rear-door heat exchanger technologies, enabling better heat management in high-density environments.

The adoption of GPU-heavy configurations in AI and machine learning applications further necessitates these innovations. As green data center initiatives gain momentum, liquid-cooled racks help reduce energy consumption and operational costs. This trend reflects a broader push toward sustainable, energy-efficient data center architecture and is expected to shape next-generation rack designs.

Adoption of Open Compute Project (OCP) Rack Standards

The industry-wide adoption of Open Compute Project (OCP) standards is reshaping how data center racks are designed and deployed. OCP-compliant racks emphasize openness, energy efficiency, and ease of maintenance, making them attractive for hyperscale operators and large enterprises. These racks support wider equipment form factors, optimized airflow, and simplified cable management, reducing operational complexity and cost.

The trend promotes vendor-neutral ecosystems, driving innovation and standardization across data center hardware. As more organizations look to adopt OCP hardware for scalability and interoperability, the demand for open rack architecture is poised to grow, signaling a shift toward open-source infrastructure in modern data centers.

Data Centre Rack Market: Research Scope and Analysis

By Rack Type Analysis

Cabinet Racks are predicted to dominate the global data center rack market by the end of 2025, accounting for over 55.0% of the total market share. The growing demand for secure, scalable, and efficient infrastructure is driving adoption, especially in hyperscale and colocation data centers. Enterprises are prioritizing organized cable management, airflow optimization, and high-density server housing, all of which are effectively supported by cabinet-style enclosures.

Additionally, increasing investments in cloud computing infrastructure, edge computing, and green data centers are further fueling demand. These racks offer enhanced physical security, a key concern in multi-tenant environments. The increasing need for robust IT infrastructure and seamless network management has positioned cabinet racks as the backbone of modern data center solutions.

Wall-Mount Racks are expected to grow at the highest CAGR in the global data center rack market by the end of 2025. This growth is fueled by the surge in demand for compact and cost-effective networking solutions in small and medium-sized enterprises (SMEs) and edge locations. Their space-saving design makes them ideal for businesses with limited floor space.

The rising implementation of Internet of Things (IoT) technologies and smart building infrastructure further increases their relevance. As organizations move toward decentralized IT environments, wall-mount systems offer flexibility and quick deployment. With the increasing proliferation of micro data centers and remote branch setups, wall-mount racks are becoming vital to support distributed data center infrastructure in a dynamic digital landscape.

By Rack Height Analysis

The 37U – 48U rack height segment is projected to dominate the global data center rack market by the end of 2025, holding approximately 45.0% of the total market share. This segment is preferred for its balance of capacity, efficiency, and compatibility with standard server equipment. Organizations deploying cloud services, AI workloads, and virtualization platforms favor these racks due to their optimal space utilization.

The increasing demand for scalable server storage and modular setups is driving adoption. These racks support better airflow management and ease of equipment access, crucial for operational continuity. Growth in colocation services and enterprise IT Infrastructure is further supporting this segment's dominance in the evolving rack server market and high-density deployment environments.

The Above 48U rack height segment is anticipated to experience the highest CAGR in the global data center rack market by the end of 2025. This rise is attributed to the escalating need for high-density server environments and maximizing vertical space in data centers. These taller racks allow for increased server capacity per footprint, which reduces real estate costs.

As hyperscale data centers expand and sustainability goals drive space optimization, above 48U racks are becoming more viable. The rise in big data analytics, high-performance computing (HPC), and containerized data center deployments contributes to the segment’s acceleration. The push toward next-generation IT rack solutions and hyper-converged infrastructure fuels this segment's rapid adoption and advanced deployment strategies.

By Rack Width Analysis

The 19-inch racks segment is forecasted to dominate the global data center rack market by the end of 2025, capturing approximately 65.0% of the overall market share. Widely adopted as an industry standard, these racks offer compatibility with most IT equipment, including servers, switches, and patch panels. Their widespread use across enterprise and colocation data centers supports streamlined deployment and integration. With increasing demand for cloud services and digital transformation initiatives, 19-inch racks remain essential for structured data center infrastructure management.

Their modularity, cost-effectiveness, and flexibility make them suitable for traditional and edge computing environments alike. Standardization continues to drive their dominance, particularly as companies expand their digital footprint and require reliable rack mounting systems.

The 23 23-inch racks segment is expected to witness the highest CAGR in the global data center rack market by the end of 2025. This growth is driven by rising adoption in telecom and carrier-grade environments where larger equipment form factors are common. These racks provide additional lateral space, improving cable routing and airflow, key for high-power density applications.

As network infrastructure scales to meet demands from 5G rollouts and edge computing, 23-inch formats offer enhanced thermal efficiency and support for complex setups. Increasing use in mission-critical sectors is accelerating deployment. With expanding rack enclosure solutions tailored to high-bandwidth systems, the segment is gaining traction among enterprises focused on optimizing performance and service delivery in modern network environments.

By Rack Service Analysis

Installation Services are projected to dominate the global data center rack market by the end of 2025, accounting for approximately 50% of the total market share. As businesses expand their digital operations and build new data centers, there is an increasing demand for professional deployment and configuration of rack systems. Proper installation ensures operational efficiency, safety compliance, and optimal airflow, all crucial in supporting mission-critical IT infrastructure.

The growing trend toward hybrid data environments and high-density server setups has heightened the need for expert handling during deployment. These services are critical in minimizing downtime and ensuring seamless integration of hardware, driving strong demand for rack system setup across both hyperscale and enterprise-level facilities.

Consulting & Integration Services are expected to experience the highest CAGR in the global data center rack market by the end of 2025. This growth is driven by increasing complexity in IT ecosystems and the need for customized solutions across cloud, edge, and hybrid infrastructures. Organizations are seeking expert advice on optimizing rack configurations for scalability, energy efficiency, and workload demands.

As digital transformation accelerates, businesses are turning to integrated planning and design services to future-proof their infrastructure. These services also address compatibility issues and improve deployment strategies. The rising focus on sustainability, security, and data-driven operations is fueling demand for strategic infrastructure integration services, especially in large-scale and multi-site deployments.

By Data Center Size Analysis

Large Data Centers are expected to dominate the global data center rack market by the end of 2025, securing nearly 60% of the total market share. The rapid expansion of hyperscale facilities by major cloud providers and tech enterprises is the primary driver. These centers require thousands of racks to support massive server volumes, high-density workloads, and complex computing environments. Their preference for scalable and durable rack infrastructures contributes significantly to this dominance.

Additionally, the surge in demand for AI, machine learning, and big data processing requires robust server rack solutions. With a strong focus on efficiency, cooling, and high availability, large data centers continue to lead in rack deployment volume and shape the global data center hardware landscape.

Mid-sized Data Centers are projected to register the highest CAGR in the global data center rack market by the end of 2025. This growth is driven by the rapid adoption of digital technologies by enterprises and government institutions aiming to modernize their IT frameworks. Mid-sized facilities are increasingly supporting hybrid cloud models and regional data processing needs.

As edge computing expands, these centers play a crucial role in providing low-latency services. They demand flexible and modular rack infrastructure systems that can support evolving workloads while optimizing space and power consumption. Investment in regional colocation services and secondary markets is further accelerating the need for agile, scalable solutions in the enterprise data environment.

By Data Center Type Analysis

Hyperscale Data Centers are forecasted to dominate the global data center rack market by the end of 2025, holding approximately 52.0% of the market share. The rapid growth of cloud service providers, content delivery networks, and global tech giants is driving large-scale rack deployments in these facilities. Hyperscale centers require extensive rack cabinet systems to support their vast computing and storage needs across thousands of servers.

These data centers prioritize energy efficiency, scalability, and automation, making advanced rack infrastructure indispensable. The continued expansion of AI, SaaS platforms, and global data exchange further reinforces demand. As digital traffic surges, hyperscale operators continue to set the standard for next-generation data center deployment strategies worldwide, solidifying their leading position.

Edge Data Centers are expected to experience the highest CAGR in the global data center rack market by the end of 2025. This surge is driven by the need to process data closer to end users, minimizing latency and improving real-time response for IoT, 5G, and AR/VR applications. These compact facilities require high-performance micro rack solutions tailored for limited-space environments.

Edge deployments support smart cities, autonomous systems, and localized data processing, demanding durable, secure, and scalable infrastructure. As organizations decentralize their IT ecosystems, edge data centers are emerging as a key component in distributed computing models. Their accelerated growth is supported by advancements in localized data infrastructure, particularly in underserved or remote regions with rising digital demand.

By End User Analysis

IT & Telecom is projected to dominate the global data center rack market by the end of 2025, capturing approximately 38.0% of the total market share. The proliferation of digital platforms, data-intensive applications, and rapid adoption of 5G infrastructure are key drivers. This sector demands highly scalable and efficient server rack enclosures to support cloud computing, virtualization, and high-speed connectivity.

Data centers supporting telecom infrastructure require robust, high-density rack solutions capable of handling complex network equipment and fluctuating workloads. With ongoing digital transformation and increased investments in global communication networks, IT & telecom companies continue to lead demand for next-gen data center hardware infrastructure, enabling resilient service delivery and uninterrupted global data transmission.

Retail & E-commerce is expected to grow at the highest CAGR in the global data center rack market by the end of 2025. This surge is driven by the explosive growth of online shopping, digital payment systems, and omnichannel retailing. Companies in this space rely heavily on real-time data analytics, customer personalization, and inventory automation, requiring efficient rack-mounted IT systems to manage dynamic workloads. With expanding data center footprints in logistics and fulfillment hubs, the need for secure and scalable infrastructure is increasing rapidly.

E-commerce platforms are investing in regional edge facilities to ensure seamless, low-latency services. These factors are accelerating the sector's demand for agile digital infrastructure deployment, ensuring operational efficiency and optimal user experience.

The Data Centre Rack Market Report is segmented on the basis of the following:

By Rack Type

- Cabinet Racks

- Open Frame Racks

- Wall-Mount Racks

By Rack Height

- Below 24U

- 25U – 36U

- 37U – 48U

- Above 48U

By Rack Width

- 19 Inch Racks

- 23 Inch Racks

- Other Widths

By Rack Services

- Installation Services

- Maintenance & Support Services

- Consulting & Integration Services

By Data Center Size

- Small Data Centers

- Mid-sized Data Centers

- Large Data Centers

By Data Center Type

- Colocation Data Centers

- Enterprise Data Centers

- Hyperscale Data Centers

- Edge Data Centers

By End User

- BFSI

- IT & Telecom

- Healthcare

- Government & Defense

- Retail & E-commerce

- Energy & Utilities

- Others

Regional Analysis

Region with the largest Share

North America holds the largest share of the data center rack market, accounting for approximately 45.3% of global revenue in 2025. This dominance is driven by the region's advanced IT infrastructure, early adoption of cloud computing, and the presence of major technology firms like Amazon, Google, and Microsoft. The United States leads the region, with strong investments in hyperscale and colocation data centers.

Additionally, increased demand for high-performance computing and the proliferation of data-intensive applications further fuel market growth. The regulatory landscape also supports innovation and data center expansion. The ongoing shift toward edge computing and IoT deployment continues to boost rack demand, cementing North America's position as the primary hub for data center infrastructure globally.

Region with Highest CAGR

Asia Pacific is projected to witness the highest CAGR in the data center rack market during the forecast period. Rapid digitalization, growing internet penetration, and the expansion of cloud services are key drivers of growth. Countries like China, India, Japan, and Singapore are experiencing a surge in data traffic and enterprise IT investments, prompting the development of new data centers.

The region’s favorable government policies, improving connectivity infrastructure, and rising demand for AI and big data analytics further contribute to this growth. Local and global tech giants are investing heavily in regional infrastructure, supporting both hyperscale and edge data centers. As a result, Asia Pacific is emerging as the fastest-growing market, attracting substantial capital and technological innovation.

By Region

North America

Europe

- Germany

- The U.K.

- France

- Italy

- Russia

- Spain

- Benelux

- Nordic

- Rest of Europe

Asia-Pacific

- China

- Japan

- South Korea

- India

- ANZ

- ASEAN

- Rest of Asia-Pacific

Latin America

- Brazil

- Mexico

- Argentina

- Colombia

- Rest of Latin America

Middle East & Africa

- Saudi Arabia

- UAE

- South Africa

- Israel

- Egypt

- Rest of MEA

Competitive Landscape

The competitive landscape of the global data center rack market is characterized by intense rivalry among key players striving to enhance product innovation, scalability, and energy efficiency. Leading companies such as Vertiv Group Corp., Schneider Electric, Eaton Corporation, Hewlett-Packard Enterprise, Rittal GmbH, and Dell Technologies dominate through diversified portfolios and global presence.

These players focus on developing advanced rack-based data center solutions that support high-density computing, modular scalability, and improved thermal management. Strategic initiatives such as mergers, acquisitions, and partnerships are common, aiming to strengthen market positioning and address evolving data center deployment trends.

Emerging vendors are also gaining traction by offering cost-effective and customizable rack enclosures for edge and micro data centers, especially in developing regions. The push for sustainable infrastructure has encouraged innovation in airflow management, cable organization, and power distribution within rack systems. Cloud computing expansion, increased investment in colocation facilities, and demand for hyper-converged systems are shaping future strategies.

Vendors are also integrating smart technologies, such as remote monitoring and AI-based diagnostics, into their rack management systems to improve operational efficiency. As digital infrastructure continues to evolve, companies that deliver flexible, secure, and energy-efficient rack solutions are expected to remain at the forefront of the competitive landscape.

Some of the prominent players in the Global Data Centre Rack Market are:

- AMCO Enclosures

- Belden Inc.

- Chatsworth Products

- Cisco Systems, Inc.

- Dell Inc.

- Eaton

- Fujitsu

- Hewlett-Packard Enterprise Development LP

- International Business Machines Corporation

- Legrand

- nVent

- Panduit Corp.

- Rittal GmbH & Co. KG

- Schneider Electric

- Vertiv Group Corp.

- Lenovo

- Huawei

- Inspur Systems

- Supermicro

- Great Lakes Data Racks & Cabinets

- Other Key Players

Recent Developments

- In April 2025, Legrand acquired Sydney-based Computer Room Solutions, a data center hardware provider with nearly two decades of experience. The company’s offerings include server racks, security caging, and uninterruptible power supplies, strengthening Legrand’s data center portfolio.

- In March 2025, Schneider Electric, ETAP, and NVIDIA formed a partnership to leverage digital twin technology within NVIDIA Omniverse, aiming to enhance real-time data center management and efficiency. This platform enables dynamic power modeling at the chip level—surpassing traditional rack-level estimates—and supports AI-focused data centers with rack power densities up to 132kW. This initiative builds on Schneider’s December 2024 introduction of a high-density, liquid-cooled reference design, as well as the March 2025 opening of a microgrid and data center R&D facility in Massachusetts.

- Also in March 2025, Eaton announced plans to acquire Fibrebond Corporation, expanding its presence in the multi-tenant data center segment. Fibrebond is known for its pre-integrated modular power enclosures, which help customers reduce installation time and costs. The deal, set to close in Q3 2025, is expected to deliver USD 110 million in adjusted EBITDA for the year.

- In February 2025, Vertiv partnered with Oxigen to develop its largest, most energy-efficient data center in Sant Cugat del Vallès, Spain. The 6,000m² Tier III facility features a 3,000m² clean room, accommodates 800 racks with 6MW of power, and is designed for AI and scalable workloads. Vertiv provided advanced cooling solutions, flexible power distribution, and monitoring software. The center operates entirely on renewable energy, prioritizing reliability, adaptability, and sustainability.

Report Details

| Report Characteristics |

| Market Size (2025) |

USD 5.7 Bn |

| Forecast Value (2034) |

USD 17.3 Bn |

| CAGR (2025–2034) |

13.2% |

| Historical Data |

2019 – 2024 |

| The US Market Size (2025) |

USD 2.2 Bn |

| Forecast Data |

2025 – 2033 |

| Base Year |

2024 |

| Estimate Year |

2025 |

| Report Coverage |

Market Revenue Estimation, Market Dynamics, Competitive Landscape, Growth Factors, etc. |

| Segments Covered |

By Rack Type (Cabinet Racks, Open Frame Racks, Wall-Mount Racks), By Rack Height (Below 24U, 25U – 36U, 37U – 48U, Above 48U), By Rack Width (19 Inch Racks, 23 Inch Racks, Other Widths), By Rack Services (Installation Services, Maintenance & Support Services, Consulting & Integration Services), By Data Center Size (Small Data Centers, Mid-sized Data Centers, Large Data Centers), By Data Center Type (Colocation Data Centers, Enterprise Data Centers, Hyperscale Data Centers, Edge Data Centers), By End User (BFSI, IT & Telecom, Healthcare, Government & Defense, Retail & E-commerce, Energy & Utilities, Others) |

| Regional Coverage |

North America – US, Canada; Europe – Germany, UK, France, Russia, Spain, Italy, Benelux, Nordic, Rest of Europe; Asia-Pacific – China, Japan, South Korea, India, ANZ, ASEAN, Rest of APAC; Latin America – Brazil, Mexico, Argentina, Colombia, Rest of Latin America; Middle East & Africa – Saudi Arabia, UAE, South Africa, Turkey, Egypt, Israel, Rest of MEA |

| Prominent Players |

AMCO Enclosures, Belden Inc., Chatsworth Products, Cisco Systems, Inc., Dell Inc., Eaton, Fujitsu, Hewlett-Packard Enterprise Development LP, International Business Machines Corporation, Legrand, nVent, Panduit Corp., Rittal GmbH & Co. KG, Schneider |

| Purchase Options |

We have three licenses to opt for: Single User License (Limited to 1 user), Multi-User License (Up to 5 Users), and Corporate Use License (Unlimited User) along with free report customization equivalent to 0 analyst working days, 3 analysts working days, and 5 analysts working days respectively. |